Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

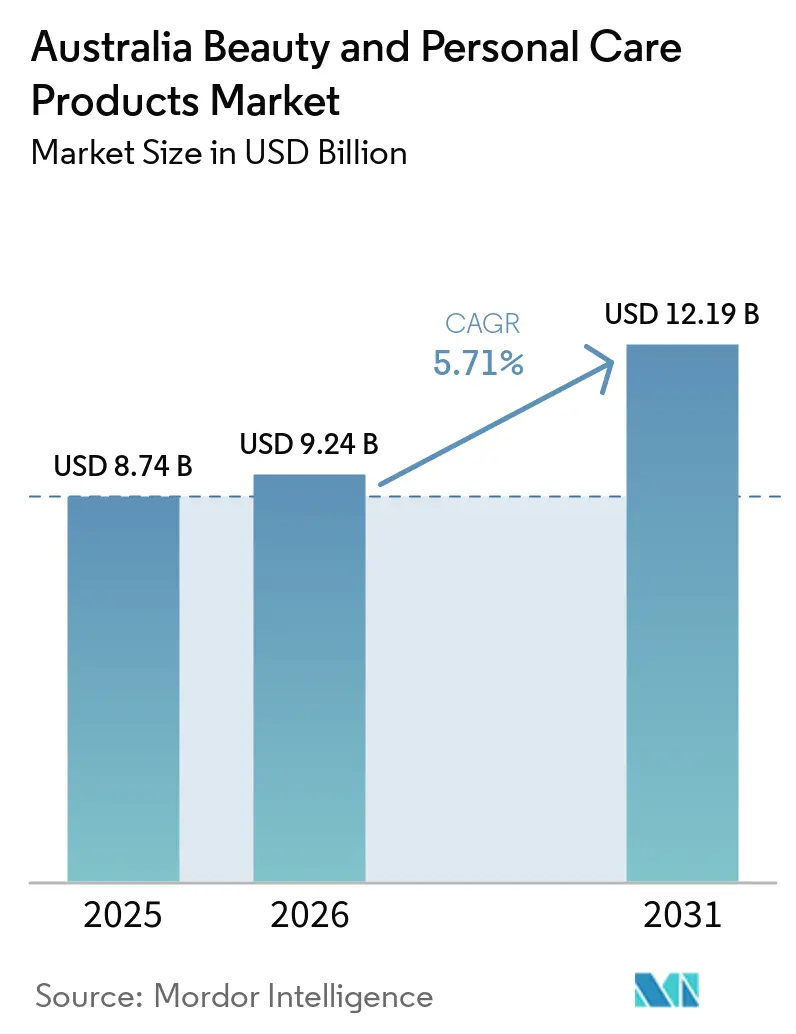

| Base Year Market Size (2025) | USD 8.74 Billion |

| Market Size (2026) | USD 9.24 Billion |

| Market Size (2031) | USD 12.19 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The Australian beauty and personal care products market size is expected to grow from USD 8.74 billion in 2025 to USD 9.24 billion in 2026 and is forecast to reach USD 12.19 billion by 2031 at 5.71% CAGR over 2026-2031. This growth is driven by increasing disposable incomes, a growing aging population seeking anti-aging solutions, and the recovery of tourism, which boosts interest in region-specific products. Consumers are now prioritizing premium formulations, sustainable packaging, and ethically sourced products, although many still prefer affordable mass-market brands. Regulatory oversight by the Australian Competition and Consumer Commission (ACCC) is helping to reduce misleading claims and counterfeit products, enhancing consumer trust and benefiting companies that comply with these standards. By product type, personal care products dominate the market, but cosmetics are gaining momentum. In terms of category, premium products are growing rapidly, challenging the dominance of mass-market options. Organic products are also gaining popularity, gradually competing with conventional offerings. The distribution landscape is evolving as digital platforms drive the shift toward omnichannel retailing. The market remains moderately fragmented, with no single company holding a dominant share, ensuring healthy competition and opportunities for innovation.

Key Report Takeaways

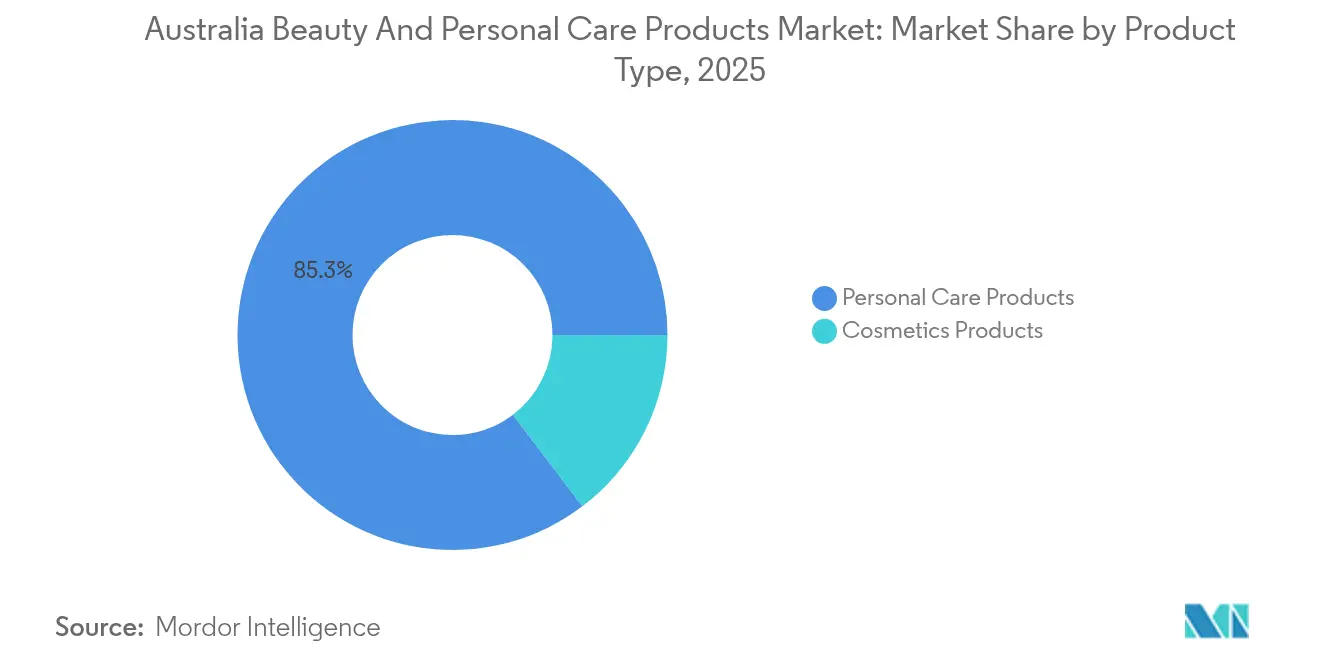

- By product type, personal care products held 85.32% of the Australian beauty and personal care products market share in 2025, while cosmetics products are advancing at a 5.79% CAGR through 2031.

- By category, mass offerings dominated with 71.98% revenue share in 2025, yet premium lines are forecast to expand at a 6.32% CAGR to 2031.

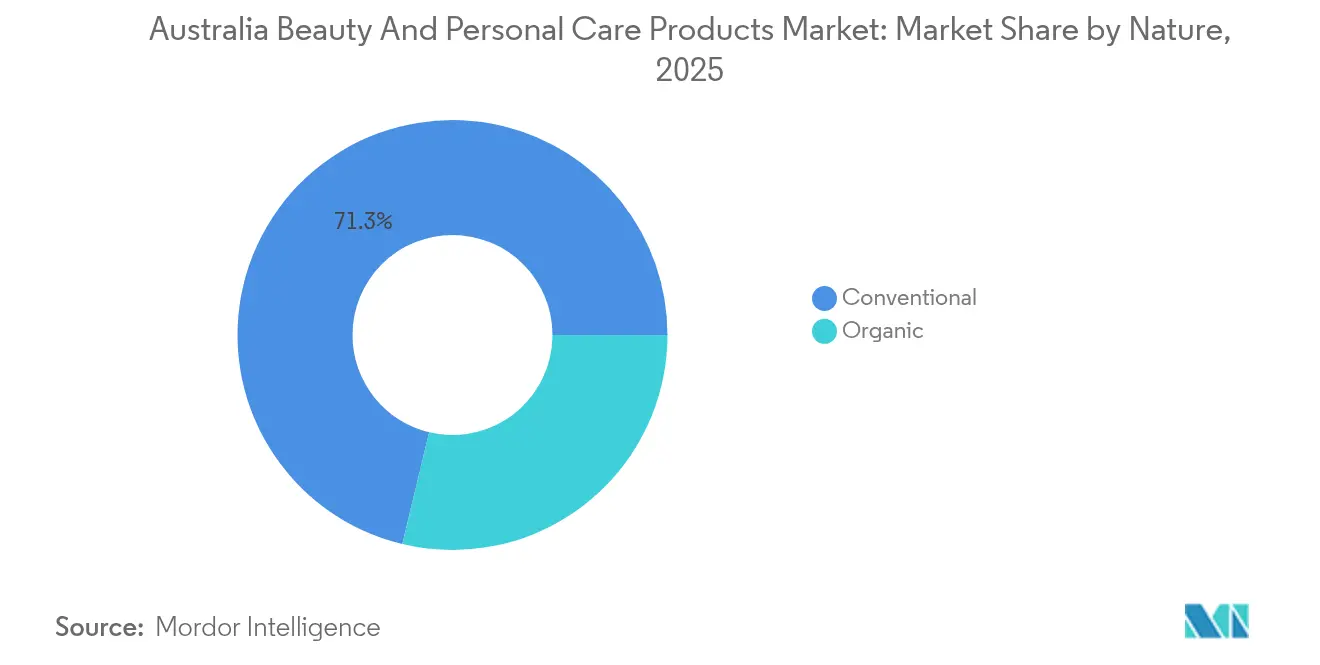

- By nature, conventional items controlled 71.25% share of the Australian beauty and personal care products market size in ,2025 and organic products are on track for a 6.95% CAGR over the outlook period.

- By distribution channel, health and beauty stores captured 37.85% revenue in 2025, whereas online retail is growing at a 7.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing consumer preference for natural and organic beauty and personal care products | +1.2% | National, with stronger adoption in Melbourne and Sydney metropolitan areas | Medium term (2-4 years) |

| Increasing demand for anti-aging and age management products | +0.8% | National, with higher penetration in affluent coastal regions | Long term (≥ 4 years) |

| Impact of social media and advancements in digital technology | +0.9% | National, with urban centers leading adoption | Short term (≤ 2 years) |

| Rising interest in men's personal care products | +0.7% | National, with premium segments concentrated in major cities | Medium term (2-4 years) |

| Demand for region-specific products driven by inbound tourism | +0.6% | Tourism hubs including Sydney, Melbourne, Gold Coast, Cairns | Short term (≤ 2 years) |

| Increased focus on self-care and wellness | +0.5% | National, with higher engagement in wellness-focused demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for anti-aging products

Australia's anti-aging products demand is growing, driven by an aging population with higher disposable incomes. In 2023, Australian women spent up to AUD 3,600 a year on beauty products, averaging about AUD 300 per month, showing a strong focus on anti-aging and skincare. Consumers are buying advanced serums, peptide complexes, and at-home devices that offer clinic-like results. For example, L'Oréal's Revitalift Filler Hyaluronic Mask, sold across the country, appeals to those who prefer non-invasive options. Awareness campaigns about ingredients like retinol, glycolic acid, and hyaluronic acid are encouraging their use in daily routines. This is supported by Australia's high spending power and awareness of sun protection. People aged 55 and older make up 26% of the population in cities and 34% in other areas, showing a key group of potential buyers for anti-aging products, according to the Australian Bureau of Statistics 2024[1]Source: Australian Bureau of Statistics, "Regional population by age and sex", abs.gov.au. This reflects a strong demand for anti-aging products and treatments.

Rising interest in men’s personal care

Australia's men's personal care market is growing steadily as more men take an active interest in grooming and self-care. This market has expanded beyond basic shaving products to include advanced options for skin, hair, and fragrances. Changing social attitudes and workplace expectations have made grooming routines more acceptable and even encouraged, leading men to adopt more comprehensive personal care habits. Hair loss and thinning are among the top concerns for men, with 43% of Australians affected as of May 2024, as per Kerastase in 2024. Furthermore, 40.8% of Australian men are expected to experience baldness by 2025, as per the World Population Review, 2025[2]Source: World Population Review, "Percentage of Bald Males by Country 2025", worldpopulationreview.com. This has created a strong demand for specialized haircare and scalp treatments designed specifically for men. In response, brands are developing products that cater to men's unique needs, such as multipurpose solutions that save time and effort. To appeal to traditional male consumers, these products are often packaged in a way that emphasizes masculinity, ensuring they resonate with their target audience.

Demand for region-specific products driven by tourism

The demand for region-specific beauty and personal care products in Australia is growing significantly, driven by the recovery of tourism and strong retail performance. In June 2025, international visitor arrivals reached 2.07 million, contributing heavily to this trend, as per the Australian Bureau of Statistics, 2024[3]Source: Australian Bureau of Statistics, "Overseas Arrivals and Departures, Australia", abs.gov.au. These visitors spent a total of AUD 32.1 billion, showcasing the importance of tourism to the market, as per the World Travel and Tourism Council (WTTC) in 2025[4]Source: World Travel and Tourism Council (WTTC), "Australia’s Travel & Tourism Sector Set to Reach Record USD 315BN in 2025", wttc.org. Retail sales in Australia also saw an increase in November 2024, exceeding AUD 37 billion, with events like Black Friday playing a major role in boosting sales. Most international visitors focus their spending in key cities like Sydney and Melbourne, which has led to increased sales in airport duty-free shops and local retail outlets. This growing interest has encouraged brands to develop locally inspired product lines that feature native Australian botanicals and limited-edition travel-friendly formats. Products highlighting Indigenous ingredients, such as Kakadu plum are becoming increasingly popular both within Australia and in international markets.

Impact of social media and digital technology

The influence of social media and digital technology on Australia’s beauty and personal care market is significant, changing how people discover, evaluate, and buy products. Social media influencers have become a powerful tool for promoting brands, often proving more effective than traditional advertisements. At the same time, stricter regulations by the Australian Competition and Consumer Commission (ACCC) on misleading posts are encouraging brands to focus on honest and authentic marketing. Digital advancements, such as augmented reality for virtual product try-ons, AI-based personalized recommendations, and live-stream shopping events, are making online shopping more engaging and convenient. These innovations are driving growth in e-commerce beauty sales. To keep up with these trends, traditional retailers are adopting data-driven tools and offering personalized in-store experiences to attract tech-savvy customers and stay competitive in the evolving market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growth of counterfeit products | -0.4% | National, with higher concentration in online marketplaces | Short term (≤ 2 years) |

| Increasing awareness regarding product safety and ingredient transparency | -0.3% | National, with stricter scrutiny in urban markets | Medium term (2-4 years) |

| Increasing adoption of DIY approaches and minimalist trends | -0.5% | National, with stronger adoption among younger demographics | Medium term (2-4 years) |

| Intense competition and pricing challenges | -0.6% | National, with particular pressure in mass market segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of counterfeit products

The rise of counterfeit products is becoming a major issue in Australia’s beauty and personal care market. Many unauthorized sellers are using online platforms to sell fake products, which often contain harmful substances like mercury or lead. These counterfeit goods not only harm consumer trust but also take away revenue from genuine brands. For example, in 2023, the Australian Competition and Consumer Commission (ACCC) removed over 50 fake cosmetic products from online marketplaces. In 2024, a legal dispute arose when Charlotte Tilbury sued MCoBeauty for trademark infringement, claiming similarities between their "Flawless Glow" product and Tilbury's "Hollywood Flawless Filter." This case highlights the challenges brands face in distinguishing between affordable alternatives and counterfeit items. To address this issue, legitimate brands are focusing on measures like serialization, tamper-proof packaging, and educating consumers about identifying authentic products.

Increasing adoption of do-it-yourself (DIY) approaches and minimalist trends

The growing popularity of do-it-yourself (DIY) methods and minimalist trends is significantly influencing Australia’s beauty and personal care market. Many consumers are now making their own skincare and haircare products at home using natural ingredients. This shift is driven by a desire for more personalized solutions, cost-effectiveness, and environmentally friendly practices. Minimalist beauty routines, which focus on using fewer but multifunctional products, are gaining traction. These trends are changing consumer preferences, leading to reduced demand for single-purpose or highly specialized products. To adapt, brands are focusing on creating versatile, multi-use formulations that align with these preferences. They are also investing in educating consumers about the advantages of professionally developed products, aiming to stay relevant in a market that increasingly values simplicity, sustainability, and customization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominance Faces Cosmetics Acceleration

In 2025, personal care products made up 85.32% of the Australian beauty and personal care market, showing that consumers prioritize essential items like hair care, skincare, and oral hygiene. These products are part of daily routines, driven by growing awareness of health, hygiene, and overall wellness. To cater to this demand, manufacturers are offering convenient options such as bundled products, subscription services, and multi-purpose items. This focus on practicality and reliability ensures that personal care remains the largest and most stable segment in the market, reflecting its importance in consumers' everyday lives.

On the other hand, the cosmetics segment is expected to grow at a faster rate, with a projected CAGR of 5.79% from 2026 to 2031. This growth is fueled by factors such as social media influence, increasing interest in premium-quality products, and the desire for professional-grade results at home. Younger, tech-savvy consumers are drawn to innovative launches in makeup and color cosmetics, which often emphasize personalization and high-quality formulations. As a result, the cosmetics segment is becoming a dynamic and rapidly expanding part of the Australian beauty and personal care market, appealing to consumers who enjoy experimenting with new products and trends.

By Category: Premium Surge Challenges Mass Dominance

In 2025, mass-market products led the Australian beauty and personal care market, contributing to 71.98% of total sales. This dominance is largely due to their affordability and widespread availability in supermarkets and pharmacies, which cater to the everyday needs of a broad consumer base. These products are popular for their practicality, offering reliable solutions at accessible price points. Frequent discounts and promotions further drive their appeal, ensuring consistent demand. As a result, mass-market products remain a cornerstone of the industry, meeting the needs of cost-conscious and convenience-driven shoppers.

On the other hand, the premium segment is expected to grow at a faster rate, with a projected CAGR of 6.32% through 2031. This growth is fueled by increasing disposable incomes and a growing preference for high-quality, luxurious products. Consumers are drawn to premium offerings for their advanced formulations, exclusive ingredients, and superior performance. Additionally, the rise of e-commerce and boutique stores has made premium products more accessible, allowing brands to target customers seeking personalized and aspirational beauty experiences. This shift highlights the evolving preferences of consumers who are willing to invest in products that align with their lifestyle and values.

By Nature: Organic Momentum Builds Against Conventional Leadership

Conventional formulations continued to lead the Australian beauty and personal care market in 2025, contributing to 71.25% of total sales. These products remain popular due to their affordability, wide availability, and trusted brand names, which have built strong consumer loyalty over time. Shoppers often rely on these formulations for their everyday needs, as they offer consistent performance and meet basic beauty and personal care requirements. The convenience of purchasing these products through supermarkets and pharmacies further supports their dominance in the market.

On the other hand, organic and natural formulations are expected to grow significantly faster, with a projected CAGR of 6.95% from 2026 to 2031. This growth is fueled by increasing consumer awareness of sustainability and the demand for products with clean, eco-friendly ingredients. Many consumers are now prioritizing health-conscious and environmentally responsible choices, driving the shift toward organic alternatives. These products appeal to individuals seeking chemical-free and skin-friendly solutions, making them a rapidly expanding category in the beauty and personal care market. The rise of e-commerce and specialty stores has also made it easier for consumers to access these niche offerings, further boosting their popularity.

By Distribution Channel: Digital Disruption Accelerates Omnichannel Evolution

Health and beauty stores continued to be a major distribution channel in Australia’s beauty and personal care market in 2025, contributing 37.85% of the sector's total revenue. These stores attract customers by offering personalized advice from pharmacists, opportunities to try products in-store, and convenient locations in suburban areas. This combination builds consumer trust and encourages informed purchasing decisions. Health and beauty stores remain a preferred choice for buying both everyday personal care items and premium products, especially those that benefit from in-person evaluation. Their role in the market is crucial, as they cater to a wide range of consumer needs.

On the other hand, online channels are growing rapidly and are expected to expand at a CAGR of 7.02% through 2031, outpacing the growth of physical stores. E-commerce platforms are gaining popularity due to features like virtual try-ons, AI-based product recommendations, and live shopping experiences. These innovations, combined with the convenience of home delivery and access to a broader range of products, are attracting tech-savvy consumers. As more people turn to online shopping for beauty and personal care products, digital platforms are reshaping the way Australians shop, offering a seamless and personalized experience.

Geography Analysis

Australia's beauty and personal care market thrives on factors such as high disposable incomes, diverse cultural influences, and an outdoor-oriented lifestyle. These elements drive demand for products like sun care and hydration solutions. Urban centers such as Sydney and Melbourne lead in the adoption of premium products, supported by affluent populations, international tourism, and luxury retail hubs. Coastal regions exhibit a strong preference for SPF-based foundations and after-sun treatments to protect and repair skin from sun exposure. Meanwhile, drier inland areas prioritize moisturizers with long-lasting hydration to combat the arid climate, reflecting the varied needs across the country.

The market benefits significantly from Australia's stable political environment, advanced infrastructure, and consistent regulatory framework, which facilitate seamless expansion for brands. Regional consumers often rely on pharmacy chains and supermarkets for everyday beauty essentials, while urban shoppers gravitate toward specialty stores offering premium and niche products. Brands incorporating native Australian ingredients, such as Kakadu plum and wattleseed, gain a competitive advantage by providing unique offerings. However, maintaining ethical sourcing practices is crucial for these brands to build trust and ensure authenticity in a market that values sustainability and transparency.

E-commerce plays an increasingly vital role in making beauty and personal care products accessible to both urban and remote consumers, leveraging Australia's reliable postal network. Government initiatives, such as export grants for small businesses, are enabling local brands to expand into international markets, including Asian duty-free stores and online platforms. A stable exchange rate helps manage the cost of imported skincare devices, while domestic manufacturers benefit from a weaker Australian dollar, which enhances the appeal of their exports to global buyers. These dynamics collectively position Australia's beauty and personal care market for sustained growth and innovation.

Competitive Landscape

The market is moderately fragmented, indicating a competitive environment where no single company dominates. Global companies like L'Oréal, Unilever, and Procter & Gamble maintain their strong positions by utilizing advanced research, patented innovations, and extensive marketing resources. Meanwhile, local brands are gaining traction by focusing on "Australian-made" products, promoting vegan and ethical values, and building direct relationships with consumers. These strategies allow smaller players to secure loyal customer bases without relying on large-scale advertising campaigns.

Businesses are increasingly adopting omnichannel strategies to enhance customer engagement and expand their market presence. For instance, Adore Beauty has implemented AI-powered kiosks that offer personalized skincare recommendations from their wide online inventory. Chemist Warehouse is focusing on growing its physical store network while also offering competitive online price matching to attract more customers. Sephora has revamped its Melbourne flagship store by introducing features like hydrafacial zones and the country’s first Sephora Beauty School, showcasing the rising importance of experiential retail in attracting and retaining customers.

There are notable growth opportunities in areas such as men’s grooming tools, products made with indigenous botanical ingredients, and zero-waste refill stations. Unilever’s Clear scalp-care patents highlight how intellectual property can provide a competitive advantage in the market. Private equity firms are actively investing in emerging natural product brands. For example, Glow Capital Partners’ acquisition of Delta Labs has helped strengthen the brand’s marketing capabilities and expand its presence in international markets, demonstrating the potential for growth in this segment.

Australia Beauty And Personal Care Products Industry Leaders

-

Colgate-Palmolive Company

-

Unilever PLC

-

L'Oréal S.A.

-

Procter & Gamble Company

-

Kenvue Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Glow Capital Partners acquired Delta Labs, which expanded its portfolio of Australian beauty brands. This move highlighted the ongoing interest of private equity firms in the growing beauty and skincare market in Australia.

- December 2024: Vanessa Megan Naturaceuticals introduced a new haircare range crafted entirely from 100% natural ingredients. This launch expanded the brand's clean beauty offerings, reinforcing its commitment to sustainable and natural product innovation.

- April 2024: Rita Ora’s TYPEBEA hair care brand was launched in Australia, marking its entry into the market. The brand's introduction aimed to cater to the growing demand for premium hair care products in the region.

- June 2022: Shiseido, a Japanese cosmetics company, introduced Sidekick, a new range of skincare products for men. The range, which consists of four products and eight inventory items, is intended primarily for the Asian market.

Australia Beauty And Personal Care Products Market Report Scope

Beauty and personal care products generally belong to hygiene practices and rinse off immediately after use. These products encompass cosmetics, haircare, skincare, and cleaning products.

The Australian beauty and personal care products market report is segmented based on product type and distribution channel. The segmentation based on product type includes personal care products and cosmetics/make-up products. The personal care market is further segmented into hair care products (shampoo, conditioner, and other hair care products), skincare products (facial care products, body care products, and lip care products), bath and shower (shower gels, soaps, and other bath and shower products), oral care (toothbrushes, toothpaste, mouthwashes and rinses, and other oral care products), men's grooming products, and deodorants and antiperspirants. The cosmetics/make-up products market is segmented into facial cosmetics, eye cosmetics, lip and nail make-up products, and hairstyling and coloring products. By distribution channel, the market is segmented into specialist stores, supermarkets/hypermarkets, convenience stores, online retail channels, and other distribution channels.

The market sizing has been done in value terms in USD for all the above-mentioned segments.

By Product Type

| Personal Care Products | Hair Care | Shampoo |

| Conditioners | ||

| Other Products | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Other Products | ||

| Oral Care | Toothbrushes | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Other Products | ||

| Men's Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Cosmetics Products | Colour Cosmetics | Facial Make-up Products |

| Eye Make-up Products | ||

| Lip and Nail Make-up Products | ||

By Category

| Mass |

| Premium |

By Nature

| Organic |

| Conventional |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Channels |

| Other Channels |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioners | |||

| Other Products | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Other Products | |||

| Oral Care | Toothbrushes | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Other Products | |||

| Men's Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Cosmetics Products | Colour Cosmetics | Facial Make-up Products | |

| Eye Make-up Products | |||

| Lip and Nail Make-up Products | |||

| By Category | Mass | ||

| Premium | |||

| By Nature | Organic | ||

| Conventional | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Health and Beauty Stores | |||

| Online Retail Channels | |||

| Other Channels | |||

Key Questions Answered in the Report

What is the current value of the Australia beauty and personal care products market?

The market is valued at USD 9.24 billion in 2026 and is forecast to reach USD 12.19 billion by 2031.

Which category is growing fastest within Australia’s beauty sector?

Premium products are projected to grow at a 6.32% CAGR, outpacing the mass segment over 2026-2031.

How significant is online retail for Australian beauty purchases?

Online sales are expanding at a 7.02% CAGR, driven by AI-powered personalization and subscription services.

What fuels the rise of organic beauty products in Australia?

Consumers seek transparent ingredient lists and certified sustainability, helping organic lines grow at 6.95% CAGR.

Page last updated on: