Liquid Smoke Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 142.36 Million |

| Market Size (2031) | USD 188.90 Million |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Liquid Smoke Market Analysis by Mordor Intelligence

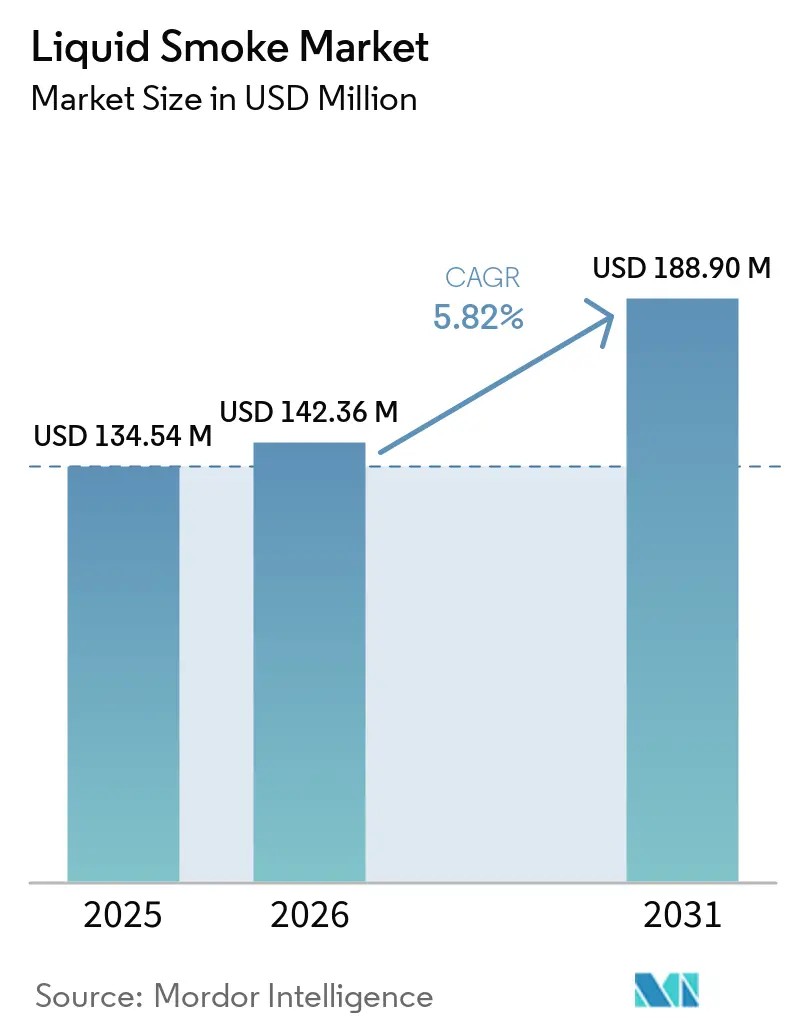

The liquid smoke market was valued at USD 134.54 million in 2025 and is projected to grow to USD 142.36 million in 2026, reaching USD 188.9 million by 2031, with a CAGR of 5.82% during the period 2026–2031. This growth is driven by increasing consumer demand for authentic smoky flavor profiles, the rising adoption of clean-label food ingredients, and the growing use of natural flavoring solutions in processed food production. Food manufacturers are increasingly adopting liquid smoke as an alternative to traditional smoking methods due to its ability to provide consistent flavor, improve processing efficiency, and offer better operational control while preserving the desired smoky aroma and taste. Additionally, the rising popularity of barbecue-inspired, grilled, and smoked culinary experiences is further boosting the use of liquid smoke in various food formulations.

Key Report Takeaways

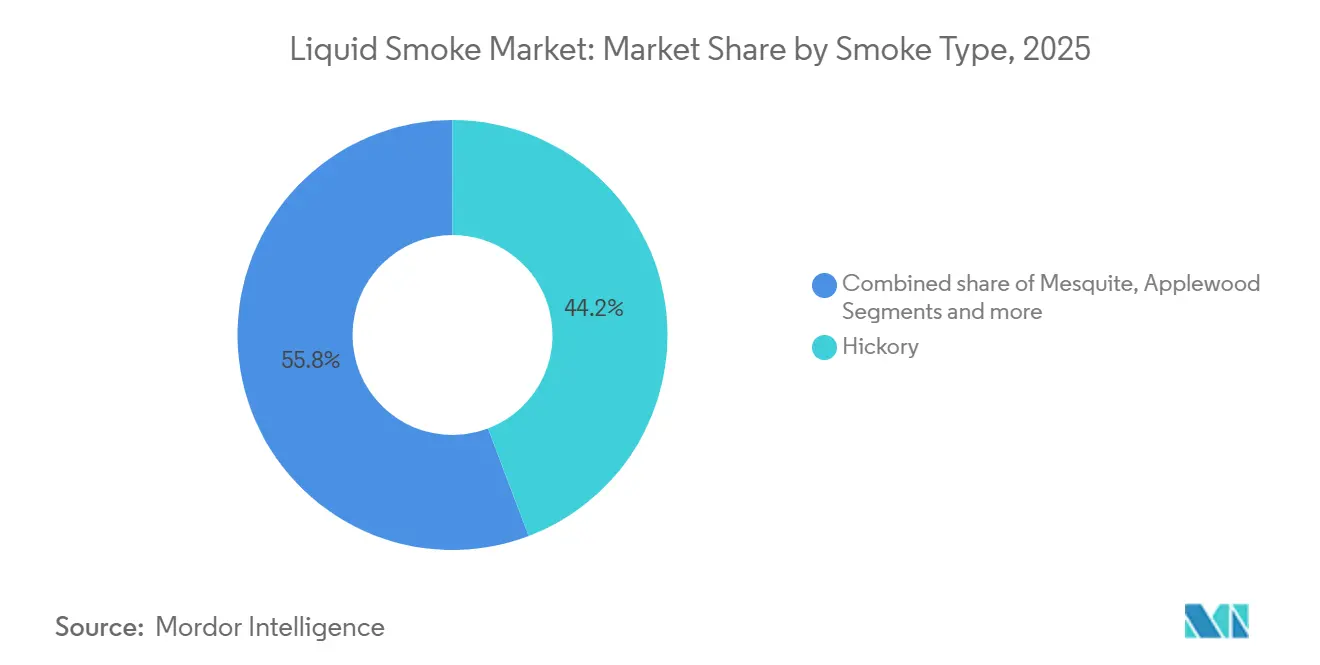

- By smoke type, hickory held 44.23% of the liquid smoke market share in 2025, while applewood is projected to grow at 5.93% CAGR through 2031.

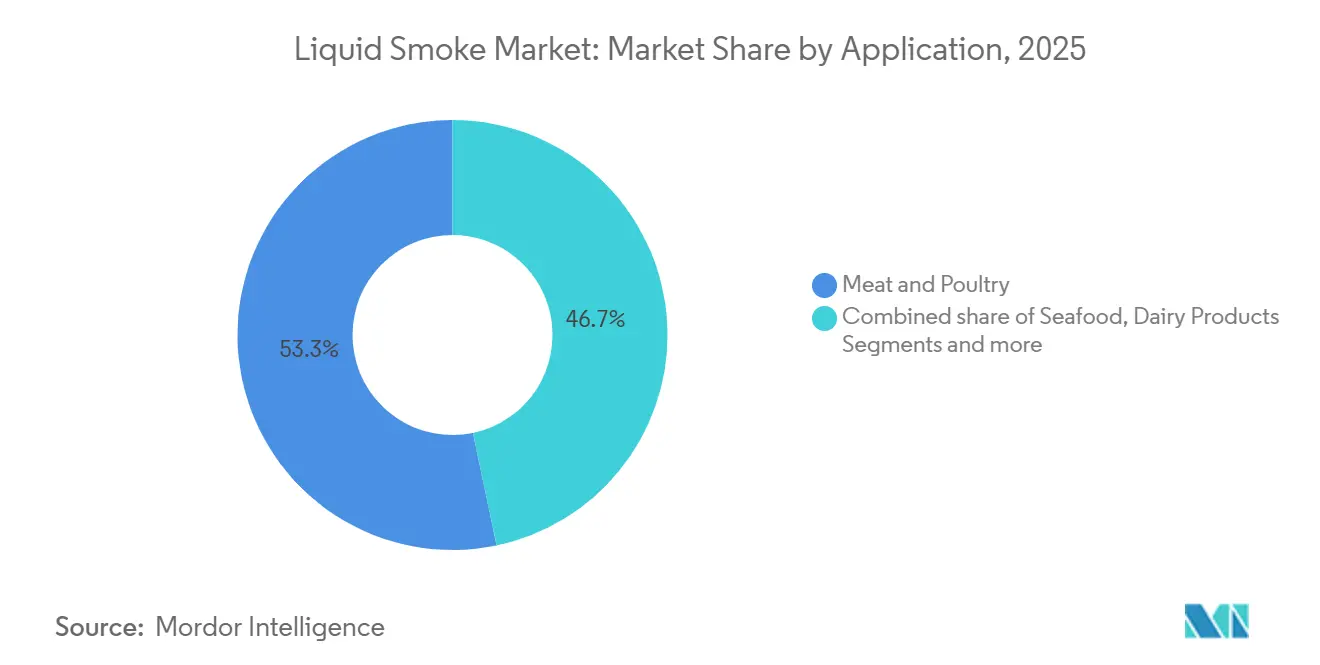

- By application, meat and poultry accounted for 53.28% share of the liquid smoke market size in 2025, while plant-based meat alternatives are forecast to expand at 6.45% CAGR through 2031.

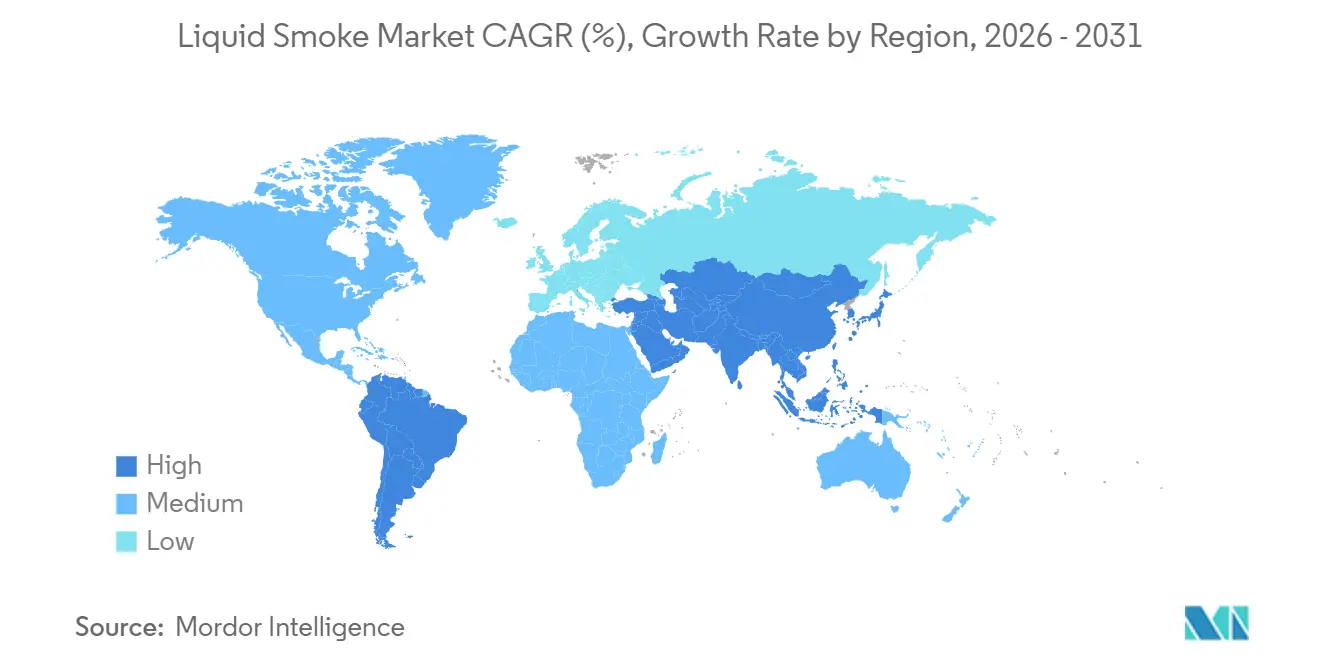

- By geography, North America held 37.32% of the liquid smoke market share in 2025, while Asia-Pacific is expected to advance at 6.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Smoke Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label natural flavoring agents | +1.2% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Growth of barbecue culture and smoked-flavor culinary trends | +1.0% | North America, Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Expansion of convenience and ready-to-eat food formats | +0.9% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2–4 years) |

| Technological advancements in smoke condensate extraction | +0.7% | Global, Research and Development concentrated in North America and Europe | Long term (≥ 4 years) |

| Growth in global fast-food and quick-service restaurant chains | +0.8% | Global, fastest acceleration in Asia-Pacific and South Americs | Short term (≤ 2 years) |

| Sustainability advantages of liquid smoke over traditional wood smoking | +0.5% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label natural flavoring agents

The increasing demand for clean-label and natural flavoring agents is a key driver for the global liquid smoke market. Consumers are progressively seeking food products made with recognizable, minimally processed, and naturally derived ingredients. Liquid smoke is gaining acceptance among food manufacturers as it is produced through the condensation of real wood smoke, enabling companies to deliver authentic smoky flavors while adhering to clean-label product standards. With growing awareness of ingredient transparency, consumers are actively avoiding artificial flavor enhancers and synthetic additives, prompting manufacturers to use natural smoke flavoring solutions in their formulations. According to the International Food Information Council (IFIC), 36% of Americans in 2024 preferred food products labeled as natural, organic, or healthy, underscoring the increasing consumer focus on clean-label purchasing behavior [1]Source: International Food Information Council (IFIC), "2024 IFIC Food & Health SURVEY", ific.org. This trend is driving the adoption of liquid smoke in the food industry, as manufacturers aim to develop products that offer authentic taste experiences alongside natural ingredient claims.

Growth of barbecue culture and smoked-flavor culinary trends

The increasing popularity of barbecue culture and smoked-flavor culinary trends is driving the growth of the global liquid smoke market. Consumers are seeking bold and authentic wood-smoked taste experiences across various food products. The demand for grilled, roasted, and barbecue-inspired foods has led food manufacturers to use liquid smoke in formulations to replicate traditional slow-smoked flavors more efficiently and consistently. There is a strong consumer preference for smoky, charred, and fire-grilled flavor notes that enhance sensory appeal and provide restaurant-style experiences in packaged and processed foods. Additionally, the global spread of culinary influences through social media, foodservice innovations, cooking shows, and premium dining trends has heightened consumer exposure to barbecue-inspired flavors, further increasing demand for smoke flavoring ingredients. Liquid smoke allows manufacturers to deliver these smoky characteristics consistently while improving production scalability and reducing dependence on traditional smoking methods.

Expansion of convenience and ready-to-eat food formats

The growth of convenience and ready-to-eat food formats is a key driver of the global liquid smoke market, as evolving lifestyles and increasing urbanization continue to influence food consumption patterns globally. The shift toward convenience-focused food options, especially in densely populated urban areas, is prompting food manufacturers to create ready-to-eat meals, packaged snacks, meal kits, and quick-preparation products that combine strong sensory appeal with reduced preparation time for consumers. Additionally, the rise in dual-income households is boosting consumer spending on convenient meal solutions that prioritize both flavor quality and ease of use. For example, data from the Ministry of Internal Affairs and Communications indicates that approximately 13.3 million households in Japan were dual-income households in 2025, underscoring the growing demand for convenient food products among working consumers with limited time for meal preparation [2]Source: Ministry of Internal Affairs and Communications (Japan), "Number of dual income households in Japan", soumu.go.jp. This is driving food producers to enhance their ready-to-eat product offerings with premium flavor profiles, thereby increasing the use of liquid smoke as a natural and efficient smoke flavoring solution.

Technological advancements in smoke condensate extraction

Technological advancements in smoke condensate extraction are significantly influencing the global liquid smoke market by enhancing product quality, flavor consistency, safety standards, and manufacturing efficiency. Modern extraction and purification technologies enable manufacturers to produce cleaner and more refined liquid smoke products with lower levels of undesirable compounds while maintaining the authentic smoky aroma and taste. Advanced systems for filtration, fractionation, and condensation provide greater control over smoke composition, facilitating the development of customized flavor intensities and specialized smoke profiles to meet the evolving needs of the food industry. These technological advancements also improve product stability, clarity, and shelf life, making liquid smoke more suitable for large-scale industrial food processing applications. Additionally, innovations in low-residue and highly concentrated smoke formulations are helping food manufacturers optimize production efficiency, enhance flavor uniformity, and reduce operational costs compared to traditional smoking methods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict food safety and labeling regulations | -0.9% | Europe (primary), United Kingdom, Codex-aligned Asia-Pacific markets | Short term (≤ 2 years) |

| Strong preference for traditionally wood-smoked foods in certain regions | -0.6% | North America (South/Texas), parts of Europe | Long term (≥ 4 years) |

| Limited consumer awareness about the safety and benefits | -0.5% | Asia-Pacific (primary), South America | Medium term (2–4 years) |

| Growing demand for low-sodium and mild-flavored food products | -0.4% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Strict food safety and labeling regulations

Strict food safety and labeling regulations pose a significant restraint on the market, as manufacturers are required to adhere to complex regulatory standards governing smoke flavoring ingredients, production methods, and permissible chemical compositions. Regulatory authorities in various regions closely monitor the presence of compounds such as polycyclic aromatic hydrocarbons (PAHs) and other substances that may form during smoke generation processes, thereby increasing compliance demands on liquid smoke producers. These stringent regulations often require advanced purification systems, ongoing product testing, and comprehensive quality assurance procedures, leading to increased operational complexity and higher production costs for manufacturers. Furthermore, differing regulatory frameworks and labeling requirements across international markets create additional challenges for companies seeking to standardize products and expand their global presence.

Strong preference for traditionally wood-smoked foods in certain regions

The preference for traditionally wood-smoked foods in certain regions serves as a significant restraint on the global liquid smoke market. Many consumers associate conventional smoking methods with greater authenticity, craftsmanship, and sensory quality. Traditional wood smoking is deeply embedded in regional culinary traditions and heritage food practices, especially in markets where artisanal preparation and slow-smoking techniques are viewed as essential for achieving the desired flavor and texture. Consequently, some consumers regard liquid smoke as a substitute that may not fully replicate the complexity, aroma, and visual appeal of naturally wood-smoked products. This perception can hinder the adoption of liquid smoke in premium and specialty food categories, where authenticity and traditional preparation methods heavily influence purchasing decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Smoke Type: Applewood's Rise Reshapes a Hickory-Dominated Market

The hickory smoke type segment held a dominant position in the global liquid smoke market, accounting for a 44.23% share in 2025. This dominance is attributed to its strong consumer acceptance, rich smoky aroma, and ability to deliver a balanced flavor profile that closely mimics traditional wood smoking. Hickory liquid smoke is widely favored for its robust combination of smoky, slightly sweet, and bacon-like notes, which align with evolving consumer preferences for authentic smoked flavors. Its versatility in flavor formulation and compatibility with various food processing systems have made it a preferred choice among manufacturers aiming for consistent sensory performance and standardized product quality.

The applewood smoke type segment is anticipated to experience the fastest growth in the global liquid smoke market, with a projected CAGR of 5.93% during 2026–2031. This growth is driven by increasing consumer demand for milder, sweeter, and more refined smoky flavor profiles. Applewood liquid smoke is gaining popularity due to its smoother and less intense smokiness compared to traditional hardwood smoke variants, appealing to consumers seeking balanced and premium flavor experiences. The segment is further supported by the rising demand for gourmet-style and artisanal flavor solutions, as applewood smoke is associated with subtle sweetness, a clean aroma, and natural wood-smoked characteristics.

By Application: Plant-Based Acceleration Diversifies a Meat-Centric Market

The meat and poultry segment accounted for a 53.28% share of the global liquid smoke market in 2025. This dominance is attributed to the high demand for authentic smoked flavor profiles, extended product shelf life, and enhanced processing efficiency in meat production. Liquid smoke has become a key ingredient in meat and poultry processing, enabling manufacturers to consistently deliver smoky taste, aroma, and surface coloration while minimizing the complexities of traditional smoking methods. The segment continues to grow as processed and ready-to-cook meat products increasingly require standardized flavor quality for large-scale production. Additionally, the antimicrobial and antioxidant properties of liquid smoke contribute to improved product stability and reduced spoilage risks, further driving its adoption in this segment.

The plant-based meat alternatives segment is expected to be the fastest-growing application in the global liquid smoke market, with a projected CAGR of 6.45% during 2026–2031. This growth is driven by the rising demand for authentic meat-like flavor experiences in alternative protein products. Liquid smoke enhances the sensory appeal of plant-based formulations by providing smoky aroma, grilled notes, and cooked-meat characteristics that consumers associate with traditional meat products. As consumer expectations for taste, texture, and overall eating experience increase in the alternative protein industry, manufacturers are incorporating liquid smoke to improve flavor complexity and more effectively replicate traditional smoked meat profiles. Furthermore, the segment benefits from innovation in vegan and vegetarian product development, where smoke flavoring is widely used to create premium-tasting and differentiated offerings.

Geography Analysis

North America accounted for a dominant 37.32% share of the global liquid smoke market in 2025, supported by strong consumption of processed and smoked meat products, increasing demand for natural smoke flavoring ingredients, and the region’s highly developed food processing industry. The market benefits from rising meat and poultry consumption levels, particularly in the United States, where smoked flavor profiles are deeply integrated into consumer food preferences. According to the United States Department of Agriculture (USDA), broiler meat consumption in the United States reached approximately 103 pounds per capita in 2025, highlighting the large-scale demand for poultry products that frequently utilize smoke flavoring technologies for taste enhancement and preservation [3]Source: United States Department of Agriculture (USDA), "Per capita consumption of poultry meat in the United States", usda.gov.

Europe is navigating a structurally complex period in the liquid smoke market due to evolving food safety regulations, changing consumer ingredient preferences, and increasing scrutiny regarding smoke flavoring compounds. Regulatory developments surrounding traditional smoke flavorings and stricter compliance standards are prompting manufacturers to invest in advanced purification technologies and cleaner production methods to maintain market competitiveness. Simultaneously, consumer demand for natural, minimally processed, and premium-quality food products is driving a gradual transition toward refined liquid smoke formulations with improved safety and flavor characteristics. The region maintains stable demand for smoked flavor profiles across processed foods, while manufacturers increasingly focus on product innovation, sustainability, and clean-label positioning.

Asia-Pacific is projected to be the fastest-growing region in the global liquid smoke market, registering a CAGR of 6.83% during 2026–2031. This growth is driven by the rapid expansion of the processed food sector, changing dietary preferences, and increasing adoption of convenience foods with smoked flavor profiles. Rising urbanization, expanding modern retail infrastructure, and growing exposure to Western-style barbecue and smoked food products are encouraging food manufacturers to integrate liquid smoke into a broader range of food formulations. Meanwhile, South America and the Middle East & Africa remain comparatively smaller but steadily growing markets due to increasing processed food consumption, gradual expansion of foodservice industries, and rising awareness regarding natural smoke flavoring ingredients.

Competitive Landscape

The global liquid smoke market is moderately fragmented, with several international and regional manufacturers competing based on product quality, smoke purification capabilities, flavor innovation, and customized formulation solutions. Key players in the market include Kerry Group plc, Azelis Group, Besmoke Ltd, Inga Group, and McCormick & Company, Inc. These companies are focusing on enhancing their market presence by offering diversified smoke flavor portfolios, developing clean-label products, and providing customized smoke solutions tailored to the evolving needs of the food industry. Competition in the market is increasingly centered on delivering authentic smoke flavor profiles, ensuring regulatory compliance, and improving product consistency for industrial-scale food manufacturing.

Technological development is emerging as a significant competitive factor in the liquid smoke market. Companies are investing in advanced smoke condensation, purification, and filtration systems to enhance product quality and safety. Modern liquid smoke technologies enable manufacturers to reduce undesirable compounds, improve flavor precision, minimize bitterness, and achieve greater consistency across production batches. Efforts are also being directed toward refining concentration technologies and developing low-residue smoke solutions that support operational efficiency and simplify integration into industrial food processing systems. Furthermore, increased research and development activities are driving innovation in specialty smoke profiles, fruitwood-based smoke varieties, and cleaner smoke extraction techniques, aligning with consumer demand for natural and minimally processed ingredients.

Market participants are expanding their production capabilities, distribution networks, and product portfolios to meet the growing global demand for smoked flavor ingredients. Many companies are strengthening their presence through strategic partnerships, acquisitions, and investments in new manufacturing facilities to improve supply chain efficiency and address increasing customer requirements. Expansion activities are also being driven by the rising demand for premium smoke flavor solutions, plant-based food innovations, and clean-label ingredients across the global food processing industry. Additionally, companies are actively broadening their application-specific offerings and customized smoke formulations to cater to changing flavor preferences and evolving regulatory standards.

Liquid Smoke Industry Leaders

-

Kerry Group plc

-

Azelis Group

-

Besmoke Ltd.

-

Inga Group (MSK Ingredients Ltd)

-

McCormick & Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Symrise has expanded its Alternative Smoke Taste Solutions portfolio by introducing EU-compliant smoke flavorings available in both dry and liquid formats. These flavorings include beechwood, hickory, and roasted smoke tonalities.

- October 2025: Givaudan announced the opening of its new liquids production facility in Reading, Ohio, highlighting its ongoing commitment to the North American market.

Global Liquid Smoke Market Report Scope

Liquid smoke is an ingredient made by capturing actual wood smoke and condensing it into a liquid form. The liquid smoke market is segmented by smoke type, application, and geography. Based on smoke type, the market is segmented into hickory, mesquite, applewood, and others. Based on application, the market is segmented into meat and poultry, seafood, dairy products, bakery and confectionery, sauces, dressings, and marinades, snacks and savory products, plant-based meat alternatives, pet food, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Hickory |

| Mesquite |

| Applewood |

| Others |

| Meat and Poultry |

| Seafood |

| Dairy Products |

| Bakery and Confectionery |

| Sauces, Dressings, and Marinades |

| Snacks and Savory Products |

| Plant-based Meat Alternatives |

| Pet Food |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Smoke Type | Hickory | |

| Mesquite | ||

| Applewood | ||

| Others | ||

| By Application | Meat and Poultry | |

| Seafood | ||

| Dairy Products | ||

| Bakery and Confectionery | ||

| Sauces, Dressings, and Marinades | ||

| Snacks and Savory Products | ||

| Plant-based Meat Alternatives | ||

| Pet Food | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is driving liquid smoke demand in food manufacturing?

Growth is being supported by clean-label positioning, smoke-forward menu development, convenience food expansion, and better control over flavor, preservation, and color in industrial production.

Which application leads current demand?

Meat and poultry led in 2025 with 53.3% share, reflecting liquid smoke’s continued importance in processed meat systems for flavor and functional performance.

Which smoke type is growing fastest?

Applewood is the fastest-growing smoke type with a projected 5.9% CAGR through 2031 because its softer and slightly sweet profile fits newer product categories.

Why does North America lead current revenue?

North America held 37.3% share in 2025 due to deep processed meat infrastructure, strong barbecue culture, and broad foodservice use of scalable smoke flavor systems.

Page last updated on: