Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

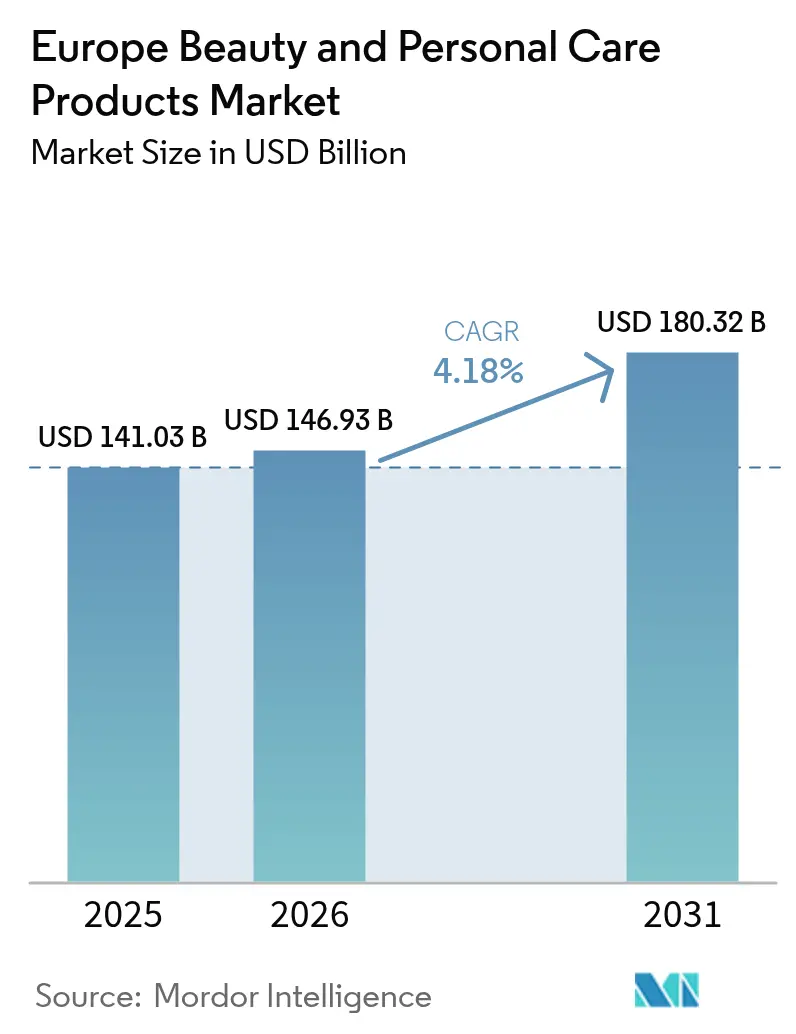

| Base Year Market Size (2025) | USD 141.03 Billion |

| Market Size (2026) | USD 146.93 Billion |

| Market Size (2031) | USD 180.32 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The Europe beauty and personal care products market size is expected to grow from USD 141.03 billion in 2025 to USD 146.93 billion in 2026 and is forecast to reach USD 180.32 billion by 2031 at 4.18% CAGR over 2026-2031. As online retail leverages data-driven personalization to boost margins, trends like premiumisation, natural-ingredient reformulations, and stringent sustainability laws are redefining value creation. Germany commands a substantial 15.83% share of the revenue pie, driven by its strong consumer base, robust infrastructure, and established market players. The United Kingdom also reflects its evolving market dynamics, increased focus on innovation, and adaptation to post-Brexit challenges. With a microplastics ban set to roll out by 2029, clean-label claims are gaining traction, steering brands towards vegetable-oil-based actives and promoting refillable packaging to meet consumer demand for sustainable and eco-friendly solutions. Annual losses of EUR 3 billion from counterfeits are significantly eroding consumer trust, prompting industry players to adopt advanced technologies like blockchain tagging and QR-based tracking[1]Source: European Union Intellectual Property Office,"Economic impact of counterfeiting in the clothing, cosmetics, and toy sectors in the EU", euipo.europa.eu. These measures aim to enhance supply chain transparency, ensure product authenticity, and rebuild consumer confidence in the market.

Key Report Takeaways

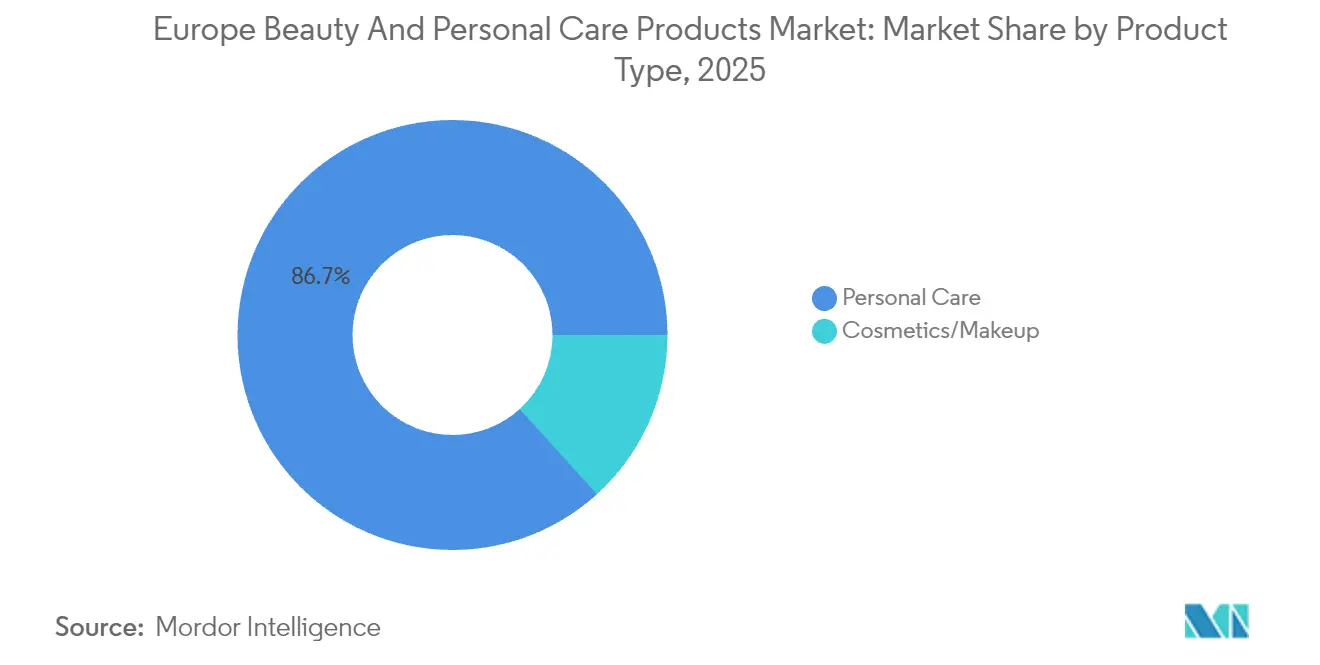

- By product type, personal care led the Europe beauty and personal care market with 86.72% share in 2025, whereas cosmetic products are set to post a 5.07% CAGR through 2031.

- By category, the mass segment captured 66.20% revenue in 2025, while premium products are projected to grow at a 5.03% CAGR between 2026-2031.

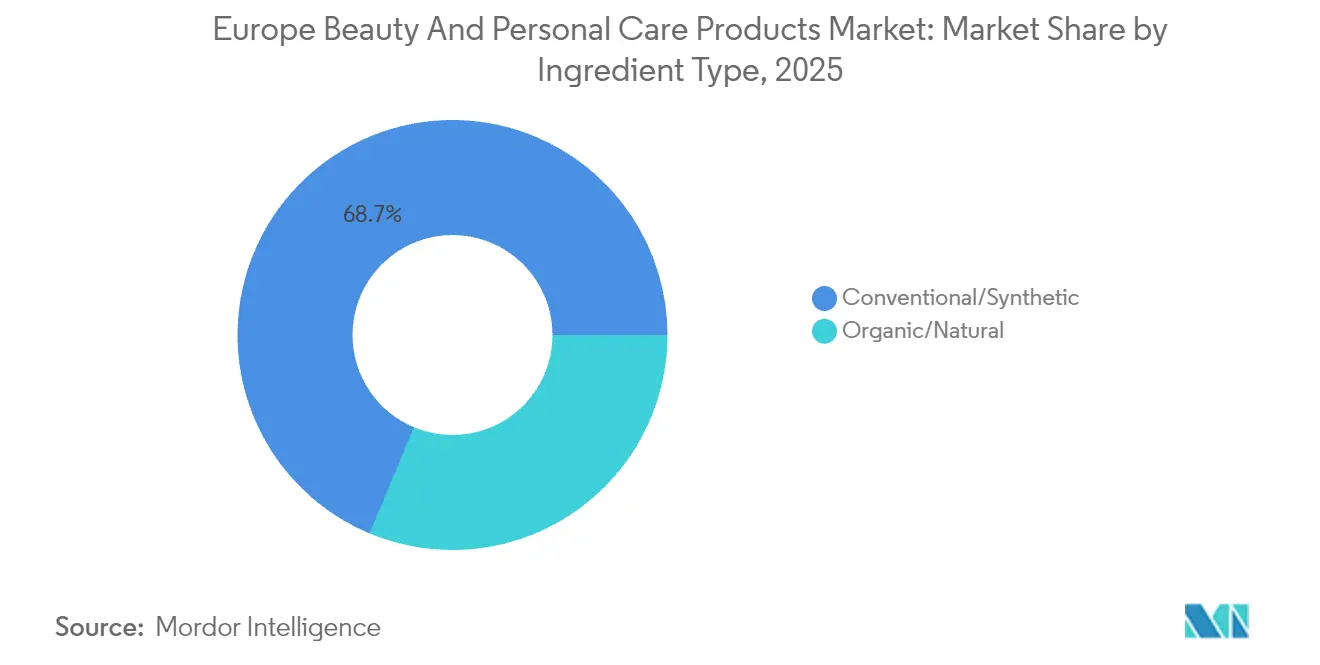

- By ingredient, conventional formulations retained 68.70% share in 2025 whereas natural and organic products are forecast to register a 5.74% CAGR to 2031.

- By distribution, pharmacies/drug stores accounted for 30.12% of 2025 sales, while online retail is on track for a 5.54% CAGR in the same horizon.

- By geography, Germany commanded 15.70% of the 2025 Europe beauty and personal care market share; the Poland represents the fastest-growing major market with a 6.93% CAGR expected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation outpacing mass-market growth | +1.2% | Western core; spreading East | Medium term (2-4 years) |

| Surge in online D2C and marketplaces | +0.8% | EU-wide; strongest Netherlands, Ireland, Denmark | Short term (≤2 years) |

| Preference for clean and microbiome formulas | +0.7% | Germany, France, Netherlands | Medium term (2-4 years) |

| Age-inclusive “skinification” of hair-care | +0.6% | Germany, United Kingdom, France | Long term (≥4 years) |

| AI-powered hyper-personalisation | +0.5% | United Kingdom, Germany, Netherlands | Medium term (2-4 years) |

| Oral-care awareness | +0.4% | Northern Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Premiumization outpacing mass-market growth

In Europe, premium beauty and personal care lines are outpacing the overall market growth nearly twofold. Consumers now view high-performance formulations as everyday essentials rather than mere indulgences, driven by a growing preference for products that deliver tangible results. Products with dermatological validation and wellness-oriented claims command a higher price, as they align with the increasing consumer focus on health and self-care. This trend is exemplified by Beiersdorf's record sales of EUR 9.9 billion in 2024, largely fueled by innovations in its Eucerin skincare line, which combines scientific research with advanced formulations. Major multinationals are shifting their focus and capital towards prestige portfolios to capitalize on this demand. A case in point is Unilever's acquisition of Dr. Squatch, coupled with its ambition to elevate the premium segment's contribution to the group's turnover to 50%. Furthermore, brand equity, bolstered by clinical data and unique delivery systems, remains robust even amidst the prevailing cost-of-living challenges, as consumers prioritize quality and efficacy over cost.

Surge in online D2C and marketplaces

In 2024, 77% of EU residents shopped online, with cosmetics accounting for 20% of those purchases[2]Source: Eurostat,"Online shopping in the EU keeps growing", ec.europa.eu. The Netherlands leads with a 94% penetration rate, highlighting the country's swift embrace of digital beauty trends driven by high internet penetration, advanced e-commerce infrastructure, and consumer preference for convenience. Direct-to-consumer (D2C) platforms empower brands to gather zero-party data, such as customer preferences, purchase behavior, and feedback, enabling them to adjust product assortments on the fly, launch targeted marketing campaigns, and maintain gross margins that were once surrendered to brick-and-mortar retailers. Additionally, AI-driven shade-matching and virtual try-on features not only minimize returns by helping customers make more accurate selections but also enhance the overall shopping experience. These tools build consumer confidence in online purchases, ultimately driving higher sales conversions, fostering brand loyalty, and positioning brands to better compete in an increasingly digital marketplace.

Preference for clean and microbiome-friendly formulations

Starting February 2025, new restrictions on nano forms of copper, silver, gold, and platinum are prompting a significant shift towards botanicals and bio-ferments as alternative solutions. These restrictions are driving innovation in ingredient sourcing, formulation strategies, and product development within the beauty industry. In 2024, Europe accounted for 48% of global imports of vegetable and essential oils for beauty applications, bolstering a strong raw-material ecosystem that supports this transition[3]Source: Centre for the Promotion of Imports from developing countries", What is the demand for natural ingredients for cosmetics on the European market?", www.cbi.eu. This robust supply chain enables manufacturers to explore diverse natural ingredients and create sustainable formulations. Brands are increasingly blending natural profiles with clinically validated efficacy to meet consumer demands for both safety and performance. Additionally, emerging probiotic actives are playing a pivotal role in bridging narratives of skin health and immunity, offering multifunctional benefits that align with evolving consumer preferences and the growing focus on holistic wellness.

Age-inclusive “skinification” of hair-care

As Europe's population ages, the focus is shifting from mere color maintenance to ensuring scalp barrier integrity and nourishing hair follicles. This demographic shift has driven demand for advanced hair care solutions that address both aesthetic and health-related concerns. L’Oréal's foray into bioprinted skin models underscores the evolving testing protocols that meld skin science with hair-care assertions, enabling more precise and effective product development. These bioprinted models allow for innovative testing methods, reducing reliance on traditional approaches and accelerating the development of targeted solutions. In Germany and the UK, premium scalp serums, now touting ingredients like niacinamide and ceramides, are beginning to rival the positioning of their facial serum counterparts. These products not only promise enhanced scalp health but also command a premium price, reflecting their perceived value, efficacy, and alignment with consumer preferences for high-quality, multifunctional formulations.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and grey-market channels | -0.6% | France, Italy, Romania most affected | Short term (≤ 2 years) |

| Retailer private-label price pressure | -0.5% | Western Europe supermarket chains | Medium term (2-4 years) |

| Fragmented eco-label regulations | -0.4% | EU-wide implementation challenges | Long term (≥ 4 years) |

| High manufacturing costs and raw material expenses | -0.3% | Manufacturing hubs: Germany, France, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit and grey-market channels

In 2023, EU customs confiscated 152 million counterfeit items, collectively valued at a staggering EUR 3.4 billion. Notably, beauty and personal care products ranked among the top five categories affected, highlighting the vulnerability of this market to counterfeit activities. France bore a significant brunt, witnessing an EUR 800 million dip in legitimate cosmetics turnover. This substantial loss has not only impacted the nation's economy but also eroded consumer confidence in e-commerce platforms, where product authentication processes remain inadequate and opaque. The prevalence of counterfeit goods in online marketplaces has made it increasingly difficult for consumers to distinguish genuine products from fake ones, further exacerbating the issue. Furthermore, premium stock-keeping units (SKUs) have become prime targets for counterfeiters due to their higher profit margins, jeopardizing brand equity, inflating warranty expenses, and forcing companies to allocate additional resources to combat counterfeiting activities.

Retailer private-label price pressure

Recent retail disclosures reveal that leading supermarket groups are expanding their own-label lines, often pricing them 30-40% lower than national brands. This shift is driven by the growing consumer demand for affordable yet quality alternatives, allowing supermarkets to strengthen their competitive positioning and capture greater market share. These own-label products often offer comparable quality to national brands, making them increasingly attractive to cost-conscious consumers. To justify their premium pricing, established players are turning to patented actives, enhanced packaging experiences, and loyalty program benefits, which aim to create a distinct value proposition and retain customer loyalty. Alternatively, some are shifting towards private-label manufacturing to safeguard their sales volume, diversify their revenue streams, and adapt to the evolving market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal-Care Stability Anchors Growth

In 2025, personal care dominated Europe's beauty and personal care landscape, accounting for 86.72% of total sales. This segment maintained a forward CAGR, demonstrating resilience as hygiene staples remain non-discretionary even during economic slowdowns. Within personal care, skin care emerged as the largest subcategory, valued at EUR 27.7 billion, fueled by rising demand for anti-aging solutions, treatments for hyperpigmentation, and products supporting barrier repair. Hair care followed closely, generating EUR 16.8 billion in revenue, supported by innovations such as scalp serums and sulfate-free cleansing bars. Oral care also benefited from a growing preventive-health mindset, further reinforcing personal care’s dominance. Mass-priced bath and shower products continued to secure steady baseline volumes, while sustainable packaging formats like refillable pouches and solid bars helped improve margins without sacrificing accessibility.

Within cosmetics, the segment recorded the fastest CAGR of 5.07%, driven by strong consumer demand for makeup and color cosmetics innovations. This growth reflects rising interest in premium formulations, multifunctional products, and inclusive shade ranges catering to diverse skin tones. Fragrance lines and color cosmetics benefited from trend-driven launches, social media influence, and increased digital engagement, further accelerating adoption. The momentum is also supported by targeted innovations in skincare-infused makeup and long-lasting formulations, creating opportunities for brands to capture value while meeting evolving consumer preferences.

By Category: Premium Momentum Reshapes Value Mix

In 2025, mass beauty and personal care products dominated the European market, accounting for 66.20% of total turnover. These offerings cater to a broad consumer base with accessible price points while maintaining strong quality standards, ensuring they remain staples in daily routines. Mass skin care, hair care, and bath and shower products continued to secure steady volumes, driven by demand for essential hygiene and grooming solutions. Brands are increasingly leveraging value packs, multi-use products, and sustainable packaging formats such as refillable pouches and solid bars to combine affordability with functionality.

Despite their already significant presence, premium products are set to be the market's fastest-growing segment, boasting a projected CAGR of 5.03% through 2031. This growth trajectory positions premium lines to account for half of all incremental industry revenue during this period, underscoring their pivotal role in market expansion. This surge is driven by consumers opting for performance-driven formulations and long-term benefits in essential skin care, even as they navigate cost-of-living challenges. While shoppers economize in certain beauty categories, they remain committed to high-efficacy premium skin-care items. Furthermore, luxury fragrance refill initiatives not only resonate with sustainability trends but also fortify brand loyalty, fostering an emotional bond that fuels growth. As mass-market segments wane either due to cautious spending or a shift to upgraded supermarket options, premium's innovation-led approach positions it for a swift ascent, outpacing all other market segments.

By Ingredient Type: Natural Adoption Accelerates

In 2025, conventional beauty and personal care formulations dominated the European market, securing a 68.70% share. These time-honored products, deeply woven into consumer routines, benefit from their widespread availability, competitive pricing, and consistent performance across categories. Even in the face of increasing regulatory scrutiny, such as the restrictions on cyclic silicones D5 and D6 and heightened oversight on microplastic content, conventional formats have maintained their lead, especially in high-performance sectors like color cosmetics. Synthetic pigments play a crucial role, ensuring stability, vibrancy, and longevity, which keeps them favored in performance-centric areas. Instead of complete overhauls, many mass and premium brands are opting for minor formulation adjustments, enabling compliance without compromising on texture or shelf life. This blend of market familiarity, proven effectiveness, and gradual adaptation solidifies the position of conventional formulas in the industry, even as regulations and consumer preferences evolve.

Natural and organic SKUs are emerging as the fastest-growing segment, with projections indicating a 5.74% CAGR in Europe's beauty and personal care market. This growth surge is largely attributed to regulatory shifts, especially the phaseouts of certain silicones and stricter microplastic regulations, which are hastening the move towards greener ingredients. There's a rising demand for plant-based actives like bakuchiol, squalane, and tremella mushroom, bolstered by advancements in green-chemistry processing that ensure a scalable and high-quality supply. Skincare leads this trend, especially as leave-on products face heightened ingredient scrutiny and consumers increasingly seek safer, sustainable options. Regulatory initiatives, such as Directive 2024/825, which mandates verifiable eco claims, have positioned certification bodies like COSMOS and NATRUE as pivotal players in ensuring transparency and trust. With consumer priorities shifting towards environmental responsibility and clean-label principles, natural and organic products are set to outpace the broader category growth.

By Distribution Channel: Online Takes Structural Lead

In 2025, pharmacies and drug stores solidified their status as Europe's premier distribution channel for beauty and personal care, clinching a 30.12% market share. Their stronghold is deeply rooted in consumer trust, especially in dermatology-sensitive categories, where recommendations from pharmacists hold considerable sway. These establishments shine in high-credibility areas like dermocosmetics, therapeutic skincare, and other health-related beauty products. Even with the surge of e-commerce, pharmacies have carved out a niche, offering in-person consultations, tailored product selections, and expert advice, a level of service that online platforms struggle to match. Additionally, their role as a convenient one-stop destination for both prescriptions and over-the-counter beauty items boosts shopper frequency. As they adapt to the digital age with services like e-prescriptions and click-and-collect, pharmacies are steadfastly banking on their clinical credibility to uphold their leading position.

Online retail is poised to emerge as the quickest-growing channel for beauty and personal care, forecasting a robust 5.54% CAGR through 2031. This momentum is fueled by innovations like virtual consultations, mirroring in-store assistance, and same-day delivery, which bridge the convenience divide with brick-and-mortar outlets. Streamlined cross-border logistics have simplified access to international brands, propelling cosmetics to the forefront of e-commerce. Countries like The Netherlands and Ireland showcase a mature digital beauty landscape, while burgeoning online markets such as Romania and Hungary present untapped growth opportunities. The rise of social commerce, highlighted by livestreaming events, influencer-driven product launches, and direct-to-cart shopping during interactive sessions, is further propelling this trend. Moreover, subscription-based replenishment models are cementing customer loyalty, ensuring online retail's rapid ascent is matched by sustained revenue streams.

Geography Analysis

Germany, with a 15.70% share of Europe's beauty and personal care market in 2025, enjoys advantages like high per-capita spending, a leading stance on chemical safety regulations, and a consumer base that prioritizes proven efficacy. Domestic players, notably Beiersdorf, are channeling research and development into niches like sensitive skin and hyperpigmentation, bolstering premium sales. The country's focus on innovation and sustainability further strengthens its position in the market, as consumers increasingly demand eco-friendly and scientifically backed products.

Poland is emerging as the fastest-growing market in Europe, with a projected CAGR of 6.93% through 2031. Rapid increases in disposable incomes, widespread e-commerce adoption, and heightened consumer awareness are fueling demand for both mass and mass-premium products. Local consumers are increasingly seeking quality solutions at accessible price points, providing opportunities for brands to capture market share through tailored offerings and digital-first strategies.

France, Italy, and Spain continue to shape the landscape through category specialization: France leads in luxury fragrances, Italy leverages its artisan heritage in color cosmetics, and Spain’s sunny climate supports strong sales of UV-protection products. Eastern Europe, led by Poland, represents a strategic growth frontier, with evolving retail infrastructure and online channels amplifying market potential. The combination of rising consumer sophistication and improved access to diverse products underscores the region’s attractiveness for both established and emerging beauty and personal care brands.

Competitive Landscape

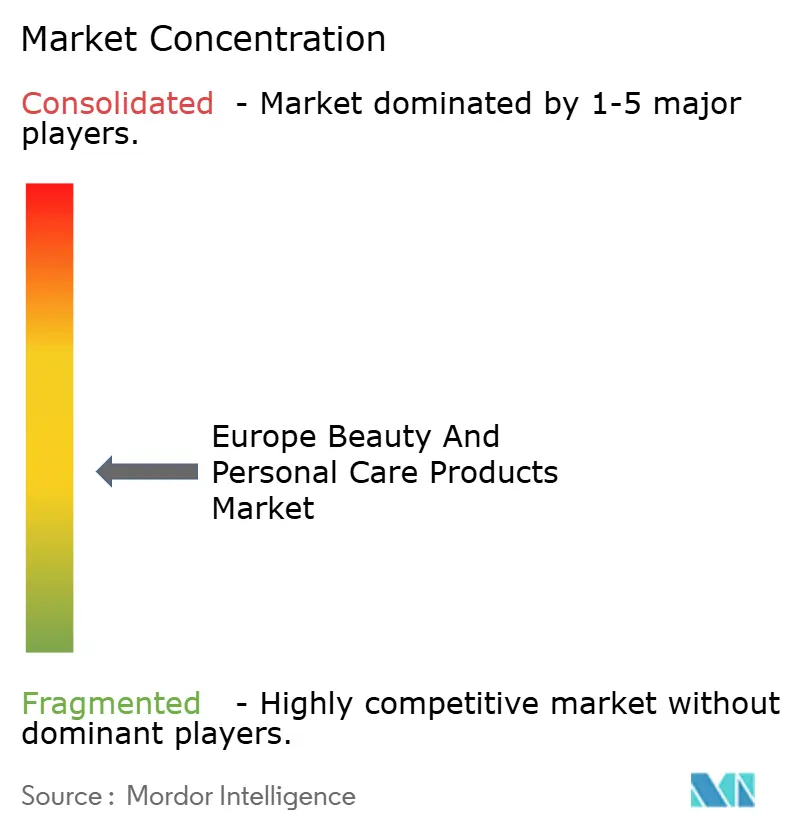

The European beauty market showcases a moderate concentration, highlighting a competitive landscape where established multinationals vie with emerging niche players and aggressive private label expansions. L’Oréal, leveraging end-to-end integration and AI-driven demand sensing, boasts a commanding 19.8% operating margin. Unilever's 4.1% growth in its Q1 2025 Beauty and Wellbeing segment underscores the success of its premium strategy. Meanwhile, Beiersdorf, with its skin-science reputation, secures prime shelf space, even as pharmacy chains tighten their assortments.

There's a burgeoning demand for age-inclusive beauty products and microbiome-friendly formulations, presenting white-space opportunities. Disruptors are capitalizing on these gaps, utilizing direct-to-consumer models to sidestep traditional retail channels. Technology adoption stands out as a pivotal competitive edge. L'Oréal's ventures into bioprinted skin development and AI-generated marketing content via CREAITECH underscore how strategic innovation investments can carve out market advantages.

Incumbents are differentiating themselves through tech investments: L’Oréal's trials with bioprinted skin aim for cruelty-free efficacy validation, while Unilever delves into blockchain for ingredient traceability. The surge of private-labels in grocery channels is pushing prices down, nudging mass-segment leaders to either upscale their offerings or provide ready-to-use formulations to retailers. With the enforcement of microplastics bans and restrictions on nano-metals, consolidation in the industry seems imminent, favoring firms equipped with robust formulation pipelines and adept regulatory affairs teams.

Europe Beauty And Personal Care Products Industry Leaders

-

L'Oréal S.A.

-

Procter & Gamble Co

-

Unilever PLC

-

Beiersdorf AG

-

Estée Lauder Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nivea unveiled its new epigenetic serum at budget-friendly prices. The serum boasts the German multinational's proprietary Epicelline technology, which is specifically designed to reverse visible signs of skin aging and enhance skin longevity by targeting the skin's cellular mechanisms. This launch highlights Nivea's commitment to innovation in the skincare market.

- January 2025: Lidl Espana debuted a line of professional hair care products. These products, crafted in partnership with Secret Code, are formulated to meet the needs of diverse hair types and provide salon-quality results. The range is set to be retailed across 700 stores in Spain, reflecting Lidl Espana's strategic focus on expanding its presence in the personal care market.

- May 2024: French start-up Mono Skincare has reintroduced its line of water-soluble, natural products. The revamped face care lineup features a cleanser, makeup remover, scrub, toner, night serum, and moisturizing lotion. These products are carefully formulated using a specialized protocol aimed at enhancing skin hydration and reducing signs of aging, catering to consumers seeking sustainable and effective skincare solutions.

- April 2024: In collaboration with the renowned stylist Rossano Ferretti, dubbed the World’s Hair Maestro, Kiko Milano unveiled a comprehensive haircare line. This range includes essential products such as shampoo, conditioner, mask, serum, and hair spray, designed to cater to diverse haircare needs while reflecting the expertise and innovation of both the brand and the stylist.

Europe Beauty And Personal Care Products Market Report Scope

The beauty and personal care market is defined here as consumer goods for cosmetics and body care. The scope includes beauty cosmetics for the face and lips, skincare products, fragrances, and personal care products, such as haircare, deodorants, and shaving products.

Europe's beauty and personal care market is segmented by product type, distribution channel, category, and geography. By product type, the market is segmented into personal care products and cosmetic/makeup products. The personal care products segment is further classified into haircare products, skincare products, bath and shower products, oral care products, perfumes and fragrances, and deodorants and antiperspirants. The cosmetics/makeup products segment is further segmented into facial makeup products, eye makeup products, and lip and nail makeup products. By distribution channel, the market is segmented into specialty stores, supermarkets/hypermarkets, convenience stores/grocery stores, pharmacies/drug stores, online retail channels, and other distribution channels. By category, the market studied is segmented into premium/luxury and mass products. The market is segmented by geography into Spain, United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Personal Care | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colorant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Others | ||

| Men's Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Makeup Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Makeup Products | ||

Category

| Premium Products |

| Mass Products |

Ingredient Type

| Natural and Organic |

| Conventional/Synthetic |

Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Other Channels |

By Geography

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

| By Product Type | Personal Care | Hair Care | Shampoo |

| Conditioner | |||

| Hair Colorant | |||

| Hair Styling Products | |||

| Others | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Others | |||

| Oral Care | Toothbrush | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Others | |||

| Men's Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Makeup Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Makeup Products | |||

| Category | Premium Products | ||

| Mass Products | |||

| Ingredient Type | Natural and Organic | ||

| Conventional/Synthetic | |||

| Distribution Channel | Supermarkets/Hypermarkets | ||

| Pharmacies/Drug Stores | |||

| Online Retail Stores | |||

| Other Channels | |||

| By Geography | Europe | Germany | |

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

Key Questions Answered in the Report

How large is the Europe beauty and personal care market in 2026?

It is valued at USD 146.93 billion, with a 4.18% CAGR projected to 2031.

Which product category is growing fastest in Europe?

Premium beauty is expanding at a 5.03% CAGR owing to consumer trade-ups into clinically validated skincare.

What is the leading distribution channel for European beauty sales?

Pharmacies remain largest, but online retail is seeing the quickest growth at 5.54% CAGR.

Which European country holds the biggest beauty market share?

Germany leads with 15.70% share thanks to high consumer spending and product safety focus.

Page last updated on: