Bourbon Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

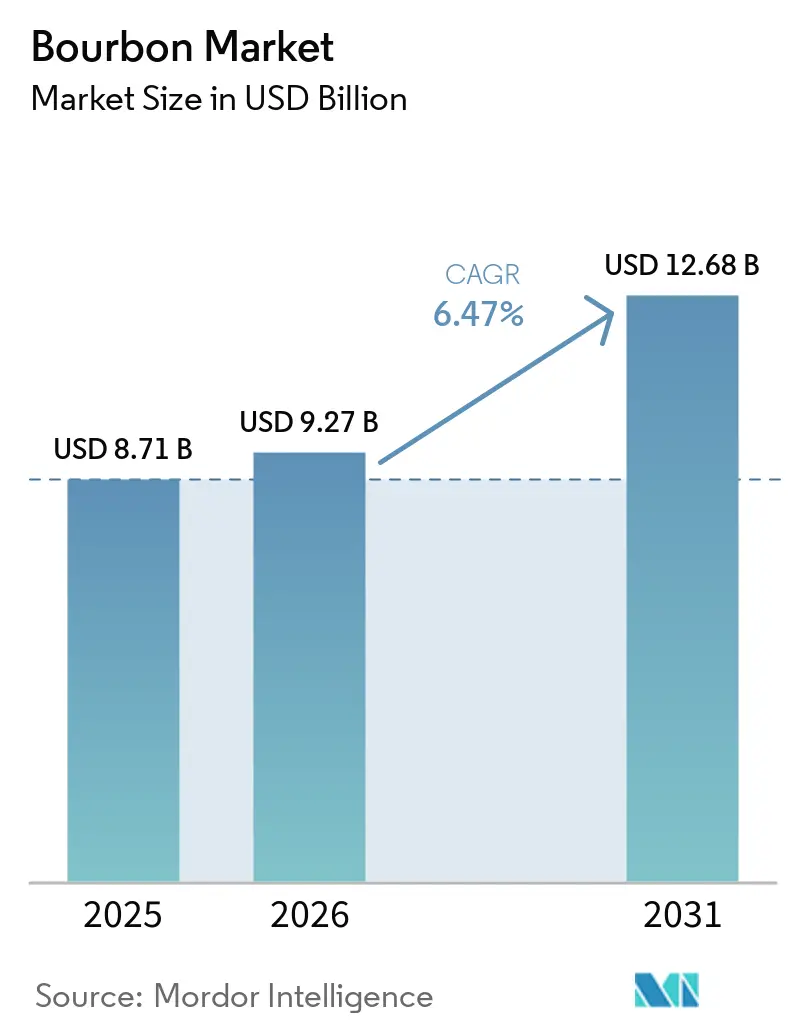

| Market Size (2026) | USD 9.27 Billion |

| Market Size (2031) | USD 12.68 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

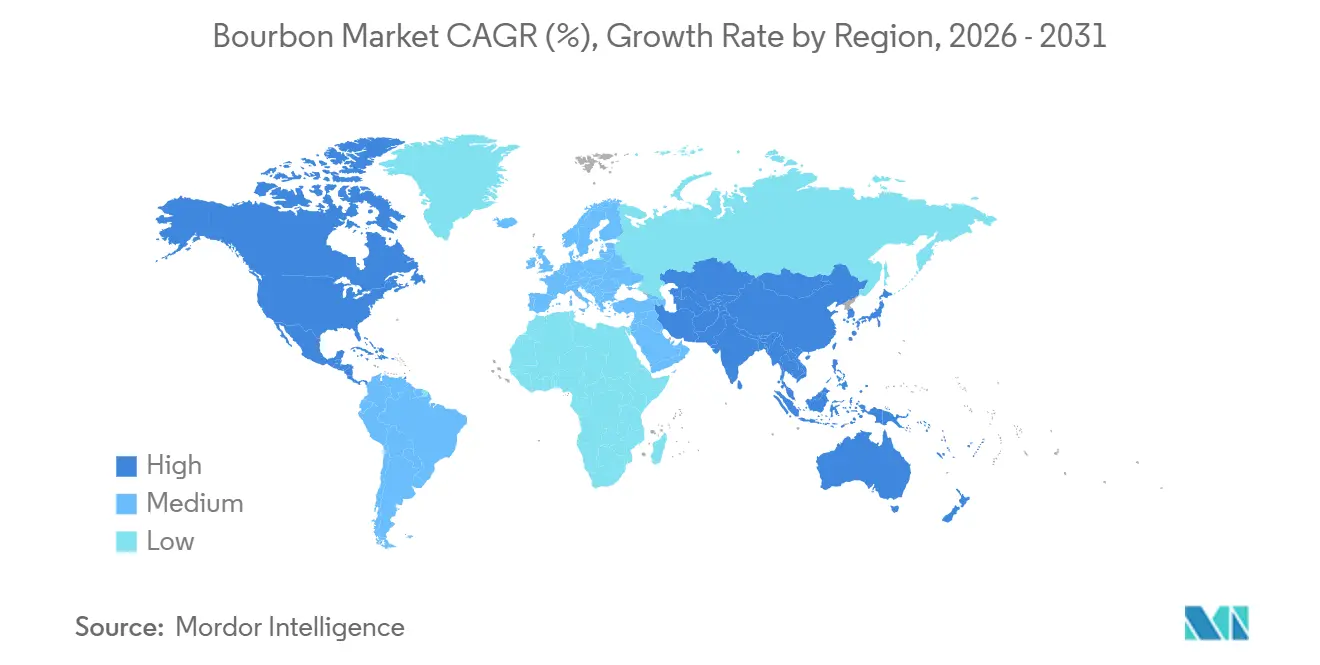

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bourbon Market Analysis by Mordor Intelligence

The bourbon market size is expected to grow from USD 8.71 billion in 2025 to USD 9.27 billion in 2026 and is forecast to reach USD 12.68 billion by 2031 at 6.5% CAGR over 2026-2031. Premiumization and an expanding international presence now drive the bourbon market's growth, replacing the short-lived spikes of the past decade. While U.S. demand has declined in volume, higher-priced offerings continue to boost revenues, keeping the bourbon market on a growth trajectory despite unstable entry-level demand. Producers now prioritize supply expansion, aged inventory management, and premium pricing alongside brand visibility to navigate a more balanced operating environment. India, Japan, South Korea, and parts of Europe provide new growth opportunities for the bourbon market as imports, cocktail culture, and gifting demand increase. However, tax pressures, health policy actions, and the rise of spirits-based ready-to-drinks (RTDs) are pushing bourbon companies to adjust their pricing, packaging, and market strategies.

Key Report Takeaways

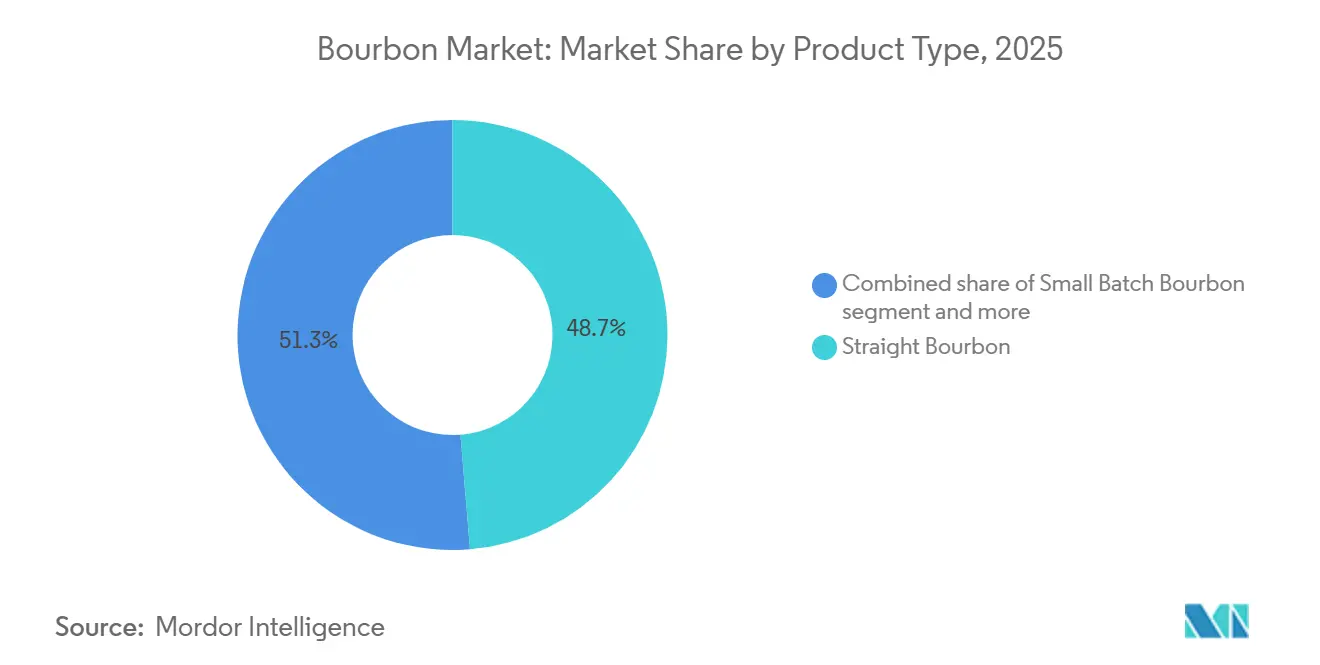

- By product type, straight bourbon held 48.71% of the bourbon market share in 2025, while flavored bourbon is forecast to grow at 7.83% CAGR through 2031.

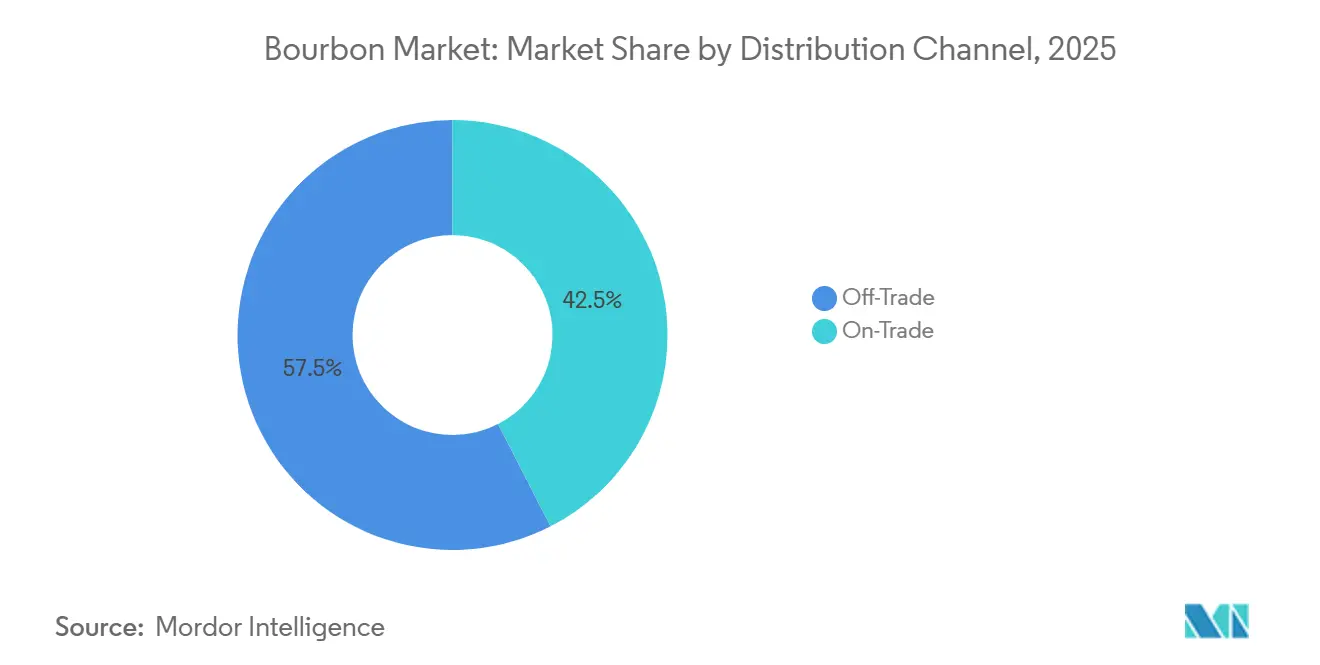

- By distribution channel, off-trade accounted for 57.59% of the bourbon market in 2025, while on-trade is projected to expand at 7.41% CAGR through 2031.

- By geography, North America represented 68.11% of the global bourbon market in 2025, while Asia-Pacific is expected to grow at 8.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bourbon Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Demand For Premium And Super-Premium Spirits | +2.2% | Global | Long term (≥ 4 years) |

| Rising Popularity Of Bourbon-Based Cocktails | +1.3% | Global, core in North America and Europe | Medium term (2-4 years) |

| Increasing Consumer Interest In American Whiskey Products | +0.9% | Global, early gains in Asia-Pacific and South America | Long term (≥ 4 years) |

| Expansion Of Craft Distilleries And Small-Batch Bourbon Offerings | +0.7% | North America | Long term (≥ 4 years) |

| Growing Disposable Incomes Supporting Premium Alcohol Purchases | +0.5% | Asia-Pacific, with spillover into the Middle East | Medium term (2-4 years) |

| Rising Demand For Aged And Limited-Edition Bourbons | +0.6% | North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing global demand for premium and super-premium spirits

The increasing consumer inclination toward premium and super-premium alcoholic beverages is a major factor supporting the growth of the bourbon market. Consumers are increasingly willing to spend more on high-quality spirits that offer superior craftsmanship, distinctive flavor profiles, and authentic heritage. This shift is particularly evident among younger legal-age drinkers and affluent consumers who prioritize quality and unique drinking experiences over volume consumption. Premium bourbons, including small-batch, single-barrel, and aged expressions, have gained popularity due to their perceived exclusivity and artisanal production methods. In addition, the growing culture of spirit appreciation, whiskey tasting events, and collector interest has further elevated demand for premium bourbon products. Distillers are responding by expanding their portfolios with limited-edition and high-end offerings to capture evolving consumer preferences.

Rising popularity of bourbon-based cocktails

The rising popularity of bourbon-based cocktails is supporting strong growth in the bourbon market. Consumers are increasingly embracing classic cocktails such as Old Fashioneds, Manhattans, and Whiskey Sours, driving greater bourbon consumption across bars and restaurants. The expansion of cocktail culture, coupled with growing interest in premium spirits, has enhanced bourbon's appeal among younger consumers. Hospitality venues are also broadening their bourbon-focused beverage offerings to meet evolving consumer preferences. For instance, the Australian Bureau of Statistics reported that 6,961 bars, pubs, and taverns were operating across Australia in 2024, providing a strong foundation for the country's expanding cocktail scene[1]Source: Australian Bureau of Statistics, “Counts of Australian Businesses, including Entries and Exits”, abs.gov.au. As cocktail consumption continues to increase globally, demand for bourbon is expected to benefit from greater on-premise consumption and consumer experimentation.

Expansion of craft distilleries and small-batch bourbon offerings

The continued expansion of craft distilleries and small-batch bourbon production is driving growth in the bourbon market. Consumers are increasingly seeking unique, locally produced, and artisanal spirits that offer distinctive flavor profiles and authentic brand stories. This trend has encouraged independent distillers to introduce innovative small-batch, single-barrel, and limited-edition bourbon expressions, broadening consumer choice and enhancing market diversity. The growing interest in craft alcoholic beverages is evident across the broader beverage industry. According to the Brewers Association, the number of U.S. craft breweries increased from 9,118 in 2021 to 9,796 in 2024, highlighting strong consumer demand for craft-produced alcoholic drinks[2]Source: Brewers Association, “Brewers Association Reports 2024 U.S. Craft Brewing Industry Figures”, brewersassociation.org. Similar preferences are benefiting craft bourbon producers, who are leveraging premium positioning and product differentiation to attract enthusiasts.

Growing disposable incomes supporting premium alcohol purchases

Rising disposable incomes are encouraging consumers to spend more on premium and super-premium alcoholic beverages, supporting growth in the bourbon market. As purchasing power increases, consumers are increasingly opting for higher-quality bourbon products that offer superior craftsmanship, flavor, and brand heritage. This trend is particularly visible in emerging and affluent markets, where premiumization is reshaping alcohol consumption patterns. Higher income levels also support demand for aged, small-batch, and limited-edition bourbon expressions. For example, according to the International Monetary Fund (IMF), GDP per capita in the United Arab Emirates increased from USD 42.84 thousand in 2021 to USD 50.22 thousand in 2024, reflecting stronger consumer spending capacity[3]Source: International Monetary Fund, “United Arab Emirates Database”, imf.org. As economic conditions improve and consumers continue trading up to premium spirits, demand for bourbon is expected to remain strong.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Alcohol Regulations And Advertising Restrictions | -0.5% | Global, with concentration in Europe and India | Short term (≤ 2 years) |

| Rising Excise Taxes On Alcoholic Beverages | -0.7% | North America and Europe | Medium term (2-4 years) |

| Increasing Health Concerns Related To Alcohol Consumption | -0.6% | Global | Long term (≥ 4 years) |

| Growing Popularity Of Low-Alcohol And Non-Alcoholic Alternatives | -0.5% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent alcohol regulations and advertising restrictions

Stringent alcohol regulations and advertising restrictions present a challenge to the growth of the bourbon market. Governments across many countries impose strict rules governing alcohol production, labeling, marketing, distribution, and sales to address public health concerns and promote responsible consumption. Restrictions on advertising across television, digital media, sponsorships, and public events can limit brand visibility and reduce opportunities for consumer engagement. In addition, varying regulatory frameworks across regions increase compliance costs and operational complexity for bourbon producers seeking international expansion. Higher excise duties, licensing requirements, and sales restrictions may also impact product affordability and market accessibility. These regulatory barriers can slow market penetration and constrain growth opportunities, particularly in emerging markets where alcohol regulations are becoming increasingly stringent.

Rising excise taxes on alcoholic beverages

Rising excise taxes on alcoholic beverages pose a challenge to the growth of the bourbon market by increasing the overall cost of products for consumers. Governments frequently adjust alcohol tax rates to generate revenue and discourage excessive alcohol consumption, leading to higher retail prices across spirits categories. For bourbon producers, increased taxation can reduce price competitiveness, particularly in markets where consumers are highly sensitive to price changes. Premium and super-premium bourbon products may be especially affected, as additional taxes further elevate already higher price points. In international markets, import duties and alcohol taxes can also impact affordability and limit market expansion opportunities. These cost pressures may influence purchasing decisions and encourage some consumers to shift toward lower-priced alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premiumization Lifts Value While Flavor Formats Broaden Reach

Straight Bourbon held a 48.71% share of the bourbon market in 2025, driven by its strong brand equity, adherence to clear legal standards, and consistent collector interest in its single-barrel and barrel-proof releases. The segment remains central to the bourbon market because producers age Straight Bourbon for at least two years and exclude additives, which solidifies its quality position and sets it apart from lower-tier formats. Small Batch and Single Barrel Bourbons strengthen the premium segment by providing consumers with a clear upgrade path from standard labels. These premium offerings also enable major producers to maintain pricing, as consumers who choose these formats focus more on character and scarcity than on price. Sazerac’s strategic positioning at Buffalo Trace post-expansion highlights the strong demand for premium labels, justifying significant long-term capacity investments.

Flavored Bourbon are projected to grow at a 7.83% CAGR through 2031, making it the fastest-growing segment in the bourbon market. Newer drinkers seeking approachable taste profiles and bars incorporating flavored variants into popular mixed drinks drive this growth. The 2025 TTB update introduced container fill standards for formats like 180mL, 300mL, and 473mL, which enhance the marketability of smaller flavored expressions and trial packs in retail and hospitality. Meanwhile, Other Bourbons, including blended and wheated styles, serve entry-level bourbon enthusiasts but face increased competition from low-alcohol alternatives and ready-to-drinks (RTDs).

By Distribution Channel: Off-Trade Anchors Volume, On-Trade Drives Discovery

Off-Trade distribution emerged as the largest channel in the bourbon market, accounting for 57.59% of total market revenue in 2025. The segment's dominance is primarily attributed to the widespread availability of bourbon through supermarkets, hypermarkets, liquor stores, specialty retailers, and e-commerce platforms. Consumers increasingly prefer purchasing bourbon through retail channels due to greater product variety, competitive pricing, and the convenience of at-home consumption. The growing trend of home entertainment, social gatherings, and premium spirit consumption outside traditional hospitality venues has further strengthened demand through off-trade outlets.

The on-trade segment is projected to register the fastest growth in the bourbon market, expanding at a CAGR of 7.41% during the forecast period through 2031. Growth in this segment is being driven by the increasing popularity of bourbon-based cocktails, premium drinking experiences, and the resurgence of social drinking occasions in bars, restaurants, hotels, and lounges. Consumers are increasingly seeking unique and experiential beverage offerings, encouraging hospitality establishments to expand their bourbon selections and cocktail menus. The rising trend of premiumization in the spirits industry is also supporting higher bourbon consumption across on-premise venues.

Geography Analysis

North America dominated the global bourbon market in 2025, accounting for 68.11% of total revenue. The region's leadership is primarily driven by the United States, which is both the birthplace and largest producer of bourbon whiskey. Strong consumer familiarity with bourbon, a well-established distilling industry, and a rich heritage associated with American whiskey continue to support high consumption levels. Premiumization trends, growing interest in craft and small-batch bourbons, and strong brand loyalty among consumers have further strengthened market demand. The presence of major bourbon producers, extensive distribution networks, and a vibrant on-trade culture also contribute to the region's substantial market share.

Asia-Pacific is projected to be the fastest-growing regional market for bourbon, registering a CAGR of 8.27% through 2031. Rapid urbanization, rising disposable incomes, and evolving consumer preferences toward premium alcoholic beverages are driving bourbon consumption across the region. Younger consumers in countries such as China, India, Japan, South Korea, and Australia are increasingly exploring international spirits and cocktail culture, creating favorable conditions for bourbon brands. The expansion of premium bars, restaurants, and hospitality establishments has also enhanced product visibility and accessibility.

Europe's bourbon market grows steadily, driven by strong consumer demand for premium spirits, a thriving cocktail culture, and imported American whiskey. The UK, Germany, France, and Spain report rising interest in premium and craft bourbon. In South America, urbanization, a growing middle class, and increasing demand for premium alcoholic beverages drive growth, particularly in Brazil, Argentina, and Chile. The Middle East & Africa region, though smaller, is gaining momentum due to expanding tourism, hospitality, and luxury dining sectors. Exposure to global beverage trends and premium spirit brands creates new opportunities in these regions.

Competitive Landscape

The bourbon market is moderately fragmented, with a mix of large multinational spirits companies, established American whiskey producers, and a growing number of craft distilleries competing for market share. While a handful of leading brands benefit from strong consumer recognition, extensive distribution networks, and long-standing heritage, numerous regional and independent distillers continue to gain traction through differentiated product offerings. Competition is driven by factors such as brand reputation, product quality, aging techniques, flavor profiles, pricing strategies, and portfolio diversity. The increasing consumer preference for premium and super-premium bourbons has encouraged companies to expand their offerings across multiple price points and consumer segments.

Product innovation and premiumization have become key competitive strategies within the bourbon industry. Companies are increasingly introducing limited-edition releases, single-barrel expressions, cask-finished variants, and small-batch bourbons to appeal to enthusiasts seeking unique drinking experiences. Premium packaging, storytelling around heritage and craftsmanship, and collaborations with hospitality and retail partners are also being used to enhance brand differentiation. In addition, producers are expanding their presence in international markets where demand for American whiskey is rising.

The competitive landscape is also being shaped by ongoing investments in production capacity, distribution expansion, and sustainability initiatives. Larger players continue to leverage their financial resources and global reach to strengthen supply chains and improve market penetration, while smaller distillers focus on authenticity, local sourcing, and craft production methods to attract niche consumer groups. Strategic partnerships, acquisitions, and portfolio expansions remain common approaches for enhancing market presence and accessing new consumer demographics. The rise of e-commerce and digital marketing channels has further enabled brands of varying sizes to engage directly with consumers and broaden their reach.

Bourbon Industry Leaders

Brown-Forman Corporation

Sazerac Company, Inc.

Diageo plc

Pernod Ricard SA

Bacardi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bardstown Bourbon Company expanded its finishing series portfolio through the launch of Cascadia Garryana Oak Barrel Finish Bourbon, a limited-edition expression matured using rare Garryana oak barrels sourced from the Pacific Northwest. The product was designed to deliver a distinctive flavor profile and further strengthen the company's premium bourbon offerings.

- March 2026: Maker's Mark unveiled the 2026 Wood Finishing Series: The Stewards Release, a limited-edition bourbon developed to recognize the contributions of the distillery's production and operations teams. The release featured a distinctive wood-finishing approach designed to deliver enhanced complexity and showcase the brand's innovation in barrel maturation.

- March 2026: Angel's Envy expanded its premium whiskey portfolio with the release of the Cask Strength Collection, featuring its annual Cask Strength Bourbon alongside the company's first age-stated 10-Year Cask Strength Rye. The launch targeted collectors and premium whiskey enthusiasts seeking high-proof, limited-production expressions.

- February 2026: Buzzard's Roost Whiskey broadened its bourbon range with the introduction of Four Grain Double Oak Bourbon, a new expression utilizing a proprietary double-oak maturation process. The release highlighted the company's continued emphasis on barrel-finishing innovation and premium craftsmanship.

Global Bourbon Market Report Scope

Bourbon is a type of American whiskey produced primarily from a grain mixture containing at least 51% corn and aged in new charred oak barrels. The bourbon market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented by straight bourbon, small batch bourbon, single barrel bourbon, flavored product types, and other bourbons. Based on the distribution channel, the market is segmented into on-trade and off-trade channels. Based on distribution channel, the market is segmented into foodservice and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East, and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million) and volume (litres).

| Straight Bourbon |

| Small Batch Bourbon |

| Single Barrel Bourbon |

| Flavored Product Types |

| Other Bourbons |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Supermarkets/Hypermarkets | |

| Other Off Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Straight Bourbon | |

| Small Batch Bourbon | ||

| Single Barrel Bourbon | ||

| Flavored Product Types | ||

| Other Bourbons | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Supermarkets/Hypermarkets | ||

| Other Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the bourbon market in 2026?

The bourbon market is valued at USD 9.27 billion in 2026 and is projected to reach USD 12.68 billion by 2031 at a 6.47% CAGR.

Which product type leads bourbon sales today?

Straight Bourbon leads with 48.71% share in 2025 because of strong brand heritage, legal quality standards, and collector demand.

Which bourbon category is growing the fastest?

Flavored Bourbon is the fastest-growing product type, with a projected 7.83% CAGR through 2031, supported by newer drinkers and cocktail use.

Why is Asia-Pacific important for future bourbon demand?

Asia-Pacific is forecast to grow at 8.27% CAGR through 2031, with India gaining momentum after a tariff cut on American spirits and rising beverage alcohol sales.

What is the biggest challenge facing bourbon producers?

Rising taxes, moderation trends, and slower domestic U.S. demand are the main pressures, especially for value-tier brands with weaker pricing power.

Page last updated on: