Pharmaceutical Caps And Closures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.80 Billion |

| Market Size (2031) | USD 13.80 Billion |

| Growth Rate (2026 - 2031) | 11.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Caps And Closures Market Analysis by Mordor Intelligence

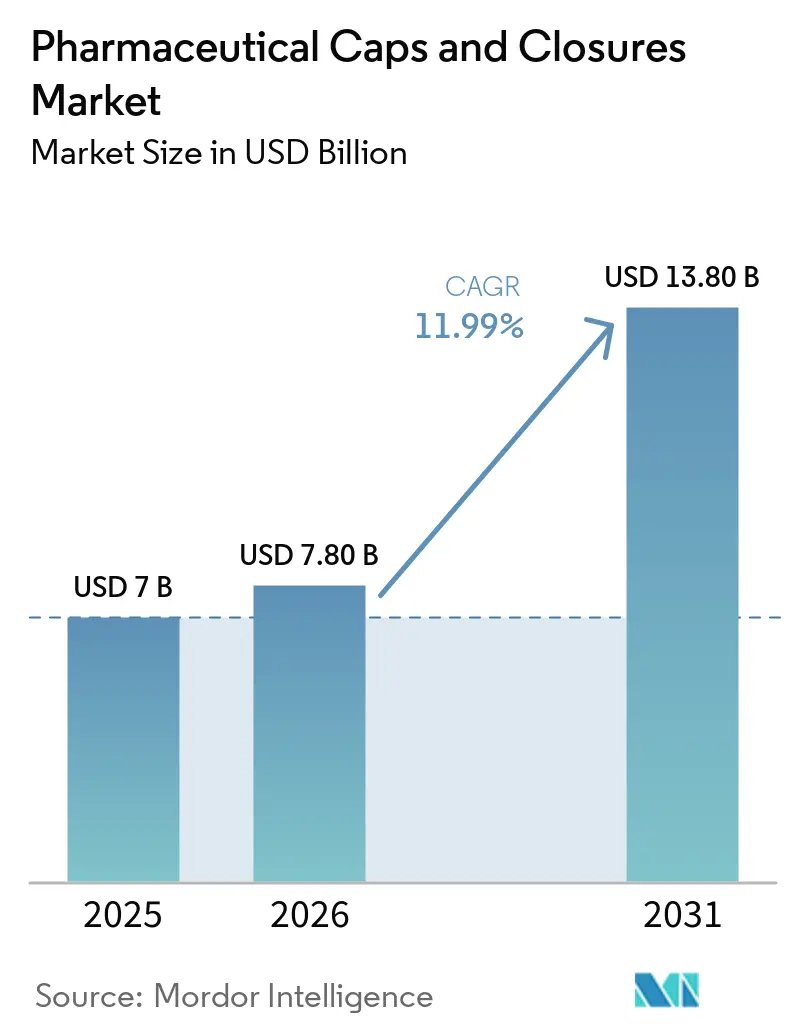

The Pharmaceutical Caps And Closures Market size is expected to grow from USD 7 billion in 2025 to USD 7.80 billion in 2026 and is forecast to reach USD 13.80 billion by 2031 at 11.99% CAGR over 2026-2031.

As demand surges for biologics and advanced injectables, the pharmaceutical caps and closures market is undergoing a transformation. This shift is driven by several factors: the push for upgrades in container-closure integrity following the EU GMP Annex 1 revision, and the rapid scaling up of prefilled systems. High-value elastomeric components are experiencing strong momentum, accompanied by significant investments in ready-to-use (RTU) formats. Stricter child-resistance regulations are further driving capital toward premium closure technologies. However, manufacturers face challenges such as fluctuating raw material prices and stricter limits on extractables and leachables (E&L), which are forcing them to redesign formulations while maintaining profitability. Amid these dynamics, established suppliers with accredited testing capabilities and extensive patent portfolios are consolidating their market share, while smaller players struggle with the high costs of validation. Given this interplay of demand and supply factors, the pharmaceutical caps and closures market is positioned for sustained double-digit growth through the decade's end.

Key Report Takeaways

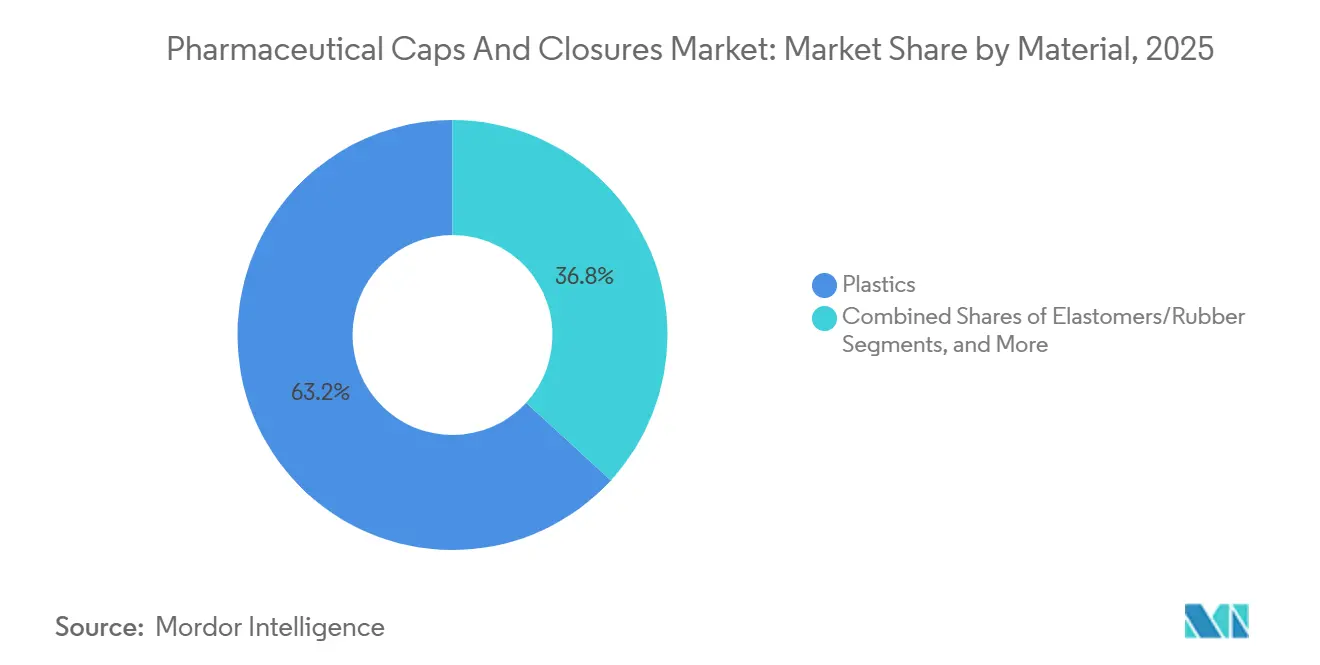

- By material, plastics held 63.18% of the pharmaceutical caps and closures market share in 2025, while elastomers are projected to record the fastest 13.87% CAGR to 2031.

- By closure type, seals led with 28.71% revenue share of the pharmaceutical caps and closures market size in 2025; syringe and cartridge components are forecast to expand at a 13.17% CAGR to 2031.

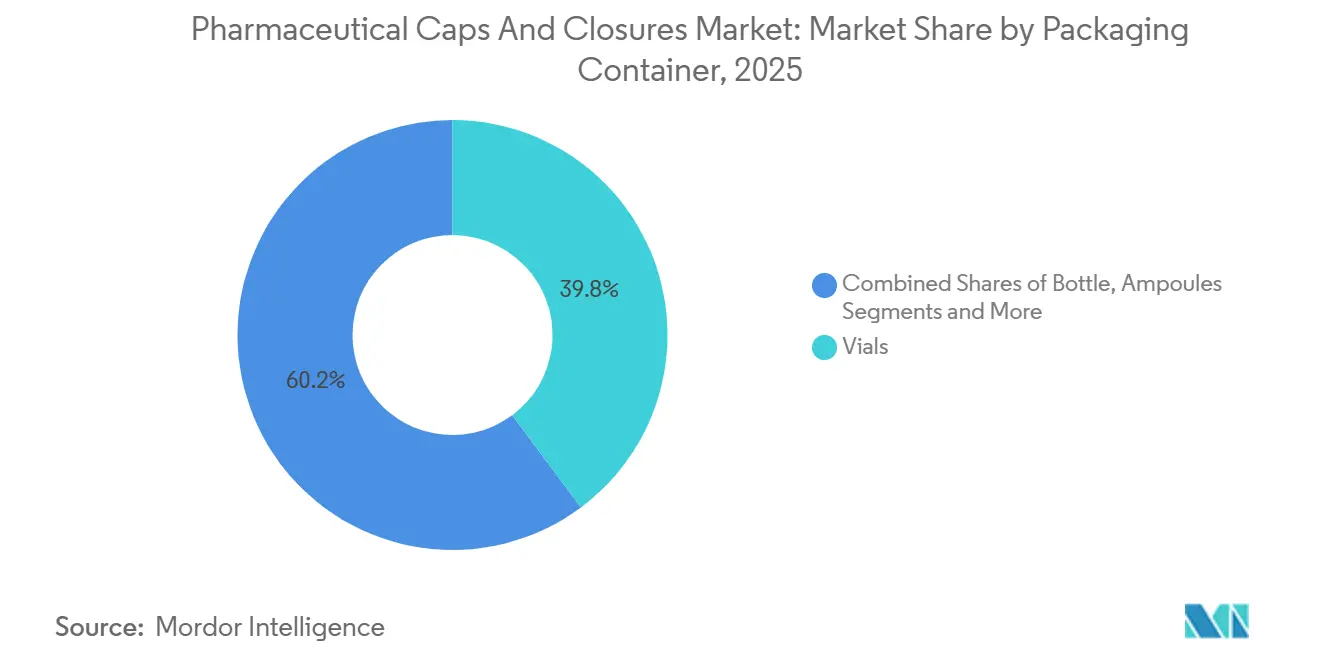

- By packaging container, vials accounted for 39.81% of the pharmaceutical caps and closures market revenue in 2025, whereas prefilled syringes are advancing at a 13.66% CAGR to 2031.

- By geography, North America commanded 35.18% of the pharmaceutical caps and closures market revenue in 2025; Asia-Pacific is projected to grow the fastest at a 14.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Caps And Closures Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growth of biologics and injectables elevates demand for vial stoppers, seals, and syringe/cartridge closures | 3.2% | Global, with concentration in North America and Europe for originator biologics; Asia-Pacific for biosimilars | Medium term (2-4 years) |

| Stricter child-resistant and tamper-evident mandates increase CRC/TE closure adoption | 1.8% | North America and EU; emerging enforcement in APAC markets | Short term (≤ 2 years) |

| Expansion of ready-to-use sterile components for aseptic fill-finish boosts RTU closures | 2.9% | Global, led by North America and Europe; APAC adoption accelerating | Medium term (2-4 years) |

| Shift to self-administration/home care raises need for user-friendly dosing and ophthalmic/nasal closures | 2.1% | North America and Europe for chronic-disease management; APAC for diabetes and respiratory therapies | Long term (≥ 4 years) |

| EU GMP Annex 1 2022 drives container closure integrity upgrades and CCIT adoption | 2.5% | Europe (mandatory); North America and APAC (voluntary best practice) | Medium term (2-4 years) |

| Ultra-cold/cryogenic storage for ATMPs requires next-gen elastomer/laminated closures | 1.4% | North America and Europe for cell/gene therapies; limited APAC penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biologics Drive Surge in Demand for Vial Stoppers, Seals, and Syringe Closures

In 2025, biologics accounted for a significantly larger share of closure value compared to volume, driving a 20.3% year-on-year increase in high-value component revenue for West Pharmaceutical Services, surpassing the company's overall sales growth.[1]Draft Guidance on Nitrosamine Impurities, U.S. Food and Drug Administration, fda.gov GLP-1 receptor agonists alone contributed 10% to West's total enterprise revenue, demonstrating the substantial impact of a single drug class on closure demand. Larger-format vials and cartridges for biologics present challenges during freeze-thaw cycles, as conventional butyl stoppers fail to address thermal-expansion mismatches. West's FluroTec-coated stoppers addressed this issue by achieving a thermal-expansion delta of under 5 ppm/°C and reducing leak rates by 40% during cryogenic validation. This innovation enabled West to ship 43 billion components in 2025 at premium pricing. As pipeline biologics progress through late-stage trials, the demand for high-quality stoppers, seals, and plungers is expected to drive significant growth in the pharmaceutical caps and closures market.

Stricter Regulations Boost Adoption of Child-Resistant and Tamper-Evident Closures

In January 2024, the U.S. Consumer Product Safety Commission revised regulations, increasing the failure rate threshold for children attempting to open packages from 80% to 85% within five minutes.[2]Draft Guidance on Chemical Characterization of Medical Device Materials, U.S. Food and Drug Administration, fda.gov Simultaneously, ISO 8317 standards in Europe mandated tamper-evident features for all oral solid-dose prescription containers. These regulatory changes are accelerating the adoption of integrated CRC/TE closures, such as those offered by Aptar and Berry Global. Non-compliant packaging now faces recalls and distribution bans, emphasizing the importance of compliance. Additionally, FDA guidance in 2025 identified CRC validation delays as a factor contributing to drug shortages. Consequently, pharmaceutical companies are increasingly partnering with vendors offering pre-validated portfolios, strengthening the position of established players and driving the adoption of CRC/TE features in the pharmaceutical caps and closures market.

Surge in Ready-to-Use Sterile Components for Aseptic Fill-Finish Fuels Demand for RTU Closures

SCHOTT Pharma initiated operations at a EUR 100 million RTU cartridge facility in Hungary in June 2025, catering to Annex 1-compliant fill-finish sites.[3]SCHOTT Pharma Invests Over EUR 100 Million in RTU Cartridge Facility in Hungary, SCHOTT Pharma, schott.com The company’s newly launched TOPPAC polymer cartridge, introduced in August 2025, reduces CO₂ emissions by 58% compared to glass while meeting stringent particulate limits. West Pharmaceutical identified approximately 700 Annex 1 remediation projects globally, with only 15% completed by early 2026. By eliminating the need for depyrogenation lines, RTU barriers reduce contamination risks and significantly shorten cycle times. Datwyler’s NeoFlex plungers and West’s NovaPure stoppers, featuring FluroTec coatings, offer low extractables, minimal particulates, and gamma-sterilization compatibility—key factors driving the rapid adoption of RTU solutions in the pharmaceutical caps and closures market.

Growing Trend of Self-Administration Elevates Demand for Intuitive Dosing and Nasal/Ophthalmic Closures

Aptar’s e-Lockout nasal spray combines child resistance with Bluetooth-enabled dose tracking, aligning with the increasing shift toward patient-controlled therapies. Nemera’s Novelia ophthalmic platform ensures sterility for 60 days after opening without the use of preservatives, complying with new EU guidelines discouraging benzalkonium chloride. The FDA's 2025 draft guidance on human factors engineering requires usability validation with at least 15 representative users for each critical task, driving the development of closure designs that prioritize ergonomic access while minimizing misuse. The growing adoption of connected, single-dose, and preservative-free formats underscores the evolving role of closures as active interfaces rather than passive barriers in the pharmaceutical caps and closures market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| E&L and CCIT compliance complexity increases validation costs/time-to-market | -1.9% | Global, with heightened impact in North America and Europe due to stringent regulatory frameworks | Medium term (2-4 years) |

| Raw material (butyl rubber, aluminum) price volatility pressures margins | -1.5% | Global, with acute impact in regions dependent on imported feedstocks (Europe, Asia-Pacific) | Short term (≤ 2 years) |

| Blow-fill-seal integration can reduce use of separate closures in select liquid formats | -0.8% | North America and Europe for sterile ophthalmics and injectables; limited APAC adoption | Long term (≥ 4 years) |

| Nitrosamine risk management constrains elastomer choices and supply flexibility | -1.3% | Global, driven by FDA and EMA regulatory enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E&L and CCIT Compliance Complexity Increases Validation Costs/Time-to-Market

Comprehensive E&L studies on a single closure-container pair can cost over USD 30,000, while method development may delay approval timelines by up to a year. The FDA's 2024 draft guidance mandates quantitative risk assessments for all patient-contacting materials, significantly increasing the E&L burden. Furthermore, ICH Q3E, set for release in 2025, lowers the daily genotoxic leachable threshold to 1.5 µg, requiring reformulation of legacy elastomers. Deterministic CCIT methods, such as laser headspace analysis, demand capital investments nearing USD 500,000, along with annual calibration costs. These challenges force smaller firms to weigh the high costs of in-house laboratories against extended outsourced timelines, potentially restricting growth in the pharmaceutical caps and closures market.

Raw Material (Butyl Rubber, Aluminum) Price Volatility Pressures Margins

In 2026, aluminum ingot prices increased to USD 2,550 per tonne, driven by U.S. tariffs that doubled from 25% to 50% between March and June 2025. This price surge is reflected in West Pharmaceutical's 36.2% gross margin in 2025, highlighting the strain of rising costs against fixed-price supply agreements with large drug manufacturers. Similarly, fluctuations in isobutylene feedstocks for butyl rubber compel elastomer suppliers to renegotiate contracts or absorb margin erosion. This volatility hampers capacity expansion and reduces long-term price visibility in the pharmaceutical caps and closures market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastics Lead the Charge, Fueled by Surge in Prefilled Syringes

In 2025, plastics accounted for 63.18% of the pharmaceutical caps and closures market revenue, with a projected compound annual growth rate (CAGR) of 13.87% through 2031. The industry's shift toward cyclic olefin polymer and polypropylene barrels for prefilled syringes has driven demand for compatible plastic caps, backstops, and plunger rods. SCHOTT’s TOPPAC polymer syringe, introduced in January 2025, reduces carbon emissions by 58% compared to glass alternatives. It is also compatible with SHL Medical’s Maggie autoinjector, which has accelerated its adoption among biologic drug manufacturers. Elastomers remain essential for high-barrier applications, such as lyophilized biologics and vaccines requiring a five-year shelf life, relying on butyl-based stoppers with fluoropolymer laminates. Datwyler’s NeoFlex and West’s FluroTec product lines demonstrate the balance between controlling extractables and managing oxygen transmission.

By Closure Type: Seals Reign Supreme, Yet Syringe Components are on the Rise

In 2025, seals represented 28.71% of the revenue in the pharmaceutical caps and closures market, reflecting their widespread use across vial formats. However, syringe and cartridge components are anticipated to grow at the fastest rate, with a 13.17% CAGR projected through 2031, driven by the increasing prevalence of self-administration and larger-volume biologic injections. A syringe launched in January 2026 integrates a rubber plunger with a polypropylene backstop, simplifying assembly during the fill-finish process. Universal plungers align with the industry's transition to higher-dose autoinjectors, particularly for GLP-1 and obesity therapeutics. Advances in coating technologies are also gaining momentum. Silicone-free plungers eliminate sub-visible particles associated with syringe lubricants, offering a significant advantage for cell therapies sensitive to immune activation. Additionally, as deterministic CCIT becomes more prevalent, aluminum seals with laser-inscribed 2D codes enable 100% in-line verification, enhancing traceability. These innovations ensure that seals maintain their market significance, even as syringe components capture a growing share.

By Packaging Container: Vials Hold Steady, But Prefilled Syringes are Gaining Momentum

In 2025, vials accounted for 39.81% of the packaging-container revenue, driven by their versatility in applications such as lyophilized biologics, vaccines, and sterile injectables. However, prefilled syringes are expected to grow at a 13.66% CAGR, supported by the increasing adoption of home-care biologics and more efficient hospital workflows. Syringes showcased in 2026 feature pre-installed plungers and a nest-and-tub delivery system that reduces changeover times by 30%, strengthening the economic case for prefilled lines. Cartridge demand is also rising, fueled by their use in diabetes and growth-hormone pens. In February 2024, a 1.5 mL cartridge plunger was introduced, designed for insulin analogs, GLP-1 combinations, and dual-hormone systems. These shifts in container preferences are expected to continuously reallocate revenue streams within the pharmaceutical caps and closures market, benefiting suppliers adept at aligning closure and container co-development.

Geography Analysis

In 2025, North America commanded a dominant 35.18% share of the pharmaceutical caps and closures market revenue, driven by the U.S.'s leadership in biologic R&D and strict enforcement of CCIT. The FDA's nitrosamine guidance, introduced in September 2024, along with ongoing discussions on Annex 1 harmonization, indicates sustained demand for validated closures well beyond 2028. Canada's Biologics and Genetic Therapies Directorate, along with Mexico's growth in near-shoring, is contributing incremental volumes, with Mexico benefiting from shorter lead times compared to Asia.

Europe, ranking second, is propelled by the adoption of ready-to-use solutions and green packaging mandates. A new RTU cartridge facility in Hungary, expected to become operational in 2027, is set to support EU Annex 1 upgrades in Germany, France, and Italy. Germany's strong contract-development sector is driving elastomer demand. Meanwhile, post-Brexit regulatory divergence requires suppliers to validate under both EMA and MHRA standards, extending timelines but increasing service revenues. Biosimilar clusters in Southern Europe, particularly in Spain and Italy, are consuming stoppers and seals at growth rates exceeding GDP, highlighting the region's significant influence on the pharmaceutical caps and closures market.

Asia-Pacific is a standout region, with an anticipated annual growth rate of 14.19% through 2031, fueled by the expansion of biosimilar production in China and India and greenfield investments in Southeast Asia. China's NMPA has streamlined review processes for imported closure systems meeting ICH Q3E standards, reducing entry barriers for premium suppliers. India's export-driven pharmaceutical sector, targeting USD 130 billion by 2030, increasingly demands compliance with FDA and EMA standards, favoring globally certified closure platforms. Although Australia's market is smaller, its enforcement of TGA nitrosamine limits, aligned with European standards, is pushing suppliers toward harmonized formulations.

Competitive Landscape

The pharmaceutical caps and closures market is moderately concentrated. Global players like West Pharmaceutical, SCHOTT Pharma, Gerresheimer, Stevanato Group, Aptar, Datwyler, and Berry Global maintain accredited laboratories and established validation pipelines, resulting in high switching costs. A September 2024 alliance among SCHOTT Pharma, Gerresheimer, and Stevanato to standardize RTU modules highlights collaborative strategies that strengthen these incumbents against regulatory challenges. Patent portfolios are a significant competitive advantage: West's portfolio, with over 800 active patents in elastomeric coatings and fluoropolymer barriers, effectively deters late entrants from replicating its innovations.

Innovation niches continue to offer profitable opportunities. Gore’s silicone-free plunger technology addresses a critical particulate issue in high-value cell therapies. Similarly, Aptar’s connected CRC devices integrate digital adherence into packaging. Material suppliers are also expanding downstream; for example, Datwyler now provides comprehensive CCIT consulting, combining elastomer solutions with testing services. Despite moderate consolidation, regional specialists remain competitive by customizing batches for niche orphan drugs and adhering to local regulatory requirements. While customer risk concentration limits bargaining power, the top five players account for approximately 55-60% of global revenue, indicating potential for further consolidation.

Pharmaceutical Caps And Closures Industry Leaders

AptarGroup, Inc.

Berry Global Group, Inc.

West Pharmaceutical Services, Inc.

Gerresheimer AG

Bormioli Pharma S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Aptar Closures partnered with Cheer Pack North America to integrate SureSnap elastomeric flow-control valves into Cheer Pack’s new SqueezeNSip spout, guaranteeing leak-free dispensing for single-serve medications.

- November 2025: Zydus Lifesciences and SIG launched single-serve spouted pouches featuring the tethered StrawCap 30 Linked and the SIG Motion Servo 3.2 filling line for liquid cough and cold medications.

- October 2025: Guala Closures agreed to acquire KWK Kunststoffwerk Kremsmünster, adding precision dosing caps for pharmaceutical and nutraceutical markets.

Global Pharmaceutical Caps And Closures Market Report Scope

As per the scope of the report, pharmaceutical caps and closures, including screw caps, pumps, and stoppers, serve as specialized sealing devices for primary pharmaceutical packaging like bottles, vials, and tubes. These closures safeguard medicines from contaminants, humidity, and leakage. They also ensure accurate dosages, provide tamper evidence, and enhance child safety. Commonly made from materials such as polypropylene (PP), polyethylene (PE), or aluminum, these closures often undergo sterilization, especially for parenteral applications.

The pharmaceutical caps and closures market is segmented by material, closure type, packaging container, and geography. By material, the market includes plastics, elastomers/rubber, and metals (e.g., aluminum seals). By closure type, it is segmented into stoppers, seals, caps, syringe and cartridge components, dropper and dispensing closures, and ports and IV closure systems. By packaging container, the categories include bottles, vials, ampoules, prefilled syringes, cartridges, and IV bags/containers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Plastics |

| Elastomers/Rubber |

| Metals (Aluminum seals) |

| Stoppers |

| Seals |

| Caps |

| Syringe & Cartridge Components |

| Dropper & Dispensing Closures |

| Ports & IV Closure Systems |

| Bottles |

| Vials |

| Ampoules |

| Prefilled Syringes |

| Cartridges |

| IV Bags/Containers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Plastics | |

| Elastomers/Rubber | ||

| Metals (Aluminum seals) | ||

| By Closure Type | Stoppers | |

| Seals | ||

| Caps | ||

| Syringe & Cartridge Components | ||

| Dropper & Dispensing Closures | ||

| Ports & IV Closure Systems | ||

| By Packaging Container | Bottles | |

| Vials | ||

| Ampoules | ||

| Prefilled Syringes | ||

| Cartridges | ||

| IV Bags/Containers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the pharmaceutical caps and closures market be by 2031?

The pharmaceutical caps and closures market size is projected to reach USD 13.8 billion by 2031, expanding from USD 7.8 billion in 2026 at an 11.9% CAGR.

Which material segment is growing the fastest in caps and closures?

Plastics are the fastest-growing material, expected to compound at 13.87% through 2031 on the back of prefilled-syringe expansion.

What drives demand for RTU closures?

EU GMP Annex 1 upgrades and aseptic fill-finish efficiency gains are propelling RTU adoption worldwide, especially in North America and Europe.

Which region will see the quickest growth?

Asia-Pacific is forecast to grow at 14.19% annually to 2031, fueled by biosimilar scale-up in China and India.

How are child-resistant mandates affecting closure design?

Stricter U.S. and EU protocols now favor integrated CRC/TE systems, pushing drug makers to source pre-validated solutions to avoid recalls.

What role do ultra-cold therapeutics play?

Advanced therapies requiring -80 °C storage are spawning next-gen elastomer and laminated closures that preserve seal integrity under cryogenic stress.

Page last updated on: