Payroll Software In Retail and Hospitality Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

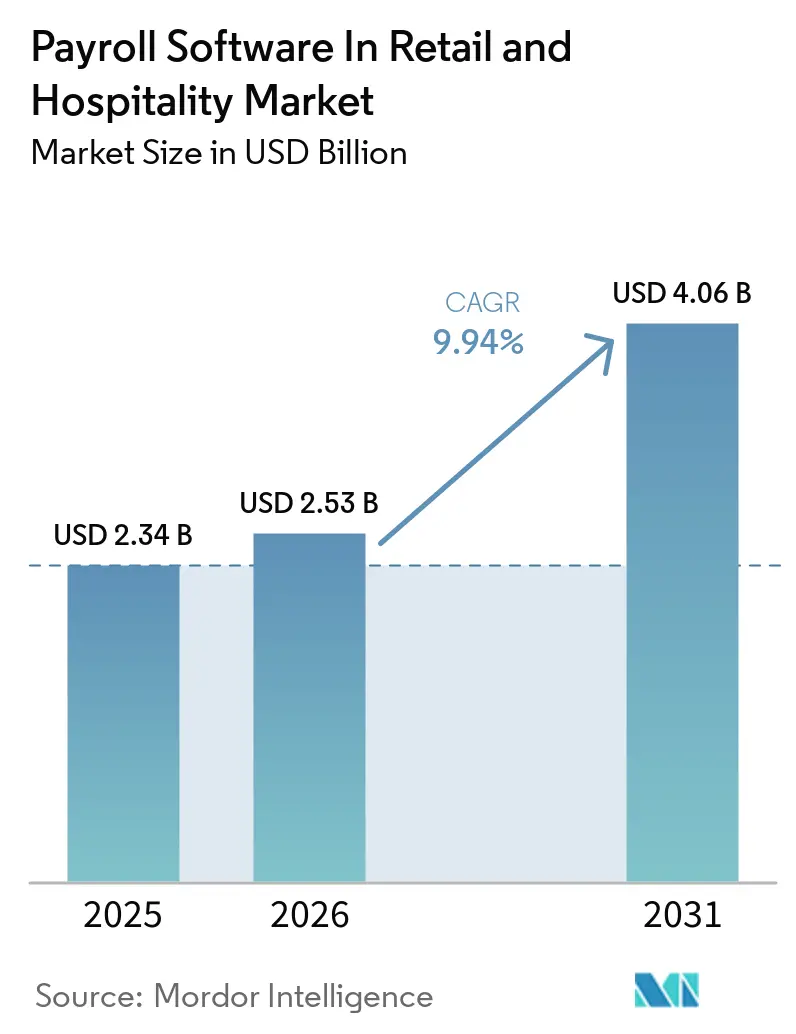

| Market Size (2026) | USD 2.53 Billion |

| Market Size (2031) | USD 4.06 Billion |

| Growth Rate (2026 - 2031) | 9.94% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payroll Software In Retail and Hospitality Market Analysis by Mordor Intelligence

The payroll software in retail and hospitality market size was USD 2.34 billion in 2025 and is projected to reach USD 2.53 billion and USD 4.06 billion by 2031, at a CAGR of 9.94% from 2026 to 2031. The payroll software in retail and hospitality market is expanding because payroll is now tied much more closely to workforce planning, compliance control, and frontline retention than it was in the past. Growth is also supported by stronger cloud infrastructure, rising cross-jurisdiction payroll obligations, and broader adoption of earned wage access and tip-management tools across shift-based businesses. Buyers are placing more value on platforms that connect payroll with time capture, schedule data, and reporting, because payroll accuracy now depends on clean data movement across several operating systems. Vendors with deep regulatory libraries and stronger update cycles are gaining an advantage, since changing wage rules, tax treatments, and reporting mandates are raising switching costs for employers. The payroll software in retail and hospitality market also has room to grow among smaller operators, where affordable cloud pricing, mobile-first workflows, and modular service models are making modern payroll systems more practical than manual or outsourced alternatives.

Key Report Takeaways

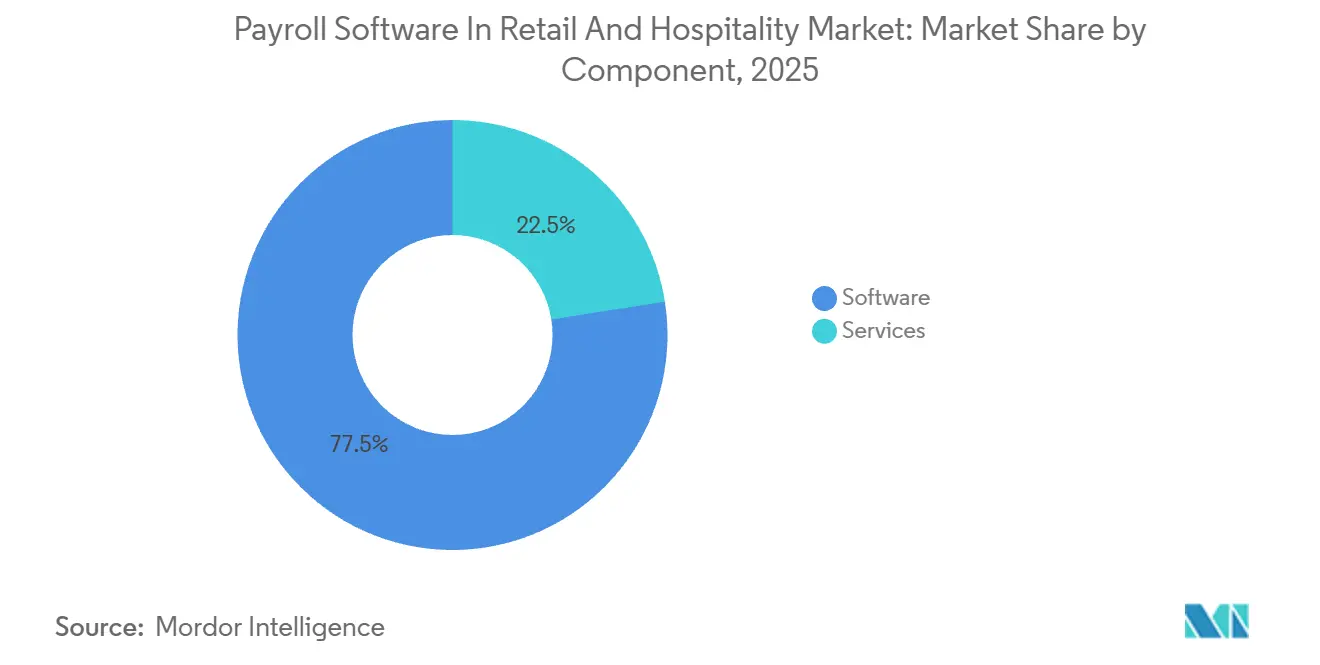

- By component, software led with 77.48% revenue share in 2025 of the payroll software in retail and hospitality market, while services is forecast to expand at a 10.68% CAGR through 2031.

- By organization size, large enterprises held 64.92% share in 2025, while SMEs recorded the highest projected CAGR at 10.12% through 2031.

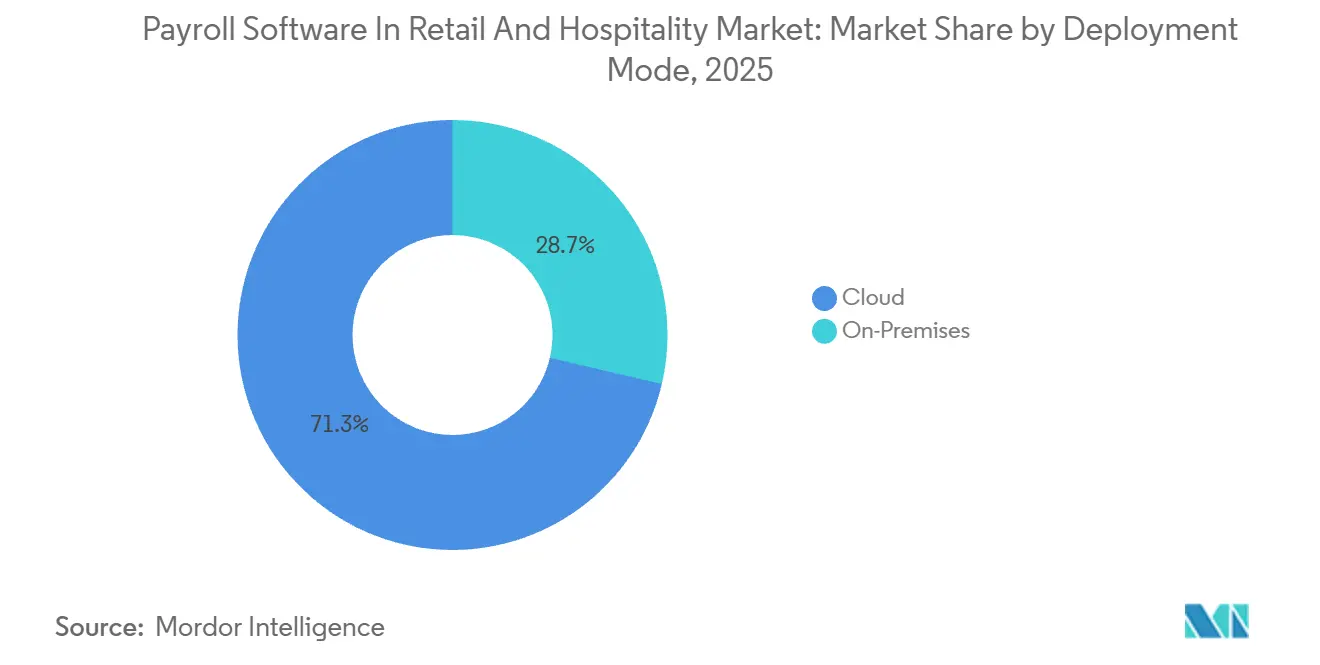

- By deployment mode, cloud accounted for 71.34% share in 2025 and also posted the fastest projected CAGR at 10.44% through 2031.

- By functionality, core payroll processing held a 33.86% share in 2025, while payroll analytics and reporting is projected to grow at an 11.58% CAGR through 2031.

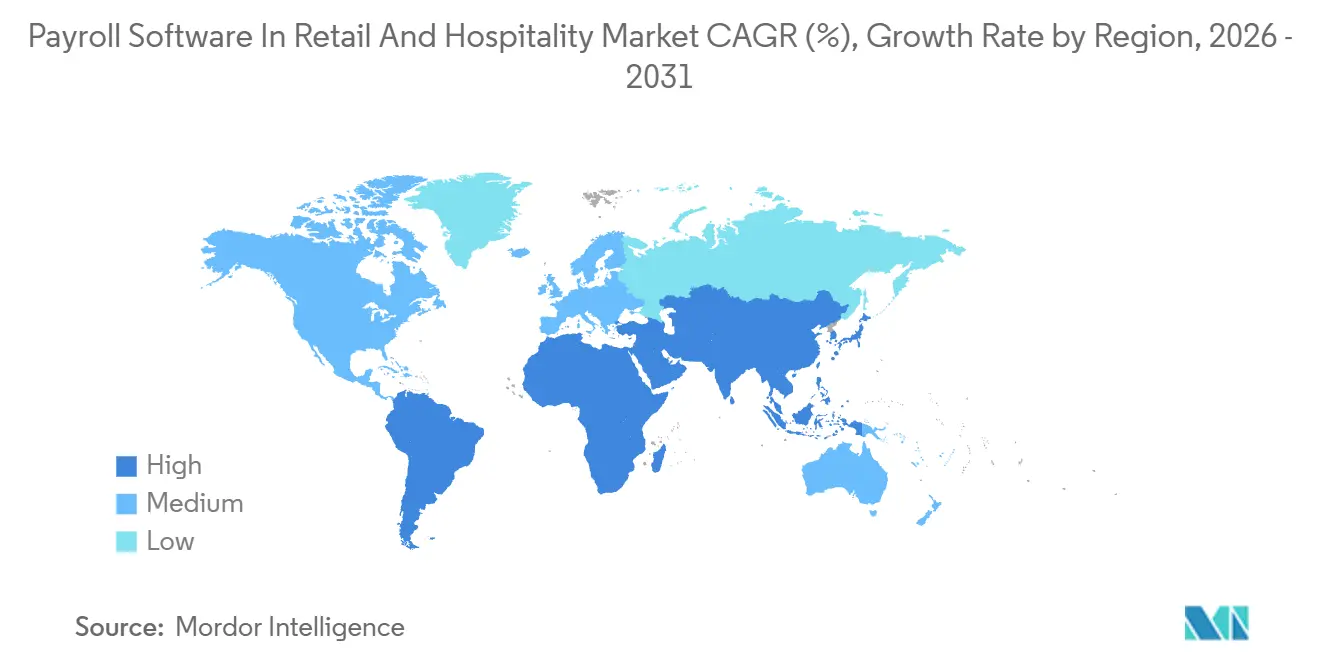

- By geography, North America accounted for 35.74% share in 2025 of the payroll software in retail and hospitality market, while Asia-Pacific is forecast to expand at an 11.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Payroll Software In Retail and Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption Of Cloud-Based Payroll Solutions | +2.8% | Global, with peak intensity in North America and Western Europe | Short term (≤ 2 years) |

| Increasing Compliance Complexity In Retail And Hospitality | +2.2% | Global, acute in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Rising Demand For Integrated HR And Payroll Suites Among SMEs | +1.6% | North America, Asia-Pacific, and Western Europe | Medium term (2-4 years) |

| Workforce Digitalization Accelerated By COVID-19 Recovery | +1.1% | Global, with catch-up momentum in South America, Middle East, and Southeast Asia | Medium term (2-4 years) |

| Surge In Multi-Country Seasonal Staffing Patterns Driving Real-Time Global Payroll | +0.8% | Europe, Middle East, and Asia-Pacific tourist corridors | Long term (≥ 4 years) |

| Expansion Of On-Demand Pay And Tip Management Features In Hospitality Chains | +0.5% | North America and Western Europe, with early adoption in GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption Of Cloud-Based Payroll Solutions

Cloud payroll has become a practical operating standard for multi-location retailers and hospitality groups, not just a lower-cost IT option. The payroll software in retail and hospitality market is benefiting from this shift because cloud systems support real-time synchronization across outlets, easier updates, and mobile access for frontline workers and managers. UKG stated that its One View multi-country payroll suite supports payroll across 120 currencies and more than 150 countries, which shows the scale advantage that cloud architecture now offers to employers with distributed workforces.[1]UKG, “UKG Tackles Next Multi-Country Payroll Pain Point With UKG One View Suite Enhancements,” UKG, ukg.com This means the payroll software in retail and hospitality market is being pushed by compliance and operating discipline at the same time, which gives cloud-first vendors a clear near-term advantage.

Increasing Compliance Complexity In Retail And Hospitality

Retail and hospitality payroll must absorb constant changes in tip treatment, overtime rules, minimum wage requirements, and location-specific filing standards. The payroll software in retail and hospitality market is gaining support from this pressure because fragmented or manual payroll setups are much less able to keep pace with frequent rule changes. Strada Global reported that per-country payroll complexity scores rose by an average of 5% in 2025, which confirms that payroll regulation is becoming more difficult to manage across markets. In the United States, IRS Notice 2025-69 confirmed separate W-2 reporting for qualified tips and qualified overtime compensation starting with the 2026 tax year, which forces vendors to redesign tip-tracking, withholding, and reporting logic. In France, hospitality payroll must also account for sector-specific calculations such as night work premiums, split-shift allowances, Sunday and holiday pay, and benefit-in-kind meal treatment under the CCN HCR framework, which raises the value of specialized payroll engines. The payroll software in retail and hospitality market is therefore favoring providers with dedicated compliance engineering depth, while smaller vendors face growing pressure to keep up.

Rising Demand For Integrated HR And Payroll Suites Among SMEs

The SME opportunity remains large because many smaller operators still rely on manual timesheets, basic accounting support, or entry-level tools that were not built for shift-heavy payroll complexity. The payroll software in retail and hospitality market is seeing stronger demand from this buyer group as lower-cost cloud products begin to close the feature gap with enterprise systems. The move toward integrated HR and payroll also aligns with retention needs, because employers want payroll, attendance, and employee access tools to work together rather than sit in separate systems. As a result, the payroll software in retail and hospitality market is opening faster for vendors that package payroll with self-service, scheduling links, and compliance automation in a format that smaller businesses can afford.

Workforce Digitalization Accelerated By COVID-19 Recovery

The labor rebuilding cycle after the pandemic exposed the limits of cash tips, paper timesheets, and manual payroll processes in fast-moving service environments. The payroll software in retail and hospitality market is still benefiting from that reset because operators who rehired at scale needed faster onboarding, cleaner time capture, and more flexible wage access. The CFPB issued an advisory opinion in December 2025 that supported employer-integrated earned wage access programs, and that helped reduce a major policy uncertainty around payroll-linked EWA tools. EBRI findings reported by Hospitality Technology in March 2025 showed that 75% of hospitality EWA users accessed wages at least weekly, and 57% used EWA to avoid borrowing from friends or family. These patterns matter because they position payroll systems as part of employee retention and financial wellness, not only as back-end payment software, which broadens the role of the payroll software in retail and hospitality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Sensitivity And Narrow Margins In Small Hospitality Businesses | -1.5% | Global, most acute in South America, Africa, and rural North America and Europe | Medium term (2-4 years) |

| Data Security And Privacy Concerns Over SaaS Payroll | -0.9% | Global, heightened in Europe, China, and Singapore | Short term (≤ 2 years) |

| Fragmented POS And Time-Clock Ecosystems Hindering Seamless Payroll Integration | -0.6% | Global, most acute in multi-unit retail chains and full-service restaurant groups | Medium term (2-4 years) |

| Slow Internet Penetration In Rural Tourist Destinations Limits Cloud Adoption | -0.3% | South America, Africa, and parts of Southeast Asia and Central Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost Sensitivity And Narrow Margins In Small Hospitality Businesses

Small hospitality operators remain highly price sensitive, which limits payroll software penetration even when the operational case is clear. The payroll software in retail and hospitality market faces this friction most strongly, where restaurants, cafés, and small hotels operate with thin margins and limited room for new monthly subscriptions. PayFit noted that food and beverage establishments often run on pre-tax margins of 3-5%, while personnel costs can represent 30-40% of revenue, which leaves little discretionary budget for software spend. This pressure tends to push very small employers toward external payroll processing, accountant-led workflows, or basic digital tools instead of full-featured payroll platforms. For the payroll software in retail and hospitality market, that means vendors need entry-level pricing, modular packaging, and a clear payback story if they want stronger adoption below the 50-employee threshold.

Data Security And Privacy Concerns Over SaaS Payroll

Payroll carries highly sensitive information, including wages, tax identifiers, bank data, and, in hospitality, daily tip flows and payout records. The payroll software in retail and hospitality market must therefore win trust not only in functionality but also in hosting, data handling, and audit readiness. This issue becomes more complex when payroll platforms exchange employee data with POS systems, scheduling tools, and EWA networks, because each connection expands the surface for operational or regulatory failure. The CFPB's December 2025 support for employer-integrated wage access also came with greater attention to how payroll-linked financial data moves through third-party payment and settlement paths. In practice, the payroll software in retail and hospitality market is consolidating around providers that can absorb the cost of certifications, security controls, and formal compliance processes more easily than smaller entrants can.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Share As Complexity Deepens

Software held 77.48% of the market in 2025, which kept it as the leading revenue component across the payroll software in retail and hospitality market. That position reflects the central role of subscription-based payroll engines that combine processing, compliance support, and workforce data in one environment. Buyers continue to treat the software layer as the system of record, especially when they need strong control over time capture, tax treatment, and reporting accuracy. The same buyer behavior also explains why platforms with stronger integration depth still command the largest part of spending in the payroll software in retail and hospitality market.

The services segment is expanding at a 10.68% CAGR through 2031, which makes it the faster-growing component in the payroll software in retail and hospitality market size. Growth is being driven less by one-time implementation and more by managed payroll outsourcing, compliance support, and vendor-led operational execution. SD Worx stated that it processes more than 6 million payrolls each month across more than 95,000 clients, including hotel brands such as Hesperia and Ibis in Spain and France, which shows how service depth supports large-volume payroll environments.[2]SD Worx España, “Software De Gestión De Nóminas,” SD Worx España, sdworx.es This shift changes the buy-versus-build balance in the payroll software in retail and hospitality industry because employers with complex schedules and limited HR teams increasingly value risk transfer as much as software ownership. Once a provider manages filings, calculations, and local compliance tasks directly, customer stickiness rises and replacement becomes harder. That is why services is growing faster even though software still anchors most revenue. The payroll software in retail and hospitality market is therefore moving toward a model where software creates the core platform and services deepen account value over time.

By Organization Size: Enterprise Revenue Leads While SMEs Set The Pace

Large enterprises held 64.92% of the payroll software in retail and hospitality market share in 2025, which reflects their broader payroll complexity and higher contract values. Large retailers and hotel groups need multi-country support, consolidated workforce data, and dependable integration with adjacent HR systems. They also manage larger frontline headcounts, more locations, and heavier compliance exposure, which supports premium spending on payroll architecture. This keeps enterprise accounts central to revenue across the payroll software in retail and hospitality market.

At the same time, SMEs are projected to grow at a 10.12% CAGR through 2031, making them the faster-moving customer group. That growth is supported by cloud-native pricing, mobile employee self-service, and products that package payroll with practical compliance automation. UKG's December 2025 acquisition of Inova Payroll, which supported more than 4,000 SMBs with frontline-heavy workforces, showed that major vendors see outsourced and smaller business payroll as a strategic growth zone rather than a side segment. The payroll software in retail and hospitality industry is adjusting to this shift as enterprise vendors move downstream and newer entrants move upmarket with broader product bundles. SME buyers were historically the least well served by legacy platforms, but that gap is narrowing. This change should keep the payroll software in retail and hospitality market on a broader growth base through 2031, even as enterprise contracts remain the main revenue anchor. It also raises competitive pressure on pricing, onboarding speed, and ease of use, because these factors matter more to SMEs than feature depth alone.

By Deployment Mode: Cloud Holds Both The Lead And The Fastest Growth

Cloud deployment accounted for 71.34% of the market in 2025 and is expected to expand at a 10.44% CAGR through 2031, which gives it both leadership and momentum in the payroll software in retail and hospitality market size. This pattern is unusual in software categories, but it fits the needs of retail and hospitality employers that manage shifting schedules, multiple outlets, and frequent employee changes. Cloud systems are better aligned with real-time compliance updates, mobile worker access, and shared visibility across locations. The payroll software in retail and hospitality market has therefore moved well past the point where cloud is a secondary option for most buyers.

Cloud is also benefiting from the practical reality that many operators cannot maintain separate payroll infrastructure across distributed properties or stores. UKG's multi-country payroll positioning points to the value of a unified process that can coordinate local providers while preserving standard controls across jurisdictions. In day-to-day operations, that matters because payroll teams need updates to flow quickly when wage, tax, or reporting rules change. On-premises tools still retain relevance in specific enterprise environments where payroll sits close to existing ERP architecture or where hosting preferences remain strict. Even so, those cases look more transitional than stable. The payroll software in retail and hospitality market is increasingly structured around cloud delivery, while hybrid support is becoming the bridge for slower adopters rather than the long-term destination. This makes deployment a strategic differentiator, since vendors that combine cloud speed with local compliance depth are best positioned to capture migration demand.

By Functionality: Analytics Is Broadening Payroll Beyond Processing

Core payroll processing held 33.86% share in 2025, which kept it as the largest functional category in the payroll software in retail and hospitality market. That result is expected because wage calculation, disbursement, and filing remain the base requirements for every employer. Core processing still carries the largest installed footprint, especially where buyers first modernize payroll before expanding into adjacent tools. It remains the entry point through which vendors establish trust and long-term account control in the payroll software in retail and hospitality market.

Payroll analytics and reporting is forecast to grow at an 11.58% CAGR through 2031, which makes it the fastest-growing functionality in the payroll software in retail and hospitality market size. Employers are using payroll data more actively to manage labor costs, identify overtime pressure, and understand where staffing patterns are affecting profitability. That shift matters in retail and hospitality because payroll accuracy is no longer enough on its own, and buyers increasingly expect dashboards that explain what is driving labor spend. IRS rule changes on separate W-2 reporting for qualified tips and qualified overtime compensation also reinforce the value of better payroll data structure and reporting depth.[3]Internal Revenue Service, “Guidance for Individual Taxpayers Who Received Qualified Tips or Qualified Overtime Compensation in 2025,” Internal Revenue Service, irs.gov The payroll software in retail and hospitality market is therefore moving from a process-first model toward a decision-support model. Time and attendance management and tax and compliance tools continue to benefit from the same trend because they improve the quality of upstream payroll inputs. Across all functionality layers, buyers still place heavy weight on POS and scheduling integration because weak source data quickly undermines payroll performance in real operating conditions.

Geography Analysis

North America accounted for 35.74% of the payroll software in retail and hospitality market share in 2025, which made it the largest regional contributor. The region benefits from a mature payroll software ecosystem, dense store and property networks, and strong use of scheduling tools for hourly labor. The United States remains the main revenue center because it combines complex wage and overtime rules with a large base of tipped and shift-based employers. IRS Notice 2025-69 added another layer by confirming separate reporting requirements for qualified tips and qualified overtime compensation from the 2026 tax year, which immediately raised the need for payroll system updates. Canada adds steady demand through provincial payroll variation and a stable formal employment base, while Mexico presents a more underpenetrated opportunity where cloud payroll adoption is still building.

Europe stands out less for size than for compliance density, and that gives specialized payroll platforms a clear role. In France, payroll for hotels, cafés, and restaurants must account for night-shift premiums, split-shift allowances, Sunday and holiday pay, and benefit-in-kind meal calculations under the CCN HCR framework, which pushes employers toward purpose-built or heavily configured payroll systems. France also faces DSN filing demands that reward accurate and timely digital submission, reinforcing the operational case for modern payroll software. These conditions support software and service demand across the payroll software in retail and hospitality market, especially where sector agreements shape pay rules directly.

Asia-Pacific is the fastest-growing region, with the payroll software in retail and hospitality market size expected to expand at an 11.06% CAGR through 2031. Growth is supported by formalization in service labor, rising digital adoption in hospitality operations, and stronger interest in mobile-first payroll platforms. India is a key example because locally relevant products are already packaging payroll with PF, ESI, and TDS handling for hospitality employers that need practical compliance tools at accessible price points.[4]SalaryBox, “Best HRMS Software For Hotels, Restaurants And Cafes In India 2025, Top Solutions For Hospitality Workforce Management,” SalaryBox, salarybox.in The broader region also benefits from high frontline turnover, which increases the value of faster onboarding and payroll-linked worker access tools. The payroll software in retail and hospitality market is therefore moving faster in Asia-Pacific than in more mature regions, even though North America still leads in current revenue. Outside these core geographies, adoption remains more uneven, but growing tourism activity and formal employment expansion continue to support medium-term demand.

Competitive Landscape

The payroll software in retail and hospitality market is moderately concentrated at the enterprise tier, where ADP, UKG, and Ceridian-Dayforce hold the strongest positions with integrated HCM suites. Their advantage comes from regulatory coverage, global operating depth, and stronger product breadth across payroll, time, scheduling, and workforce management. These strengths matter most to large retail chains and hotel groups that want fewer systems and a lower risk of compliance gaps. The payroll software in retail and hospitality market still remains far more fragmented below the enterprise band, where smaller businesses compare vendors closely on price, setup speed, and ease of integration. That split between concentration at the top and fragmentation in the SME band defines much of the current competitive shape.

ADP strengthened its position in November 2025 when it launched a unified global workforce management suite across ADP Workforce Now, ADP Lyric HCM, and ADP Global Payroll after integrating WorkForce Software capabilities into a broader platform offer. UKG also moved decisively in December 2025 through its acquisition of Inova Payroll, which expanded its direct-service reach in the SMB and outsourced payroll segment. These moves show that leading vendors are not just improving core payroll, they are widening their control over adjacent workforce processes and service delivery. In the payroll software in retail and hospitality market, that strategy raises switching costs and helps incumbents defend accounts across both enterprise and growing mid-market segments.

Competition is sharper in the SME and vertical-native space, where buyers care deeply about POS links, accounting flows, and frontline usability. Gusto's July 2025 launch of payroll-to-accounting integration flows for Xero and QuickBooks Online, together with a General Ledger API, showed how payroll vendors are moving closer to the day-to-day bookkeeping workflow of smaller restaurant and retail operators.[5]Ravi Dehar, “Closing The Embedded Payroll-To-Accounting Gap,” Gusto Embedded, embedded.gusto.com The payroll software in retail and hospitality market is also being shaped by platforms such as Fourth, Harri, and 7shifts, which start with scheduling, labor visibility, or onboarding and then build payroll capability around those needs. This reverses the older payroll-first sales approach and fits buyers who want one operating layer for the whole frontline workforce. It is also why integration breadth has become a central competitive variable rather than a secondary feature. Vendors that can tie payroll directly to tips, attendance, schedules, and accounting are better placed to win in fragmented buyer groups where operational friction matters as much as brand scale.

Payroll Software In Retail and Hospitality Industry Leaders

ADP LLC

UKG Inc.

Paychex Inc.

Dayforce, Inc.

Paycom Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: EPG Group formally integrated its EPG Payroll and HR services into the Xemplo cloud platform, effective April 1, 2026, consolidating its Asia-Pacific payroll and HR offerings into a single compliance-ready system covering multi-jurisdictional tax codes across 14+ APAC regulatory frameworks.

- February 2026: Valeria, a Barcelona-based hospitality payroll platform, closed a EUR 1.7 million (USD 1.92 million) seed funding round led by VentureFriends, with participation from Fortino Capital and 10K Ventures, to accelerate platform development targeting high-turnover hospitality businesses across Spain and Southern Europe.

- December 2025: UKG acquired Inova Payroll, a Nashville-based HCM and payroll services provider supporting over 4,000 SMBs with frontline-heavy workforces, including significant retail and hospitality accounts. The acquisition extended UKG's direct-service capability into the outsourced HR and benefits-brokerage segment of the SMB market.

- December 2025: The US Consumer Financial Protection Bureau issued an advisory opinion formally supporting employer-integrated earned wage access programs, providing regulatory clarity that removed a significant adoption barrier for hospitality payroll vendors integrating on-demand pay features.

Global Payroll Software In Retail and Hospitality Market Report Scope

The payroll software in retail and hospitality market refers to software platforms and associated services specifically designed to manage employee compensation, wage calculations, tax deductions, compliance reporting, scheduling-linked payroll processing, and workforce payment operations for businesses operating in the retail and hospitality sectors. The market includes cloud-based and on-premises payroll applications that support high-volume, shift-based, seasonal, hourly, and geographically distributed workforce environments commonly found across retail stores, restaurants, hotels, resorts, cafes, entertainment venues, and food-service chains.

The Payroll Software in Retail and Hospitality Market is Segmented by Component (Software, and Services), Organization Size (Large Enterprises, and SMEs), Deployment Mode (Cloud, and On-Premises), Functionality (Core Payroll Processing, Time and Attendance Management, Payroll Analytics and Reporting, Tax and Compliance Management, and Other Functionalities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Large Enterprises |

| SMEs |

| Cloud |

| On-Premises |

| Core Payroll Processing |

| Time and Attendance Management |

| Payroll Analytics and Reporting |

| Tax and Compliance Management |

| Other Functionalities |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Functionality | Core Payroll Processing | |

| Time and Attendance Management | ||

| Payroll Analytics and Reporting | ||

| Tax and Compliance Management | ||

| Other Functionalities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is payroll software in retail and hospitality expected to become by 2031?

The payroll software in retail and hospitality market is projected to reach USD 4.06 billion by 2031, up from USD 2.34 billion in 2025, at a 9.94% CAGR from 2026 to 2031.

Which deployment model leads spending in this space?

Cloud leads the category, with 71.34% share in 2025, and it is also the fastest-growing deployment mode with a 10.44% CAGR through 2031.

Why are SMEs becoming more important buyers of payroll platforms?

SMEs are the fastest-growing customer group at a 10.12% CAGR because lower-cost cloud suites, mobile access, and built-in compliance support are making modern payroll systems more accessible.

Which region is growing the fastest for payroll software used by retailers and hospitality operators?

Asia-Pacific is the fastest-growing region with an 11.1% CAGR through 2031, supported by labor formalization, digital adoption, and mobile-first payroll tools.

What makes competition intense in this category?

Enterprise vendors are strong at the top end, but the broader field is fragmented, especially in SME accounts where integration with POS, scheduling, accounting, and tip workflows strongly shapes vendor choice.

Page last updated on: