Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

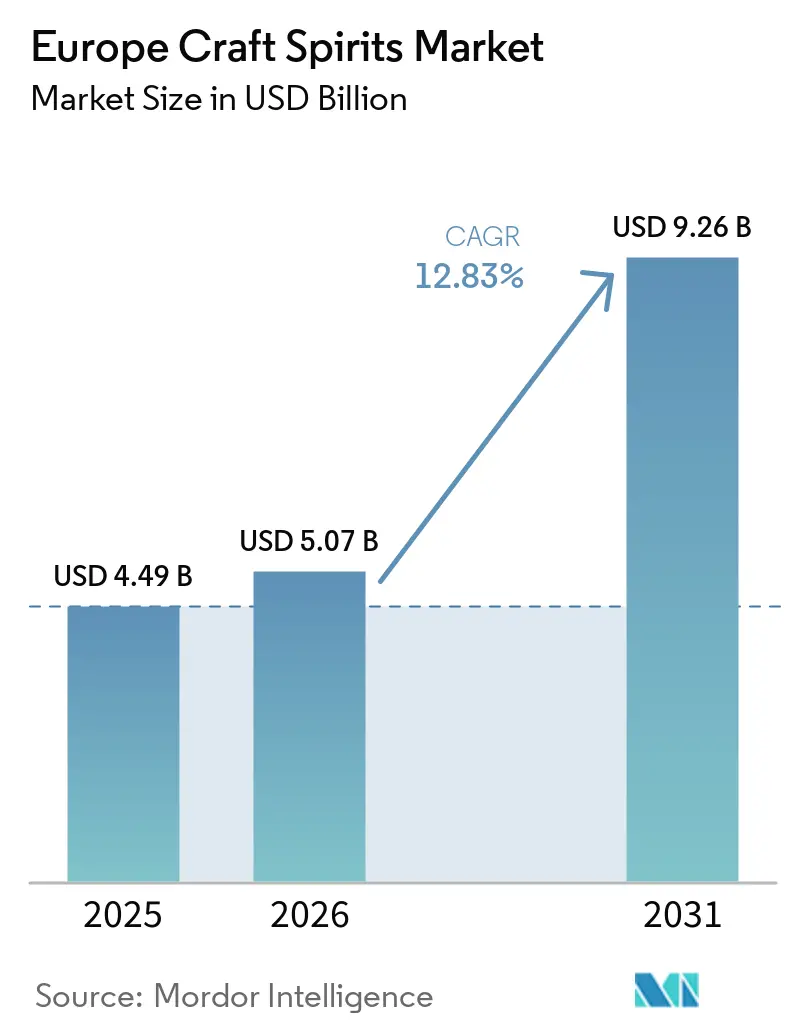

| Base Year Market Size (2025) | USD 4.49 Billion |

| Market Size (2026) | USD 5.07 Billion |

| Market Size (2031) | USD 9.26 Billion |

| Growth Rate (2026 - 2031) | 12.83% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Craft Spirits Market Analysis by Mordor Intelligence

The Europe craft spirits market size was valued at USD 4.49 billion in 2025 and estimated to grow from USD 5.07 billion in 2026 to reach USD 9.26 billion by 2031, at a CAGR of 12.83% during the forecast period (2026-2031). The market is demonstrating a clear transition toward sustainable production practices, with distillers implementing eco-friendly packaging, energy-efficient processes, and sourcing local ingredients. These environmental initiatives align with consumer preferences for sustainable products. The Europe craft spirits landscape is characterized by a diverse range of artisanal producers, with countries like the United Kingdom, Germany, and France leading in craft distillery establishments. Small-batch production methods, unique flavor profiles, and regional ingredients distinguish craft spirits from mass-produced alternatives. The market benefits from strong regional traditions, protected geographical indications, and increasing consumer interest in authentic, locally produced spirits. Additionally, the rise of cocktail culture and the increasing demand for premium on-trade venues has created new opportunities for craft spirit manufacturers across Europe.

Key Report Takeaways

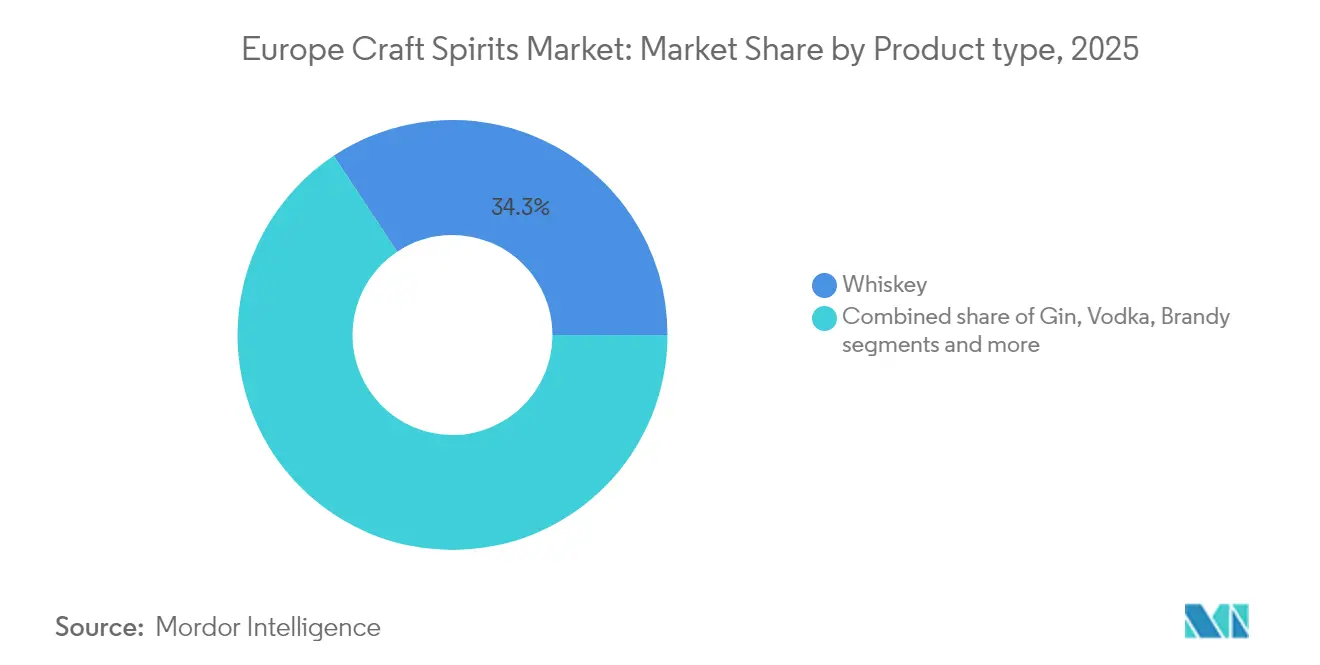

- By product type, whiskey led with 34.32% of the Europe craft spirits market share in 2025; gin is projected to clock the fastest 13.03% CAGR through 2031.

- By ingredient, grain-based spirits accounted for 55.74% of the Europe craft spirits market size in 2025, whereas fruit-based spirits are poised to expand at 13.28% CAGR between 2026-2031.

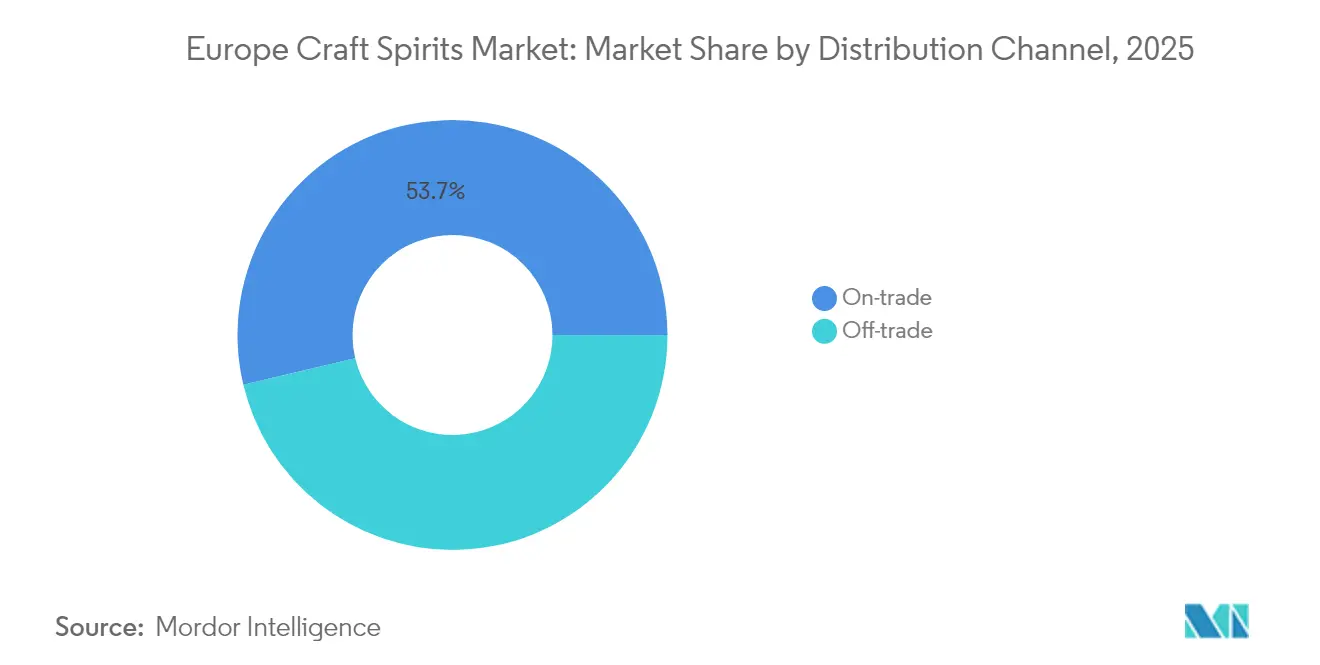

- By distribution channel, the on-trade captured 53.72% of the revenue in 2025; the off-trade is forecast to accelerate at a 12.64% CAGR, owing to the rise of digital and direct-to-consumer models.

- By geography, the United Kingdom commanded a 24.52% share of the Europe craft spirits market size in 2025, while Germany is on course for a 13.74% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Craft Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing tourism and hospitality impact positive growth | +3.2% | United Kingdom, Germany, France, Spain, Italy | Medium term (2-4 years) |

| Product differentiation in terms of ingredients and alcohol content | +2.6% | Germany, United Kingdom, France, Sweden | Medium term (2-4 years) |

| Surge in demand for premium alcoholic beverages | +2.3% | United Kingdom, France, Germany, Netherlands | Short term (≤2 years) |

| Increasing preference for innovative flavors | +1.9% | Germany, United Kingdom, Sweden, Poland | Short term (≤2 years) |

| Increased focus on sustainable production methods in spirit manufacturing | +1.6% | Sweden, Germany, Netherlands, France | Long term (≥4 years) |

| Enhanced market accessibility through e-commerce and direct-to-consumer channels | +1.3% | United Kingdom, Germany, France, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing tourism and hospitality impact positive growth

Tourism and hospitality sector growth drives expansion in the Europe craft spirits market. The rise in international and domestic tourism across Europe increases demand for authentic, high-quality beverages that represent local traditions and craftsmanship. Tourists seek unique drinking experiences featuring regional flavors, particularly from local distilleries. This trend is prominent in tourist destinations and cities, where bars, pubs, and specialized craft spirit venues introduce visitors to diverse European craft spirits. According to the World Tourism Organization (UN Tourism), international tourist arrivals in Europe increased significantly in 2024 compared to the previous year. In 2024, inbound arrivals in Europe reached approximately 747 million [1]Source: The United Nations World Tourism Organization, "International tourism recovers pre-pandemic levels in 2024", unwto.org.

Product differentiation in terms of ingredients and alcohol content

Europe craft spirits manufacturers actively create unique products by developing innovative ingredients and offering diverse alcohol content options. These companies build extensive product portfolios that combine premium spirits with low and non-alcoholic alternatives to meet various consumer preferences and drinking occasions. The market responds to growing health awareness trends, as documented in Diageo's 2025 Foresight Report, which shows younger consumers adopting "zebra striping" behaviors. This practice involves consumers deliberately alternating between alcoholic and non-alcoholic beverages during social occasions, reflecting a broader shift toward balanced consumption habits. The trend demonstrates that health-conscious decisions influence purchasing patterns and shape product development strategies in the craft spirits market, particularly among younger demographic groups that prioritize both enjoyment and well-being in their beverage choices.

Surge in demand for premium alcoholic beverages

The Europe spirits market demonstrates a significant shift toward premium products, even amid economic pressures. Consumers across Europe increasingly favor high-quality, artisanal spirits that feature unique flavors, authentic ingredients, and traditional craftsmanship. This trend is particularly evident among younger demographics and urban consumers who value products offering individuality, heritage, and authentic brand narratives. The market shows growing demand for premium, super-premium, and flavored spirits. Consumers demonstrate increased willingness to invest in limited-edition releases, aged spirits, and products emphasizing regional characteristics and traditional production methods. United Spirits Limited's financial results reflect this trend, with their Prestige and Above segment accounting for 87.4% of net sales in 2023-24, achieving 11.9% growth. The strong preference for premium options among younger consumers indicates a fundamental shift in quality perception, suggesting sustained category value growth in the long term.

Increasing preference for innovative flavors

Flavor innovation has emerged as a key growth driver in the spirits market, particularly among younger consumers who show increased interest in experimental taste profiles. Flavored tequilas demonstrate significant growth, attracting consumers who seek new drinking experiences while valuing traditional production methods. European craft distilleries have strengthened this trend by introducing innovative botanical combinations and aging techniques, which larger companies later adopt. The expanding flavor landscape has dissolved traditional category distinctions, as gin producers incorporate whiskey-style botanicals and vodka brands develop fruit-forward profiles similar to liqueurs. This evolution creates new market dynamics and consumption opportunities. In May 2024, Absolut introduced a honey-flavored vodka in the United Kingdom, featuring natural flavors and a distinct golden honey taste profile.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -1.9% | United Kingdom, Sweden, Finland, France | Medium term (2-4 years) |

| Health concern over excessive consumption | -1.6% | Sweden, Netherlands, Germany, France | Long term (≥4 years) |

| Premium pricing of craft spirits faces resistance from price-sensitive consumers | -1.0% | Spain, Poland, Italy, Rest of Europe | Short term (≤2 years) |

| Storage and aging requirements increase production cycles and operational costs | -0.6% | United Kingdom, France, Germany, Spain | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations

The Europe spirits market faces increasing regulatory pressures that create compliance challenges and potential market access barriers. The United Kingdom's implementation of an alcohol duty system bases taxation on alcohol content instead of product category, affecting pricing strategies across spirits portfolios. The European Union's consideration to classify ethanol as a carcinogenic, mutagenic, or toxic for reproduction (CMR) substance may significantly impact product formulations and marketing claims. Belgium's 2024 introduction of alcohol sales restrictions limits product availability and imposes stricter penalties for violations [2]Source: Belga News Agency, "Government approves restrictions on sale of tobacco and alcohol," belganewsagency.eu. These regulatory changes create a complex compliance environment, increasing operational costs and constraining marketing flexibility, particularly affecting smaller producers with limited regulatory resources.

Health concern over excessive consumption

Health consciousness and concerns regarding excessive alcohol consumption constitute fundamental constraints to the growth trajectory of the Europe craft spirits market. Consumer preferences demonstrate a measurable transformation toward products with reduced alcohol content or complete abstinence from alcohol consumption. In many European countries, spirits consumption is relatively low compared to beer and wine. This is partly due to cultural preferences, with wine often enjoyed with meals and in moderation. Additionally, there's a growing trend towards moderate alcohol consumption and a decrease in heavy episodic drinking. There's a trend towards moderate alcohol consumption, with more people choosing lower-alcohol options or opting for non-alcoholic beverages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whiskey Dominates, Gin Accelerates Growth

Whiskey holds a 34.32% market share in the Europe spirits market in 2025, maintaining its position as the leading product category. This dominance stems from its strong heritage and effective premium positioning strategies. Gin demonstrates significant momentum with a projected CAGR of 13.03% from 2026-2031, driven by botanical innovations and craft production methods that resonate with consumers seeking unique experiences. Vodka remains a substantial market presence through its flavor variations and mixability attributes, while brandy sustains its premium status in France and Spain. Tequila and rum categories are expanding through premium offerings and increased presence in cocktail culture.

The market structure is transforming as product categories become increasingly interconnected through cross-category innovation. Diageo exemplifies this trend, with its premium portfolio strategy yielding notable results, particularly in its tequila segment, where Don Julio showed substantial growth in fiscal 2024. Companies manage diverse spirit portfolios rather than focusing on single categories, necessitating refined brand architecture and portfolio management approaches to establish distinct market positions.

By Ingredient: Grain-Based Leadership Faces Fruit-Based Challenge

Grain-based spirits hold a dominant 55.74% share of the Europe market in 2025. This leadership position stems from well-established production infrastructure and widespread consumer acceptance across the whiskey, vodka, and gin categories. The segment's robust supply chain and scalable production capabilities ensure consistent quality across price segments, from value to ultra-premium offerings. Fruit-based spirits are expected to grow at a CAGR of 13.28% during 2026-2031.

This growth reflects increasing consumer preference for natural ingredients and distinct flavor profiles, particularly in premium brandy and fruit liqueurs that highlight regional origins and traditional manufacturing processes. Agave-based spirits, specifically tequila and mezcal, are expanding their presence in the European market despite supply limitations, attracting consumers interested in authentic experiences. Ingredient innovation has emerged as a crucial market differentiator, with sustainability considerations increasingly affecting consumer purchasing decisions. In March 2025, Doghouse introduced London's first 'Bourbon-style' whisky, aged for three years in virgin, charred American oak casks, producing vanilla, caramel, and spice notes.

By Distribution Channel: On-Trade Dominance, Off-Trade Acceleration

On-trade channels command 53.72% of the Europe spirits market in 2025, benefiting from the hospitality sector's recovery and consumers' renewed interest in experiential consumption. Premium spirits show strong performance in this channel, with signature cocktails enabling product trials and brand development in high-visibility venues. The channel's significance extends beyond sales volume, offering essential brand-building opportunities through bartender advocacy and experiential marketing that influences consumer preferences and supports premiumization.

The off-trade is projected to grow at a CAGR of 12.64% from 2026 to 2031, reflecting the sustained impact of pandemic-era consumption patterns and e-commerce growth. Specialty and liquor stores play a vital role in distributing premium spirits, offering curated selections and expert guidance that encourage the purchase of premium products. Direct-to-consumer models support these specialty retailers, as brands develop e-commerce platforms that generate valuable consumer data while improving profit margins. The European Commission's approval of a EUR 5 billion French plan to support wine and spirits exports to the United States underscores the importance of international distribution channels and the potential impact of trade disputes on market access.

Geography Analysis

The United Kingdom holds 24.52% market share in the Europe craft spirits market in 2025, driven by its established whiskey heritage and cocktail culture. The country's extensive network of micro-distilleries and artisanal producers combines traditional production methods with innovation to address increasing consumer demand for premium and local spirits. The United Kingdom's hospitality sector supports craft spirit growth through its cocktail culture and on-trade presence, enabling brands to showcase products through tasting experiences and cocktail offerings.

Germany shows significant market potential with a projected CAGR of 13.74% from 2026-2031, supported by premiumization trends and product innovation. The craft beer's in europe witnessing steady growth, driven by rising consumer preference for premium, artisanal, and locally produced alcoholic beverages across the region. The country's economic stability, with real GDP growth at 1.1% in the European Union for 2025, sustains premium spirits consumption despite economic challenges. France maintains market strength through its cognac production and expanding craft spirits segment, while Spain benefits from its established gin and tonic consumption. The Netherlands, Italy, Sweden, and Poland each offer unique market opportunities, with Sweden focusing on sustainable and health-conscious products.

Eastern European markets within the Rest of Europe segment show increasing potential for premium spirits as consumer disposable incomes increase. While regional inflation has decreased, core inflation continues, affected by increasing real wages and tight labor markets. Growth in household consumption is expected to benefit the craft spirits market. The services sector's positive performance across Europe creates favorable conditions for on-trade spirits consumption, supported by the ongoing recovery of the tourism and hospitality sectors.

Competitive Landscape

The Europe spirits market is highly fragmented, with significant participation from multinational corporations such as Pernod Ricard SA and Diageo PLC, alongside established regional players like William Grant and Sons and Remy Cointreau. These companies pursue strategies centered on premium product development and portfolio diversification, including ultra-premium products and non-alcoholic or low-alcohol alternatives, to adapt to changing consumer preferences. The focus on premiumization is driven by increasing consumer demand for high-quality, unique offerings, while the no- or low-alcohol segment caters to the growing health-conscious demographic.

To strengthen their market position, these companies also invest in marketing campaigns, collaborations, and innovative packaging to enhance brand appeal. Competition has intensified further with the rise of craft distilleries, which challenge established manufacturers through heritage-focused marketing and innovative ingredients. These craft distilleries emphasize authenticity, local sourcing, and artisanal production methods, particularly in the gin and whiskey segments, appealing to consumers seeking distinctive and niche products. Additionally, the growing popularity of experiential marketing by craft distilleries, such as distillery tours and tasting events, has further contributed to their competitive edge in the market.

Companies across the market implement digital technologies to gain competitive advantages. They improve their operations and strengthen customer relationships through digital initiatives, while e-commerce platforms enable direct sales to consumers and support data collection efforts. Companies also use artificial intelligence to enhance their production processes and better understand consumer behavior patterns.

Europe Craft Spirits Industry Leaders

-

Pernod Ricard SA

-

Bacardi Limited

-

Diageo PLC

-

Constellation Brands Inc.

-

William Grant and Sons Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnnie Walker introduced the Johnnie Walker Vault, a global luxury platform focused on whisky blending. The Vault maintains a collection of 500 whiskies sourced from rare, aged, and ghost casks.

- March 2025: Radico Khaitan introduced Ankahi Zaffran Spiced Liqueur, the first product in its Ankahi Liqueur series. The product debuted at ProWein in Düsseldorf, Germany. The company aims to expand its global footprint in the premium spirits market.

- Feb 2025: Jason Momoa launched his Meili Vodka brand in the United Kingdom through a partnership with Amathus Drinks, which serves as the United Kingdom distributor.

- April 2024: Brave New Spirits, a Scotch bottler, introduced the Whisky heroes series. The initial release features eight whiskies, including seven single malts and one single grain, aged or finished in sherry casks and bourbon barrels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe craft spirits market as the annual value of distilled beverages produced in small or independently owned facilities, in batches typically under 750 L, where distillers control each step from mashing to bottling. According to Mordor Intelligence, the scope covers whiskey, gin, vodka, brandy, and similar artisanal variants sold through on-trade and off-trade channels across 10 European countries.

Scope exclusion: flavored ready-to-drink spirit cocktails and bulk industrial alcohol are not counted.

Segmentation Overview

-

By Product Type

- Whiskey

- Gin

- Vodka

- Brandy

- Other Types

-

By Ingredient

- Grain-based

- Fruit-based

- Agave-based

- Others

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Other Off Trade Channels

-

By Geography

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed craft distillers, distributors, bar managers, and regulatory officers in Germany, the U.K., France, Italy, and Spain. The conversations validated typical ex-distillery price points, average batch sizes, and the pace at which new labels secure shelf space, thereby filling gaps left by desk work.

Desk Research

We begin by mapping the production and consumption footprint using non-paywalled tier-1 datasets such as Eurostat beverage output, UN Comtrade HS-2208 trade flows, SpiritsEurope annual statistical reports, and national excise registries that list active micro-distilleries. Company filings, IPO prospectuses, and hospitality association whitepapers complement supply metrics with channel and pricing cues.

Subscription tools, D&B Hoovers for company revenue splits and Dow Jones Factiva for deal/news tracking, help us vet financial signals and spot capacity additions. These sources collectively frame the demand pool; yet the list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction starts with Eurostat production liters, aligned with import-export balances to obtain apparent consumption, which is then multiplied by weighted average craft-segment selling prices. Select bottom-up checks, sampled ASP x bottles from 60 surveyed distilleries, anchor the totals. Key model inputs include registered distillery counts, liter-per-capita spirits intake, craft penetration in on-trade sales, excise duty shifts, and premiumization pricing ladders. A multivariate regression, using GDP-per-capita and tourism inflows as predictors, projects volumes; exponential smoothing refines near-term ASP trends. Where bottom-up samples undershoot, ratios are scaled to match verified shipment data before final triangulation.

Data Validation & Update Cycle

Outputs undergo variance scans against trade data and SpiritsEurope benchmarks; anomalies trigger re-contact of sources. Two analysts review assumptions before sign-off. We refresh each model annually and issue interim tweaks when tax reforms, major capacity launches, or consumption shocks occur.

Why Mordor's Europe Craft Spirits Baseline Commands Reliability

Published values often diverge because firms choose different product mixes, channel splits, and refresh cadences, which shifts both volumes and average prices.

Key gap drivers include whether moonshine and flavored RTDs are folded into totals, the aggressiveness of price-inflation assumptions, and how frequently primary interviews recalibrate the model. Mordor's scope mirrors EU excise definitions, uses 2024 as a clean base year, and is updated every twelve months, which reduces drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.49 B (2025) | Mordor Intelligence | |

| USD 8.40 B (2024) | Global Consultancy A | Bundles flavored RTDs and regional liqueurs; no primary price verification |

| USD 4.98 B (2023) | Regional Consultancy B | Applies constant 22.6 % CAGR without scenario stress tests |

| USD 1.12 B (2022) | Industry Insights C | Counts only registered micro-distilleries, excluding contract-distilled brands |

In sum, by selecting EU-aligned definitions, blending verified production data with channel-level price audits, and refreshing the model on a strict annual cycle, Mordor delivers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the Europe craft spirits market?

The Europe craft spirits market is valued at USD 5.07 billion in 2026.

How fast is the Europe craft spirits market expected to grow?

It is projected to expand at a 12.83% CAGR between 2026 and 2031, reaching USD 9.26 billion.

Which product category leads the European craft spirits market?

Whiskey leads with 34.32% share in 2025, supported by robust premiumization and export momentum.

Which country is the fastest-growing Europe craft spirit’s market?

Germany is forecast to post a 13.74% CAGR from 2026-2031, outpacing other major economies.

Page last updated on: