Payroll Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

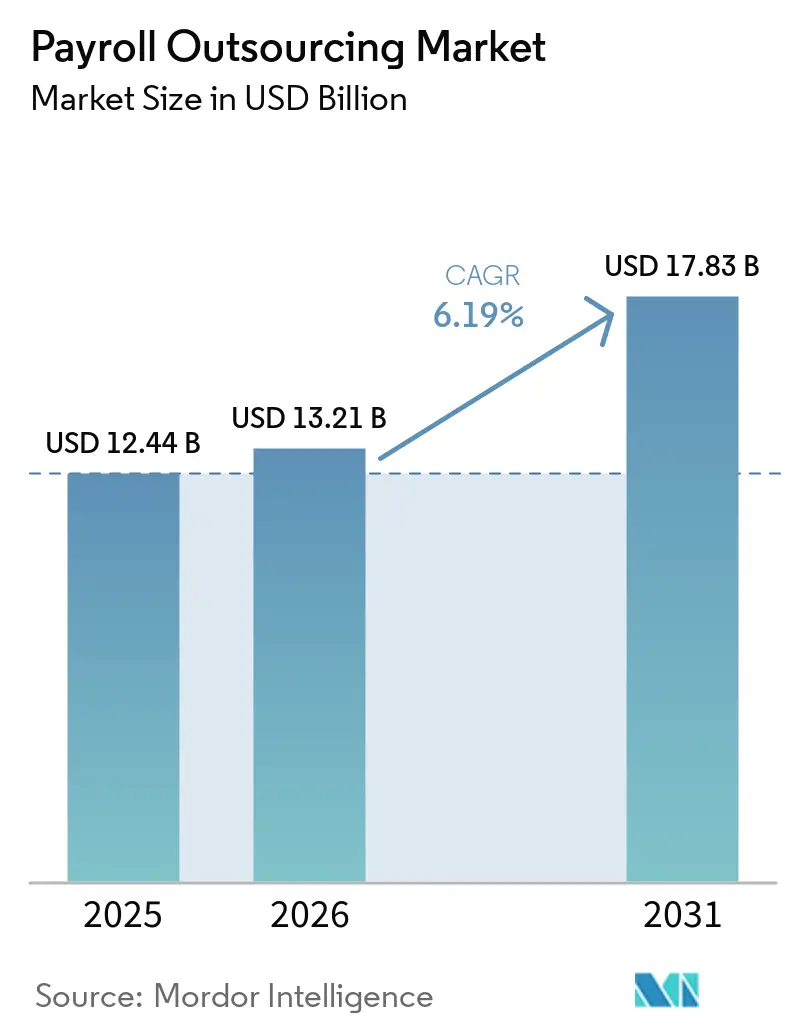

| Market Size (2026) | USD 13.21 Billion |

| Market Size (2031) | USD 17.83 Billion |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

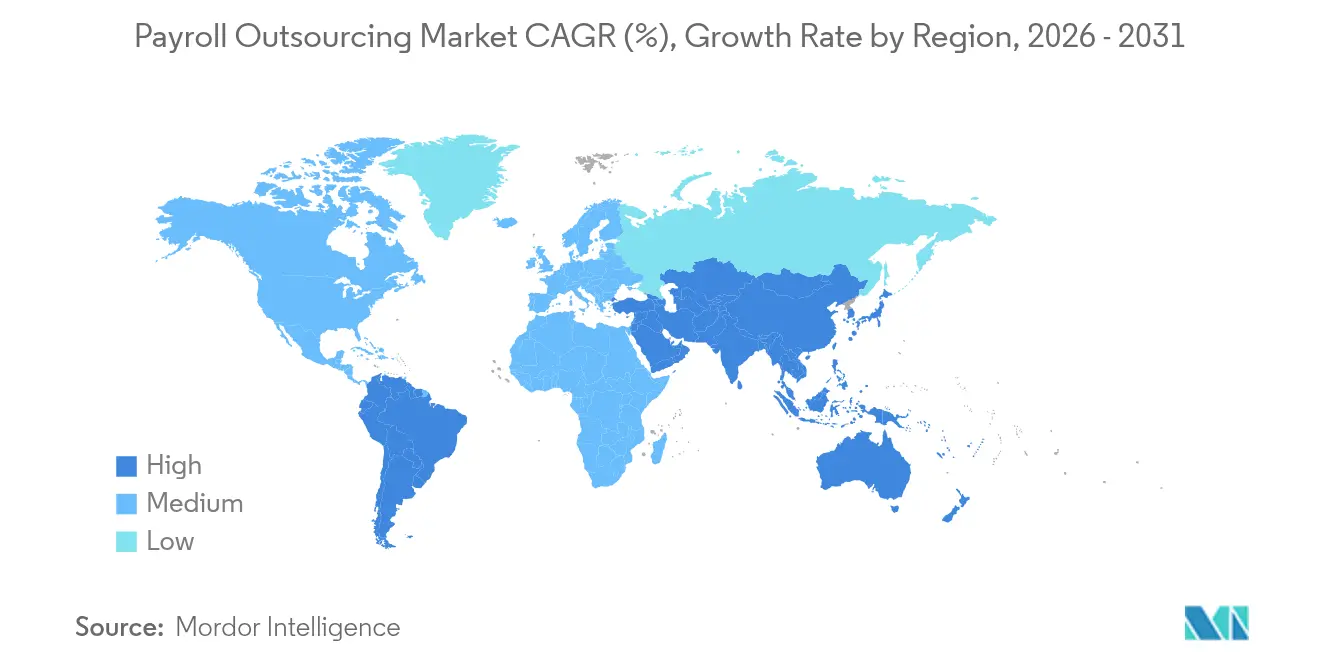

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payroll Outsourcing Market Analysis by Mordor Intelligence

The payroll outsourcing market size was valued at USD 12.44 billion in 2025 and estimated to grow from USD 13.21 billion in 2026 to reach USD 17.83 billion by 2031, at a CAGR of 6.19% during the forecast period (2026-2031). This momentum comes from organizations seeking relief from escalating compliance obligations, the spread of remote work, and the steady pivot toward cloud-native human-capital platforms. Rising expectations for real-time analytics, seamless time-tracking, and error-free tax filing keep technology spending elevated, while scale economies allow providers to price services competitively. Vendors that combine AI-driven anomaly detection with localized regulatory expertise are widening their addressable base across sectors and company sizes. At the same time, mergers among global and regional specialists indicate that the payroll outsourcing market is entering a phase where platform breadth matters as much as price. [1]U.S. Department of the Interior, “Tax Changes Implemented Pay Period 2025-03,” ibc.doi.gov

Key Report Takeaways

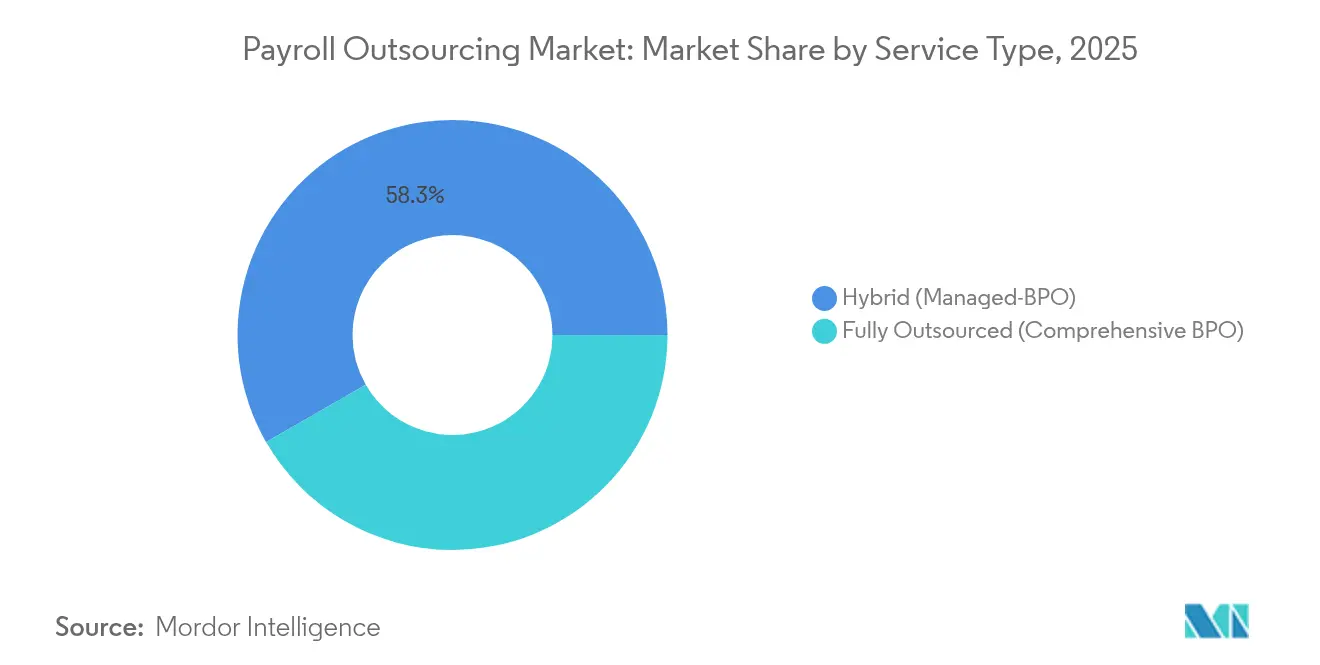

- By service type, the hybrid model led with 58.30% of payroll outsourcing market share in 2025, while fully outsourced services are projected to post an 8.39% CAGR to 2031.

- By deployment model, cloud solutions commanded 80.40% revenue share in 2025; the segment is forecast to expand at a 10.06% CAGR through 2031.

- By enterprise size, large enterprises held 63.20% share of the payroll outsourcing market size in 2025, whereas SMEs are advancing at a 9.58% CAGR to 2031.

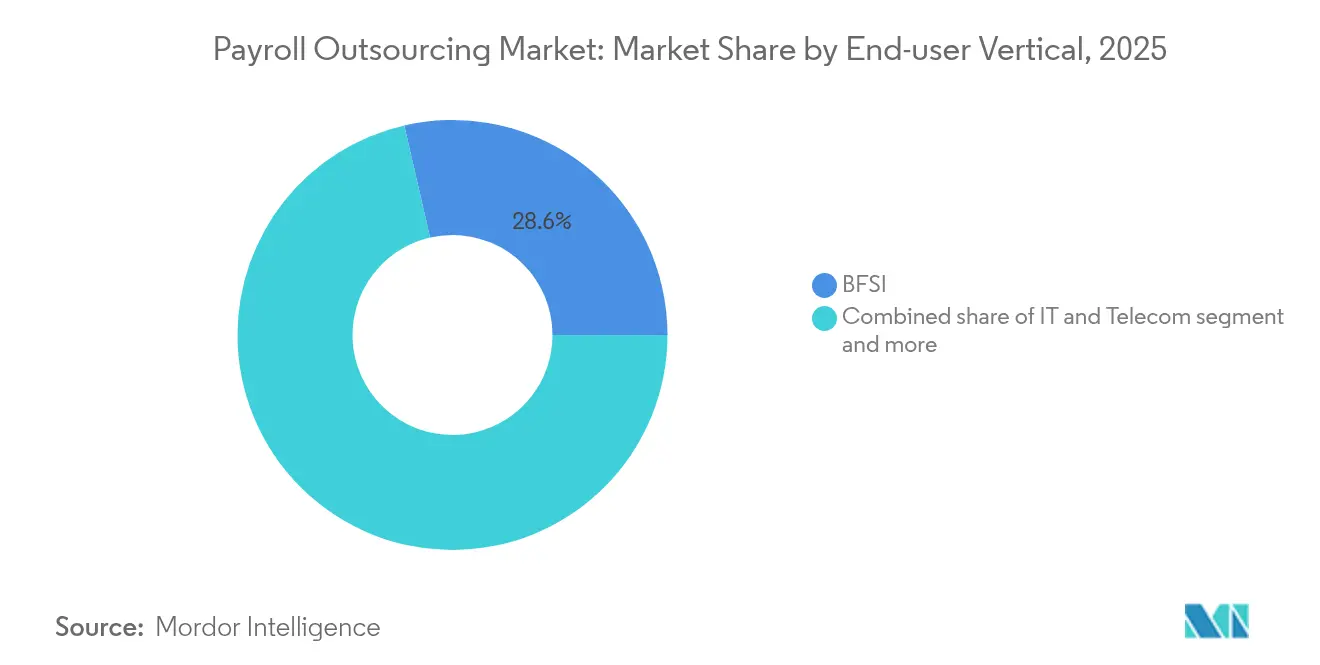

- By end-user vertical, BFSI captured 28.60% of 2025 revenue; healthcare and life sciences is slated to grow at a 9.66% CAGR out to 2031.

- By geography, North America accounted for 40.70% of 2025 revenue, while Asia-Pacific is the fastest-growing region at an 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Payroll Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for end-to-end automation | 1.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Shift to remote & hybrid workforces | 1.50% | Global, particularly North America & APAC | Short term (≤ 2 years) |

| Compliance proliferation across jurisdictions | 1.20% | Global, with emphasis on US states & EU | Long term (≥ 4 years) |

| Cost-containment pressure on HR functions | 1.00% | Global, with focus on SME segment | Medium term (2-4 years) |

| AI-led anomaly detection in gross-to-net | 0.80% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| ESG-driven vendor selection criteria | 0.40% | Europe & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for End-to-End Automation

Payroll is shifting from a periodic back-office task to a continuous data flow that touches time collection, tax filing, benefits, and analytics. Integrating these pieces can eliminate up to 80% of manual inputs, freeing HR staff for higher-value work. ADP’s 2024 rollout of generative-AI helpers showed that automation heightens both speed and accuracy, supporting record customer-satisfaction scores. Providers therefore package robotic process automation with conversational interfaces to remove keystrokes from pay-run approvals. As early adopters report measurable error reductions, demand ripples outward, lifting the payroll outsourcing market beyond traditional cost-saving narratives. Expanded APIs also let clients push payroll data into financial-planning tools, reinforcing platform stickiness.

Shift to Remote & Hybrid Workforces

Distributed work has turned single-jurisdiction payroll services into a labyrinth of state, provincial, and national rules. Each cross-border hire triggers new income-tax, social-security, and benefits obligations that many internal teams cannot track. Workday’s 2024 move into Australian payroll, bundled with AI across 50-plus use cases, underscored this pain point and prompted global firms to standardize on cloud providers that carry country-level compliance libraries. Because remote-work ratios remain elevated, demand for multi-country calculators and localized e-filing will persist. As a result, the payroll outsourcing market is becoming a core enabler of borderless talent strategies, not just an administrative afterthought. [2]Workday, “Investor Presentation,” workday.com

Compliance Proliferation Across Jurisdictions

Regulators continue to add complexity: the US Social Security wage base climbed from USD 168,600 to USD 176,100 for 2025, while the SECURE 2.0 Act imposes fresh retirement-plan reporting layers. European authorities are revising withholding thresholds, and emerging markets are copying these playbooks. Every change demands code updates, audit trails, and employee notices, stretching in-house teams. Outsourcers amortize these costs across thousands of clients, offering scale advantages that pull new buyers into the payroll outsourcing market. Growing penalty sizes for late or wrong filings also shift risk calculations decisively toward specialized vendors.

Cost-Containment Pressure on HR Functions

Boards expect HR to produce analytics and talent insights without raising headcount. Outsourcing transactional work lets HR leaders redeploy budgets into strategic programs such as reskilling and employee-experience enhancements. Paychex’s 2024 revenue of USD 5.3 billion across 745,000 clients illustrates how shared-service models unlock economies of scale, which providers partly pass on as price relief. For SMEs, the delta between internal processing cost and vendor subscription fees widens as compliance grows, explaining the 9.70% CAGR in that segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-sovereignty regulations | -0.90% | Europe & APAC, with spillover to global operations | Long term (≥ 4 years) |

| Cyber-security skill shortages at vendors | -0.70% | Global, with acute impact in North America & Europe | Medium term (2-4 years) |

| Complex union-specific wage rules | -0.50% | North America & Europe, sector-specific impact | Medium term (2-4 years) |

| AI "black-box" regulatory scrutiny | -0.30% | Global, with early focus in Europe & California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Sovereignty Regulations

More jurisdictions now demand that personal data remain inside national borders, forcing outsourcers to duplicate infrastructure and fragment databases. The EU’s continued GDPR enforcement and proposed APAC data-localization bills require regional hosting nodes, driving up capital spending and slowing rollouts. Multinationals that once sought single-instance global payroll must adopt hub-and-spoke architectures, raising complexity. Regional providers with in-country hosting gain an advantage, restraining the global scale plays that once defined the payroll outsourcing market.

Cyber-Security Skill Shortages at Vendors

Payroll files store bank numbers, social-security IDs, and salary histories—prime targets for attackers. Yet outsourcers compete with banks and cloud giants for scarce cybersecurity talent, inflating payroll costs and stretching patch cycles. Smaller vendors, in particular, struggle to staff 24/7 security-operations centers, making them less attractive to heavily regulated clients. Persistent talent gaps elevate vendor-selection hurdles and may limit the payroll outsourcing market’s growth until automation offsets staffing needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hybrid Models Drive Market Evolution

Hybrid offerings retained a 58.30% payroll outsourcing market share in 2025, signalling buyer appetite for retaining control over data validation while offloading complex calculations. This structure appeals to organizations still aligning data-privacy policies with external hosting requirements. However, fully outsourced packages are recording an 8.39% CAGR, indicating a gradual shift as trust in vendor controls rises. The payroll outsourcing market size associated with comprehensive BPO services is projected to surpass USD 7.35 billion by 2031, riding on evidence that end-to-end hand-offs reduce total processing cost per employee by double-digit percentages.

As clients mature, many migrate from hybrid to full outsourcing to capture deeper automation and analytics. Vendors support this glide path with modular contracts that let companies activate additional components—tax filing, garnishment, or mobility-related services—on a shared platform. This staircase approach keeps churn low and increases account value. Providers that demonstrate seamless transitions without data re-implementation earn higher NPS scores, reinforcing market momentum.

By Deployment Model: Cloud Dominance Accelerates Innovation

Cloud deployments held 80.40% of revenue in 2025, making software-as-a-service the de-facto standard for new deals. The cloud slice of the payroll outsourcing market size is forecast to reach USD 14.35 billion by 2031, supported by a 10.06% CAGR. Buyers cite instant regulatory updates, integration APIs, and geographic scalability as key motives. Cloud suites also embed analytics dashboards that let finance leaders reconcile payroll to GL in near real time.

On-premises and hosted models persist in defense, energy, and public-sector accounts that require air-gapped environments. Yet their aggregate share shrinks yearly as FedRAMP-authorized clouds clear security hurdles. With hyperscale data-center footprints expanding in Latin America and Africa, latency barriers are falling, encouraging late adopters to switch. Therefore, the payroll outsourcing market is steadily tilting toward subscription revenue, changing cash-flow profiles for providers.

By Enterprise Size: SME Segment Emerges as Growth Engine

Large organizations still contribute 63.20% of 2025 billings, but the SME cohort is outpacing them, growing at a 9.58% CAGR. Competitive SaaS pricing tiers, self-onboarding portals, and marketplace plug-ins make enterprise-grade functions attainable for firms with fewer than 1,000 staff. For many, the alternative is non-compliance risk in multiple states or countries, making the outsourcing fee a predictable insurance premium.

Vendors court SMEs with bundled HR, benefits, and recruiting add-ons, raising stickiness. Paychex’s addition of 50,000 small-business clients in Q4 2024 illustrated the volume potential in this band. As more SMEs adopt digital wallets and on-demand pay, vendors that integrate such features without extra modules can capture wallet share. Consequently, the payroll outsourcing market is broadening beyond Fortune 500 budgets.

By End-User Vertical: Healthcare Leads Sectoral Transformation

Financial-services institutions accounted for 28.60% of 2025 revenue because of stringent audit trails and multi-entity structures. However, healthcare and life sciences will be the fastest riser at a 9.66% CAGR. Hospitals juggle union differentials, credential-based pay scales, and rotating schedules that strain legacy systems. Outsourcers with nurse-staffing templates and credential checks gain traction, encouraging vertical specialization.

Manufacturers adopt outsourcing to handle global plant footprints where currencies, allowances, and shift premiums differ. Retail chains rely on providers to compute variable hours and seasonal spikes without internal re-coding. Government agencies, once reluctant to externalize payroll, now pilot shared-service models to cut IT upkeep. These sector dynamics diversify revenue, lessening exposure to any single industry cycle.

By Payroll Component Covered: Integration Drives Comprehensive Solutions

Core pay-run engines remain the entry point, but clients increasingly bundle time & attendance, tax filing, and employee self-service. Vendors report attach rates above 60% for statutory-reporting modules as new tax rules intensify. Analytics and reporting add-ons are growing fastest, driven by CFO demands for labour-cost transparency.

Time-tracking integration becomes crucial for hybrid offices, where biometric devices, mobile apps, and geofencing must sync with payroll. Employee portals reduce HR ticket volume by giving staff visibility into pay slips, PTO balances, and withholding elections. Together, these shifts reinforce the payroll outsourcing market’s transition from single-function services to unified workforce platforms.

Geography Analysis

North America remained the largest regional contributor with 40.70% of 2025 revenue, fuelled by intricate federal, state, and local regulations. Frequent IRS rule changes, such as the updated Social-Security wage base, keep in-house teams under pressure, sustaining vendor pipeline activity. Canada’s bilingual requirements and Mexico’s CFDI electronic-invoice mandates further expand addressable demand.

Asia-Pacific is the growth pacesetter, posting an 8.78% CAGR to 2031. Rapid digitization in China and India aligns with multi-country payroll rollouts among exporters and tech firms. Ramco’s 2024 launch of a bilingual Japan payroll module shows how regional players tailor features like social-insurance deductions to local norms. Cloud data-center buildouts in Indonesia and the Philippines cut latency and comply with sovereignty laws, unlocking pent-up adoption.

Europe offers a stable but demanding market due to GDPR and ever-evolving social-contribution ceilings. Providers differentiate on pan-EU coverage and Brexit-specific workflows for UK firms hiring EU residents. In Eastern Europe, wage-code complexity and currency fluctuations prompt shared-service pilots. Elsewhere, Middle East, Africa, and South America present greenfield opportunities tied to economic diversification and tax simplification. Collectively, these trends keep the payroll outsourcing market firmly on an upward trajectory.

Competitive Landscape

The competitive field combines global heavyweights and nimble disruptors. ADP closed fiscal 2024 with USD 19.2 billion in revenue, serving over 1.1 million clients in more than 140 countries. Scale enables it to absorb compliance costs and invest consistently in AI R&D. Paychex expanded its portfolio by acquiring Paycor for USD 4.1 billion in 2025, a move expected to generate USD 80 million in annual synergies and bolster AI-powered mid-market offerings.

On the emerging side, Rippling’s USD 16.8 billion valuation after a USD 450 million raise underscores investor confidence in unified workforce stacks that merge payroll, IT provisioning, and spend management. Deel’s purchase of Safeguard Global’s payroll division broadens multi-country coverage to more than 150 nations, positioning it for Workday-adjacent ecosystem deals.

Competition now centers on depth of regulatory content, quality of AI models, and breadth of ancillary modules such as earned-wage access or embedded payments. Providers unable to maintain cybersecurity talent or meet rising ESG disclosure demands risk relegation to niche roles. Overall, the payroll outsourcing market is moderately consolidated: the top five vendors command just under 60% of global revenue. [4]Automatic Data Processing Inc., “Form 10-K for the Year Ended June 30, 2024,” sec.gov

Payroll Outsourcing Industry Leaders

Automatic Data Processing, Inc.

Paychex, Inc.

Alight Solutions LLC

Ceridian HCM Holding Inc.

TMF Group B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Rippling completed a USD 450 million funding round, reaching a USD 16.8 billion valuation and surpassing USD 350 million in annual recurring revenue.

- April 2025: Paychex finalized the USD 4.1 billion acquisition of Paycor, creating a combined HCM portfolio that serves nearly 800,000 customers and processes pay for 1 in 11 US private-sector employees.

- March 2025: Deel acquired Safeguard Global’s payroll division, expanding its multi-country capabilities across 150+ jurisdictions and deepening integration with Workday.

- February 2025: ADP posted 7% YoY revenue growth in Q1 2025, lifting its full-year Employer Services outlook to 6%-7% revenue expansion.

Global Payroll Outsourcing Market Report Scope

Payroll outsourcing is a service that is supplied by a third-party company. It assists firms with legal, tax, and accounting services so that employees receive their paychecks on schedule. The services ensure that the people are paid accurately and on time, in compliance with regulations.

The payroll outsourcing market is segmented by type (hybrid, fully outsourced), by enterprise size (SMEs, large enterprises), by end-users (BFSI, IT and telecom, healthcare, manufacturing, government, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hybrid (Managed-BPO) |

| Fully Outsourced (Comprehensive BPO) |

| Cloud-based |

| On-premises / Hosted |

| Large Enterprises (?1,000 employees) |

| Small and Mid-sized Enterprises (<1,000 employees) |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Manufacturing |

| Government and Public Sector |

| Retail and E-commerce |

| Others (Hospitality, Education, etc.) |

| Core Pay-run Processing |

| Time and Attendance Integration |

| Tax Filing and Statutory Reporting |

| Employee Self-Service and Analytics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Hybrid (Managed-BPO) | |

| Fully Outsourced (Comprehensive BPO) | ||

| By Deployment Model | Cloud-based | |

| On-premises / Hosted | ||

| By Enterprise Size | Large Enterprises (?1,000 employees) | |

| Small and Mid-sized Enterprises (<1,000 employees) | ||

| By End-user Vertical | BFSI | |

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Retail and E-commerce | ||

| Others (Hospitality, Education, etc.) | ||

| By Payroll Component Covered | Core Pay-run Processing | |

| Time and Attendance Integration | ||

| Tax Filing and Statutory Reporting | ||

| Employee Self-Service and Analytics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the payroll outsourcing market in 2026?

The payroll outsourcing market is valued at USD 13.21 billion in 2026, with a projected rise to USD 17.83 billion by 2031.

Which deployment model is growing fastest?

Cloud-based solutions are expanding at a 10.06% CAGR as organizations favour scalable, update-rich platforms.

Why are SMEs turning to payroll outsourcing?

SMEs gain enterprise-grade compliance and automation at subscription prices that are often lower than maintaining in-house systems, driving a 9.58% CAGR for the segment.

Which region leads in market share, and which is growing fastest?

North America holds 40.70% of global revenue, while Asia-Pacific is the fastest-growing region at an 8.78% CAGR through 2031.

What is the major driver behind healthcare’s rapid adoption?

Healthcare organizations face intricate union rules, credential-based pay scales, and compliance mandates, pushing them toward specialized outsourcing and fuelling a 9.66% CAGR.

How is AI influencing payroll outsourcing?

AI-powered anomaly detection and chat-based query resolution cut error rates and enhance user experience, becoming a standard differentiator among top vendors.

Page last updated on: