Payroll Software In BFSI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 5.09 Billion |

| Growth Rate (2026 - 2031) | 10.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

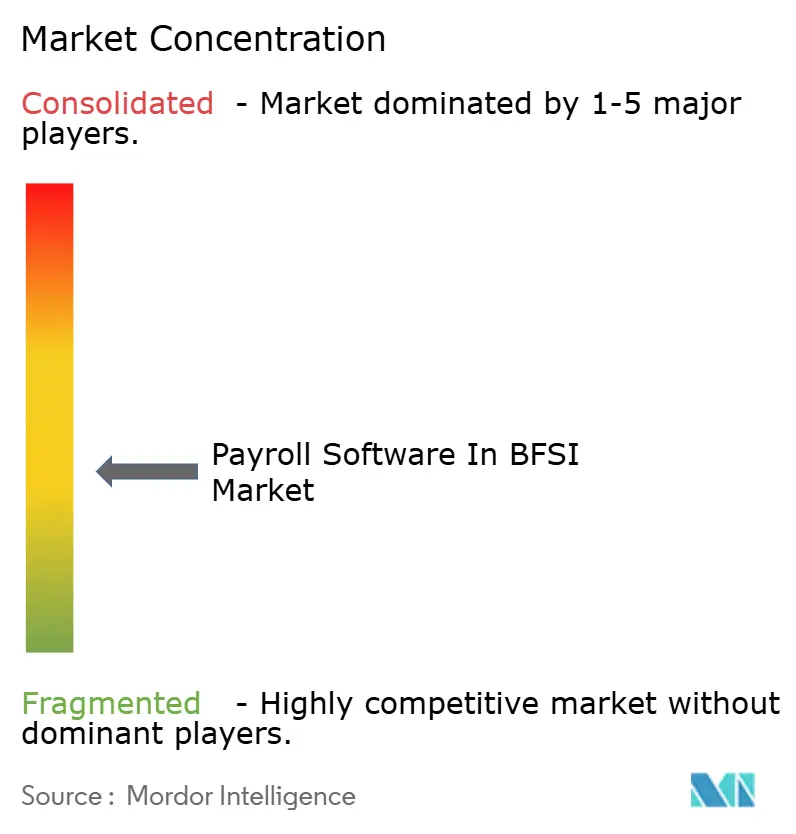

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payroll Software In BFSI Market Analysis by Mordor Intelligence

The Payroll software in BFSI market size is projected to expand from USD 2.88 billion in 2025 and USD 3.12 billion in 2026 to USD 5.09 billion by 2031, registering a CAGR of 10.28% between 2026 to 2031. Demand is rising because banks, insurers, and investment firms now treat payroll systems as part of wider operating control, not as a back-office utility. Regulatory change is pushing institutions to move away from monthly batch processing and toward systems that can support faster reporting, cleaner audit trails, and closer links with payment infrastructure. Cloud maturity is also changing buying behavior because institutions want payroll platforms that can connect with core banking systems, HR systems, and finance tools through standard interfaces. Vendor competition is increasingly shaped by compliance breadth, embedded payroll capabilities, and AI-enabled error detection, which gives an advantage to providers that can support multi-country operations at scale. The Payroll software in the BFSI market also has room to expand among smaller financial institutions as subscription pricing lowers the entry barrier for enterprise-grade payroll platforms.

Key Report Takeaways

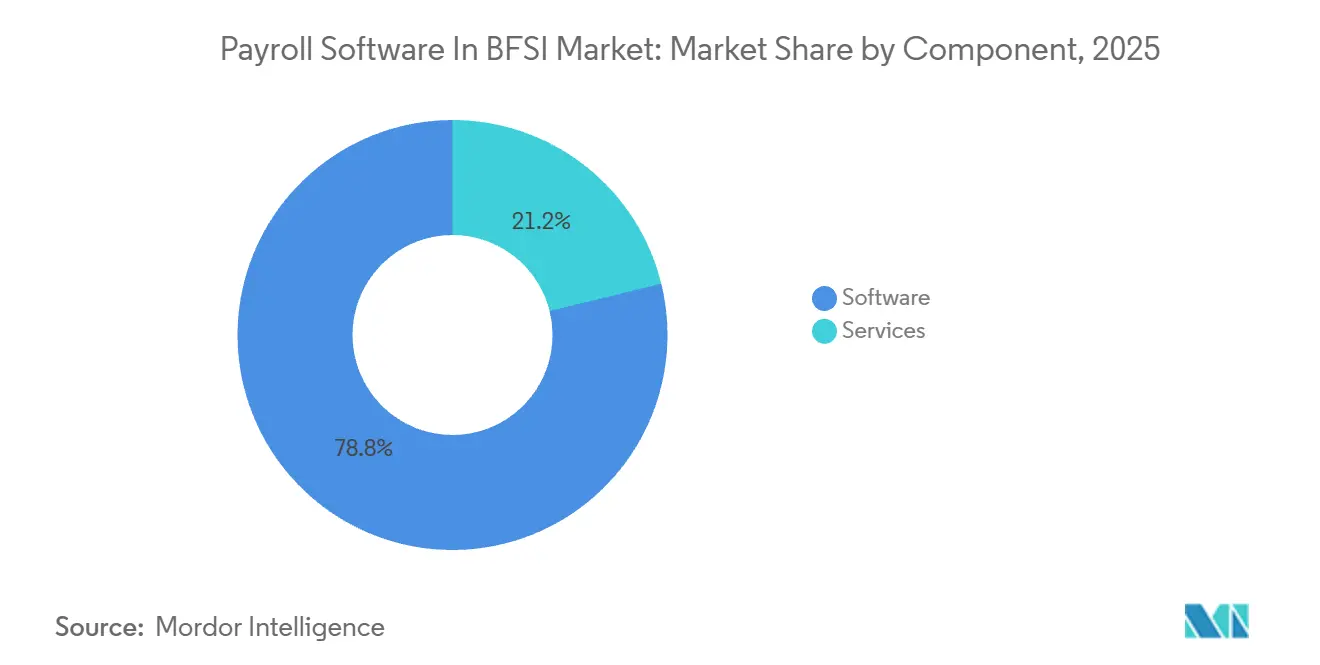

- By component, software led with 78.84% revenue share in 2025 of the payroll software in BFSI market, while services is forecast to expand at 11.04% CAGR through 2031.

- By organization size, large enterprises held 69.22% share in 2025, while SMEs recorded the highest projected CAGR at 10.58% through 2031.

- By deployment mode, cloud accounted for 72.91% share in 2025 and is also advancing at 10.92% CAGR through 2031.

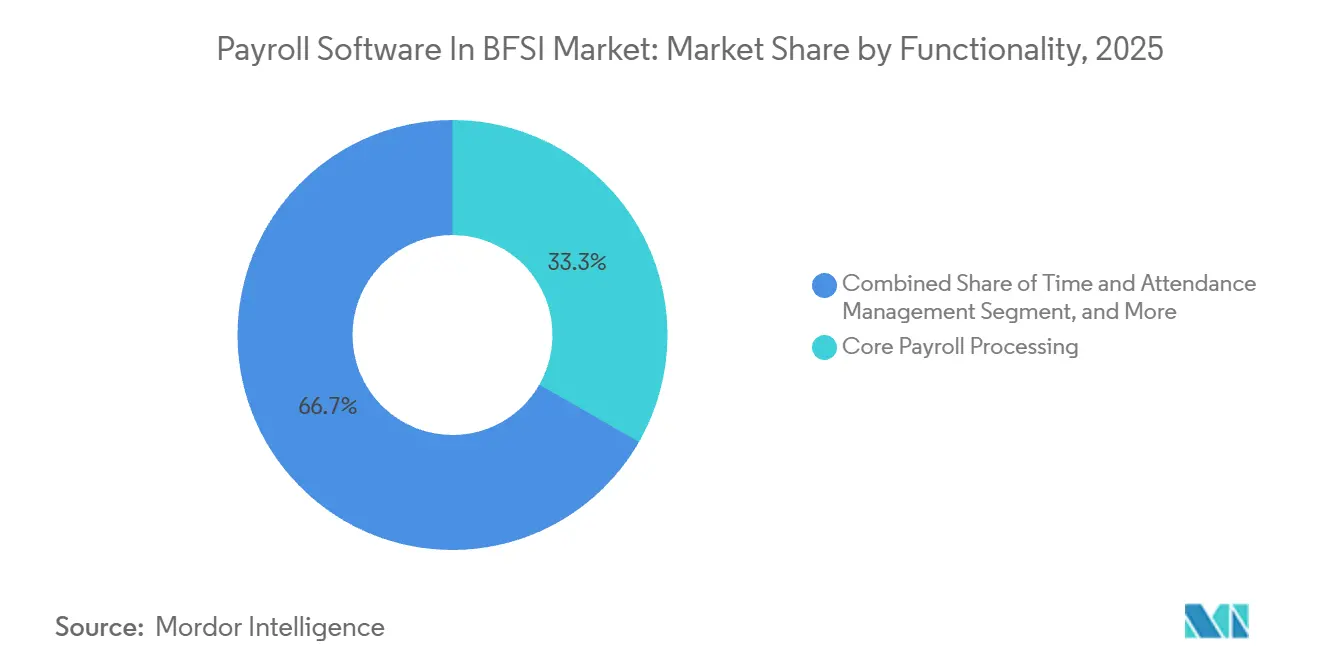

- By functionality, core payroll processing accounted for 33.28% share in 2025, while payroll analytics and reporting is advancing at 12.16% CAGR through 2031.

- By financial institution type, banking companies held 46.74% share in 2025, while investment firms and brokerages are projected to grow at 11.88% CAGR through 2031.

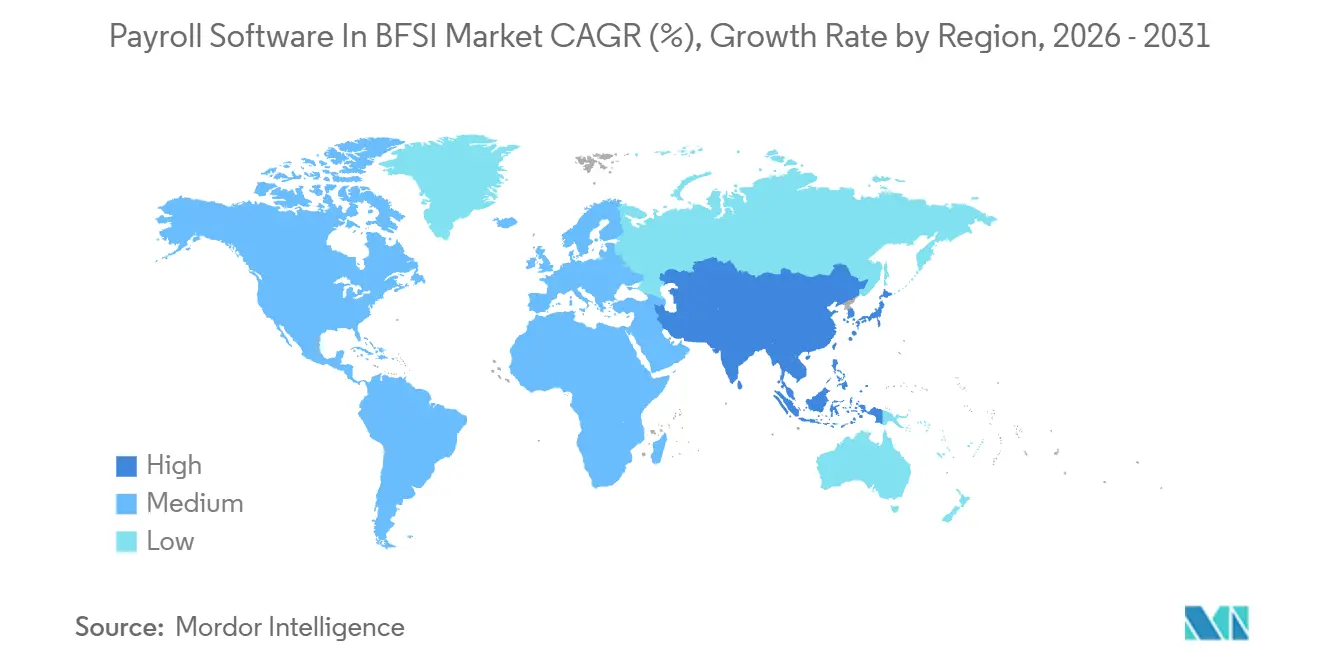

- By geography, North America led with 37.96% share in 2025 of the payroll software in BFSI market, while Asia-Pacific is forecast to expand at 11.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Payroll Software In BFSI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Digital Transformation in Banking | +2.6% | Global | Medium term (2-4 years) |

| AI-Driven Compliance Monitoring | +1.9% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Real-Time Payroll Reporting Demand | +1.7% | Global, with concentration in North America, EU, and India | Short term (≤ 2 years) |

| Cloud-Native Core Banking Adoption | +1.4% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Embedded Payroll in BaaS Offerings | +0.9% | North America and Europe | Medium term (2-4 years) |

| Neo-Bank Expansion for Gig and Freelance Workers | +0.6% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital Transformation Initiatives In Banking

Banks have moved from isolated HR upgrades to broader operating model redesign, and payroll now sits inside that core technology refresh cycle. Zalaris showed that Danske Bank consolidated 4 Nordic payroll vendors into 1 cloud platform covering 20,000 employees under a no-customization approach. That example matters in the Payroll software in BFSI market because fragmented payroll stacks raise system complexity and weaken consistency across employee and compensation records. When banks rebuild around modern APIs, payroll becomes part of the shared data layer that supports finance, workforce, and payment workflows. ADP reinforced this direction in November 2025 when it launched a unified global workforce management suite across its HCM platforms for 140 countries. The payroll software in BFSI market is therefore benefiting from modernization programs that begin with digital transformation but end with demand for standardized payroll infrastructure.

AI-Driven Compliance Monitoring Reducing Manual Audit Costs

The Payroll software in BFSI market is moving from post-run error checks toward predictive monitoring that can flag problems before payment files are released. UKG launched UKG Pro Pay with Workforce AI in May 2026, and the product compares payroll runs against up to 5 years of historical payroll data. ADP expanded in the same direction in January 2026 with AI agents that can identify payroll variances, missing tax IDs, and other compliance gaps across payroll and HR workflows.[1]ADP, Inc., “ADP Accelerates AI Leadership with Launch of New AI Agents Designed to Solve Workforce Challenges,” ADP Media Center, mediacenter.adp.com For banks and insurers, that shift is important because payroll records increasingly serve as control evidence for internal reviews and regulatory examinations. Thomson Reuters noted in April 2026 that AI in payroll still requires auditable workflows and clear human review before final action. That requirement is steering the Payroll software in BFSI market toward platforms with immutable logs, role-based controls, and governance features that compliance teams can defend.

Heightened Regulatory Demand For Real-Time Payroll Reporting

Compliance deadlines are shortening replacement cycles across the Payroll software in BFSI market because payroll systems now need to support faster reporting and event-based processing. HM Revenue and Customs requires Real Time Information submissions on or before each payday, which weakens the fit of legacy, monthly batch-only payroll models. In the United States, real-time payment infrastructure and ACH labeling changes are pushing institutions to update the payment side of payroll operations. Ogletree Deakins also explained that earned wage access arrangements may require FICA withholding at each disbursement event rather than at a later pay-cycle stage. California added new 2026 pay-data reporting requirements and penalties, which increased pressure on employers to reconcile HR, payroll, and classification data more accurately. The Payroll software in BFSI market is therefore seeing demand from institutions that can no longer treat payroll upgrades as a low-priority technology decision.

Growing Adoption Of Cloud-Native Core Banking Platforms

Cloud migration in banking is pulling payroll replacement activity higher because modern payroll platforms fit more naturally into API-first operating environments. Workday reported USD 2.2 billion in Q1 FY2026 revenue, up 12.6% year over year, and identified Mutual of Omaha Insurance Company as a new BFSI customer.[2]Workday, Inc., “Investor Presentation Q1 FY26,” Workday, workday.com That signals that insurers are adopting cloud HCM and payroll platforms as part of wider enterprise software modernization rather than as stand-alone replacements. Germany also shows how compliance and cloud adoption now meet in the same buyer decision, because payroll complexity and data protection standards sharply narrow the qualified vendor pool. In markets like this, financial institutions want cloud vendors that can show regulatory fitness, secure hosting, and stable update cycles without heavy local customization. The Payroll software in BFSI market is benefiting because cloud-native core banking programs often make payroll modernization a parallel investment rather than a separate budget request.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Core Systems with Limited API Interoperability | -2.3% | Global, especially North America and Europe | Medium term (2-4 years) |

| Cyber-Security and Data Sovereignty Concerns | -1.7% | EU, Asia-Pacific, and North America | Long term (≥ 4 years) |

| High Switching Costs from On-Premise Payroll Engines | -1.3% | Global | Medium term (2-4 years) |

| Shortage of Domain-Specific Payroll Talent in Emerging Markets | -0.8% | Asia-Pacific core, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Core Systems With Limited API Interoperability

Legacy banking cores remain a direct brake on the Payroll software in BFSI market because many institutions still run payroll through older file-based processes. CloudPay reported in late 2025 that 62% of global businesses lacked the resources or expertise to adopt APIs across end-to-end payroll processes. The same research said 38% of enterprise respondents cited budget constraints, which becomes more restrictive in regulated BFSI settings. TechHQ also noted that many multinational organizations still rely on file transfers rather than API-first payroll integration patterns. That slows implementation, extends testing cycles, and keeps payroll teams exposed to manual workarounds even after modernization programs begin. The Payroll software in BFSI market, therefore, faces a timing gap between strategic intent and operational readiness, especially in institutions with long change-control cycles.

Cyber-Security And Data Sovereignty Concerns

Security and data-location requirements continue to slow consolidation in the Payroll software in BFSI market because payroll records combine employee identity data and payment data in one flow. ADP found that 70% of organizations experienced a payroll-related cybersecurity incident during the previous 2 years. That history is forcing banks and insurers to review payroll vendors through a security lens that goes far beyond basic functionality. Procurement guidance in 2026 also showed stronger demand for sovereignty clauses that govern where payroll data, backups, and privileged access can reside. In Europe and parts of the Asia-Pacific, those requirements make cross-border standardization harder because one technical design may not satisfy every local rule. The Payroll software in BFSI market keeps growing, but vendor qualification takes longer when institutions must prove data residency, incident response, and access governance in detail.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Tempered By Accelerating Services Demand

Software held 78.84% of market revenue in 2025, giving it the largest share of the payroll software in BFSI market. BFSI institutions have historically favored software platforms because they want stronger control over configuration, security rules, and integrations with finance and HR systems. That preference is especially strong in large institutions that operate across multiple jurisdictions and need support for complex deduction logic, audit trails, and multi-currency payroll processing. Workday reported a subscription backlog of USD 24.6 billion in Q1 FY2026, which supports the view that enterprise payroll and HCM contracts remain highly sticky once deployed.

The services segment is projected to grow faster at an 11.04% CAGR through 2031, even though it starts from a smaller base. Demand is rising because many financial institutions struggle to recruit and retain specialists who can manage payroll operations in compliance-heavy jurisdictions. Haufe noted that more than half of German tax consultants handling payroll accounts were over 50, which points to a narrowing labor pipeline in payroll administration. That pressure is encouraging mid-tier banks and insurers to outsource payroll administration while still keeping policy control and reporting oversight internally. The Payroll software in BFSI market is therefore likely to keep software as the core revenue base, while services gains share as institutions respond to talent scarcity and operating continuity risk.

By Organization Size: Large Enterprises Lead, But SMEs Define The Next Growth Frontier

Large enterprises accounted for 69.22% of the market in 2025, reflecting the scale of payroll spending required across large banking groups, insurers, and investment firms. These institutions usually manage thousands of employees across different legal entities, currencies, benefit structures, and reporting rules. They also tend to buy broad enterprise suites that connect payroll with talent, finance, and workforce analytics rather than relying on narrow point tools. In that environment, larger contracts continue to set the revenue base for the Payroll software in BFSI market.

SMEs are the fastest-growing organization size at a 10.58% CAGR through 2031, which shows that the next expansion wave is shifting lower in the institution-size spectrum. Pricing at USD 25 to USD 35 per employee per month has lowered the capital barrier that once kept regional banks and smaller insurers on manual or spreadsheet-led processes. Community credit unions, boutique investment houses, and smaller insurance carriers can now adopt cloud payroll services without the heavy upfront implementation burden of legacy enterprise systems. Compliance expectations are also rising for smaller institutions, especially where audit-grade payroll records are required during reviews or examinations. The Payroll software in BFSI market is widening because lower entry pricing and stronger compliance pressure are now moving smaller financial institutions into the addressable base.

By Deployment Mode: Cloud Consolidation Driven By Banking API Ecosystems

Cloud deployment accounted for 72.91% share of the payroll software in BFSI market size in 2025 and is also the fastest-growing deployment mode at a 10.92% CAGR through 2031. Its lead reflects a structural advantage because cloud payroll platforms connect more easily with cloud core banking systems, real-time payment rails, and modern compliance tools. That matters for banks and insurers that want payroll data to move cleanly across workforce, finance, and payment systems without heavy batch reconciliation. Workday expanded Workday GO in November 2025 with integrated global payroll and an AI deployment agent that can reduce implementation time by up to 25%.[3]Workday, Inc., “Workday Expands Workday GO, the All-in-One ‘Workday for All’ Solution, to Support Businesses of All Sizes,” Workday Investor Relations, investor.workday.com

On-premises deployment still plays a role in institutions that want direct control over infrastructure or must comply with local data-location rules. This is especially relevant in jurisdictions where regulatory interpretation or internal policy favors institution-managed environments for sensitive payroll records. Vendors serving these accounts still need strong security credentials, including ISO/IEC 27001 certification and region-compliant hosting capabilities. Ramco Systems also noted that cloud payroll had already moved into a leading position in the broader payroll services space in 2024 and was growing at a double-digit rate. The Payroll software in BFSI market is therefore consolidating around cloud models, while on-premises remains relevant where compliance or control concerns override speed and flexibility.

By Functionality: Analytics Redefines Payroll As A Strategic Data Asset

Core payroll processing held 33.28% of the market in 2025, making it the largest functionality segment. Every BFSI institution depends on this layer because it controls gross-to-net calculations, statutory deductions, payment files, and filing outputs. Time and attendance management also remains important in branch networks and service operations where staffing patterns affect labor cost and compliance tracking. Tax and compliance management has become more central because updates such as the 2026 U.S. Social Security wage base change and the UK's employer contribution threshold change require payroll systems to adjust quickly.

The payroll analytics and reporting segment is the fastest-growing functionality, with a 12.16% CAGR through 2031, indicating that payroll is increasingly treated as an operating intelligence function. Finance leaders want faster visibility into labor cost movement, exception trends, and payroll timing across legal entities. That demand is shifting payroll from a purely transactional process toward a recurring data layer that supports planning, control, and governance. European reporting obligations are adding urgency, as banks and insurers need more granular pay and role-level data than many legacy systems can provide. The Payroll software in BFSI market is responding by placing greater value on dashboards, exception analytics, and audit-ready reporting rather than on processing speed alone.

By Financial Institution Type: Banking Companies Anchor Volume, Investment Firms Drive Growth

Banking companies held 46.74% of the payroll software in BFSI market share in 2025 because they combine large employee bases with broad regulatory and operating complexity. They also moved earlier than many other financial institutions on cloud-core and embedded workflow strategies, which made payroll modernization easier to justify as part of wider platform spending. In China, ICBC's Salary Butler platform served 369 enterprises in its Jiaxing branch by the end of 2024.[4]Sina Finance, “Digital Empowerment and Specialized Salary Services,” Sina Finance, finance.sina.com.cn China Merchants Bank also reported that XinFuTong payroll agency volume grew 22% in 2024 as it strengthened the link between HR workflows and corporate banking deposit flows.

Investment firms and brokerages are the fastest-growing financial institution type at an 11.88% CAGR through 2031. Their compensation structures are more difficult to administer because they often combine salary, bonuses, deferred compensation, restricted stock vesting, and performance-linked payouts. That raises the value of payroll engines that can support detailed tax treatment, stronger reporting logic, and clearer audit traceability. Insurance companies and credit unions remain steady adopters, but their smaller workforces and more measured technology budgets keep growth below that of the brokerage segment. The Payroll software in BFSI market therefore continues to rely on banks for present-day volume while investment firms create a faster growth path through higher compensation complexity.

Geography Analysis

North America accounted for 37.96% share of the payroll software in BFSI market size in 2025, making it the largest regional contributor. The region leads because it combines mature cloud infrastructure, complex payroll regulation, and high technology spending by financial institutions. The United States remains the main product and compliance frontier, and ADP's November 2025 workforce management launch for 140 countries reflects the scale of enterprise payroll demand anchored in the region. The March 2026 ACH descriptor mandate also illustrates how payment-network rules can trigger payroll system upgrades across banks and related financial institutions. Canada adds demand through province-level variation in payroll taxes, labor rules, and benefits administration, while Mexico expands the regional opportunity through a broader fintech and banking customer base.

Europe remained one of the more developed regions for enterprise payroll demand in 2025, with the UK, Germany, and France standing out as the most sophisticated buyer markets. Germany is especially important because payroll complexity is high, which increases the value of compliance-grade software for financial institutions. The June 2026 pay-transparency reporting timetable is raising demand for analytics and reporting functions among banks and insurers that operate across multiple EU markets. HiBob's payroll workflow integration with Modulr also shows how European platforms are reducing friction between payroll calculation, payment execution, and tax submission.

Asia-Pacific is the fastest-growing geography at an 11.42% CAGR through 2031, which makes it the main expansion engine for the Payroll software in BFSI market. China is shaping an unusual regional model because major banks are building embedded payroll platforms to retain deposits and deepen client relationships rather than treating payroll as a separate software sale. Shanghai Pudong Development Bank's upgraded one-stop HR and payroll service platform shows the same direction, where payroll becomes part of a wider enterprise banking proposition. India's labor code reforms are expected to widen demand for digital payroll compliance platforms by 2027. Japan also supports growth through platforms such as Bakuraku Payroll, which reported a service continuation rate above 99% and highlighted ISO/IEC 27001 certification as a core operating feature. Middle East demand is concentrated in Saudi Arabia and the United Arab Emirates because financial institution expansion and WPS compliance keep payroll investment active. Africa remains earlier in development, but mobile-first neobanks and embedded payroll models are gradually broadening the long-term opportunity for the Payroll software in BFSI market.

Competitive Landscape

The Payroll software in BFSI market shows moderate fragmentation at the global level, but competition is tighter inside large enterprise financial accounts, where a small group of vendors appears repeatedly in major deals. ADP, Workday, SAP, and UKG remain the most visible platforms in these higher-value institutional tiers because they can combine payroll with broader HCM and compliance workflows. Their strategy is increasingly centered on platform depth rather than on payroll calculation alone. ADP's January 2026 rollout of AI agents across payroll, HR, and tax workflows shows how incumbents are using automation to defend enterprise accounts with stronger control features. Paychex followed in February 2026 with agentic workforce management capabilities across Paycor and Paychex Flex, including AI-powered scheduling and timesheet automation.

Workday also expanded Workday GO in November 2025 with integrated global payroll support, which shows that incumbents are pushing faster into mid-size accounts as well as large ones. At the same time, the Payroll software in BFSI market is being reshaped by embedded payroll, where banks and banking platforms package payroll directly into their client-facing products. U.S. Bank launched an embedded payroll solution for small businesses in September 2025 using Gusto infrastructure inside its online banking dashboard. Axos Bank then partnered with Rollfi in February 2026 to embed payroll and benefits into its commercial banking platform after a competitive RFP process.[5]“Axos Bank Partners with Rollfi to Embed Payroll and Benefits in Its Digital Banking Platform,” HRTech Edge, hrtechedge.com

These moves matter because they shift part of the buying decision away from HR software procurement and toward business banking relationships. Cloud-native challengers such as Deel, Rippling, and Papaya Global are also creating pressure by emphasizing faster implementation and more flexible international payroll deployment models. Deel's October 2025 funding round and its plan to build native payroll infrastructure in more than 100 countries by 2029 show how aggressively newer vendors are expanding global payroll coverage. The clearest white-space opportunity remains compliance-intensive payroll for investment firms and brokerages, where compensation structures are harder than in standard banking payroll environments. The Payroll software in BFSI market is likely to reward vendors that can combine real-time auditability, embedded payment connectivity, and strong multi-jurisdiction compliance support in one platform.

Payroll Software In BFSI Industry Leaders

Automatic Data Processing, Inc.

Paychex, Inc.

Paycom Software, Inc.

Ultimate Kronos Group (UKG Inc.)

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UKG launched UKG Pro Pay with Workforce AI, an AI-driven payroll product that compares each payroll run against up to 5 years of historical data to proactively flag anomalies before disbursement, directly targeting the estimated 2% to 4% of total labor spend lost annually to payroll leakage in large institutions.

- May 2026: BambooHR and Clair launched "BambooHR On-Demand Pay," a fully embedded earned wage access feature within BambooHR Payroll.

- April 2026: OnePay, Walmart's digital banking platform, partnered with Workday Wellness to embed enhanced direct deposit switching into Workday Payroll, giving U.S.-based employees at over 11,500 Workday customer organizations the ability to set up payroll deposits to OnePay accounts within their employer's HR platform.

- March 2026: Digits launched expanded payroll connectivity with 18 additional payroll providers, including ADP Run, Paychex Flex, Paylocity, and UKG Pro, enabling AI-driven automatic categorization and booking of payroll accounting entries into its Agentic General Ledger, backed by nearly USD 100 million from Benchmark, SoftBank, and GV.

Global Payroll Software In BFSI Market Report Scope

The payroll software in BFSI market refers to payroll management platforms and associated services specifically deployed by banking, financial services, and insurance (BFSI) organizations to automate employee compensation management, tax compliance, benefits administration, attendance-linked payroll, audit-ready reporting, and workforce payment operations across regulated financial institutions. The market includes cloud-based and on-premises payroll software platforms tailored for highly regulated financial environments requiring secure, compliant, scalable, and real-time payroll processing capabilities.

The Payroll Software in BFSI Market Report is Segmented by Component (Software, and Services), Organization Size (Large Enterprises, and SMEs), Deployment (Cloud, and On-Premises), Functionality (Core Payroll Processing, Time and Attendance Management, Payroll Analytics and Reporting, Tax and Compliance Management, and Other Functionalities), Institution Type (Banking Companies, Insurance Companies, Investment and Brokerage Firms, Credit Unions, andOther Financial Institutions Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Large Enterprises |

| SMEs |

| Cloud |

| On-Premises |

| Core Payroll Processing |

| Time and Attendance Management |

| Payroll Analytics and Reporting |

| Tax and Compliance Management |

| Other Functionalities |

| Banking Companies |

| Insurance Companies |

| Investment and Brokerage Firms |

| Credit Unions |

| Other Financial Institutions Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Functionality | Core Payroll Processing | |

| Time and Attendance Management | ||

| Payroll Analytics and Reporting | ||

| Tax and Compliance Management | ||

| Other Functionalities | ||

| By Financial Institution Type | Banking Companies | |

| Insurance Companies | ||

| Investment and Brokerage Firms | ||

| Credit Unions | ||

| Other Financial Institutions Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the expected value of payroll software in BFSI by 2031?

The market is expected to reach USD 5.09 billion by 2031, rising from USD 3.12 billion in 2026 at a 10.28% CAGR.

Which region currently leads payroll software demand in banking and insurance?

North America led in 2025 with a 38.04% share, supported by mature cloud adoption, complex compliance needs, and active payment infrastructure changes.

Which deployment model is gaining the most traction among financial institutions?

Cloud leads with a 72.91% share in 2025 and is also the fastest-growing deployment mode, expanding at a 10.92% CAGR through 2031.

Why are investment firms and brokerages adopting newer payroll platforms faster?

They are projected to grow at an 11.88% CAGR because variable compensation, deferred pay, and securities-related reporting create more payroll complexity.

What is the largest functionality segment in payroll platforms for BFSI users?

Core payroll processing remained the largest functionality segment in 2025 with a 33.28% share because every institution depends on accurate gross-to-net calculations and statutory deductions.

Page last updated on: