Market Overview

| Study Period | 2021 - 2031 |

|---|---|

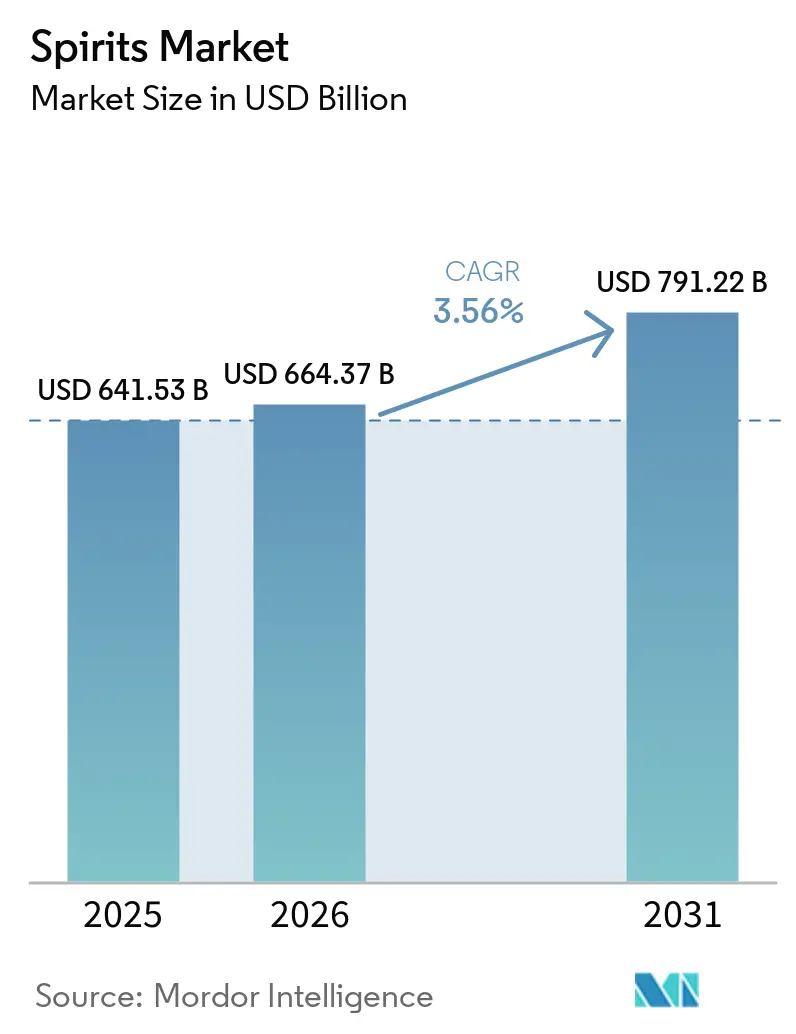

| Market Size (2026) | USD 664.37 Billion |

| Market Size (2031) | USD 791.22 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

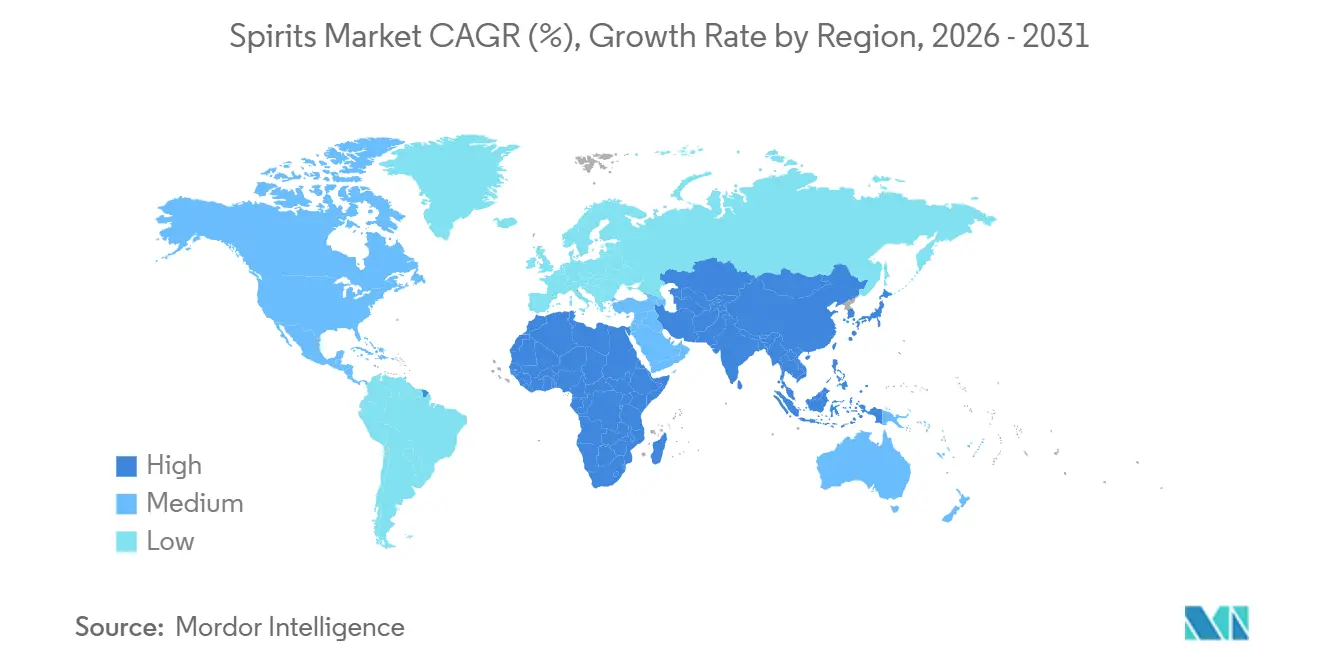

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

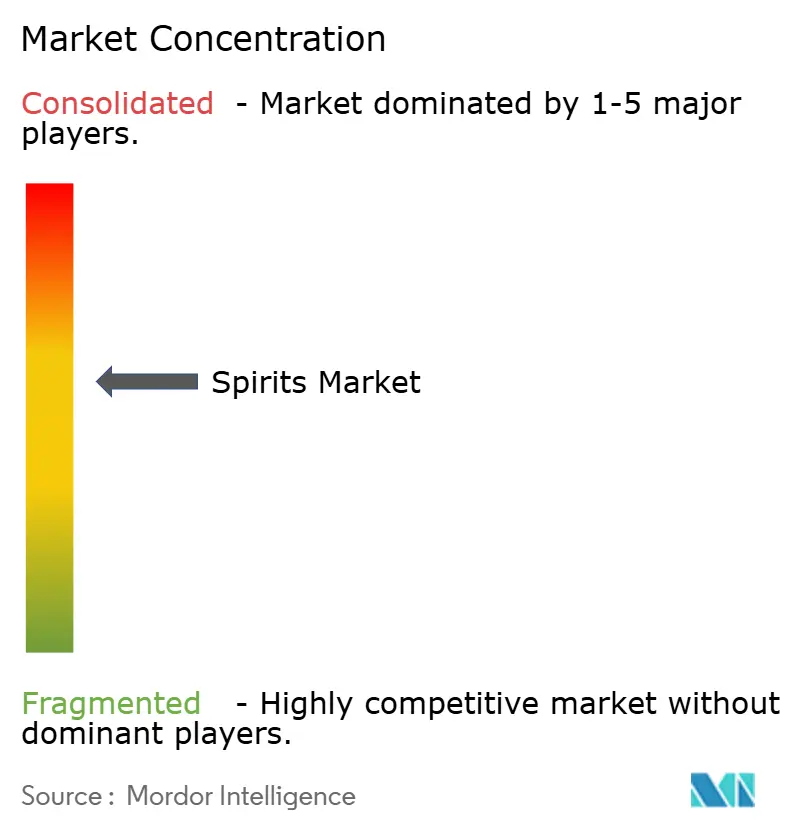

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spirits Market Analysis by Mordor Intelligence

The spirits market was valued at USD 641.53 billion in 2025 and estimated to grow from USD 664.37 billion in 2026 to reach USD 791.22 billion by 2031, at a CAGR of 3.56% during the forecast period (2026-2031). This growth is being driven by rising premiumization, a wave of innovative product launches, and the global revival of on-premise consumption in bars, restaurants, and lounges. Consumers are increasingly gravitating toward premium whiskies, artisanal gins, flavored vodkas, and low-sugar ready-to-drink (RTD) beverages, reflecting a shift toward more refined and health-conscious choices. Simultaneously, brands are strengthening their digital ecosystems by deploying AI-driven recommendations, partnering with social media influencers, and hosting immersive virtual tasting experiences to deepen engagement. Companies are also making significant investments in omnichannel distribution, forging stronger retail partnerships, expanding direct-to-consumer (DTC) e-commerce platforms, and implementing smart logistics to enhance accessibility, reduce delivery times, and personalize the buying journey. Sustainability has become a central strategic focus, with increasing consumer demand for eco-friendly packaging pushing brands to rethink product design, from lightweight glass bottles to biodegradable labels.

Key Report Takeaways

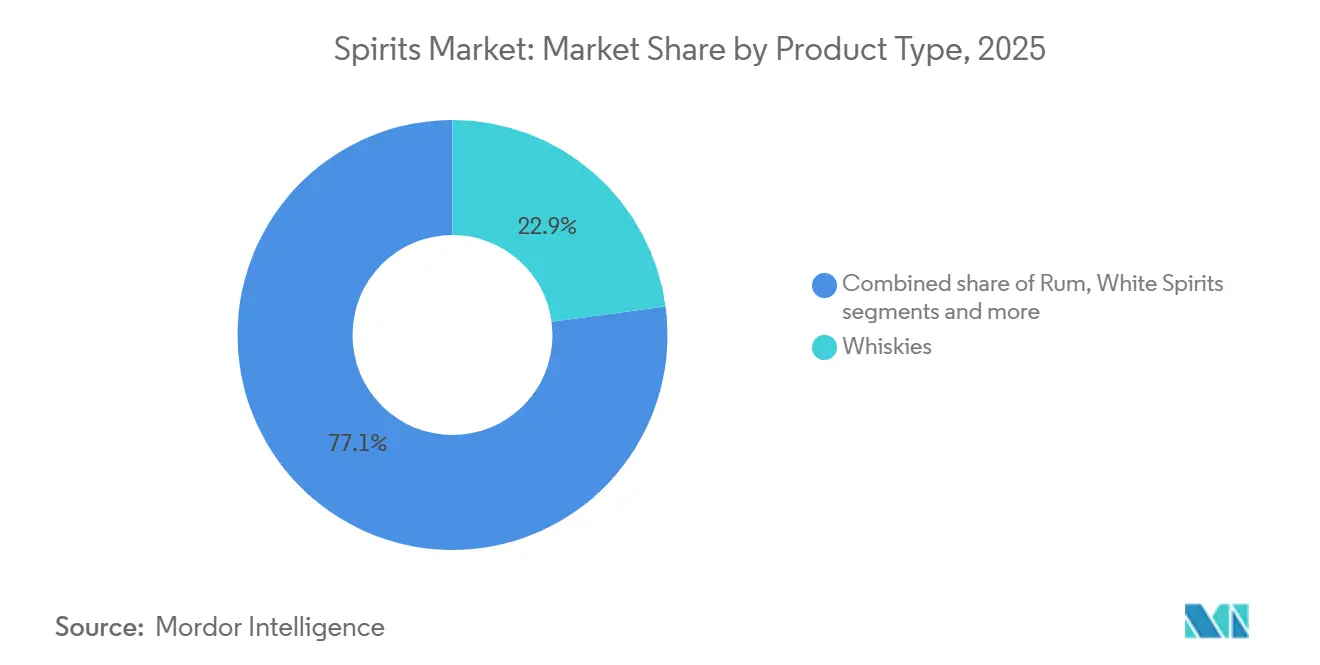

- By product type, whiskies led with 22.89% of the spirits market share in 2025, while white spirits are forecast to expand at a 4.07% CAGR through 2031.

- By distribution channel, the off-trade segment controlled 57.71% of the spirits market size in 2025; on-trade venues are projected to grow at a 3.96% CAGR as experiential outlets regain footfall.

- By end user, men accounted for 76.22% of the spirits market share in 2025, whereas the female segment is advancing at a 4.42% CAGR to 2031.

- By geography, Asia-Pacific accounted for 45.31% of the spirits market in 2025, and the Middle East and Africa is set to post the fastest 5.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for craft and small-batch spirits | +0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Expansion of tourism and hospitality sector contributing to strong market growth | +0.6% | Global, with concentration in Middle East, Asia-Pacific, Caribbean | Short term (≤ 2 years) |

| Rising demand for high-end and premium alcoholic beverages | +0.9% | Global, led by North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Greater product differentiation based on raw ingredients and alcohol strength | +0.5% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Expanding cocktail culture acting as a major driver of market demand | +0.7% | Global, strongest in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Ongoing innovation in flavors and packaging enhancing market growth | +0.6% | Global, with rapid uptake in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for craft and small-batch spirits

Craft spirits are increasingly capturing consumer interest, driving strong momentum in the global spirits market. This segment is flourishing as demand grows for unique, high-quality beverages with authentic character. Artisanal distilleries, from FEW Spirits in the United States to Sipsmith in the United Kingdom, are gaining popularity with their distinctive flavor profiles across gin, whiskey, vodka, and other categories. By highlighting locally sourced botanicals, heirloom grains, and sustainable production practices, these producers are enhancing the appeal and perceived value of their craft offerings. Highlighting this trend, the American Craft Spirits Association reported a notable 11.5% uptick in active craft distillers in the United States bringing the total to 3,069 in 2023[1]Source: American Craft Spirits Association, "Craft Spirits Data Project Report-2024,"americancraftspirits.org. Developed markets, especially the United States, Germany, and the United Kingdom are witnessing this craft fervor, bolstered by rising disposable incomes that encourage a dive into niche, high-quality spirits. Rising consumer demand for transparency in production methods and authentic brand stories is further reinforcing the appeal of craft spirits. Collaborations between craft distilleries and local businesses are also driving innovation and broadening market exposure. As more consumers shift toward artisanal offerings, both retail shelves and bar menus are experiencing a significant shift, increasingly favoring craft labels over mass-produced alternatives.

Expansion of the tourism and hospitality sector contributing to strong market growth

A burgeoning tourism and hospitality sector is propelling the spirits market. The World Tourism Organization (UNWTO) reported a significant milestone in 2024, with global international tourist arrivals hitting 1.4 billion, underscoring a vigorous rebound in global travel[2]World Tourism Organization, "International tourism recovers pre-pandemic levels in 2024,"unwto.org. This resurgence has fueled rising demand for premium and locally crafted spirits, as tourists increasingly seek authentic cultural experiences often expressed through tasting regional specialties such as tequila in Mexico, Scotch in Scotland, or sake in Japan. To capitalize on this trend, governments around the world are investing strategically in tourism development. For example, the Indian government allocated INR 1,900 crore in its 2024–25 Union Budget to strengthen tourism infrastructure and attract both domestic and international visitors. Meanwhile, the United States Travel Association announced that domestic travel expenditures reached USD 1.3 trillion in 2024, indicating a robust recovery in the hospitality sector[3]Source: U.S. Travel Association, “National Economic Impact of Travel 2024,”impact.ustravel.org. Such momentum is translating into heightened spirits consumption across hotels, restaurants, resorts, and bars, especially in sought-after tourist locales. With travel and experiential spending on the upswing, the hospitality industry's appetite for a diverse range of premium spirits is poised to drive the market's expansion. Additionally, the rise of culinary tourism and the growing trend of pairing spirits with local cuisines are further contributing to this demand. The increasing popularity of destination weddings and events is also creating new opportunities for the spirits market.

Rising demand for high-end and premium alcoholic beverages

The demand for premium alcoholic beverages is increasing rapidly, becoming a key catalyst for growth in the spirits market. This momentum is driven by consumers’ heightened interest in high-quality, craft, and artisanal spirits that offer superior taste and authenticity. The growing appeal of premium whiskey such as single malt Scotch and small-batch bourbon illustrates this shift, alongside rising demand for botanical craft gins and uniquely filtered premium vodkas. Consumers are increasingly willing to pay more for distinctive flavors, limited-edition releases, and brands with strong heritage narratives. The expansion of cocktail culture, supported by mixology-focused bars, at-home cocktail kits, and social media influence, further boosts interest in sophisticated drinking experiences. Premium brands like Johnnie Walker Blue Label, Hendrick’s Gin, and Grey Goose Vodka are successfully capitalizing on this trend. Additionally, the continued rise of craft distilleries and growing preference for premiumization across alcoholic beverages further reinforces this market shift.

Greater product differentiation based on raw ingredients and alcohol strength

In an increasingly competitive spirits market, brands are strengthening their positioning through strategic product differentiation, especially by innovating with raw materials and adjusting alcohol content. The distinctive identity of each spirit, whether whiskey made from grains, rum from sugarcane or molasses, vodka from potatoes or corn, or gin infused with botanicals, originates from its foundational ingredients. These ingredient-driven variations influence flavor, texture, and consumer appeal, often aligning with regional tastes, such as the popularity of fruit-based brandies in parts of Europe or rice-based shochu in Japan. Additionally, differences in alcohol content help brands cater to diverse consumer segments. High-ABV (Alcohol by Volume) products like Ardbeg Supernova Scotch whisky, with an ABV exceeding 60%, attract experienced enthusiasts, while lower-ABV innovations like Tanqueray Flor de Sevilla gin, at around 30%, appeal to casual drinkers and increasingly health-conscious consumers. In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) mandates stringent labeling and classification based on ABV, ensuring transparency and empowering consumers to make informed choices[4]TTB Alcohol and Tobacco Tax and Trade Bureau, "TTB Proposes 'Alcohol Facts' and Major Allergen Labeling for Alcohol Beverages", ttb.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight government controls and compliance requirements | -0.7% | Global, particularly stringent in Europe, North America, Middle East | Long term (≥ 4 years) |

| Increasing health concerns related to heavy alcohol intake | -0.5% | Global, most pronounced in Europe, North America, Australia | Medium term (2-4 years) |

| Growing consumer move toward low- and zero-alcohol options | -0.4% | Europe, North America, urban Asia-Pacific | Short term (≤ 2 years) |

| Awareness and advocacy campaigns discouraging alcohol consumption and slowing market growth | -0.3% | Global, led by government and non-governmental organization (NGO) initiatives in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight government controls and compliance requirements

Stringent government regulations continue to pose substantial constraints on the spirits market, as many countries enforce high excise duties and import taxes that raise production costs and drive up retail prices. Nations like Norway and Sweden, which impose some of the world’s highest alcohol taxes, often see spirits priced at more than twice the levels found in neighboring European markets. At the same time, strict advertising and marketing rules in key regions such as the European Union and the United States limit brand visibility and promotional flexibility. For instance, the United States Alcoholic Beverage Labeling Act requires health warnings on all packaging, while EU policies prohibit alcohol advertising during children’s programming and restrict digital promotions that could appeal to minors. Regulatory complexity is even greater in markets like India, where state-specific rules including full prohibitions in Bihar and Gujarat create significant barriers for producers, and in Saudi Arabia, where alcohol is completely banned. Adding to these challenges is a rising global focus on health and wellness, intensifying scrutiny around alcohol consumption and further constraining market growth.

Increasing health concerns related to heavy alcohol intake

Health concerns surrounding excessive alcohol consumption have become a major limiting factor for the global spirits market. Heavy drinking is strongly associated with serious health risks, including liver cirrhosis, cardiovascular diseases, certain cancers, and mental health disorders. The World Health Organization (WHO) has reported a significant rise in alcohol-related liver cirrhosis cases over the past decade, highlighting the growing public health challenge and the need for stronger preventive measures. In response, governments and health agencies are intensifying regulatory actions to reduce alcohol misuse, introducing higher excise taxes, mandating graphic health warnings on labels, and tightening advertising and sponsorship restrictions especially those that could influence younger audiences. For example, Australia’s “DrinkWise” initiative promotes responsible consumption through national awareness campaigns, while France’s Loi Évin law imposes strict limits on alcohol promotion across media and sports. Although these policies aim to safeguard public health, they also weaken demand for conventional spirits, ultimately restraining overall market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whiskies Anchor Share, White Spirits Accelerate

Whiskies held the largest share of the spirits market in 2025, accounting for 22.89% of total revenue. This strong position reflects the category’s deep-rooted popularity among affluent consumers and collectors who value authenticity, craftsmanship, and aged expressions. Premium and super-premium whiskies continue to attract substantial interest due to their perceived exclusivity and investment potential. The segment also benefits from a thriving culture of tastings, limited-edition releases, and brand-led storytelling, all of which enhance consumer engagement. Continued innovation in cask finishes and regional expressions further broadens appeal across diverse demographics. As a result, whiskies remain a cornerstone of the global spirits market and a reliable driver of overall category value.

White spirits are projected to grow at a CAGR of 4.07% through 2031, making them the fastest-expanding product category in the spirits market. This momentum is underpinned by rising interest in versatile and mixable spirits such as vodka, gin, and white rum, which align well with the global cocktail culture. Younger consumers, in particular, are driving experimentation with new flavor profiles, botanical blends, and low-sugar formulations. The category is further boosted by the popularity of ready-to-drink (RTD) beverages, where white spirits often serve as the base. Increasing innovation in premium and craft offerings is also elevating the segment’s perception and fueling demand.

By End User: Men Retain Majority, Women Drive Growth

Men accounted for 76.22% of total spirits consumption in 2025, firmly establishing them as the dominant consumer demographic in the market. This leading share is rooted in long-standing cultural norms and consumption patterns that have traditionally positioned spirits as a male-oriented category. Higher per-capita intake among men continues to reinforce their influence on overall market demand. The segment also benefits from strong engagement with premium and aged spirits, categories where male consumers historically exhibit strong purchasing power and brand loyalty. Marketing campaigns and product launches have often been tailored toward male preferences, further solidifying their market share.

Women represent the fastest-growing consumer group in the spirits market, with consumption projected to rise at a CAGR of 4.42% through 2031. This rapid growth is reshaping traditional market dynamics and prompting brands to rethink product innovation and positioning. Increasing female interest in flavored spirits, low-sugar cocktails, and premium RTD beverages is contributing to the segment’s momentum. Social and cultural shifts such as greater acceptance of women’s participation in nightlife, dining, and social occasions are also expanding consumption opportunities. Brands are responding by introducing more diverse flavor profiles, elegant packaging, and marketing campaigns specifically tailored to female preferences.

By Distribution Channel: Retail Transformation and Hybrid Models

Off-trade channels dominated the spirits market in 2025, securing 57.71% of total market share. This strong performance can be largely attributed to the pandemic-driven shift toward at-home consumption, where consumers increasingly stocked up through retail stores, supermarkets, and online platforms. Convenience, competitive pricing, and broad product availability further reinforced the appeal of off-trade purchases. Many consumers also developed new habits, such as home mixology and virtual social gatherings, which sustained off-trade demand even post-pandemic. The growth of e-commerce and rapid delivery services provided an additional boost by making spirits more accessible than ever before.

On-trade venues are experiencing a strong resurgence and are projected to grow at a CAGR of 3.96% through 2031, making them the fastest-growing channel in the spirits market. This rebound is driven by the renewed popularity of experiential dining, nightlife, and social entertainment as consumers return to restaurants, bars, and lounges. The revival of tourism and hospitality is also contributing to higher on-trade consumption levels across major global cities. Enhanced cocktail programs, craft spirit menus, and premium drink experiences are further elevating engagement within this channel. Many spirits brands are leveraging on-trade environments for product launches, signature serves, and brand-building activations, adding to the segment’s momentum.

Geography Analysis

In 2025, the Asia-Pacific region commands a significant 45.31% share of the global spirits market. This leadership is supported by the region’s large population base, rising disposable incomes, and evolving drinking habits. In mature markets like Japan and South Korea, local spirits such as shochu and soju remain central to social traditions and daily consumption. Australia blends long-standing drinking culture with a rapidly expanding craft distillery movement, appealing especially to younger consumers seeking authenticity and locally crafted products. China continues to stand out with strong demand for both domestic offerings like Baijiu and international brands, driven by an emphasis on premiumization and gift-giving culture.

The Middle East and Africa (MEA) region is set for rapid expansion, with a projected CAGR of 5.09% between 2026 and 2031, though it begins from a smaller market base. South Africa leads the region, supported by major players like Diageo South Africa promoting high-end brands such as Johnnie Walker, Tanqueray, and Smirnoff. Growth is further fueled by the country’s expanding middle class and their increasing preference for premium spirits. In the United Arab Emirates, a rising expatriate population and gradually shifting cultural attitudes are driving demand for luxury alcohol. Saudi Arabia is also seeing early signs of potential, with recent easing of alcohol rules for foreign visitors indicating new opportunities.

North America and Europe remain mature markets characterized by a strong inclination toward premium and craft spirits. The United States continues to lead in North America, with stable demand for whiskey, vodka, and tequila. This trend is reinforced by ongoing premiumization and the growth of craft distilling, with brands like Tito’s Handmade Vodka and Buffalo Trace gaining prominence. In Europe, markets remain anchored by heritage-rich producers in Scotland, Ireland, and France, where globally recognized spirits such as Scotch whisky, Irish whiskey, and French cognac maintain strong international appeal supported by geographic indications.

Competitive Landscape

The market reflects a moderate level of consolidation, with leading companies utilizing broad brand portfolios spanning multiple categories and price tiers to sustain their competitive advantage. These key players are actively advancing premiumization by elevating product quality and exclusivity to appeal to higher-value consumer segments. A clear example is Pernod Ricard’s expansion of its Prestige Collection, featuring brands such as Royal Salute and Martell Cordon Bleu, aimed directly at the ultra-premium market. Expanding into high-growth regions across Asia and Africa remains a central strategic focus. Countries such as India, Nigeria, and Vietnam, supported by rising incomes and a growing middle class, offer significant potential for premium spirits.

Diageo’s introduction of Godawan, an artisanal Indian single malt, exemplifies efforts to align with local flavor preferences while leveraging India’s rapid premium whisky growth. Digital transformation is also reshaping competition, as companies adopt technology to improve engagement, streamline processes, and accelerate innovation. Diageo’s ‘Breakthrough Innovation’ team has led AI-enabled projects such as ‘What’s Your Whisky,’ which delivers personalized recommendations, and ‘Elli,’ an AI concierge for Seedlip, enhancing tailored experiences. These tools also generate valuable data to support product development and targeted marketing.

Sustainability has become a vital pillar of competitive strategy as environmentally conscious consumers increasingly demand responsible practices. Major distilleries are deploying initiatives such as carbon capture technology, heat recovery systems, and renewable energy solutions to reduce their ecological footprint. Chivas Brothers, part of Pernod Ricard, has committed to achieving carbon-neutral distillation across all its facilities by 2026. Prioritizing sustainability not only advances environmental goals but also strengthens brand trust and long-term market value.

Spirits Industry Leaders

-

Diageo plc

-

Brown–Forman Corporation

-

Suntory Holdings Limited

-

Bacardi Limited

-

Pernod Ricard SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Diageo opened a new manufacturing facility in Alabama, enhancing its supply network in the Southern United States. The Diageo Montgomery facility represents an investment of USD 415 million and incorporates advanced technology and sustainability features, such as electric boilers and automated guided vehicles.

- March 2026: Roku Japanese Gin has launched its Noryo Tea Edition, a limited-time summer expression inspired by the Japanese cultural tradition of Noryo. The Noryo Tea Edition highlights two of Roku’s six signature Japanese botanicals, Sencha tea and Gyokuro green tea, elevating them to provide a fresh, tea-forward sensory experience.

- March 2026: Mount Gay launched its latest product, "Bajan Spiced," marking its entry into the growing spiced spirit's segment. Developed by Master Blender Trudiann Branker, this 35% ABV rum-based spirit is meticulously crafted in Barbados. The product combines unaged pot and column-distilled rums with a distinctive infusion of natural Barbadian ingredients, including red grapefruit, local ginger, orange peel, and cinnamon.

- February 2026: Hendrick’s Gin has launched "Another Hendrick’s.“The new spirit maintains the house's signature rose and cucumber foundation while introducing a distinct flavor profile featuring orange blossom and cacao beans.

Global Spirits Market Report Scope

Spirits are one of the major segments of alcoholic beverages which are manufactured by distillation of fermented fruits, vegetables, or grains.

The global spirits market is segmented by product type, end user, distribution channel, and geography. Based on product type, the market is segmented into brandy and cognac, liqueur, rum, tequilla and mezcel, whiskies, white spirits and other spirit types. Based on end-user, the market is segmented into men and women. Based on distribution channels, the market is segmented into On-trade and Off-trade. Off-trade is further sub-segmented into speciality/liquor stores and other off-trade channels. The report provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD).

By Product Type

| Brandy and Cognac |

| Liqueur |

| Rum |

| Tequilla and Mezcel |

| Whiskies |

| White Spirits |

| Other Spirit Types |

By End User

| Men |

| Women |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off Trade Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Brandy and Cognac | |

| Liqueur | ||

| Rum | ||

| Tequilla and Mezcel | ||

| Whiskies | ||

| White Spirits | ||

| Other Spirit Types | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global spirits market in 2026?

The spirits market size stands at USD 664.37 billion in 2026 and is projected to reach USD 791.22 billion by 2031.

Which product segment grows fastest through 2031?

White spirits, including vodka, gin, and unaged cane spirits, are forecast to post a 4.07% CAGR, the highest among product categories.

What share do off-trade channels hold today?

Off-trade venues such as liquor stores and e-commerce accounted for 57.71% of 2025 sales, although on-trade is recovering.

Which region contributes the most revenue?

Asia-Pacific leads with 45.31% of global spirits turnover, driven by China’s baijiu and India’s whisky consumption.

How are health concerns shaping product innovation?

Brands are launching lower-ABV and zero-alcohol lines, with examples like Gordon’s 0.0% claiming 3% share in the U.K. gin market within half a year.

Page last updated on: