Online Beauty and Personal Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

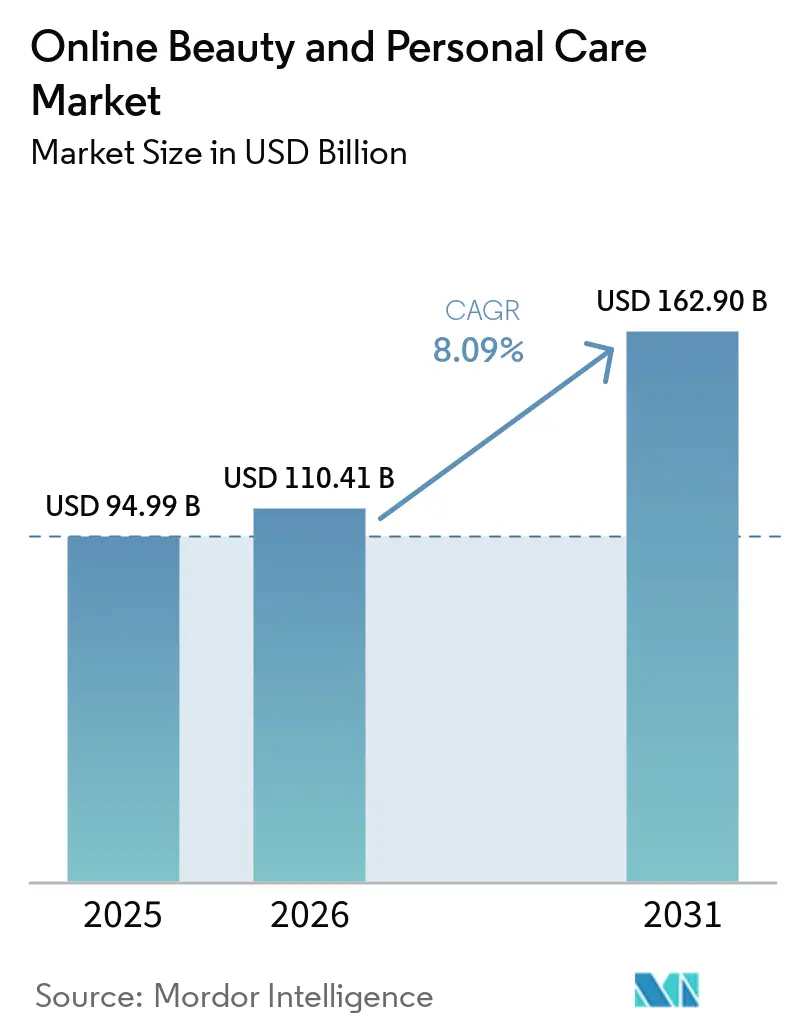

| Market Size (2026) | USD 110.41 Billion |

| Market Size (2031) | USD 162.90 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Online Beauty and Personal Care Market Analysis by Mordor Intelligence

The online beauty and personal care market size was valued at USD 94.99 billion in 2025 and is estimated to grow from USD 110.41 billion in 2026 to reach USD 162.90 billion by 2031, at a CAGR of 8.09% during the forecast period (2026-2031). Growing concerns regarding the side effects of chemicals in personal care products, which lead to skin irritation, allergies, and dullness, have been fueling the demand for natural and organic skincare products. Oral diseases, while largely preventable, pose a major health burden for many countries and affect people throughout their lifetime, causing pain, discomfort, disfigurement, and even death. The World Health Organization (WHO) estimated that oral diseases affect close to 3.5 billion people worldwide, with caries of permanent teeth being the most common condition. Globally, it is estimated that 2 billion people suffer from caries of permanent teeth, and 520 million children suffer from caries of primary teeth. The headline risks include the persistence of counterfeit beauty products on third-party marketplaces and the exposure of consumer data platforms to ransomware attacks, both of which can erode the trust premium that online channels have accumulated over physical retail [1]Source: Personal Care Products Council, "Counterfeit Cosmetics", personalcarecouncil.org.

Key Report Takeaways

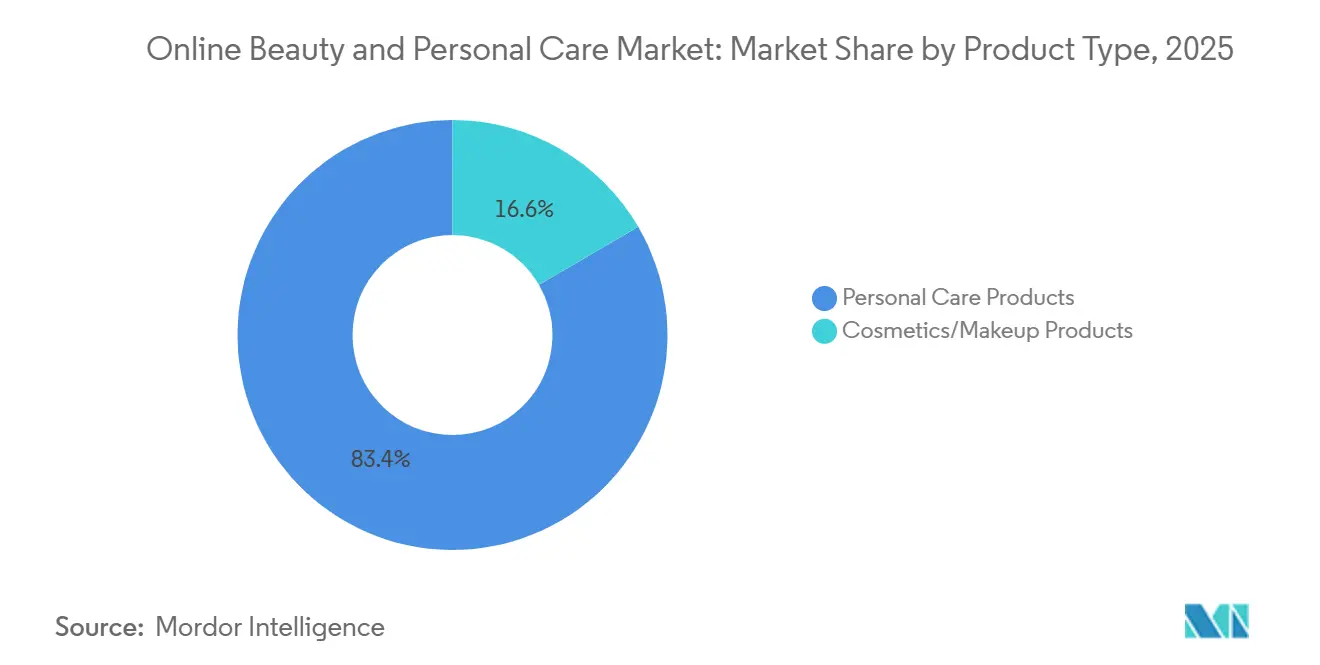

- By product type, personal care products led with 83.40% of the beauty and personal care market share in 2025, while cosmetics/makeup products are projected to record the fastest CAGR at 8.78% through 2031.

- By price, mass products held 66.87% share of the beauty and personal care products market size in 2025, whereas the premium is forecast to expand at a 10.34% CAGR between 2026 and 2031.

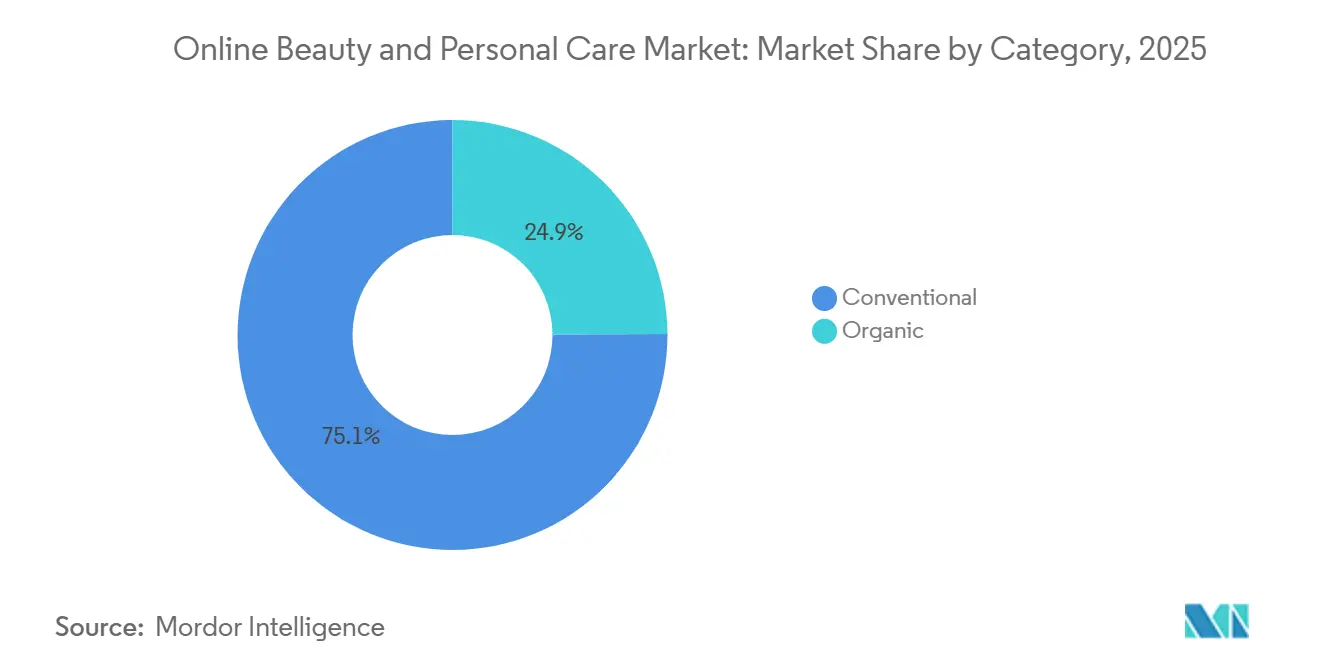

- By category, conventional generated 75.03% revenue in 2025; organic alternatives are set to grow at a 9.54% CAGR to 2031.

- By distribution channel, the third-party retailer platform generated 75.80% revenue in 2025; company-owned platforms are set to grow at a 8.44% CAGR to 2031.

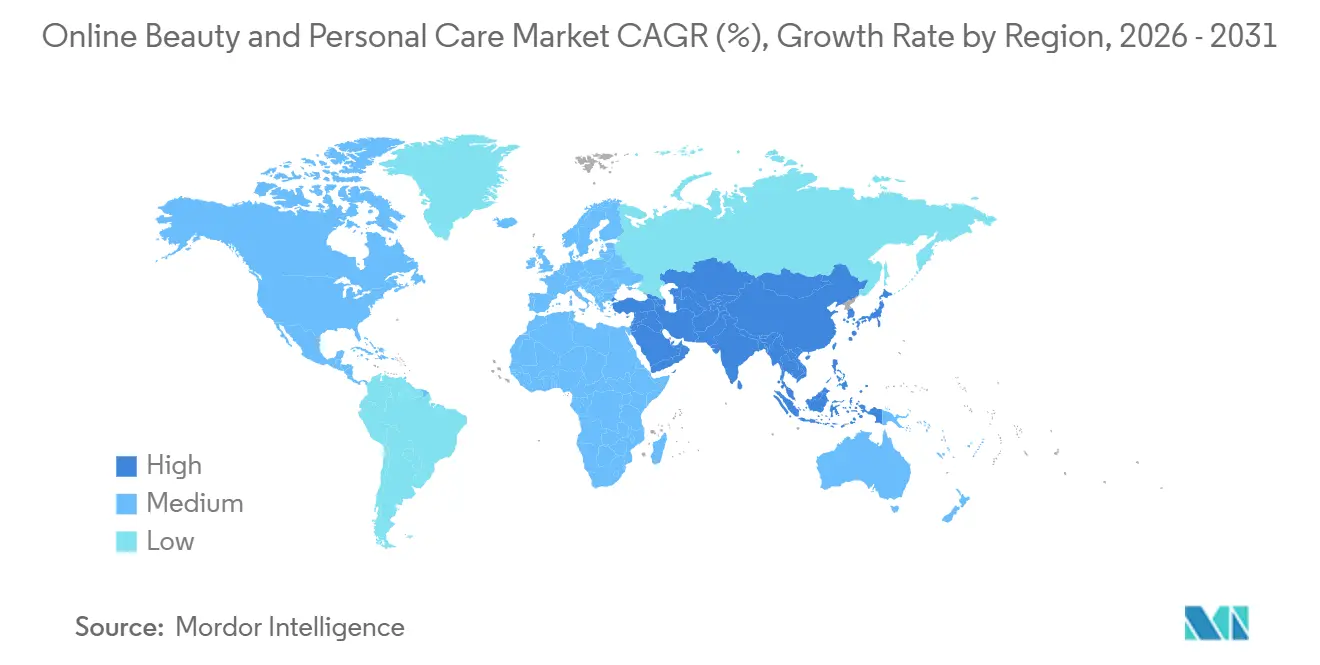

- By geography, Asia-Pacific accounted for 36.78% of revenue in 2025 and will post the strongest 9.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Online Beauty and Personal Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | ~% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone adoption increases digital beauty shopping | +1.4% | Global, concentrated in APAC (Asia-Pacific) and emerging markets | Short term (≤ 2 years) |

| Social media influencers drive product discovery | +1.8% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| AI-powered recommendations enhance shopping experiences | +1.2% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Direct-to-consumer brands strengthen digital sales channels | +1.0% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Faster delivery services improve consumer convenience | +0.9% | Global, strongest in North America and East Asia | Short term (≤ 2 years) |

| Growing demand for personalized beauty solutions | +1.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone Adoption Increases Digital Beauty Shopping

Mobile commerce accounts for the foundational layer of beauty e-commerce growth, particularly in markets where smartphone penetration is still expanding. In South Korea, one of the world's most digitally mature beauty markets, online beauty sales increased, with mobile shopping accounting for 80.4% of those online transactions [2]Source: Statistics Korea, "Online Cosmetic Sales", mods.go.kr. In Brazil, hygiene and beauty products represent a significant portion of total e-commerce value in the mass consumer goods segment, with online channel penetration crossing 33% of households for the first time in 2025, driven by the continued improvement in mobile payment infrastructure, according to the Worldpanel by Numerator, via Mercado e Consumo. The strategic implication that is routinely underweighted is that smartphone-driven beauty commerce does not simply replicate desktop behaviour at smaller screen sizes; it enables discovery-driven rather than search-driven purchase patterns, with consumers encountering products through algorithmic recommendations and creator content before they ever form an intent to buy.

Social Media Influencers Drive Product Discovery

Social commerce has become the primary discovery engine for the beauty and personal care category, displacing keyword search as the default starting point for purchasing decisions. Beauty and personal care accounted for a significant share of US TikTok Shop sales in 2025, with consumers spending increasing annually on beauty products through the platform. The second-order dynamic here is that influencer virality on TikTok now directly monetizes on Amazon: products that trend organically on social platforms generate immediate lifts in branded and non-branded search volume on marketplace channels, effectively turning influencer content into a low-cost performance marketing channel. In China, livestreaming accounts for the majority of beauty sales on platforms like Douyin, demonstrating the ceiling toward which other markets are converging.

AI-Powered Recommendations Enhance Shopping Experiences

Generative AI is restructuring the beauty discovery funnel in a way that disadvantages brands optimized for keyword search rather than semantic authority. A majority of beauty consumers have already received product recommendations from generative AI tools, a proportion that is expanding as conversational AI becomes embedded in retail apps, beauty brand websites, and marketplace search interfaces. AI also generates advantages upstream: Shiseido deployed its VOYAGER AI formulation development platform to produce its first AI-designed suncare product for Summer 2026, compressing product development cycles in a category where speed-to-trend is a material competitive variable. In India, most consumers familiar with AI report that it makes online beauty shopping easier, suggesting that APAC adoption will accelerate adoption timelines faster than Western markets anticipated.

Growing Demand for Personalized Beauty Solutions

Personalization has shifted from a marketing claim to a formulation and product development imperative, as consumers demonstrate consistent willingness to share personal data, skin type, purchase history, and routine preferences, in exchange for tailored product experiences. The convergence of AI diagnostics, augmented-reality try-on tools, and proprietary customer data platforms is enabling brands to move from mass product lines toward dynamically configured recommendation stacks that are difficult for competitors to replicate. Estée Lauder's partnership with Shopify and its concurrent integration with Accenture's AI services, announced in late 2025, is partly about manufacturing this personalization moat, giving the company real-time consumer behavioural data across DTC and freestanding stores that can feed product development as well as digital merchandising.

Restraints Impact Analysis*

| Restraint | ~% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit products undermine consumer trust online | -1.2% | Global, acute in North America, Europe, and APAC | Medium term (2-4 years) |

| Cybersecurity threats affect customer trust and transactions | -0.8% | Global | Medium term (2-4 years) |

| Supply chain disruptions delay product availability online | -0.9% | Global, acute in APAC and Europe | Short term (≤ 2 years) |

| Regulatory compliance requirements increase business complexity | -0.7% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Undermine Consumer Trust Online

The proliferation of counterfeit beauty products on third-party marketplaces represents one of the most acute structural threats to the online channel's long-term trust premium. The cosmetics industry loses approximately USD 5.4 Bn annually to fraudulent sellers, with counterfeit and lookalike products undercutting legitimate brands on price while eroding the safety and efficacy associations that premium beauty products depend upon. In February 2026, Estée Lauder filed suit against Walmart, alleging that counterfeit versions of La Mer, Tom Ford, Clinique, and other prestige brands were sold through its third-party marketplace, with the retailer allegedly profiting from SEO manipulation that drove traffic to the fraudulent listings. The regulatory influence of the US Modernization of Cosmetics Regulation Act (MoCRA) and the proposed Shop Safe Act provides a compliance framework that gives brands stronger legal tools to report fraudulent marketplace listings to the FDA and US Customs and Border Protection, though enforcement efficacy is constrained by the speed at which counterfeit listings regenerate [3]Source: U.S. Food & Drug Administration, "Modernization of Cosmetics Regulation Act of 2022 (MoCRA)", fda.gov.

Cybersecurity Threats Affect Customer Trust and Transactions

Beauty and personal care companies have become high-value ransomware targets because they combine consumer payment data, skin-type analytics, purchase history, and proprietary formulation data within interconnected digital infrastructure. In July 2025, the Kairos ransomware group claimed responsibility for an attack on Inspired Beauty Brands, a US-based personal care developer, exfiltrating 1.55 TB of sensitive data and threatening to publish it unless a ransom was paid. Separately, the Everest ransomware gang claimed to have obtained records tied to more than 600,000 Clarins customers across the United States, France, and Canada, publishing sample purchase histories and product-category data that cybersecurity analysts noted substantially increased the value of the stolen dataset to downstream fraudsters. Estée Lauder's ERP systems were also targeted via a zero-day Oracle vulnerability, with the Cl0p group claiming access to manufacturing, quality control, and supply chain documentation, underscoring that the attack surface extends well beyond consumer-facing platforms into core operational infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Products Anchor as Cosmetics Rebound Online

Personal care products accounted for 83.4% of market value in 2025, a dominance anchored by the structural advantages of habitual replenishment: hair care, skin care, bath and shower, oral care, and deodorants are all high-frequency, subscription-compatible categories that benefit disproportionately from the convenience of online autoship and bundle models. Within this broad segment, hair care is experiencing a particularly pronounced upgrade cycle, as the "skinification" trend, the application of skin care science and active ingredients to scalp and hair formulations, generates new premium subcategories that carry higher average selling prices and encourage trading-up behaviour. L'Oréal Paris launched the Elvive Collagen Peptide + Lifter collection exclusively at Walmart online in May 2026 as a direct expression of this trend, extending clinically framed personalised hair care into the mass accessible channel.

Cosmetics and makeup products, with a projected CAGR of 8.78% over 2026-2031, represent the fastest-growing product type segment and the most dynamic area of competitive disruption. After a period of subdued demand, colour cosmetics are rebounding through social commerce. Facial cosmetics and lip and nail makeup are the subsets generating the highest virality metrics, as visually demonstrable products translate better into short-form video formats than nuanced personal care formulations. Men's grooming and sun care remain relatively under-penetrated within the online channel, pointing to a meaningful addressable whitespace as category awareness broadens among male consumers and sun protection transitions from seasonal to year-round use.

By Price: Mass Dominates Penetration as Premium Outpaces on Growth

Mass products maintained 66.87% of market value in 2025, reflecting the reality that online platforms have become the dominant replenishment channel for everyday personal care essentials, where price comparison tools and promotional density favour high-volume, price-elastic segments. Mass beauty's digital penetration advantage is reinforced by marketplace logistics. Amazon, Shopee, and Flipkart can now fulfil personal care orders in hours, removing the last convenience advantage that physical drug stores held over online channels for routine purchases. This mass channel growth is also being sustained by TikTok Shop's democratising effect, bringing mass-positioned brands into social commerce alongside premium players.

The premium segment's 10.34% CAGR forecast for 2026-2031, the fastest in the pricing dimension, signals that the online channel is overcoming the "touch and feel" barrier that historically constrained prestige beauty online. Estée Lauder's migration to Shopify, completed in Q1 2026, was explicitly designed to unify prestige DTC commerce with real-time consumer analytics, a capability investment that signals that premium brands now view their digital shelf as their highest-margin growth lever. The narrowing price gap between mass and premium in online discoverability metrics, where algorithmic recommendation surfaces both tiers equally, is likely to sustain the premium segment's outperformance through the forecast period.

By Category: Conventional Leads Share as Organic Transitions Toward Mainstream

The conventional category maintained 75.03% of market value in 2025, sustained by its embedded position across all major online and mass retail channels. The category's scale advantage is structural: established formulations benefit from supply chain optimisation, broad SKU availability, and the merchandising weight of large-brand promotional budgets that drive visibility on both marketplace search and social commerce platforms. Despite healthy headline growth in organic, Conventional products retain the loyalty of the substantial consumer cohort that prioritises performance, price, and accessibility over ingredient provenance.

The organic segment is projected to grow at 9.54% CAGR through 2026-2031, outpacing the overall market and reflecting the sustained structural shift driven by ingredient transparency demands, particularly among Millennial and Gen Z consumers. The segment's key distinction from prior growth cycles is that its growth is no longer driven by niche or specialty channels alone: online retail is forecast to register the highest growth rate across all distribution channels for organic personal care products, as DTC platforms enable brands to communicate sustainability credentials, sourcing transparency, and certifications directly to consumers at scale without the shelf-space constraints of physical retail.

By Distribution Channel: Third-Party Retailer Platform Leads Share as Company-Owned Platform Transitions Toward Mainstream

Third-Party Retailer Platforms accounted for 75.8% of the online beauty and personal care market in 2025, making them the dominant sales channel. Their leadership is driven by extensive product assortments, competitive pricing, consumer reviews, loyalty programs, and convenient delivery options that attract a broad customer base. Major marketplaces and beauty-focused e-commerce platforms also provide brands with immediate access to large audiences, making them the preferred purchasing destination for most online beauty shoppers.

Company-Owned Platforms are projected to be the fastest-growing channel, expanding at a CAGR of 8.44% during 2026–2031. Growth is being fueled by beauty brands' increasing focus on direct-to-consumer (D2C) strategies, which enable greater control over customer relationships, first-party consumer data, product launches, and brand experiences. Investments in personalized recommendations, subscription services, virtual try-on tools, and exclusive online offerings are encouraging consumers to purchase directly from brand-owned websites, supporting their accelerated growth trajectory.

Geography Analysis

Asia-Pacific holds 36.78% of the global online beauty and personal care market value in 2025 and is simultaneously the fastest-growing geography, with a 9.47% CAGR projected through 2026-2031. China alone captures significantly, the online skin care sales, with digital channels of the country's skin care market, powered by a livestreaming-dominant purchase model. Southeast Asia is an accelerating sub-region: Shopee's combined beauty GMV across Indonesia, Thailand, and Vietnam reached significant heights in the twelve months to March 2026, with TikTok Shop's share in Vietnam surging in a single year, the fastest social commerce penetration in the region. India's trajectory adds a further growth layer, with the country emerging as the next high-frequency mobile beauty commerce market as quick commerce infrastructure expands beyond grocery into beauty and personal care categories.

North America remains the second-largest regional bloc, with the United States dominant in online skin care sales alone, supported by marketplace maturity and a social commerce ecosystem increasingly centred on Amazon and TikTok Shop. US beauty e-commerce sales grew in 2024-2025, reflecting the structural reordering of how American consumers discover, evaluate, and replenish beauty products. Europe demonstrates solid momentum, with Germany and the United Kingdom as the primary digital beauty markets. In France, online beauty and personal care purchases were made by all online shoppers, and the adoption of generative AI for purchase guidance among French e-commerce shoppers grew year-on-year in 2025, pointing to the early contours of AI-mediated beauty commerce even in a market culturally inclined toward human advisory models.

South America, the Middle East, and Africa are the highest-velocity growth regions, albeit from smaller bases. Brazil's beauty e-commerce channel grew in 2025, and with the premium segment posting small growth in Q1 2026, outperforming the global average. Online cosmetics revenue in Brazil grew, driven by the rise of digitally native DTC brands and the shift of platform traffic to marketplaces such as Mercado Livre, Amazon Brasil, and Shopee. In the Middle East and Africa, cultural identity trends are reshaping product demand. In Saudi Arabia, quick delivery now captures more than 10% of online beauty GMV, with the two-hour delivery window functioning as a genuine distribution channel rather than a premium service feature.

Competitive Landscape

The online beauty and personal care products market is fragmented, with no single player holding a dominant share across the full spectrum of product types, price tiers, and geographies. The strategic pattern among large incumbents is a convergence on AI and data infrastructure investment: L'Oréal reported that e-commerce now accounts for 30% of group revenue and has deployed agentic AI to manage product listings, pricing consistency, and content quality across global digital storefronts, with a 60% infrastructure overhaul targeted for completion by end of 2026; Unilever's AI-enabled B2C digital commerce platform processes 75,000 orders daily across 500,000 retail connections and achieved 25% e-commerce growth in the US in FY 2025, while Estée Lauder accelerated its "Beauty Reimagined" recovery plan by partnering with both Shopify and Accenture in a simultaneous DTC infrastructure and AI deployment investment that has few precedents in prestige beauty.

Among smaller challengers, the acquisition of rhode by e.l.f. Beauty for USD 1 Bn in May 2025 represents the clearest strategic signal that creator-economy brands with high social commerce traction are being absorbed into mid-tier beauty portfolios at a premium, validating the hypothesis that organic digital reach, not distribution breadth, is now the primary asset being acquired. White space in the competitive landscape is most visible in three areas: AI-personalised formulation at accessible price points, same-day delivery infrastructure in emerging e-commerce markets, and the intersection of clinical efficacy with certified sustainability. Coty's strategic pivot under its "Coty.Curated." framework, which concentrates investment behind core prestige fragrance franchises and selected mass colour cosmetics while exiting peripheral SKUs, illustrates a broader de-complexification trend among mid-tier incumbents who are reducing breadth in favour of digital-channel dominance in fewer, higher-margin categories.

A notable and underappreciated dynamic is that fast-growing K-beauty independent brands, many competing with zero paid-sponsorship strategies via organic creator networks, are capturing market share in the US and European prestige skincare segments at the expense of established Western conglomerates, as evidenced by Amorepacific's TikTok Shop listings for COSRX, Laneige, and Innisfree in global markets. Compliance factors under the EU Cosmetics Regulation and MoCRA in the US are becoming a competitive differentiator for brands that invest in proactive registration and ingredient safety documentation, as these frameworks tighten third-party marketplace vetting requirements and raise the cost of entry for sub-scale or counterfeit-adjacent sellers.

Online Beauty and Personal Care Industry Leaders

-

L'Oréal S.A.

-

Colgate-Palmolive Company

-

Coty Inc.

-

Revlon, Inc.

-

Chanel S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: AS Watson Group and L'Oréal Paris unveiled the first-ever exclusively co-created beauty product, the Infallible Setting Mist Cherry Edition, designed for Gen Z consumers and slated for rollout across 14+ global markets, setting a new precedent for retailer-brand co-innovation in beauty commerce

- June 2026: The Body Shop launched on Uber Eats across the UK, enabling on-demand delivery of beauty products in minutes. The partnership extends Uber Eats' rapid expansion into beauty retail, following its earlier deals with Ulta Beauty and Boots

- May 2026: Ulta Beauty, Inc. added 1,500+ stores to the Uber Eats marketplace for nationwide same-day delivery of 600+ brands, signaling that omnichannel beauty retail is increasingly defined by rapid fulfilment partnerships rather than owned logistics infrastructure

Global Online Beauty and Personal Care Market Report Scope

Beauty and personal care products include a wide range of skincare products, hair care products, bath and shower products, oral care products, color cosmetics, and deodorants and perfumes that both men and women use to maintain their hygiene and enhance their facial and body appearance. The online beauty and personal care market report is segmented by product type (personal care products, cosmetics/makeup products), price (premium and mass), category (organic and conventional), distribution channel (third-party retailer platform and company-owned platform), and geography (North America, Europe, and others). The market forecasts are provided in terms of value (USD).

| Personal Care Products | Hair Care Products | Shampoo |

| Conditioners | ||

| Hair Colorants | ||

| Hair Styling Products | ||

| Other Hair Care Products | ||

| Skin Care Products | Facial Care Products | |

| Body Care Products | ||

| Lip Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Bath Salts | ||

| Other Bath and Shower Products | ||

| Oral Care | Toothbrushes and Replacements | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Other Oral Care Products | ||

| Men’s Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Sun Care Products | ||

| Perfumes and Fragrances | ||

| Cosmetics/Makeup Products | Facial Cosmetics | |

| Eye Cosmetic Products | ||

| Lip and Nail Makeup Products | ||

| Premium |

| Mass |

| Organic |

| Conventional |

| Third-Party Retailer Platform |

| Company-Owned Platform |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Personal Care Products | Hair Care Products | Shampoo |

| Conditioners | |||

| Hair Colorants | |||

| Hair Styling Products | |||

| Other Hair Care Products | |||

| Skin Care Products | Facial Care Products | ||

| Body Care Products | |||

| Lip Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Bath Salts | |||

| Other Bath and Shower Products | |||

| Oral Care | Toothbrushes and Replacements | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Other Oral Care Products | |||

| Men’s Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Sun Care Products | |||

| Perfumes and Fragrances | |||

| Cosmetics/Makeup Products | Facial Cosmetics | ||

| Eye Cosmetic Products | |||

| Lip and Nail Makeup Products | |||

| Price | Premium | ||

| Mass | |||

| Category | Organic | ||

| Conventional | |||

| By Distribution Channel | Third-Party Retailer Platform | ||

| Company-Owned Platform | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the projected value of the online beauty and personal care products market by 2031?

The online beauty and personal care products market is forecast to reach USD 162.90 Bn by 2031, rising from USD 110.41 Bn in 2026 at an 8.09% CAGR during 2026-2031.

Which product type leads online beauty and personal care sales?

Personal Care Products led with 83.4% of value in 2025 because refill-led categories such as hair care, skin care, oral care, and bath products fit digital repeat purchasing very well.

Which segment is growing fastest in this space?

Cosmetics and Makeup Products is the fastest-growing product type at 8.8% CAGR through 2031, while Premium is the fastest-growing price tier at 10.3% CAGR.

Which region is strongest for digital beauty growth?

Asia-Pacific is both the largest and fastest-growing region, with 36.78% share in 2025 and a projected 9.5% CAGR through 2031.

Page last updated on: