Payroll And HR Compliance Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

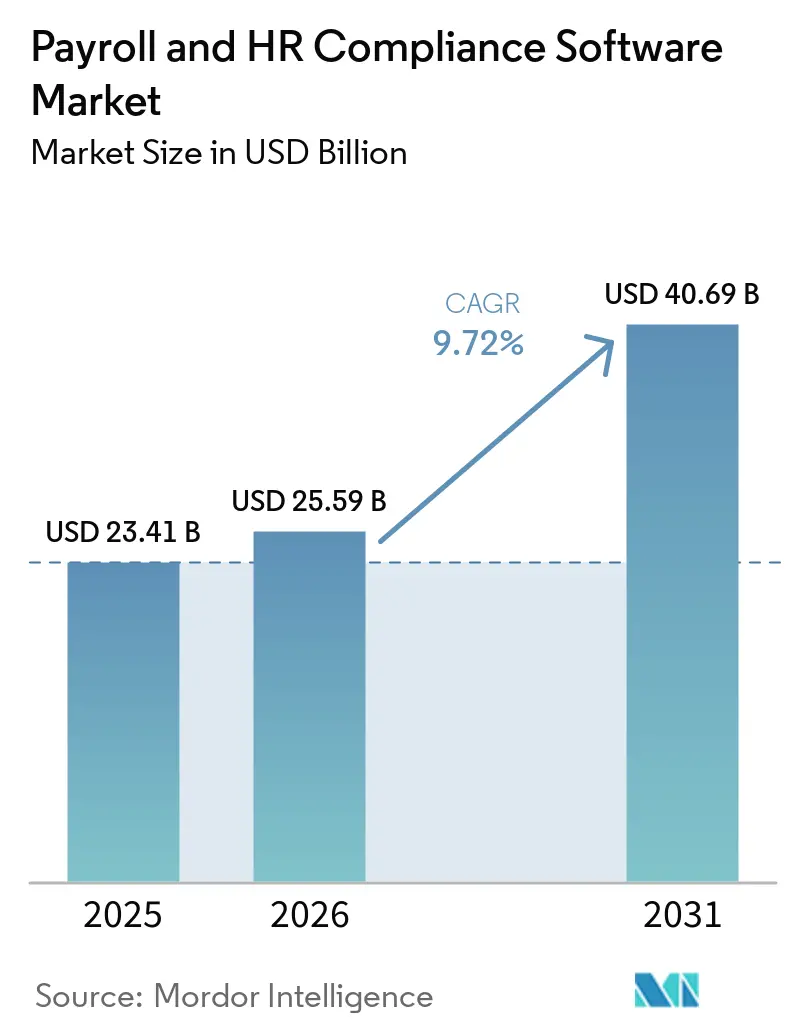

| Market Size (2026) | USD 25.59 Billion |

| Market Size (2031) | USD 40.69 Billion |

| Growth Rate (2026 - 2031) | 9.72% CAGR |

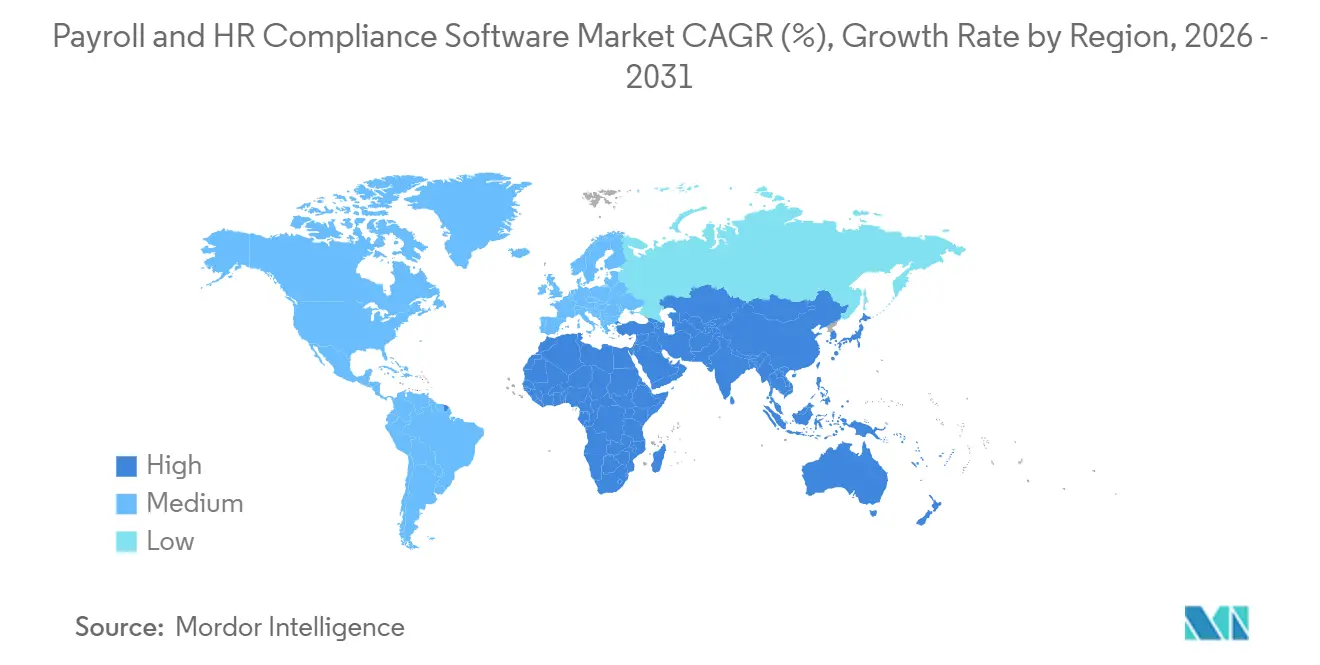

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payroll And HR Compliance Software Market Analysis by Mordor Intelligence

The payroll and HR compliance software market size is projected to expand from USD 23.4 billion in 2025 and USD 25.6 billion in 2026 to USD 40.7 billion by 2031, registering a CAGR of 9.72% between 2026 and 2031. The payroll and HR compliance software market is growing as employers face steady pressure to automate payroll across multiple jurisdictions, keep pace with labor rules, and reduce manual errors in core workforce processes. Cloud deployment has become the operating default because it supports continuous rule updates, faster implementation, and simpler scaling across business entities and countries. A more international workforce footprint is also shaping the payroll and HR compliance software market more than a few years ago, underscoring the value of unified, rules-based platforms over disconnected local tools. Competition remains active at both ends of the market, with large incumbents extending AI, API, and ecosystem capabilities, and cloud-native challengers gaining traction with faster deployment and lighter operating models. The same regulatory complexity that supports demand also limits product standardization, which means vendors that balance automation, localization, and data governance are better placed to capture long-term opportunities.

Key Report Takeaways

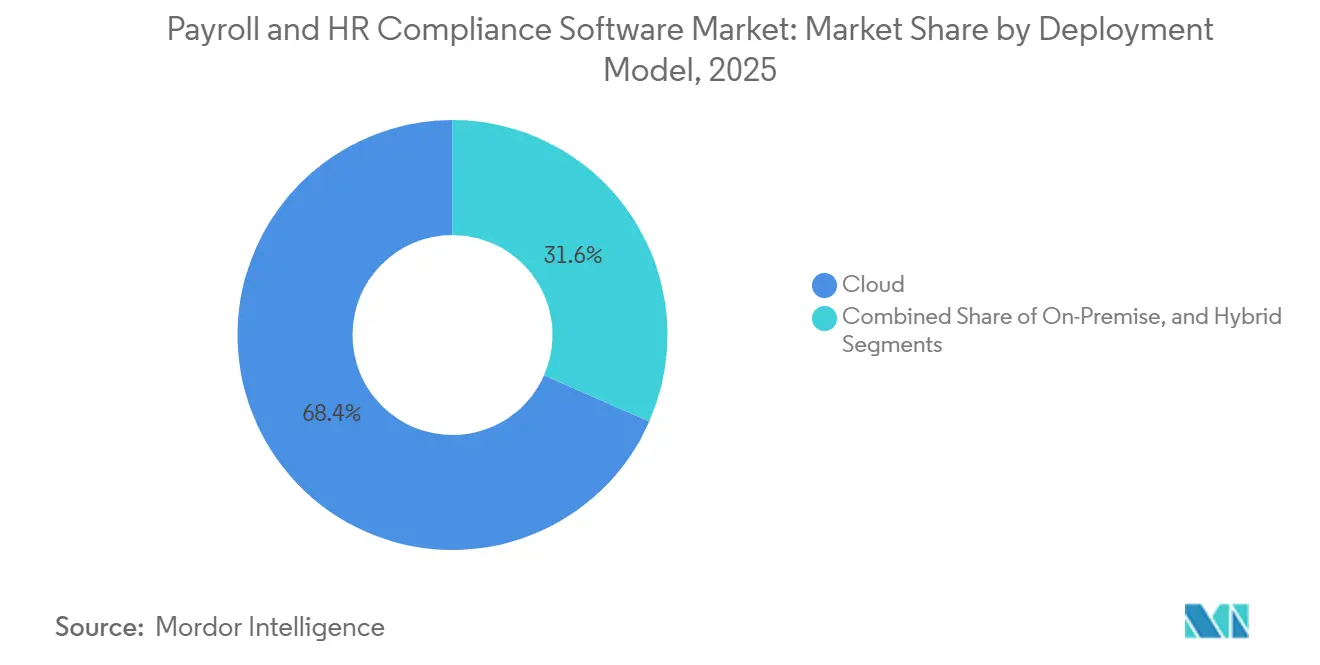

- By deployment model, cloud led with a 68.4% revenue share of payroll and HR compliance software market in 2025, and it also recorded the fastest projected CAGR at 10.8% through 2031.

- By end-user enterprise size, large enterprises accounted for 61.7% of revenue in 2025, while SMEs are forecast to expand at a 10.4% CAGR through 2031.

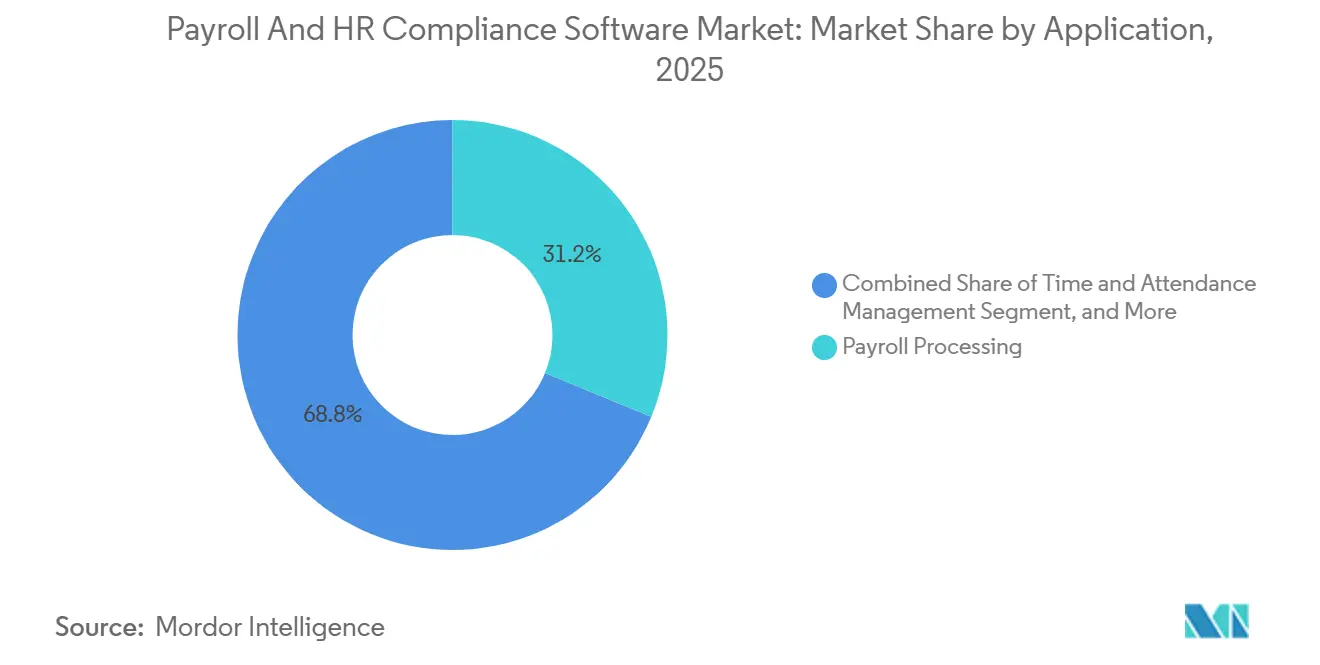

- By application, payroll processing accounted for a 31.2% share in 2025, while HR compliance and regulatory management is advancing at an 11.6% CAGR through 2031.

- By end-user industry vertical, BFSI commanded a 19.8% share of payroll and HR compliance software market in 2025, while healthcare and life sciences are forecast to grow at a 11.9% CAGR through 2031.

- By geography, North America held 38.6% share in 2025, while Asia-Pacific is projected to expand at a 12.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Payroll And HR Compliance Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud Adoption by SMEs Accelerating SaaS Payroll Uptake | +2.8% | Global, with concentrated gains in North America, Western Europe, and Southeast Asia | Short term (≤ 2 years) |

| Stringent Multi-Country Tax and Labor Compliance Mandates | +2.2% | Global, with peak exposure in Europe, North America, and APAC emerging markets | Medium term (2-4 years) |

| AI-Driven Payroll Error Detection and Fraud Prevention | +1.5% | Global, with early adoption concentrated in North America and Europe | Medium term (2-4 years) |

| Integration of Payroll APIs into Fintech Ecosystems | +1.0% | North America and Europe core, with growing spillover to APAC and the Middle East | Medium term (2-4 years) |

| Shift Toward On-Demand Pay and Earned Wage Access | +0.7% | North America primary, with Europe and APAC emerging | Short term (≤ 2 years) |

| Growing Freelancer and Gig Workforce Requiring Agile Payroll | +0.5% | Global, pronounced in North America, India, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud Adoption by SMEs Accelerating SaaS Payroll Uptake

The payroll and HR compliance software market is seeing one of its clearest demand shifts in the SME segment, where buyers are moving from manual processes and narrow payroll tools to cloud systems that combine payroll, records, and compliance tasks in a single environment. This change matters because smaller firms usually need lower setup effort, faster product updates, and fewer vendor handoffs than large enterprise buyers. In France, 86% of companies used payroll software in 2025, and 62% of employees received digital payslips, indicating how commonplace digital payroll administration has become in a mature SME setting.[1]Emma Hunter, “Managing Multi-country Payroll Compliance in 2025,” CloudPay, cloudpay.com As more SMEs adopt broader HR platforms, standalone accounting-linked payroll modules become less relevant, as buyers prefer a single workflow for pay, employee records, and compliance actions. The payroll and HR compliance software market, therefore, benefits from a structural shift in buying behavior, not just from short-term software replacement cycles.

Stringent Multi-Country Tax and Labor Compliance Mandates

The payroll and HR compliance software market continues to gain support from compliance mandates that now span pay transparency, payroll documentation, cyber controls, and country-specific labor administration rules. The commercial case becomes stronger when employers manage payroll across several jurisdictions, because rule changes, reporting demands, and local filing practices no longer sit neatly inside one payroll team or one local system. CloudPay reported in late 2025 that more than 36% of organizations now manage payroll across 6 or more countries, underscoring the need for centralized rules and local compliance enforcement within a single platform.[2]Jeremy Zhang, “The Rise of the Open Employment Ecosystem,” Finch, tryfinch.com This multi-country burden does not act as a one-time trigger, because new country rules and compliance updates continue to arrive after the initial implementation. The payroll and HR compliance software market is therefore being pulled forward by recurring compliance work that employers increasingly want software to manage inside the payroll process itself.

AI-Driven Payroll Error Detection and Fraud Prevention

The payroll and HR compliance software market is moving toward AI as a routine control layer, especially where employers want faster detection of payroll anomalies and more consistent audit trails. This matters because payroll teams need to identify exceptions before disbursement, not weeks later during a review cycle. In September 2025, early users of a payroll anomaly-flagging tool reported saving up to 30 minutes per payroll cycle, demonstrating how AI is being applied to day-to-day payroll control work rather than solely for experimentation. In February 2026, new AI-driven workforce management features were introduced, including agentic timesheet approvals and time-off tools that apply pattern recognition inside workforce administration. As AI shifts from feature add-on to core workflow logic, the payroll and HR compliance software market is likely to reward vendors that can explain outputs, log decisions, and support audit review without adding more manual work.

Integration of Payroll APIs Into Fintech Ecosystems

The payroll and HR compliance software market is increasingly tied to API connectivity, because payroll data now supports benefits, financial wellness, workforce finance, and other linked services beyond the core pay run. The U.S. payroll landscape included more than 5,700 providers, and the top 35 systems accounted for 70% of employer penetration in 2025, making interoperability a practical requirement for ecosystem scale.[3]Alexandre Martin, “Comparatif Des Meilleurs Logiciels De Paie 2025,” Eurécia, eurecia.com It was also noted that 94% of employers wanted integrations across the systems they use to manage employees, and 97% of HR professionals saw system connectivity as important in the employment technology stack. The earned wage access use case shows how this connectivity is turning payroll into infrastructure for adjacent services, with employer-integrated EWA rising from USD 3.2 billion in 2018 to USD 22.8 billion across 214 million transactions by 2022. The December 2025 advisory opinion covering EWA products is not considered credit, which has added more confidence to payroll-linked deployment models in the U.S. As a result, the payroll and HR compliance software market is being shaped by API depth as much as by traditional payroll functionality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexities in Global Data Privacy Regulations | -1.2% | Global, with highest friction in Europe, China, India, and Brazil | Long term (≥ 4 years) |

| High Switching Costs From Legacy ERP Modules | -0.9% | North America and Europe, prevalent in large enterprise and regulated verticals | Medium term (2-4 years) |

| Skill Shortage in Payroll Compliance Specialists | -0.6% | Global, acute in APAC emerging markets and South America | Medium term (2-4 years) |

| Resistance to Payroll Process Outsourcing in Regulated Verticals | -0.4% | North America and Europe, concentrated in BFSI and government sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complexities in Global Data Privacy Regulations

The payroll and HR compliance software market still faces a major restraint from data privacy rules that do not align neatly across countries. Payroll systems handle sensitive employee records, pay details, tax identifiers, and banking data so that each cross-border workflow can trigger extra controls, local review, or product redesign. This becomes harder when one employer runs payroll across multiple countries and expects one system to support both centralized oversight and local legal requirements. Multi-country payroll findings show how common these cross-border operating models have become, indicating that privacy friction now affects a wider share of buyers than in earlier deployment cycles. The payroll and HR compliance software market, therefore, faces slower standardization because vendors often need local hosting choices, regional process logic, and more careful data access design to win multinational clients.

High Switching Costs From Legacy ERP Modules

The payroll and HR compliance software market is also restrained by the cost and risk of replacing legacy ERP-linked payroll modules, especially in large enterprises and regulated sectors. Migration is not a simple software swap, because employers need to validate gross pay, taxes, deductions, and reporting outputs before full cutover. That process often requires parallel runs, historical data mapping, retraining, and coordination between payroll, HR, finance, and compliance teams. In November 2025, an AI-powered Deployment Agent was reported to reduce implementation time by up to 25% in early deployments, underscoring how much vendor competition now focuses on reducing migration friction. Even with better deployment tools, the payroll and HR compliance software market still has to work through a large installed base that prefers a slower transition over payroll disruption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Consolidation Rewires The Competitive Default

Cloud accounted for 68.4% of revenue in 2025 and is projected to expand at a 10.8% CAGR through 2031, keeping it clearly ahead of on-premises and hybrid options. Cloud, therefore, represented 68.4% of the payroll and HR compliance software market share in 2025, and that lead reflects more than hosting preference alone. Buyers are choosing the cloud because payroll rules change frequently, local requirements vary, and software updates need to move faster than traditional release cycles. In the payroll and HR compliance software market, this model also supports easier rollout across new business units and new country payrolls. On-premises and hybrid deployments still matter for enterprises with heavy ERP customization, strict control requirements, or gradual migration plans.

The remaining deployment mix continues to serve buyers that cannot move all payroll workloads at once, particularly in regulated verticals and multinational groups with uneven country readiness. Hybrid deployments remain useful where firms want cloud speed for new-country payrolls but still want tighter local control for selected data sets or legacy integrations. Third-party certifications, secure hosting, and documented control frameworks have become a basic entry requirement for cloud vendors in Europe and other sensitive regions. That dynamic is narrowing the field of credible providers in the payroll and HR compliance software industry, because smaller vendors need a stronger compliance posture just to stay on the shortlist. The payroll and HR compliance software market is thus becoming more cloud-led, but the migration path still depends on risk tolerance, localization needs, and installed-base complexity.

By End User Enterprise Size: SMEs Become The Strongest Growth Engine

Large enterprises accounted for 61.7% of revenue in 2025, while SMEs are expected to record the faster 10.4% CAGR through 2031. The large enterprise base still anchors the payroll and HR compliance software market because multi-entity structures, global tax filings, audit demands, and ERP links create higher software intensity per customer. These employers often need deeper workflow control, stronger reporting layers, and closer coordination between payroll and finance systems. SMEs, however, are shifting from the margin of the category to the center of future demand because they now see payroll software as an operating necessity rather than an optional back-office tool. That demand is especially evident among small firms that want a single platform for payroll, employee records, benefits, and compliance.

Growth in the SME segment also reflects a shift in product design, as newer vendors emphasize speed of deployment and lower operational burden rather than heavy configuration. In France, 86% of companies were already using payroll software in 2025, suggesting that adoption can move quickly once the value case becomes clear among SMEs. Challenger vendors are also turning payroll into a platform entry point, then expanding into adjacent services that raise retention and wallet share over time. That cross-sell pattern matters for the payroll and HR compliance software industry because it shifts competition away from simple payroll processing and toward broader workforce administration. The payroll and HR compliance software market should therefore see the SME segment remain the most commercially active buyer group during the forecast period.

By Application: Compliance Management Gains Ground Alongside Core Processing

Payroll processing held the largest application share at 31.2% in 2025, while HR compliance and regulatory management is projected to grow at 11.6% CAGR through 2031. Payroll processing, therefore, remained the foundation of the payroll and HR compliance software market size in 2025, as every employer still starts with calculation, validation, and disbursement. The faster rise of compliance management shows that software demand is moving beyond pay execution and into rule monitoring, documentation, and audit readiness. Employers increasingly want compliance checks built into the workflow at the point of entry, not handled after the payroll run through manual review. That shift reduces correction cycles and ties payroll operations more closely to legal and policy controls.

Workforce time and attendance, benefits administration, and core HR records remain important adjacent layers, but they now feed more directly into the platform's compliance logic. This is one reason product boundaries are becoming less distinct, especially when vendors bundle payroll, time management, and record management into a single system. In November 2025, a major expansion of a global payroll platform included AI-powered deployment tools, reflecting how processing and compliance functionality are being packaged together for faster adoption.[4]Workday, Inc., “Workday Completes Acquisition of Sana,” Workday, newsroom.workday.com The payroll and HR compliance software market size for compliance-heavy workflows is therefore rising faster than the legacy processing core, even though processing still anchors total revenue. The payroll and HR compliance software market is moving toward application stacks that embed compliance, are continuous, and are closely tied to each payroll event.

By End User Industry Vertical: Healthcare Expands Faster While BFSI Holds The Lead

BFSI held the largest vertical share at 19.8% in 2025, while healthcare and life sciences are forecast to advance at an 11.9% CAGR through 2031. BFSI therefore accounted for 19.8% of the payroll and HR compliance software market size in 2025, supported by strict audit expectations, close control over workforce costs, and a low tolerance for payroll failure. Large financial institutions often operate across several jurisdictions, which keeps demand high for synchronized payroll outputs and documented compliance processes. Healthcare and life sciences are expanding faster because complex shift patterns, staffing volatility, and credential-linked workforce structures create a more challenging payroll environment than in many other verticals. That complexity increases the value of automated checks, time-linked pay logic, and accurate records across multiple worker types.

IT and telecom remain strong demand centers because global remote teams create ongoing tax and compliance complexity across borders. Manufacturing, retail, and government each bring distinct payroll needs tied to hourly work, seasonal headcount, union rules, or public-sector pay structures. Vendors that can explain AI outputs are also gaining an advantage in highly regulated verticals, as buyers seek automation without sacrificing audit transparency. This is especially relevant in the payroll and HR compliance software market, where platform selection is reviewed by payroll, compliance, finance, and IT simultaneously. The payroll and HR compliance software market, therefore, shows a split pattern, with BFSI holding scale and healthcare gaining momentum as its workforce administration burden intensifies.

Geography Analysis

North America accounted for 38.6% of global revenue in 2025, making it the largest regional market for payroll and HR compliance software. North America, therefore, accounted for 38.6% of the payroll and HR compliance software market share in 2025, led by the United States, which has a dense base of payroll platforms, integrations, and compliance-oriented product demand. The region also benefits from active development in earned wage access, which has become a major adjacent use case for payroll connectivity. In December 2025, it was clarified that covered earned wage access products are not considered credit under Regulation Z, which reduced one important regulatory concern for employer-integrated models. The payroll and HR compliance software market in North America also remains attractive because enterprise clients continue to invest in systems that connect payroll, workforce administration, and employee financial services.

Europe remained the second-largest regional market, with the United Kingdom, Germany, France, and Spain forming the main demand centers. The payroll and HR compliance software market in Europe is shaped by country-specific payroll formats, reporting requirements, and data-handling expectations that require both localization and scale. In France, 86% of companies used payroll software in 2025, and 62% of employees received digital payslips, indicating a mature digital payroll environment with room for validation and upgrade demand. These local requirements make Europe a strong region for vendors that combine multi-country coverage with deep in-country workflow support.

Asia-Pacific is projected to grow at a 12.7% CAGR through 2031, making it the fastest-growing region in the payroll and HR compliance software market. Demand is rising as labor markets formalize, SME digitization spreads, and multinational employers expand deeper into India, Southeast Asia, and Australia. In October 2025, one vendor announced plans to target native payroll coverage in 100+ countries by 2029, which shows how seriously vendors now view in-country capability as a growth lever across fast-moving regions. South America, the Middle East, and Africa are still earlier-stage markets, but adoption is rising as labor law modernization, employer-of-record services, and global HR platform expansion push payroll administration away from manual processes.

Competitive Landscape

The payroll and HR compliance software market is moderately consolidated at the top tier and highly fragmented across the mid-market and SME base. The U.S. payroll market had more than 5,700 providers, and the top 35 systems accounted for 70% of employer penetration in 2025, up from 60.4% three years earlier. That pattern means scale matters, but no single group of providers controls the full market across customer sizes, geographies, and workforce models. In the payroll and HR compliance software market, leading incumbents such as ADP, Paychex, Workday, UKG, and SAP are competing by deepening AI, global payroll, and partner ecosystem capabilities. At the same time, challengers such as Rippling, Deel, Gusto, and HiBob are winning attention with faster deployment, cleaner interfaces, and strong appeal among growing companies.

ADP's January 2026 launch of persona-based ADP Assist AI agents showed how the largest vendors are turning data scale into a product advantage, with a global data platform that spans 1.1 million clients and 42 million wage earners across 140 countries. Workday strengthened its position with the November 2025 acquisition of Sana and the March 2026 launch of Sana from Workday, which added a broader AI interface and 300+ automation skills across HR and finance workflows. UKG also expanded its AI position in October 2025 through a broader partnership with Google Cloud, which supports UKG Bryte AI agents and a wider analytics stack. These moves show that the payroll and HR compliance software market is increasingly rewarding vendors that pair core payroll strength with automation and ecosystem reach.

The main white space remains global contractor and distributed workforce payroll, where traditional enterprise models have not always offered enough speed or country depth. Deel's USD 300 million Series E round in October 2025, at a USD 17.3 billion valuation, underlined investor confidence in owned payroll infrastructure and cross-border workforce administration. Interoperability is also becoming a gatekeeping factor, as shown by Ramco Payce achieving Workday Global Payroll Connect certification in early 2026. The payroll and HR compliance software market is therefore becoming harder to win through payroll functionality alone, because buyers now evaluate AI execution, ecosystem fit, country coverage, and implementation speed together.

Payroll And HR Compliance Software Industry Leaders

Automatic Data Processing, Inc.

Workday, Inc.

UKG Inc.

SAP SE

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Gusto surpassed USD 1 billion in actual revenue over the prior 12 months, with AI generating 50% of new code and resolving 50% of customer support cases. The milestone positions Gusto closer to a potential IPO and follows its 2025 acquisition of Guideline for approximately USD 600 million, adding 401(k) retirement plan management to its payroll and HR platform.

- April 2026: Papaya Global and Tech Mahindra announced a strategic alliance to modernize global workforce operations and payments across 180 countries, combining Papaya's AI-first Workforce OS and Payments OS with Tech Mahindra's technology consulting and managed services. The partnership targets global enterprises managing diverse international workforce structures and complex cross-border payment requirements.

- March 2026: Workday launched "Sana from Workday," an AI superintelligence interface offering 300+ automation skills for HR and finance workflows, covering self-service requests, multi-system orchestration, and no-code workflow creation. Available to all Workday customers through Workday Flex Credits, the launch represents the first major AI-native payroll interface at enterprise scale.

- March 2026: ADP launched AI agent capabilities within ADP Marketplace, enabling agentic AI partners to complete multistep HR and payroll tasks. Participating partners include Tapcheck and Payactiv for earned wage access, among others, reinforcing ADP's strategy of embedding EWA directly into its payroll workflow.

Global Payroll And HR Compliance Software Market Report Scope

The payroll and HR compliance software market refers to digital platforms that automate payroll processing, workforce administration, and regulatory compliance. These solutions integrate employee records, tax filings, benefits, and audit controls into unified workflows, enabling organizations to streamline operations, reduce errors, and meet legal requirements while supporting scalability across enterprises and SMEs.

The Payroll and HR Compliance Software Market is Segmented by Deployment Model (Cloud, On-premise, and Hybrid), End User Size (Large Enterprises, and SMEs), Application (Payroll Processing, HR Compliance, Time and Attendance, Benefits, and Core HR), Vertical (BFSI, Healthcare, IT and Telecom, Manufacturing, Retail, Government, and Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Payroll Processing |

| Time and Attendance Management |

| HR Compliance and Regulatory Management |

| Benefits and Compensation Administration |

| Core HR and Employee Records Management |

| Information Technology (IT) and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Industrial Manufacturing |

| Retail and eCommerce |

| Government and Public Sector |

| Other End User Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Model | Cloud | |

| On-premise | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Payroll Processing | |

| Time and Attendance Management | ||

| HR Compliance and Regulatory Management | ||

| Benefits and Compensation Administration | ||

| Core HR and Employee Records Management | ||

| By End User Industry Vertical | Information Technology (IT) and Telecom | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Industrial Manufacturing | ||

| Retail and eCommerce | ||

| Government and Public Sector | ||

| Other End User Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the payroll and HR compliance software market?

The payroll and HR compliance software market size is estimated at USD 25.6 billion in 2026 and is projected to reach USD 40.7 billion by 2031 at a 9.7% CAGR.

What is driving demand for payroll and HR compliance platforms?

Demand is being supported by multi-country payroll complexity, labor law compliance needs, cloud adoption, AI-based anomaly detection, and tighter integration with fintech services.

Which deployment model leads revenue growth?

Cloud leads the deployment mix with 68.4% share in 2025 and is also the fastest-growing deployment model at a 10.8% CAGR through 2031.

Which customer group is growing the fastest?

SMEs are the fastest-growing enterprise-size segment, with projected growth of 10.4% through 2031, even though large enterprises still hold the bigger revenue base.

Which application area is expanding the fastest?

HR compliance and regulatory management is the fastest-growing application, with an 11.6% CAGR, while payroll processing remains the largest application segment.

Which region shows the strongest future growth?

Asia-Pacific is the fastest-growing region at a 12.7% CAGR through 2031, while North America remains the largest regional market with 38.6% share in 2025.

Page last updated on: