Payroll Software In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

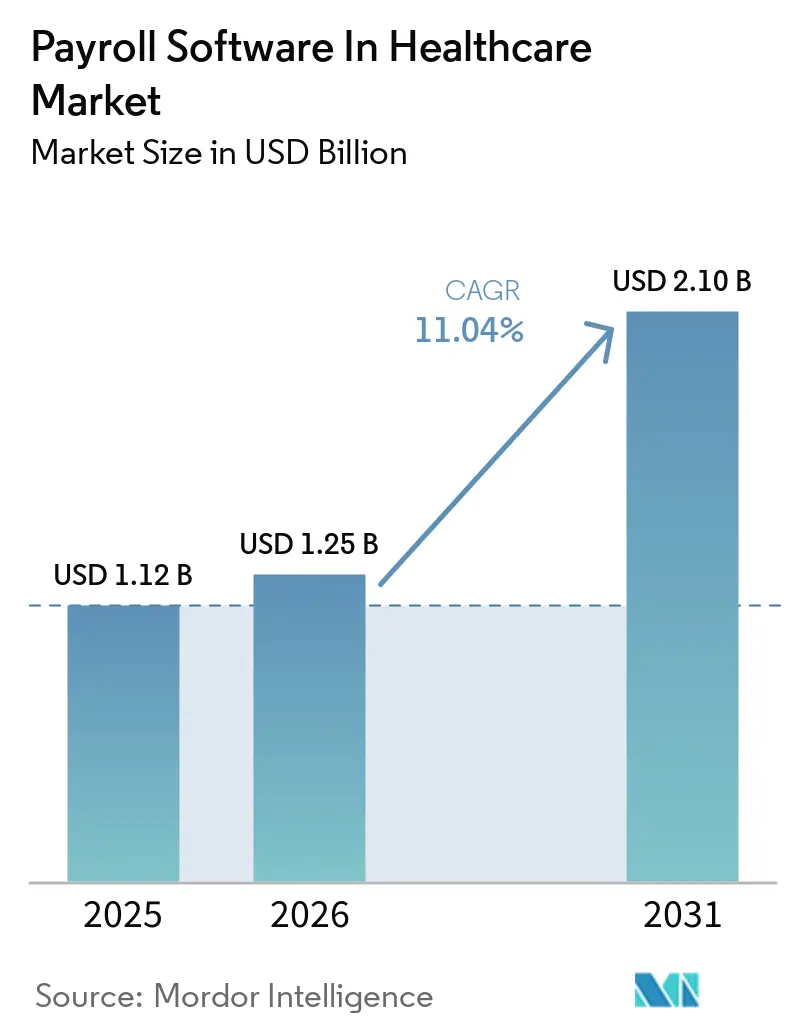

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2031) | USD 2.10 Billion |

| Growth Rate (2026 - 2031) | 11.04% CAGR |

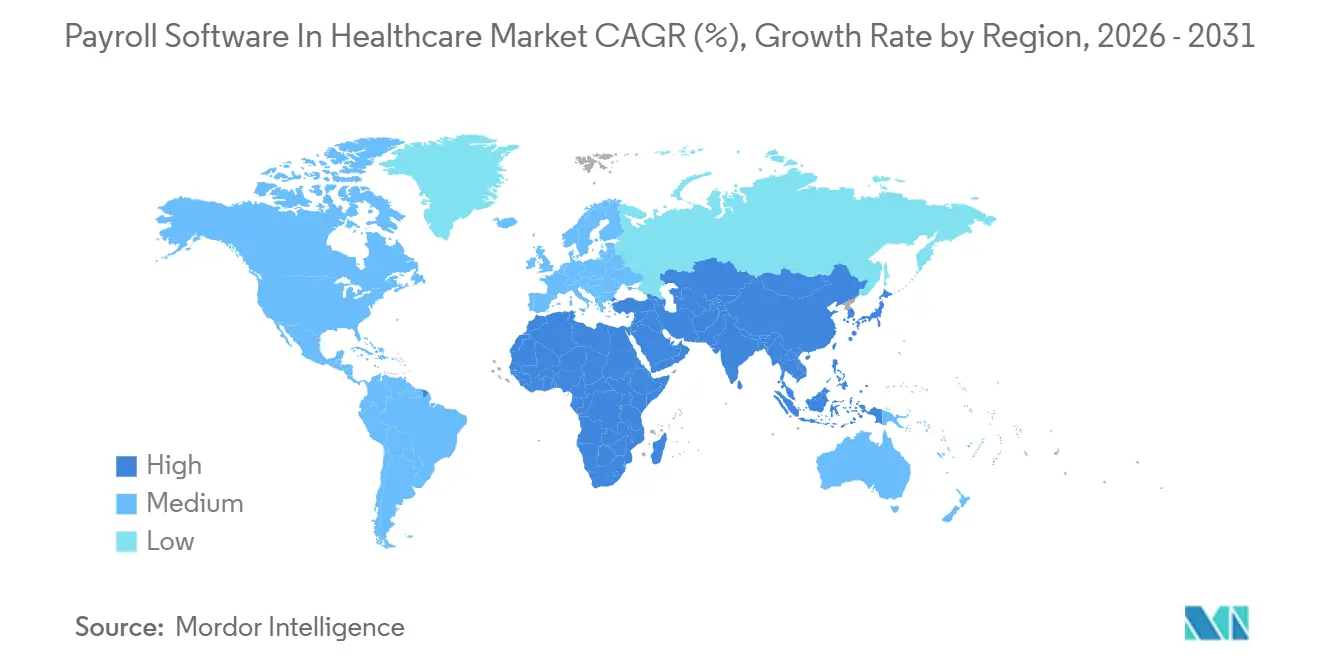

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payroll Software In Healthcare Market Analysis by Mordor Intelligence

The payroll software in healthcare market size is projected to expand from USD 1.12 billion in 2025 and USD 1.25 billion in 2026 to USD 2.10 billion by 2031, registering a CAGR of 11.04% between 2026 to 2031. Hospitals and health systems are pressing vendors to automate union wage scales, multi-state taxes, and new paid-leave mandates inside a single pay cycle, exposing gaps in older human-resource information systems. The 2026 Medicare Physician Fee Schedule forces real-time recalibration of physician compensation, which has made granular labor-cost allocation a must-have capability. Security scrutiny also intensified after the 2024 Change Healthcare breach, adding encryption and multi-factor authentication to vendor selection checklists. At the same time, value-based care contracts now link 40% of Medicare fee-for-service payments to quality metrics that require payroll data to map labor costs to diagnosis-related groups.

Key Report Takeaways

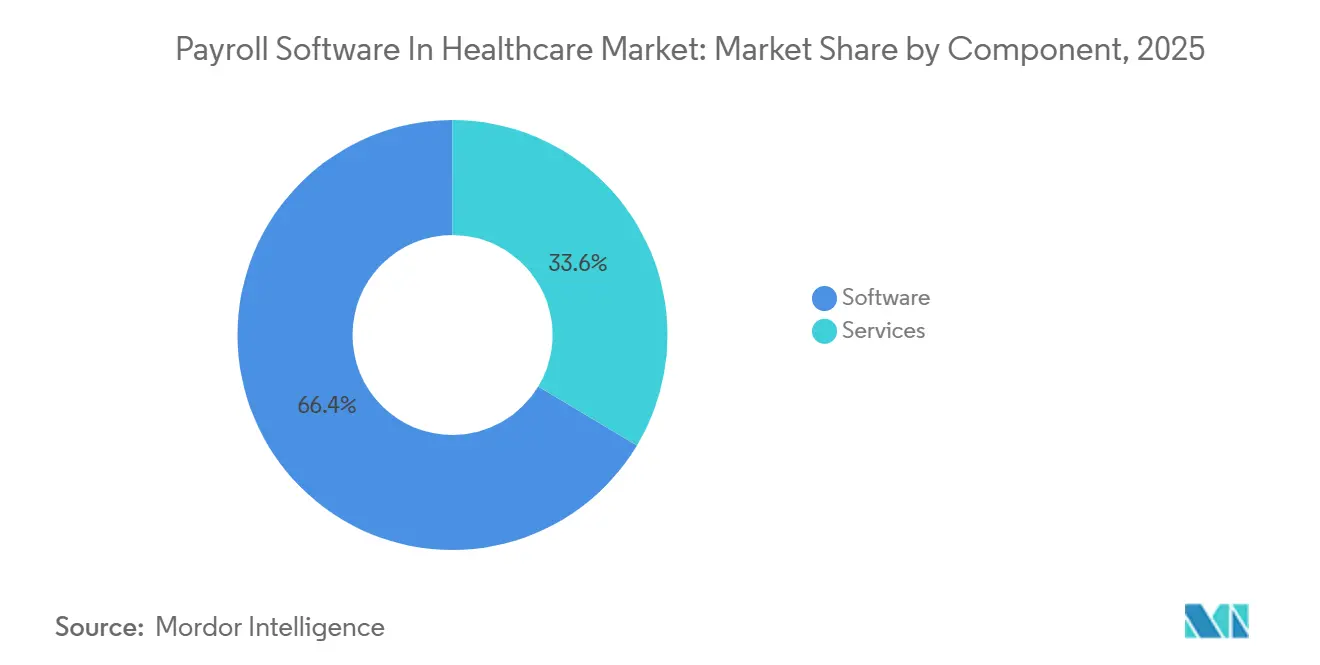

- By component, software led with 66.41% revenue share in 2025, while services are forecast to expand at a 13.76% CAGR through 2031.

- By application, payroll processing accounted for a 45.89% share of the payroll software in healthcare market size in 2025 and compliance and tax management is advancing at a 12.98% CAGR through 2031.

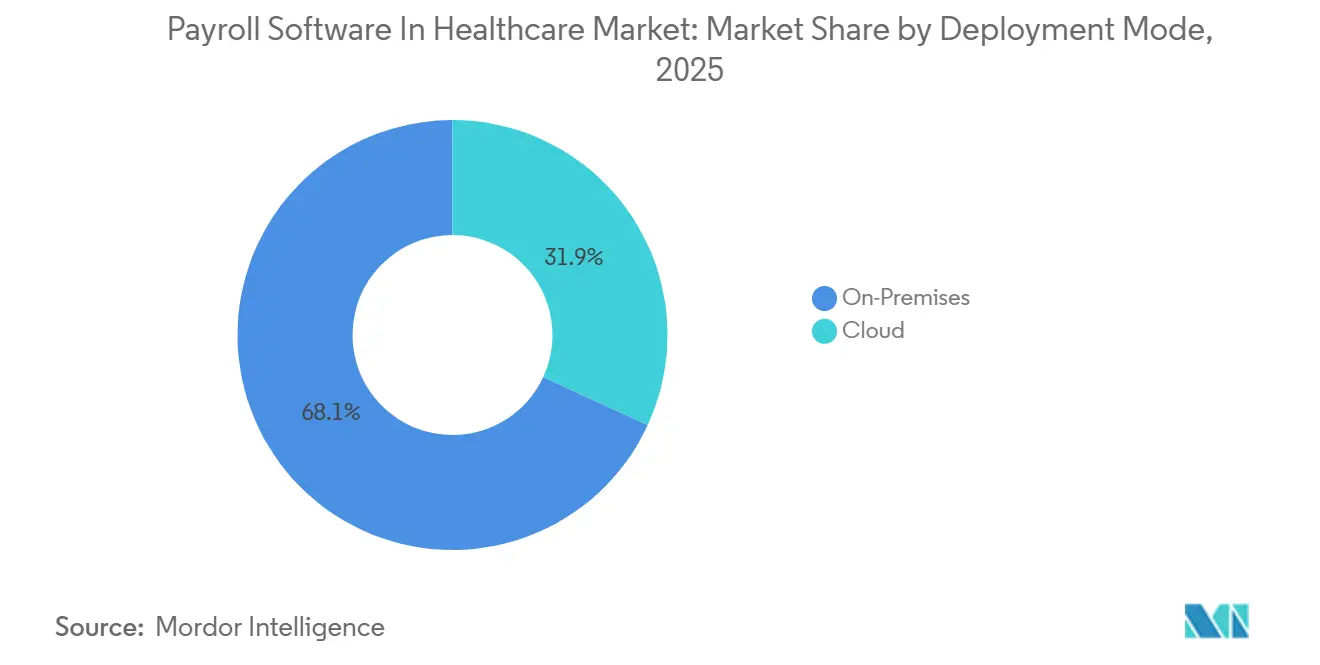

- By deployment mode, on-premises retained 68.12% of revenue in 2025, yet cloud is projected to grow at a 14.02% CAGR between 2026 and 2031.

- By end user, hospitals commanded 51.67% of revenue in 2025, whereas ambulatory and diagnostic centers are on track for a 13.23% CAGR through 2031.

- By geography, North America captured 37.54% of revenue in 2025 and Asia-Pacific is expected to register the fastest regional CAGR at 12.54% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Payroll Software In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Complexity of Multi-Jurisdiction Healthcare Payroll Compliance | +2.3% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Accelerating Shift Toward Cloud-Based Payroll Solutions in Hospitals | +2.1% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Increasing Adoption of Integrated Workforce Management to Reduce Administrative Costs | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Growing Demand for Real-Time Analytics for Staffing Optimization | +1.5% | Global, early adoption in North America | Short term (≤ 2 years) |

| Expansion of Value-Based Care Models Requiring Granular Labor Cost Allocation | +1.3% | North America, emerging in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Surge in Healthcare Gig Workforce Driving Need for Flexible Payroll Engines | +1.2% | Global, pronounced in North America and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Complexity of Multi-Jurisdiction Healthcare Payroll Compliance

Paid-leave mandates in Minnesota and Maryland that took effect in 2026 oblige employers to withhold premiums, maintain separate accrual ledgers, and file quarterly returns, tasks that manual workflows cannot scale. The SECURE Act 2.0 adds Roth catch-up deferrals for employees earning above USD 145,000, forcing mid-year code changes. Symmetry Tax Engine Premium now processes more than 7,000 tax jurisdictions with sub-four-millisecond latency, proving that artificial intelligence can parse overlapping rules faster than human auditors. A 2026 ADP survey showed 71% of Asia-Pacific organizations paid non-compliance penalties, underlining the financial stakes.[1]ADP Research Institute, “People at Work 2025,” adp.com For multistate hospital chains, the risk of audits and back-tax assessments erodes already-tight margins, making compliance automation a primary purchasing criterion.

Accelerating Shift Toward Cloud-Based Payroll Solutions in Hospitals

The U.S. Department of Health and Human Services migrated payroll to a cloud platform in 2025, citing lower maintenance overhead and better disaster recovery. ChristianaCare cut payroll-processing time by 30% after its own migration. Security expectations rose after the 2024 Change Healthcare breach, which compromised 192.7 million records, prompting regulators to propose mandatory encryption and 72-hour breach notification windows. Workday and Salesforce experienced a 2025 breach that affected more than 700 organizations, demonstrating that even tier-one vendors remain vulnerable. Despite these incidents, cloud deployments are set to grow at a 14.02% CAGR because ambulatory surgery centers and rural clinics prefer capital-light models and continuous feature updates that on-premises systems lack.

Increasing Adoption of Integrated Workforce Management to Reduce Administrative Costs

Hospitals that unify scheduling, credentialing, and payroll on one platform avoid duplicate data entry. At a 400-physician group, QGenda reduced scheduling labor by 50% and lowered overtime by 15% through predictive analytics. Health Catalyst clients save roughly USD 2 million annually by spotting shift-differential leakage. An AMN Healthcare survey found 68% of providers plan to consolidate vendor contracts by 2027. Symplr prevents payroll runs for unlicensed staff, eliminating fines such as the USD 1.8 million penalty levied on a Texas system in 2024. Vendors offering deep application-programming-interface libraries are winning because they embed payroll data inside electronic-health-record workflows.

Growing Demand for Real-Time Analytics for Staffing Optimization

Strata Decision Technology flags departments that exceed labor budgets by 5% within 24 hours, preserving USD 3.2 million at a 600-bed hospital in 2025. M7’s intelligence tool linked a 10% overtime reduction to a 7% fall in hospital-acquired infections. The 2026 Medicare Physician Fee Schedule adjustment exposed platforms that rely on overnight batch updates rather than streaming changes. LotusOne forecasts staffing needs 14 days ahead, cutting agency-nurse spend by 22%. Analytics modules cost about 20% more than base payroll subscriptions but usually pay for themselves within a year by curbing premium-pay leakage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security and Patient Privacy Concerns Hindering Cloud Payroll Adoption | -0.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| High Switching Costs From Legacy HRIS in Large Health Systems | -0.7% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Shortage of Healthcare-Specific Payroll Tax Professionals | -0.4% | Global, particularly North America | Long term (≥ 4 years) |

| Implementation Risk and Project Overruns in Complex Payroll Transitions | -0.3% | Global, visible in North America and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Security and Patient Privacy Concerns Hindering Cloud Payroll Adoption

Because payroll files contain leave data and benefit elections, they qualify as protected health information under HIPAA. Proposed 2025 amendments require encryption at rest and in transit, multi-factor authentication, and breach notification in under 72 hours. The 2025 breach at Workday and Salesforce triggered class-action lawsuits and forced some hospitals to revert to on-premises backups. IBM pegged the average healthcare breach at USD 7.42 million, triple the cross-industry mean, due to fines and credit-monitoring expenses. Security officers now demand annual penetration tests and cyber-insurance policies above USD 50 million, delaying procurements by up to nine months and putting small cloud startups at a disadvantage.

High Switching Costs From Legacy HRIS in Large Health Systems

Replacing entrenched enterprise-resource-planning modules involves data cleansing, parallel runs, and union negotiations that send costs north of USD 50 million for systems with more than 20,000 employees. OhioHealth spent USD 29.1 million integrating Epic, Workday, and Kronos across 14 months of parallel payroll tests. Northwell Health had to retain Lawson tables for pension calculations after finding actuarial logic too complex to migrate. Saskatchewan Health Authority’s payroll rebuild escalated from CAD 86 million (USD 63.2 million) to CAD 203 million (USD 149.2 million) and still produced manual checks, showing how interface complexity derails timelines. High-profile overruns deter other providers from initiating replacements, slowing market expansion even when functional gaps are obvious.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Mitigate Penalty Exposure

Services accounted for a rising slice of the payroll software in healthcare market as health systems outsource tax filing to avoid penalties that 71% of Asia-Pacific organizations report each year. Software still generated 66.41% of 2025 revenue because large integrated delivery networks favor perpetual licenses that can handle union rules at scale. However, ADP’s co-employment model transfers liability for withholding errors, attracting ambulatory centers that lack dedicated payroll staff. The SECURE Act 2.0 Roth catch-up mandate and new state paid-leave premiums increased filing complexity in 2026, spurring a surge in managed-payroll inquiries. Paychex’s USD 4.1 billion purchase of Paycor underscores the convergence of software and services under one roof.

Hybrid offerings blur segment boundaries. Vendors now sell software subscriptions bundled with tax-filing services, complicating the attribution of payroll software in healthcare market share. Mid-sized hospitals prefer predictable pricing over configuration control, driving double-digit growth in outsourcing. Legacy on-premises suites still dominate among multistate systems processing 50,000 paychecks every two weeks, but even these providers are piloting service extensions that guarantee penalty reimbursement. Over the forecast horizon, service revenues are set to outpace license revenues even if software retains the largest absolute pool.

By Application: Compliance Modules Outpace Core Processing

While payroll processing captured 45.89% of 2025 revenue, compliance and tax management is on course for the fastest expansion at a 12.98% CAGR. Hospitals cannot afford fines or remediation time, so they pay a 30% to 40% premium for real-time compliance feeds. Symmetry Tax Engine Premium demonstrates the value of sub-four-millisecond rule processing across 7,000 jurisdictions, turning an erstwhile cost center into a strategic feature. The 2026 Medicare Physician Fee Schedule’s 2.5% work-relative-value-unit change forced mid-cycle updates, stressing systems that treat compliance as static tables instead of streaming feeds.

Time and attendance remains the connective tissue between scheduling and payroll, adding biometric scanners and mobile geofencing to curb buddy punching. Benefits administration automates enrollment and premium reconciliation, reducing off-cycle adjustments. Garnishment processing and union-dues remittance remain niche, yet they push buyers toward platforms that handle the full payments spectrum. The payroll software in healthcare market size for compliance modules grows because errors escalate to audits, back taxes, and damaged credit for clinicians, dwarfing software fees. Vendors able to monetize compliance updates weekly rather than annually will capture the incremental spend.

By Deployment Mode: Cloud Gains as Capital Constraints Outweigh Security Concerns

In 2025, on-premises deployments held a dominant 68.12% market share, underscoring integrated delivery networks' preference for data control and customization. However, cloud adoption is set to surge at a rate of 14.02% through 2031. This shift is largely driven by ambulatory surgery centers, diagnostic imaging chains, and rural hospitals, all of which are gravitating towards capital-light models. The operational advantages of cloud migration are underscored by the United States Department of Health and Human Services' 2025 cloud migration initiative and ChristianaCare's achievement of a 30% reduction in processing times. Yet, the landscape is not without its challenges. The Change Healthcare breach, which saw 192.7 million records compromised and incurred costs of USD 2.9 billion, has intensified security concerns.

Meanwhile, Workday Inc.'s introduction of agentic artificial-intelligence tools in February 2025 showcases the cloud's edge. These tools can auto-reconcile time-card discrepancies and flag overtime thresholds pre-payroll, a feat not achievable with on-premises systems. While on-premises systems remain prevalent in academic medical centers and public-hospital networks, largely due to data-sovereignty mandates and union contracts prohibiting offshore processing, there is a noticeable shift. These institutions are increasingly leaning towards hybrid architectures, keeping payroll calculations on-premises but transitioning tax filing and reporting to the cloud.

By End User: Ambulatory Centers Take the Lead

In 2025, hospitals held a 51.67% market share, a testament to their scale and operational complexity. A typical 500-bed hospital processes between 8,000 to 12,000 paychecks biweekly, navigating intricacies like shift differentials, on-call premiums, and union wage scales. However, as the industry landscape shifts, ambulatory and diagnostic centers are poised for growth, projected at 13.23% through 2031. This momentum is fueled by the Centers for Medicare and Medicaid Services' 2026 proposal to add 547 new codes to the ambulatory surgical center's covered-procedures list. Such additions compel these centers to recruit credentialed staff and allocate budgets for variable shift premiums.

Long-term and aged-care facilities face challenges with high turnover rates, averaging 50% to 70% annually for certified nursing assistants. This necessitates efficient onboarding workflows that can verify credentials and enroll benefits within a tight 48-hour window. Other stakeholders, like home-health agencies and hospice providers, leverage mobile time-capture tools. These tools not only validate GPS coordinates but also ensure patient visit logs are accurate before approving payments. The growth of ambulatory centers is emblematic of a broader industry trend, shifting from inpatient to outpatient settings. Here, the allure of lower overheads and higher margins is driving increased investments in workforce technology.

Geography Analysis

North America retained 37.54% of payroll software in healthcare market revenue in 2025 because state and local tax regimes demand specialized compliance engines. California alone posts nine disability-insurance rates and 58 county levies, all of which must be reflected in each paycheck. The 2026 Medicare Physician Fee Schedule and practice-expense updates forced real-time physician-compensation recalibration, revealing that nightly batch updates no longer suffice. Canada’s Saskatchewan cost blowout illustrates the switching-cost hurdle. Mexico’s 2024 social-security reform pushed private hospital chains toward cloud payroll that integrates electronic filing.

Europe is governed by the General Data Protection Regulation and the forthcoming European Health Data Space, both of which compel in-region data residency.[2]European Union, “European Health Data Space Regulation 2025/327,” eur-lex.europa.eu National health services in the United Kingdom, Germany, and France digitalize timekeeping to enforce Working Time Directive limits. Vendors such as Zalaris use sovereign data centers to navigate these requirements. Meanwhile, Asia-Pacific is forecast to grow at 12.54% through 2031, buoyed by workforce shortages and government digitalization. India’s Unified Payments Interface enables instant salary disbursement; Japan enforces monthly overtime caps, and Australia’s single-touch payroll regime submits every run to the tax office in real time.

The Middle East and Africa invest in cloud infrastructure under Saudi Vision 2030 and United Arab Emirates health-care expansion plans, though contract awards skew to vendors offering Arabic localization and local data centers. South America and Africa remain earlier in the adoption curve, but Brazil’s eSocial initiative and South Africa’s PAYE modernization lay groundwork for future growth. Together, these regional nuances encourage vendors to broaden tax-engine coverage while adding localization features that extend the payroll software in healthcare market addressable base.

Competitive Landscape

The payroll software in healthcare market is moderately fragmented. The top five suppliers, ADP, Ceridian, Paychex, Paycom, and Workday, collectively control roughly 45% to 50% of global revenue. Paychex’s USD 4.1 billion Paycor acquisition in April 2025 demonstrates consolidation aimed at selling unified human-capital suites to mid-market hospitals. Workday’s February 2025 release of agentic artificial-intelligence utilities that auto-reconcile time cards and flag overtime thresholds highlights the competitive edge of continuous integration pipelines.

White space persists in gig-workforce modules: travel nurses and per-diem therapists earn USD 43 to USD 54 an hour versus a USD 35.24 median, yet most platforms lack credential-verification automation.[3]U.S. Bureau of Labor Statistics, “Registered Nurse Wage Data,” bls.gov Deel and Gusto target outpatient centers with transparent per-employee pricing but lack compliance depth for multistate hospitals. Symmetry Software differentiates through 3.32-millisecond tax-rule processing across 7,000 jurisdictions.

Oracle and SAP maintain academic-medical-center footholds via bundled enterprise-resource-planning deals, though their monolithic code bases update more slowly than cloud-native peers. Competitive advantage now rests on combining breadth, payroll, time, benefits, compliance, with depth in healthcare-specific workflows.

Payroll Software In Healthcare Industry Leaders

SAP SE

Oracle Corporation

Workday, Inc.

Neeyamo Inc.

Automatic Data Processing, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Fairview Health Services selected Workday to unify payroll, scheduling, and credentialing for 32,000 employees, targeting a 20% administrative cost cut within 24 months.

- February 2026: Lewisham and Greenwich NHS Trust awarded Epic Systems a GBP 52 million (USD 65.5 million) contract that embeds payroll into its electronic patient record to enable department-level labor-cost allocation.

- January 2026: Payscale detailed how Cheyenne Regional Medical Center uncovered USD 80,000 in yearly overpayments after deploying compensation-management software.

- October 2025: Acrisure bought Heartland Payroll Solutions from Global Payments for USD 1.1 billion, expanding its professional-employer-organization reach in healthcare.

Global Payroll Software In Healthcare Market Report Scope

The Payroll Software in Healthcare Market is witnessing significant traction, tailored for the unique payroll challenges of hospitals, clinics, long-term care entities, and expansive health networks. These specialized systems adeptly navigate union stipulations, credential-based pay scales, shift differentials, overtime, per-diem staffing, and stringent healthcare labor regulations. Central to the efficiency of healthcare payroll is the seamless integration with scheduling, time-tracking, credentialing, and broader workforce management platforms. The market's growth trajectory is propelled by staffing shortages, escalating regulatory demands, and an overarching push for automation in round-the-clock clinical settings.

The Payroll Software in Healthcare Report is Segmented by Component (Software, and Services), Application (Payroll Processing, Time and Attendance Tracking, Compliance and Tax Management, Benefits Administration, and Other Applications), Deployment Mode (Cloud, and On-Premises), End User (Hospitals, Clinics and Outpatient Centers, Ambulatory and Diagnostic Centers, Long-Term Care and Aged Care Facilities, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Payroll Processing |

| Time and Attendance Tracking |

| Compliance and Tax Management |

| Benefits Administration |

| Other Applications |

| Cloud |

| On-Premises |

| Hospitals |

| Clinics and Outpatient Centers |

| Ambulatory and Diagnostic Centers |

| Long‑Term Care and Aged Care Facilities |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Application | Payroll Processing | |

| Time and Attendance Tracking | ||

| Compliance and Tax Management | ||

| Benefits Administration | ||

| Other Applications | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By End User | Hospitals | |

| Clinics and Outpatient Centers | ||

| Ambulatory and Diagnostic Centers | ||

| Long‑Term Care and Aged Care Facilities | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current payroll software in healthcare market size?

The payroll software in healthcare market size stands at USD 1.25 billion in 2026 and is set to reach USD 2.10 billion by 2031.

Which segment is growing fastest within this market?

Compliance and tax management is projected to grow at a 12.98% CAGR through 2031 due to escalating regulatory changes across jurisdictions.

Why are hospitals moving from on-premises to cloud payroll platforms?

Hospitals favor cloud deployments to cut maintenance costs, gain continuous feature updates, and align with capital-light strategies, even as security requirements tighten after high-profile breaches.

How do services compare with software in terms of growth?

Although software retained 66.41% of 2025 revenue, managed-payroll services are forecast to expand at a 13.76% CAGR as providers outsource tax filing to mitigate penalty risks.

Which regions offer the highest growth potential?

Asia-Pacific is expected to post a 12.54% CAGR to 2031, driven by government digitalization mandates, workforce shortages, and rising non-compliance penalties.

Page last updated on: