Premium Alcoholic Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

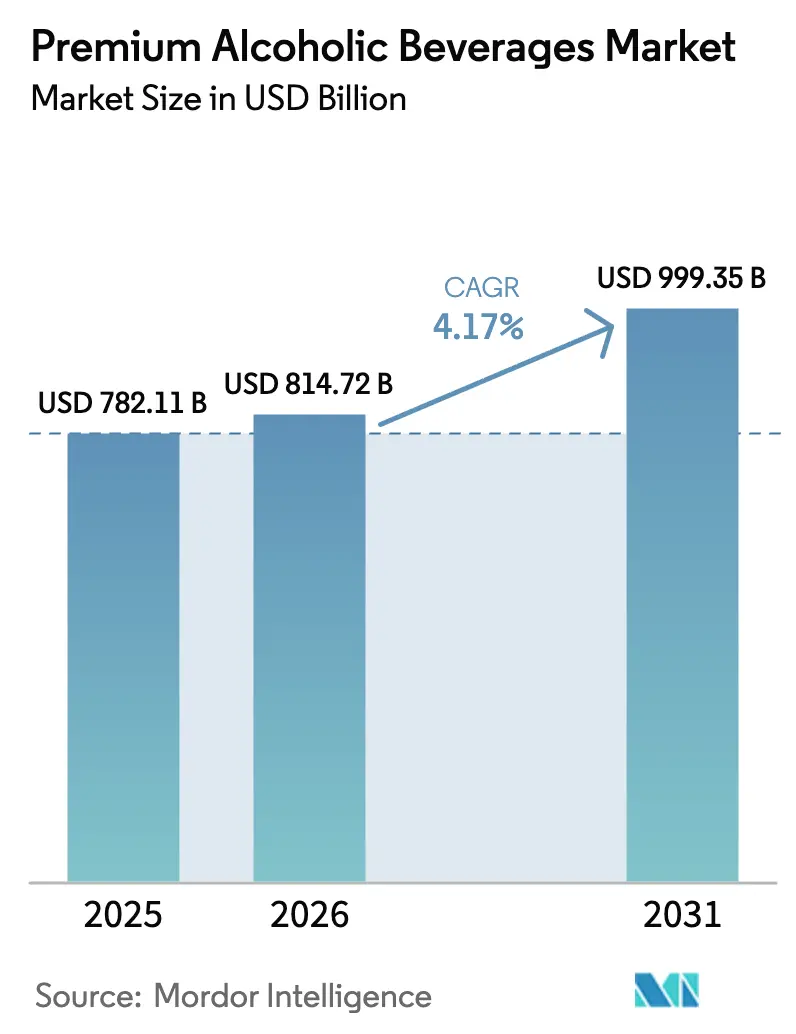

| Market Size (2026) | USD 814.72 Billion |

| Market Size (2031) | USD 999.35 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

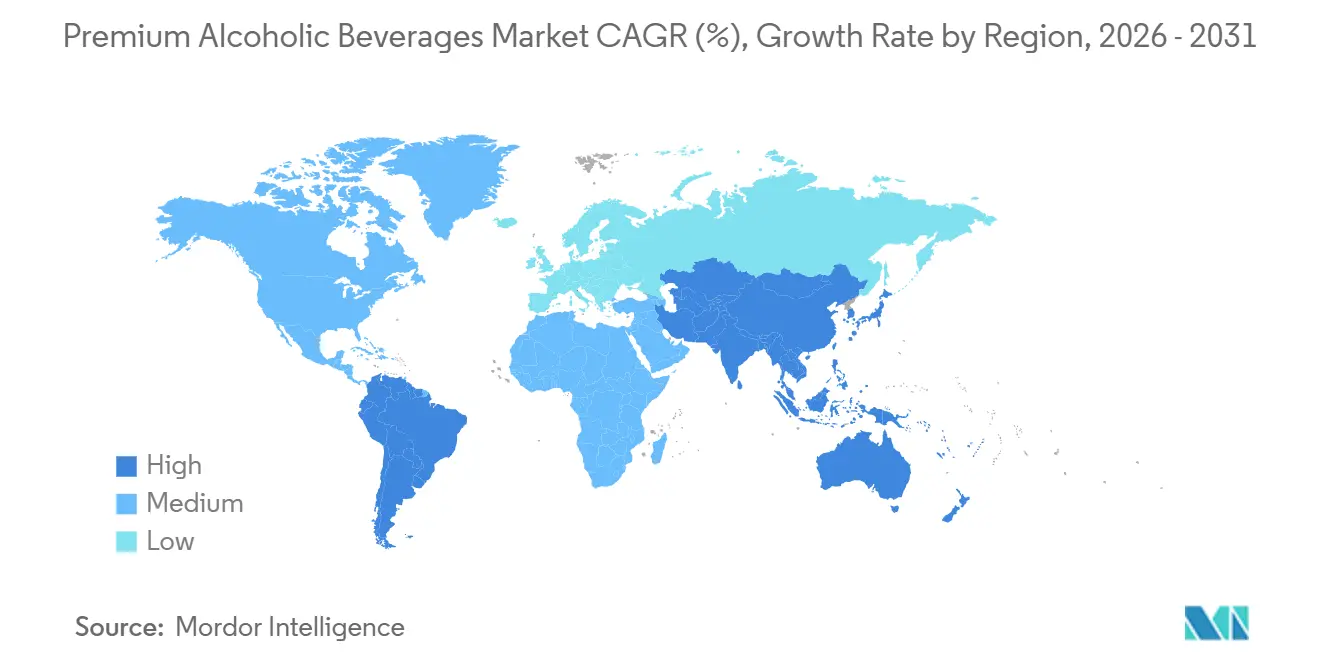

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Premium Alcoholic Beverages Market Analysis by Mordor Intelligence

The Premium Alcoholic Beverages Market size is expected to grow from USD 782.11 billion in 2025 to USD 814.72 billion in 2026 and is forecast to reach USD 999.35 billion by 2031 at 4.17% CAGR over 2026-2031. Growth is driven by rising demand for small-batch spirits, biodynamic wines, and craft beers that highlight transparency and quality. Premium tequila, Japanese whisky, and botanical gins are expanding price options, while low-calorie RTD cocktails attract health-conscious consumers. Glass bottles remain a symbol of quality, but slim aluminum cans are gaining popularity due to their sustainability and convenience. Off-trade retail leads the market, but experiential venues like brewpubs, taprooms, and luxury hotel bars are enhancing customer experiences, boosting brand loyalty, and increasing spending per visit.

Key Report Takeaways

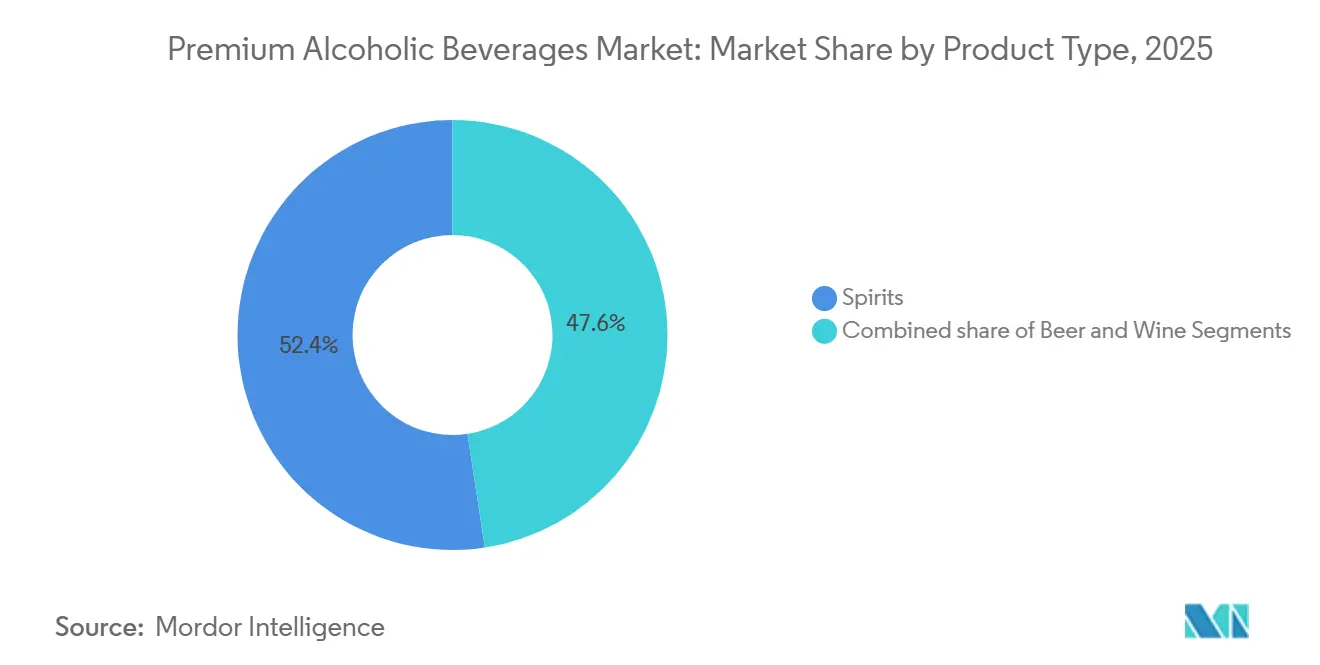

- By product type, spirits led with 52.39% of premium alcoholic beverages market share in 2025, while wine shows the fastest expansion at a 5.52% CAGR through 2031.

- By end user, male drinkers accounted for 53.45% of volume in 2025; in contrast, female-targeted offerings are advancing at a 4.89% CAGR.

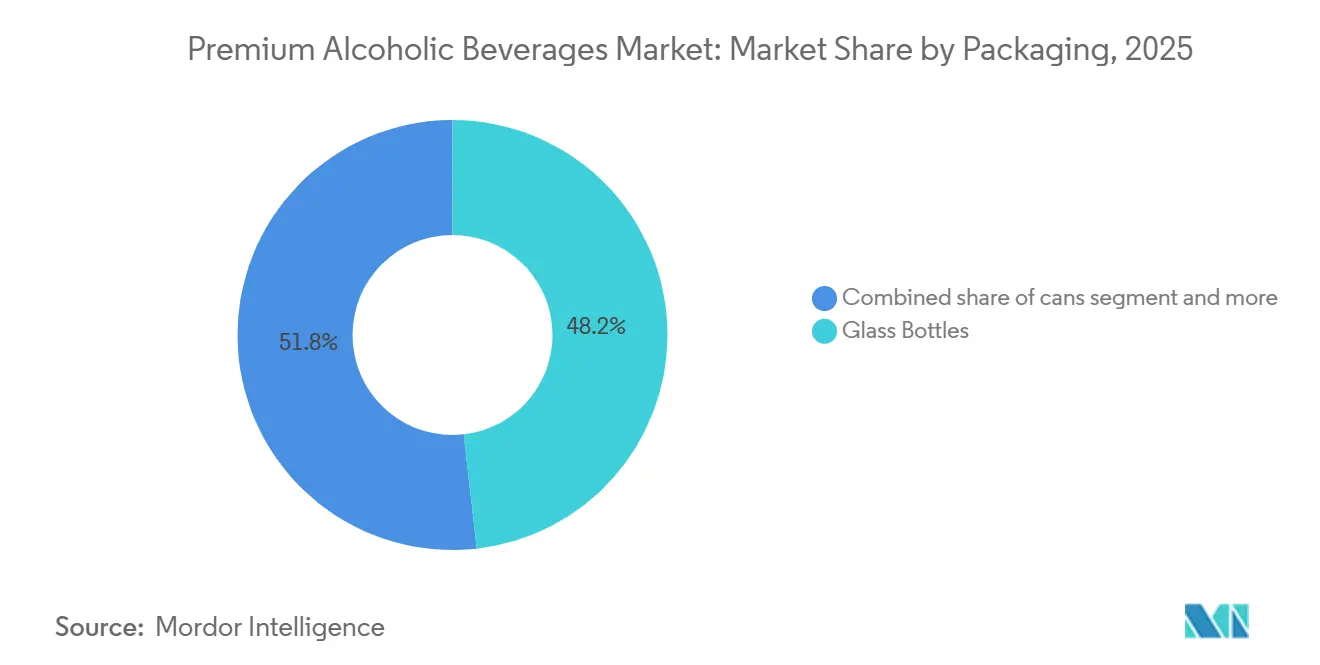

- By packaging, glass held a 48.21% share in 2025, yet aluminum cans are projected to grow at a 6.21% CAGR.

- By distribution channel, off-trade captured 61.29% of value in 2025, while on-trade venues are rising at a 5.17% CAGR.

- By geography, North America represented 36.87% of the value in 2025, and Asia-Pacific is pacing the field at a 6.13% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Premium Alcoholic Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of craft beers, artisanal spirits, and flavored innovations like CBD-infused options | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Mixology trends and cocktail culture drive premium spirit consumption in upscale bars | +0.9% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Sustainable sourcing and eco-friendly packaging meet wellness demands | +0.8% | Europe, North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| E-commerce expands access to rare and aged beverages | +0.7% | Global, early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Low-calorie and RTD premium cocktails cater to moderate consumption | +0.6% | North America, Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Surge in on-trade channels like brewpubs, taprooms, and luxury hospitality venues fueling premium sales | +0.5% | North America, Europe, Asia-Pacific metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing popularity of craft beers, artisanal spirits, and flavored innovations like cbd-infused options

Craft breweries and micro-distilleries are redefining consumer expectations with small-batch production, local ingredients, and unique flavors that large-scale brands struggle to replicate. In 2024, the United States had 9,796 craft breweries, contributing over 13% of total beer volume, according to the Brewers Association[1]Source: Brewers Association, "National Beer Sales and Production Data", brewersassociation.org. Artisanal spirits, such as botanical gin, whiskey aged in unique casks, and tequila finished in wine barrels, command 20-40% price premiums, enabling profitability with lower production volumes. CBD-infused alcoholic beverages face delays due to regulatory hurdles, as the U.S. Alcohol and Tobacco Tax and Trade Bureau requires individual approval for hemp-derived CBD in alcohol. However, niche producers in permissive states are building brand equity ahead of potential federal harmonization. Additionally, innovations like adaptogenic herbs, nootropics, and fermented botanicals are attracting wellness-focused consumers, blending indulgence with functional benefits and blurring the line between alcoholic beverages and nutraceuticals.

Mixology trends and cocktail culture drive premium spirit consumption in upscale bars

Craft cocktail bars and speakeasy-style venues have elevated spirits from basic commodities to premium culinary ingredients, with bartenders playing a key role as brand ambassadors who educate consumers about terroir, distillation techniques, and flavor pairings. This premiumization trend is self-reinforcing, as higher check averages encourage venues to stock rare bottles, attracting enthusiasts willing to travel for exclusive tastings and boosting off-premise sales. Agave-based spirits, particularly tequila, highlight this dynamic, with U.S. imports reaching approximately 70.7 million proof gallons in 2024 and premium and ultra-premium segments growing significantly faster than mixto categories[2]Source: Distilled Spirits Council of the United States (DISCUS), "Import Volume of Tequila in the United States from 2017 to 2024," distilledspirits.org. The revival of cocktail culture has also driven renewed demand for bitters, vermouths, and liqueurs, enabling niche producers to thrive without direct competition from multinational portfolios. On-premise consumption serves as a discovery channel, where consumers try new brands in bars and later purchase them in retail. E-commerce platforms are replicating this pathway through virtual tastings and subscription boxes, further enhancing brand discovery and consumer engagement.

Sustainable sourcing and eco-friendly packaging meet wellness demands

Sustainability has shifted from being a marketing strategy to an essential operational focus as regulators enforce recyclability targets and consumers demand greater accountability in supply chain practices. Heineken has committed to making all its packaging 100% recyclable, reusable, or compostable by 2025, replacing plastic shrink wrap with cardboard carriers, a change that has already reduced packaging waste by 12,000 metric tons annually. The European Union's Packaging and Packaging Waste Regulation 2025/40 mandates that beverage containers must include at least 30% recycled content by 2030, compelling glass and aluminum suppliers to invest in closed-loop recycling systems or face penalties[3]Source: European Commission, "Packaging and Packaging Waste Regulation 2025/40," ec.europa.eu. Distillers are also prioritizing water stewardship, with Pernod Ricard cutting water usage by 18% per liter of alcohol produced between 2020 and 2024, a metric now featured in their annual sustainability reports and closely monitored by ESG-focused investors. Additionally, the intersection of wellness and sustainability is driving demand for ingredient transparency, as consumers increasingly reject artificial colors, added sugars, and undisclosed additives. This trend is pressuring producers to reformulate their products to remain competitive in premium markets.

E-commerce expands access to rare and aged beverages

Direct-to-consumer e-commerce has opened the doors to limited-edition releases and aged spirits, once the domain of auction houses and specialty retailers. This shift not only allows producers to secure higher margins but also fosters direct relationships with their customers. While shipping regulations vary by state, only 45 states allow direct wine shipments and a mere 14 permit direct sales of spirits; there's a noticeable legislative push. Tax authorities are increasingly viewing e-commerce as a revenue stream rather than a compliance challenge. Subscription services, like Flaviar and Caskers, are on the rise, delivering curated monthly selections of rare whiskeys and craft spirits. These platforms serve as discovery hubs, introducing consumers to brands often overlooked in traditional retail. In 2024, auction platforms such as Sotheby's Wine and Whisky reported record volumes, with Japanese whisky and rare Scotch fetching prices exceeding USD 100,000 per bottle. This trend underscores the growing perception of aged spirits as alternative investments. Furthermore, e-commerce empowers producers to sidestep the traditional three-tier distribution system. This is particularly beneficial for craft distilleries and wineries, which often struggle to secure prime retail placements due to their smaller scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeiting risks undermine brand trust and authenticity in luxury segments | -0.6% | Global, acute in Asia-Pacific and Europe | Medium term (2-4 years) |

| Intense competition from craft distilleries and standard alcohols | -0.5% | North America, Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Fluctuations in raw material availability | -0.4% | Global, concentrated in agave (Mexico), barley (Europe), grapes (global) | Short term (≤ 2 years) |

| Rising popularity of non-alcoholic and moderation movements | -0.3% | North America, Europe, early signals in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeiting risks undermine brand trust and authenticity in luxury segments

In 2024, counterfeit premium spirits and wines continue to erode brand equity and pose health risks, with fatalities reported in India and Southeast Asia due to fake bottles containing methanol or industrial alcohol. Luxury scotch and rare Japanese whisky are frequent targets, with Sotheby's estimating 5-10% of auction submissions as counterfeit or mislabeled. To combat this, Sotheby's introduced blockchain-based provenance tracking and tamper-evident closures, while Diageo deployed NFC-enabled labels on select ultra-premium products, allowing smartphone-based authenticity checks. However, adoption remains limited due to high costs exceeding USD 0.50 per unit. The Asia-Pacific region faces acute counterfeiting issues due to weak intellectual property enforcement and fragmented distribution networks, enabling gray-market operators to infiltrate supply chains. Beyond lost sales, brands risk liability for harm caused by counterfeit products and face long-term reputational damage.

Intense competition from craft distilleries and standard alcohols

Craft distilleries are gaining market share by offering hyper-local stories and limited-edition releases that command premium prices, even without the extensive marketing budgets of multinational companies. This shift has compelled established players to acquire or partner with craft brands to remain competitive. For instance, in 2024, Pernod Ricard acquired a minority stake in Codigo 1530 tequila, valuing the brand at USD 150 million despite its annual volumes being under 100,000 cases, highlighting strategic priorities over immediate profitability. Intensifying competition is squeezing margins across the value chain, with distributors demanding higher slotting fees and promotional allowances, while retailers are expanding premium private-label offerings that undercut branded products by 15-25%. Meanwhile, craft producers face challenges such as rising ingredient costs, labor shortages, and capital constraints, which limit their scalability. Many also struggle to navigate the complex three-tier distribution systems. As a result, the market is developing into a barbell structure, where global giants and niche craft producers thrive, while mid-sized regional brands are increasingly pushed out.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirits Dominate Yet Wine Accelerates Through Organic Viticulture

In 2025, spirits seized a commanding 52.39% of the market share, buoyed by a trend towards premiumization in whiskey, tequila, and gin. Consumers are increasingly opting for aged expressions and craft-distilled offerings that highlight their unique terroir and production methods. Diageo's tequila portfolio, led by Don Julio and Casamigos, saw an 8% volume surge in FY2024. Meanwhile, scotch enjoyed a 3% uptick, outpacing flat trends in the broader category, a testament to effective premiumization strategies. The spirits segment boasts higher margins, averaging 60-70% gross profit per liter for premium spirits, compared to 40-50% for beer, and a longer shelf life. This longevity allows producers to navigate demand fluctuations without the risk of spoilage. Regulatory measures, like the U.S. Craft Beverage Modernization Act, which slashed federal excise taxes for small distillers, have eased entry barriers and spurred a surge in craft distilleries.

Wine is set to outpace all product types with a projected 5.52% CAGR growth from 2026 to 2031. This momentum is driven by organic and biodynamic viticulture, which commands a 25-40% retail premium. Consumers increasingly link regenerative agriculture with enhanced taste and health benefits. Treasury Wine Estates highlighted this trend, noting its luxury portfolio, led by Penfolds, accounted for 48% of total revenue in FY2024, despite making up just 12% of the volume. This underscores the lucrative margin potential in premium wine. While beer may not be the fastest-growing segment, it remains a cornerstone of on-premise consumption. Craft breweries have evolved into experiential venues, bolstering brand loyalty and driving additional revenue through taproom sales.

By End User: Female Consumers Drive Premiumization Through Wellness-Aligned Products

In 2025, male consumers represented 53.45% of the market volume, a trend consistent with historical patterns and a higher per-capita intake. However, this male dominance is waning as producers craft offerings that cater to female tastes. In 2024, Brown-Forman's Woodford Reserve Bourbon introduced a lower-proof variant, targeting female consumers with a preference for smoother flavors. This move highlights a nuanced understanding of gender-based taste differences, steering clear of clichéd packaging. Meanwhile, products aimed at men continue to spotlight heritage, craftsmanship, and robust flavors. Aged whiskeys and barrel-strength spirits, in particular, have garnered a loyal following among enthusiasts who treat collecting as a cherished hobby.

From 2026 to 2031, premium offerings tailored for women are projected to grow at a 4.89% CAGR, outpacing all other segments. This surge is largely fueled by ready-to-drink (RTD) cocktails, botanical-infused spirits, and low-calorie wines, all of which resonate with contemporary wellness trends. Constellation Brands' Fresca Mixed line, boasting just 100 calories per serving and a focus on natural ingredients, swiftly captured 2.3% of the RTD market within half a year of its 2024 debut. Furthermore, the female demographic is championing transparency in product ingredients. Brands that openly share comprehensive ingredient lists and nutritional data are seeing better performance than those that opt for ambiguous "natural flavors" labels. This push for clarity is prompting many in the industry to reformulate their products. In a bid to resonate with this evolving demographic, producers are increasingly bringing female master distillers and winemakers on board, not just for diverse product development but also to underscore authenticity and representation.

By Packaging: Aluminum Cans Surge as Sustainability and Portability Converge

In 2025, glass bottles commanded a 48.21% share of the packaging market, underscoring their association with heritage branding. Consumers often perceive glass as a symbol of quality and tradition, especially when it comes to aged spirits and premium wines. Ardagh Group, a prominent player in the glass packaging arena, noted a surge in demand for premium spirit bottles. These bottles, often featuring custom molds, embossing, and heavy-base designs, are now outpacing standard formats. Beyond aesthetics, glass packaging offers transparency, allowing consumers to gauge color and clarity—key sensory cues that can sway retail purchase decisions. Yet, the use of glass isn't without its challenges. While it's a favored choice, its production is energy-intensive, and its weight during transportation amplifies carbon footprints. Producers are actively addressing these concerns through initiatives like lightweighting and incorporating increased recycled content.

Aluminum cans are set to witness the fastest growth among packaging formats, with a projected CAGR of 6.21% from 2026 to 2031. This surge is largely driven by the adoption of these lightweight, infinitely recyclable cans for premium ready-to-drink (RTD) cocktails and craft beers. Such choices resonate with the sustainability values of millennials and Gen Z. Ball Corporation highlighted a notable trend: the rising demand for slim 12-ounce cans. These cans, favored for their sleek aesthetic, are increasingly sought after for premium cocktails. Producers are even willing to shell out a 10-15% premium over standard cans for these differentiated formats. Beyond their sustainability appeal, cans boast functional advantages. They effectively block light and oxygen, prolonging the shelf life of light-sensitive beverages. Additionally, they chill faster than glass, catering to the on-the-go consumer. The long-held belief that cans are inferior to bottles is fading. Premium brands like Underwood Wines and Cutwater Spirits are now championing the can format, emphasizing quality through design and marketing rather than the packaging material itself.

By Distribution Channel: Off-Trade Dominates Yet On-Trade Delivers Experiential Premiums

In 2025, off-trade channels secured a dominant 61.29% market share, propelled by the allure of convenience, competitive pricing, and diverse selections at supermarkets, hypermarkets, online retailers, and specialty stores. Supermarkets and hypermarkets, the titans of the off-trade realm, capitalize on high foot traffic and spur-of-the-moment purchases. Yet, they grapple with mounting pressure on margins from the encroachment of private-label competitors. Meanwhile, online retail emerges as the swiftest-growing off-trade segment, boasting double-digit expansion rates. This surge is largely attributed to direct-to-consumer models and subscription services, which are making rare and aged beverages more accessible. Other off-trade venues, like duty-free shops and convenience stores, cater to travelers and impulse buyers. However, they grapple with challenges stemming from a dip in international travel and certain jurisdictions' stringent regulations on alcohol sales.

On-trade channels, which include bars, restaurants, brewpubs, and upscale hospitality venues, are witnessing the fastest growth rate among distribution channels, expanding at a 5.17% CAGR from 2026 to 2031. This surge is largely driven by a cultural shift towards experiential consumption and mixology, elevating spirits from mere commodities to essential culinary ingredients. The American Craft Spirits Association highlights the financial advantage for craft distilleries: those with on-site tasting rooms derive 30-50% of their revenue directly from sales, a strategy that shields them from distributor markups. Furthermore, on-trade venues play a pivotal role in brand promotion. Data from the Brewers Association underscores this, revealing that consumers who sample a product at a bar or restaurant are 2.8 times more inclined to buy it at retail. Luxury hotels are not just serving drinks; they're curating 'spirits libraries' akin to prestigious wine cellars. Some even offer guided tastings, fetching between USD 150-300 per person, significantly boosting their beverage revenue.

Geography Analysis

In 2025, North America captured 36.87% of the market share, driven by the rapid growth of craft distilleries, increasing exports of agave-based spirits from Mexico, and the rising demand for premium products in the U.S. and Canada. The U.S. craft spirits market included 2,687 distilleries in 2024, generating over USD 7.8 billion in revenue, as consumers increasingly preferred locally produced and exclusive offerings. Mexican tequila and mezcal exports reached 35 million 9-liter cases, with premium categories growing faster due to the influence of celebrity endorsements and the growing popularity of mixology. Additionally, regulatory support, such as the U.S. Craft Beverage Modernization Act and relaxed state shipping laws, played a significant role in boosting the market.

Asia-Pacific is projected to grow at a 6.13% CAGR from 2026 to 2031, leading global market expansion. This growth is driven by the rising demand for Japanese whisky, the internationalization of Chinese baijiu, and the increasing popularity of Indian single malts. Japanese whisky achieved record export levels, while Chinese baijiu producers partnered with luxury venues to position baijiu as a premium spirit. Despite fragmented regulations, governments across the region are easing restrictions to promote alcohol exports and support the market's growth.

Europe, renowned for its historic wine regions and scotch whisky heritage, is experiencing slower growth due to market saturation and regulatory challenges, such as the EU’s 2025/40 Packaging Regulation. However, craft distilleries in countries like Germany, the Netherlands, and Poland are disrupting traditional brands with innovative offerings. In 2024, alcohol duty reforms in the United Kingdom provided much-needed support to smaller producers, enabling them to compete more effectively. South America is witnessing a shift toward premiumization in wine and cachaça, driven by the adoption of geographic indications and organic certifications. Meanwhile, in the Middle East and Africa, demand for imported spirits and wines is rising in tourism hubs like Dubai and South Africa. Luxury hotels in these regions are catering to affluent travelers, further driving market growth.

Competitive Landscape

The premium alcoholic beverage market is moderately fragmented, with both regional and international players competing for market share. Prominent companies such as The Brown-Forman Corporation, Pernod Ricard SA, Gruppo Campari, Diageo plc, and Bacardi Limited dominate the market. These players utilize advanced distribution networks and strong manufacturing capabilities to expand their product offerings and maintain a competitive edge. Additionally, many companies in the flavonoid industry are heavily investing in Research and Development to drive product innovation, which is expected to significantly boost sales during the forecast period.

Emerging and high-growth markets such as the United States, Brazil, China, and India are becoming key strategic priorities for premium alcoholic beverage manufacturers. These markets are benefiting from rising disposable incomes, expanding middle-class populations, and rapid urbanization. Changing consumer preferences toward premium, craft, and differentiated alcoholic beverages are further supporting demand growth. In response, leading companies are strengthening their regional footprints through localized production, portfolio customization, and focused distribution strategies. Targeted brand-building and experiential marketing initiatives are also being implemented to appeal to younger, affluent consumers.

Competition in the market is primarily shaped by factors such as brand equity, premiumization, and innovation, rather than price-based strategies. Leading companies are actively investing in super-premium and ultra-premium product lines, adopting advanced barrel-aging techniques, and implementing experiential marketing strategies to enhance consumer engagement and foster brand loyalty. Furthermore, mergers, acquisitions, and strategic partnerships are being selectively pursued to tap into high-growth premium segments. This trend indicates a gradual move toward market consolidation while retaining the moderately fragmented nature of the premium alcoholic beverage market.

Premium Alcoholic Beverages Industry Leaders

-

Pernod Ricard SA

-

Diageo plc

-

Bacardi Limited

-

The Brown-Forman Corporation

-

Gruppo Campari

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Globus Spirits introduced a new product, 'Doaab Expression 02: The Old Man & The Blossom,' expanding its portfolio. This launch represents a strategic move to potentially strengthen the company's presence in the premium spirits segment and diversify its product range.

- October 2024: Allied Blenders and Distillers Ltd. (ABDL), an Indian-made foreign liquor (IMFL) company, announced its plans to launch a blended malt Scotch whisky. Additionally, ABDL is looking to enhance its whisky and non-whisky product lines by targeting the premium segment and is developing new variants to appeal to a wider range of consumers.

- July 2024: Urban Spirit Vodka launched its Signature Vodka in mid-2025 as a small-batch, premium vodka offering. The brand said it creates the liquid in small batches using premium sugar cane to create a crisp and clean finish.

- July 2024: Ad Gefrin has launched a new limited-edition whisky, Tácnbora Cognac Cask Finish. The small-batch cask strength blend has been finished in ex-Cognac oak for six months, which the brand said brings depth, structure and sweetness.

Global Premium Alcoholic Beverages Market Report Scope

Premium alcoholic beverages are commodities, including beer, spirits, and others, that utilize packaging and ingredients to increase the perceived value of beverages. The global premium alcoholic beverages market is segmented by type, distribution channel, and geography. By type, the market is classified as beer, wine, and spirits. By distribution channel, the market is segmented into on-trade and off-trade. Moreover, the study analyzes the premium alcoholic beverages market in emerging and established markets worldwide, including North America, Europe, Asia-Pacific, South America, Middle East & Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Beer |

| Wine |

| Spirits |

| Male |

| Female |

| Glass Bottles |

| Cans |

| Others |

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Online Retail Store | |

| Specialty Stores | |

| Other Off-trade Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Beer | |

| Wine | ||

| Spirits | ||

| End User | Male | |

| Female | ||

| Packaging | Glass Bottles | |

| Cans | ||

| Others | ||

| Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Online Retail Store | ||

| Specialty Stores | ||

| Other Off-trade Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the premium alcoholic beverages market in 2026?

It reached USD 814.72 billion in 2026 and is on track for USD 999.35 billion by 2031.

What CAGR is projected for premium alcohol between 2026 and 2031?

The market is forecast to grow at 4.17% per year during the 2025-2030 period.

Which product type holds the biggest share today?

Spirits lead with 52.39% of premium alcoholic beverages market share in 2025.

Which region is expanding the fastest?

Asia-Pacific shows the highest growth, advancing at a 6.13% CAGR through 2031.

Page last updated on: