Germany Pharmaceutical Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

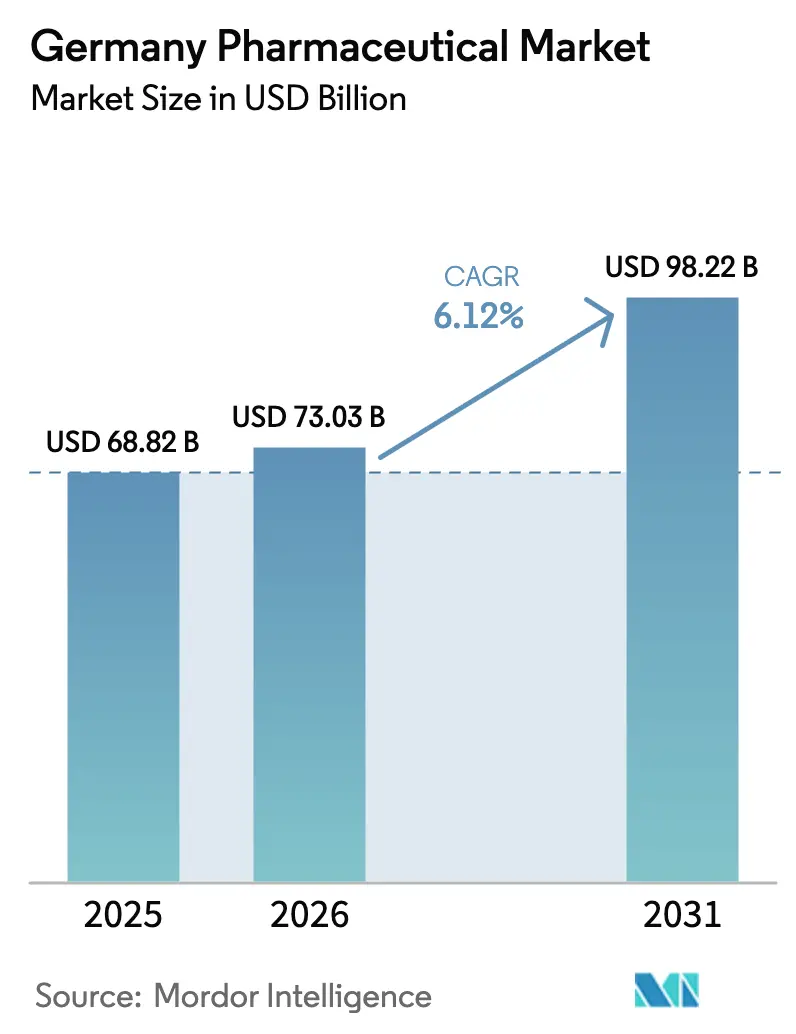

| Base Year Market Size (2025) | USD 68.82 Billion |

| Market Size (2026) | USD 73.03 Billion |

| Market Size (2031) | USD 98.22 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

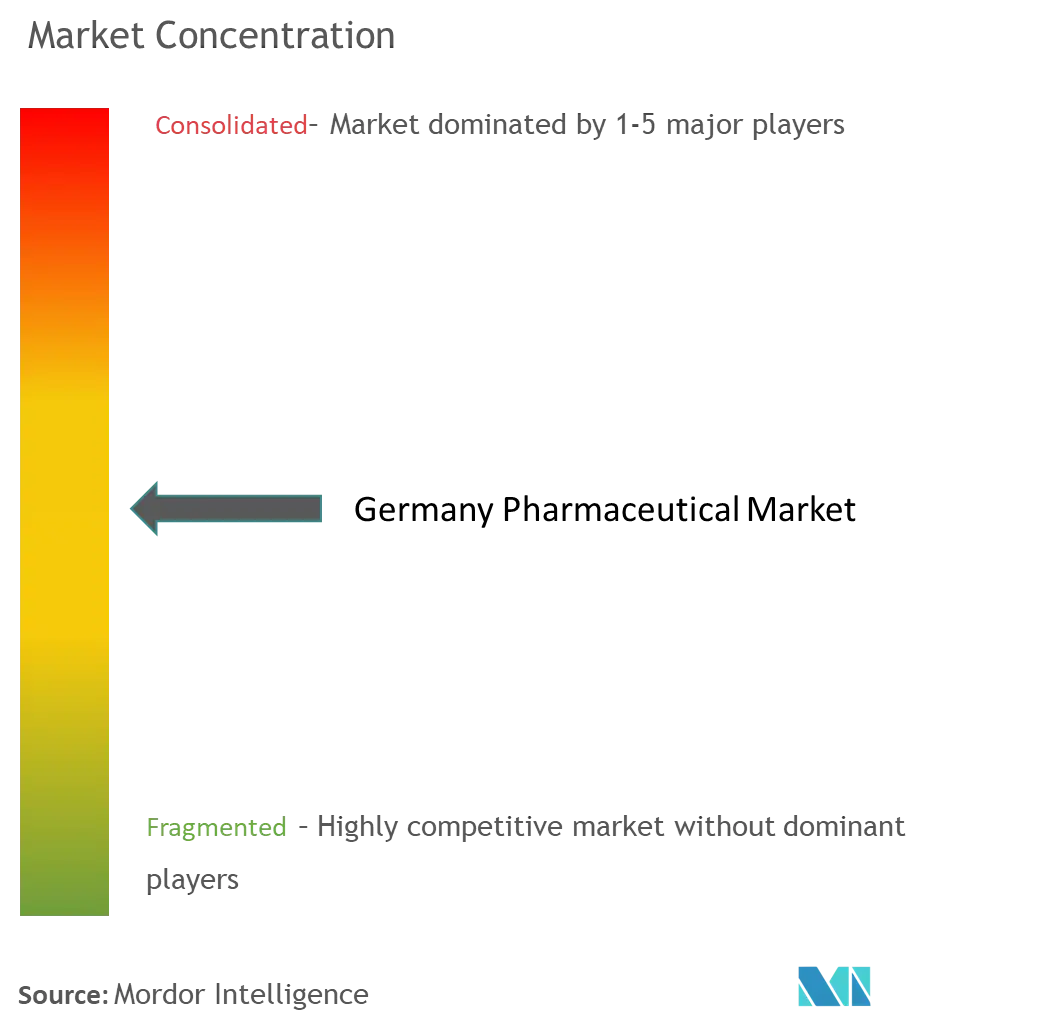

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Pharmaceutical Market Analysis by Mordor Intelligence

Germany Pharmaceutical Market size in 2026 is estimated at USD 73.03 billion, growing from 2025 value of USD 68.82 billion with 2031 projections showing USD 98.22 billion, growing at 6.12% CAGR over 2026-2031.

Rapid population aging, strong biopharmaceutical investment, and targeted government programs—such as the Medical Research Act and the nationwide electronic-prescription rollout—anchor long-term expansion. Scalability in biologics, swift uptake of GLP-1 obesity drugs, and early deployments of AI in clinical development collectively reinforce Germany’s position as Europe’s largest and the world’s fourth-largest medicine market. Competitive intensity grows as multinational suppliers increase local production and local champions pursue mRNA consolidation, while digital health tools lift prescription adherence and channel flexibility across the Germany pharmaceutical market. At the same time, AMNOG price negotiations, persistent skilled-labour gaps, and fragile API imports introduce margin pressure that firms must navigate through manufacturing automation and near-shoring strategies.

Key Report Takeaways

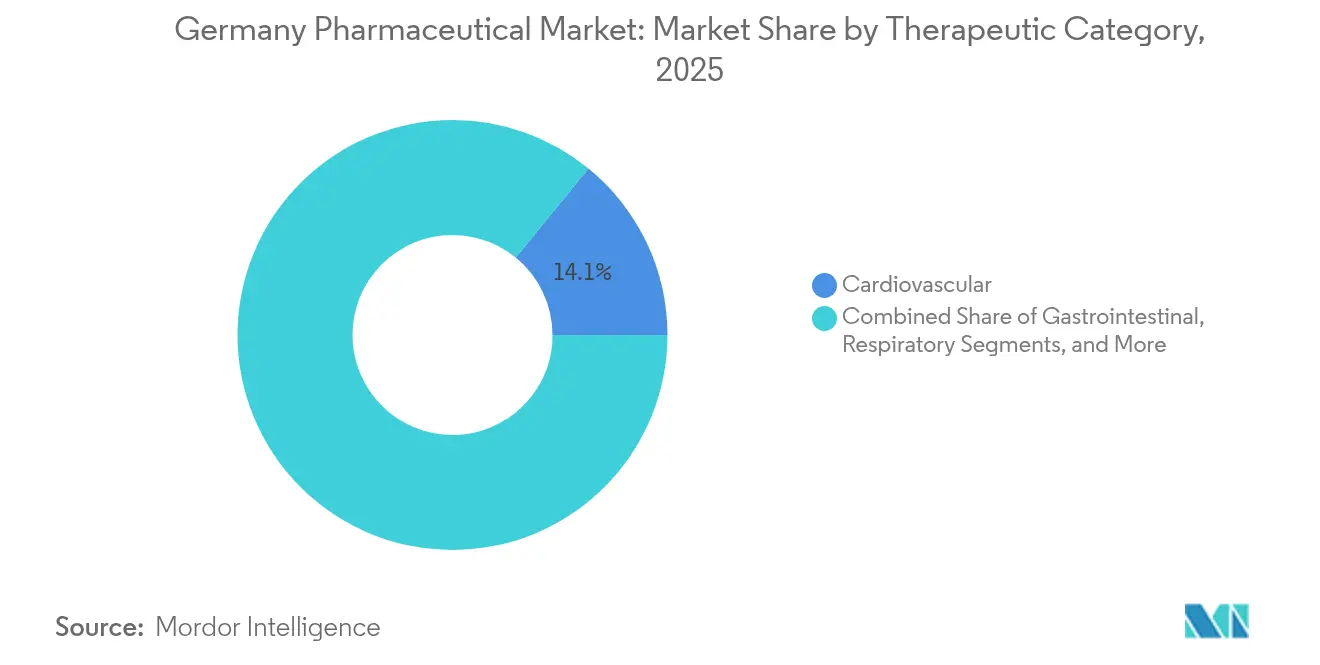

- By therapeutic category – Cardiovascular drugs led with 14.10% of Germany pharmaceutical market share in 2025; dermatological products are forecast to expand at a 6.72% CAGR through 2031.

- By drug type – Prescription medicines accounted for 86.55% of Germany pharmaceutical market size in 2025, while over-the-counter items post the strongest 6.65% CAGR to 2031.

- By molecule type – Small molecules held 66.90% Germany pharmaceutical market share in 2025; biologics are set to grow at 6.90% CAGR to 2031.

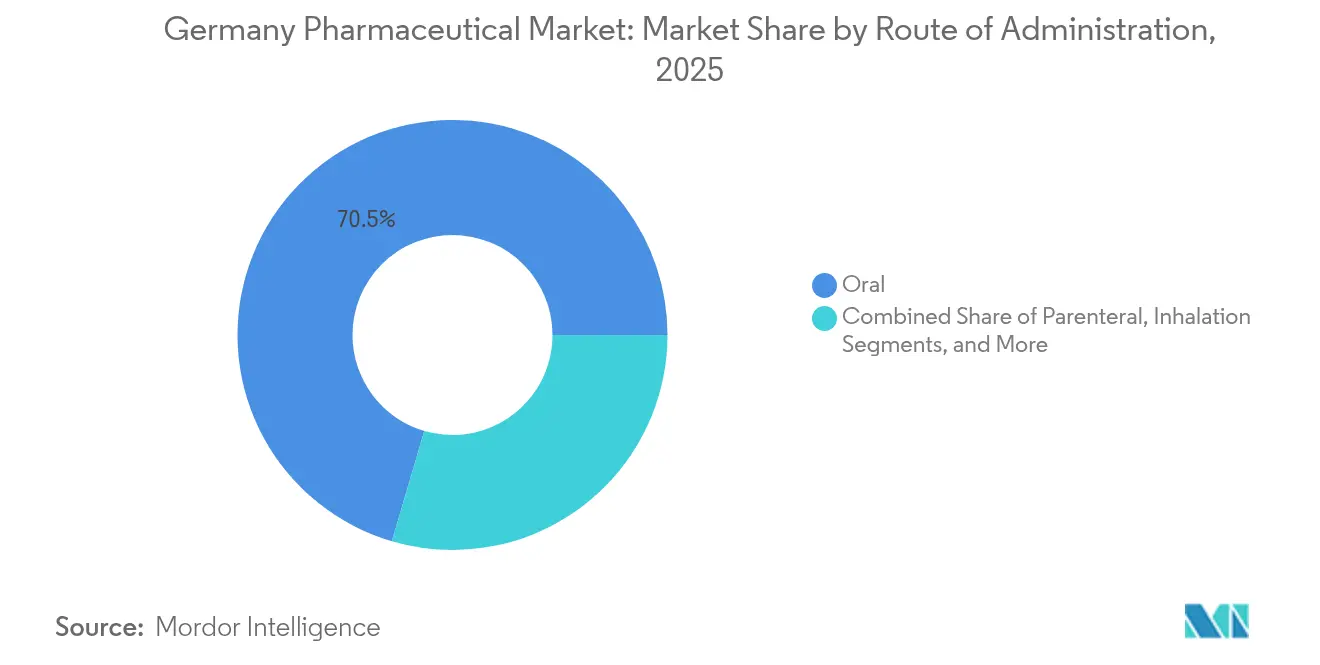

- By route of administration – Oral formulations represented 70.45% of Germany pharmaceutical market size in 2025; parenteral delivery is rising at 6.78% CAGR.

- By distribution channel – Hospital pharmacies captured 45.70% Germany pharmaceutical market share in 2025, whereas online pharmacies will advance at a 6.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Pharmaceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in biopharmaceutical production capacity | +1.8% | Berlin, Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Rapid uptake of GLP-1 obesity drugs | +1.2% | Urban centers | Short term (≤ 2 years) |

| AI-enabled clinical-trial optimization | +0.9% | University medical hubs nationwide | Medium term (2-4 years) |

| Growth of personalized-medicine companion Dx | +0.7% | Oncology centers | Long term (≥ 4 years) |

| Hospital budget expansion under GKV-FinStG | +0.6% | Level 1i hospitals nationwide | Short term (≤ 2 years) |

| Near-term biosimilar patent cliffs | +0.4% | High-cost therapy areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in biopharmaceutical production capacity

An unprecedented wave of facility expansion is reshaping the Germany pharmaceutical market. Eli Lilly’s EUR 2.3 billion Alzey campus, Wacker Biotech’s EUR 100 million mRNA hub in Halle, and Merck KGaA’s EUR 300 million antibody center in Darmstadt collectively add large-scale capacity for complex biologics [1]Germany Trade & Invest, “Pharmaceutical Industry in Germany,” gtai.de. These projects align with biosimilar patent expiries, letting domestic plants win originator and follow-on volumes while strengthening supply autonomy. The clustering of talent and infrastructure around Berlin, Bavaria, and North Rhine-Westphalia further draws global contract-development work to Germany pharmaceutical market leaders.

Rapid uptake of GLP-1 obesity drugs

Wegovy’s 2023 entry marked a pivotal shift, with German statutory insurers reimbursing the therapy at EUR 79 monthly—far below United States pricing—and electronic prescriptions lifting adherence from 75–80% to 94% [2]Smartpatient GmbH, “eRezept Adoption Statistics 2024,” smartpatient.eu. Urban clinics now integrate GLP-1 agents into cardiometabolic care bundles, broadening revenue pools inside the Germany pharmaceutical market beyond traditional diabetes indications and reinforcing the nation’s digital-health lead.

AI-enabled clinical-trial optimization

Policy makers incorporated AI modules into the National Pharma Strategy, trimming protocol-approval times and improving recruitment efficiency. More than 200 digital health applications secured reimbursement status by 2024, supplying real-world evidence that accelerates precision-medicine studies. A nationwide electronic patient record by 2025 will feed richer data to trial-design engines, helping sponsors cut cycle times and directing additional global R&D budgets toward the Germany pharmaceutical market.

Growth of personalized-medicine companion diagnostics

Over 200 targeted therapies with embedded genetic tests were approved in Germany by 2024, most in oncology. Confidential pricing under the Medical Research Act allows manufacturers to monetize high-value Dx-drug bundles, while university hospitals validate CRISPR-based gene therapies for hemato-oncology. As electronic health records link genomic with outcome data, payers refine value-based formulas that reward clinical precision and encourage new entrants to the Germany pharmaceutical industry.

Hospital budget expansion under GKV-FinStG

The 2025 statutory-insurance financing law raises capital allocations for Level 1i hospitals, letting them procure costlier biologics and digital therapeutics more readily. Procurement teams channel fresh funds to comprehensive stroke and cancer centers, benefiting high-complexity suppliers and boosting near-term volumes across the Germany pharmaceutical market.

Near-term biosimilar patent cliffs

Epoetin alfa, trastuzumab, and adalimumab clones are converging on expiry windows that promise procurement savings. Domestic manufacturers can seize share quickly, and payers expect savings to redeploy toward first-in-class therapies, reinforcing a diversified but balanced growth path for the Germany pharmaceutical market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AMNOG price-cut intensification | -1.4% | National, innovative brands | Medium term (2-4 years) |

| Skilled-labour shortage in biomanufacturing | -0.8% | Specialized clusters | Long term (≥ 4 years) |

| Supply-chain exposure to U.S. IRA export rules | -0.6% | Firms with U.S. inputs | Medium term (2-4 years) |

| Data-privacy limits on RWD linkage | -0.4% | Digital health sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AMNOG price-cut intensification

AMNOG negotiations now lean on domestic cost-effectiveness files instead of broader European referencing, deepening rebate demands on novel drugs. Payers predict confidential rebates may add EUR 840 million in first-year costs, prompting steeper claw-backs in later rounds. Oncology and rare-disease developers inside the Germany pharmaceutical market must craft stronger outcomes dossiers or risk margin compression.

Skilled-labour shortage in biomanufacturing

Five hundred thirty-two thousand skilled vacancies persisted nationwide in 2024, with 80% of biopharma firms citing hiring delays. Process-development and QC talent scarcity lifts wage inflation by 25% since 2020, slowing scale-up timelines for new biologic lines. Unless automation quickens, production may drift to countries with deeper bioprocess talent pools, tempering long-run capacity gains in the Germany pharmaceutical market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Category: Cardiovascular dominance faces dermatological disruption

Cardiovascular agents captured 14.10% Germany pharmaceutical market share during 2025, led by integrated antihypertensive-diabetes protocols that position SGLT2 inhibitors and GLP-1 injectables in single care pathways. Robust reimbursement and aging demographics keep volumes high, yet growth rates plateau as guidelines focus on cost containment. Dermatological drugs, by contrast, are forecast to post a 6.72% CAGR to 2031, supported by biologic atopic-dermatitis therapies and heightened consumer skincare awareness. Expansion benefits from tele-dermatology platforms that steer prescriptions toward mild-to-moderate cases previously untreated, deepening penetration across the Germany pharmaceutical market.

Rising prevalence of chronic skin disease, coupled with favorable OTC switch policies for topical steroids, sustains the momentum. Oncology precision regimens further influence dermatology through cutaneous adverse-event management products, reinforcing cross-specialty demand. Anti-infectives regain policymaker focus as antimicrobial-resistance targets tighten, though absolute spend remains moderate. Gastrointestinal and nervous-system products log steady mid-single-digit CAGRs, while musculoskeletal agents gain from active senior lifestyles. Altogether, therapeutic diversity insulates the Germany pharmaceutical market from single-segment volatility.

By Drug Type: Prescription dominance challenged by OTC innovation

Prescription volumes stood at 86.55% of Germany pharmaceutical market size in 2025 as physician-centric care pathways prevailed and statutory insurance kept patient co-pays low. Electronic scripts processed more than 90 million transactions that year, pushing adherence to 94% and supporting brand loyalty. Growth now moderates as AMNOG rounds intensify, but high-value specialty lines maintain share. Over-the-counter spending logs a 6.65% CAGR to 2031, driven by self-care culture, remote consultation, and pharmacy-assistant programs that elevate consumer confidence in autonomous treatment.

STADA’s consumer-health revenue jumped 17% during 2023, highlighting appetite for trusted cold-and-flu and gastrointestinal brands. Regulatory switches for proton-pump inhibitors and antihistamines expand shelf offerings, while m-health apps guide safe usage. The prescription-to-OTC transition consequently diffuses innovation across multiple pricing tiers, fostering balanced trajectory inside the Germany pharmaceutical market.

By Molecule Type: Small-molecule leadership yields to biologic innovation

Small molecules still supply 66.90% German prescription volumes and underpin generic-competition savings that stabilize national health budgets. They remain indispensable for primary-care indications, including cardiovascular and metabolic diseases. Yet biologics advance at 6.90% CAGR as monoclonal antibodies, fusion proteins, and mRNA payloads unlock previously untreatable disorders. BioNTech’s USD 1.25 billion CureVac purchase concentrates mRNA know-how and speeds oncology pipeline synergies.

Biosimilar entrants depress mature biologic prices, but overall spend climbs because patient pools expand and novel targets emerge. Manufacturing upgrades at Merck KGaA’s EUR 300 million antibody center enable dual sourcing of originators and follow-ons, capturing scale economies. The widened biologic footprint re-balances revenues across the Germany pharmaceutical market while protecting access through local supply.

By Route of Administration: Oral convenience competes with parenteral precision

Oral dosage forms accounted for 70.45% Germany pharmaceutical market size in 2025, anchored by chronic therapy regimens and patient preference. Modified-release tablets sustain compliance, and manufacturing lines are fully amortized, keeping unit costs low. Biologics, however, propel parenteral volumes at a 6.78% CAGR as infusion and subcutaneous devices deliver targeted immunology and oncology effects. Hospital day clinics expand chair capacity, while connected autoinjectors transmit adherence data to physicians.

Inhaled routes capitalize on pandemic-era respiratory awareness; digital spirometers dovetail with smart inhalers for COPD and asthma programs. Topical and transdermal patches grow where localized relief reduces systemic exposure. Collectively, diversified delivery formats ensure clinicians can pair molecule profiles with optimal pharmacokinetics, fortifying therapeutic outcomes in the Germany pharmaceutical market.

By Distribution Channel: Hospital pharmacies lead digital transformation

Hospital dispensaries retained 45.70% Germany pharmaceutical market share in 2025 because complex biologics and oncology regimens demand coordinated inpatient-outpatient management. Level 1i institutions draw larger budgets under GKV-FinStG, letting pharmacy teams stock high-cost CAR-T and gene therapies. Online channels, however, chart the fastest 6.45% CAGR as e-prescription interoperability simplifies doorstep delivery.

Retail stores pivot toward clinical services—vaccination rooms, chronic-care coaching, polypharmacy audits—to defend foot traffic. PHOENIX Group’s EUR 12.6 billion wholesale arm stabilizes multi-channel supply by integrating real-time inventory feeds. The blended network keeps last-mile logistics resilient and patient-centric inside the Germany pharmaceutical market.

Geography Analysis

Bavaria, Berlin-Brandenburg, and North Rhine-Westphalia anchor Germany’s tri-cluster life-science map. Bavaria’s 540 biotech firms, employing 57,000 staff, raised EUR 910 million in 2024—nearly double prior-year financing—driven by oncology and metabolic start-ups. The Berlin Center for Gene and Cell Therapies unites Charité and Bayer to test autologous CAR-T protocols, drawing contract partners from the wider Germany pharmaceutical market. North Rhine-Westphalia’s Marburg corridor hosts CSL, GSK, and BioNTech, with shared pilot bioreactors and an Innovation Hub that accelerates scale-up for mRNA products.

Digital infrastructure is consistent across states, yet urban centers log faster electronic-script penetration and GLP-1 uptake, widening therapeutic access gaps that policy makers monitor via the forthcoming national health-data hub. Balanced public-private investment funnels at least EUR 8.7 billion annually into R&D, sustaining regional competitiveness across the Germany pharmaceutical industry.

Competitive Landscape

Global majors (Merck KGaA, Bayer, Boehringer Ingelheim) combine diversified portfolios with double-digit R&D intensity, maintaining legacy leadership while pivoting to AI-guided discovery. International entrants (Pfizer, Novartis, AbbVie) co-locate translational research sites near German university hospitals to capture local talent and clinical-trial infrastructure. Domestic champions double down on technology platforms: BioNTech reinforces mRNA dominance through CureVac integration, and STADA expands biosimilar lines via Alvotech tie-ups.

Digital differentiation accelerates. Boehringer uses machine-vision QC in Biberach to trim batch-release intervals; Bayer’s cloud-based pharmacovigilance automates adverse-event detection. Mid-cap innovators build niche positions: Evotec scales induced-pluripotent-stem-cell libraries, and Fresenius Kabi upgrades parenteral nutrition plants for personalized compounding. Strategic alliances proliferate around AI startups, with Sanofi and Merck VC arms funding algorithm developers that shorten lead-optimization cycles.

Competitive pressure mounts as hospital tenders bundle biosimilar lots, favoring price-agile suppliers. Yet market presence also hinges on sustainability metrics—many hospitals incorporate CO₂-audit scores into procurement, giving local green-energy plants an edge. Consequently, victory in the Germany pharmaceutical market derives from synergizing scientific leadership, manufacturing scale, digital fluency, and ESG credibility.

Germany Pharmaceutical Industry Leaders

AbbVie Inc.

AstraZeneca plc

Bayer AG

GlaxoSmithKline plc

C.H. Boehringer Sohn AG & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Merck KGaA allocated EUR 300 million for an Advanced Research Center in Darmstadt to advance antibody and mRNA manufacturing, adding 550 jobs by 2027.

- January 2024: Germany’s Federal Institute for Drugs and Medical Devices cleared Eli Lilly’s Mounjaro; the firm concurrently unveiled a EUR 2.3 billion expansion of its Alzey site to support injectable output.

- October 2023: The European Commission authorized trastuzumab deruxtecan from AstraZeneca-Daiichi Sankyo for monotherapy in advanced non-small-cell lung cancer, enabling early German launch through centralized procedure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany pharmaceutical market as all human prescription and non-prescription drugs, biologics, and biosimilars supplied through retail, hospital, and online channels, valued at ex-manufacturer prices in U.S. dollars.

Scope Exclusions: veterinary medicines, active pharmaceutical ingredient trade, medical devices, and nutraceuticals are outside the stated boundary.

Segmentation Overview

- By Therapeutic Category

- Anti-infectives

- Cardiovascular

- Gastrointestinal

- Anti-diabetic

- Respiratory

- Dermatologicals

- Musculo-skeletal

- Nervous System

- Other Therapeutic Categories

- By Drug Type

- Prescription Drugs

- Branded

- Generic

- OTC Drugs

- Prescription Drugs

- By Molecule Type

- Small-molecule

- Biologic / Biopharmaceutical

- Biosimilar

- By Route of Administration

- Oral

- Parenteral

- Inhalation

- Topical / Transdermal

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with hospital pharmacists, biotech manufacturing managers, statutory insurance negotiators, and wholesale buyers in Bavaria, North-Rhine Westphalia, Berlin, and Saxony. These discussions confirmed channel splits, average selling prices, uptake curves for GLP-1 and CAR-T therapies, and informed our scenario probabilities.

Desk Research

We begin with a line-by-line review of open datasets from Destatis, Eurostat, the Federal Joint Committee (G-BA) price lists, and the European Medicines Agency register, which give foundational production, import, and reimbursement volumes. Market-moving trends are further traced through peer-reviewed journals, EFPIA industry briefs, and selected company 10-Ks, while news and financial filings inside D&B Hoovers and Dow Jones Factiva guide quarterly adjustments.

Therapeutic pipeline counts, patent expiries, and hospital tender wins gathered from Questel, Global Security, and Tenders Info signal directional shifts that we later translate into demand multipliers.

The sources quoted illustrate the mix; numerous other public and licensed datasets were assessed to validate and enrich each variable.

Market-Sizing & Forecasting

A top-down reconstruction starts with Destatis production and trade tables, which are then reconciled with reimbursement outlays to form a 2024 demand pool. Selective bottom-up checks, sampled supplier revenues, e-pharmacy volume probes, and hospital formulary audits anchor price and volume reasonableness before final alignment.

Key model drivers include chronic disease prevalence, biologics share, reference-price claw-backs, average pack size, and euro-dollar exchange paths. A multivariate regression coupled with ARIMA smoothing projects each driver, and scenario analysis flexes policy reform or breakthrough therapy shocks.

Data gaps in bottom-up rolls are bridged using weighted averages from disclosed manufacturer splits.

Data Validation & Update Cycle

Outputs pass anomaly screens versus EFPIA turnover trends, IQVIA sell-out panels, and customs data; variances above two standard deviations trigger analyst re-checks. A senior reviewer signs off after peer review. Reports refresh annually, with mid-cycle edits when regulatory or macro shocks materially move the baseline.

Why Our Germany Pharmaceutical Baseline Commands Reliability

Published values often diverge because providers pick different therapeutic baskets, apply alternate price points, or refresh on dissimilar cadences. We openly declare our scope, and we update currency, volume, and policy inputs each year, thereby limiting vintage bias.

Key gap drivers include whether biologics and OTC drugs sit inside totals, how rebates under AMNOG are netted, and if exchange rates are locked or rolling. Some publishers report aspirational pipeline sales, while others freeze estimates from earlier years. Mordor's base case reports only commercialized molecules, and it converts euros using the average annual rate, which keeps short-run volatility in check.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 68.82 B (2025) | Mordor Intelligence | - |

| USD 95.11 B (2024) | Industry Databook A | Includes medical devices and uses spot FX, leading to inflated totals |

| USD 64.70 B (2024) | Market Press Note B | Excludes OTC drugs and applies 2022 consumption shares without refresh |

In sum, our disciplined variable selection and dual cross-checks give users a balanced, transparent baseline that traces directly back to public statistics and confirmatory field insights, letting decision-makers plan with greater confidence.

Key Questions Answered in the Report

How big is the Germany Pharmaceutical Market?

The Germany Pharmaceutical Market size is expected to reach USD 73.03 billion in 2026 and grow at a CAGR of 6.12% to reach USD 98.22 billion by 2031.

Which therapeutic category leads sales in Germany?

Cardiovascular drugs rank first, holding 14.10% of Germany pharmaceutical market share in 2025.

Who are the key players in Germany Pharmaceutical Market?

AbbVie Inc., AstraZeneca plc, Bayer AG, GlaxoSmithKline plc and C.H. Boehringer Sohn AG & Co. KG are the major companies operating in the Germany Pharmaceutical Market.

Why are biologics growing faster than small molecules?

Breakthrough antibodies, mRNA vaccines, and targeted cell therapies address high-unmet needs and post a 6.90% CAGR as capacity expands in new German plants.

Page last updated on: