Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

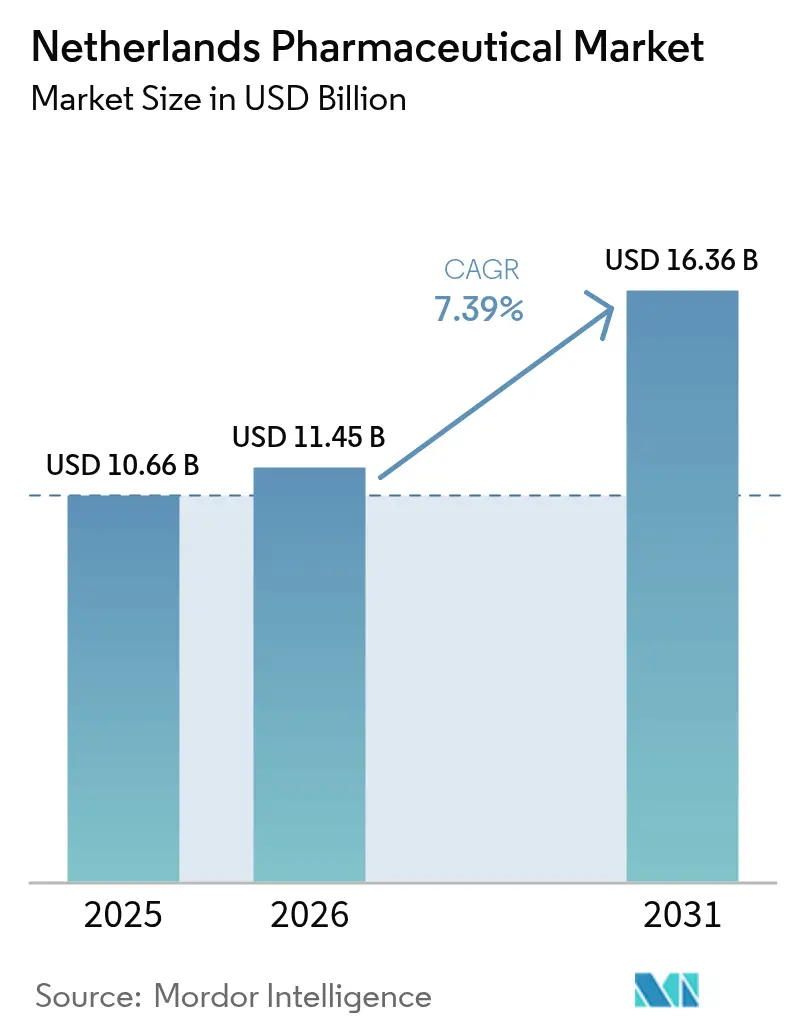

| Base Year Market Size (2025) | USD 10.66 Billion |

| Market Size (2026) | USD 11.45 Billion |

| Market Size (2031) | USD 16.36 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Pharmaceutical Market Analysis by Mordor Intelligence

The Netherlands pharmaceutical market size in 2026 is estimated at USD 11.45 billion, growing from 2025 value of USD 10.66 billion with 2031 projections showing USD 16.36 billion, growing at 7.39% CAGR over 2026-2031. Strong public investment, rapid uptake of advanced therapies, and a coordinated life-sciences ecosystem position the Netherlands pharmaceutical market as a pivotal European growth engine. Momentum stems from rising chronic-disease prevalence, sustained investment in biotech clusters, and the European Medicines Agency’s 2019 relocation to Amsterdam. An innovation-friendly policy mix that includes a €1.3 billion National Growth Fund commitment, coupled with Europe’s lowest antimicrobial-resistance rates, underpins investor confidence. Yet persistent drug-shortage incidents, aggressive insurer preference policies, and escalating R&D costs temper the otherwise favorable outlook.

Key Report Takeaways

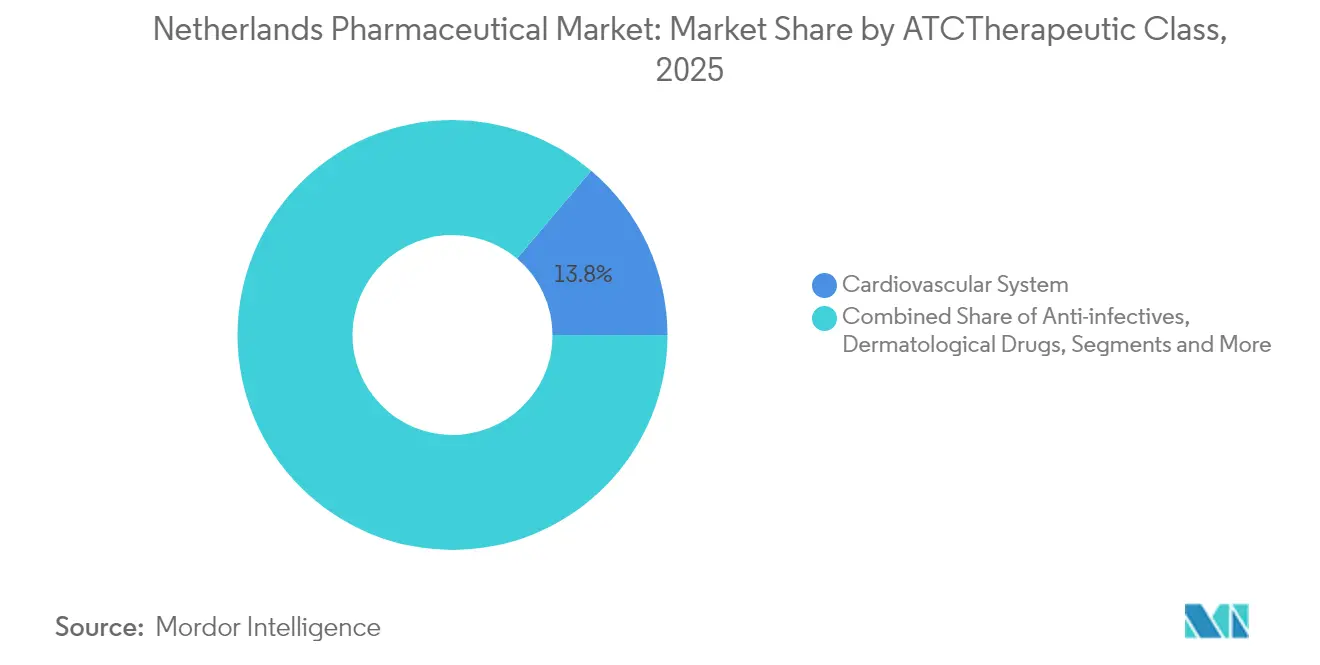

- By ATC/Therapeutic class, cardiovascular system drugs held 13.84% of the Netherlands pharmaceutical market share in 2025, while antineoplastic and immunomodulating agents are projected to expand at an 8.12% CAGR through 2031.

- By molecule type, branded medicines commanded 55.02% share of the Netherlands pharmaceutical market size in 2025; biosimilars record the fastest growth at an 8.63% CAGR over 2026-2031.

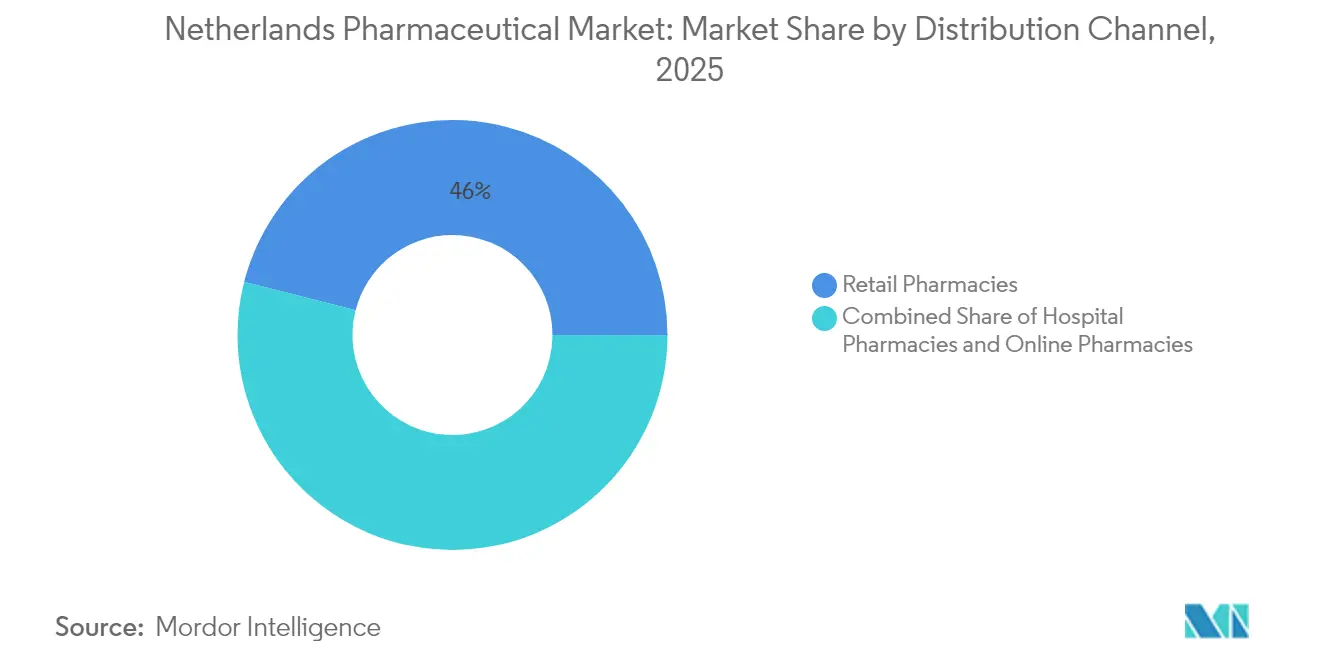

- By distribution channel, retail pharmacies accounted for 46.02% revenue in the Netherlands pharmaceutical market size in 2025, whereas online pharmacies lead growth at an 8.48% CAGR to 2031.

- By mode of dispensing, prescription products represented 87.33% of the Netherlands pharmaceutical market share in 2025, while OTC medicines are advancing at a 8.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Pharmaceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation-friendly government & research institutes | +1.2% | National, Leiden–Amsterdam corridor | Long term (≥ 4 years) |

| Rising prevalence of chronic diseases | +1.8% | National | Medium term (2-4 years) |

| Robust biotechnology clusters | +1.0% | Regional spillover | Long term (≥ 4 years) |

| Universal reimbursement system | +0.9% | National | Short term (≤ 2 years) |

| Expansion of hospital advanced-therapy centers | +0.7% | Academic medical centers | Medium term (2-4 years) |

| Early-access & compassionate-use programs | +0.4% | National, EU-aligned | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Innovation-Friendly Government & World-Class Research Institutes

The National Technology Strategy channels €5.7 billion in annual funding toward ten key enabling technologies, with molecules and cells enjoying top priority. This long-range commitment stimulates commercialization pathways for personalized medicines and advanced biologics. The €1.3 billion National Growth Fund allocation boosts domestic manufacturing capacity and reduces reliance on external supply chains. Academic centers such as Leiden University Medical Center translate bench innovation into GMP-compliant pluripotent stem-cell lines ready for clinical application, while multinational firms like Bristol Myers Squibb locate Europe’s first CAR-T production plant in Leiden. Collectively, these initiatives elevate the Netherlands pharmaceutical market as a magnet for late-stage clinical trials, high-value biologics, and tech-enabled discovery [1]IO+, “Cabinet: in 2040 the Netherlands is frontrunner in biotech,” ioplus.nl.

Rising Prevalence of Chronic Diseases

Chronic conditions affect 10.4 million residents, creating durable demand across multiple therapeutic classes. Dementia and osteoarthritis cases are projected to double by 2050, intensifying the need for neurology and musculoskeletal interventions. Cardiovascular disease remains the leading mortality driver, though shorter hospital stays signal therapeutic progress. Obesity trends add urgency to metabolic treatments, including GLP-1 receptor agonists, despite reimbursement gaps that widen health-equity concerns. This large patient pool ensures that the Netherlands pharmaceutical market retains stable volume drivers even as high-margin specialty categories accelerate.

Robust Biotechnology Clusters in Leiden & Amsterdam

Leiden Bio Science Park hosts more than 200 companies and 18,000 life-sciences employees, generating substantial licensing revenue and attracting contract-development projects. Amsterdam’s life-sciences hub complements discovery activity with translational research strengths, aided by the European Medicines Agency’s proximity. Facilities such as Lonza’s Gene-edited Cell Therapy plant in Geleen and QurAlis’s European headquarters reflect growing foreign direct investment. The tight geographic footprint fosters rapid knowledge transfer, making the Netherlands pharmaceutical market a prototype for cluster-based innovation[2]Universiteit Leiden, “Leiden Bio Science Park,” universiteitleiden.nl.

Strong Universal Reimbursement System Accelerating Patient Access

Dutch universal coverage ensures rapid uptake of cost-effective breakthroughs while using drug-sluice mechanisms to phase in high-cost treatments. Recent inclusion of dostarlimab for uterine cancer following Health Technology Assessment highlights balanced access. Budget optimization trims total pharmaceutical outlays to €4.5 billion in 2025, yet early-access and compassionate-use channels keep innovative medicines within reach. Insurer preference policies drive generic substitution, lowering costs but intensifying margin pressures for originators.

Expansion of Hospital Advanced-Therapy Centers (Cell & Gene)

Academic centers in Utrecht, Leiden, and Groningen expand GMP suites to manage autologous and allogeneic cell-therapy production. New CAR-T infusion sites reduce patient travel time and shorten treatment queues. Early real-world evidence supports outcome-based contracting, which aligns payer risk with therapeutic performance. Growing installed capacity helps the Netherlands pharmaceutical market absorb rising demand for personalized oncology solutions.

Early Access & Compassionate-Use Programs Post-COVID

COVID-19 accelerated regulatory agility, allowing clinicians to use investigational drugs under strict monitoring. These frameworks persist, shortening the time between EMA approval and Dutch market entry from nearly one year to under six months for priority medicines. Pharmaceutical firms leverage early-access data to build real-world evidence packages that support broader reimbursement engagements.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D failure rates & escalating costs | -0.8% | Global, Dutch spillover | Long term (≥ 4 years) |

| Stringent insurer preference policy | -1.1% | National | Medium term (2-4 years) |

| Litigation-led push for drug-price transparency | -0.6% | National, EU-aligned | Medium term (2-4 years) |

| Supply-chain pressure from FMD compliance | -0.9% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High R&D Failure Rates and Escalating Development Costs

Average out-of-pocket R&D outlays surpass USD 1 billion per novel entity, and only 1 in 10 candidates entering Phase I achieves market authorization. The Netherlands’ 2.3% R&D-to-GDP ratio trails the EU’s 3% target, widening the funding gap for capital-intensive drug programs. Midsize firms face cash-burn constraints, exemplified by consolidation such as Medios’s purchase of Ceban Pharmaceuticals. Artificial-intelligence platforms promise savings but require large, curated data sets and regulator guidance to scale, limiting near-term relief [3]QbD Group, “Digital health in pharma,” qbdgroup.com.

Stringent Insurer “Preference Policy” Driving Price Erosion

Mandatory tendering and one-winner formularies suppress prices up to 60% below EU averages. Pharmaceutical firms often reduce Dutch supply volumes to avoid parallel trade arbitrage, contributing to 2,292 reported shortages in 2023. While biosimilar uptake soars, innovators wrestle with diminished returns, raising concerns over launch sequencing and willingness to supply niche drugs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By ATC/Therapeutic Class: Cardiovascular Leadership Drives Volume

Cardiovascular system drugs accounted for 13.84% of 2025 revenue, maintaining the largest slice of the Netherlands pharmaceutical market. Uptake of PCSK9 inhibitors and next-generation anticoagulants offsets price decline in statins. The antineoplastic and immunomodulating agents segment is forecast to grow at an 8.12% CAGR, propelled by PD-1/L1 immunotherapies and targeted small-molecule launches. Alimentary-tract medicines gain from double-digit diabetes incidence, while blood-forming organ therapies expand via novel oral anticoagulants. Dermatology and genitourinary categories post stable mid-single-digit gains underpinned by lifestyle-driven demand. Antibiotics remain below EU volume averages, reflecting stringent stewardship, yet steady sales of reserve antibiotics address resistant pathogens. Musculoskeletal and nervous-system classes benefit from an aging society, whereas systemic hormonal products leverage improved diagnostic pathways.

Emerging GLP-1 analogs and gene-silencing therapies blur traditional class boundaries, presenting cross-segment growth pockets. Hospital formularies negotiate indication-specific pricing, linking reimbursement to real-world outcomes. Academic centers conduct combination-therapy trials that elevate oncology’s share of the Netherlands pharmaceutical market size and set a precedent for future value-based frameworks. Specialty-pharmacy services align with intricate dosing regimens, enhancing adherence and generating data for pharmacoeconomic modeling.

By Molecule Type: Branded Dominance Faces Biosimilar Disruption

Branded products held 55.02% of total sales in 2025, underscoring sustained value capture from innovative launches. However, the patent cliff for monoclonal antibodies, including ustekinumab, unlocks space for biosimilar entrants. The Netherlands pharmaceutical market size for biosimilars is predicted to climb 8.63% annually through 2031 as tender-friendly policies accelerate switching. Generics preserve meaningful volume share through automatic substitution at retail pharmacies, supported by insurer mandates. Originators respond with lifecycle extensions such as subcutaneous formulations, digital companion apps, and real-world evidence studies demonstrating superior persistence.

Manufacturers partner with local contract-development organizations to streamline dossier preparation in anticipation of centralized EMA filings, shortening time-to-tender. Patient-support programs focusing on home infusion and remote monitoring add differentiation beyond molecular equivalence. Despite margin compression, predictable biosimilar uptake stabilizes payer budgets, fostering headroom for premium advanced-therapy medicinal products, thereby reinforcing the dual-speed nature of the Netherlands pharmaceutical market.

By Distribution Channel: Retail Strength Meets Digital Innovation

Retail pharmacies captured 46.02% revenue in 2025, cementing their role as primary medication-dispensing hubs and frontline health advisors. The PHOENIX group’s 340-store BENU network illustrates ongoing chain consolidation that affords negotiating power with suppliers. Online pharmacies grow at an 8.48% CAGR, capitalizing on pandemic-induced e-commerce familiarity, same-day delivery offerings, and e-prescription integration. Hospital pharmacies manage high-complexity biologics and advanced-therapy medicinal products that require on-site compounding and close clinical supervision.

Hybrid “click-and-collect” models bridge digital and physical spheres, enabling patients to order online and pick up in store, reinforcing relationship continuity. EU Falsified Medicines Directive scanners at points of dispense enhance trust, while blockchain pilots explore end-to-end provenance tracking. Channel strategies increasingly incorporate telepharmacy counseling and remote adherence monitoring, broadening the Netherlands pharmaceutical market’s service layer and deepening data insights for population-health management.

By Mode of Dispensing: Prescription Dominance Reflects Regulatory Rigor

Prescription medicines represented 87.33% of 2025 turnover, reflecting a system that favors physician oversight and evidence-based selection. Controlled OTC expansion at a 8.87% CAGR arises from prescription-to-OTC switches in allergy, gastrointestinal, and dermatology categories. Self-care momentum aligns with digital symptom-triaging tools, yet pharmacists’ independent-prescribing scope remains limited to collaborative protocols, ensuring clinical governance.

E-prescription penetration approaches full national coverage, facilitating refill automation and dosage-reminder services. Micro-fulfillment centers linked to community pharmacies enable 24-hour locker pickup, serving shift workers and rural customers. Future regulatory proposals consider pharmacist vaccination authority and chronic-therapy initiation under strict algorithms, potentially nudging the Netherlands pharmaceutical industry toward broader pharmacist clinical roles without compromising patient safety.

Geography Analysis

The Netherlands pharmaceutical market benefits from compact geography that concentrates R&D, regulatory, and manufacturing assets within the Randstad corridor. Leiden’s biotechnology focus, Amsterdam’s clinical-research and regulatory depth, and Utrecht’s veterinary-health specialization create complementary capabilities. EMA’s presence elevates Amsterdam’s visibility, drawing multinational regulatory-affairs units and accelerating centralized-procedure familiarity. Post-Brexit adjustments channel company relocations to Dutch sites to safeguard EU market access.

Export competitiveness remains robust; port infrastructure in Rotterdam and air-cargo facilities at Schiphol facilitate cold-chain throughput for biologics and cell therapies destined across Europe and North America. Government cluster policies provide tax incentives and streamlined permitting, catalyzing additional investment in greenfield GMP manufacturing. Regional development funds prioritize cell-and-gene manufacturing capacity in peripheral provinces, distributing economic benefits beyond the Randstad.

Cross-border collaboration with Belgium and Germany nurtures a tri-national life-sciences belt that pools clinical-trial participants and harmonizes ethics approvals. Digital-health startups orbit around academic medical centers, leveraging open-data initiatives and interoperability standards to pilot AI-driven diagnostic tools, further enriching the Netherlands pharmaceutical market ecosystem.

Competitive Landscape

The market exhibits moderate concentration, with the top five players controlling roughly 45% of branded-drug sales. Multinationals dominate high-value oncology and immunology niches, while domestic and regional biotechs carve focused pipelines in metabolic and infectious-disease areas. Bristol Myers Squibb’s CAR-T plant and Pfizer’s RNA-manufacturing collaboration underscore inward investment trends. Innovative SMEs like Leyden Labs and NewAmsterdam Pharma raise sizable late-stage financing rounds, challenging incumbents in pandemic preparedness and cardiovascular lipoprotein modulation.

Strategic alliances proliferate as large firms license local discovery assets to expand modality coverage. Digital-therapeutic add-ons accompany specialty launches, enhancing adherence and feeding real-world data into post-marketing effectiveness dossiers. EMA’s 2024 AI reflection paper offers a clear governance framework, prompting accelerated deployment of machine-learning drug-design platforms.

Generic and biosimilar competitors, led by Teva, Sandoz, and Viatris, successfully leverage insurer tenders, capturing share in off-patent monoclonal antibodies and inhalation therapies. Margin compression spurs cost-optimization initiatives such as multi-country packaging and shared serialization hubs. Specialty wholesalers deepen value by bundling pharmacovigilance services and at-home infusion support, extending influence along the supply chain.

Netherlands Pharmaceutical Industry Leaders

Abbott Laboratories

AbbVie Inc.

AstraZeneca Plc

Novartis AG

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ampersand Capital Partners acquires CurTec, enhancing specialty pharmaceutical packaging capacity.

- April 2025: Government commits €1.3 billion via National Growth Fund to cement biotech leadership by 2040.

- April 2025: CNX Therapeutics and Adalvo launch first generic nitrofurantoin modified-release tablets in the Netherlands.

- April 2025: Nordic Pharma receives CE mark for Lacrifill®, a novel dry-eye therapy slated for EU rollout.

Netherlands Pharmaceutical Market Report Scope

Pharmaceuticals are referred to as prescribed and non-prescribed drugs. These medicines can be bought by an individual with or without the doctor's prescription and are safe for consumption for various illnesses with or without the doctor's consent. The report also covers an in-depth analysis of qualitative and quantitative data. The Dutch pharmaceutical market is segmented by ATC/therapeutic class (alimentary tract and metabolism, blood and blood-forming organs, cardiovascular system, dermatological drugs, genitourinary system and reproductive hormones, systemic hormonal preparations, excluding reproductive hormones and Insulins, antiinfectives for systemic use, antineoplastic and immunomodulating agents, musculoskeletal system, nervous system, antiparasitic products, insecticides and repellents, respiratory system, sensory organs, and various ATC structure), and mode of dispensing (Prescription and OTC). The report offers values in USD million for all the above-mentioned segments.

By ATC / Therapeutic Class

| Alimentary Tract & Metabolism |

| Blood & Blood-Forming Organs |

| Cardiovascular System |

| Dermatological Drugs |

| Genitourinary System & Reproductive Hormones |

| Systemic Hormonal |

| Anti-infectives |

| Antineoplastic & Immunomodulating Agents |

| Musculoskeletal System |

| Nervous System |

| Others |

By Molecule Type

| Branded |

| Generic |

| Biosimilar |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

By Mode of Dispensing

| Prescription |

| OTC |

| By ATC / Therapeutic Class | Alimentary Tract & Metabolism |

| Blood & Blood-Forming Organs | |

| Cardiovascular System | |

| Dermatological Drugs | |

| Genitourinary System & Reproductive Hormones | |

| Systemic Hormonal | |

| Anti-infectives | |

| Antineoplastic & Immunomodulating Agents | |

| Musculoskeletal System | |

| Nervous System | |

| Others | |

| By Molecule Type | Branded |

| Generic | |

| Biosimilar | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| By Mode of Dispensing | Prescription |

| OTC |

Key Questions Answered in the Report

How big is the Netherlands Pharmaceutical Market?

The Netherlands Pharmaceutical Market size is expected to reach USD 11.45 billion in 2026 and grow at a CAGR of 7.39% to reach USD 16.36 billion by 2031.

Which therapeutic class currently generates the highest revenue?

Cardiovascular system drugs hold the largest share at 13.84% of 2025 revenue.

Who are the key players in Netherlands Pharmaceutical Market?

Abbott Laboratories, AbbVie Inc., AstraZeneca Plc, Novartis AG and F. Hoffmann-La Roche AG are the major companies operating in the Netherlands Pharmaceutical Market.

How fast is the biosimilar segment expected to grow?

Biosimilars are projected to expand at an 8.63% CAGR between 2026 and 2031.

Page last updated on: