United States Beauty And Personal Care Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

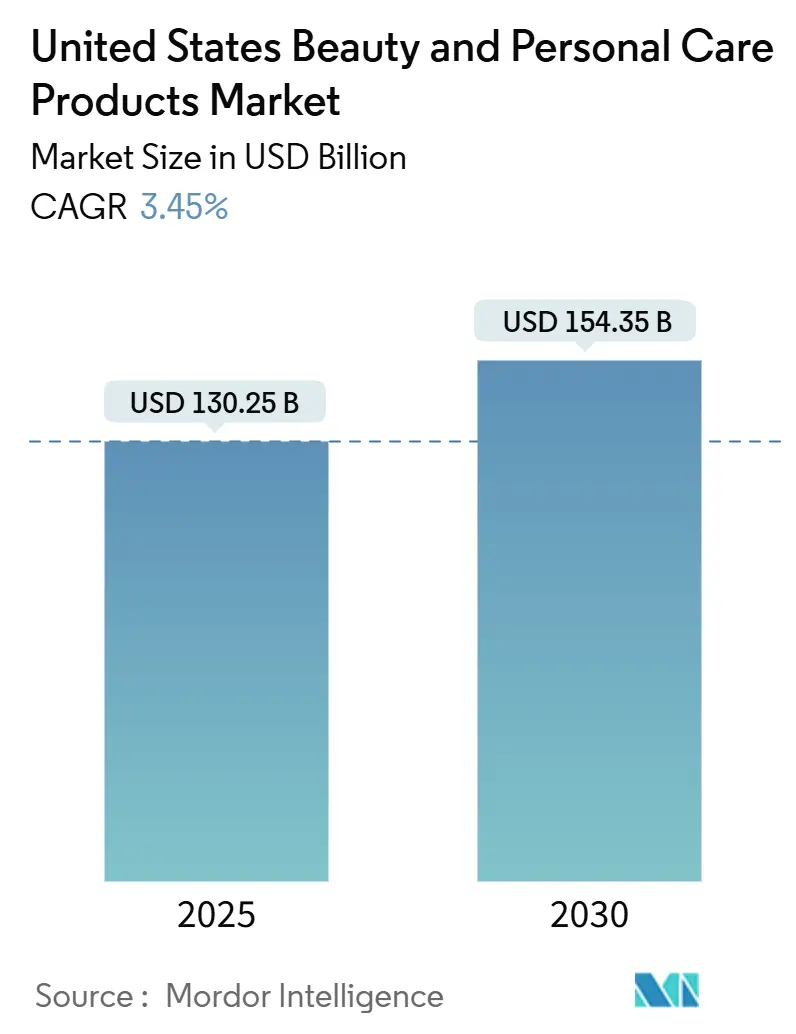

| Market Size (2025) | USD 130.25 Billion |

| Market Size (2030) | USD 154.35 Billion |

| Growth Rate (2025 - 2030) | 3.45% CAGR |

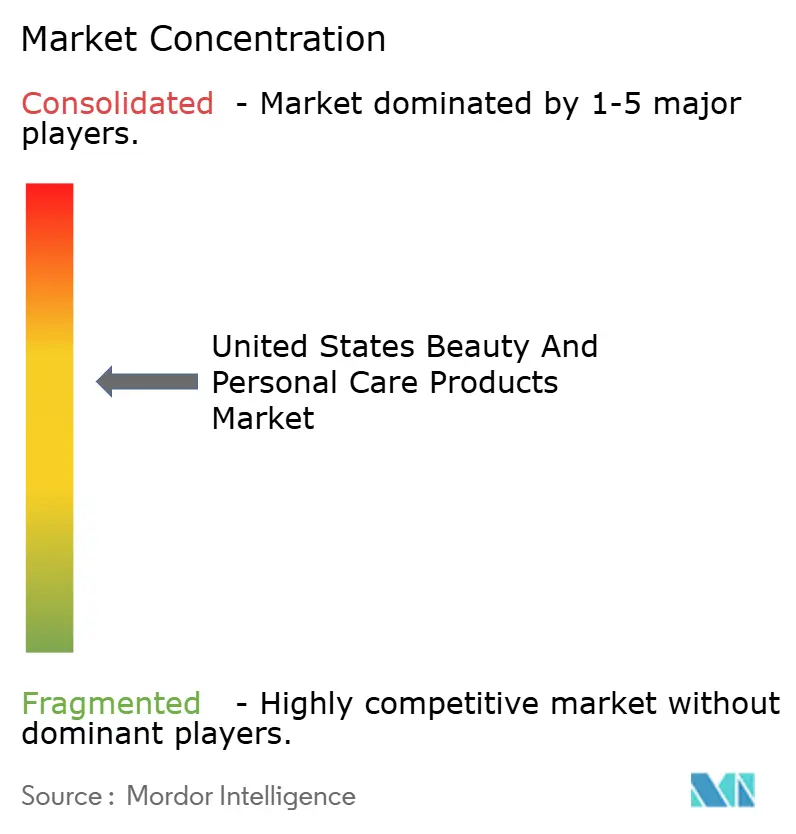

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The United States beauty and personal care products market size is estimated to be USD 130.25 billion in 2025 and is forecast to reach USD 154.35 billion by 2030, advancing at a 3.45% CAGR. The market's growth is fueled by several key factors, including increasing consumer awareness about personal grooming and hygiene, the rising influence of social media platforms and beauty influencers, and the growing preference for natural, organic, and sustainable products. Consumers are increasingly seeking products that align with their values, such as cruelty-free and eco-friendly options, which has prompted manufacturers to innovate and expand their product portfolios. Technological advancements in product formulations, such as anti-aging solutions and multifunctional products, are also driving demand. Additionally, the expansion of e-commerce platforms has significantly enhanced product accessibility, offering consumers a convenient shopping experience and a wide variety of choices. The rise of direct-to-consumer (DTC) brands and subscription-based models has further reshaped the market dynamics, providing personalized solutions and fostering brand loyalty. The premium segment within the beauty and personal care market is witnessing notable growth, driven by higher disposable incomes and a willingness among consumers to invest in high-quality products.

Key Report Takeaways

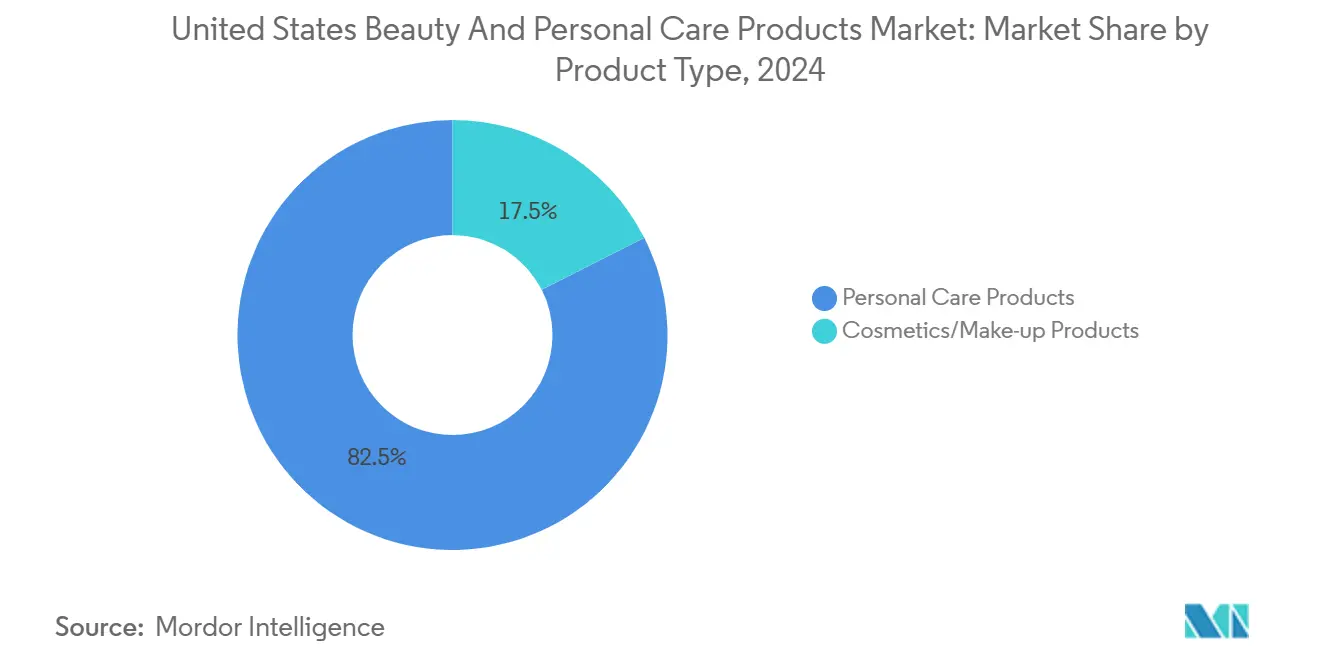

- By product type, personal care items dominated with 82.48% of the US beauty and personal care products market share in 2024 and are expanding at a CAGR of 4.23%

- By category, mass segment captured 70.41% of the US beauty and personal care products market size in 2024, whereas the premium segment is advancing at a 4.83% CAGR to 2030.

- By ingredient type, conventional/synthetic held 66.33% of the US beauty and personal care products market share in 2024, and natural/organic are forecast to grow at a 5.23% CAGR.

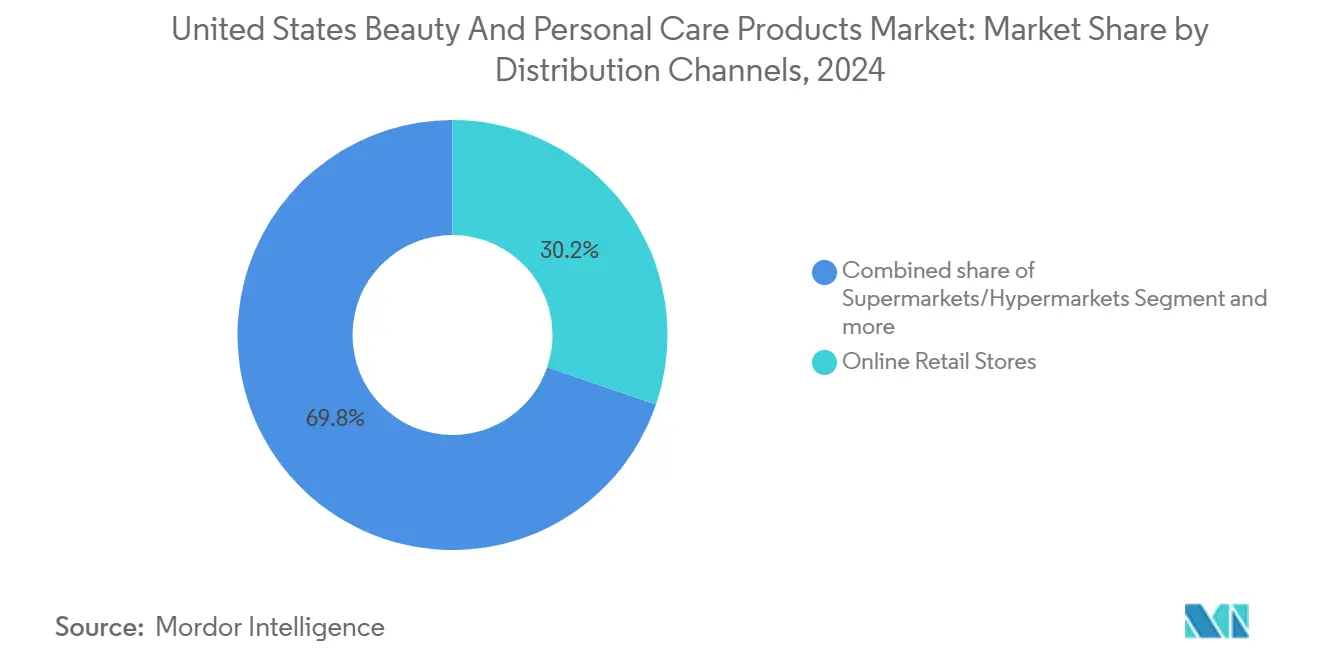

- By distribution channel, online retail held 30.23% of the US beauty and personal care products market size in 2024 and is expanding at a 5.92% CAGR.

United States Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in product formulations and ingredients | +0.8% | National, with concentration in California and New York | Medium term (2-4 years) |

| Expansion of premium beauty product segment | +0.6% | National, with higher penetration in urban markets | Long term (≥ 4 years) |

| Increasing male grooming product consumption | +0.4% | National, with early adoption in metropolitan areas | Medium term (2-4 years) |

| Increased personal care spending | +0.5% | National, driven by high-income demographics | Short term (≤ 2 years) |

| Growing aging population | +0.3% | National, with concentration in Florida, Arizona, and California | Long term (≥ 4 years) |

| Social media influence on beauty trends and product adoption | +0.7% | National, with higher impact among younger demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Innovation in Product Formulations and Ingredients

Innovation in product formulations and ingredients is a significant driver in the US beauty and personal care products market. Companies are increasingly focusing on developing products with unique formulations to cater to evolving consumer preferences. For instance, the demand for clean beauty products has led to the incorporation of natural and organic ingredients, such as aloe vera, shea butter, and essen tial oils, in skincare and haircare products. Additionally, brands are leveraging advanced technologies to create multifunctional products, such as moisturizers with SPF or foundations infused with skincare benefits. The rise of vegan and cruelty-free products has also prompted manufacturers to replace animal-derived ingredients with plant-based alternatives, such as squalane derived from sugarcane. These innovations not only address consumer demand for sustainable and ethical products but also help brands differentiate themselves in a competitive market.

Increasing Male Grooming Product Consumption

The increasing consumption of male grooming products is a significant driver of the United States beauty and personal care market. Over the years, there has been a noticeable shift in consumer behavior, with men becoming more conscious of their grooming routines. This growth is fueled by the rising demand for skincare, haircare, and beard grooming products among men. Among these, shampoos have emerged as a key factor in men's grooming, driven by the growing focus on hair health and hygiene. As per ITC Trade Map, the U.S. saw its shampoo imports surge from USD 357.5 million in 2021 to USD 482.9 million in 2024, highlighting the increasing demand for such products [1]Source: ITC Trade Map, Ïmport Value of Shampoos (HS Code:3305)", trademap.org. Additionally, the increasing influence of social media and celebrity endorsements has played a pivotal role in shaping male grooming trends. The availability of a wide range of products tailored specifically for men, coupled with growing awareness about personal hygiene and appearance, continues to drive this segment within the market.

Increased Personal Care Spending

The increasing expenditure on personal care products is a significant driver of the United States beauty and personal care products market. According to the Maine DECD Report, in 2024, consumers across the US spent approximately USD 74 billion on personal care products [2]Source: Maine Department of Economic and Community Development (DECD), "Consumer Spending Trends on Personal Care Products", maine.gov. Of this total, the largest share (47%) was allocated to cosmetics, including perfumes, skincare, and nail care. Consumers are allocating more of their disposable income toward personal grooming and self-care, driven by rising awareness of personal hygiene, appearance, and wellness. This trend is further supported by the growing influence of social media, which promotes beauty standards and encourages the adoption of premium and innovative personal care products. Additionally, the availability of a wide range of products catering to diverse consumer needs, including organic and sustainable options, has contributed to this surge in spending. The shift in consumer preferences toward high-quality and specialized products is expected to sustain the growth of the market during the forecast period.

Growing Aging Population

In the U.S., the expanding elderly demographic is significantly driving the demand for beauty and personal care products. As the senior population grows, there is an increasing focus on addressing age-related concerns, such as wrinkles, fine lines, skin elasticity, and hair thinning, through targeted solutions like anti-aging creams, serums, and specialized hair care products. This trend is further supported by data from the Population Reference Bureau Report, the number of Americans aged 65 and older is projected to increase from 58 million in 2022 to 82 million by 2050 (a 47% increase) [3]Source: Population Reference Bureau, "Fact Sheet-Ageing in the United States", prb.org. The aging population is not only seeking products that address these concerns but also prioritizing formulations that are gentle, effective, and cater to sensitive skin. This demographic evolution is encouraging manufacturers to invest in research and development, leading to the creation of innovative and specialized products tailored to the unique needs of older consumers. Consequently, this shift is playing a pivotal role in propelling the growth of the beauty and personal care products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns about packaging waste | -0.4% | National, with stricter regulations in California and Washington | Medium term (2-4 years) |

| Competition from counterfeit products | -0.3% | National, with higher impact in e-commerce channels | Short term (≤ 2 years) |

| Market saturation and intense competition | -0.5% | National, particularly in mass market segments | Long term (≥ 4 years) |

| Presence of toxic substances in cosmetics | -0.2% | National, with state-level regulatory variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Counterfeit Products

The market faces significant restraint due to the increasing prevalence of counterfeit products. These counterfeit goods not only undermine the revenue of legitimate manufacturers but also pose potential health risks to consumers. For instance, fake cosmetics, such as lipsticks and foundations, often contain harmful chemicals like lead and arsenic, which can cause severe skin reactions or long-term health issues. Additionally, counterfeit perfumes frequently use substandard ingredients, leading to poor quality and potential allergic reactions. The rise of e-commerce platforms has further exacerbated this issue, as counterfeiters exploit online marketplaces to distribute fake products under the guise of reputable brands. This challenge not only erodes consumer trust but also compels companies to invest heavily in anti-counterfeiting measures, such as advanced packaging technologies and authentication systems, to safeguard their brand integrity. Addressing this issue remains critical for the sustained growth of the United States' beauty and personal care products market.

Environmental Concerns About Packaging Waste

Packaging waste has emerged as a significant restraint in the market. The increasing use of single-use plastics and non-biodegradable materials in product packaging contributes to environmental degradation. For instance, many beauty products, such as shampoos, conditioners, and skincare items, are packaged in plastic containers that are not easily recyclable. This has led to growing concerns among environmentally conscious consumers, who are now demanding sustainable and eco-friendly packaging solutions. Additionally, regulatory bodies in the United States are implementing stricter guidelines to reduce plastic waste, further pressuring manufacturers to adopt sustainable practices. Companies like L'Oréal and Unilever have started introducing refillable packaging and biodegradable materials to address these concerns. However, the transition to sustainable packaging often increases production costs, posing challenges for smaller players in the market. This restraint highlights the need for innovation and investment in sustainable packaging technologies to align with consumer preferences and regulatory requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominance Drives Market Stability

In 2024, personal care items dominated the United States beauty and personal care products market, holding an 82.48% share. This dominance was driven by their everyday necessity and appeal across diverse demographics, making them an essential component of consumers' daily routines. Products such as skincare, haircare, and hygiene-related items contributed significantly to this segment's performance. The increasing focus on health and wellness, coupled with the rising demand for natural and organic personal care products, has further fueled the growth of this segment. Additionally, advancements in product formulations, such as the inclusion of active ingredients and multifunctional benefits, have enhanced consumer interest. The sub-segment is set to grow at a 4.23% CAGR, continuing through 2030, supported by increasing consumer awareness of personal grooming and hygiene, as well as the introduction of innovative and sustainable product offerings by key players in the market.

Cosmetic and makeup products also play a vital role in the United States' beauty and personal care products market. These products cater to a wide range of consumer preferences, including foundations, lipsticks, eyeliners, and other makeup essentials. The segment benefits from rising trends in self-expression, social media influence, and the growing demand for premium and organic cosmetic products. While not as dominant as personal care items, the cosmetic/makeup segment continues to exhibit steady growth, driven by evolving beauty standards and increasing disposable incomes.

By Category: Premium Segment Outpaces Mass-Market Growth

In 2024, mass offerings dominated the United States beauty and personal care products market, capturing 70.41% of total sales. This significant share highlights the widespread consumer preference for affordable and accessible products. Mass labels continue to cater to a broad audience by offering a variety of options that meet basic beauty and personal care needs at competitive price points. These products are often distributed through multiple retail channels, including supermarkets, drugstores, and online platforms, ensuring their availability to a diverse consumer base. The affordability and convenience of mass offerings make them a staple choice for consumers seeking value-driven solutions without compromising on essential functionality.

However, premium offerings are gaining traction, exhibiting a faster CAGR of 4.83%. This growth reflects a shift in consumer behavior, with individuals increasingly willing to trade up for products that promise proven efficacy and enhanced sensory experiences. Premium products often feature high-quality ingredients, advanced formulations, and sophisticated packaging, appealing to consumers who prioritize luxury and performance. Additionally, the rise of wellness trends and the growing focus on self-care have further fueled demand for premium beauty and personal care products. These offerings are frequently marketed through exclusive channels, such as specialty stores and high-end e-commerce platforms, targeting a more discerning and affluent customer segment.

By Distribution Channel: Online Retail Transforms Shopping Patterns

In 2024, online retail captured 30.23% of total sales and is projected to grow at a 5.92% CAGR. This growth is largely fueled by mobile-savvy consumers who demand seamless purchasing experiences and swift deliveries. Augmented reality try-ons are helping to minimize returns by allowing customers to visualize products before purchase, enhancing their confidence in buying decisions. Meanwhile, AI-driven chat advisors replicate the personalized guidance typically offered at beauty counters, providing tailored recommendations and improving customer engagement. Furthermore, influencer-led storefronts are adeptly transforming entertainment moments into actual purchases by leveraging their reach and credibility. As a result, e-marketplaces have emerged as the quickest and most efficient avenue for expansion in the U.S. beauty and personal care products sector.

Specialty chains defend traffic through fragrance bars, spa-style treatments, and exclusive capsule launches. Supermarkets and big-box stores depend on impulse checkout placements, yet increasingly add QR codes that link shelf items to digital tutorials. Direct-to-consumer subscriptions leverage data to curate replenishment and cross-sell. Each channel’s evolution underscores an omnichannel imperative that is reshaping inventory, merchandising, and marketing across the US beauty and personal care products market.

By Ingredient Type: Natural/Organic Acceleration Outpaces Conventional/Synthetic

Conventional/synthetic products continue to dominate consumer preferences. In 2024, this segment accounted for 66.33% of total sales, reflecting its widespread availability, affordability, and established presence in the market. These products are often favored for their consistent performance, longer shelf life, and cost-effectiveness, making them a staple choice for a broad consumer base. Additionally, the extensive marketing efforts by major brands and the continuous innovation in synthetic formulations have further solidified their position in the market. Despite growing awareness of natural alternatives, conventional and synthetic offerings remain a significant contributor to the market's overall revenue and are expected to maintain a strong presence in the coming years.

On the other hand, natural and organic products are gaining traction, driven by increasing consumer demand for sustainable and eco-friendly options. This segment is projected to grow at a faster CAGR of 5.23% through 2030, indicating a shift in consumer preferences toward healthier and environmentally conscious choices. Factors such as rising awareness of ingredient transparency, the perceived benefits of natural formulations, and the growing influence of clean beauty trends are fueling this growth. Moreover, the expansion of distribution channels, including e-commerce platforms and specialty stores, has made natural and organic products more accessible to consumers.

Geography Analysis

The United States beauty and personal care products market exhibits significant regional variations influenced by demographic profiles, regulatory frameworks, and cultural preferences. California stands out as a leader in market innovation and regulatory advancements. The state has implemented landmark legislation, such as the Toxic-Free Cosmetics Act and SB 54 packaging requirements, which have set national benchmarks and influenced industry-wide practices. These regulations reflect California's proactive approach to addressing consumer safety and environmental concerns, positioning the state as a trendsetter in the market.

California's unique market dynamics are further shaped by its concentration of technology companies and the entertainment industry, which drive demand for premium and innovative beauty products. The state's environmentally conscious population has also accelerated the adoption of sustainable packaging solutions and clean beauty formulations. These factors collectively make California a critical market for brands aiming to align with emerging consumer preferences and regulatory standards. Meanwhile, New York continues to play a pivotal role in the industry, serving as a hub for major corporate headquarters and a testing ground for luxury and premium product launches. Its diverse consumer base and global influence make it a strategic location for market expansion and innovation.

Regional regulatory disparities across the United States add complexity for national brands operating in the beauty and personal care market. States such as Washington, California, Colorado, and Minnesota have introduced stricter chemical restrictions, effectively setting de facto national standards. This is primarily due to the logistical and financial challenges of maintaining separate formulations for different states. As a result, brands are compelled to adapt to these stringent regulations, which often shape product development and marketing strategies on a national scale. These regional dynamics underscore the importance of understanding local market conditions and regulatory landscapes to succeed in the U.S. beauty and personal care market.

Competitive Landscape

The United States beauty and personal care products market demonstrates a moderate consolidation. Established multinational corporations, such as L'Oréal S.A., The Estée Lauder Companies Inc., and Procter and Gamble Company, continue to dominate the market, leveraging their extensive resources and brand equity. However, these traditional players are facing increasing competition from agile direct-to-consumer brands and social commerce disruptors, which are rapidly gaining traction among younger, tech-savvy consumers. This shift is reshaping the competitive landscape, compelling established companies to adapt their strategies to maintain their market share.

Traditional beauty giants are adopting a dual approach to navigate this evolving market. On one hand, they are heavily investing in research and development to enhance their product offerings and integrate advanced biotechnology capabilities. These investments aim to meet the growing consumer demand for innovative, sustainable, and personalized beauty solutions. On the other hand, these companies are actively acquiring emerging brands to diversify their portfolios and gain access to new consumer segments. Such acquisitions also enable them to expand their presence in alternative distribution channels, including e-commerce and social commerce platforms, which are becoming increasingly important in the current market dynamics.

Meanwhile, the rise of direct-to-consumer brands and social commerce disruptors is intensifying competition. These newer entrants are leveraging digital platforms and influencer marketing to build strong connections with consumers, particularly Millennials and Gen Z. Their ability to quickly adapt to changing trends and offer niche, customizable products has allowed them to carve out a significant share of the market. As a result, the US beauty and personal care products market is witnessing a dynamic interplay between traditional powerhouses and emerging challengers, driving innovation and reshaping consumer expectations.

United States Beauty And Personal Care Products Industry Leaders

-

L'Oréal S.A.

-

The Estee Lauder Companies Inc.

-

Procter and Gamble Company

-

Unilever PLC

-

Shiseido Company, Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: L'Oréal S.A. invested USD 160 million to establish its North America Research and Innovation Center in Clark, New Jersey. The facility, which encompassed 250,000 square feet, became L'Oréal's largest research and development center outside France. It incorporated modular laboratories, consumer testing facilities, and a mini-factory for product scaling. The center employed more than 600 scientists and focused on developing personalized beauty solutions and sustainability initiatives.

- February 2025: Estée Lauder Companies established a partnership with Serpin Pharma to research anti-inflammatory applications in cosmetics. The collaboration utilized Serpin's biotechnology, which demonstrated effectiveness in reducing inflammation and enhancing cell resilience for longevity-focused skincare ingredients.

- February 2025: Dove introduced the Density Boost range for hair thinning. The product launch aligned with the company's strategy to address the increasing consumer demand for scalp-care products, as consumer preferences shifted from facial care to hair and scalp health solutions.

- May 2024: Deos Hair Care introduced a Hair Growth Shampoo and Conditioner for consumers who experienced thinning hair and hair loss. The products were free from parabens, sulfates, and aluminum, and contained caffeine, biotin, rosemary oil, keratin, castor seed oil, and panthenol. These ingredients helped strengthen and revitalize hair while blocking DHT.

United States Beauty And Personal Care Products Market Report Scope

| Personal Care Products | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colourant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Others | ||

| Men's Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Make-up Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Make-up Products | ||

| Premium Products |

| Mass Products |

| Natural and Organic |

| Conventional/Synthetic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioner | |||

| Hair Colourant | |||

| Hair Styling Products | |||

| Others | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Others | |||

| Oral Care | Toothbrush | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Others | |||

| Men's Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Make-up Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Make-up Products | |||

| By Category | Premium Products | ||

| Mass Products | |||

| By Ingredient Type | Natural and Organic | ||

| Conventional/Synthetic | |||

| By Distribution Channel | Specialty Stores | ||

| Supermarkets/Hypermarkets | |||

| Online Retail Stores | |||

| Other Channels | |||

Key Questions Answered in the Report

What is the current value of the US beauty and personal care products market?

The market is worth USD 130.25 billion in 2025 and is projected to climb to USD 154.35 billion by 2030 at a 3.45% CAGR.

Which product category holds the largest share?

Personal care items account for 82.48% of 2024 spending, driven by daily-use essentials and rising male grooming routines.

Why is premium beauty growing faster than mass products?

Premium growth at a 4.83% CAGR stems from consumer focus on proven efficacy, biotech advances, and the perceived value of prestige self-care even during economic volatility.

How important is e-commerce to category sales?

Online retail already captures 30.23% of revenue and is the fastest-growing channel at 5.92% CAGR, propelled by social-commerce platforms and virtual try-on tools.

Page last updated on: