Pharmaceutical Chemicals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

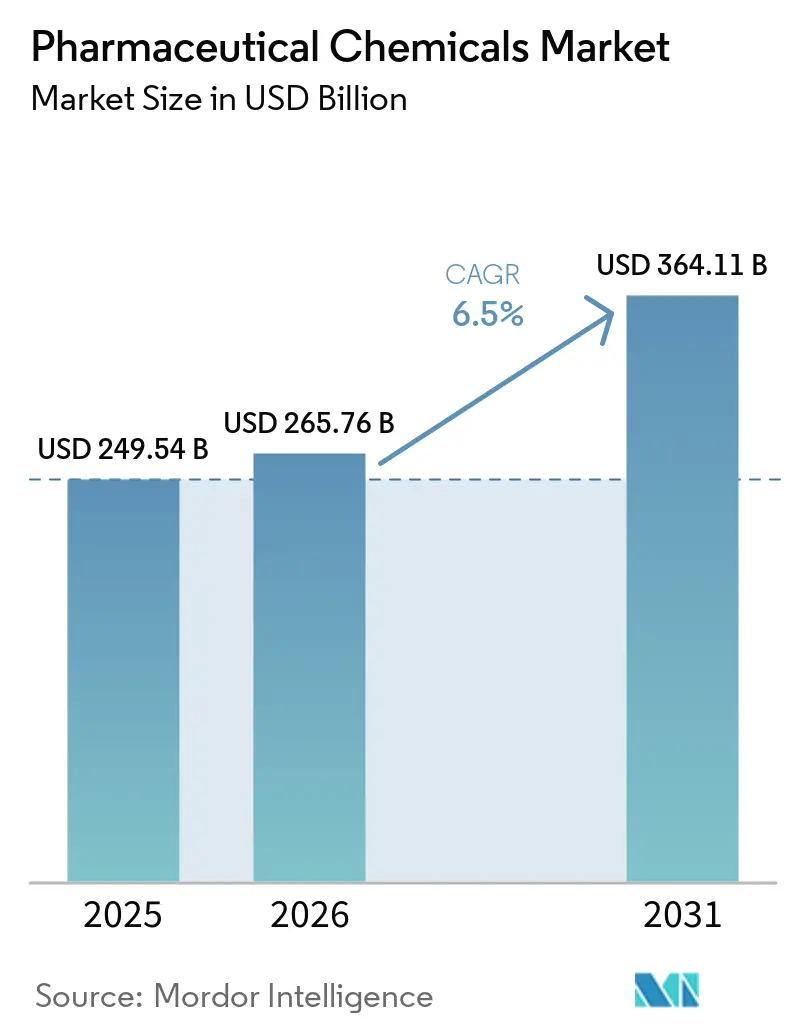

| Market Size (2026) | USD 265.76 Billion |

| Market Size (2031) | USD 364.11 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Chemicals Market Analysis by Mordor Intelligence

The Pharmaceutical Chemicals Market size was valued at USD 249.54 billion in 2025 and is estimated to grow from USD 265.76 billion in 2026 to reach USD 364.11 billion by 2031, at a CAGR of 6.5% during the forecast period (2026-2031).

The pharmaceutical chemicals market is witnessing a shift as companies focus on domestic supply security, qualified manufacturing networks, and stable access to critical inputs. The U.S. policy move in August 2025 to establish the Strategic Active Pharmaceutical Ingredients Reserve has positioned pharmaceutical chemistry at the core of supply planning and procurement strategies, driving domestic API demand over the forecast period.[1]White House, “Ensuring American Pharmaceutical Supply Chain Resilience by Filling the Strategic Active Pharmaceutical Ingredients Reserve,” White House, whitehouse.gov Rising demand for high-purity APIs, specialty excipients, biologic intermediates, and advanced delivery materials is enhancing the value of qualified suppliers while increasing shipment volumes. Additionally, outsourcing is reshaping the market as innovator companies and generic manufacturers increasingly rely on specialist CDMO and CMO platforms for complex synthesis, scale-up, and regulated manufacturing. This trend creates opportunities for companies with strong compliance, specialty chemistry expertise, and dependable regional manufacturing capabilities.

Key Report Takeaways

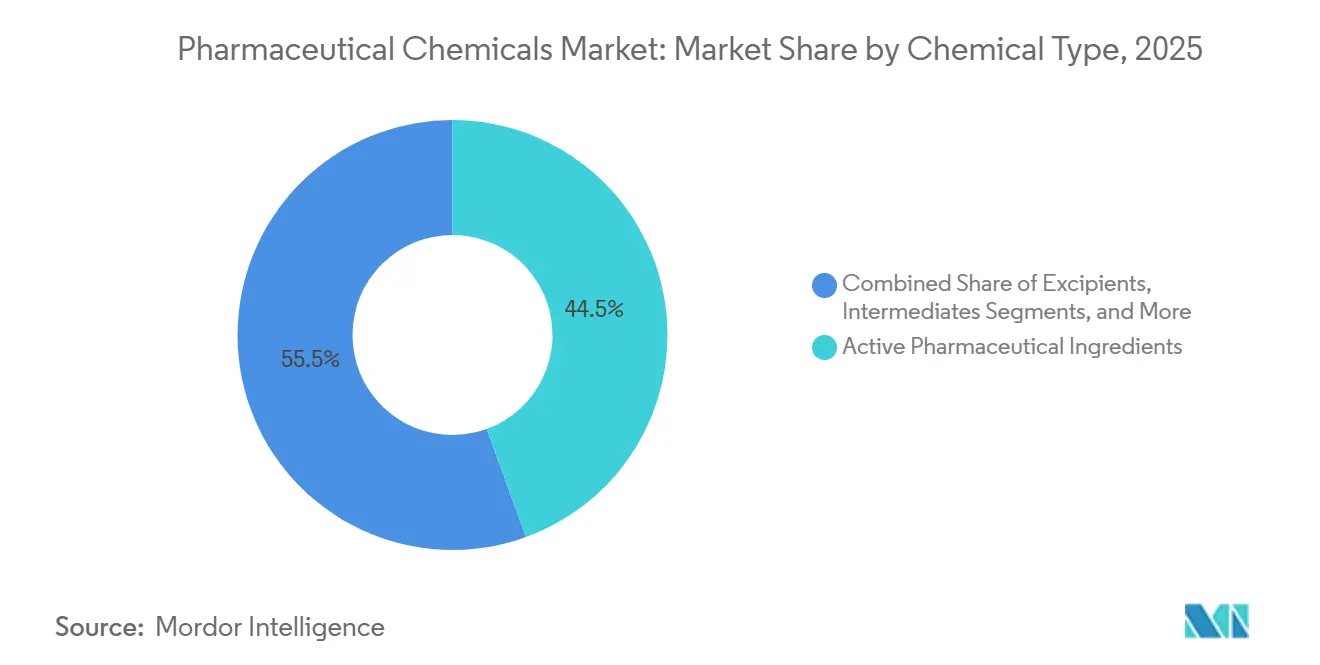

- By chemical type, active pharmaceutical ingredients led with 44.45% revenue share in 2025, while excipients are forecast to expand at a 6.99% CAGR through 2031.

- By therapeutic area, oncology accounted for 26.78% share in 2025, while cardiovascular is projected to record the highest CAGR at 7.95% through 2031.

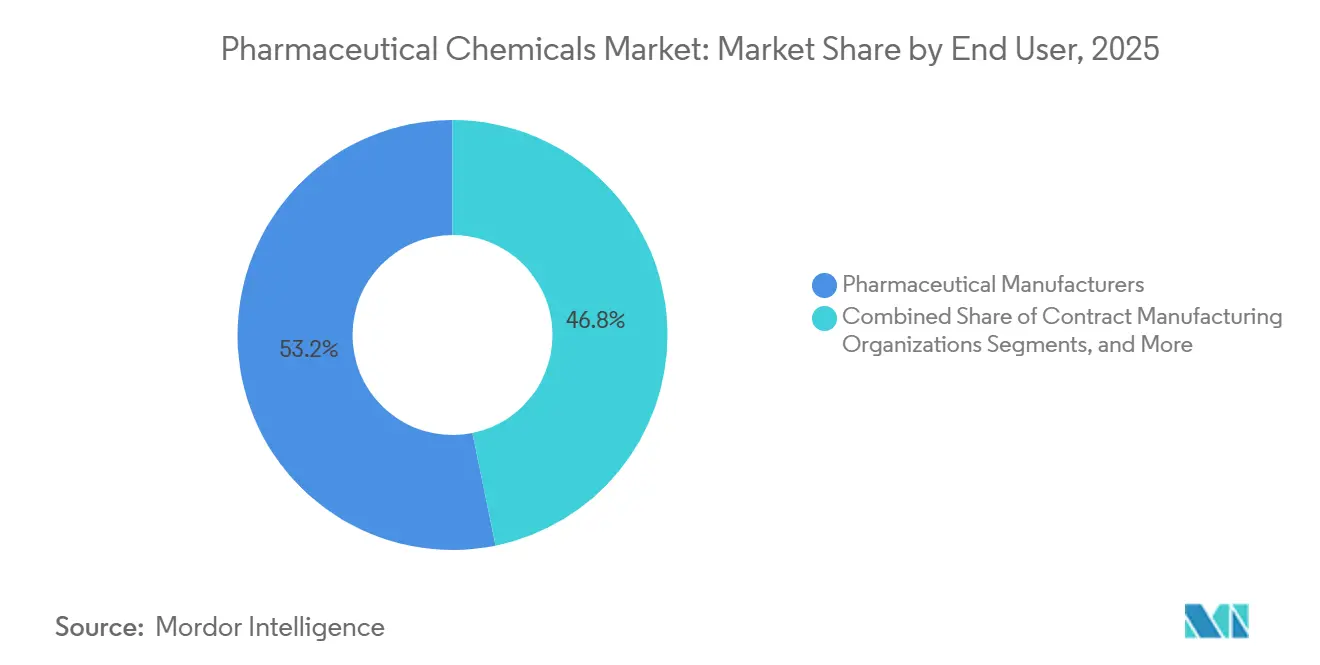

- By end user, pharmaceutical manufacturers held 53.25% of the pharmaceutical chemicals market share in 2025, while contract manufacturing organizations are expected to grow fastest at a 7.55% CAGR through 2031.

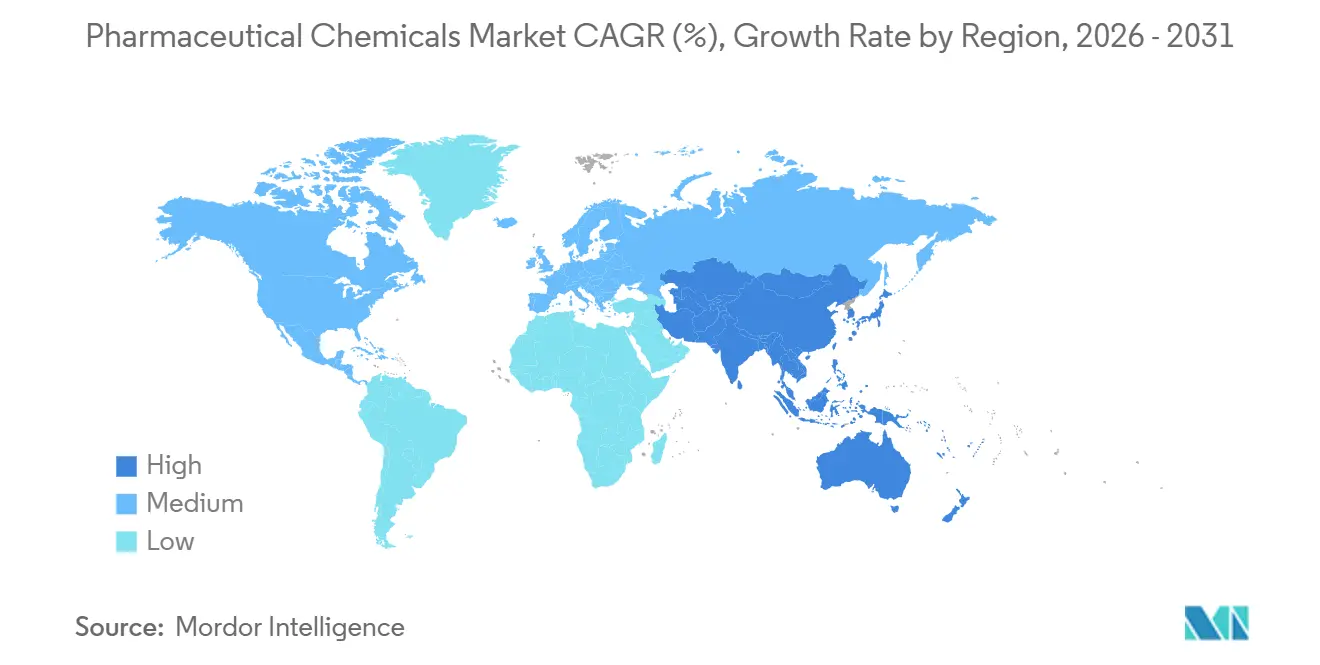

- By geography, North America held 38.95% share in 2025, while Asia-Pacific is projected to expand at a 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Chemicals Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising chronic disease burden and medicine demand | +1.6% | Global, with stronger pull in North America, Europe, and aging Asia-Pacific populations | Medium term (2-4 years) |

| Generic and biosimilar pipeline expansion | +1.0% | Asia-Pacific, especially India and South Korea, with spillover into Europe | Medium term (2-4 years) |

| Shift toward high-purity APIs and specialty intermediates | +0.8% | North America and Europe, with regulatory influence from FDA and EMA standards | Long term (≥ 4 years) |

| Supply chain de-risking through dual sourcing and onshoring | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Adoption of green chemistry and continuous manufacturing | +0.5% | Europe, North America, and selected Asia-Pacific hubs | Long term (≥ 4 years) |

| Growth in biologics, peptides, and oligonucleotide chemicals | +1.2% | North America and Europe, with India and Singapore expanding capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden and Medicine Demand

The pharmaceutical chemicals market thrives on the persistent demand driven by chronic diseases. Long-term treatments for conditions like cardiovascular diseases, diabetes, and cancer necessitate a consistent supply of active ingredients, intermediates, and formulation chemicals. As patients increasingly stay on therapies longer and often use multiple medications, the demand for tighter impurity controls, reliable synthesis, and consistent input materials has surged. Consequently, the market's growth is not just linked to rising prescriptions but also to the intricate nature of molecules and delivery systems in chronic care, spanning both traditional small molecules and advanced therapies.

Generic and Biosimilar Pipeline Expansion

The pharmaceutical chemicals market benefits from the expanding pipelines of generics and biosimilars as more products exit exclusivity. Generic launches bolster the demand for standard APIs and intermediates, while biosimilars expand the need for cell culture media, buffer salts, and specialty excipients. This growth isn't merely a result of off-patent small molecules. In 2025, Aurobindo Pharma’s CuraTeQ biosimilars division received U.S. FDA approvals in oncology and immunology, with 15 products advancing through 2030, highlighting the rising demand for regulated biologics-related chemical inputs. The market capitalizes on the vast demand for generics and the specialized chemical needs of biosimilar development, benefiting suppliers in India and other export hubs, even as clients reevaluate sourcing and regional supply resilience.

Shift Toward High-Purity APIs and Specialty Intermediates

The pharmaceutical chemicals market is shifting towards high-value supplies, focusing on high-potency APIs, peptide synthesis, and specialized intermediates. Advanced oncology therapies and biologic products demand stringent handling and quality control, pushing suppliers to enhance process capabilities. A 2026 study highlighted that continuous flow API manufacturing can cut process mass intensity by 42%, reducing solvent use and energy consumption. Suppliers combining purity, safety, and efficiency are better positioned to succeed, as these factors increasingly determine qualification and retention in regulated supply chains.[2]American Chemical Society, “Insights into Flow and Continuous Systems in Pharmaceutical Manufacturing: Challenges and Opportunities,” Organic Process Research & Development, pubs.acs.org

Supply Chain De-Risking Through Dual Sourcing and Onshoring

The pharmaceutical chemicals market is pivoting towards dual sourcing, regional redundancy, and domestic manufacturing. The industry remains heavily reliant on imported APIs and starting materials, even with production near end markets. In 2025, the API Innovation Center revealed that over 80% of the top 100 generic medicines in the U.S. lacked a domestic API source, highlighting upstream supply concentration.[3]API Innovation Center, “Building a Resilient Domestic Drug Supply Chain,” API Innovation Center, apicenter.org The Strategic Active Pharmaceutical Ingredients Reserve bolstered domestic sourcing and stock security, reinforcing the case for local API and intermediate capacity. Procurement strategies now prioritize resilience, favoring suppliers with approved facilities, regional manufacturing, and reliable delivery of critical molecules.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| GMP and DMF compliance burden across jurisdictions | -0.8% | Global, with the strongest pressure in North America and Europe | Medium term (2-4 years) |

| Raw material concentration and trade volatility | -1.0% | Asia-Pacific centered, with spillover into Europe, North America, and MEA | Short term (≤ 2 years) |

| High capex and environmental compliance costs | -0.6% | Global, with a higher burden on European manufacturers | Long term (≥ 4 years) |

| Price erosion in commoditized intermediates and solvents | -0.7% | Asia-Pacific, with pressure extending into Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GMP and DMF Compliance Burden Across Jurisdictions

The pharmaceutical chemicals market faces significant regulatory challenges, particularly for suppliers operating across multiple regions. Companies must continuously manage documentation, process validation, site readiness, audits, and change controls under varying regulatory frameworks. Meeting FDA standards, European regulations, and customer-specific quality benchmarks simultaneously often benefits larger manufacturers with dedicated quality teams and resources for repeated inspections. This has led to a shrinking pool of globally qualified suppliers in regulated categories, slowing new supplier entry despite strong demand. Smaller producers, burdened by GMP and DMF compliance requirements, often struggle to expand into higher-value segments.

Raw Material Concentration and Trade Volatility

The market is constrained by the concentration of key starting materials and upstream inputs in a few countries, increasing exposure to trade disruptions, shipping delays, inventory fluctuations, and cost volatility. In 2025, the API Innovation Center reported that 72% of FDA-approved API manufacturing facilities were located outside the U.S., emphasizing reliance on offshore capacities. Even with diversified downstream drug manufacturing, dependence on imported materials creates production inconsistencies, pricing pressures, and planning challenges. While resilience investments are essential, not all market participants can absorb the associated costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: APIs Anchor Revenue While Excipients Capture Emerging Modalities

In 2025, Active Pharmaceutical Ingredients (APIs) held a 44.45% share of the pharmaceutical chemicals market, maintaining their position as the leading chemical type. This dominance highlights their critical role in finished medicines and the premium placed on regulated, high-purity synthesis. Demand is particularly strong in biologics, oncology therapies, peptide drugs, and other complex treatment platforms requiring stringent controls and specialized processing. APIs remain the primary revenue driver, central to both innovator and generic manufacturing.

Excipients are the fastest-growing chemical type, with a projected CAGR of 6.99% from 2026 to 2031, reflecting the rising importance of delivery technologies. Growth is driven by advancements like lipid nanoparticle chemistry, essential for mRNA, gene therapy, and nucleic acid delivery. Evonik’s USD 220 million Lipid Innovation Center in Indiana, operational since 2025, and expanded lipid GMP manufacturing in Germany exemplify this trend. Intermediates, solvents, and reagents still hold a significant market share but face challenges from generic volume cycles and commodity pricing pressures.

By Therapeutic Area: Oncology Drives Value While Cardiovascular Demand Accelerates

Oncology accounted for 26.78% of the pharmaceutical chemicals market in 2025, making it the leading therapeutic area. This reflects the complexity of cytotoxic APIs, antibody-drug conjugate payloads, high-potency compounds, and targeted cancer therapies, which require specialized intermediates and dedicated manufacturing capabilities. Johnson & Johnson’s acquisition of Firefly Bio in 2026 to enhance its degrader antibody conjugate platform highlights continued investment in oncology-linked chemistry.

Cardiovascular is projected to grow at a 7.95% CAGR through 2031, driven by the increasing demand for peptide and metabolic disease treatments. The surge in GLP-1 receptor agonists is accelerating peptide API capacity and process chemistry development. Suppliers capable of supporting complex synthesis at scale under regulatory control are gaining prominence. While the market mix is becoming more specialized, areas like CNS, infectious diseases, and endocrinology continue to provide a broad demand base, ensuring activity across mature and emerging treatment categories.

By End User: Pharmaceutical Manufacturers Lead While CDMOs Gain Momentum

In 2025, Pharmaceutical Manufacturers held a 53.25% share of the pharmaceutical chemicals market, reflecting their direct procurement of APIs, excipients, solvents, and reagents for in-house manufacturing and finished dosage production. While large drug companies protect proprietary chemistry for patented molecules, many are outsourcing routine or capital-intensive synthesis to external partners, reshaping demand distribution.

Contract Manufacturing Organizations (CMOs) are expected to grow at a 7.55% CAGR from 2026 to 2031, driven by increased outsourcing of complex synthesis, development support, and regulated commercial manufacturing. Jubilant Pharmova’s API business transfer to Jubilant Biosys in 2025 and the establishment of a new CRDMO discovery facility in 2026 illustrate this trend. Biotechnology companies are also becoming key buyers, particularly for specialty lipids and small-batch materials for clinical production.

Geography Analysis

In 2025, North America led the pharmaceutical chemicals market with a 38.95% share, driven by strong demand for innovator drugs, high-quality standards, and efforts to boost domestic production of critical pharmaceutical inputs. Merck initiated a USD 3 billion, 400,000-square-foot Center of Excellence for Pharmaceutical Manufacturing in Elkton, Virginia, in October 2025. BASF launched a GMP Solution Center in Wyandotte, Michigan, in June 2025, focusing on pharmaceutical excipients and bioprocessing ingredients. Avantor expanded microbial and stability testing capabilities at its St. Louis site in April 2026. These developments highlight the region's focus on policy support and investment in manufacturing and quality services.

Europe ranked as the second-largest region in 2025, with Germany as the leading pharmaceutical chemicals hub. Germany secured 12 major pharmaceutical manufacturing contracts in 2025, attracting investments from U.S. and European drug companies for production expansions. BASF inaugurated its Zhanjiang Verbund site in China in March 2026 and launched world-scale menthol and linalool plants in Ludwigshafen in April 2026. Despite a 6% year-over-year decline in

Asia-Pacific is the fastest-growing region in the pharmaceutical chemicals market, with a projected 7.88% CAGR from 2026 to 2031. India plays a key role with its large generic API base, mature GMP capabilities, and growing presence in custom synthesis and biologics manufacturing. In 2026, Divi’s Laboratories allocated INR 2,500 crore (USD 300 million) for Kakinada expansion and new custom synthesis contracts, while Aurobindo Pharma launched its INR 1,200 crore (USD 145 million) TheraNym biologics contract manufacturing facility in Telangana. China is advancing in specialty pharmaceutical chemicals under environmental and GMP pressures, while Japan, South Korea, Singapore, and Australia focus on high-value biologics and advanced manufacturing systems. The Middle East, Africa, and South America, though smaller in scale, are expanding due to increased domestic production, biosimilar access, and public health initiatives.

Competitive Landscape

In the pharmaceutical chemicals market, a competitive landscape emerges: at the pinnacle, established global specialty chemical and CDMO companies reign, while a diverse array of regional API and intermediate producers populate the base. Here, competition at the upper echelons hinges not merely on price, but on compliance records, modality expertise, supply security, and the capacity for specialized synthesis. Conversely, many regional suppliers, especially those dealing in standard APIs and commoditized intermediates, predominantly vie on cost, scale, and local manufacturing advantages. This dynamic results in a market that's neither tightly concentrated nor entirely fragmented; leadership is more pronounced in high-specification categories than across the broader supply spectrum. Consequently, a strategic position in this market is heavily influenced by the ability to ascend the value chain.

Evonik strengthened its position through a September 2025 partnership with Ethris to enhance nucleic acid delivery offerings, integrating excipient capabilities with advanced therapeutic platforms. These strategic moves highlight how market leaders are prioritizing platform depth, specialized chemistry, and alignment with customer development needs. Companies focused on standard categories face tighter margins and reduced differentiation.

Key opportunities in the pharmaceutical chemicals market include domestic starting material capacities, integrated peptide and oligonucleotide platforms, and manufacturing systems emphasizing efficiency and sustainability. Buyers increasingly prefer suppliers offering validated quality systems, advanced process control, and regional manufacturing flexibility. This trend elevates the importance of approved facilities, inspection readiness, and the ability to support development and commercial supply within a unified network. The market is shifting toward a structure where top-tier players strengthen their positions in complex, regulated categories, while the broader supplier base remains fragmented and price-sensitive.

Pharmaceutical Chemicals Industry Leaders

BASF SE

Divi's Laboratories Limited

Lonza Group AG

Thermo Fisher Scientific Inc.

Sun Pharmaceutical Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Onco-Innovations Limited commenced process development and intermediate scale-up activities for A83B4C63, the active pharmaceutical ingredient in ONC010, as part of its chemistry, manufacturing, and controls strategy in preparation for IND-enabling studies and first-in-human clinical trials.

- June 2026: Axplora disclosed plans to consolidate ursodeoxycholic acid manufacturing at its Vizag site in India, with production transitioning from Gropello Cairoli, Italy, by the end of 2026.

- May 2026: BioDuro established a joint venture with Cenra API Solutions, also known as Chunghwa Chemical Synthesis & Biotech Co., Ltd., to expand commercial-scale API manufacturing capacity at Cenra’s Taipei campus in Taiwan.

- May 2026: CordenPharma acquired AmbioPharm, a U.S.-based peptide CDMO with facilities in South Carolina and China, to enhance global peptide API capacity and support its EUR 900 million (USD 1,038 million) peptide program.

- February 2026: Lonza announced the divestment of its Capsules & Health Ingredients business to Lone Star Funds for an enterprise value of CHF 2.3 billion (USD 3 billion). The proceeds will be allocated to expanding its biologics, peptide, and cell and gene therapy capacities.

Global Pharmaceutical Chemicals Market Report Scope

As per the scope of the market, pharmaceutical chemicals are the specialized raw materials used to create medicines. They include the active ingredients that treat diseases, and the supporting inactive materials that help deliver those drugs to the body safely.

The pharmaceutical chemicals market is segmented by chemical type, therapeutic area, end-user, and geography. By chemical type, the market includes active pharmaceutical ingredients, excipients, intermediates, and solvents & reagents. By therapeutic area, the market is categorized into oncology, cardiovascular, central nervous system, infectious diseases, endocrinology, respiratory, gastroenterology, dermatology, and other therapeutic areas. By end-user, the market is segmented into pharmaceutical manufacturers, biotechnology companies, contract manufacturing organizations, pharmaceutical R&D institutions, and chemical suppliers & distributors. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Active Pharmaceutical Ingredients |

| Excipients |

| Intermediates |

| Solvents and Reagents |

| Oncology |

| Cardiovascular |

| Central Nervous System |

| Infectious Diseases |

| Endocrinology |

| Respiratory |

| Gastroenterology |

| Dermatology |

| Other Therapeutic Areas |

| Pharmaceutical Manufacturers |

| Biotechnology Companies |

| Contract Manufacturing Organizations |

| Pharmaceutical R and D Institutions |

| Chemical Suppliers and Distributors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Chemical Type | Active Pharmaceutical Ingredients | |

| Excipients | ||

| Intermediates | ||

| Solvents and Reagents | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular | ||

| Central Nervous System | ||

| Infectious Diseases | ||

| Endocrinology | ||

| Respiratory | ||

| Gastroenterology | ||

| Dermatology | ||

| Other Therapeutic Areas | ||

| By End User | Pharmaceutical Manufacturers | |

| Biotechnology Companies | ||

| Contract Manufacturing Organizations | ||

| Pharmaceutical R and D Institutions | ||

| Chemical Suppliers and Distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for pharmaceutical chemicals demand through 2031?

The pharmaceutical chemicals market is projected to grow from USD 265.76 billion in 2026 to USD 364.11 billion by 2031 at a 6.50% CAGR, supported by supply security efforts, specialty chemistry demand, and outsourcing growth.

Which chemical type leads revenue today?

Active Pharmaceutical Ingredients led with a 44.45% revenue share in 2025, reflecting their central role in both innovator and generic medicine production.

Which therapeutic area is creating the strongest value pool?

Oncology held the largest share at 26.78% in 2025 because it depends on high-potency APIs, complex intermediates, and specialized payload chemistry.

Which therapeutic area is growing fastest?

Cardiovascular is projected to expand at a 7.95% CAGR through 2031, mainly because peptide and metabolic disease treatments are increasing demand for complex synthesis capacity.

Why are CDMOs gaining importance in this space?

Contract Manufacturing Organizations are forecast to grow at a 7.55% CAGR through 2031 as drug companies outsource more development, scale-up, and regulated manufacturing work.

Which region leads, and which region is growing fastest?

North America led with 38.95% share in 2025, while Asia-Pacific is projected to record the fastest growth at a 7.88% CAGR through 2031.

Page last updated on: