Germany Beauty And Personal Care Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

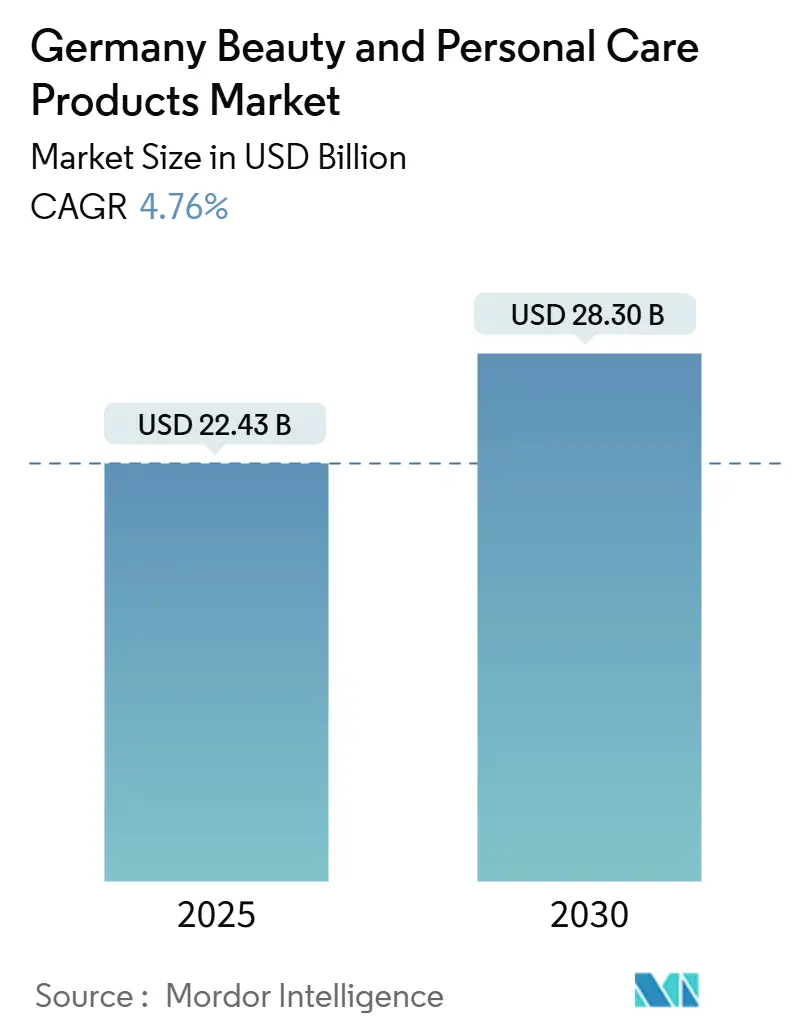

| Market Size (2025) | USD 22.43 Billion |

| Market Size (2030) | USD 28.30 Billion |

| Growth Rate (2025 - 2030) | 4.76% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The Germany Beauty And Personal Care Products Market size is estimated at USD 22.43 billion in 2025, and is expected to reach USD 28.30 billion by 2030, at a CAGR of 4.76% during the forecast period (2025-2030). Rising disposable incomes and increased focus on personal grooming have enabled consumers to invest more in appearance-enhancing products. The market growth is supported by the increasing number of working women and the impact of social media and beauty influencers, driving the adoption of premium and innovative beauty products. The aging population, particularly consumers aged 65 and above, has increased the demand for anti-aging, skin health, and specialized haircare products that address concerns like wrinkles, elasticity, and hair thinning. Growing awareness of skin health issues caused by pollution, stress, and climate change has boosted the demand for skincare products containing active ingredients, along with solutions for sensitive skin, acne, and other dermatological conditions. The growth of e-commerce platforms has improved product accessibility, while specialty stores continue to provide expert guidance and personalized product selections.

Key Report Takeaways

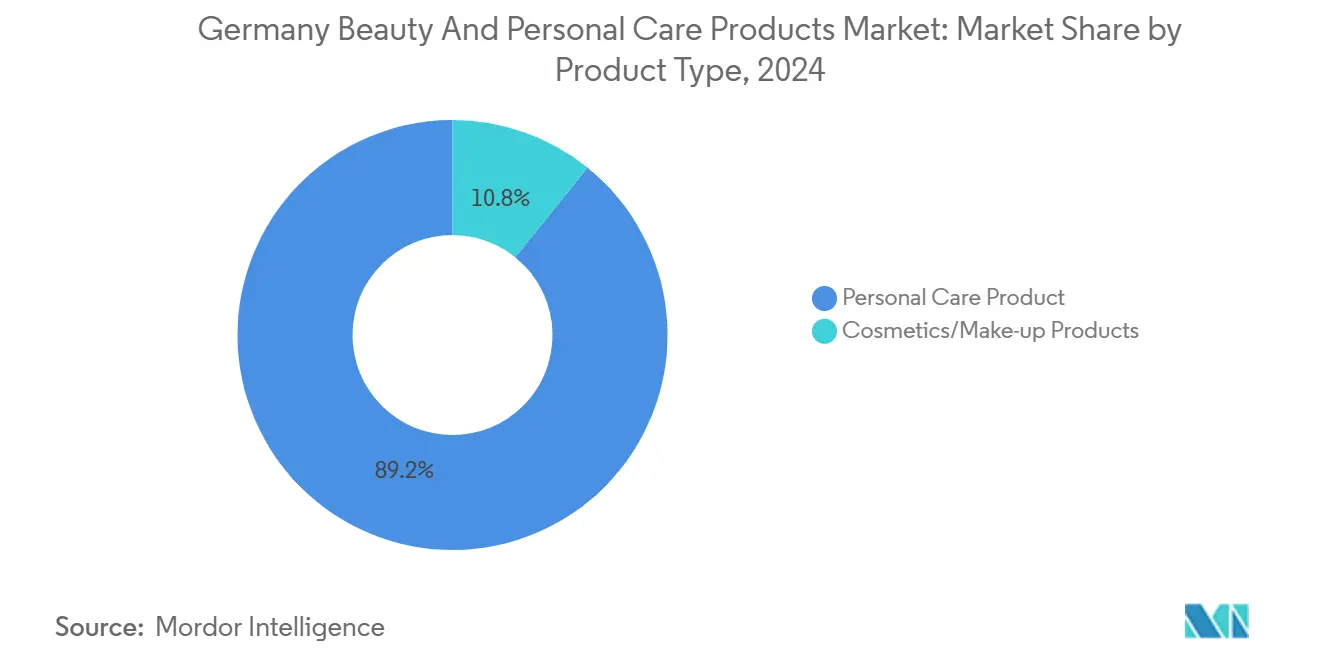

- By product type, personal care products led with an 88.19% Germany beauty personal care market share in 2024 and are projected to grow at a 4.61% CAGR through 2030.

- By category, mass products held 70.82% of the German beauty and personal care market in 2024, whereas the premium segment is forecast to expand at a 5.55% CAGR to 2030.

- By ingredient type, conventional/synthetic formulations dominated 67.43% of the German beauty and personal care market size in 2024, while natural and organic products are projected to register a 6.13% CAGR.

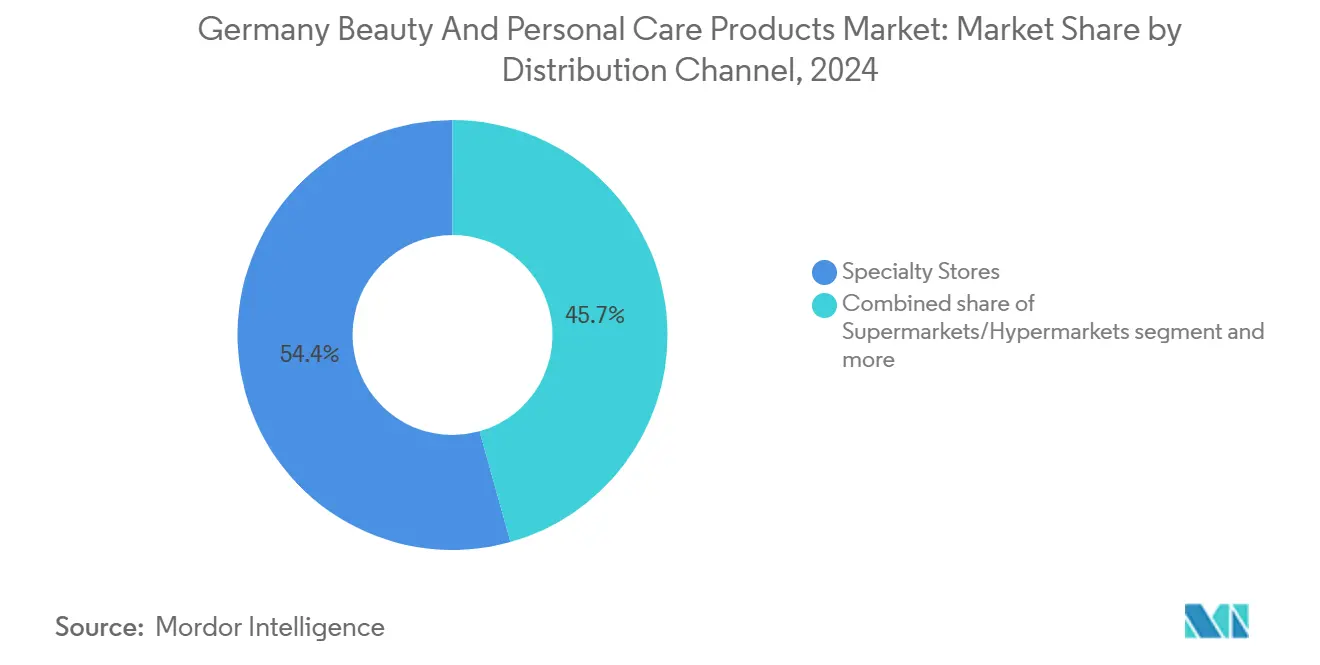

- By distribution channel, specialty stores accounted for 27.40% of the German beauty and personal care market in 2024, whereas online retail is projected to post a 6.41% CAGR through 2030.

Germany Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and organic beauty products | +1.2% | Germany, with spillover to European Union markets | Medium term (2-4 years) |

| Increasing concerns related to hair fall and scalp care product | +0.8% | Germany, particularly urban centers | Short term (≤ 2 years) |

| Aging population in Germany seeking anti-aging solutions | +0.9% | Germany, concentrated in affluent regions | Long term (≥ 4 years) |

| Consumer awareness of vegan and cruelty-free beauty products | +0.6% | Germany, with influence across DACH region | Medium term (2-4 years) |

| Rising disposable incomes leading to increased spending on premium beauty products | +0.7% | Germany, focus on metropolitan areas | Short term (≤ 2 years) |

| Innovations in product formulations driving the market growth | +1.0% | Germany, with global technology transfer | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and organic beauty products

The rising demand for natural and organic beauty products is a defining trend in Germany's beauty and personal care market, driven by a combination of environmental awareness, health consciousness, and shifting consumer values. German consumers exhibit a strong inclination toward products featuring clean ingredients, eco-friendly packaging solutions, and ethically sourced materials. According to the Center for the Promotion of Imports (CBI), 70% of German consumers incorporated sustainability considerations in their cosmetics and personal care product purchases in 2023[1]Source: Center for the Promotion of Imports (CBI), "What is the demand for natural ingredients for cosmetics on the European market?", www.cbi.eu. This consumer behavior is particularly evident among millennials and Gen Z demographics, who demonstrate strict preferences for products devoid of parabens, sulfates, and synthetic fragrances, while supporting brands that maintain supply chain transparency and cruelty-free certifications. Germany's historical foundation in natural remedies and herbal-based wellness practices, including naturopathy, establishes a robust market environment for natural beauty products. This convergence of consumer preferences and cultural heritage indicates sustained growth potential for natural and organic beauty products in the German market.

Increasing concerns related to hair fall and scalp care product

Hair loss and scalp care concerns are significantly influencing the German beauty and personal care products market. This trend is driven by demographic shifts, lifestyle changes, and environmental factors, along with the increasing prevalence of chronic health conditions like diabetes, which are associated with higher alopecia risk. Environmental factors, including pollution and nutritional deficiencies, are further contributing to the demand for effective hair and scalp care solutions. German consumers are seeking scientifically proven products and treatments, including those containing minoxidil or finasteride, as well as specialized therapies and customized regimens for prevention and restoration. The psychological impact of hair loss, particularly its effect on self-confidence, has strengthened the demand for both therapeutic and cosmetic solutions. As a result, the German market is experiencing substantial growth in advanced hair care formulations and specialized scalp treatments to address these increasing consumer concerns.

Germany's demographic transformation creates sustained demand for anti-aging

Germany's demographic transformation is driving growth in the beauty and personal care products market, particularly in the anti-aging segment. According to the Federal Statistical Office, in 2023, 18.89 million people in Germany were aged 65 years and older [2]Source: Federal Statistical Office, "Population in Germany", www.destatis.de. This aging population segment demonstrates increased health and appearance consciousness, seeking products that address visible signs of aging such as wrinkles, sagging skin, dryness, and age spots. German consumers aged 65 and above are more active and digitally connected compared to previous generations, showing greater willingness to invest in personal care products. This has resulted in increased demand for anti-aging skincare products, including retinol creams, collagen boosters, hyaluronic acid serums, and firming treatments with clinical validation. Premium and dermocosmetic brands have gained market share within this consumer segment, as older consumers demonstrate brand loyalty toward products with proven efficacy. The continued growth of Germany's aging population indicates sustained demand for anti-aging solutions in the beauty and personal care market.

Consumer awareness of vegan and cruelty-free beauty products

Consumer awareness and demand for vegan and cruelty-free beauty products in Germany have increased significantly, driven by ethical, environmental, and health considerations. German consumers prioritize products that avoid animal-derived ingredients and animal testing, reflecting a broader commitment to sustainability and ethical consumption. Germany's regulatory framework enforces strict bans on animal testing and requires clear labeling, ensuring consumer confidence in vegan and cruelty-free claims. German beauty brands continue to expand their eco-certified, cruelty-free, and vegan product lines. The market development is particularly evident at industry events such as Vivaness 2024, where companies like Dak Matter introduced specialized in organic scalp care products for conditions including psoriasis and seborrheic eczema. This trend demonstrates the German beauty and personal care market's continued evolution toward sustainable and ethical beauty solutions, supported by increasing consumer awareness and regulatory compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU microplastics ban inducing costly reformulations | -0.8% | Germany, with EU-wide regulatory alignment | Short term (≤ 2 years) |

| Counterfeit luxury fragrance imports via cross-border E-commerce | -0.5% | Germany, particularly premium segment | Medium term (2-4 years) |

| Supply chain disruptions impacting raw material costs and product availability | -0.6% | Germany, with global supply chain dependencies | Short term (≤ 2 years) |

| Intense price competition reduces profit margins | -0.4% | Germany, concentrated in mass market segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU microplastics ban inducing costly reformulations

The implementation of the European Union's microplastics ban in October 2023 constitutes a substantial market restraint for Germany's beauty and personal care products industry. This regulatory measure explicitly prohibits the incorporation of intentionally added microplastics in various consumer products, including exfoliating scrubs, shower gels, toothpastes, and color cosmetics, aligning with the European Union's comprehensive plastic pollution reduction strategy. Despite resonating with the environmental consciousness of German consumers, this regulation necessitates extensive product reformulation initiatives across the industry. The ban specifically impacts formulations containing polyethylene beads, which traditionally served essential functions in texture enhancement, color stability, and controlled-release mechanisms. Manufacturing entities must now allocate substantial resources toward research and development for alternative natural and biodegradable ingredients, while simultaneously managing prolonged development cycles encompassing reformulation, safety testing, and regulatory re-certification procedures. These requirements significantly impact operational expenditure and extend product launch timelines, thereby constraining market growth.

Counterfeit luxury fragrance imports via cross-border e-commerce

The rise of cross-border e-commerce platforms has increased the distribution of counterfeit luxury fragrances in Germany, making it one of the most impacted markets. Online marketplaces present enforcement challenges, as counterfeit products typically originate from regions with weak intellectual property protection and enter Germany through intricate distribution networks. Premium fragrance brands are particularly susceptible to counterfeiting due to their strong brand recognition and high price points. This illicit trade reduces legitimate retailers' pricing power and diminishes consumer confidence in online channels, especially affecting specialty stores that depend on authentic product guarantees. German authorities face difficulties in monitoring and enforcing regulations across multiple online platforms, while consumers risk purchasing counterfeit products that do not meet safety standards. The problem becomes more pronounced during peak shopping seasons and is exacerbated by social media marketing campaigns that imitate legitimate brand communications, creating persistent brand protection issues for premium fragrance manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominance Drives Innovation

Personal care products dominate with an 88.19% market share in 2024, and the segment is projected to grow at a steady CAGR of 4.61% through 2030, reflecting both high consumer penetration and sustained demand. A major driving force behind this dominance is the deep-rooted cultural emphasis on daily hygiene, grooming, and skin health across all age groups. According to IfD Allensbach, in 2024, around 17.2 million people in the German-speaking population aged 14 and over expressed particular interest in skin and body care, underscoring the widespread consumer engagement in this category. This enthusiasm is further supported by growing demand for anti-aging and sensitive skin solutions, and a heightened awareness of personal wellness. Moreover, the rise in natural and dermatologically tested personal care items continues to drive market growth.

The cosmetics/make-up segment represents a smaller portion of the market but benefits from specific high-growth drivers. This segment is influenced by social media trends, influencer marketing, and product innovation, particularly in areas like long-wear foundations, vegan makeup, and skin-caring color cosmetics. Although makeup adoption is more selective and occasion-driven in Germany compared to some other European countries, younger consumers are driving renewed interest in cosmetics that blend aesthetics with skincare benefits. The increasing demand for inclusive shade ranges, cruelty-free formulations, and refillable packaging has enabled brands to attract ethically and socially conscious consumers. While cosmetics remain a niche compared to personal care in Germany's overall market share, they are positioned to gain traction through digital consumer engagement and premiumization strategies.

By Category: Premium Acceleration Reshapes Value Dynamics

In 2024, mass-market products command a dominant 70.82% share of Germany's beauty and personal care sector. This stronghold is attributed to their affordability, widespread accessibility, and broad appeal among consumers. German shoppers emphasize essential care items, from skincare and oral hygiene to haircare, predominantly sourced from retail channels that account for nearly half of the market's sales. The mass segment thrives on frequent purchases, bolstered by both established local and international brands. These brands, with their value-centric offerings, resonate deeply with price-sensitive consumers and families. Additionally, the segment benefits from economies of scale, enabling competitive pricing and consistent availability across various distribution channels. Moreover, as consumer preferences shift, mass brands have adeptly integrated natural and organic formulations into their standard product lines, ensuring their continued relevance. This adaptation aligns with the growing consumer demand for sustainable and health-conscious products, further solidifying the segment's position in the market.

Meanwhile, the premium segment is on an upward trajectory, boasting a 5.55% CAGR, outpacing the overall market growth. This surge is fueled by rising disposable incomes, an escalating interest in self-care and wellness, and the influential role of social media in spotlighting premium beauty products. German consumers in the premium bracket are on the lookout for cutting-edge formulations, tailored skincare regimens, and products that marry efficacy with an enriched user experience. To cater to these discerning tastes, premium brands are harnessing technological innovations, from AI-driven skin analyses to virtual product trials. These advancements not only enhance personalization but also improve consumer engagement and satisfaction. Furthermore, premium brands are attuned to the growing demand for cruelty-free and eco-friendly offerings, often incorporating sustainable packaging and ethically sourced ingredients to align with the values of environmentally conscious consumers. This strategic focus on innovation and sustainability positions the premium segment as a key driver of growth in the beauty and personal care market.

By Ingredient Type: Natural Transformation Accelerates

In 2024, conventional or synthetic formulations command a dominant 67.43% share of the German beauty and personal care products market. Their affordability, proven efficacy, and widespread availability fuel this dominance. These products, trusted by consumers for their consistent performance and swift results, are the go-to choice for daily hygiene, skincare, and grooming. Supermarkets, drugstores, and pharmacies ensure these products are easily accessible, catering to a broad consumer base. Moreover, ongoing research and development empower manufacturers to effectively tackle diverse skin and hair concerns, enabling them to introduce innovative solutions that meet evolving consumer demands.

Meanwhile, the natural and organic segment is on the rise, boasting a 6.13% CAGR. This growth is largely attributed to heightened consumer awareness surrounding health, environmental, and ethical issues. Many German consumers are turning away from synthetic chemicals, wary of potential skin irritations and allergies. Instead, they gravitate towards products featuring plant-based ingredients and clean-label certifications, which vouch for safety and transparency. Notably, Germany stands as Europe's largest importer of essential oils. In 2023, data from the Center for the Promotion of Imports (CBI) highlighted that 49% of these oils were sourced from developing countries. This strategic positioning bolsters manufacturers' supply chain capabilities, allowing them to procure natural ingredients efficiently. As a result, manufacturers can offer a diverse array of natural product options, catering to the growing demand for sustainable and ethically produced beauty and personal care products.

By Distribution Channel: Digital Disruption Transforms Retail

In 2024, specialty retailers commanded a notable 27.4% share of Germany's beauty and personal care products market. These retailers, often found in metropolitan hubs and commercial zones, have carved a niche by curating premium and specialized brands. They cater to discerning consumers seeking products that align with specific values, such as natural, organic, vegan, and cruelty-free formulations. Beyond just selling, these establishments prioritize professional consultations and foster sophisticated retail environments, cultivating lasting customer relationships. Their emphasis on personalized service and consumer education distinctly sets them apart from mass-market distribution channels. Additionally, these retailers often host in-store events, workshops, and product demonstrations, further enhancing customer engagement and loyalty.

Online retail stores in Germany's beauty market are on an upward trajectory, eyeing a robust CAGR of 6.41%. This growth is a direct response to the rising consumer appetite for both accessibility and a wider product range. Digital platforms are not just about sales; they're enhancing market reach with competitive pricing and tech-savvy features. Innovations like virtual product sampling, tailored algorithmic recommendations, and detailed product specs are becoming the norm. Furthermore, the convenience of doorstep delivery and flexible return policies has significantly contributed to the popularity of online channels. Meanwhile, traditional outlets like supermarkets and hypermarkets continue to play a pivotal role, leveraging their vast distribution networks to cater to a broad spectrum of consumers in both urban and suburban locales. These formats also benefit from offering a mix of affordable and mid-range products, appealing to price-sensitive customers while maintaining a strong presence in the market.

Geography Analysis

Germany stands out as the largest beauty and personal care products market in Europe, accounting for a significant share of both the continent's population and economic output. According to Germany Trade and Invest, as of 2023, Germany constitutes 25% of the EU-27's Gross Domestic Product (GDP) and is home to 19% of the total European Union population, underscoring its central economic and demographic role in the region[3]Source: Germany Trade and Invest (GTAI), "The German Market - Europe’s Economic Hub", www.gtai.de. This prominence is reflected in the beauty and personal care sector, where Germany leads Europe in market share.

Urban centers such as Berlin, Hamburg, and Munich are key growth engines, driven by affluent, trend-conscious consumers who are influenced by social media and digital marketing. These urban populations are early adopters of premium, innovative, and sustainable products, while rural and smaller towns tend to favor mass-market and essential personal care items. The widespread presence of health and beauty specialists and drugstores ensures strong market penetration across all regions, while e-commerce expansion is bridging the urban-rural divide.

Innovation leadership distinguishes the German market, with companies investing heavily in Research and Development and advanced manufacturing technologies to maintain competitive advantages. The regulatory environment supports innovation while ensuring consumer safety, with Germany's implementation of European Union microplastics restrictions driving industry transformation toward sustainable formulations. Western and southern Germany, with higher disposable incomes, show greater demand for premium and organic brands, while eastern states experience rising demand among younger, digitally savvy consumers. The market features a strong presence of both international giants and local champions.

Competitive Landscape

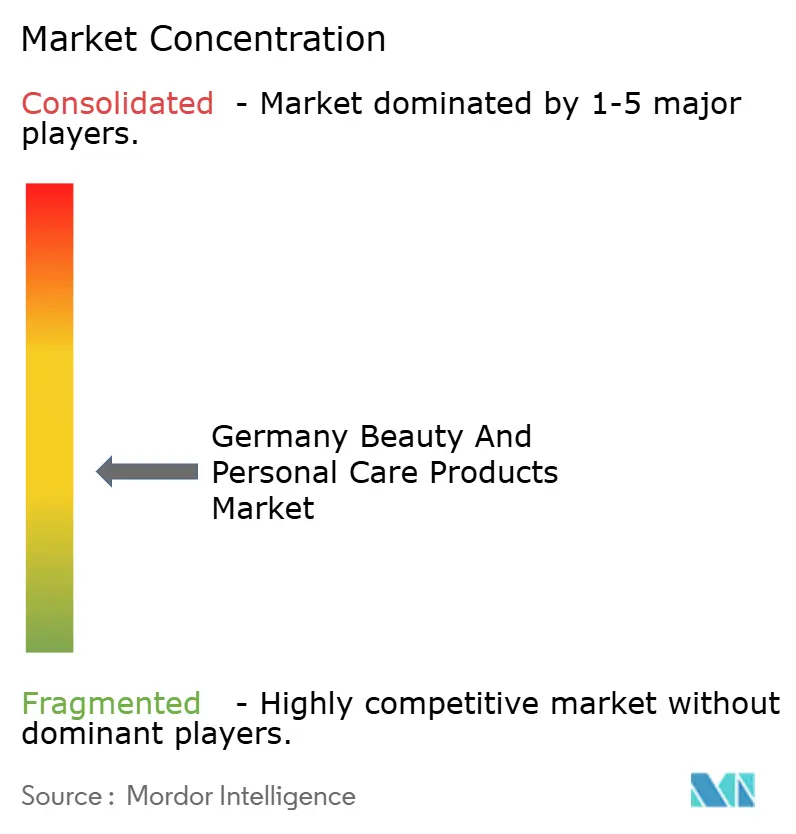

The German beauty and personal care market demonstrates a structured competitive environment characterized by moderate market concentration. Established multinational corporations and domestic manufacturers maintain significant market presence through extensive research capabilities and product innovation. Key market participants, including Beiersdorf AG, L'Oréal S.A., Henkel AG and Co. KGaA, The Procter and Gamble Company, and Unilever PLC, have established robust operational frameworks through their German manufacturing facilities and research centers.

The competitive differentiation in the market primarily stems from technological integration across the value chain. Market participants are implementing artificial intelligence systems for product personalization, conducting advanced ingredient research programs, and developing comprehensive digital engagement platforms. These technological implementations serve dual objectives of enhancing consumer retention metrics and optimizing operational parameters.

The market presents strategic opportunities in sustainable packaging development, personalized beauty technology integration, and specialized product formulations for diverse consumer demographics. New market entrants are establishing competitive positions through direct-to-consumer distribution channels and digital marketing strategies. The competitive landscape reflects systematic transformation toward environmental sustainability initiatives, digital infrastructure development, and scientific research validation. Successful market participants demonstrate effective resource allocation between innovation investments and operational optimization while maintaining regulatory compliance and addressing evolving consumer requirements.

Germany Beauty And Personal Care Products Industry Leaders

-

Beiersdorf AG

-

L'Oréal S.A.

-

Unilever PLC

-

Henkel AG and Co. KGaA

-

The Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TikTok Shop expanded into Germany as part of its European growth strategy. This expansion allows new brands to enter the platform and provides beauty brands with an entry point into the European market. Brands such as Benefit, Glow Hub, and others feature their products in the store.

- January 2025: e.l.f. Beauty launched its "e.l.f. von zehn" campaign in Germany, highlighting its affordable, high-performance products through a playful approach to beauty. The campaign featured products such as the Power Grip Primer and Glow Reviver Lip Oil.

- January 2025: Kao Corporation introduced its global skincare brand Curél in German pharmacies. This launch aligns with Kao's expansion strategy in the skincare market, emphasizing derma-cosmetics and skin protection products.

- September 2024: Beiersdorf introduced its first epigenetic serum under the Eucerin brand, incorporating the company's patented skin-specific age clock technology. The technology utilizes an algorithm based on epigenetic patterns to measure the skin's biological age.

Germany Beauty And Personal Care Products Market Report Scope

| Personal Care Products | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colorants | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Others | ||

| Men’s Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Make-up Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Make-up Products | ||

| Premium Products |

| Mass Products |

| Natural and Organic |

| Conventional/Synthetic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioner | |||

| Hair Colorants | |||

| Hair Styling Products | |||

| Others | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Others | |||

| Oral Care | Toothbrush | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Others | |||

| Men’s Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Make-up Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Make-up Products | |||

| By Category | Premium Products | ||

| Mass Products | |||

| By Ingredient Type | Natural and Organic | ||

| Conventional/Synthetic | |||

| By Distribution Channel | Specialty Stores | ||

| Supermarkets/Hypermarkets | |||

| Online Retail Stores | |||

| Other Channels | |||

Key Questions Answered in the Report

What is the current value of the Germany beauty personal care market?

The Germany beauty personal care market size stands at USD 22.43 billion in 2025.

Which segment is growing the fastest in Germany’s beauty sector?

Premium products are projected to expand at a 5.55% CAGR between 2025 and 2030, outpacing all other segments.

How significant is natural and organic beauty demand in Germany?

Natural and organic formulations are expected to grow at a 6.13% CAGR, fueled by strong consumer sustainability preferences.

Which distribution channel is set to gain the most share?

Online retail is forecast to post a 6.41% CAGR as German shoppers increasingly value convenience and personalized digital experiences.

Page last updated on: