Market Overview

| Study Period | 2021 - 2031 |

|---|---|

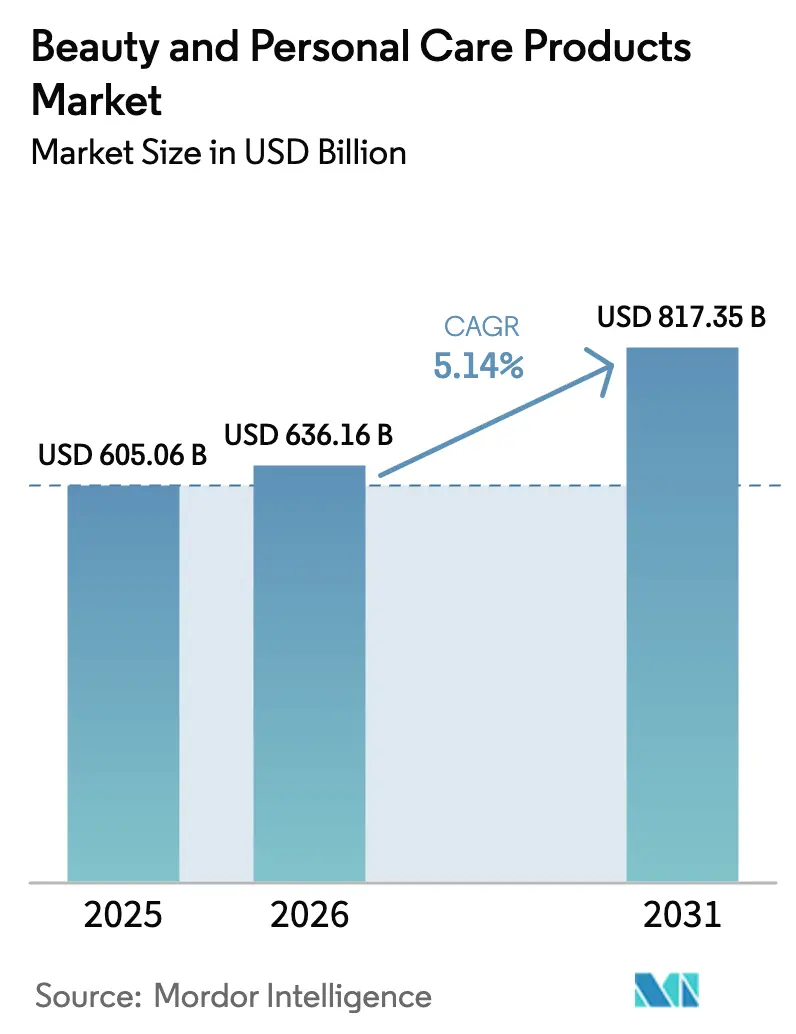

| Market Size (2026) | USD 636.16 Billion |

| Market Size (2031) | USD 817.35 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The beauty and personal care products market size is expected to grow from USD 605.06 billion in 2025 to USD 636.16 billion in 2026 and is forecast to reach USD 817.35 billion by 2031 at 5.14% CAGR over 2026-2031. This growth trajectory is largely influenced by evolving consumer preferences, especially among Generation Z, who now prioritize product efficacy and sustainability over mere brand loyalty. Heightened awareness of side effects from chemical-based products, like skin irritation and allergies, has spurred a surge in demand for natural and organic skincare solutions. In response, market players are broadening their product portfolios with strategic launches and embracing technological advancements, such as artificial intelligence (AI)-driven virtual makeup try-ons, to elevate the digital shopping journey. The industry's resilience shines through its adeptness at navigating economic uncertainties while sustaining growth. Furthermore, benefiting from economies of scale, companies are channeling investments into research and development, all while keeping their pricing strategies competitive. As the beauty and personal care landscape transforms, those companies that adeptly juggle innovation, sustainability, and consumer preferences are poised to ascend as market frontrunners.

Key Report Takeaways

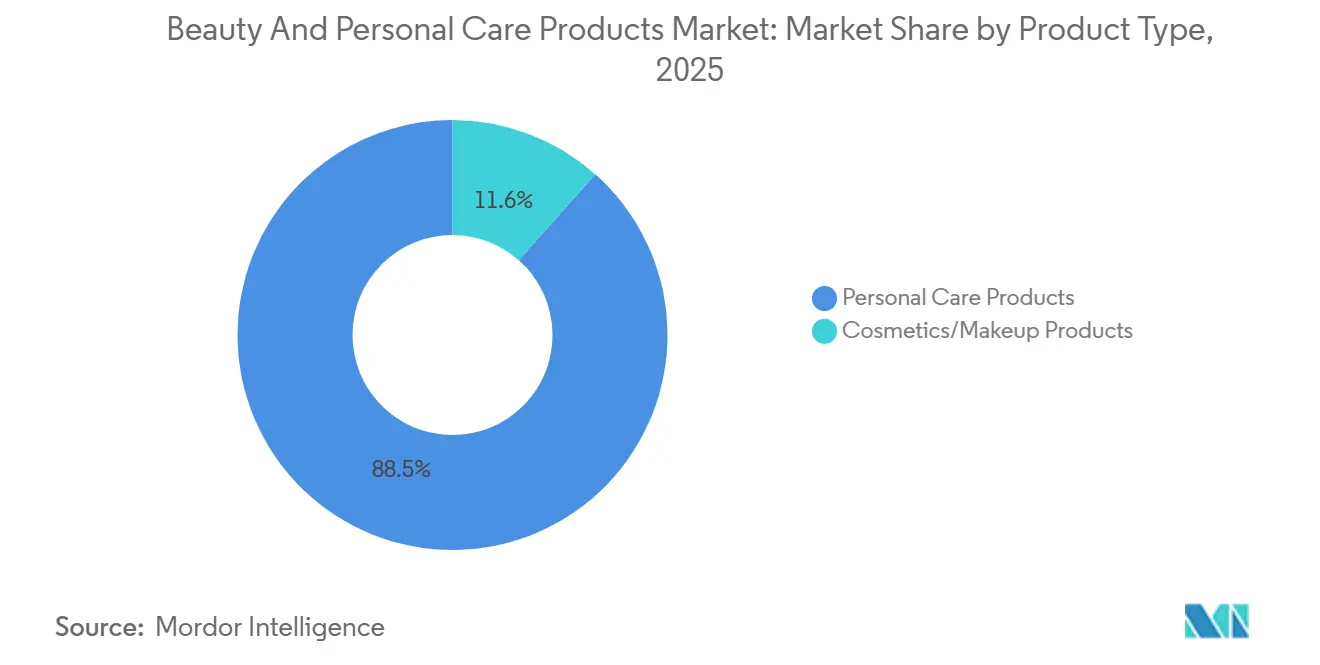

- By product type, personal care products led with 88.45% of the beauty and personal care products market share in 2025, while cosmetics is projected to record the fastest 5.89% CAGR through 2031.

- By category, mass products held 72.37% share of the beauty and personal care products market size in 2025 whereas the premium tier is forecast to expand at a 6.45% CAGR between 2026 and 2031.

- By ingredient type, conventional formulations generated 71.38% revenue in 2025; natural and organic alternatives are set to grow at a 6.89% CAGR to 2031.

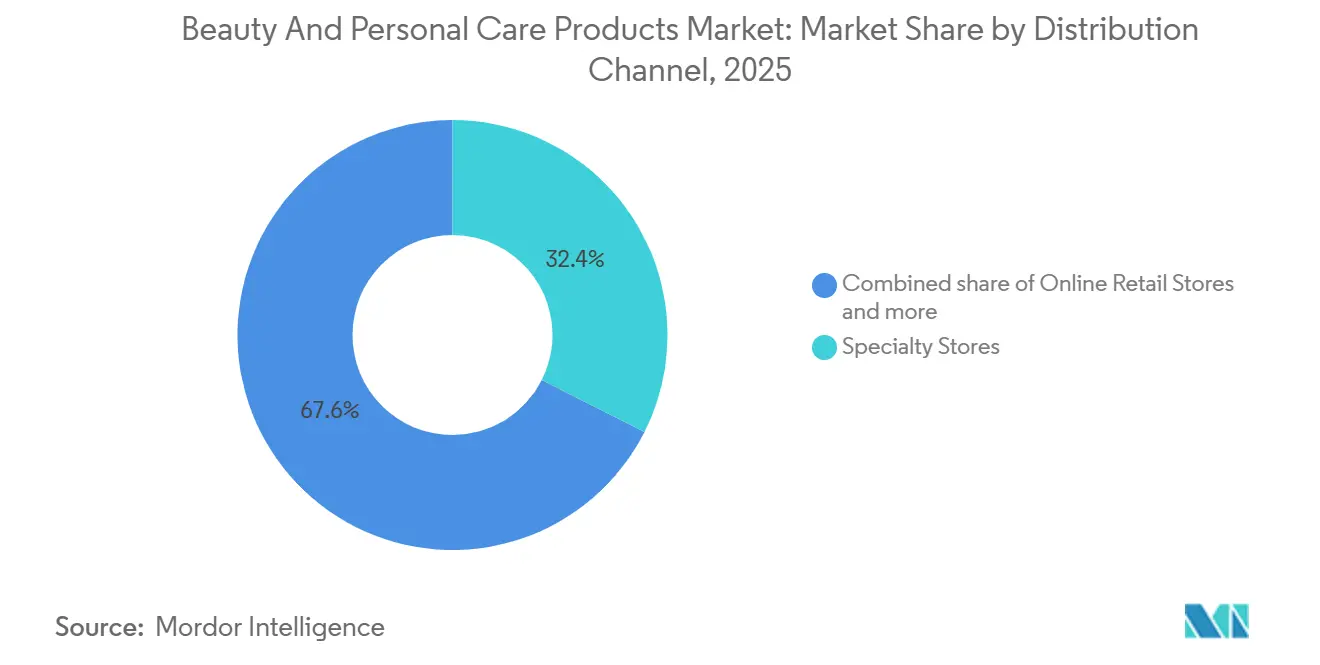

- By distribution channel, specialty stores captured 32.44% revenue in 2025 yet online retail will advance at a 7.97% CAGR through 2031.

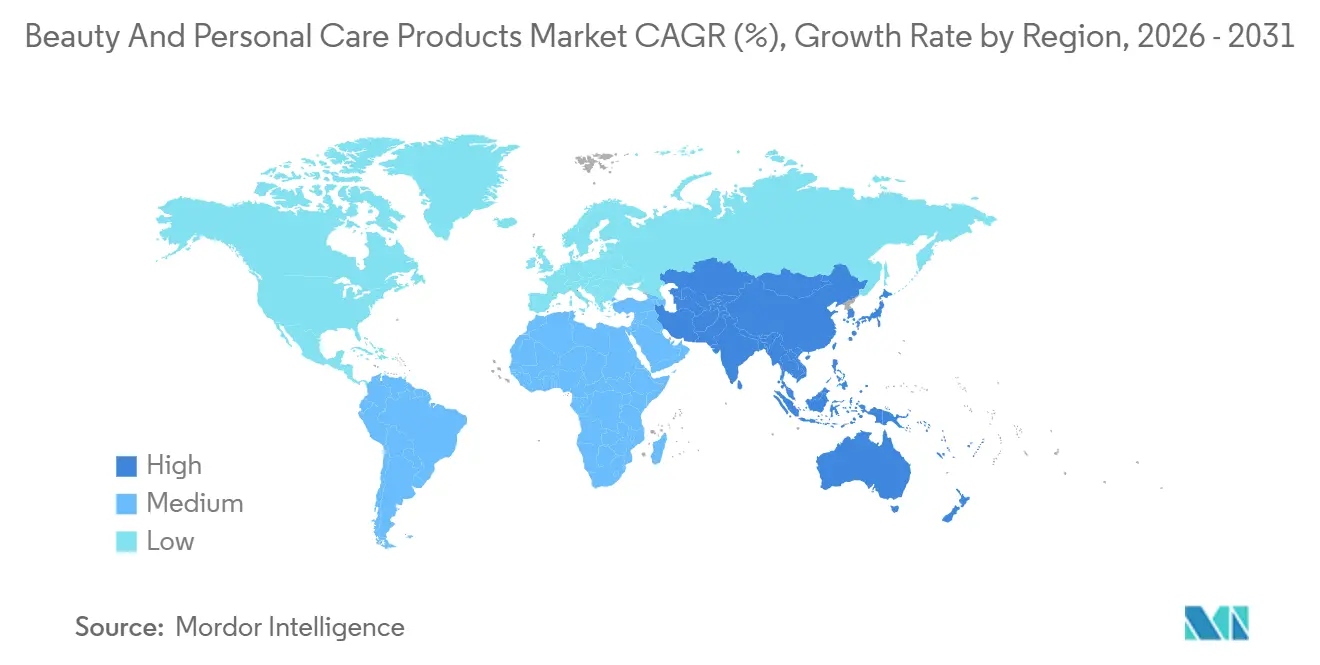

- By geography, Asia-Pacific commanded 35.39% revenue in 2025 and will post the strongest 7.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for natural and organic beauty and personal care products | +1.8% | Global, with strongest adoption in North America and European Union | Medium term (2-4 years) |

| Growing demand for anti-aging and age management products | +1.2% | Global, with premium segments in Asia-Pacific and North America | Long term (≥ 4 years) |

| Influence of social media and impact of digital technology on the market | +0.9% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Rising demand for men's personal care products | +0.7% | North America and European Union core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Digital transformation and virtual try-on | +0.6% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Increased awareness about oral hygiene among consumers | +0.5% | Global, with strongest growth in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer preference for natural and organic beauty and personal care products

Concerns about the negative effects of chemical ingredients in beauty and personal care products, such as skin irritation, allergies, and hormonal imbalances, have significantly increased. This has driven a growing demand for natural and organic skincare alternatives. Unlike synthetic cosmetics, organic products derived from plant extracts and natural oils provide gentle skincare solutions while offering additional benefits like hydration and nourishment. Consumers are becoming more aware of the importance of ingredient transparency, which has become a key factor influencing their purchasing decisions. They are actively seeking products that clearly list recognizable, plant-based components. In response to this shift in consumer preferences, manufacturers have expanded their product portfolios to include items labeled as organic, vegan, natural, chemical-free, and cruelty-free. This approach addresses both health-related concerns and ethical considerations within the skincare industry. A study conducted by NSF International, a leading global public health and safety organization, and published in March 2025, revealed that 74% of consumers consider organic ingredients essential in personal care products[1]Source: NSF International, “Consumers Consider Personal Care Organic Ingredients Important,” nsf.org . This finding highlights a clear and growing trend toward clean beauty products. However, the widespread issue of greenwashing, where brands falsely market products as environmentally friendly, and the lack of consumer trust in voluntary organic labels emphasize the need for third-party testing and certification. Such measures are critical to ensuring transparency and building consumer confidence in the authenticity of organic and natural skincare products.

Influence of social media and impact of digital technology on the market

Technological advancements, including smartphones, personal computers, the internet, and e-commerce, have significantly transformed the global beauty and personal care market. Social media platforms have emerged as a critical tool for brands to showcase their products, connect with potential customers, and generate interest in the market. Prominent companies such as L'Oréal, Unilever, and Estée Lauder utilize platforms like Facebook, Instagram, and YouTube to not only launch new products but also engage with consumers through tutorials and promotional campaigns. These platforms have become a cornerstone for brands to build relationships with their audience and foster loyalty in an increasingly digital world. Additionally, companies are implementing influencer marketing strategies to drive brand conversations into the digital space. Influencers, who often have a strong connection with their followers, play a pivotal role in shaping consumer perceptions. A 2024 survey conducted by the University of Portsmouth revealed that 60% of consumers trusted recommendations from influencers, while nearly half of all purchasing decisions were influenced by these endorsements [2]Source: University of Porth, “New Research Unveils the "Dark Side" of Social Media Influencers and Their Impact on Marketing and Consumer Behaviour”, port.ac.uk. This type of content has proven to be highly effective in increasing brand visibility and enhancing consumer engagement, particularly among younger demographics who are frequent users of social media platforms.

Rising demand for men's personal care products

Driven by evolving social attitudes and heightened consumer awareness, the men's grooming market has experienced significant growth in recent years. Modern men are no longer limiting themselves to basic hygiene routines; instead, they are adopting comprehensive grooming practices. This shift includes the use of specialized skincare products such as cleansers, moisturizers, serums, and masks, which address specific concerns like acne, aging, and sun protection. While traditional shaving products continue to hold a strong presence, the rising popularity of beard care products has further diversified the market. Additionally, the product range now includes body care items such as body washes and lotions, as well as specialized hair care products designed for styling, scalp health, and hair growth. These developments reflect a broader trend of men prioritizing personal care and grooming as part of their daily routines. Significant market developments have also shaped the competitive landscape. For instance, in April 2024, LeBron James entered the beauty sector with the launch of The Shop Men's Grooming Line, created in collaboration with Parlux Fragrances, Limited Liability Company (LLC). This comprehensive product line includes face washes, shaving creams, beard creams, and hair care products, catering to a wide range of grooming needs. Companies are increasingly focusing on strengthening their market presence by leveraging both physical retail outlets and digital platforms. This dual-channel approach aims to enhance product accessibility and provide a seamless shopping experience for consumers, reflecting the industry's commitment to meeting evolving customer expectations.

Increased awareness about oral hygiene among consumers

Consumers are increasingly recognizing the importance of oral hygiene, which is driving significant growth in the beauty and personal care products market. With a deeper understanding of the connection between oral health and overall well-being, individuals are seeking specialized oral care products such as natural and organic toothpaste, mouthwashes, dental floss, and teeth whitening solutions. Social media platforms and digital marketing campaigns by leading oral care companies have been instrumental in educating consumers about effective dental hygiene practices. This heightened awareness, coupled with the rising prevalence of dental issues and the escalating costs of dental treatments, has encouraged consumers to prioritize preventive oral care. Additionally, the rapid expansion of e-commerce platforms has made a broader range of oral care solutions more accessible to consumers, further fueling market growth. Oral diseases, despite being largely preventable, continue to pose a significant health burden globally. These conditions affect individuals throughout their lives, causing pain, discomfort, disfigurement, and, in severe cases, even death. According to the World Health Organization (WHO), as of March 2025, nearly 3.7 billion people worldwide are affected by oral diseases[3]Source: World Health Organization, “Oral Health Fact Sheet,” who.int. This staggering statistic underscores the critical role of oral care products in modern healthcare and personal hygiene routines. The growing demand for these products reflects a shift in consumer behavior toward proactive health management, emphasizing the importance of maintaining oral health as an integral part of overall wellness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products impacts market development | -0.3% | Global, with highest incidence in APAC and Middle East | Short term (≤ 2 years) |

| Growing concerns over product safety and ingredients | -0.4% | Global, particularly North America and EU | Medium term (2-4 years) |

| Intense market competition leading to price pressure and reduced profit margins | -0.5% | Global, most acute in mass-market segments | Long term (≥ 4 years) |

| High manufacturing costs and raw material expenses limit market growth | -0.6% | Global, with supply chain vulnerabilities in APAC and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products impacts market development

Counterfeit goods are posing an escalating challenge to the beauty and personal care sector, with digital channels emerging as the dominant platform for their distribution. These counterfeit products are predominantly found in smaller beauty supply outlets and on e-commerce platforms, where regulatory oversight tends to be less stringent compared to larger retail chains. The widespread availability of discounted options online makes it increasingly difficult for consumers to differentiate between genuine and counterfeit products. This confusion not only risks customer dissatisfaction but also damages the reputation of legitimate brands, potentially impacting their market share and long-term growth. The scale of this issue is highlighted by recent enforcement actions. In October 2025, the United States Customs and Border Protection (CBP) and the United States Food and Drug Administration (FDA) seized 398 shipments containing 8,521 pairs of undeclared or misdeclared contact lenses. Furthermore, officials confiscated 50 additional shipments of misbranded or misdeclared FDA-regulated items, including GLP1 (glucagon-like peptide-1) medications, Botox, dermal fillers, skincare products, and other FDA-prohibited substances. This unchecked distribution of counterfeit goods not only undermines consumer trust but also disrupts market dynamics, creating an uneven competitive landscape for legitimate brands. Addressing this pressing issue requires a collaborative effort among regulatory authorities, e-commerce platforms, and authentic manufacturers to protect consumers and ensure the integrity of the market.

High manufacturing costs and raw material expenses limit market growth

In the beauty and personal care products market, manufacturers face significant challenges due to high production costs and raw material expenses. This industry relies heavily on premium ingredients such as natural extracts, essential oils, and specialized chemicals, which require advanced manufacturing facilities and specialized equipment. Additionally, price fluctuations in raw materials, particularly for natural and organic ingredients, coupled with strict regulatory compliance requirements, further escalate operational costs. These rising costs directly impact product pricing and limit market penetration in price-sensitive regions. Small and medium-sized enterprises (SMEs) are particularly affected, as they often struggle to maintain profitability while competing with well-established players in the market. Furthermore, manufacturers must continuously invest in research and development to meet evolving consumer preferences and adhere to stringent safety standards. This ongoing investment adds another layer of financial burden. The need to implement extensive quality testing protocols and certification processes throughout the production cycle further complicates cost management. These factors collectively contribute to the operational and financial complexities faced by manufacturers in the beauty and personal care products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominates Across Categories

In 2025, personal care products held a significant 88.45% share of the market, while the cosmetics segment is projected to record a 5.89% CAGR through 2031. This growth is primarily driven by key segments such as oral care, which is evolving from traditional hygiene solutions to advanced formulations that incorporate innovative ingredients like peptides and hydroxyapatite. Additionally, the cosmetics segment is transforming as Generation Z consumers exhibit a strong preference for skincare, with 60% identifying it as their primary beauty-related purchase. The men's grooming category is also expanding its scope, moving beyond conventional offerings to include skincare and color cosmetics. This diversification of product categories highlights the industry's proactive response to shifting consumer demographics and preferences.

The evolution of the market is further characterized by the growing integration of wellness concepts into personal care product formulations, leading to the development of hybrid products that transcend traditional category boundaries. This trend is particularly evident in the skincare segment, where consumer priorities have shifted from corrective treatments to preventative health measures. This change reflects a broader transformation in consumer behavior, emphasizing a holistic approach to health and comprehensive personal care routines. The convergence of beauty and wellness is creating new opportunities for innovation in product development and driving market expansion.

By Category: Premium Gains Momentum Despite Mass Dominance

In 2025, mass products hold a commanding 72.37% share of the market, driven by its extensive availability across supermarkets, drugstores, convenience stores, and online platforms. This strong market position is a result of its accessibility, competitive pricing strategies, and widespread acceptance among diverse demographic groups. Despite the dominance of mass products, the premium product segment is poised for significant growth, with a compound annual growth rate (CAGR) of 6.45% projected for the period from 2026 to 2031. The market has demonstrated resilience even during periods of economic uncertainty, as consumers purchasing prestige products also tend to buy mass products, reflecting a value-conscious mindset across different pricing tiers.

Prominent companies, including Unilever, Procter & Gamble Company, and private-label brands, are actively responding to shifting consumer preferences by focusing on the development of ethical and environmentally friendly products. The convergence of mass and premium product categories has intensified competition while simultaneously increasing consumer access to high-quality formulations. Mass Products continues to maintain its leadership through ongoing product innovation and competitive pricing, while the premium segment is experiencing growth driven by the introduction of natural and organic skincare products and the strategic use of beauty influencer marketing. This evolving market dynamic ensures that consumers benefit from broader access to premium-quality formulations while also addressing their practical needs for everyday beauty and personal care solutions.

By Ingredient Type: Natural Surge Challenges Conventional Dominance

In 2025, conventional and synthetic ingredients held a significant 71.38% market share. This dominance is attributed to their superior performance and cost-effectiveness, particularly in mass market segments where consumers are highly price-sensitive. On the other hand, natural and organic formulations are witnessing the fastest growth, with a compound annual growth rate (CAGR) of 6.89%. This growth is supported by third-party certifications, which enhance transparency and build consumer trust by validating the authenticity of these products. The market is progressively shifting toward hybrid solutions that integrate natural active ingredients with synthetic stabilizers and delivery systems. This balanced strategy enables manufacturers to address diverse consumer preferences while ensuring product stability and maintaining high levels of effectiveness.

The increasing consumer awareness of potential health risks associated with synthetic cosmetics, such as skin irritation and hormonal imbalances, is driving the demand for natural ingredients. Products derived from plant extracts and oils are gaining traction as they offer gentler alternatives along with additional benefits like hydration and nourishment. The preference for chemical-free skincare products with transparent labeling and easily identifiable plant-based ingredients continues to grow. This trend aligns with the rising health consciousness among consumers and their inclination toward values-based purchasing decisions. Furthermore, the influence of social media and the availability of educational content highlighting the advantages of natural ingredients in skincare routines are reinforcing this shift in consumer behavior.

By Distribution Channel: Digital Revolution Reshapes Retail Landscape

In 2025, specialty stores held a dominant 32.44% market share. At the same time, online retail stores are expected to achieve the highest growth rate, with a compound annual growth rate (CAGR) of 7.97% through 2031. Supermarkets and hypermarkets continue to maintain a strong market presence due to their accessibility, proximity to consumers, and ability to attract shoppers with late-night deals and exclusive promotions. However, these traditional retail channels are increasingly facing competition from specialized online retailers and beauty-focused platforms. These platforms offer curated shopping experiences and expert advice, which appeal to a growing segment of consumers. This competitive landscape has even impacted well-established luxury retailers, as demonstrated by Farfetch and Net-a-Porter discontinuing their in-house beauty operations.

Convenience stores differentiate themselves by providing product testing and sampling services, which enhance brand visibility and optimize retail space utilization. The e-commerce channel continues to gain traction as consumers increasingly value the convenience of 24/7 shopping access and the ability to avoid crowded physical stores. Online platforms offer an extensive variety of products and enable consumers to compare and select brands that best meet their individual preferences. Additionally, supermarkets and hypermarkets remain attractive to consumers by offering generic brands at lower price points compared to well-known branded products, thereby catering to a wide range of price sensitivities and preferences.

Geography Analysis

Asia-Pacific is projected to lead the market with a 35.39% share by 2025, maintaining the highest growth rate at 7.47% compound annual growth rate (CAGR) through 2031. This growth is driven by increasing disposable incomes, urbanization, and a growing focus on beauty and personal care. The region's rapid digital adoption, particularly through social media platforms, significantly influences product discovery and purchasing decisions among Generation Z consumers. Additionally, K-beauty brands continue to expand their global influence and are expected to implement price adjustments in 2025 to address economic challenges. In India, there is a rising demand for dermatologist-certified hair care products, prompting brands like Schwarzkopf and L'Oreal to introduce nutrient-enriched shampoos containing vitamin B3.

North America remains a strong performer due to its well-established market infrastructure and high per-capita spending on beauty products, despite moderate growth in this mature market. In the United States, consumer preferences are shifting towards clean-label and "free-from" product claims, reflecting a growing focus on self-care. Europe is experiencing steady growth, supported by sustainability initiatives and regulatory frameworks that encourage innovation. France continues to hold its position as a global hub for luxury beauty products. Regulatory changes, such as the implementation of the Modernization of Cosmetics Regulation Act (MoCRA) in the United States and restrictions on per- and polyfluoroalkyl substances (PFAS) in Europe, are reshaping compliance requirements. Meanwhile, digital platforms like Amazon and TikTok Shop are transforming retail models and influencing consumer behavior.

South America and the Middle East and Africa are emerging as high-growth markets with unique characteristics. In Brazil, the beauty market is undergoing significant transformation, driven by the influence of digital media and increased consumer awareness of product formulations. In the Middle East, demand for halal cosmetics is rising, fueled by growing awareness of animal cruelty and adherence to religious principles. Both regions benefit from urbanization and increasing disposable incomes but face challenges such as currency volatility, reliance on imports, and evolving regulatory frameworks. These factors necessitate strategic approaches for market entry and expansion.

Regulatory Landscape

Regulation is tightening around ingredient safety, labeling, and supply-chain accountability, increasing compliance demands for global beauty and personal care manufacturers. In the United States, the FDA is enforcing the Modernization of Cosmetics Regulation Act (MoCRA), which focuses on facility registration and product listing as companies align governance and documentation for cosmetics and adjacent personal care categories.

In Europe, updates to Regulation (EC) No 1223/2009 accelerated in 2026 through Commission Regulation (EU) 2026/78 (applied from 1 May 2026) and Commission Regulation (EU) 2026/909 (27 April 2026), adding or tightening restrictions for specific substances and aligning cosmetics controls with CLP-based CMR classifications. Labeling requirements also tightened in mid-2026, including a 15 July 2026 threshold-linked warning requirement for products that release formaldehyde above 0.001% (10 ppm), which is driving reformulation, testing, and artwork changes across multinational portfolios.

Competitive Landscape

The beauty and personal care products market is led by large multinational corporations such as L'Oréal, Unilever, and Procter & Gamble. These companies capitalize on their extensive distribution networks and economies of scale to maintain their dominance. However, they face increasing competition from digitally native brands that utilize social commerce and direct-to-consumer strategies. This competitive environment has allowed smaller, innovation-driven companies to secure significant market shares by focusing on differentiated offerings, particularly in segments like natural and organic formulations, men's grooming, and specialized skincare.

Among the fastest-growing segments, natural and organic formulations, along with men's grooming and specialized skincare, are gaining traction. These segments are driven by evolving consumer preferences for sustainable and tailored solutions. For instance, The Ordinary, a brand known for its science-based skincare, expanded its reach in January 2024 by launching on the United States Amazon Premium Beauty marketplace. This move enables U.S. customers to purchase authentic products directly through amazon.com/theordinary, ensuring product authenticity and accessibility through authorized channels.

Beyond these segments, the market holds significant opportunities in underserved demographics, particularly male consumers and older age groups. Additionally, geographic expansion into high-growth regions such as India and the Middle East offers substantial potential for companies that can adapt their products and marketing strategies to align with local preferences and cultural nuances. This adaptability creates a dynamic environment for both established players and emerging brands to capture market share through targeted approaches.

Beauty And Personal Care Products Industry Leaders

-

The Procter & Gamble Company

-

L'Oreal SA

-

Unilever PLC

-

Colgate-Palmolive Company

-

The Estee Lauder Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven reformulation and traceability are creating room for ingredient substitution, testing, and certified claims in natural and organic products, where consumers are increasingly evaluating efficacy and sustainability. Regulatory tightening on CMR-related substances in the EU (including the 2026 amendments) and active enforcement under the FDA's MoCRA are pushing brands to improve documentation, safety substantiation, and supplier qualification, which raises the value of third-party certification and authenticated distribution. This is particularly relevant as counterfeit products remain a visible restraint in digital channels.

Manufacturing localization and scale-up investments are also improving supply reliability and supporting premiumization opportunities, especially in fragrances and dermocosmetics. In 2026, CHANEL opened a new 30,000-square-meter fragrance manufacturing facility in Venette, France (EUR 150 million investment, 50 million bottles annual capacity), while Pierre Fabre announced a EUR 50 million investment to transform and expand its Avene-les-Bains production site under its 2023-2027 industrial plan. These additions support higher-capacity, quality-controlled supply for premium and clinical-positioned lines, and parallel North American capacity expansions in cosmetic ingredients and contract manufacturing, such as validated cosmetic-ingredient production at Gattefosse's Lufkin, Texas facility, reinforce resilience as online retail extends and brands pursue faster replenishment cycles with tighter controls on authenticity.

Recent Industry Developments

- July 2026: L'Oreal entered a 50-year exclusive worldwide beauty license agreement with Kering for the Gucci brand, with the agreement taking effect on July 1, 2027. The deal secures long-duration access to a major luxury house, supporting L'Oreal's position in prestige beauty categories where licensing underpins fragrance and cosmetics portfolios.

- April 2026: Unilever agreed to acquire Gruns, a US-based greens supplement company, to strengthen its Beauty and Wellbeing portfolio. The acquisition extends Unilever further into ingestible wellness-adjacent routines that sit alongside topical beauty and personal care regimens, supporting cross-category brand building and broader consumer lifetime value.

- December 2024: Unilever's Dove introduced the Cream Serum Collection, bringing niacinamide-rich facial skincare-style ingredients into body care products. The launch shows ongoing formulation convergence between skincare and personal care, helping mass brands compete with premium cues through ingredient-led positioning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue from consumer beauty and personal care products that are sold as packaged goods through store-based retail and online channels, and are meant for cleansing, grooming, odor control, or appearance enhancement.

Scope exclusions: We exclude professional salon services, aesthetic procedures, dietary supplements, and at-home beauty devices from the market totals.

Segmentation Overview

-

By Product Type

-

Personal Care Products

-

Hair Care

- Shampoo

- Conditioner

- Hair Colorant

- Hair Styling Products

- Others

-

Skin Care

- Facial Care Products

- Body Care Products

- Lip and Nail Care Products

-

Bath and Shower

- Shower Gels

- Soaps

- Others

-

Oral Care

- Toothbrush

- Toothpaste

- Mouthwashes and Rinses

- Others

- Men's Grooming Products

- Deodorants and Antiperspirants

- Perfumes and Fragrances

-

Hair Care

-

Cosmetics/Makeup Products

- Facial Cosmetics

- Eye Cosmetics

- Lip and Nail Makeup Products

-

Personal Care Products

-

By Category

- Premium Products

- Mass Products

-

By Ingredient Type

- Natural and Organic

- Conventional/Synthetic

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we start by mapping the demand pool and the supply environment behind packaged beauty and personal care sales. Common references include public sources such as UN Comtrade for trade flows, World Bank and IMF macro indicators, OECD consumer and inflation series where available, and national statistical offices that publish household spending and price index details.

To ground category logic, we also review regulatory and standards sources such as the US FDA cosmetics guidance and the EU Cosmetics Regulation pages, followed by open literature and peer-reviewed articles on ingredient and formulation trends. Company annual reports, earnings decks, and investor presentations are used to understand portfolio mix, geographic exposure, and channel priorities, and reputable press helps validate timing of launches and pricing moves. In parallel, we use approved paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import and export data to cross-check scale and direction. The sources listed here are illustrative only, and additional public and internal references were used for collection, cross-verification, and clarification.

Primary Interviews and Surveys

Primary work is used to test what desk research cannot fully confirm, especially around category boundaries, pricing behavior, and channel mix across regions. We speak with a spread of brand owners, contract manufacturers, ingredient suppliers, distributors, and retail-channel stakeholders, and then validate assumptions across APAC, EMEA, and the Americas so the model does not rely on a single region's trend cycle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 39% |

| Mid tier: 46% | Functional/Unit leaders: 29% | EMEA: 34% |

| Smaller Players: 15% | Managers: 59% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where consumption and retail sell-through signals are reconstructed from macro spend capacity, category penetration, and price progression, and then allocated into beauty and personal care based on observed category weights. Since data availability varies by country, we corroborate the totals with selective bottom-up checks such as sampled price per unit by category, channel checks with distributors and retailers, and roll-ups from a set of representative suppliers to keep the output realistic.

Key inputs used in the model include household consumption expenditure trends, urbanization and working population mix, beauty and personal care CPI movements that influence ASPs, and e-commerce share shifts versus store-based retail. We also review import and export movements for finished products and selected intermediates as a sanity check. Where direct indicators are missing for smaller countries, gaps are handled through proxy mapping using nearby markets with similar income bands, channel structure, and observed price ladders, and then confirmed in interviews.

For forecasting, we mainly use multivariate regression supported by scenario analysis so the model can reflect both income and pricing drivers without overstating either. The variable outlook is tuned using expert feedback on near-term price normalization, premiumization intensity, and channel expansion pace, and then the final curve is reviewed for smoothness and plausibility at the regional roll-up.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, followed by variance checks that flag outliers at the country, category, and regional levels. When a number looks off, we re-check the input series, revisit the conversion and inflation handling, and then re-contact selected respondents to confirm whether the change is real or driven by the model.

Before sign-off, the model and assumptions go through a multi-step analyst review so definitions, arithmetic, and year-to-year movement are consistent with known market dynamics. Reports are refreshed annually, and interim updates are added when major events materially affect pricing, demand, or channel structure. Right before delivery, a fresh pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Global Beauty and Personal Care Products Market Market Size Measured Against Other Published Estimates

Published market sizes for beauty and personal care products can vary even when they appear to describe the same topic, because each publisher draws its own line around product revenue and which year is treated as the starting point. Differences in channel coverage, treatment of inflation in pricing, and how quickly assumptions are refreshed also tend to widen the spread.

By tracking retail-channel scope checks, inflation-adjusted ASP movement, and annual assumption refreshes, Mordor Intelligence anchors the 2026 total to packaged product sales only, which avoids mixing in salon services or adjacent wellness spend that can silently inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 636.16 B (2026) | |

| Global Consultancy A | USD 683.15 B (2026) | Uses a higher 2026 value tied to a 2025 base-year build and a longer horizon, and the page shows internal inconsistencies in CAGR and repeated 2025 lines, which can shift the total depending on the data cut used. |

| Industry Publisher B | USD 599.15 B (2024) | Anchors sizing to a different base year and a shorter 2024 to 2030 window, and it presents alternate market-size endpoints on the same page, which suggests revisions or scope variants across editions. |

Overall, the spread is mostly explained by base-year choice, how pricing is carried forward, and whether adjacent spend categories are unintentionally blended into product revenue. Our approach stays traceable because the inputs are linked to repeatable demand and pricing indicators, and the checks can be rerun when new public series or interview confirmations become available.

Key Questions Answered in the Report

What is the current value of the beauty and personal care products market in 2026?

The category is valued at USD 636.16 billion in 2026 with a 5.14% CAGR forecast toward 2031.

Which region will contribute the largest incremental revenue through 2031?

Asia-Pacific, already leading with 35.39% share in 2025, will add the most new revenue at a 7.47% CAGR.

Which distribution channel is growing the fastest?

Online retail leads with a projected 7.97% CAGR as consumers favor digital discovery and subscription replenishment.

How large is the natural and organic ingredient opportunity?

Natural and organic formulations are projected to expand at a 6.89% CAGR, outpacing conventional alternatives while still below 30% revenue share.

Page last updated on: