Whiskey Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 162.18 Billion |

| Market Size (2031) | USD 197.65 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

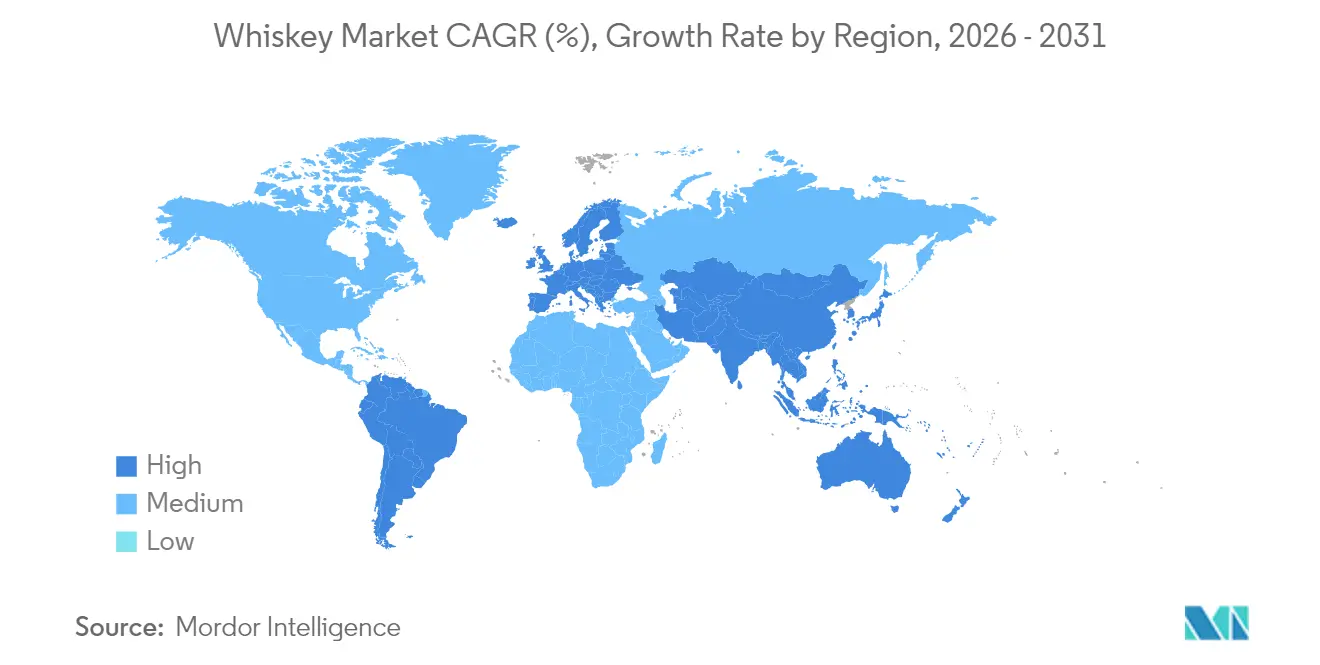

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Whiskey Market Analysis by Mordor Intelligence

Whiskey market size in 2026 is estimated at USD 162.18 billion, growing from 2025 value of USD 155.87 billion with 2031 projections showing USD 197.65 billion, growing at 4.05% CAGR over 2026-2031. According to the Alcohol and Tobacco Tax and Trade Bureau, this growth is driven by evolving consumer preferences, the formal recognition of American Single Malt in January 2025, and a continued focus on premiumization. Scotch remains the dominant category; however, Irish whiskey is experiencing the fastest growth in terms of volume. Additionally, the increasing participation of female consumers and the expansion of e-commerce channels are significantly transforming market dynamics and distribution strategies. Regulatory reforms in major whiskey-producing countries are reducing barriers for craft distillers, fostering innovation and competition. Despite these positive developments, the market faces challenges such as potential EU tariffs and proposed U.S. labeling regulations, which could increase operational costs. On the supply side, capacity expansions, such as Buffalo Trace's USD 1.2 billion investment announced in January 2025, demonstrate confidence in the market's long-term growth potential. This expansion will increase the distillery's production capacity by 150%, enabling it to produce up to 500,000 barrels annually, ensuring readiness to meet future demand despite short-term inventory fluctuations.

Key Report Takeaways

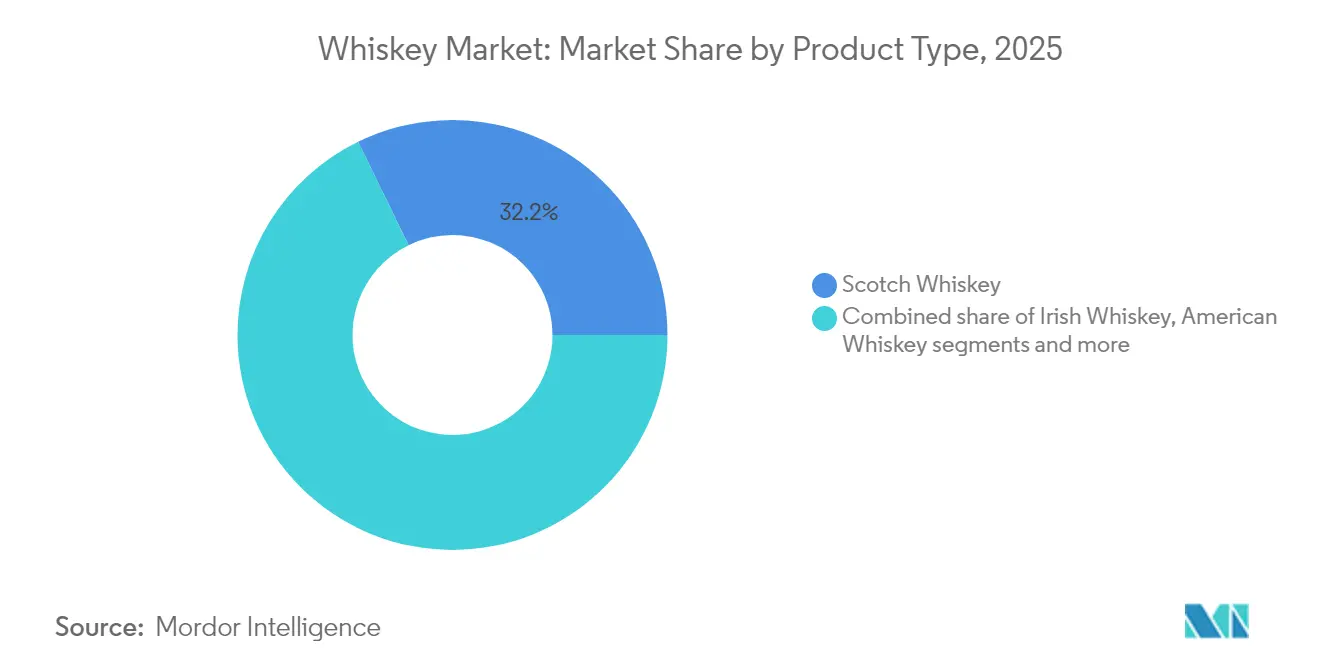

- By product type, scotch retained 32.23% of whiskey market share in 2025, whereas Irish whiskey is projected to grow at a 4.76% CAGR through 2031.

- By end user, male consumers accounted for 66.61% of the whiskey market in 2025; the female segment is expanding at a 4.89% CAGR to 2031.

- By category, the mass segment held 60.84% of the whiskey market size in 2025; premium expressions are forecast to rise at a 5.18% CAGR to 2031.

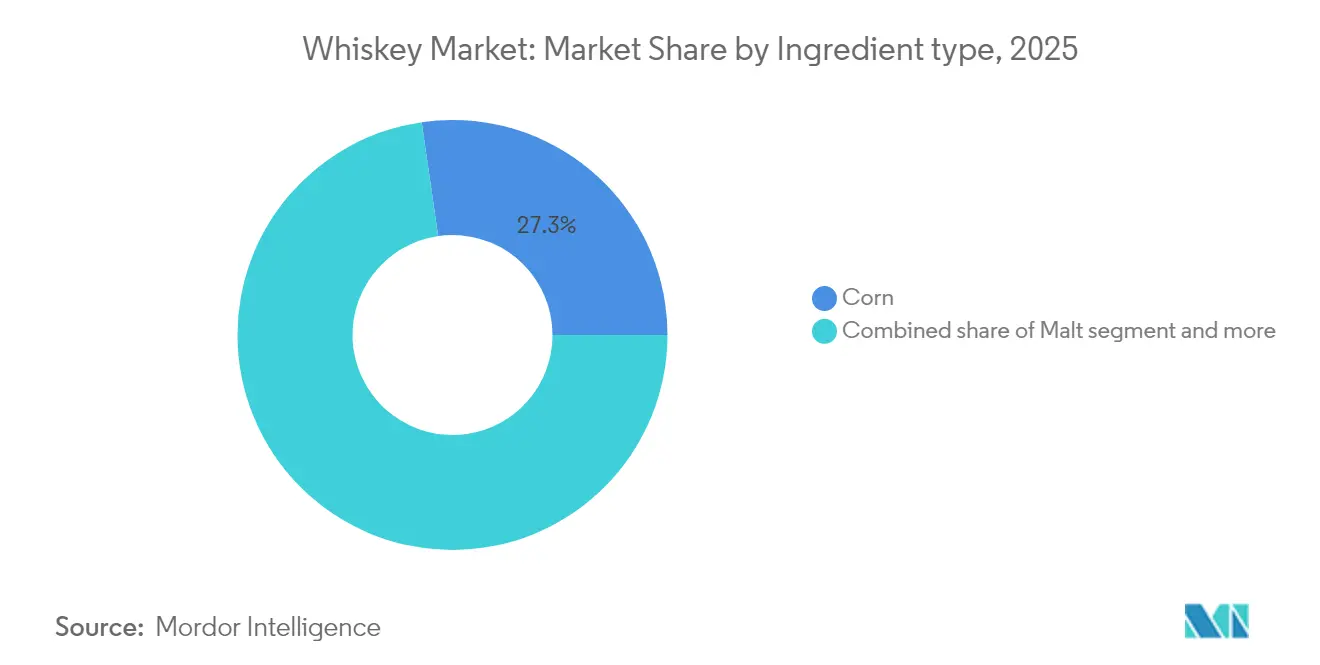

- By ingredient, corn-based spirits commanded 27.29% of the whiskey market size in 2025, while malt-based are advancing at a 5.47% CAGR between 2026-2031.

- By distribution channel, on-trade captured 53.10% of the 2025 whiskey market; off-trade is expected to expand at a 4.44% CAGR through 2031.

- By geography, Asia-Pacific led with 30.30% whiskey market share in 2025, yet South America is set for the highest regional CAGR of 5.62% to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Whiskey Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of aged, limited releases | +1.0% | North America and Europe | Medium term (2-4 years) |

| Global cocktail culture and mixology growth | +0.7% | Urban Asia-Pacific, global metros | Short term (≤ 2 years) |

| Growing connoisseurship and education | +0.6% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Sustainability and eco-friendly packaging | +0.3% | Europe, North America, global spill-over | Medium term (2-4 years) |

| Expansion of craft distilleries | +0.5% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Whiskey tourism and experiential marketing | +0.4% | Traditional whiskey regions worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization and Demand for Aged, Limited-Edition Whiskeys

Driven by a growing consumer appetite for premium whisky, super-premium bottles are now commanding higher prices. Distillers, by emphasizing scarcity, heritage narratives, and innovative cask techniques, not only justify these elevated price points but also bolster their brand equity. Scotch, Irish, and American whiskies, celebrated for their unique production processes, enjoy a competitive edge in the premium segment. The rise of whiskey investment funds, backed by high-net-worth individuals seeking alternative assets, has tightened supply and extended aging cycles. Furthermore, producers who highlight transparent provenance data on their labels cultivate deeper trust with collectors. This robust demand not only supports ambitious warehouse expansions but also encourages extended maturation periods, collectively propelling the whiskey market upwards. A case in point: In May 2025, International Beverages Company unveiled a significant expansion of its whiskey warehouse in Scotland. This expansion, entailing an investment of USD 9.37 million, boosted the facility's capacity by 60,000 casks, bringing the total to an impressive 700,000 casks.

Expanding Global Cocktail Culture and Mixology Trends

Urbanization and the growing influence of social media have brought bartender creativity into the spotlight, driving whiskey's integration into both classic and contemporary cocktails. This trend reflects evolving social behaviors, with Diageo's 2025 trends report identifying "zebra striping" a practice where consumers alternate between alcoholic and non-alcoholic beverages as a response to the increasing focus on wellness while maintaining active social lives. The impact of mixology extends beyond bars and restaurants, influencing home consumption patterns as well. Consumers are increasingly seeking premium whiskeys that not only excel when consumed neat but also enhance the quality of cocktails. The expanding number of bars and pubs across the market has further fueled the demand for cocktails and mixed drinks. To capitalize on this growing trend, manufacturers are focusing on ready-to-drink cocktail offerings. In the Asia-Pacific region, bars are promoting flavored highballs and low-ABV spritzes, which are particularly appealing to younger, legal-age consumers, encouraging them to explore the category. Additionally, the rising popularity of ready-to-serve batched cocktails is blurring the lines between on-trade and off-trade consumption occasions, further driving the demand for versatile whiskey styles and increasing overall volume growth in the market.

Rising Whiskey Appreciation and Connoisseurship

Driven by a growing appreciation for premium and craft experiences, consumers are increasingly turning to whiskey. This trend, fueled by whiskey clubs, festivals, and active social media communities, highlights a rising interest in whiskey tasting, education, and collecting. Educational initiatives and experiential marketing deepen consumer engagement, with distillery tourism now emerging as a significant revenue stream alongside traditional sales. Prestigious institutions are stepping in, offering courses on whiskey technology and tasting. For example, the University of Glasgow presents "Whisky: Technology, Product and Marketing," while the London School of Whisky boasts an "Advanced Whisky Tasting" course. As consumers become savvier, there's a heightened demand for unique, high-quality, and limited-edition whiskeys. This evolving appreciation not only drives innovation in production techniques and aging processes but also enhances product differentiation and market appeal.

Sustainability Initiatives and Innovative Packaging

Industry leaders, motivated by ambitious climate goals, are accelerating the adoption of renewable energy and circular packaging solutions. Diageo's carbon-neutral Kentucky facility exemplifies this shift by offsetting an impressive 117,000 metric tons of emissions annually, demonstrating that large-scale operations can successfully align with net-zero objectives. Johnnie Walker has initiated trials of recyclable paper bottles, aiming to significantly reduce reliance on traditional glass packaging. At the same time, smaller distillers are achieving net-zero emissions for scopes 1 and 2 by leveraging biomass boilers and utilizing 100% recycled glass in their production processes. The growing importance of certifications and life-cycle disclosures is increasingly shaping consumer purchasing decisions, highlighting that sustainability attributes now stand on par with traditional factors like age and provenance as key drivers of consumer choice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -0.5% | Global, particularly stringent in Europe and North America | Short term (≤ 2 years) |

| Consumers' inclination towards healthy beverages | -0.4% | Developed markets primarily, emerging in Asia-Pacific | Medium term (2-4 years) |

| Climate change impact on raw material supply | -0.3% | Global, most acute in traditional grain-growing regions | Long term (≥ 4 years) |

| Increasing consumer shift towards low-alcohol and non-alcoholic alternatives | -0.6% | Developed markets, expanding to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations

As trade complexities intensify between producing and consuming nations, the demand for whiskeys, including Scotch, Irish, and American varieties, is expected to face significant challenges in importing countries. These challenges stem from limited product availability and rising prices, which could deter consumer interest. The U.S. Tax and Trade Bureau is currently evaluating the introduction of “alcohol facts” panels and allergen disclosures on product labels. If implemented, these regulatory changes would likely impose substantial financial burdens on distillers, as they would require comprehensive label redesigns and extensive laboratory testing to ensure compliance. Additionally, a 50% tariff on American whiskey entering the European Union is set to take effect in April 2025. In response to these developments, distillers may consider redirecting their focus to emerging markets in Asia-Pacific and Latin America. However, this strategic shift would necessitate significant investments in developing new logistics frameworks and route-to-market strategies. Such efforts could compress profit margins and potentially dampen overall market demand, adding further complexity to the industry's growth trajectory.

Consumers’ Inclination Toward Healthy Beverages

In several developed economies, moderation trends driven by millennials and Gen Z are significantly reducing per-capita ethanol consumption. To address this shift, major producers are adjusting their marketing strategies by focusing on mindful-drinking campaigns and encouraging smaller serve sizes, moving away from the traditional "big pour" approach. For example, Spirits Europe reported that approximately 98 information campaigns successfully reached up to 80 million consumers across 25 European countries [1]Source: Spirits Europe, "Responsible Drinking Initiatives, Annual Impact Report 2025," spirits.eu. This strategic change reflects the growing consumer demand for beverages that provide refreshment with fewer calories and a lower alcohol by volume (ABV). This trend is further highlighted by the increasing popularity of functional flavored water and hard seltzer. Although premium whiskey continues to represent aspirational value, its consumption frequency may gradually decline as health-conscious narratives and lifestyle preferences become more influential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Irish Agility Challenges Scotch Heft

In 2025, scotch whiskey held a significant 32.23% share of the global whiskey market, underscoring its enduring reputation and extensive global distribution network. The category's dominance is rooted in its premium age-statement expressions, which continue to be highly sought after, particularly in Asian markets where the strong gifting culture drives consistent demand. However, Scotch whiskey is not without its challenges. Rising costs, driven by the EU's carbon-border adjustment mechanisms, are expected to increase import expenses for glass bottles, potentially impacting pricing strategies. Additionally, the category faces growing competition from emerging whiskey types and evolving consumer preferences that lean toward innovation and variety. Despite these hurdles, Scotch whiskey's deep heritage, consistent quality, and established presence in the luxury segment ensure its position as a cornerstone of the global whiskey market remains unshaken.

Irish whiskey is experiencing rapid growth, with a projected CAGR of 4.76% through 2031. This growth is fueled by targeted investments in advanced triple-distillation techniques, diverse cask finishes, and immersive visitor experiences that enhance brand engagement. According to the Irish Whiskey Association, the number of operational distilleries in Dublin and Cork has seen a remarkable increase, rising from just four in 2010 to an anticipated 32 by 2025. These distilleries are leading the way in innovation, experimenting with unique cask finishes such as Calvados, Sauternes, and even tea barrels, creating distinctive flavor profiles that set Irish whiskey apart from traditional Highland and Speyside Scotch varieties. Globally, Irish whiskey brands are gaining traction on premium cocktail menus in cities ranging from Singapore to São Paulo. Their lighter, more approachable styles are particularly appealing to new legal-age consumers, further solidifying Irish whiskey's growing prominence in the global market.

By End User: Female Participation Reframes Demand

In 2025, men continued to dominate global whiskey consumption, accounting for 66.61% of the market share. This demographic has long influenced whiskey culture and purchasing trends, favoring bold, barrel-strength expressions and traditional flavor profiles such as fermented rye florals. Distilleries have consistently catered to this core audience by focusing on offerings that emphasize depth, complexity, and heritage. However, marketing strategies are gradually evolving to strike a balance between honoring tradition and appealing to contemporary tastes. These strategies are incorporating more inclusive narratives while ensuring they do not alienate the loyal male consumer base.

Women are emerging as the fastest-growing demographic in the whiskey market, boasting a projected CAGR of 4.89% through 2031. Their rising involvement in formal tasting clubs underscores their significant sway over the market, influencing everything from flavor innovations and packaging designs to event programming. For instance, data from the Spanish Observatory on Drugs and Addictions indicates that, as of 2024, younger women are consuming more alcohol than their older counterparts . In light of this trend, distilleries are honing in on barrel-strength profiles and floral rye notes, tailoring them to female palates. Marketing strategies have evolved, shifting from traditional masculine narratives to inclusive storytelling that highlights the diversity of master blenders and distillery leaders. Women are gravitating towards premium whiskey segments, frequently opting for limited editions as gifts or personal acquisitions.

By Category: Premium Keeps Outpacing Mass

In 2025, mass-market whiskey variants captured 60.84% of the global volume, becoming pivotal for consumers diving into highball culture and cocktail trends, particularly in emerging markets. These budget-friendly options not only familiarize newcomers with whiskey but also serve as popular bases for mixed drinks during casual gatherings. Yet, despite their volume lead, mass-market variants grapple with challenges from inflation and evolving consumer tastes, straining both margins and discretionary spending. Producers in this arena face the dual challenge of ensuring affordability while upholding a quality image to stay relevant and maintain volume.

Meanwhile, the premium and super-premium whiskey segments are on a rapid ascent, eyeing a CAGR of 5.18% through 2031. This growth is fueled by consumers opting for upscale choices during celebrations and gifting, especially in Asian markets. Here, luxury touches, like embossed bottles, custom closures, and reusable decanters, serve as markers of quality, justifying their elevated price tags. The trend of premiumization is further bolstered by cask-strength releases, which exude authenticity and craftsmanship. At the same time, ultra-premium whiskeys, particularly those aged 18 years and above, enjoy robust demand, often flying off the shelves through direct-to-consumer sales.

By Ingredient: Corn Dominance Meets Experimental Wave

In 2025, bourbon, a corn-based spirit, held a commanding 27.29% share of the global whiskey market. This dominance is largely attributed to bourbon's entrenched popularity in the U.S. and its surging appeal in global markets. For instance, the Distilled Spirits Council of the United States reported that exports reached a record USD 2.4 billion in 2024 . Bourbon's unique sweet and full-bodied profile, combined with its rich heritage, has solidified its status as a global whiskey staple. This segment enjoys advantages from established production standards, widespread consumer recognition, and strong distribution networks. Furthermore, blended grain whiskeys, which often mix corn with other grains, maintain a prominent position at mainstream price points. They achieve this by offering consistent flavors and scale efficiencies, ensuring their availability in both on-trade and off-trade channels.

Forecasted to grow at a 5.47% CAGR through 2031, malt-based whiskeys are emerging as the fastest-growing segment, fueled by rising global appreciation for craftsmanship and authenticity. Crafted from 100% malted barley, these whiskeys attract connoisseurs who value depth, complexity, and heritage. The American single malt category stands out, merging traditional Scotch-making with domestic innovations like aging in smaller casks and regional experimentation. This trend mirrors a wider consumer shift towards premiumization and narrative-driven choices. Rye and wheat whiskeys, meanwhile, carve out their niches: rye for cocktail aficionados and wheat for those with a preference for a smoother taste. The surging demand for malt not only highlights an evolution in consumer preferences but also underscores the segment's growing significance in the global whiskey landscape.

By Distribution Channel: Digital Off-Trade Accelerates

In 2025, bars, restaurants, and experiential venues, collectively known as the on-trade channel, commanded a significant 53.10% share of the global whiskey market. This segment flourishes on consumers' cravings for immersive drinking experiences, innovative cocktails, and social interactions in curated settings. The allure of premium whiskey selections and tailored cocktail menus enhances the on-trade's appeal, prompting consumers to pay a premium. While digital commerce gains traction, the on-trade channel remains paramount for brand discovery and sensory exploration, nurturing profound emotional ties between consumers and whiskey brands.

Off-trade channels, encompassing retail outlets and online platforms, are set to expand at a 4.44% CAGR until 2031, spurred by regulatory changes and digital advancements. In the U.S., shifting alcohol e-commerce regulations now permit direct-to-consumer shipping across 48 states, with many EU markets mirroring this approach. Online specialty retailers are boosting engagement through livestream tastings, turning viewers into immediate buyers and simplifying the purchasing process. In China, social-commerce platforms host brand live-streams, attracting tens of thousands of viewers, frequently

Geography Analysis

In 2025, Asia-Pacific holds a 30.30% share of the whiskey market, reflecting the region's growing affluence and evolving drinking habits. India, the largest whiskey market globally by volume, continues to benefit from increasing per-capita alcohol consumption and a strong focus on premiumization. This trend is further emphasized by Pernod Ricard's significant investment of INR 1,785 crore in a malt facility in Nagpur, set to enhance local sourcing capabilities in September 2024. Additionally, regulatory changes favoring higher-quality grain import quotas are creating a supportive environment for growth in the region.

South America is projected to achieve a 5.62% CAGR through 2031, driven by several key factors. Brazil's formal recognition of Scotch as a geographical indication in 2024 has provided greater legal clarity, enhancing consumer trust in the category. Furthermore, the expanding middle class and increasing inbound tourism in countries like Chile and Colombia are broadening the demand for premium whiskey imports. Local distillers in regions such as São Paulo and Patagonia are also leveraging native woods for cask finishing, which not only reinforces authenticity but also aligns with the growing narrative of import substitution and sustainability.

North America and Europe, while mature markets, remain critical for establishing and maintaining brand equity. In Europe, whiskey consumption continues to be deeply rooted in social settings, including cocktail bars and at-home gatherings, which sustain steady demand. Meanwhile, Africa and the Gulf regions, though still emerging markets, present significant growth opportunities. In Kenya, regulatory liberalization is paving the way for market expansion, while selective duty-free openings in the UAE are introducing premium whiskey categories to previously untapped consumer segments, signaling potential for long-term growth.

Regulatory Landscape

Whiskey regulation is framed by standards of identity, labeling rules, and geographical indication (GI) protections, which affect market access and compliance costs across major trading blocs. In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) finalized a standard of identity for American Single Malt Whisky (published as a final rule in December 2024), providing a clearer labeling and positioning framework for domestic producers alongside existing distilled spirits standards in 27 CFR (including 27 CFR 5.143). Trade measures also remain a swing factor for cross-border pricing and portfolio planning; for example, the Office of the United States Trade Representative (USTR) issued a statement in April 2026 on preferential duty access for whiskey produced in the United Kingdom, highlighting how tariff treatment can shift competitiveness for imported UK-origin whiskey.

In Europe, product definitions and GI frameworks continue to anchor category integrity and enforcement. EU Regulation (EU) 2019/787 sets core spirit drink rules, including a 40% minimum ABV for products labeled as whisky/whiskey, while EU Regulation (EU) 2024/1143 (effective 2024) updates processes around registration, opposition, and enforcement for GIs, which is relevant for protected names such as Scotch Whisky. In the United Kingdom, Scotch Whisky production and labeling are governed through UK requirements and guidance (including rules around production and maturation in Scotland), reinforcing provenance claims that support premiumization and export positioning.

Competitive Landscape

The global whiskey market is moderately fragmented, and a dynamic mix of multinational corporations and agile independent players shapes the competitive landscape. Pernod Ricard's move to establish a dedicated whiskey division in the United States, coupled with its investment in a high-end malt distillery in China, highlights its strategic efforts to diversify its portfolio beyond its established Scotch offerings and cater to evolving consumer preferences.

Capacity expansion continues to be a key focus across the industry, as brands aim to position themselves to meet growing future demand while ensuring consistent product allocations. Concurrently, emerging players are increasingly adopting advanced technologies to secure a competitive edge in the market. A prominent example is Whiskey House of Kentucky, which, in July 2024, introduced artificial intelligence to enhance its fermentation processes. This technological advancement resulted in an impressive 50% reduction in energy consumption compared to Energy Star benchmarks. This achievement highlights the significant role of technology-driven innovations in promoting sustainability within whiskey production.

While mergers among craft whiskey producers remain selective, strategic consolidations are increasingly focused on achieving operational efficiencies. These include shared bottling facilities, enhanced visitor-center experiences, and the scaling of digital storefronts to reach broader audiences. As competition intensifies, the industry faces the challenge of balancing the preservation of brand heritage with the adoption of data-driven production methods and sustainability practices that resonate with environmentally conscious and modern consumers.

Whiskey Industry Leaders

-

Diageo PLC

-

Pernod Ricard SA

-

Suntory Holdings Ltd

-

Asahi Group Holdings Ltd

-

Bacardi Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Decarbonization and process innovation are creating space around energy-intensive distillation and peated malt supply, with multiple named initiatives moving from pilot work to deployment. In March 2026, Supercritical Solutions completed the WhiskHy project with Suntory Global Spirits, demonstrating a direct-fired hydrogen-distilled spirit, and in April 2026 Annandale Distillery commissioned a modular thermal energy storage hub (Exergy3) designed to generate high-temperature heat for distilling steam using renewable wind power. On the inputs side, Boortmalt introduced Ionsmoke (March 2026), an ionization approach developed with EBSmoke that reduces peat consumption by 30-40% for peated malt, which supports producers facing tighter sustainability scrutiny and supply constraints.

Investment is also clustering around visitor-centric capacity additions and localization of production in growth markets, strengthening route-to-market control and brand-experience monetization. In July 2026, Horse Soldier Bourbon opened the USD 200 million American Freedom Distillery and visitor center in Somerset, Kentucky, reflecting destination-distillery models that integrate production with tourism and direct engagement. In Japan, Karuizawa Distillers broke ground on a second facility, the Furaliss Distillery in Hokkaido (June 2026), in partnership with Seibu Group and Furano City, indicating ongoing premium whisky capacity build-out tied to place-based storytelling and regional development partnerships.

Recent Industry Developments

- July 2026: Horse Soldier Bourbon opened the USD 200 million American Freedom Distillery and visitor center in Somerset, Kentucky. The project adds new U.S. whiskey production capacity while expanding destination-led revenue through a Kentucky Bourbon Trail style tourism model. It reinforces the broader industry shift toward integrated production and brand-experience investments.

- February 2025: Brown-Forman and Reyes Beverage Group entered into a strategic partnership to manage a distribution network in California. The arrangement strengthens route-to-market execution in a key U.S. state, supporting improved availability and shelf presence for whiskey portfolios across on-trade and off-trade accounts. It also signals continued focus by major suppliers on distributor scale and logistics capabilities.

- November 2024: Diageo began production of whiskey and other alcoholic beverages in China backed by an investment of around USD 120 million to establish a production facility. This move expands localized supply for a major demand market and supports portfolio control across pricing, packaging, and compliance. It also increases competitive intensity for premium whiskey positioning within China by pairing a production footprint with brand building.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the whisky market is defined as revenues generated from commercial sales of whisky across on-trade and off-trade channels, tracked at the producer and brand level, and reported in USD for a consistent global view.

Scope exclusions: illicit or unrecorded alcohol, home distillation, and non-whisky spirits are excluded from the market totals.

Segmentation Overview

-

By Product Type

- American Whiskey

- Irish Whiskey

- Scotch Whiskey

- Canadian Whiskey

- Other Product Types

-

By End User

- Men

- Women

-

By Category

- Mass

- Premium

-

By Ingredient

- Corn

- Malt

- Blended

- Others

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Others Off Trade Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Norway

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Vietnam

- Indonesia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Rest of South America

-

Middle East and Africa

- South Africa

- Nigeria

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the market context and to anchor the model to real-world signals that can be checked year over year. We relied on public datasets and official publications such as UN Comtrade trade statistics, national customs and excise releases, and government statistics offices that publish alcohol production and consumption indicators.

To keep assumptions realistic, company annual reports, investor presentations, and filings were reviewed to understand geographic exposure, premiumization mix, and channel strategies. Additional validation points were gathered from trade associations and public briefings, including Scotch whisky export and shipment summaries, along with peer-reviewed articles that discuss alcohol demand trends and pricing behavior. Where available, analysts also used approved paid subscriptions for company financials and for shipment-level import and export checks, and then compared results back to public series for consistency. The sources listed here are illustrative, and other public references were also used during data collection, validation, and follow-up clarification.

Primary Interviews and Surveys

Primary work focused on filling gaps that desk sources cannot answer cleanly, especially around channel price realization, mix shifts, and how volumes translate into value by region. We spoke with a spread of industry participants across the supply chain, including distillers, distributors, importers, and retail and on-trade decision makers. Coverage was kept broad across APAC, EMEA, and the Americas to avoid a single-region bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 19% | APAC: 42% |

| Mid tier: 47% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 20% | Managers: 50% | Americas: 22% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs value by combining alcohol category demand signals with trade flows and reported market structure, and then converts those into whisky-specific spend using mix and price ladders. Once the initial totals were formed, they were cross-checked with selective bottom-up approximations, such as sampling typical price per liter trends by channel and region, and then multiplying by implied consumption volumes to see if the totals remained sensible.

Key inputs that shaped the model included export and import values for whisky-linked HS codes, estimated consumption levels in liters of alcohol where available, on-trade versus off-trade share shifts, premium and super-premium mix changes, and regional currency timing for converting local spend into USD. Where data was missing for smaller markets, gaps were handled through proxy indicators such as neighboring-market consumption patterns and trade intensity, followed by adjustments after expert feedback.

For forecasting, scenario analysis was used so that growth paths could be tied to clear drivers, including price realization, premiumization pace, and channel recovery patterns in travel retail and bars. Assumptions were kept practical, and any step that pushed results away from observable trade and consumption signals was reviewed and corrected before finalizing.

Data Validation & Update Cycle

Validation was done through step-by-step checks, so model outputs were compared with independent metrics like trade value trends, reported category growth, and major regional demand indicators. When the numbers showed unusual jumps, the inputs were rechecked, and follow-up calls were triggered to confirm whether the change came from pricing, mix, or a data timing issue.

Before sign-off, results go through more than one analyst review, which helps catch unit errors, currency conversion timing issues, and double counting between channels. Reports are refreshed annually, and interim updates are made when material events occur that could shift pricing, supply, or demand. Right before delivery, a fresh final pass is performed so clients receive the most current view available.

Mordor Intelligence's Whisky Market Size Versus Other Published Estimates

Different publishers often show different whisky market sizes because they do not always count the same scope, time window, and pricing logic, even when they use similar words in the title. Variations also come from whether value is measured closer to retail spending or closer to producer revenues, and from how currency conversion is handled across regions.

The main gap comes from price and channel treatment, where Mordor Intelligence counts whisky value in a way that stays consistent across on-trade and off-trade pricing and avoids inflating totals with taxes and retail markups that are not part of producer-level revenue in several countries.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 162.18 B (2026) | |

| Industry Publisher A | USD 67.43 B (2024) | Uses an earlier base year and appears to apply a narrower value pool, which can happen when only selected channels, markets, or recorded sales are counted. Currency conversion timing is also not stated. |

| Industry Publisher B | USD 77.92 B (2025) | Blends value with volume framing and may apply different price realization assumptions by category and region. This can shift totals depending on whether retail-level spend or producer-level revenues are being represented. |

Across the three figures, the spread is mainly explained by what gets counted as value, which year is used, and how regional prices are translated into USD. By keeping the calculation steps tied to observable trade and demand signals, and by checking assumptions with primary inputs, the resulting estimate stays easier to trace and to repeat.

Key Questions Answered in the Report

What is the current size of the whiskey market?

The whiskey market is valued at USD 162.18 billion in 2026.

How fast is the whiskey market expected to grow?

It is forecast to expand at a 4.05% CAGR, reaching USD 197.65 billion by 2031.

Which whiskey category is growing the quickest?

Irish whiskey leads with a projected 4.76% CAGR through 2031, outpacing Scotch.

Which region shows the strongest growth potential?

South America tops the outlook with a 5.62% regional CAGR to 2031, led by Brazil.

Page last updated on: