Flavored Whiskey Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 39.35 Billion |

| Market Size (2031) | USD 52.10 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

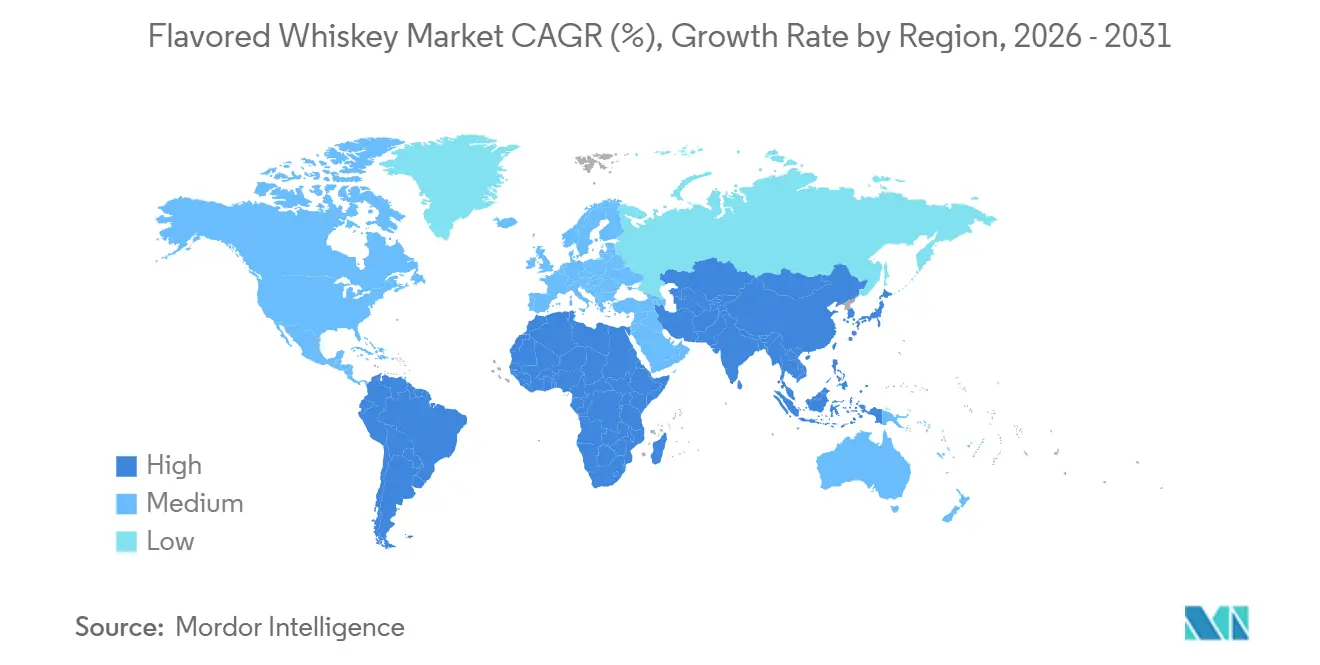

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Flavored Whiskey Market Analysis by Mordor Intelligence

The Flavored Whiskey Market size is expected to increase from USD 38.05 billion in 2025 to USD 39.35 billion in 2026 and reach USD 52.10 billion by 2031, growing at a CAGR of 5.80% over 2026-2031.

This ascent is increasingly driven by shifting consumer behavior, with younger and non-traditional drinkers favoring experiential consumption over traditional whiskey rituals, boosting demand for approachable flavored variants. The Distilled Spirits Council of the United States (DISCUS) continues to highlight strong category momentum, with flavored expressions benefiting from rising participation among women and new entrants. Major players such as Brown-Forman, Diageo, Beam Suntory, and Pernod Ricard maintain strong market control, while craft distillers continue to innovate with local ingredients and limited-edition offerings despite distribution challenges. Regulatory developments remain critical, with the U.S. Alcohol and Tobacco Tax and Trade Bureau (TTB) advancing labeling and transparency requirements, potentially impacting flavored whiskey positioning among health-conscious consumers[1]Source: Distilled Spirits Council, “Market Trends 2026,” distilledspirits.org.

Key Report Takeaways

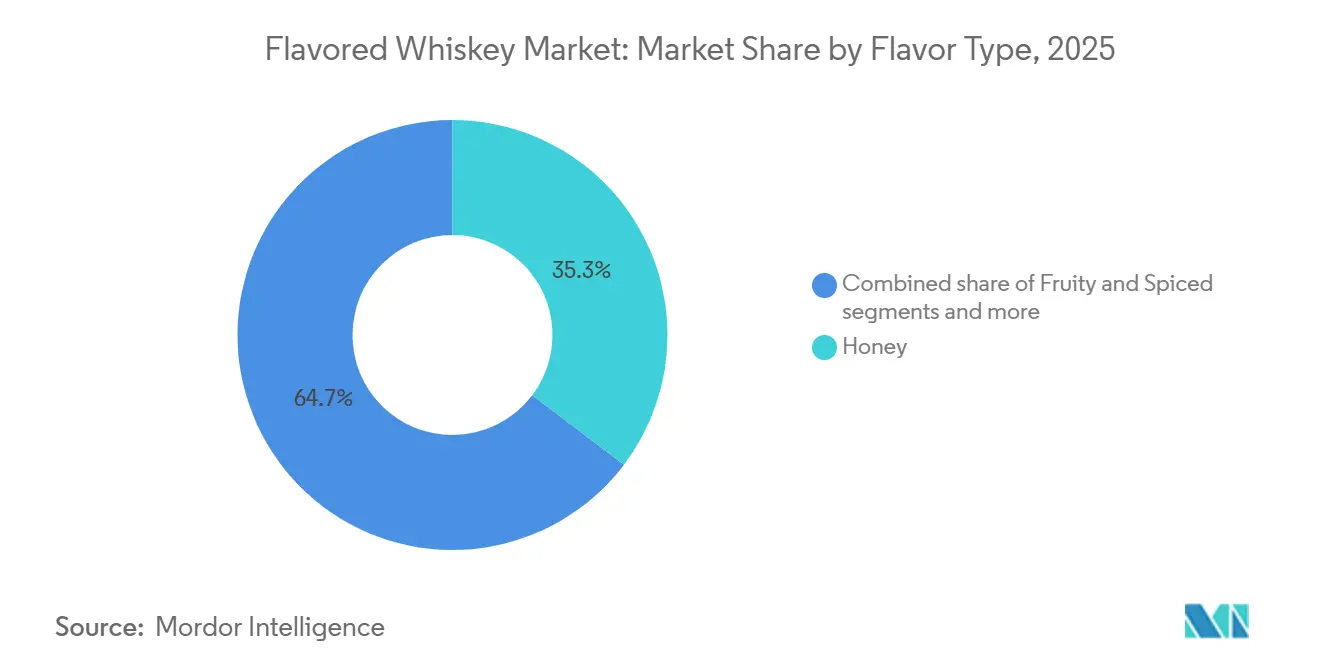

- By flavor, honey led with 35.30% of the flavored whiskey market share in 2025; fruity variants are forecast to expand at a 7.25% CAGR to 2031.

- By whiskey type, American expressions held 33.45% of the flavored whiskey market size in 2025, while Irish whiskey is set to record the highest CAGR at 6.10% through 2031.

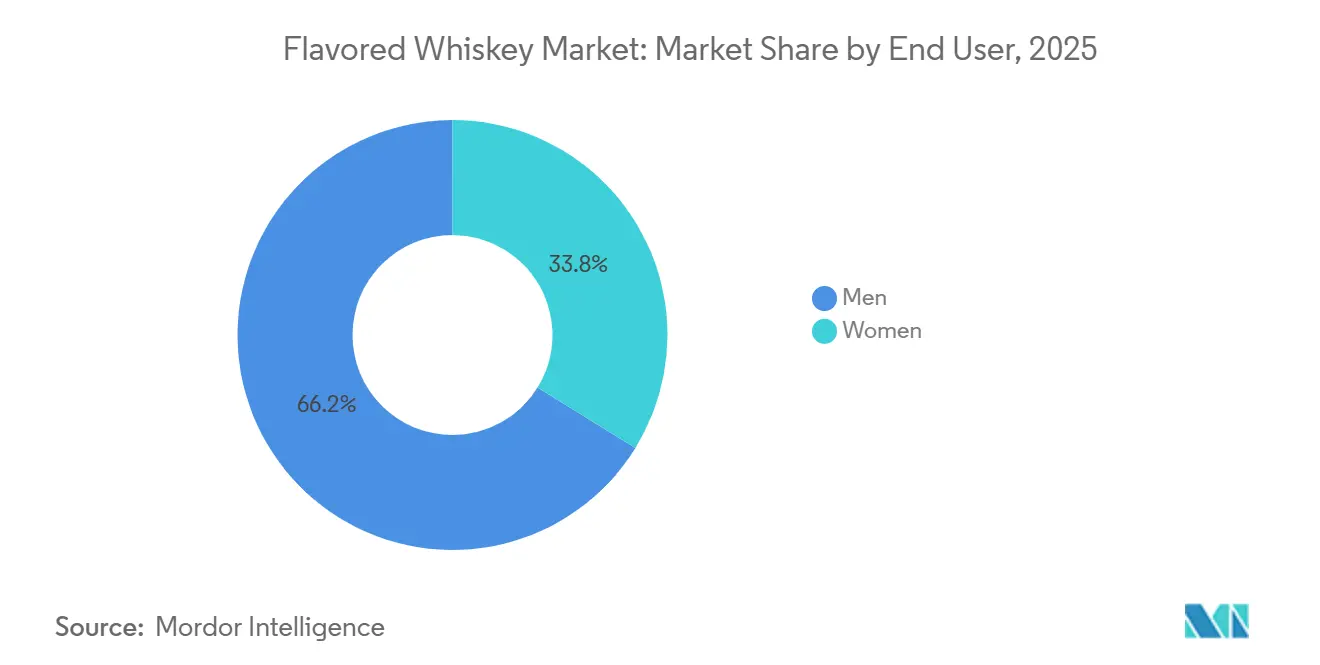

- By end user, men accounted for 66.20% of consumption in 2025; women represent the fastest-growing segment at a 6.35% CAGR to 2031.

- By distribution channel, off-trade captured 62.10% of revenues in 2025, whereas on-trade sales are expected to advance at a 5.91% CAGR between 2026 and 2031.

- By geography, Asia-Pacific commanded 33.10% of 2025 value; South America is projected to grow the quickest at 8.90% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flavored Whiskey Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shifting Consumer Preferences Toward Innovative Flavors and Formats | +1.2% | Global; strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Expanding Consumer Base, Including Increased Adoption Among Women | +0.9% | Global; notably North America and Europe | Long term (≥ 4 years) |

| Adoption of Experiential and Innovative Marketing Strategies | +0.7% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Premiumization and Rising Demand for High-Quality Flavored Whiskies | +0.8% | Global, led by developed economies | Medium term (2-4 years) |

| Growth of Craft and Artisanal Whiskey Segments | +0.5% | North America core, expanding worldwide | Long term (≥ 4 years) |

| Increasing Integration of Flavored Whiskies in Cocktail Mixology | +0.6% | Urban centers globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shifting Consumer Preferences Toward Innovative Flavors and Formats

Shifting consumer behaviors, increasingly linking alcohol consumption to lifestyle, identity, and sensory exploration, continue to drive the flavored whiskey market. Younger demographics, particularly Millennials and Gen Z, are prioritizing flavor experimentation over traditional brand heritage, accelerating demand for fruity, botanical, and hybrid variants. Research from the Yale School of Management highlights that purchase intent among these younger groups surges by over 20% when products are tied to social experiences, such as music festivals or summer events [2]Source: Yale School of Management, “Emotional Drivers in Beverage Alcohol Marketing,” som.yale.edu. In response, brands are introducing bold innovations across dessert-style, botanical, and fruit-infused expressions to capture evolving tastes. Recent launches such as Fireball’s Blazin’ Apple highlight how companies are leveraging familiar flavor profiles while introducing novelty to sustain consumer interest. Ready-to-drink formats are further accelerating adoption by removing preparation barriers and aligning with convenience-driven, on-the-go consumption patterns, particularly in urban markets.

Expanding Consumer Base, Including Increased Adoption Among Women

Flavored whiskey is witnessing a surge in popularity, particularly among women and first-time whiskey drinkers, who are gravitating toward smoother, fruitier, and more approachable profiles. This demographic shift is expanding the category, with flavored variants acting as gateway expressions that reduce the intensity typically associated with traditional whiskey. Brands are adopting inclusive, lifestyle-driven marketing strategies that emphasize mixability, versatility, and social consumption occasions. Honey-flavored expressions, in particular, have gained strong traction among female consumers due to their smoothness and cocktail adaptability. Products like Jack Daniel’s Tennessee Honey continue to exemplify this trend, reinforcing accessibility while maintaining brand familiarity. Additionally, the rise of women-led whiskey clubs and tasting events is fostering organic advocacy and repeat purchases, especially among urban, educated consumers. This evolving consumer base is reshaping brand narratives away from heritage-focused messaging toward more experiential and inclusive positioning, strengthening long-term engagement with the flavored whiskey category.

Adoption of Experiential and Innovative Marketing Strategies

Flavored whiskey brands are increasingly shifting from traditional advertising to immersive, experience-led marketing to build deeper emotional connections with consumers. Distilleries and premium brands are investing in activations such as themed tastings, pop-up bars, and festival sponsorships that allow consumers to engage directly with the product. Campaigns like The Macallan’s “You Know Me So Well” illustrate this trend, combining curated bar experiences, limited-edition collectibles, and travel incentives to create memorable, shareable moments. These strategies are particularly effective for flavored whiskey, where in-person tastings and cocktail demonstrations help overcome skepticism around flavor additives while educating consumers on versatility and usage occasions. Mobile tasting tours and event-based outreach further enable brands to connect with younger, experience-driven audiences in social settings, reducing reliance on traditional retail channels.

Premiumization and Rising Demand for High-Quality Flavored Whiskies

As consumers particularly those aged 21 to 44, increasingly prioritize quality, authenticity, and craftsmanship over volume, the flavored whiskey market is undergoing a notable premiumization shift. This “less but better” mindset is driving demand for higher-proof, aged, and limited-edition variants that offer exclusivity and strong provenance narratives. The 2025 Bartender Spirits Awards survey indicates that a significant share of U.S. drinkers in this demographic are gravitating toward premium spirits, reinforcing this upward trend. Producers are responding by investing in advanced techniques such as barrel finishing, extended maturation, and artisanal infusions to justify premium price points. The 2025 Bartender Spirits Awards survey reveals that 41% of U.S. drinkers within this demographic are now gravitating towards premium spirits [3]Bartender Spirits Awards, "Consumer Insight Report 2025", bartenderspiritsawards.com. Markets such as India exemplify this shift, with rising incomes and aspirational consumption fueling demand for premium and imported variants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Consumer Preference for Traditional Whiskey Variants | -0.6% | Global; steepest in traditional producing regions | Long term (≥ 4 years) |

| Premium Pricing Constraints on Flavored Whiskey Products | -0.4% | Global; accentuated in price-sensitive markets | Medium term (2-4 years) |

| Health Concerns Related to Sugar Content in Flavored Whiskies | -0.5% | North America and Europe; broadening worldwide | Short term (≤ 2 years) |

| Regulatory and Compliance Challenges Across Key Markets | -0.3% | Market-specific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Consumer Preference for Traditional Whiskey Variants

Traditional whiskey consumers, particularly purists in bourbon, Scotch, and Irish whiskey segments, continue to resist flavored variants, viewing added flavors as a dilution of authenticity and craftsmanship. Regulatory frameworks reinforce this stance; for instance, the Scotch Whisky Association prohibits flavor additions beyond caramel coloring, effectively excluding flavored expressions from the Scotch category and strengthening the divide between tradition and innovation. This resistance is most pronounced among older, high-value consumers, creating a strategic dilemma for producers balancing growth among younger cohorts with the need to protect legacy brand equity. As a result, companies are increasingly adopting portfolio segmentation strategies, where core brands remain unflavored while separate sub-brands or extensions carry flavored offerings to minimize reputational risk. Industry signals, such as record-breaking sales of premium unflavored whiskies like Macallan and continued demand for age-statement single malts from Glenfiddich, highlight enduring loyalty to traditional expressions. This dynamic limits premiumization potential and often leads retailers to position flavored variants outside high-end categories, constraining their role primarily to casual consumption and experimentation rather than gifting or investment-grade purchases.

Health Concerns Related to Sugar Content in Flavored Whiskies

Flavored whiskeys typically contain 8–12 grams of sugar per 1.5-ounce serving, placing them at odds with the growing consumer shift toward low-sugar and zero-calorie alcoholic beverages. Health-conscious consumers, particularly in North America and Europe, are increasingly scrutinizing ingredient labels and favoring “better-for-you” options such as vodka sodas, tequila, and unflavored whiskeys that align with wellness-oriented lifestyles. Regulatory developments add further pressure, as the U.S. Alcohol and Tobacco Tax and Trade Bureau (TTB) advances allergen disclosure and potential sugar-labeling requirements, which could heighten transparency and negatively impact consumer perception of high-sugar variants. This evolving landscape creates a regulatory overhang that may limit both trial and repeat purchases. Hence, producers are reformulating products with natural sweeteners, reducing sugar content, and introducing “light” or “skinny” flavored variants to align with health trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor Type: Fruity Variants Outpace Honey's Dominance

In 2025, honey-flavored variants continue to lead the flavored whiskey segment, accounting for approximately 35.30% of total revenue. Their dominance is driven by strong consumer preference for smooth, sweet, and approachable profiles that bridge traditional whiskey with enhanced drinkability. Products like Jack Daniel’s Tennessee Honey exemplify this appeal, maintaining strong traction across key markets due to their versatility and established brand equity. However, this dominance is gradually being challenged as consumer palates evolve beyond simple sweetness.

Fruity flavors are emerging as the fastest-growing segment, projected to expand at a CAGR of 7.25% through 2031. This growth is fueled by increasing demand for vibrant, cocktail-friendly profiles and innovations such as cinnamon-apple hybrids that introduce layered complexity. These offerings cater to younger consumers seeking experimentation and novelty in their drinking experiences. Meanwhile, spiced whiskeys retain a stable but mature position, while botanical variants, featuring herbal, floral, and tea-infused notes, are gaining traction among more sophisticated consumers. The “other flavors” category, including chocolate, coffee, and dessert-inspired expressions, is also expanding through limited-edition releases that drive trial and occasion-based consumption.

By Whiskey Type: Irish Whiskey's Tariff Edge Fuels Fastest Growth

In 2025, American whiskey continues to dominate the flavored whiskey market, accounting for approximately 33.45% of segment revenue. This leadership is underpinned by the strong heritage of bourbon and rye, alongside the global reach of brands like Jack Daniel’s and Jim Beam, which have successfully extended into flavored variants through established distribution networks and loyal consumer bases.

Irish whiskey is emerging as the fastest-growing segment, projected to expand at a CAGR of 6.10% through 2031. This growth is driven by favorable tariff structures and a global perception of Irish whiskey as smooth and approachable, qualities that align well with flavored expressions. Products such as Jameson Orange exemplify this trend, gaining traction among cocktail-oriented consumers, particularly in high-growth regions like Asia-Pacific. Scotch whisky remains constrained in the flavored segment due to regulatory restrictions from the Scotch Whisky Association, which prohibit flavor additives beyond caramel coloring, limiting its participation in this category. Meanwhile, Canadian whisky holds a stable position, supported by strong retail presence and flavored portfolios, while other categories, including Japanese, Indian, and emerging regional whiskies, represent nascent but promising opportunities driven by provenance and storytelling.

By End User: Women Drive Demographic Expansion

In 2025, men continue to dominate the flavored whiskey segment, accounting for approximately 66.20% of total market share, reflecting the category’s strong roots in traditional whiskey consumption. However, consumption patterns are evolving, with male consumers increasingly exploring flavored variants that blend classic whiskey character with sweeter, more approachable profiles.

Women are the fastest-growing demographic, with a projected CAGR of 6.35%, driven by increasing participation and shifting perceptions of whiskey as a more inclusive and versatile spirit. Brands are responding with targeted marketing strategies that emphasize lifestyle, social occasions, and cocktail culture, moving away from traditionally masculine narratives. This transition is shaping product development, with a focus on smoother taste profiles, refined packaging, and experiential positioning.

By Distribution Channel: Off-Trade Dominance Meets On-Trade Innovation

In 2025, flavored whiskey sales are predominantly driven by off-trade channels, which account for 62.10% of total revenue. This reflects a sustained shift toward at-home consumption, supported by convenience, price transparency, and the rapid growth of e-commerce and direct-to-consumer models. Specialty liquor stores play a key role within this segment by offering curated selections, in-store expertise, and tasting events that encourage trial, particularly for premium and craft expressions.

On-trade channels are experiencing a recovery, projected to grow at a CAGR of 5.91% through 2031. This resurgence is fueled by the return of experiential consumption in bars, restaurants, and entertainment venues, where bartenders активно incorporate flavored whiskeys into signature cocktails, enhancing both product visibility and consumer engagement, as highlighted by the National Restaurant Association. Direct-to-consumer models are also gaining traction, enabling producers to strengthen customer relationships and capture higher margins. However, distributor consolidation continues to challenge smaller brands, pushing them to focus on experiential and niche channels where differentiation can offset scale limitations.

Geography Analysis

In 2025, the Asia-Pacific region leads the flavored whiskey market with a 33.10% share, driven by strong consumption growth in countries like India and China. India, in particular, stands out with rising whiskey demand and exports, while younger urban consumers increasingly favor flavored variants for their mixability and social appeal. Japan, traditionally a purist market, is gradually embracing limited-edition flavored innovations, while Southeast Asian countries such as Vietnam, Indonesia, and Thailand present high-growth opportunities due to low penetration and openness to experimentation.

South America is the fastest-growing region, projected to expand at a CAGR of 8.90% through 2031. Growth is fueled by rising disposable incomes and a cultural shift toward spirits in markets like Brazil, Argentina, and Chile. The region’s relatively low resistance to flavored variants supports strong trial and adoption, although challenges such as currency volatility and distribution fragmentation persist.

North America remains a mature and significant market, supported by the dominance of American whiskey-based flavored variants, though growth is moderating due to saturation and increasing health consciousness. Europe faces regulatory and cultural constraints, particularly in traditional whiskey markets, while the Middle East and Africa represent emerging opportunities, with growth concentrated in urban centers. Overall, regional dynamics highlight the need for localized strategies that balance expansion in high-growth markets with stability in mature regions.

Competitive Landscape

The flavored whiskey market exhibits moderate consolidation, where global players such as Brown-Forman, Diageo, Beam Suntory, Pernod Ricard, and Sazerac dominate through strong distribution networks, brand equity, and continuous innovation. These companies leverage large-scale production capacity and data-driven strategies to expand flavored portfolios across price points, while maintaining consistency and global reach.

Craft distilleries and regional players are carving out niche opportunities through botanical infusions, locally sourced ingredients, and limited-edition releases that command premium pricing. This has created a bifurcated competitive landscape, where large players focus on portfolio breadth and shelf dominance, while smaller producers emphasize differentiation and storytelling through direct-to-consumer and experiential channels.

Industry consolidation is accelerating, highlighted by strategic moves such as Pernod Ricard’s divestiture of Imperial Blue and ongoing merger discussions with Brown-Forman, reflecting the need to scale premium portfolios in a slowing global spirits market. Significant capital investments, including large-scale distillery expansions, further raise entry barriers and favor established incumbents.

Flavored Whiskey Industry Leaders

-

Brown-Forman Corporation

-

Diageo plc

-

Beam Suntory Inc.

-

Pernod Ricard SA

-

Sazerac Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Heaven Hill Brands introduced Evan Williams Blackberry, a fruit-flavored whiskey aimed at younger consumers and cocktail use, leveraging its large-scale production and strong distribution to expand presence across both on-trade and off-trade channels.

- September 2025: Heaven Hill opened its USD 200 million Springs Distillery in Kentucky, boosting capacity and innovation capabilities, alongside launching the USD 225 Master Distillers Unity limited-edition bourbon.

- August 2025: Diageo launched Crown Royal Chocolate Flavored Whisky, a limited-edition, dessert-inspired variant , aimed at expanding its flavored portfolio and driving cocktail-based consumption.

- March 2025: Round Barn Distillery debuted its Harvest Infusion Series Apple, Cinnamon, Vanilla and Peach showcasing Michigan-grown ingredients.

Global Flavored Whiskey Market Report Scope

The global flavored whiskey market is analyzed across multiple dimensions, including flavor type, whiskey type, end user, distribution channel, and geography. By flavor type, the market is segmented into honey, fruity, spiced, botanical, and others. By whiskey type, it includes American, Irish, Canadian, Scotch, and others. By end user, the market is categorized into men and women. Distribution channels comprise off-trade and on-trade channels. Geographically, the study covers key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. For each segment, market sizing and forecasts are provided in terms of value (USD million) and volume (in liters)

| Honey |

| Fruity |

| Spiced |

| Botanical |

| Other Flavor Type |

| American |

| Canadian |

| Irish |

| Scotch |

| Others |

| Men |

| Women |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off-Trade Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Norway | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Nigeria | |

| Rest of Middle East and Africa |

| By Flavor Type | Honey | |

| Fruity | ||

| Spiced | ||

| Botanical | ||

| Other Flavor Type | ||

| By Whiskey Type | American | |

| Canadian | ||

| Irish | ||

| Scotch | ||

| Others | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off-Trade Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in the flavored whiskey market?

Younger consumers’ demand for sweeter profiles, premiumization momentum and cocktail culture adoption are the chief growth engines for the flavored whiskey market.

Which flavored segment holds the largest share of the flavored whiskey market size?

Honey variants led with 35.30% share of the flavored whiskey market size in 2025.

Which region leads the flavored whiskey market?

Asia-Pacific headed the flavored whiskey market with 33.10% value share in 2025.

How fast is the women consumer segment growing in the flavored whiskey market?

Women are the fastest-growing consumer group, posting a 6.35% CAGR between 2026 and 2031.

Page last updated on: