Sustainable Personal Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

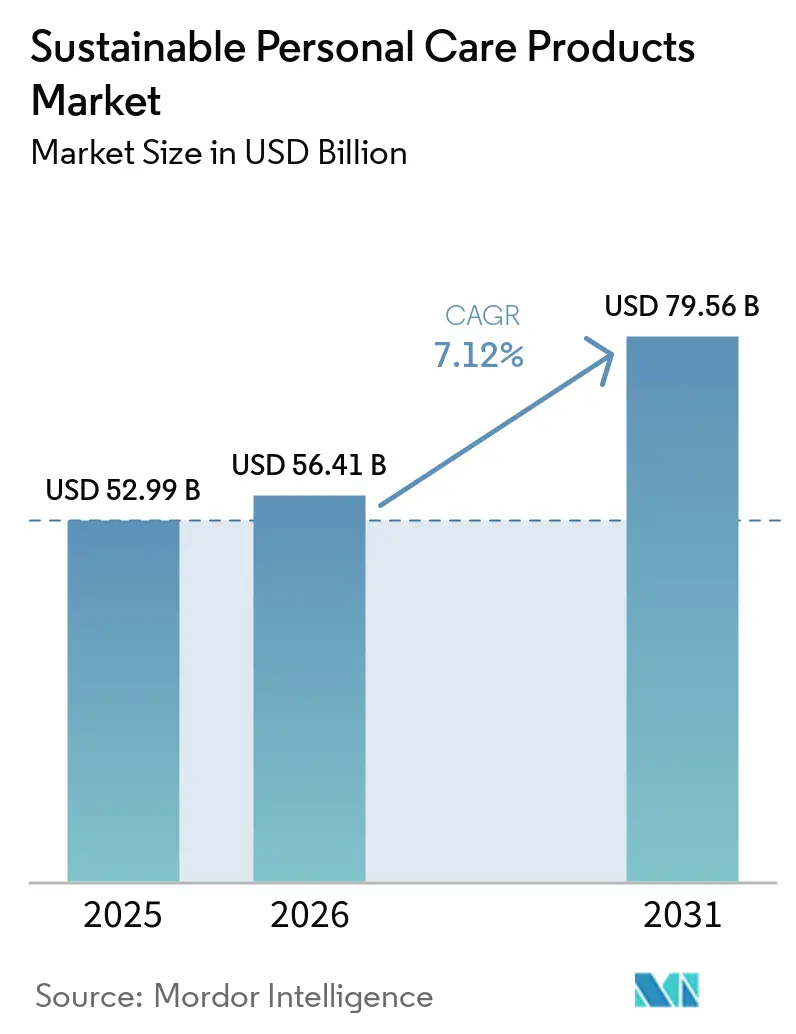

| Market Size (2026) | USD 56.41 Billion |

| Market Size (2031) | USD 79.56 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

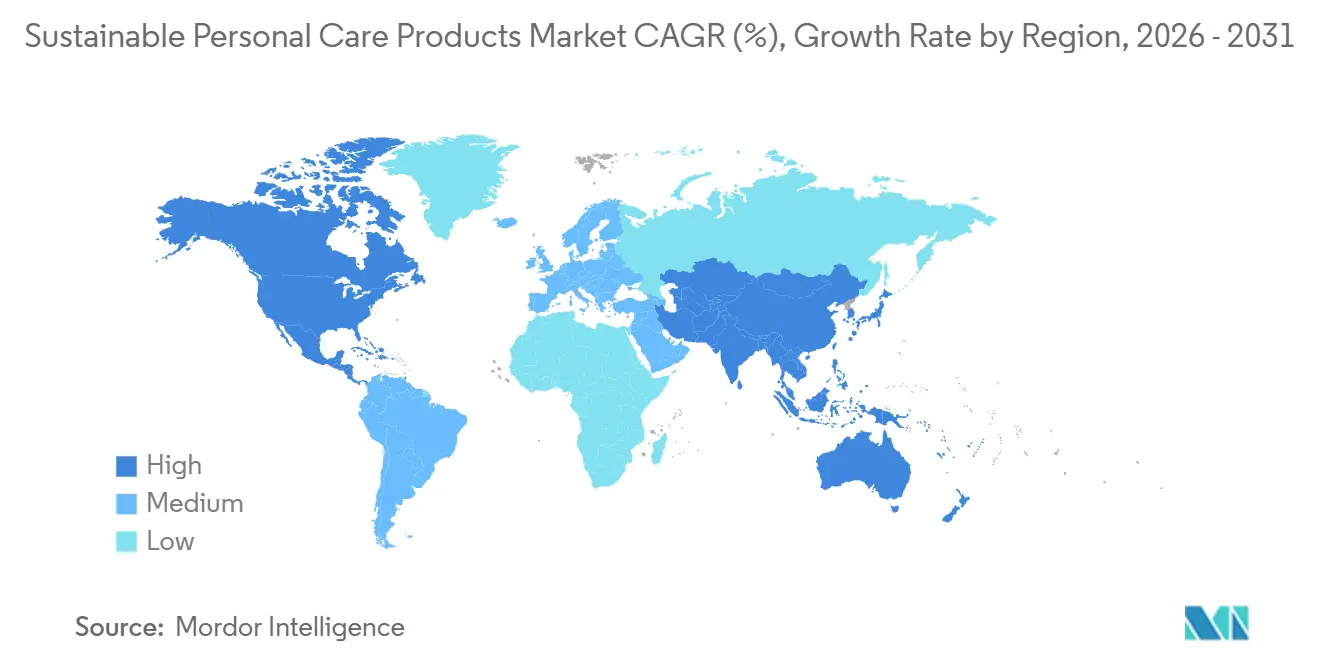

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sustainable Personal Care Products Market Analysis by Mordor Intelligence

The sustainable personal care products market size is expected to grow from USD 52.99 billion in 2025 to USD 56.41 billion in 2026 and is forecast to reach USD 79.56 billion by 2031 at 7.12% CAGR over 2026-2031. The category is expanding as buyers increasingly expect product performance, ingredient transparency, and packaging accountability to be integrated rather than treated as separate purchase criteria. Certification frameworks and clean ingredient standards are reinforcing this shift, raising the baseline for product credibility across both premium and mass channels. This trend keeps the sustainable personal care products market on a structural growth path, as the change is tied to routine buying behavior rather than a short-term consumer cycle. Large companies are responding through parallel initiatives, including reformulating established brands, strengthening disclosure practices, and adding newer sustainable labels to expand their reach across digital and store-led channels.

Key Report Takeaways

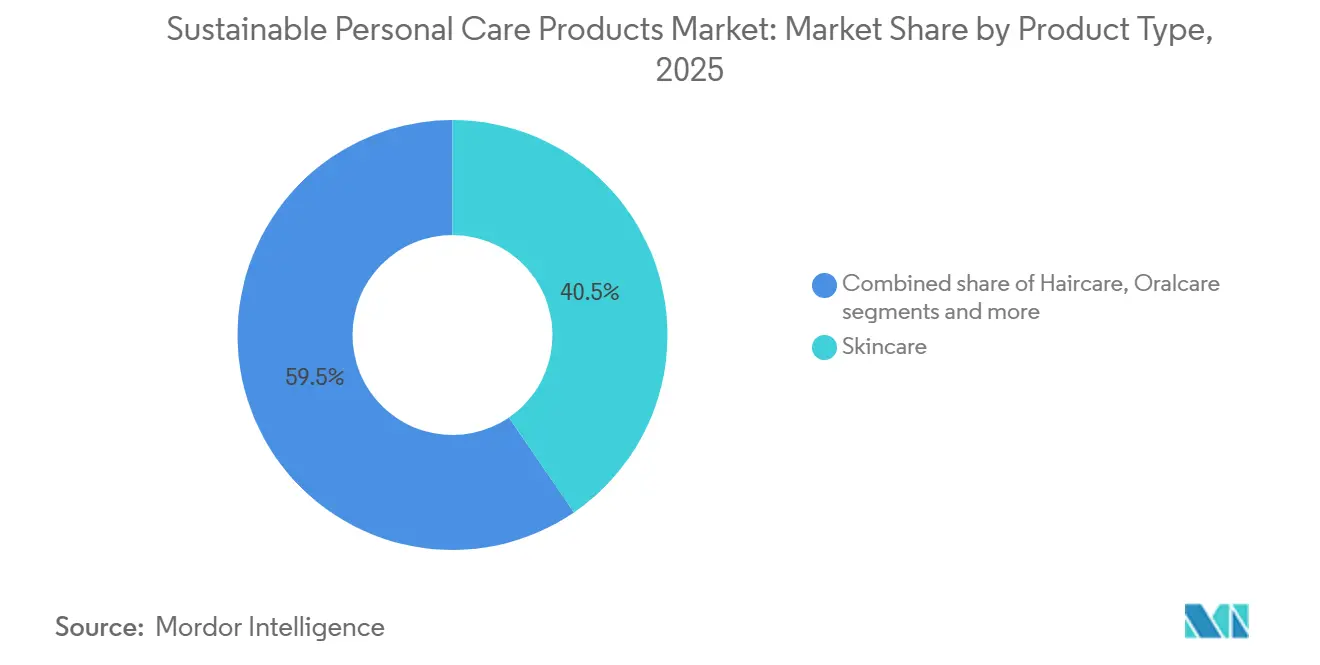

- By product type, skin care led with 40.45% revenue share in 2025, while hair care is forecast to expand at a 7.46% CAGR through 2031.

- By end user, women held 57.71% of the sustainable personal care products market share in 2025, while men recorded the highest projected CAGR at 7.69% through 2031.

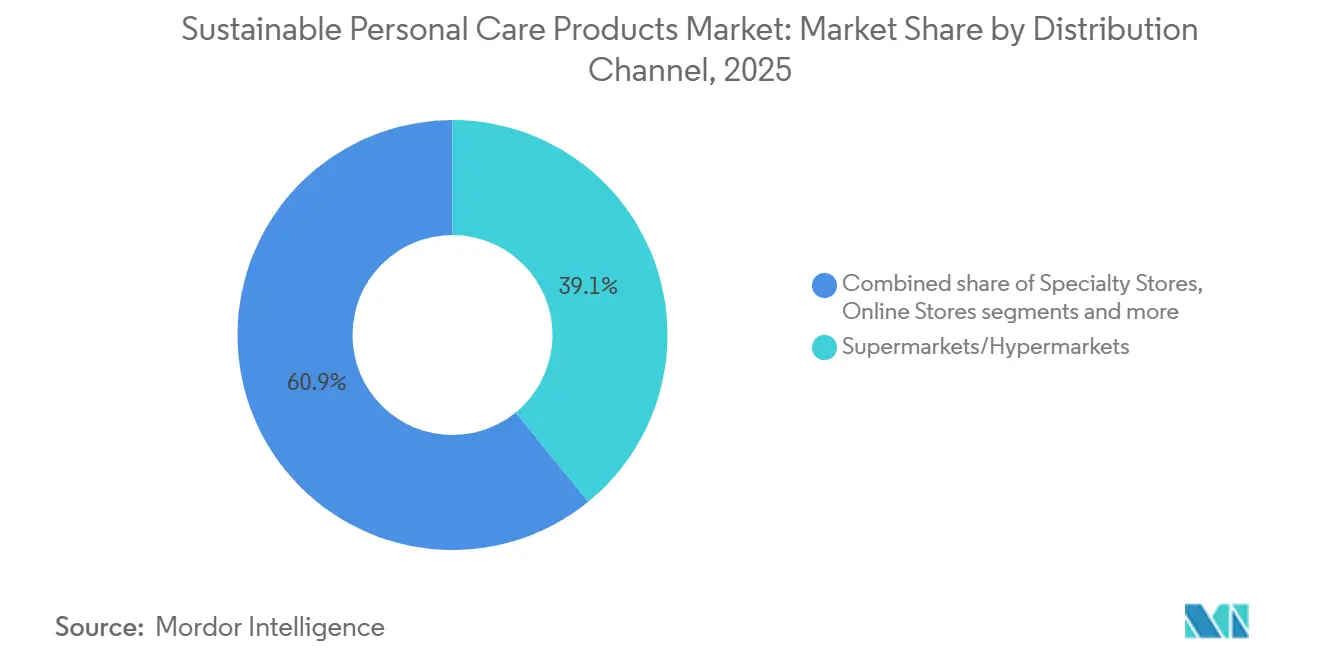

- By distribution channel, supermarkets and hypermarkets accounted for a 39.51% share of the sustainable personal care products market size in 2025, while online retail stores are advancing at an 8.11% CAGR through 2031.

- By geography, North America held 34.81% of the sustainable personal care products market share in 2025, while Asia-Pacific posted the fastest projected CAGR at 7.52% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sustainable Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for natural and eco-friendly personal care products | +2.5% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Growing awareness of environmental sustainability and plastic waste reduction | +1.5% | Global, with accelerating momentum in Asia-Pacific | Medium term (2-4 years) |

| Increasing demand for clean-label and non-toxic ingredient formulations | +1.2% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Expansion of vegan and cruelty-free beauty product adoption | +0.8% | North America and Europe core, Asia-Pacific emerging | Short term (≤ 2 years) |

| Government regulations promoting sustainable packaging and ingredient transparency | +0.6% | Europe North America, South Korea, Japan | Long term (≥ 4 years) |

| Rising disposable incomes supporting premium sustainable product purchases | +0.5% | Asia-Pacific, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for natural and eco-friendly personal care products

Growing awareness of environmental sustainability and health-conscious lifestyles is encouraging consumers to choose personal care products made with natural, plant-based, and biodegradable ingredients. Increasing concerns about the environmental impact of synthetic chemicals, plastic packaging, and resource-intensive manufacturing are accelerating the shift toward eco-friendly alternatives. Consumers are also placing greater value on cruelty-free, vegan, and ethically sourced formulations that align with their personal values. This trend has prompted manufacturers to expand their portfolios with clean-label products that emphasize ingredient transparency and sustainable packaging. As sustainability becomes a key purchasing criterion across global markets, demand for natural and eco-friendly personal care products continues to strengthen, supporting long-term market expansion.

Growing awareness of environmental sustainability and plastic waste reduction

Increasing public concern over environmental degradation and plastic pollution is encouraging the adoption of sustainable personal care products with minimal ecological impact. Consumers are actively seeking brands that use recyclable, biodegradable, refillable, or plastic-free packaging to reduce household waste. Governments, environmental organizations, and advocacy campaigns are also raising awareness about the harmful effects of single-use plastics, influencing purchasing behavior. In response, manufacturers are investing in innovative packaging solutions, such as paper-based containers, reusable systems, and compostable materials. Sustainability certifications and transparent environmental claims further strengthen consumer trust and brand loyalty.

Increasing demand for clean-label and non-toxic ingredient formulations

Growing consumer awareness of ingredient safety and product transparency is accelerating demand for clean-label and non-toxic personal care formulations. Buyers are increasingly avoiding products containing parabens, sulfates, phthalates, synthetic fragrances, and other potentially harmful chemicals in favor of formulations made with naturally derived and recognizable ingredients. According to research by the CBI, Ministry of Foreign Affairs, clean-label products are projected to constitute over 70% of product portfolios in 2025 and 2026, up from 52% in 2021, highlighting the rapid shift toward transparent product development[1]Source: CBI Ministry of Foreign Affairs, “Which trends offer opportunities”, cbi.eu. This trend is encouraging manufacturers to reformulate existing products and introduce safer, plant-based alternatives with clear ingredient labeling. Brands that emphasize non-toxic formulations, third-party certifications, and full ingredient disclosure are gaining stronger consumer trust.

Rising disposable incomes supporting premium sustainable product purchases

Higher disposable incomes across both developed and emerging economies are enabling consumers to spend more on premium sustainable personal care products. Eco-friendly formulations often carry higher prices due to responsibly sourced ingredients, ethical production practices, and sustainable packaging, making stronger purchasing power an important factor in market growth. For example, according to the International Monetary Fund (IMF), GDP per capita in the United Arab Emirates increased from USD 42.84 thousand in 2021 to USD 50.22 thousand in 2024, reflecting improved consumer spending capacity[2]Source: International Monetary Fund, “United Arab Emirates Database”, imf.org. As incomes rise, consumers are becoming more willing to invest in high-quality products that offer health, environmental, and ethical benefits. The combination of increasing purchasing power and growing sustainability awareness continues to support demand for premium sustainable personal care products.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs of sustainable raw materials and packaging | -1.2% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Premium pricing limiting adoption among price-sensitive consumers | -0.8% | South and Southeast Asia, South America, Middle East and Africa | Medium term (2-4 years) |

| Complex and costly regulatory compliance for sustainability certifications | -0.5% | Europe, North America | Long term (≥ 4 years) |

| Supply chain challenges in sourcing ethical and traceable ingredients | -0.6% | Global, concentrated in Southeast Asia and Africa sourcing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher production costs of sustainable raw materials and packaging

The use of sustainably sourced ingredients and environmentally friendly packaging significantly increases production costs for sustainable personal care manufacturers. Organic botanical extracts, certified natural raw materials, biodegradable packaging, recycled plastics, and refillable containers are generally more expensive than conventional alternatives due to limited supply, certification requirements, and complex sourcing processes. In addition, investments in sustainable manufacturing practices, ethical supply chains, and regulatory compliance further raise operational expenses. These higher costs are often passed on to consumers through premium pricing, which can reduce affordability and limit adoption in price-sensitive markets. As a result, elevated production costs continue to constrain the widespread adoption and profitability of sustainable personal care products.

Premium pricing limiting adoption among price-sensitive consumers

The premium pricing of sustainable personal care products remains a significant challenge for widespread market adoption, particularly in price-sensitive regions. Products made with organic ingredients, ethical sourcing practices, eco-friendly packaging, and certified formulations typically cost more than conventional alternatives, resulting in higher retail prices. While environmentally conscious consumers may be willing to pay a premium, many households continue to prioritize affordability over sustainability during purchasing decisions. This price gap limits repeat purchases and slows penetration into mass-market consumer segments. Manufacturers also face difficulties in balancing sustainability initiatives with competitive pricing without compromising product quality or profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skin Care Leads as Hair Care Advances with Scalp-First Innovation

By product type, skin care accounted for the largest revenue share of 40.45% in 2025, maintaining its leadership position within the sustainable personal care products market. The segment's dominance is driven by strong consumer demand for natural, organic, vegan, and clean-label skincare formulations that are perceived as safer and environmentally responsible. Rising awareness regarding skin health, ingredient transparency, and the harmful effects of synthetic chemicals has encouraged consumers to shift toward sustainable skincare products. Manufacturers continue to expand their portfolios with refillable packaging, biodegradable materials, plant-based ingredients, and cruelty-free certifications to align with evolving consumer preferences.

Hair care is projected to register the fastest growth during the forecast period, expanding at a CAGR of 7.46% through 2031. Growth is being fueled by increasing consumer preference for sulfate-free, silicone-free, and naturally derived shampoos, conditioners, hair oils, and styling products that minimize environmental impact. Rising concerns regarding hair damage, scalp health, pollution, and chemical exposure are encouraging consumers to adopt sustainable hair care solutions. Companies are investing heavily in innovative formulations featuring botanical extracts, biodegradable ingredients, water-efficient production processes, and recyclable packaging to differentiate their offerings.

By End User: Women Anchor Demand While Men Post the Fastest Growth

Women accounted for the largest share of the sustainable personal care products market within the segment, representing 57.71% of total revenue in 2025. The segment's leadership is primarily driven by higher adoption of skincare, hair care, personal hygiene, and beauty products among female consumers. Women generally demonstrate stronger awareness of ingredient safety, ethical sourcing, cruelty-free certifications, and environmentally friendly packaging, making them a key consumer group for sustainable personal care brands. Manufacturers continue to introduce premium organic, vegan, and plant-based product lines specifically designed to meet women's diverse beauty and wellness needs.

The men segment is projected to record the fastest growth during the forecast period, expanding at a CAGR of 7.69% through 2031. This growth is being driven by increasing awareness of personal grooming, skincare, beard care, and hair care among male consumers across both developed and emerging markets. Changing social perceptions regarding men's self-care and appearance have encouraged greater adoption of sustainable grooming products made with natural ingredients and eco-friendly packaging. Brands are responding by expanding dedicated men's product portfolios that include sulfate-free shampoos, organic face washes, natural deodorants, beard oils, and multifunctional grooming products.

By Distribution Channel: Physical Scale Holds While Online Retail Reshapes Brand Economics

By distribution channel, supermarkets and hypermarkets accounted for the largest share of the sustainable personal care products market, contributing 39.51% of total revenue in 2025. The segment's leadership is supported by its extensive retail presence, broad product assortment, and the convenience of one-stop shopping for everyday personal care needs. Consumers continue to prefer these retail formats because they offer access to multiple sustainable brands, competitive pricing, promotional discounts, and the opportunity to physically evaluate products before purchase. Retail chains have also expanded their shelves to include organic, vegan, cruelty-free, and eco-certified personal care products in response to rising consumer demand for sustainable alternatives.

Online retail stores are projected to witness the fastest growth during the forecast period, expanding at a CAGR of 8.11% through 2031. The rapid growth of e-commerce is driven by increasing internet penetration, widespread smartphone usage, and the growing preference for convenient digital shopping experiences. Consumers are increasingly purchasing sustainable personal care products online due to the availability of extensive product selections, detailed ingredient information, customer reviews, and easy price comparisons. Subscription services, personalized product recommendations, and direct-to-consumer brand strategies have further enhanced customer engagement and encouraged repeat purchases.

Geography Analysis

North America held the largest share of the sustainable personal care products market, accounting for 34.81% of global revenue in 2025. The region's leadership is driven by high consumer awareness regarding clean-label products, ethical sourcing, and environmental sustainability. Strong demand for organic skincare, natural hair care, vegan cosmetics, and cruelty-free personal care products has encouraged manufacturers to continuously expand their sustainable product portfolios. Well-established retail infrastructure, widespread e-commerce adoption, and the presence of leading global personal care companies further support market growth across the United States and Canada.

Asia-Pacific is projected to register the fastest CAGR of 7.52% through 2031, making it the most rapidly expanding regional market for sustainable personal care products. Rising disposable incomes, rapid urbanization, and a growing middle-class population are significantly increasing demand for eco-friendly beauty and personal care products across countries such as China, India, Japan, South Korea, and Southeast Asia. Around 54% of the global urban population, more than 2.2 billion people, live in Asia. By 2050, the urban population in Asia is expected to grow by 50% - an additional 1.2 billion people[3]Source: UN-Habitat, “Asia and the Pacific Region”, unhabitat.org. Consumers are becoming more conscious of natural ingredients, chemical-free formulations, and environmentally responsible packaging, driving higher adoption of sustainable products.

Europe is a mature, highly regulated market, driven by strong demand for organic, vegan, and environmentally certified personal care products, along with clean beauty trends and advanced recycling initiatives. In South America, rising consumer awareness, expanding retail networks, and demand for naturally derived products, particularly in Brazil and Argentina, support market growth. The Middle East and Africa region is growing steadily, driven by rising disposable incomes, urbanization, and wider availability of premium sustainable brands through modern retail and online channels.

Competitive Landscape

The sustainable personal care products market is highly fragmented, with competition distributed among multinational consumer goods companies, specialized natural beauty brands, regional manufacturers, and emerging direct-to-consumer startups. Leading companies compete by expanding their portfolios of organic, vegan, cruelty-free, biodegradable, and clean-label products to address evolving consumer preferences. Innovation remains a primary competitive strategy, with manufacturers investing heavily in plant-based formulations, sustainable ingredient sourcing, refillable packaging, and environmentally friendly manufacturing processes.

Strategic partnerships, mergers and acquisitions, and geographic expansion continue to shape the competitive dynamics of the market. Major players are acquiring niche sustainable beauty brands to strengthen their clean beauty portfolios and accelerate entry into fast-growing product categories. Companies are also collaborating with sustainable packaging providers, ingredient suppliers, and certification organizations to enhance product credibility and reduce environmental impact across the value chain.

Digital transformation has become another important competitive differentiator in the sustainable personal care products market. Companies are increasingly leveraging e-commerce platforms, direct-to-consumer sales channels, social media marketing, and influencer collaborations to improve brand visibility and consumer engagement. Personalized product recommendations, subscription services, and digital education campaigns regarding ingredient transparency and sustainability have enhanced customer loyalty and repeat purchases.

Sustainable Personal Care Products Industry Leaders

L'Oréal S.A.

The Estée Lauder Companies Inc.

Unilever PLC

Procter & Gamble Company

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Henkel expanded its Schwarzkopf consumer hair care portfolio with the launch of the KERATÎME™ Care & Styling range, introducing a new line powered by proprietary Multiplex Bonding Technology™ to strengthen hair, protect against damage, and support color retention. The collection includes Deep Repair, Color Protect, and Styling sublines and debuted exclusively through Walmart, reinforcing Henkel's strategy to expand its presence in the premium mass-market hair care segment.

- February 2026: Unilever's Dove launched its first refillable 72-hour antiperspirant range, introducing reusable aluminum cases with interchangeable refill cartridges to reduce packaging waste while maintaining premium product performance. The range combines 72-hour sweat and odor protection with Dove's signature skincare formulation and includes multiple starter kits and refill variants, supporting the company's circular packaging strategy and strengthening its position in the growing sustainable personal care and refillable deodorant segments.

- January 2026: Beiersdorf launched NIVEA Creme Natural Touch in Germany, the first line extension of its iconic blue tin, featuring a vegan formula with 99% natural-origin ingredients. Developed as part of the company's Climate Care strategy and Net Zero 2045 ambition, the product features a 99.9% biodegradable formula and packaging made from 95% recycled aluminum, reinforcing Beiersdorf's commitment to sustainable skincare innovation while preserving the trusted performance of the original NIVEA Creme.

Global Sustainable Personal Care Products Market Report Scope

Sustainable personal care products are personal hygiene and beauty products that are developed, manufactured, packaged, and distributed in ways that minimize environmental impact while promoting social and ethical responsibility throughout their lifecycle. The sustainable personal care products market is segmented by product type, end user, distribution channel, and geography. Based on product type, the market is segmented by skin care, hair care, bath and shower products, oral care, feminine care, sun care, and other product types. Based on end user, the market is segmented by men, women and children. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD).

| Skin Care |

| Hair Care |

| Bath and Shower Products |

| Oral Care |

| Feminine Care |

| Sun Care |

| Other Product Types |

| Men |

| Women |

| Children |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Sweden | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| New Zealand | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Skin Care | |

| Hair Care | ||

| Bath and Shower Products | ||

| Oral Care | ||

| Feminine Care | ||

| Sun Care | ||

| Other Product Types | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| New Zealand | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving demand for sustainable personal care products through 2031?

Demand is rising because buyers now expect product performance, ingredient transparency, and packaging accountability together, which supports a 7.12% CAGR from 2026 to 2031.

Which product category leads current revenue?

Skin care is the largest product category, with 40.45% share in 2025, supported by daily use patterns and continued innovation in bio-fermented and treatment-led formulas.

Which product area is growing the fastest?

Hair care is the fastest-growing product type, with a 7.46% CAGR through 2031, helped by scalp-focused routines and stronger interest in natural-origin actives.

Which buyer group is expanding the quickest?

Men are the fastest-growing end-user segment at a 7.69% CAGR through 2031, as eco-certified grooming routines become more normalized among younger consumers.

How important is online retail in this category?

Online retail stores are the fastest-growing distribution channel at an 8.11% CAGR, because they reduce shelf-access barriers for newer brands and support stronger product education.

Page last updated on: