HCM And Payroll Convergence Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.77 Billion |

| Market Size (2031) | USD 47.55 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM And Payroll Convergence Platform Market Analysis by Mordor Intelligence

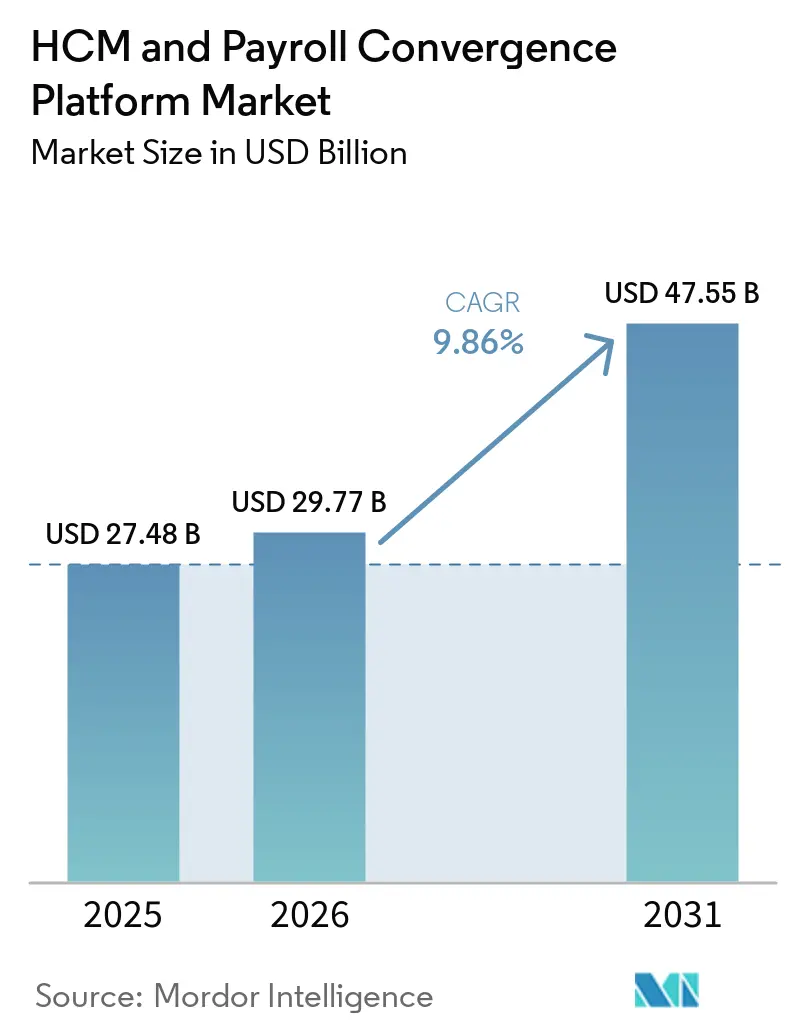

The HCM and payroll convergence platform market size is expected to increase from USD 27.48 billion in 2025 to USD 29.77 billion in 2026 and reach USD 47.65 billion by 2031, growing at a CAGR of 9.86% over 2026-2031. Demand is shifting toward platforms that consolidate workforce data, pay calculation, and compliance logic in a single environment, because buyers no longer want to manage fragile integration layers across separate HR and payroll systems. Enterprise spending is also becoming easier to approve because payroll is now viewed more as a reputational and regulatory issue than as a back-office IT process, which is bringing stronger C-suite support for consolidation decisions. Cloud migration and multi-country compliance complexity continue to pull buyers away from older on-premise estates, while new compliance requirements around compensation transparency are increasing the value of unified records and analytics. Competitive activity remains strong because incumbents are defending their installed bases with broader suites and deeper documentation, while newer vendors are using contractor payments, employer-of-record capabilities, and workflow simplicity to move into larger HCM and payroll-convergence platform budgets. The main constraint is still the risk tied to payroll migration, since multi-year records, local rules, and validation cycles make switching slow even when customers are dissatisfied with existing systems.

Key Report Takeaways

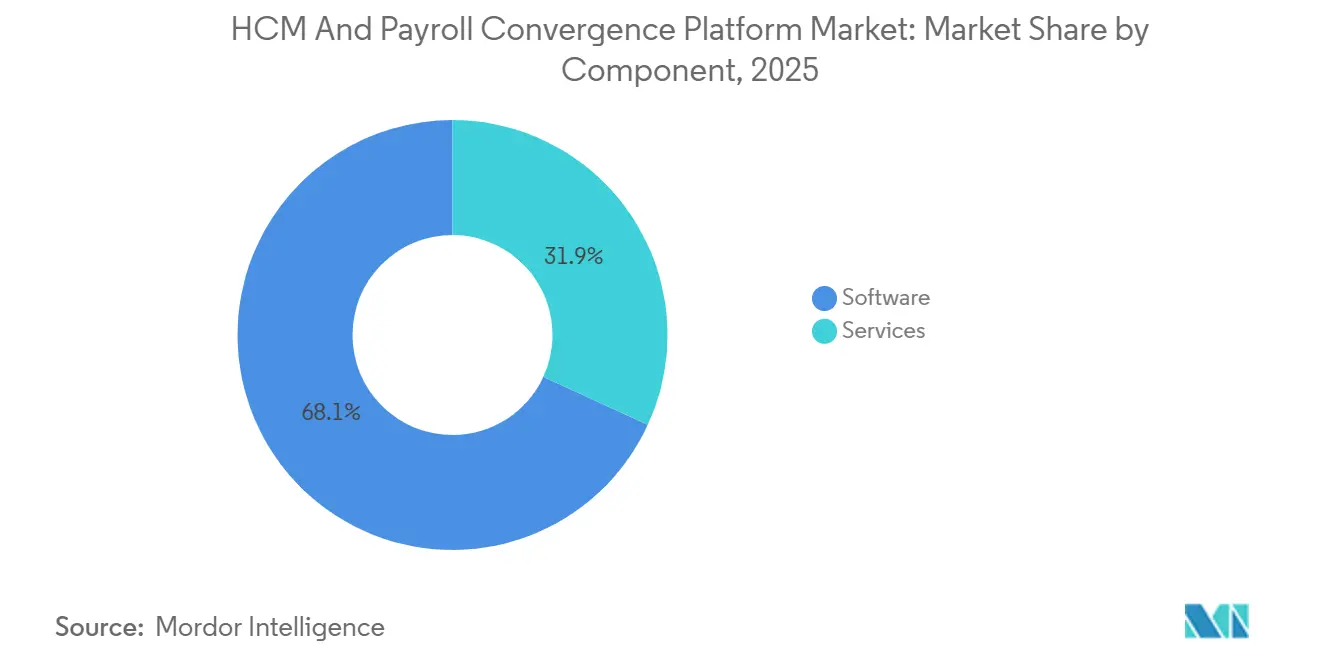

- By component, software held 68.14% of the HCM and payroll convergence platform market revenue in 2025, while services are projected to expand at a 12.47% CAGR through 2031.

- By deployment model, cloud-based deployments accounted for 70.82% of revenue in 2025, while hybrid deployments are expected to record the highest CAGR of 14.63% through 2031.

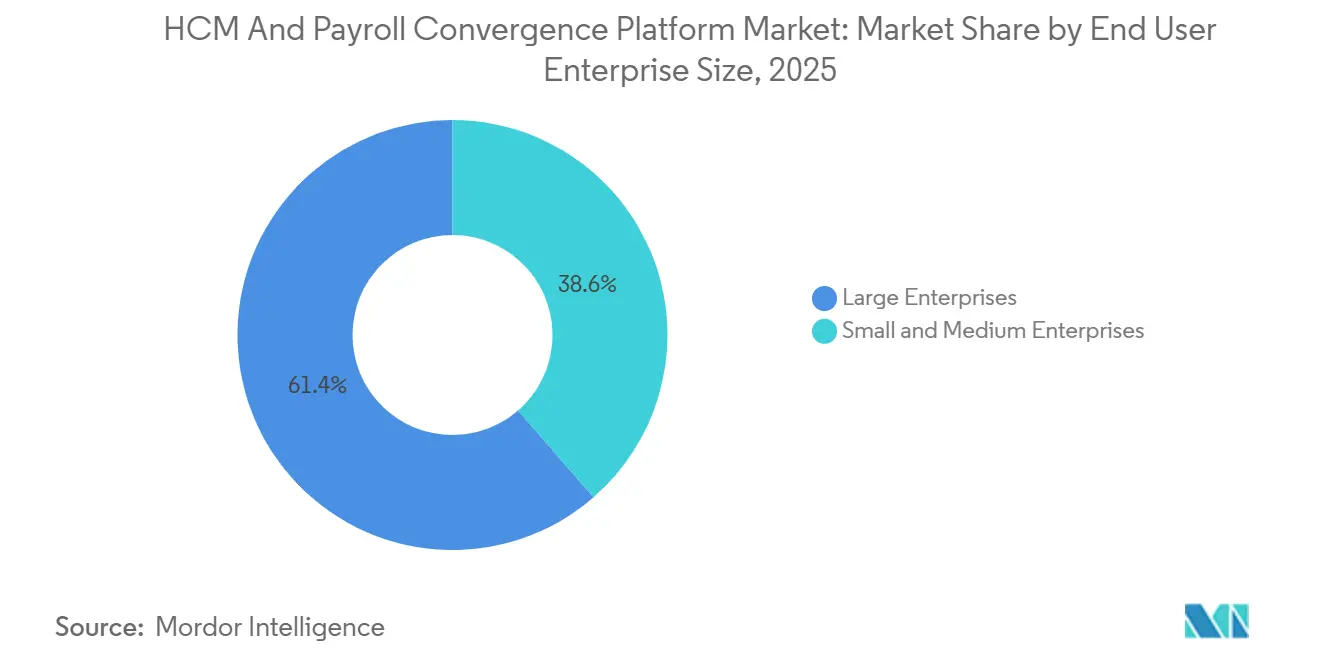

- By enterprise size, large enterprises held 61.39% of the HCM and payroll convergence platform market revenue in 2025, while small and medium enterprises are projected to grow at a 13.92% CAGR through 2031.

- By end-user industry, information technology and telecom captured 26.71% of revenue in 2025, while healthcare and life sciences are projected to expand at a 14.88% CAGR through 2031.

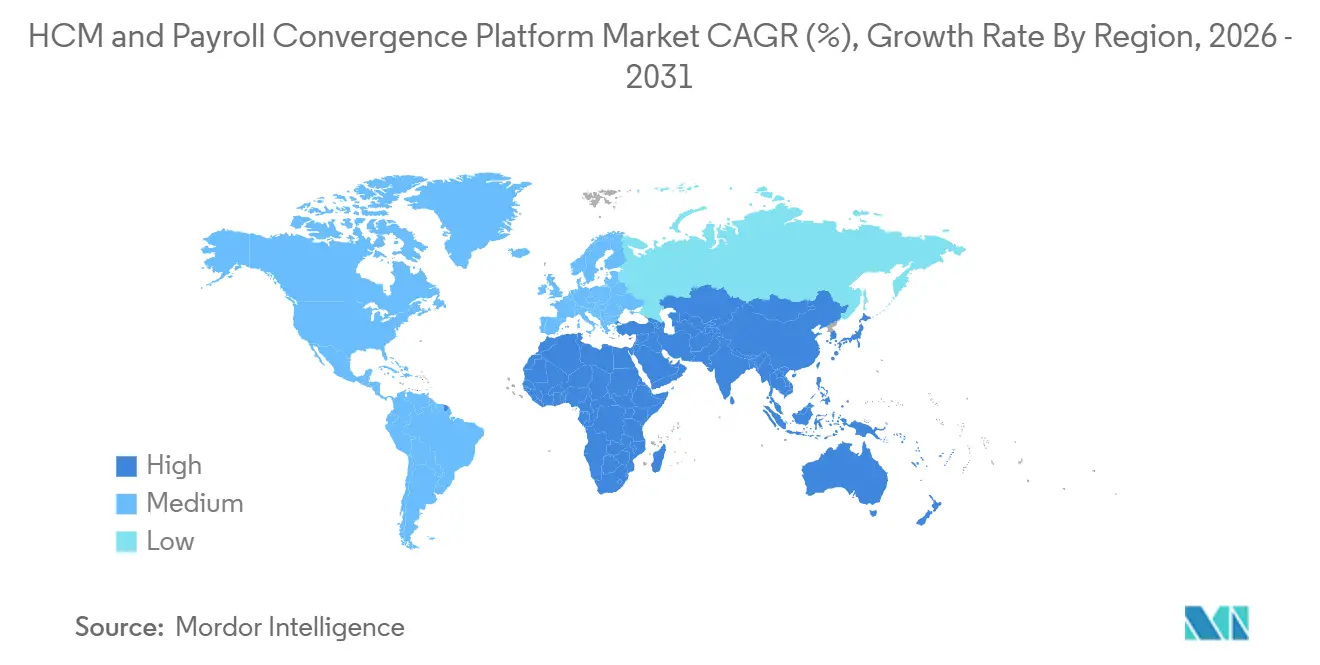

- By geography, North America accounted for 41.26% of the HCM and payroll convergence platform market revenue in 2025, while Asia-Pacific is expected to grow at the highest CAGR of 15.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM And Payroll Convergence Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud Migration From Legacy HR and Payroll Stacks | +2.8% | Global, with highest concentration in North America and Europe | Medium term (2-4 years) |

| Rising Complexity of Multi-country Payroll and Labor Compliance | +2.2% | Global, with highest intensity in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Demand for Unified Employee Experience and Self-service | +1.5% | Global | Medium term (2-4 years) |

| AI-enabled Payroll Automation and Workforce Intelligence | +1.4% | Global, with leading adoption in North America and Asia-Pacific | Short term (≤ 2 years) |

| EU Pay Transparency Directive Driving Shared Compensation Data Models | +0.7% | Europe, with spill-over to global multinationals with EU operations | Short term (≤ 2 years) |

| Convergence of Payroll With Workforce Payments and Contractor Payout Rails | +0.5% | Global, with early leadership in North America, Asia-Pacific, and EMEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud Migration from Legacy HR and Payroll Stacks

Cloud migration remains the strongest structural force in the HCM and payroll convergence platform market because older HR and payroll estates are becoming harder to maintain and slower to update. A May 2026 payroll transformation completed by SAP SE and Tata Consultancy Services delivered 30-40% faster payroll processing cycles after migration to SAP Cloud ERP Private, showing the operating advantage that cloud environments are now producing in live enterprise settings. Cloud-native platforms also make compliance updates easier because vendors can push rule changes across tenant environments at once, while on-premise users still depend on internal patching schedules and local testing cycles. This gap matters more as regulatory changes become more frequent and payroll teams have less tolerance for the lag between policy and configuration changes. SAP's standard maintenance for on-premises HCM software is due to end in 2027, turning passive interest in migration into active contract decisions for many enterprise accounts. The same pressure is evident in operating practice, as Strada reported in May 2026 that 77% of large employers still relied on manual payroll backup processes despite using an HCM platform, indicating that technical debt in legacy environments continues to slow modernization.[1]SAP SE and Tata Consultancy Services, “SAP and TCS Complete Global Payroll Transformation to SAP Cloud ERP Private,” SAP Newsroom, news.sap.com

Rising Complexity of Multi-country Payroll and Labor Compliance

Compliance complexity is rising faster than many payroll teams can absorb, keeping the HCM and payroll convergence platform market closely tied to regulatory execution rather than software preference alone. The EU Pay Transparency Directive set a June 7, 2026, transposition deadline and will require the first gender pay gap reporting cycle in June 2027 for covered employers, underscoring the need for shared compensation data models across payroll and HR systems.[2]European Parliament and Council of the European Union, “Directive 2023/970/EU of the European Parliament and of the Council on Pay Transparency,” Official Journal of the European Union, eur-lex.europa.eu Outside Europe, digital reporting frameworks such as Brazil's eSocial and India's Employees' Provident Fund Organization filing requirements are adding local configuration work that global employers cannot manage well through fragmented systems. That is why buyers increasingly value platforms that can combine centralized oversight with local rule execution and local documentation support. The operational strain does not benefit only the biggest suites; deep local compliance knowledge also protects in-country engine specialists who can deliver trusted jurisdiction coverage. As a result, the HCM and payroll convergence platform market is expanding not only through software subscriptions but also through implementation, validation, and managed payroll services that help enterprises stay compliant across multiple countries.

Demand For Unified Employee Experience and Self-service

Demand for a unified employee experience is changing how buyers evaluate the HCM and payroll convergence platform market, especially when they compare single-database systems with environments built on separate applications. Paylocity reported in its 2026 survey that only 13% of organizations operated HR and finance on a single native platform, which shows how large the remaining consolidation gap still is. Employees now expect real-time payslip access, self-service updates, and benefits interactions through one interface, and vendors that spread these tasks across multiple logins are creating unnecessary friction in daily use. This matters beyond convenience because reconciliation gaps between HR and payroll records increase finance overhead and slow basic administrative work. Single-environment platforms are therefore gaining appeal not only with HR leaders but also with finance teams that want cleaner records and fewer manual fixes. In the HCM and payroll convergence platform market, the practical value of self-service is becoming one of the clearest renewal and replacement drivers because workforce users interact with the platform far more often than procurement teams do.

AI-enabled Payroll Automation and Workforce Intelligence

AI is becoming a meaningful differentiator in the HCM and payroll convergence platform market because payroll teams want faster processing, earlier anomaly detection, and fewer manual checks before finalization. UKG launched Pro Pay with Workforce AI in May 2026 and positioned the offering around anomaly detection using up to 5 years of data, enabling pay cycle issue resolution to be compressed from days to hours. ADP also expanded AI activity in 2026, deploying its AI Payroll Variance agent across more than 40 countries and reporting that 49% of Asia-Pacific organizations were exploring AI for learner payroll operations, while 33% named AI as their primary technology investment priority for the next 2-3 years. The advantage is becoming structural, as vendors with long histories of payroll transactions can train models on deeper, country-level data than newer entrants can access. That gives leading platforms a better chance of spotting variance patterns, detecting risky exceptions, and improving automation accuracy across recurring payroll cycles. If this trend continues, the HCM and payroll convergence platform market will become more clearly divided between vendors with durable AI data depth and those that add only surface-level AI features without the same transaction history.[3]Paylocity, “State of HR Technology Survey 2026,” Paylocity, paylocity.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Switching Costs and Payroll Data Migration Risk | -1.8% | Global | Long term (≥ 4 years) |

| Data Privacy, Cybersecurity, and Cross-border Data Transfer Exposure | -1.4% | Global, with highest sensitivity in Europe and Asia-Pacific | Medium term (2-4 years) |

| In-country Payment Rail Fragmentation and Local Banking Mandates | -1.1% | Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Limited Native Country Engine Coverage Behind Aggregated Global Claims | -0.9% | Global, with concentration in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Switching Costs And Payroll Data Migration Risk

Switching costs remain one of the strongest brakes on the HCM and payroll convergence platform market, as payroll migration carries direct financial, legal, and reputational risks. Strada's May 2026 findings on manual payroll backup dependence show that even organizations with HCM platforms still rely on fallback processes, indicating the extent of operational caution around payroll change programs. The difficulty is not limited to system cutover, since enterprises must also convert historical records, run parallel validations, test local rules, and document every step for audit readiness. That makes established vendors harder to displace because their embedded payroll configurations often hold years of organization-specific logic that buyers hesitate to disturb. The result is an HCM and payroll convergence platform market where dissatisfaction alone is rarely enough to trigger replacement, and challengers must usually prove lower migration risk before they can prove better product economics.

Data Privacy, Cybersecurity, And Cross-border Data Transfer Exposure

Data privacy and cybersecurity are constraining the HCM and payroll convergence platform market because payroll systems contain both personally identifiable information and financially material transaction data. Microsoft published threat intelligence in April 2026 describing Storm-2755, a payroll-focused attack path that targeted salary rerouting via compromised self-service portals and exploited session tokens to bypass common controls.[4]Microsoft, “Storm-2755 Payroll Attack Vector, Threat Intelligence Report,” Microsoft Security Blog, microsoft.com ADP also reported that 44% of Asia-Pacific organizations had experienced a cybersecurity incident directly affecting payroll systems, showing that the risk is no longer theoretical in fast-digitizing payroll environments. At the same time, GDPR in Europe and similar frameworks elsewhere require vendors to handle data residency, transfer controls, and compliance design by jurisdiction, which raises cost and technical complexity for cross-border payroll architectures. Verizon's 2024 breach report found that 68% of breaches involved a human element, indicating that vendors are increasingly expected to support governance, training, and controls for payroll-specific risk rather than offering only platform security features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads Revenue While Services Scale With Complexity

Software accounted for 68.14% of total revenue in 2025 and remained the anchor of the HCM and payroll convergence platform market, as subscription licensing still accounts for the largest share of enterprise budgets. Software held 68.14% of the HCM and payroll convergence platform market share in 2025, showing that buyers continue to prioritize core platform ownership before layering external support. Within this layer, core HR and payroll remained the base contract for most buyers, and that base is still the point from which vendors expand into time and attendance, benefits administration, talent tools, and workforce management. Demand is moving quickly toward global payroll orchestration and analytics modules, as employers seek a single view of payroll registers, workforce costs, and compliance status across jurisdictions. That expansion pattern keeps software central to vendor revenue because each additional module makes the platform harder to replace and more valuable to finance and HR teams.

Services are projected to expand at a 12.47% CAGR through 2031, making them the fastest-growing component of the HCM and payroll convergence platform market, despite starting from a smaller revenue base. This growth reflects the fact that many buyers can purchase software faster than they can configure governance, validate local rules, and manage live cutovers across countries. Multi-country deployments still need implementation consulting, managed payroll support, parallel-run testing, and change management, especially when internal HR teams lack jurisdiction-specific expertise. AI-assisted templates and pre-configured country workflows may shorten parts of the deployment process, but they do not eliminate the need for specialist services. Instead, they are shifting service effort toward governance, exception handling, and long-term optimization inside the HCM and payroll convergence platform industry.

By Deployment Model: Hybrid Architecture Supports Controlled Modernization

Cloud-based deployment accounted for 70.82% of revenue in 2025, reflecting the long-standing preference for SaaS in new implementations across the HCM and payroll convergence platform market. Cloud platforms remain attractive because they simplify updates, reduce internal infrastructure burdens, and support a cleaner employee self-service experience than many older local installations. That advantage is strongest in organizations that want faster compliance updates and a more unified interface across HR, payroll, and workforce management. Even so, the installed base of regulated enterprises still limits how quickly some workloads can be fully migrated to public cloud environments. On-premises systems, therefore, retain a meaningful role in sectors where data residency, audit practice, or internal risk controls still favor local processing.

Hybrid deployment is projected to record a 14.63% CAGR through 2031, making it the fastest-growing model and an important part of the HCM and payroll convergence platform market size discussion for phased modernization. Mercans and PayrollOrg reported in 2025 that 37% of organizations used a hybrid in-house and outsourced payroll model, while 21% fully outsourced to in-country providers, underscoring why a flexible delivery architecture remains commercially important. Large enterprises often prefer to keep calculation engines or sensitive country processes in place while moving self-service, workforce management, and analytics to the cloud. Vendors with connectors to older SAP, Oracle, and PeopleSoft estates are benefiting from this pattern, as it reduces cutover risk without forcing a full replacement on day 1. In the HCM and payroll convergence platform industry, hybrid is acting less like a temporary compromise and more like a practical long-term model for organizations with layered ERP estates and strict governance requirements.

By End User Enterprise Size: SME Adoption Gains Speed As Usability Improves

Large enterprises accounted for 61.39% of revenue in 2025 and remained the primary spending center in the HCM and payroll convergence platform market, as global payroll complexity, mobility needs, and entity-level governance demands are highest in this segment. These buyers often operate across many tax jurisdictions and hold years of embedded payroll rules, which makes convergence platforms valuable but also lengthens sales, implementation, and displacement cycles. Enterprise contracts are therefore large, but they require stronger executive sponsorship and tighter validation than smaller deals. This dynamic helps scaled incumbents because buyers place a heavy weight on compliance documentation, implementation history, and the ability to support complex local requirements. It also means that renewal defense matters almost as much as new customer acquisition at the top end of the market.

Small and medium enterprises are projected to grow at a 13.92% CAGR through 2031, making them the fastest-growing size segment in the HCM and payroll convergence platform market. Gusto announced in April 2026 that it had reached 500,000 small-business customers and introduced 75 new features, including AI-generated payslips, ChatGPT integration, and Slack-based payroll query handling, signaling that the platform's usability has moved decisively downmarket. This shift matters because SMEs often lack dedicated HR operations teams and need platforms that reduce reliance on specialists rather than adding process complexity. Buyers in this segment respond strongly to easy onboarding, simple compliance workflows, and a single interface that combines employee records, payroll, and support tasks. As that product design improves, the HCM and payroll convergence platform market is expanding beyond traditional enterprise buyers and attracting organizations that once relied on accountants, local bureaus, or disconnected tools.

By End-user Industry: Technology Holds The Largest Share While Healthcare Expands Fastest

Information technology and telecom accounted for 26.71% of total revenue in 2025 and remained the largest vertical in the HCM and payroll convergence platform market, as these organizations tend to run distributed workforces and adopt digital self-service earlier than many other sectors. Workday reported USD 8.4 billion in fiscal year 2025 revenue and noted broad enterprise penetration, which reflects the depth of spending on integrated workforce systems among technology-heavy customer groups. Demand in this vertical is shaped by globally distributed teams, high employee-to-revenue ratios, and a strong preference for unified digital workflows. Retail and e-commerce followed a different pattern, with hourly workforces, seasonal staffing, and shift-rule complexity making time-and-attendance integration critical to payroll accuracy. Government and public sector adoption also continued, but procurement stayed slower because tender cycles, certifications, and local hosting commitments remain central to public buying decisions.

Healthcare and life sciences are projected to expand at a 14.88% CAGR through 2031, the highest rate among end-user industries in the HCM and payroll convergence platform market size by vertical growth. This pace reflects the operational challenges posed by shift-differential pay, clinical staffing ratio rules, and the growing link between workforce cost visibility and scheduling decisions. Healthcare employers need payroll data that closely aligns with labor analytics, as staffing costs are frequently reviewed and often tied directly to service delivery decisions. Industrial manufacturing is also benefiting from closer ties between time capture, machine utilization, and labor cost attribution, while BFSI continues to value platforms that can support variable compensation and disclosure requirements. Across the broader HCM and payroll convergence platform market, growth is spreading into education, hospitality, logistics, and other structured-employment fields as implementation barriers fall and integrated platforms become easier to adopt.

Geography Analysis

North America accounted for 41.26% of global revenue in 2025 and represented the largest regional position in the HCM and payroll convergence platform market. North America held 41.26% of the HCM and payroll convergence platform market share in 2025, supported by a deep installed base of enterprise HCM suites and mature HR technology procurement practices. The United States remains the main engine because employers face frequent payroll tax obligations and a growing mix of state-level leave and wage rules that favor ongoing platform investment. Paylocity's 2026 survey also showed that only 13% of organizations operated HR and finance on a single native platform, which confirms that large replacement and consolidation opportunities still exist in the region. Canada and Mexico add to this demand through cross-border workforce mobility and the complexity of contractor payments, pushing mid-market firms toward native multi-jurisdictional capability.

Europe remained the second-largest region in the HCM and payroll convergence platform market and carried the heaviest regulatory burden. The EU Pay Transparency Directive set a June 7, 2026, transposition deadline and will require annual gender pay gap reporting for covered employers from June 2027, pushing organizations toward unified HR and payroll records that support compensation analysis and reporting. Germany and the United Kingdom remained the two largest national markets in the region because codetermination rules, contractor status complexity, and local compliance expectations all increase integration needs. Personio reported its first profitable quarter in Q1 2026, with 16,000 customers and 1.5 million end users, demonstrating that integrated HR and payroll demand in the European SME base has reached meaningful scale. South America is also gaining relevance as Brazil's eSocial framework and Argentina's wage indexation complexity increase demand for platforms with stronger native regional compliance support.

Asia-Pacific is projected to grow at a 15.12% CAGR through 2031, making it the fastest-growing region in the HCM and payroll convergence platform market. ADP reported in March 2026 that 49% of organizations in the region were exploring AI for learner payroll operations, and 33% viewed AI as their primary technology investment priority for the next 2-3 years, highlighting both the urgency of modernization and the willingness to adopt new payroll tools. India and Southeast Asia are benefiting from payroll formalization, while China, Australia, and Japan continue to raise digital filing expectations that support platform upgrades. In the Middle East and Africa, demand is being shaped by workforce nationalization programs, the formalization of payroll infrastructure, and mobile-first adoption in early-stage markets, extending the HCM and payroll convergence platform market opportunity beyond the most mature enterprise regions.

Competitive Landscape

The HCM and payroll convergence platform market is fragmented at the top tier, but rivalry remains active because scale incumbents and fast-moving challengers are approaching the same budgets from different entry points. Automatic Data Processing, Inc., Dayforce, Inc., and UKG Inc. continue to hold strong positions in enterprise accounts where buyers value global engine breadth, compliance documentation, and implementation depth. At the same time, Deel Inc., Rippling People Center Inc., and Gusto, Inc. are gaining relevance by using contractor payments, employer-of-record services, and product-led growth to enter accounts that once would have defaulted to traditional suite vendors. This creates a market where leadership is real but not uncontested, and where competitive pressure comes from both replacement risk and category expansion into adjacent workflows. The HCM and payroll convergence platform market, therefore, rewards vendors that can combine trust, coverage, usability, and deployment flexibility rather than relying on only one advantage.

Incumbents are defending share through broader suites and more unified commercial offers. ADP launched the ADP WorkForce Suite in November 2025 after integrating WorkForce Software, bringing Workforce Now, Lyric HCM, and Global Payroll into a single platform for large enterprises. Dayforce also shifted its sales posture in February 2026 by publishing ROI documentation for board-level and CFO audiences, demonstrating how vendors are increasingly using business-case evidence to support consolidation budgets. UKG moved in a similar direction with its May 2026 Pro Pay with Workforce AI launch, focusing on anomaly detection and faster issue resolution for the pay cycle.

Challengers are expanding by widening geographic coverage and tying payroll more closely to workforce payments. Rippling expanded its employer-of-record infrastructure to 80 countries by March 2026, up from 40, and added native payroll engines in Brazil, Mexico, the Philippines, and Spain, which sharpened its position in multi-country payroll corridors. Papaya Global and Tech Mahindra formed an alliance in April 2026 covering 180 countries, increasing the scale at which they can pursue integrated payroll and employer-of-record services for multinationals. Deel also launched Big Deel 2026 as a unified platform for hiring, compensation management, payroll, and global operations, reinforcing its move from employer-of-record roots into broader HCM and payroll-convergence platform competition. As a result, the HCM and payroll convergence platform market is becoming harder to cleanly segment by legacy vendor type, as payroll, workforce management, compliance, and global hiring capabilities are converging within the same platform decisions.

HCM And Payroll Convergence Platform Industry Leaders

Automatic Data Processing, Inc.

Paychex, Inc.

UKG Inc.

Dayforce, Inc.

Paycom Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Paychex, Inc. launched WISE, an agentic AI platform integrating Flex, Paycor, and SurePayroll across its 800,000-customer base. WISE deployed conversational AI agents for payroll processing, HR compliance, and workforce analytics, positioning Paychex as the first legacy payroll bureau to commercialize a multi-brand agentic AI stack under unified governance.

- May 2026: SAP SE and Tata Consultancy Services completed a global payroll transformation migrating enterprise clients to SAP Cloud ERP Private, delivering 30-40% faster payroll processing cycles. The migration established a quantifiable benchmark for cloud-native payroll performance and accelerated decision timelines for enterprises evaluating on-premise maintenance extension ahead of SAP's 2027 standard maintenance end date.

- May 2026: UKG Inc. launched Pro Pay with Workforce AI, an agentic payroll module incorporating five-year anomaly detection capability. The system compressed pay cycle resolution from days to hours and autonomously flagged cross-cycle discrepancies before payroll finalization, reducing late-payment regulatory exposure for global enterprise clients.

- April 2026: Gusto, Inc. announced it reached 500,000 small-business customers and released 75 new product features, including AI payslip generation, native ChatGPT integration, and Slack-based payroll query resolution. The milestone confirmed product-led growth as a commercially scalable acquisition strategy for SME-tier converged HCM-payroll platforms.

Global HCM And Payroll Convergence Platform Market Report Scope

The HCM and Payroll Convergence Platform market comprises integrated technology solutions and services that unify human capital management functions with payroll operations, spanning core HR, workforce management, talent management, time and attendance, benefits administration, workforce analytics, and global payroll orchestration. Delivered through cloud-based, on-premises, and hybrid models, these platforms serve both large enterprises and SMEs across industries, including BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The core purpose of this market is to provide a centralized, automated, and data-driven system that enhances compliance, reduces operational complexity, improves workforce productivity, and delivers a seamless employee experience by converging HR and payroll into a single platform.

The HCM and Payroll Convergence Platform market report is segmented by Component (Software, [Core HR and Payroll, Workforce Management, Talent Management, Time and Attendance, Benefits Administration, Workforce Analytics and AI, and Global Payroll Orchestration] and Services), Deployment Model (Cloud-based, On-premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Core HR and Payroll |

| Workforce Management | |

| Talent Management | |

| Time and Attendance | |

| Benefits Administration | |

| Workforce Analytics and AI | |

| Global Payroll Orchestration | |

| Services |

| Cloud-based |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Core HR and Payroll |

| Workforce Management | ||

| Talent Management | ||

| Time and Attendance | ||

| Benefits Administration | ||

| Workforce Analytics and AI | ||

| Global Payroll Orchestration | ||

| Services | ||

| By Deployment Model | Cloud-based | |

| On-premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the HCM and payroll convergence platform market?

The HCM and payroll convergence platform market was valued at USD 27.48 billion in 2025, is estimated at USD 29.77 billion in 2026, and is projected to reach USD 47.65 billion by 2031 at a 9.86% CAGR.

Why are enterprises consolidating HR and payroll systems now?

Buyers are moving away from fragmented integration-layer architectures because unified platforms improve compliance response, reduce reconciliation work, and give leadership a single source of truth for workforce and pay data.

Which deployment model is growing the fastest?

Hybrid deployment is the fastest-growing model, with a 14.63% CAGR through 2031, because many large employers prefer phased modernization over full cutover of sensitive payroll records.

Which regions are leading adoption and growth?

North America led with 41.26% of revenue in 2025, while Asia-Pacific is projected to grow the fastest at a 15.12% CAGR through 2031 due to payroll formalization, digital tax filing, and multinational workforce expansion.

Which customer groups are creating the strongest new demand?

Small and medium enterprises are the fastest-growing size segment at 13.92% CAGR, and healthcare and life sciences is the fastest-growing end-user vertical at 14.88% CAGR.

What is the biggest challenge vendors and buyers still face?

Payroll migration risk remains the main barrier because switching platforms involves historical data conversion, multi-country validation, and the risk of wage, compliance, and reputational errors during cutover.

Page last updated on: