Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

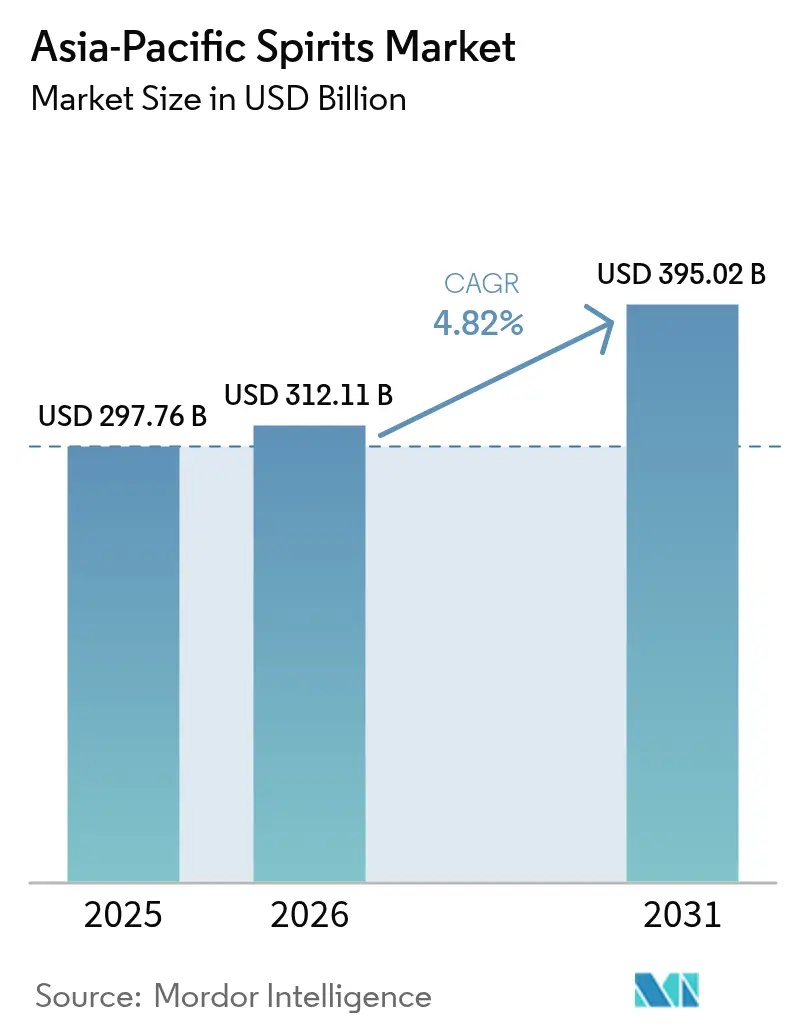

| Base Year Market Size (2025) | USD 297.76 Billion |

| Market Size (2026) | USD 312.11 Billion |

| Market Size (2031) | USD 395.02 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Spirits Market Analysis by Mordor Intelligence

Asia-Pacific spirits market size in 2026 is estimated at USD 312.11 billion, growing from 2025 value of USD 297.76 billion with 2031 projections showing USD 395.02 billion, growing at 4.82% CAGR over 2026-2031. Rising disposable incomes, a shift towards premiumization, and an increasing preference for global spirit styles over traditional local options are driving this growth. Consumers are actively seeking novelty and authenticity, which has allowed whisky to maintain its category leadership while agave-based spirits and craft variations gain significant traction. The growing popularity of craft spirits reflects a broader consumer trend toward unique and high-quality products, with many buyers willing to pay a premium for these offerings. Digital commerce continues to expand, enabling brands to reach a wider audience and offer personalized experiences. On-trade sales are recovering strongly as consumers return to bars and restaurants, while the rebound in tourism is further boosting value growth by increasing demand for premium and exotic spirits. Companies are investing heavily in regional distilling capacities, reflecting their confidence in sustained long-term demand and their commitment to meeting evolving consumer preferences. The competitive landscape remains dynamic, as heritage producers, multinational corporations, and agile craft brands actively target segmented audiences by leveraging niche taste profiles and distinctive storytelling.

Key Report Takeaways

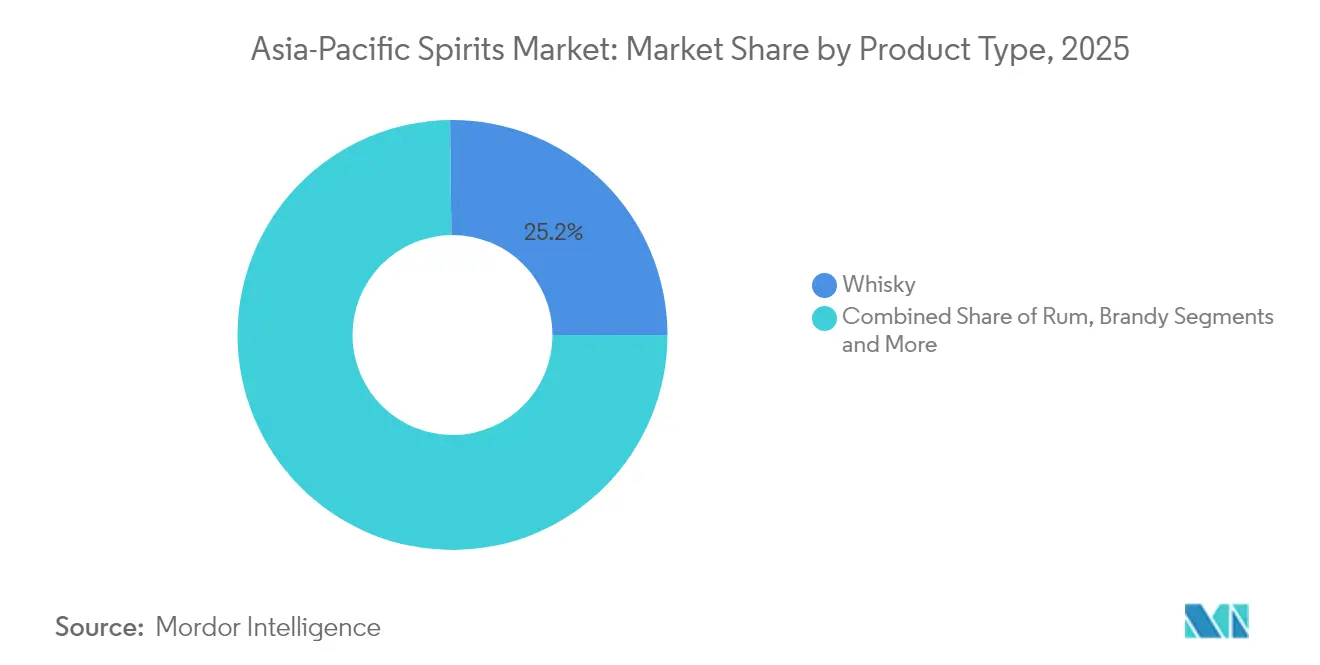

- By product type, whisky held 25.18% of the Asia-Pacific spirits market share in 2025, whereas tequila and mezcal are forecast to expand at a 5.12% CAGR through 2031.

- By end user, the male segment accounted for 79.02% share of the Asia-Pacific spirits market size in 2025, while female consumption is advancing at a 5.48% CAGR toward 2031.

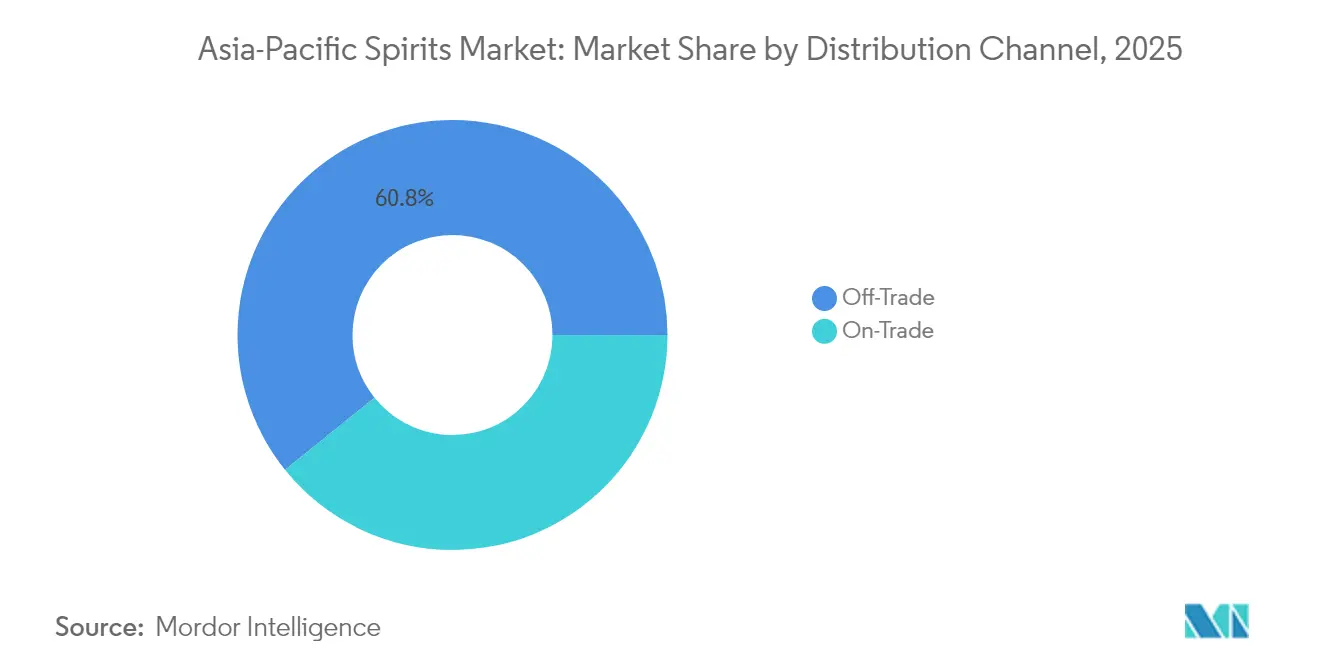

- By distribution channel, off-trade captured 60.78% revenue in 2025; on-trade is projected to rise at a 5.88% CAGR to 2031.

- By geography, China accounted for 41.02% market share in 2025, Philippines is projected to grow at a CAGR of 5.79% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumers inclination towards craft spirits | +0.8% | Regional, with strong adoption in Japan, Australia, South Korea | Medium term (2-4 years) |

| Growing tourism and hospitality impact positive growth | +0.6% | Thailand, Philippines, Malaysia, with spillover to Vietnam, Indonesia | Short term (≤ 2 years) |

| Strategic marketing by major brands boosting awareness and demand | +0.5% | China, India, South Korea, with expansion to emerging markets | Medium term (2-4 years) |

| Surge in demand for premium alcoholic beverages | +0.9% | China, Japan, South Korea, Australia, with growth in urban centers | Long term (≥ 4 years) |

| Growing cocktail culture fueling the market growth | +0.7% | Urban centers across China, Japan, South Korea, Thailand, Philippines | Medium term (2-4 years) |

| Expanding culture of social gatherings and clubbing | +0.6% | Metropolitan areas in China, Japan, South Korea, Thailand, Malaysia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumers inclination towards craft spirits

Consumers’ growing inclination towards craft spirits is emerging as a significant market driver for the Asia-Pacific spirits market. This trend is fueled by increasing consumer demand for unique, artisanal, and locally produced alcoholic beverages that emphasize authenticity, craftsmanship, and distinctive flavors. Millennials and Gen Z consumers, in particular, show a strong preference for small-batch, handcrafted spirits such as whiskey, gin, and rum, often seeking novel drinking experiences through cocktail culture and mixology. The rising urban nightlife scene, along with a growing number of craft distilleries in countries like China, Japan, India, and Vietnam, supports this trend by expanding consumer access to diverse craft products. The growth is also supported by investments in innovative production processes, incorporation of local botanicals, and strategic marketing efforts focused on promoting the artisanal value and story behind craft brands, further elevating consumer interest and driving market growth.

Surge in demand for premium alcoholic beverages

The Asia-Pacific spirits market is witnessing a notable surge in demand for premium alcoholic beverages, driven by rising disposable incomes and shifting consumer preferences toward quality and exclusivity. For instance, the National Bureau of Statistics of China reported that in 2024, the average annual per capita disposable income of Chinese households rose to approximately 41,300 yuan, up from 39,218 yuan in 2023 [1]Source: National Bureau of Statistics of China, "Average annual per capita disposable income of households in China from 1990 to 2024", www.stats.gov.cn, highlighting stronger consumer purchasing power and a willingness to trade up to premium products. Middle-class and affluent consumers across China, India, Japan, and Southeast Asia increasingly view premium and super-premium spirits as symbols of lifestyle and social status, while younger demographics especially millennials and Gen Z are fueling the trend through cocktail culture and an appetite for authenticity and craftsmanship. Upscale hotels, fine-dining restaurants, and bars in cities such as Tokyo, Shanghai, and Singapore are reinforcing this premiumization by offering curated portfolios of high-value whiskies, vodkas, gins, and craft spirits. In response, leading players like Diageo, Pernod Ricard, and Beam Suntory are expanding their premium ranges and intensifying marketing investments, solidifying premiumization as a major growth engine for the Asia-Pacific spirits market.

Growing tourism and hospitality impact positive growth

The rapid expansion of tourism and hospitality is a key driver of growth in the Asia-Pacific spirits market, as the influx of international visitors directly boosts alcohol consumption in hotels, resorts, restaurants, and nightlife venues. In 2024, the Asia-Pacific region welcomed an impressive 316 million international tourists, with Northeast Asia including Macao leading at 146 million arrivals, followed by Southeast Asia with 121 million, and South Asia and Oceania attracting 33 million and 15 million visitors, respectively [2]Source: Macao News, “Asia welcomed 316 million travellers in 2024, still below 2019 numbers”, www.macaonews.org. These rising numbers have increased demand for spirits, as travelers commonly associate leisure with premium dining, vibrant nightlife, and authentic cultural experiences. Popular hotspots such as Tokyo, Singapore, Phuket, and Bali have become centers where both global brands and indigenous spirits like sake, soju, baijiu, and arrack are prominently featured in upscale bars, themed restaurants, rooftop lounges, and resort events. Alongside this, the growth of luxury hotels, cruise tourism, and curated events is accelerating the premiumization trend, with international and local spirit brands benefiting significantly. To further fuel this growth, governments across the region are making strategic investments; for example, India allocated INR 2,541.06 crore in its 2025–26 Union Budget to enhance tourism infrastructure, aiming to attract more domestic and international visitors [3]Source: Ministry of Tourism, “Tourism as a Key Driver for Employment and Growth Budget 2025-26 Focuses on Infrastructure, Medical Tourism, and Heritage Conservation”, www.pib.gov.in. This coordinated push by both private and public sectors amplifies tourism’s role as a powerful engine for the Asia-Pacific spirits market expansion.

Strategic marketing by major brands boosting awareness and demand

Strategic marketing initiatives by major spirits brands are playing a pivotal role in boosting awareness and demand across the Asia-Pacific spirits market. Leading players are adopting digital-first campaigns, influencer collaborations, and targeted advertising to connect with younger demographics, while also investing in experiential marketing such as cocktail festivals, pop-up bars, and cultural events to strengthen brand engagement. Sponsorship of sports tournaments, music festivals, and lifestyle events further enhances visibility and consumer recall, aligning brands with evolving urban entertainment trends. Importantly, companies such as Diageo, Pernod Ricard, and Suntory significantly increased their marketing expenditures in Asia-Pacific, channeling investments into digital channels, localized brand campaigns, and premiumization-focused promotions tailored to markets like China, India, Japan, and Southeast Asia. These sustained marketing efforts, coupled with the growth of e-commerce and direct-to-consumer channels, are propelling competitive differentiation, driving premium spirit adoption, and supporting long-term market expansion across the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concern over excessive consumption | -0.4% | Regional, with particular focus in Japan, Australia, South Korea | Long term (≥ 4 years) |

| High governmental taxes and excise duties on spirits | -0.6% | Philippines, Thailand, Malaysia, India, with varying impact levels | Short term (≤ 2 years) |

| Shift toward low- or no-alcohol beverages among younger consumers | -0.3% | Japan, Australia, South Korea, urban China | Medium term (2-4 years) |

| Anti-alcohol campaigns hindering the growth | -0.2% | China, India, with government-led initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High governmental taxes and excise duties on spirits

Excise duty structures across the Asia-Pacific region impose significant cost pressures on the spirits market, impacting pricing and accessibility, especially for price-sensitive consumers. For example, the Philippines set an excise duty of PHP 66 per liter in 2024, with planned increases expected to further raise costs for consumers and limit affordable market access. Thailand’s taxation is notably complex, combining excise duties with import tariffs that create substantial barriers for international brands while simultaneously protecting strong domestic players like Thai Beverage PLC. In Malaysia, the excise framework heavily affects premium imports, where duties can represent 30-40% of retail prices, making it difficult for international brands to penetrate the market effectively. These fiscal policies aim to balance revenue generation and public health goals but inadvertently create market distortions favoring local production over imports. Additionally, the increasing complexity and variation of tax regulations across countries raise compliance costs for international companies, necessitating specialized legal and tax advisory services to navigate the diverse regulatory landscape in Asia-Pacific. This layered excise duty environment therefore poses challenges to market expansion, pricing strategies, and competitive dynamics across the region.

Health concern over excessive consumption

Health concerns over excessive alcohol consumption represent a significant restraint on the Asia-Pacific spirits market. Increasing awareness among consumers and governments about the risks associated with heavy drinking, including chronic diseases, accidents, and social problems, has led to stricter regulations and public health campaigns aimed at reducing alcohol consumption. Various countries in the region have introduced measures such as mandatory health warnings on packaging, restrictions on advertising—especially targeting young adults—and limits on drinking hours and sale points. Industry-wide initiatives, like the Asia Pacific International Spirits and Wines Alliance (APISWA) Moderation Week campaign, promote responsible drinking to curb harmful consumption patterns. Despite these efforts supporting safer consumption, heightened public scrutiny and regulatory controls constrain market growth by limiting promotional activities and creating barriers for expanding alcohol availability. This growing health consciousness combined with tightening policies creates a challenging environment, particularly affecting price-sensitive and socially conscious consumer segments across Asia-Pacific.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whisky Dominance Amid Tequila Emergence

Whisky holds the largest market share in the Asia-Pacific spirits market, commanding a substantial 25.18% share in 2025. This dominant position is significantly supported by Scotland's strong export performance, which continues to reinforce Scotch whisky's global prestige and preference. Additionally, Japan has experienced a domestic renaissance in whisky production, drawing both local and international attention. The resurgence of Japanese whisky has added considerable momentum to the overall market, boosting consumer interest and sales. The cultural significance of whisky in the region, coupled with rising disposable incomes and evolving consumer preferences, has further cemented its leadership. Moreover, the trend towards premiumization and artisanal products has enabled whisky brands to capture affluent segments, driving growth and profitability.

On the other hand, tequila and mezcal stand out as the fastest-growing segment in the Asia-Pacific spirits market, with a notable CAGR of 5.12% projected through 2031. These agave-based spirits are gaining rapid popularity due to increasing consumer curiosity for innovative and exotic flavors. Driven by younger consumers and millennials who seek unique drinking experiences, tequila and mezcal are expanding their footprint beyond traditional markets. The rise of cocktail culture and mixology has also spurred the demand for these spirits in trendy bars and clubs. Importantly, the diversification in product offerings and improved distribution channels across the region support this accelerating growth. As awareness and appreciation for these authentic Mexican spirits grow, tequila and mezcal are positioned to continue their robust expansion well into the next decade.

By End User: Male Dominance with Female Acceleration

Male consumers hold the largest share of the Asia-Pacific spirits market, representing 79.02% of total consumption in 2025. This commanding lead reflects long-established cultural and social norms in the region, where men traditionally have been the primary consumers of alcoholic beverages. The dominance of male consumers is also fueled by targeted marketing efforts and product offerings tailored to masculine preferences. Spirits such as whiskey, rum, and brandy often align with male-centric social activities and gatherings, reinforcing this trend. Furthermore, this large market share emphasizes the sustained influence of male drinkers on the overall market dynamics and brand strategies across Asia-Pacific. Despite emerging changes, men currently shape the majority of consumption patterns, deeply embedded in the region’s liquor culture.

Conversely, female consumption of spirits in Asia-Pacific is the fastest-growing segment, accelerating at a CAGR of 5.48% through 2031. This rapid growth is driven by shifting demographics, changing social norms, and evolving lifestyle preferences among women. Women are increasingly exploring spirits categories like flavored vodkas, botanical gins, and low-alcohol beverages that cater to their tastes and wellness concerns. The rise of female consumers in on-trade and off-trade channels signals broader acceptance and inclusion in the traditionally male-dominated market. Marketing strategies are adapting by focusing on sophisticated packaging, lower alcohol content options, and diverse flavor profiles attractive to women. This surge in female consumption points towards fundamental demographic shifts that will significantly reshape the Asia-Pacific spirits market landscape over the coming years.

By Distribution Channel: Off-Trade Leadership with On-Trade Recovery

Off-trade channels command a dominant market share of 60.78% in the Asia-Pacific spirits market in 2025. This large share reflects significant behavioral shifts induced by the pandemic, where consumers adapted to purchasing alcoholic beverages primarily for consumption at home. The growth of e-commerce platforms and modernization of retail infrastructures further contributed to the expansion of off-trade channels. Convenience, wider product availability, and competitive pricing attract a diverse consumer base, reinforcing off-trade’s preeminence in the region. With the increased penetration of online shopping and home delivery services, off-trade is poised to maintain a leading role in consumer purchasing habits. The persistence of hybrid consumption models and lifestyle changes fuel sustained demand through off-trade channels as manufacturers and retailers double down on digital engagement and personalized offerings.

Conversely, the on-trade segment, comprising bars, restaurants, hotels, and clubs, is experiencing a robust recovery and has emerged as the fastest-growing distribution channel with a projected CAGR of 5.88% through 2031. This resurgence is fueled by the reopening and revival of hospitality sectors as pandemic restrictions ease and tourism rebounds across key markets. Consumers are returning to social venues for premium and experiential drinking occasions, driving increased spend in on-trade environments. The growth is supported by rising disposable incomes, evolving consumer preferences for mixology and craft spirits, and intensified marketing efforts targeting on-premise sales. On-trade operators are enhancing customer experiences through innovative beverage offerings, themed events, and strategic partnerships with premium spirit brands. As social consumption regains prominence, the on-trade channel is expected to accelerate market expansion and contribute significantly to revenue growth in the coming years.

Geography Analysis

In 2025, China commands a dominant 41.02% share of the Asia-Pacific spirits market, highlighting its massive scale and ongoing transformation. Traditional baijiu consumption has been declining for the eighth consecutive year, signaling a shift in consumer preferences. This decline is attributed to changing lifestyles, health-conscious choices, and the growing influence of younger generations who are exploring alternatives to traditional spirits. At the same time, international spirits are gaining significant traction, driven by increasing exposure to global brands, rising disposable incomes, and the growing appeal of premium and imported products. Additionally, the expansion of e-commerce platforms and digital marketing strategies has made international spirits more accessible to Chinese consumers, further accelerating this shift. The growing trend of cocktail culture, particularly in urban areas, is also contributing to the rising demand for international spirits, as consumers seek diverse and innovative drinking experiences.

The Philippines stands out as the market with the most rapid growth, boasting a 5.79% CAGR projected through 2031, buoyed by strong economic fundamentals. In the Philippines, spirits have overtaken beer and wine in popularity, mirroring cultural trends that prioritize higher-proof beverages for social gatherings and celebrations. Additionally, the rising disposable income and the growing influence of Western drinking habits are further fueling the demand for spirits in the country, particularly among urban consumers. The increasing penetration of international brands and the expansion of distribution networks are also contributing to the growth of the spirits market in the Philippines, making it a lucrative opportunity for both domestic and global players. Furthermore, the government's support for the tourism sector, coupled with the growing number of bars, restaurants, and nightlife establishments, is creating a favorable environment for the spirits market to thrive, particularly in metropolitan areas.

Japan, South Korea, and Australia showcase developed markets with unique growth trajectories. Meanwhile, Indonesia, Vietnam, and Malaysia present burgeoning opportunities, as urbanization and economic strides cultivate a middle class eager for premium alcohol experiences. In Indonesia, the rising urban population and increasing disposable incomes are driving demand for spirits, particularly among young professionals. Vietnam is witnessing a surge in premium spirits consumption, supported by the growing influence of Western culture and the expansion of modern retail channels. Malaysia, on the other hand, is experiencing a shift in consumer preferences toward premium and imported spirits, driven by the aspirational lifestyles of its middle-class population. Across these emerging markets, the growing presence of international brands, coupled with targeted marketing campaigns and the development of on-trade channels, is further fueling the demand for spirits.

Competitive Landscape

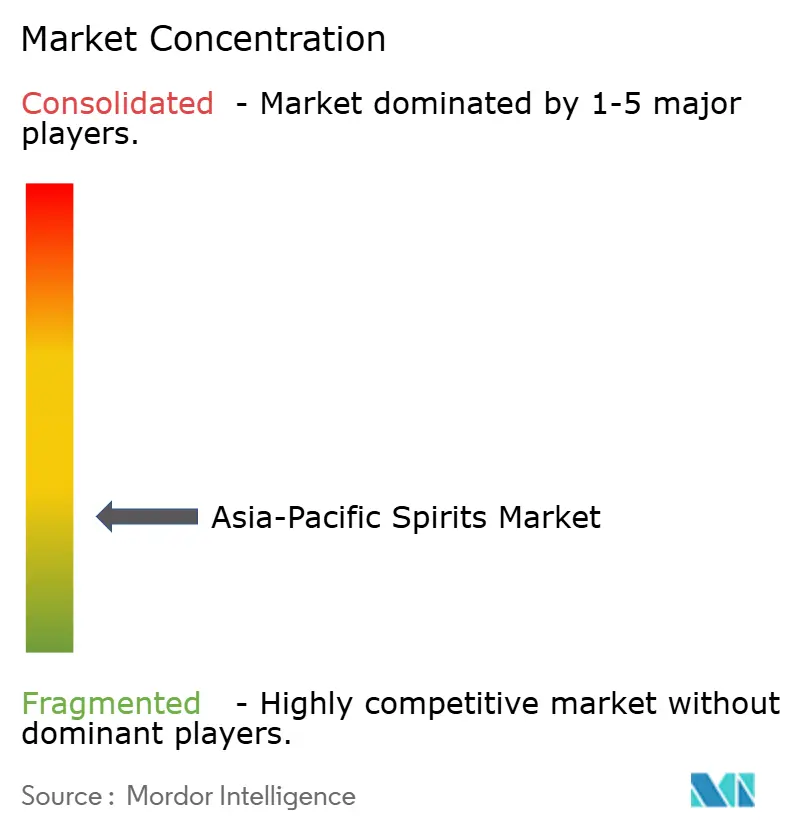

The Asia-Pacific spirits market exhibits a moderate level of concentration, characterized by a concentration score of 3. This degree of concentration implies a balanced competitive environment where both global multinational corporations and emerging craft distilleries have opportunities to thrive. Leading multinational companies leverage their broad distribution networks, extensive brand portfolios, and significant marketing budgets to maintain a strong presence across various price tiers and regions. These established players benefit from economies of scale, brand recognition, and global supply chains that help them deliver products consistently to meet diverse consumer demands. Their ability to innovate with product variations, premium offerings, and marketing campaigns positions them as dominant forces within the market.

Simultaneously, the moderate concentration level fosters an inclusive environment for smaller, agile craft distillers to compete effectively. These emerging players capitalize on niche markets driven by consumer interest in artisanal, small-batch, and locally sourced spirits. Craft producers focus on innovation around flavor profiles, unique ingredients, and sustainable production methods to differentiate their brands. They often appeal to younger, urban consumers seeking authenticity and experiential drinking, thereby carving out meaningful market share despite competition from larger companies. This dynamic fuels diversity in product offerings and enriches consumer choices, spurring growth in premium and craft segments. The moderate concentration score thus reflects a marketplace where size alone does not guarantee success, but creativity and connection to local markets play a vital role.

Multinational conglomerates maintain dominance in developed economies such as Japan, South Korea, and Australia, where premiumization and luxury consumption are key trends. Meanwhile, craft distillers are particularly active in markets with burgeoning middle classes and evolving preferences, such as China, India, and Southeast Asia. The accessibility of digital platforms and e-commerce channels enables both large and small producers to reach consumers more efficiently, further intensifying competition. Overall, the moderate concentration fosters a vibrant market landscape where a mix of legacy brands and innovative newcomers influence industry evolution, making Asia-Pacific one of the most dynamic spirits markets globally.

Asia-Pacific Spirits Industry Leaders

-

Diageo PLC

-

Kweichow Moutai Co., Ltd.

-

Wuliangye Yibin Co., Ltd.

-

Bacardi Limited

-

Pernod Ricard SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thai Beverage Public Company Limited has unveiled PRAKAAN, marking Thailand's debut in the premium single malt whisky arena. PRAKAAN introduces three unique variants: Select Cask, Peated Malt, and Double Cask. This launch comes in response to Thailand's evolving consumer preferences, notably the surging appetite for premium spirits.

- April 2025: Himmaleh Spirits, the force behind brands such as Kumaon&I and Bandarful, has unveiled Neoli Himalayan Rum. This rum, hailing from the Kumaon region, is introduced as the world's first white pure single Himalayan Agricole-style rum, setting a fresh benchmark for terroir-driven Indian spirits.

- November 2024: Diageo, the world's top whisky producer and a premium beverage alcohol leader, has launched the YunTuo Single Malt Whisky Distillery in Eryuan County, Yunnan Province, China. Marking its inaugural whisky production site in China, the YunTuo distillery comes with a hefty USD 120 million investment, set to unfold over nine years.

- June 2024: Diageo, in collaboration with celebrated Japanese chef Kei Kobayashi, has unveiled a limited-edition Johnnie Walker Blue Label Elusive Umami. This launch not only highlights the surging appetite for premium experiences but also underscores the blend of diverse cultural craftsmanship.

Asia-Pacific Spirits Market Report Scope

Spirit is an alcoholic drink produced by distillation and includes brandy, gin and genever, liqueurs, rum, specialty spirits, tequila and mezcal, vodka, and whiskey.

The Asia-Pacific spirits market is segmented by product type (whiskey, vodka, rum, brandy, and other product types), distribution channel (specialty/liquor stores, online retail stores, on-trade, and other sales channels), and geography (India, China, Japan, Australia, and Rest of Asia-Pacific). The report offers market size and values in (USD million) during the forecast period for the above segments.

By Product Type

| Whiskey |

| Vodka |

| Rum |

| Brandy |

| Gin |

| Tequilla and Mezcel |

| Other Spirit Types |

By End User

| Male |

| Female |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off-Trade Channels |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Australia |

| New Zealand |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Philippines |

| Rest of Asia-Pacific |

| By Product Type | Whiskey | |

| Vodka | ||

| Rum | ||

| Brandy | ||

| Gin | ||

| Tequilla and Mezcel | ||

| Other Spirit Types | ||

| By End User | Male | |

| Female | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off-Trade Channels | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific spirits market by 2031?

It is expected to reach USD 395.02 billion, growing at a 4.82% CAGR.

Which product category currently leads regional sales?

Whisky holds the largest share, accounting for 25.18% of value in 2025.

Which country is forecast to grow fastest within the region?

The Philippines shows the highest forecast growth at a 5.79% CAGR through 2031.

How are premium trends influencing consumer behavior?

Rising affluence and social-status signaling push consumers toward higher-quality labels, lifting average spend per serve across channels.

Page last updated on: