Agave Spirits Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

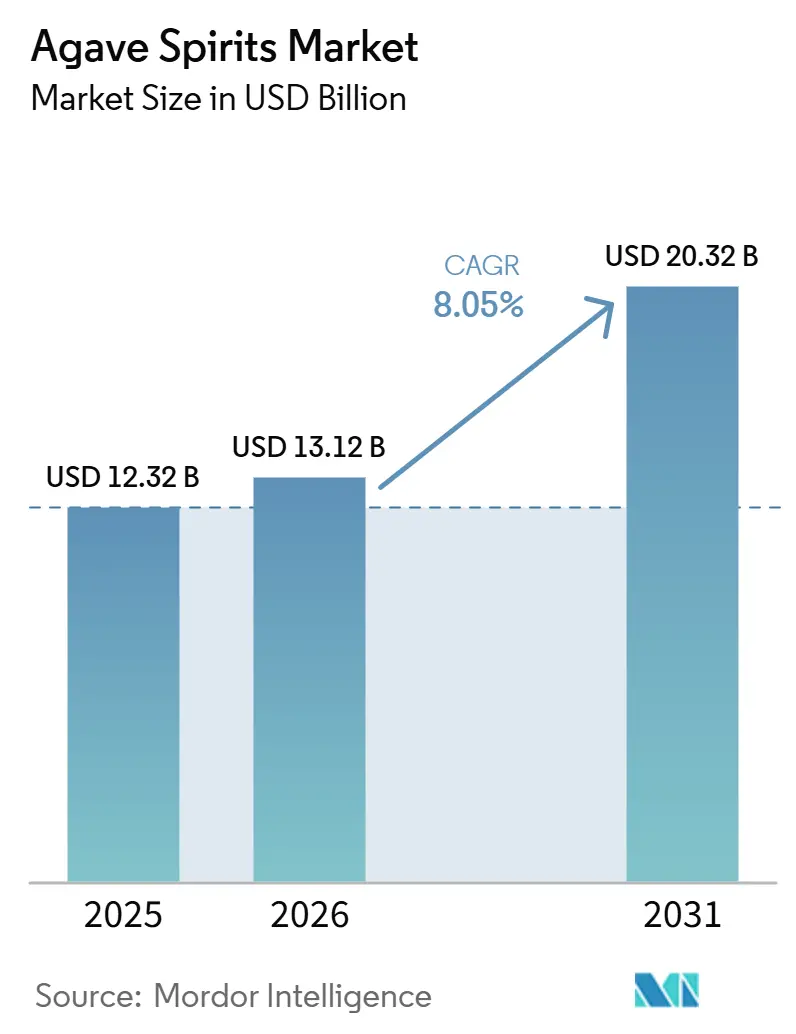

| Market Size (2026) | USD 13.12 Billion |

| Market Size (2031) | USD 20.32 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agave Spirits Market Analysis by Mordor Intelligence

The agave spirits market size is expected to grow from USD 12.32 billion in 2025 to USD 13.12 billion in 2026 and is forecast to reach USD 20.32 billion by 2031 at 8.05% CAGR over 2026-2031. The agave spirits market is moving from a narrow growth base to a wider one, as mature demand in North America is being balanced by stronger adoption in newer markets and channels. Premium buying behavior remains central to the agave spirits market, and that is pushing producers to focus more on pricing discipline, brand quality, and clearer product positioning rather than only chasing volume. The agave spirits market is also being shaped by stronger consumer attention to authenticity, which is raising the importance of production transparency, regional identity, and 100% agave credentials in both retail and hospitality channels. Product development is widening the addressable consumer base of the agave spirits market through non-alcoholic formats, premium line extensions, and occasion-based launches that reach both traditional drinkers and sober-curious buyers. At the same time, the agave spirits market faces cost and supply pressure from agave price swings, which makes planning more difficult for both large producers and smaller artisanal operators.

Key Report Takeaways

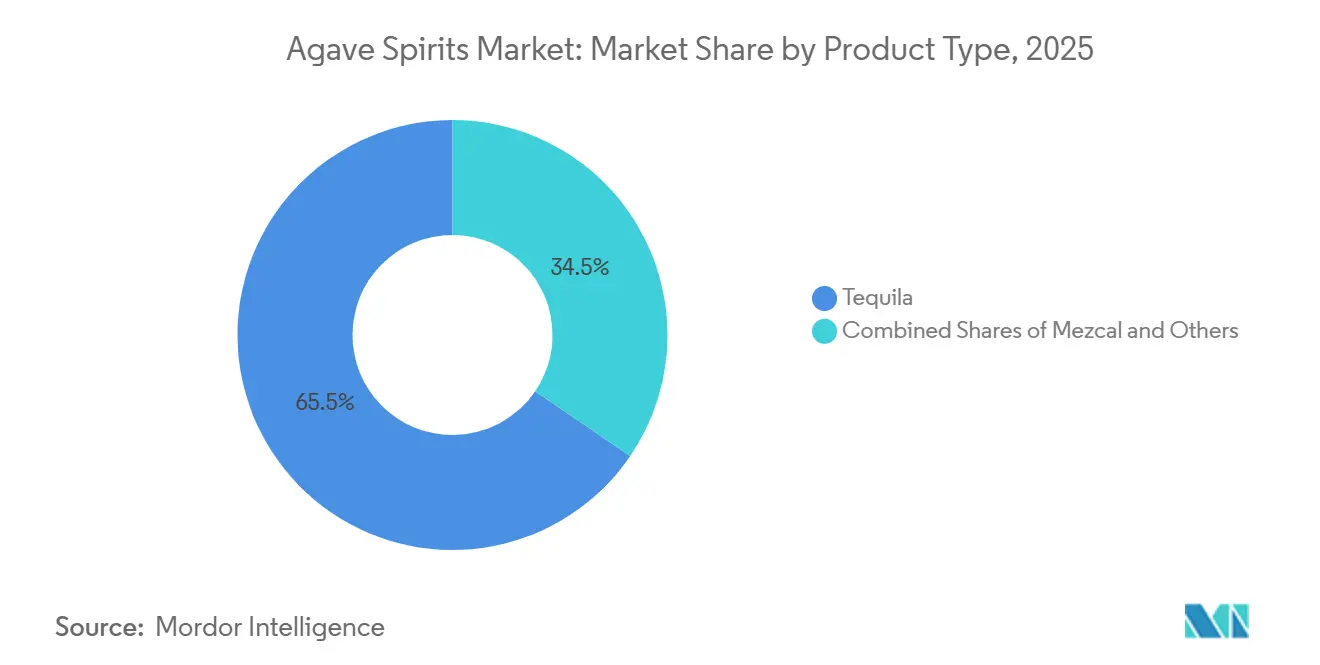

- By product type, tequila held 65.48% share in 2025, while mezcal is forecast to expand at 9.11% CAGR through 2031.

- By price point, standard expressions held 86.79% of the agave spirits market share in 2025, while the premium segment is projected to grow at 9.56% CAGR through 2031.

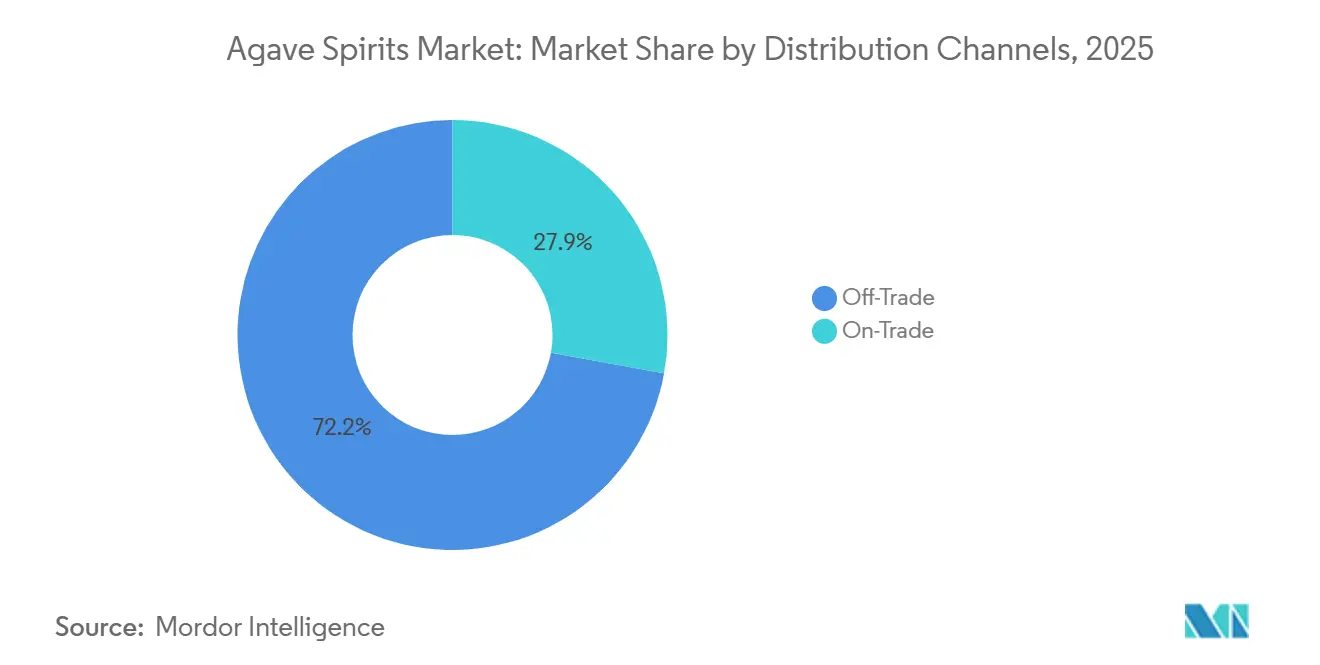

- By sales channels, off-trade accounted for 72.15% of the agave spirits market size in 2025, while on-trade is expected to grow at 9.85% CAGR through 2031.

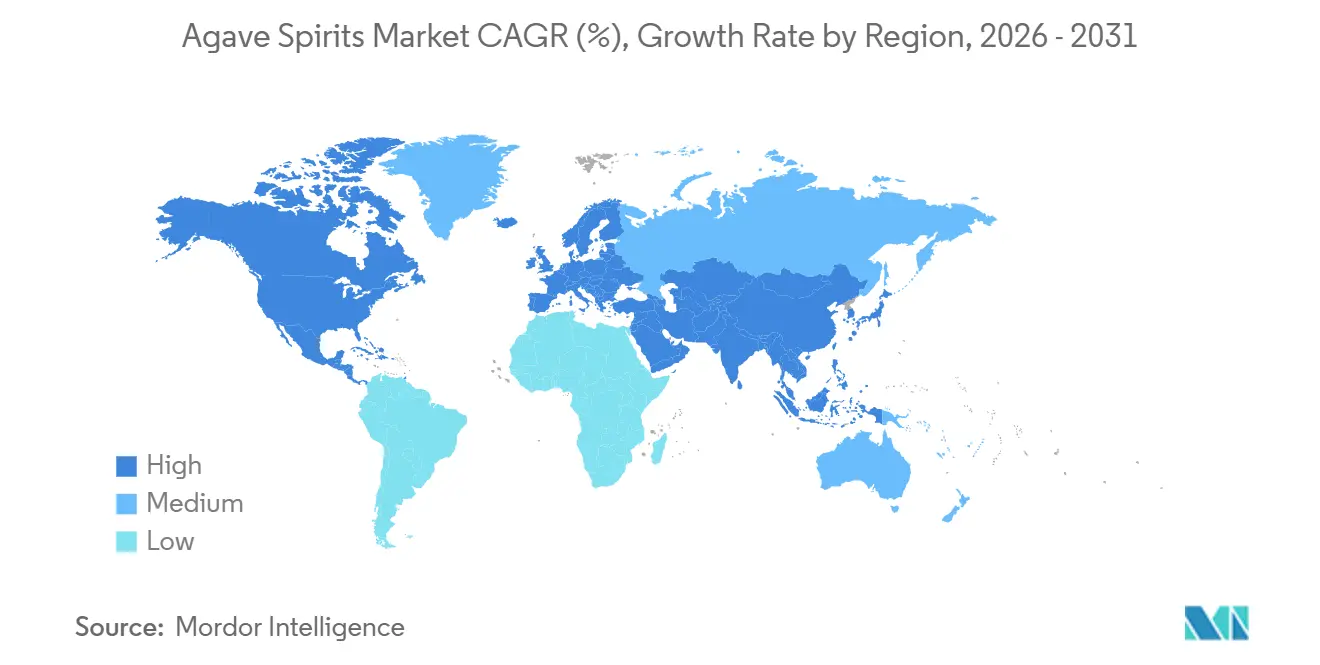

- By geography, North America led with 33.46% share in 2025, while Asia-Pacific is forecast to advance at 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agave Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Premium And Ultra-Premium Spirits | +2.3% | Global, with strongest intensity in North America and Europe | Long term (≥ 4 years) |

| Increasing Consumer Preference For Authentic And Craft Spirits | +1.9% | North America & Europe, spill-over to APAC urban centres | Medium term (2–4 years) |

| Cocktail Menu Penetration In Bars And Restaurants | +1.3% | Global, with accelerating gains in Europe and APAC | Medium term (2–4 years) |

| Product Innovation Across Agave Spirit Categories | +0.8% | Global, led by North America and UK | Short term (≤ 2 years) |

| Growth of E-Commerce Alcohol Sales | +0.7% | North America, EU, APAC core | Short term (≤ 2 years) |

| Rising Demand for Different Flavored Alcohol Products | +0.5% | North America, APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand For Premium And Ultra-Premium Spirits

The agave spirits market is being pushed higher by a steady move from volume-led buying to value-led buying in key consumer markets. In the United States, super-premium and high-end agave segments grew by 1,268% and 1,400% in volume between 2003 and 2025, and super-premium expressions alone reached nearly 7.5 million 9-liter cases by 2025[1]Source: Distilled Spirits Council of the United States, “2025 Tequila/Mezcal in the U.S. Fact Sheet,” Distilled Spirits Council of the United States, distilledspirits.org. The same source shows that tequila and mezcal remained the only spirits category with positive revenue growth in 2024, which indicates that consumers still accepted premium pricing even when broader spirits demand softened. That shift matters because it changes how the agave spirits market rewards brand owners, with better returns now going to producers that defend quality signals and pricing rather than only pushing case volumes. It also gives distributors a stronger reason to support labels with clearer premium credentials, since those labels can hold shelf value better across different retail and hospitality settings. Over time, this keeps the agave spirits market tied more closely to value creation than to simple shipment growth.

Increasing Consumer Preference For Authentic And Craft Spirits

Authenticity now carries more weight in the agave spirits market than broad brand visibility on its own. Buyers are looking more closely at additive-free claims, production methods, origin stories, and the use of 100% agave, which is changing the standard for what counts as a premium label. Mexico’s tequila regulator reported that exports of 100% agave tequila rose to 278.62 million liters in 2025, showing that demand is shifting toward products with stronger authenticity cues within the category itself [2]Source: Consejo Regulador del Tequila via El Informador, “Industria Incrementó La Exportación Y La Producción De Tequila En 2025,” El Informador, informador.mx. The agave spirits market is therefore rewarding producers that can explain where the agave came from, how the spirit was made, and why the label reflects a genuine production tradition. This change also raises the cost of participation, because provenance and process transparency are becoming basic entry conditions rather than extra selling points. As a result, the agave spirits market is becoming more selective even while it continues to expand.

Cocktail Menu Penetration In Bars And Restaurants

Cocktail culture remains an important route of consumer recruitment for the agave spirits market. Tequila and mezcal benefit from drinks that are already familiar to a wide audience, and that makes trial easier in bars and restaurants than in many retail settings. Once consumers enter through high-frequency cocktails such as the Margarita or Paloma, they are more likely to trade up into sipping expressions and more distinct agave profiles. That pattern helps the agave spirits market because on-trade exposure does more than generate immediate sales, it also educates consumers and raises comfort with premium price points. The effect is strongest where bartenders actively shape drink choices and where menus highlight origin, style, or production detail. For that reason, restaurant and bar menus continue to play a larger role in category development than their direct revenue share alone would suggest.

Product Innovation Across Agave Spirit Categories

The agave spirits market is also expanding through product innovation that reaches new use occasions and new buyer groups. In August 2025, Almave launched Almave Humo, a non-alcoholic mezcal alternative made with traditional pit-roasting methods and Espadín agave from Puebla, priced at USD 36.99 per 700 mL. That launch showed that innovation in the agave spirits market is no longer limited to aging ladders or line extensions within alcoholic spirits alone. It is now reaching sober-curious occasions, gifting needs, and premium experimentation, which broadens the number of points where consumers can engage with agave-based products. The same logic supports ready-to-drink and crossover concepts that help brands enter grocery, convenience, and casual social settings with less friction than full-bottle spirits require. Innovation therefore supports the agave spirits market by opening incremental occasions rather than just refreshing existing stock-keeping units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Agave Raw Material Prices | -1.2% | Mexico as the origin market, with global supply chain effects | Short term (≤ 2 years) |

| Changing Consumer Preferences Toward Low- and No-Alcohol Beverages | -0.9% | North America and Europe | Medium term (2-4 years) |

| Competition From Other Premium Spirits Categories | -0.7% | North America and Europe | Medium term (2-4 years) |

| Supply Chain Disruptions Affecting Global Distribution | -0.6% | Global, especially North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility In Agave Raw Material Prices

Agave supply swings remain one of the clearest restraints on the agave spirits market. Blue agave prices in Mexico moved from record highs to much lower levels by early 2025 after heavy planting followed the earlier demand surge, and that has made long-range cost planning less stable for producers of different sizes. This matters because agave takes years to mature, so oversupply today can turn into shortage later if weaker prices discourage new planting. The agave spirits market is therefore exposed to a repeating cycle where short-term input relief can create longer-term supply stress and strain smaller growers first. Larger producers may absorb part of that pressure through scale, but artisanal and emerging brands have less room to manage those changes without margin loss or pricing disruption. If this pattern persists, the agave spirits market could see more uneven supply quality and less diversity in smaller premium offerings.

Changing Consumer Preferences Toward Low- And No-Alcohol Beverages

The rise of low- and no-alcohol drinking occasions is creating a slower but visible headwind for the agave spirits market. Younger consumers in developed markets are not leaving premium beverage occasions altogether, but they are cutting alcohol frequency more often and moving across formats. The launch of Almave Humo in 2025 showed that category participants themselves now treat this change as durable enough to justify direct product investment. DISCUS also reported that total U.S. spirits supplier revenues fell in 2024 for the first time in more than 20 years, which reinforces the idea that alcohol moderation is measurably affecting established categories. For the agave spirits market, the implication is clear: brands that create low-ABV or non-alcoholic extensions may protect consumer relevance better than those that leave that occasion to competing beverage formats. That does not remove demand for tequila or mezcal, but it does change where future wallet share will be contested.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mezcal Gaining Ground Within a Tequila-Dominated Category

Tequila accounted for 65.48% of the agave spirits market size in 2025, giving it a strong lead over other product categories in both retail visibility and export readiness. The segment benefits from mature certification systems, wider global recognition, and a supply chain that already supports large export volumes. Mexico’s tequila industry produced 583.53 million liters in 2025 and exported 407.80 million liters to more than 120 countries, which confirms the scale advantages that continue to support tequila’s lead position. Exports of 100% agave tequila reached 278.62 million liters in the same year, which shows that premium positioning is also becoming stronger inside the largest product category. Within the agave spirits industry, tequila remains the category that sets the commercial baseline for consumer access, brand recognition, and price ladder development.

Mezcal is projected to grow at 9.11% CAGR through 2031, making it the faster-moving product type in the agave spirits market. Its growth reflects a lower maturity level, stronger craft appeal, and a more distinct flavor profile that often attracts experienced consumers after tequila entry. The product is also benefiting from bartender support and premium menu positioning, which gives it a stronger role in high-value trial occasions than its current scale alone suggests. Certified mezcal production had reached 12.24 million liters in 2023 before moving down to 6.91 million liters in 2025, a shift that points to post-boom rationalization and tighter quality discipline rather than a loss of long-term relevance. The smaller others category, including raicilla, bacanora, and sotol, remains niche but still matters because it keeps the agave spirits market open to boutique experimentation and regional differentiation.

By Price Point: Premium Momentum Building from a Standard Volume Base

Standard expressions held 86.79% share in 2025, which means they continue to carry the main volume burden of the agave spirits market across modern retail, convenience channels, and broad on-premise availability. This tier remains important because it gives consumers an accessible point of entry and helps brands maintain wide physical distribution. It also supports trial, gifting, and repeat buying in settings where price sensitivity remains higher than interest in production detail. The role of standard products should not be treated as weak positioning, because they help sustain shelf space and keep the agave spirits market visible across a larger set of outlets. Within the agave spirits industry, this segment still provides the reach that allows premium labels to build from a broad installed base rather than from isolated luxury demand.

The premium segment is forecast to grow at 9.56% CAGR through 2031, which makes it the faster-value layer inside this segmentation. Long-term demand patterns support that direction, as super-premium and high-end tequila in the United States expanded more than 1,400% in volume between 2003 and 2025. Premium growth now depends less on price alone and more on proof of quality, which includes additive-free positioning, estate sourcing, and production transparency. That change shortens the gap between product story and purchase decision, especially for informed consumers who no longer treat celebrity association as enough. As a result, the agave spirits market is seeing value migrate upward even while standard expressions continue to anchor category breadth.

By Sales Channels: Off-Trade Anchors Volume While On-Trade Drives Category Elevation

Off-trade represented 72.15% of the agave spirits market share in 2025, which shows that retail-led channels still account for most category revenue. This channel matters because it gives the agave spirits market scale, regular replenishment, and a broad geographic footprint across supermarkets, liquor stores, travel retail, and online ordering where permitted. Off-trade is also where price comparison is easiest, which makes packaging clarity, brand trust, and recognizable category cues more important. That setting tends to favor labels that can communicate quality quickly and maintain distribution consistency across many points of sale. For producers, strong off-trade execution remains essential because it keeps the agave spirits market visible to both frequent buyers and newer consumers.

On-trade is forecast to grow at 9.85% CAGR through 2031, making it the faster channel in the agave spirits market. Bars and restaurants do more than sell drinks, they also introduce category language, shape first impressions, and encourage consumers to move from cocktails into premium sipping formats. That is why on-premise activity has strategic value beyond immediate sales, especially for mezcal and high-end tequila expressions that need guided trial. It also helps brands build credibility through bartender advocacy, curated menus, and menu placement in venues where product story influences what consumers order. The result is a channel structure where off-trade provides volume stability while on-trade raises perception, upgrades mix, and supports longer-term value growth in the agave spirits market.

Geography Analysis

North America held 33.46% share in 2025, which made it the leading regional contributor to the agave spirits market. The region remains central because it combines great installed demand, premium consumer awareness, and a well-developed route to market for imported spirits. DISCUS reported that U.S. tequila and mezcal volumes reached 32.10 million 9-liter cases in 2025, showing that the category still moved at scale even as revenue conditions became more selective. That scale gives North America a large influence on pricing, innovation, and distributor behavior across the wider agave spirits market. At the same time, the region is more mature than many emerging markets, so premium positioning and authenticity now matter more than simple shelf expansion.

Europe remains established but less saturated, which gives the agave spirits market room to build further through hospitality and premium retail channels. The region benefits from strong cocktail culture in major urban centers and from consumer openness to imported premium spirits with protected origin status. The legal standing of tequila and mezcal origin frameworks also supports confidence in category authenticity, which helps premium products justify higher prices. For brands entering Europe, well-placed on-trade partnerships can still create an early advantage because consumer education remains an important part of growth.

Asia-Pacific is forecast to grow at 11.02% CAGR through 2031, making it the fastest regional segment in the agave spirits market. Growth in this region is tied to rising urban incomes, premium spirits curiosity, and stronger bar culture in cities across China, Japan, India, and Australia. India stands out because its large consumer base and growing premium appetite create clear long-term interest, even though tariff barriers remain an important constraint in the imported spirits trade environment[3]Source: Cámara Nacional de la Industria Tequilera via El Economista, “Agroindustria Tequilera Se Consolida Como Motor Económico Y Símbolo Nacional,” El Economista, eleconomista.com.mx. South America is also developing premium demand through hospitality expansion, while the Middle East and Africa remain more selective because regulatory conditions vary sharply by country. Even so, the faster pace in Asia-Pacific shows that the agave spirits market is no longer defined only by its traditional Western demand centers.

Competitive Landscape

The agave spirits market remains fragmented, with global spirits groups, heritage houses, and small artisanal producers competing across different price tiers and use occasions. No single company controls the category in a way that closes access for challengers, which keeps competitive pressure high across tequila, mezcal, and adjacent premium offerings. Large producers still hold important advantages in distribution, marketing reach, and portfolio management, but smaller brands can win attention when they offer a clear origin story and distinct production identity. That balance keeps the agave spirits market active on both brand building and portfolio reshaping. It also means scale alone is not enough to secure long-term momentum if authenticity or channel fit is weak.

Recent strategic moves show that large companies still prefer to buy or back proven brands instead of building every label internally in the agave spirits market. In April 2026, Sazerac made a strategic financial investment in 818 Tequila and secured exclusive U.S. sales and distribution rights, which highlights continued interest in brands that already show measurable consumer traction. In 2025, Maguey Spirits acquired Bozal Mezcal and Pasote Tequila from 3 Badge Beverage Corporation, which pointed to a parallel push toward heritage-led consolidation within premium agave labels. In July 2025, Luxury Spirits International added De Nada Tequila and Los Javis Mezcal to its U.S. portfolio, showing that distributors and importers still see room to scale artisanal and premium agave propositions.

The white space in the agave spirits market is now split between scale and specialization. Large groups have room to expand by backing authentic craft labels and then widening distribution without weakening the production narrative that made those labels credible in the first place. Smaller players can still compete by focusing on single-village mezcal, additive-free tequila, estate sourcing, and adjacent formats that connect with moderation-led occasions. Direct-to-consumer and premium e-commerce partnerships also help these brands reach buyers outside traditional distribution systems, which can narrow the advantage of larger incumbents in selected markets. The result is a competitive field where the agave spirits market rewards both disciplined scale and clear specialization, but offers less room for middle-positioned brands with weak differentiation.

Agave Spirits Industry Leaders

Becle, S.A.B. de C.V.

Diageo plc

Pernod Ricard S.A.

Bacardi Limited

Constellation Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Agave Spirits partnered with Helmsman Imports to launch its sustainability-focused mezcal portfolio in the U.S. market. The expansion strengthens the brand's international distribution network and capitalizes on the growing U.S. demand for premium and artisanal agave spirits.

- March 2026: tock Spirits Group expanded its tequila portfolio by launching the Sierra 100% Agave range, featuring Blanco, Reposado, and Añejo expressions made from 100% Blue Weber agave. The new range debuted through global travel retail in partnership with Gebr. Heinemann.

- May 2025: Rio Agave Blanco Tequila launched in Texas, introducing an additive-free tequila crafted from 100% handpicked Blue Weber agave sourced from Jalisco, Mexico. The launch strengthens the brand's presence in the rapidly growing premium agave spirits market.

Global Agave Spirits Market Report Scope

| Tequila |

| Mezcal |

| Others |

| Standard |

| Premium |

| On-Trade |

| Off-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Tequila | |

| Mezcal | ||

| Others | ||

| Price Point | Standard | |

| Premium | ||

| Sales Channels | On-Trade | |

| Off-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of agave spirits worldwide?

The agave spirits market is estimated at USD 13.12 billion in 2026 and is forecast to reach USD 20.32 billion by 2031 at 8.05% CAGR.

Which product category leads agave-based spirits sales?

Tequila leads by product type with 65.48% share in 2025, supported by large-scale production, broad export reach, and stronger global recognition.

Which product type is growing the fastest through 2031?

Mezcal is the fastest-growing product type with a projected 9.11% CAGR, helped by stronger craft appeal and rising bartender support.

Which channel is expanding faster, retail or bars and restaurants?

Off-trade remains larger at 72.15% share in 2025, but on-trade is growing faster with a projected 9.85% CAGR through 2031.

Page last updated on: