France Beauty And Personal Care Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

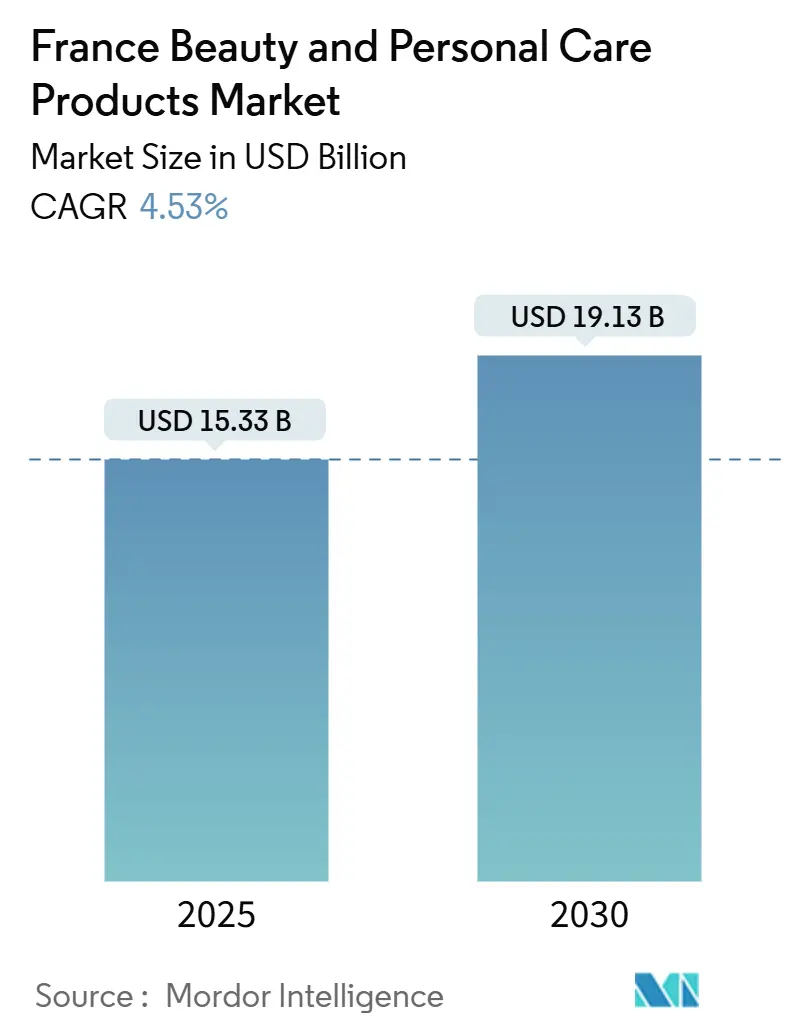

| Market Size (2025) | USD 15.33 Billion |

| Market Size (2030) | USD 19.13 Billion |

| Growth Rate (2025 - 2030) | 4.53% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The France beauty and personal care products market size is USD 15.33 billion in 2025 and is forecast to reach USD 19.13 billion by 2030, reflecting a 4.53% CAGR through the period. Strong brand heritage, rising male-grooming adoption, and a cultural attachment to daily beauty rituals sustain demand even while inflation constrains household budgets, confirming the “lipstick effect” in French retail behavior. Digital discovery via TikTok and Instagram accelerates product cycles, yet brick-and-mortar specialists preserve traffic by offering professional advice and experiential retailing. Regulatory leadership, exemplified by France’s 2026 PFAS ban, forces rapid reformulation and favors brands prepared to certify clean ingredient lists. Counterfeit trade and macroeconomic uncertainty temper the outlook, but persistent premiumization, ingredient transparency, and science-backed innovation position the France personal care and cosmetics market for steady value expansion.

Key Report Takeaways

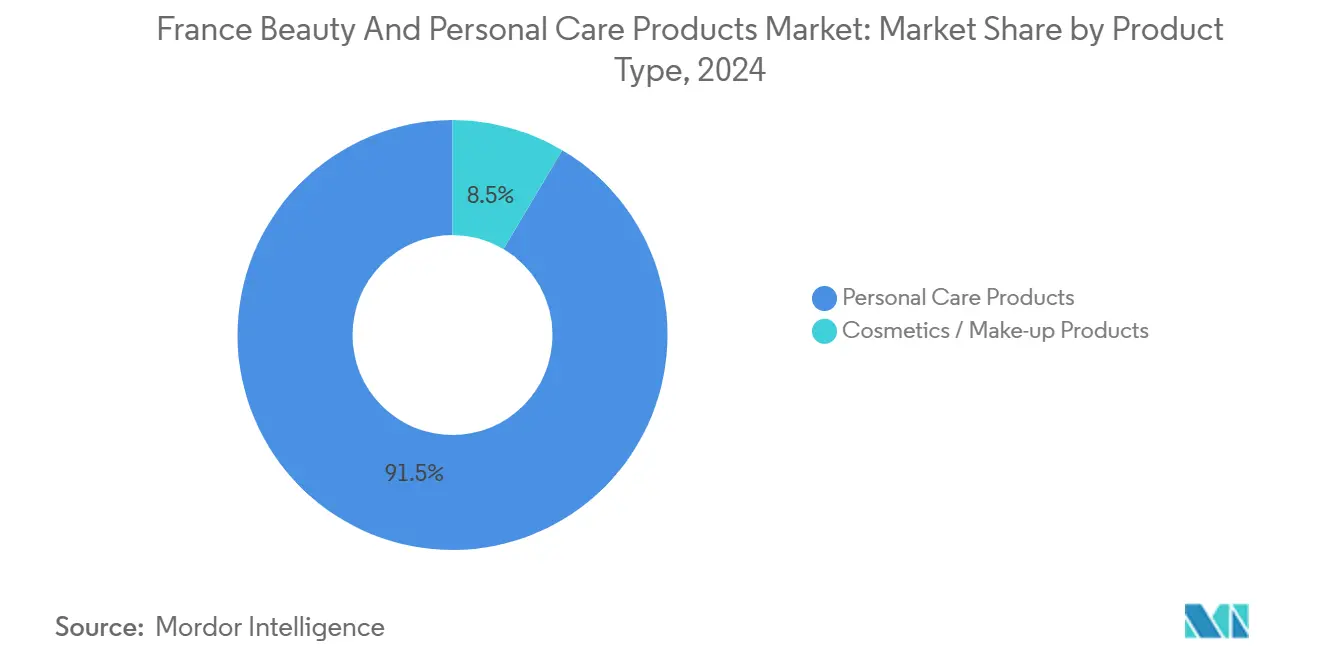

By product type, personal care products held 91.57% market share in 2024 and will compound at 4.47% CAGR to 2030.

By category, mass products led with a 53.70% share in 2024, while the premium segment is projected to advance at a 5.52% CAGR through 2030.

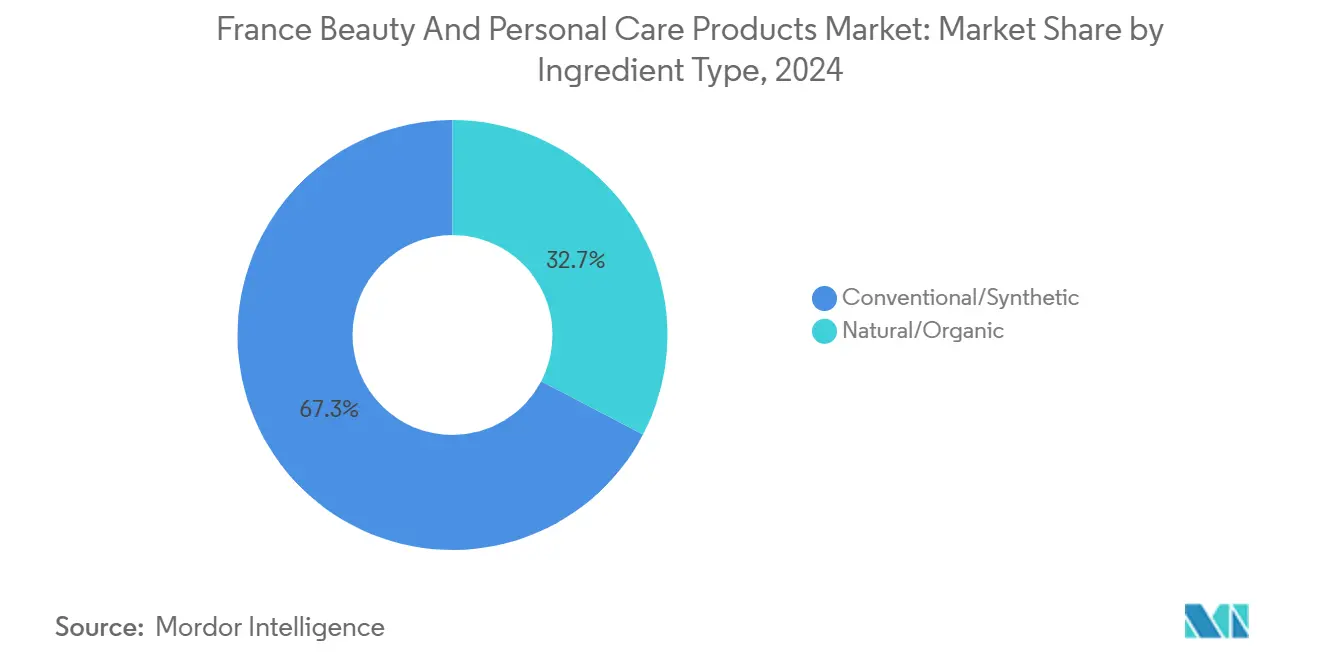

By ingredient type, conventional/synthetic items accounted for 67.34% of the 2024 share, whereas natural/organic formulations expanded fastest at 6.93% CAGR for 2025-2030.

By distribution channel, Supermarkets/ Hypermarkets commanded a 35.21% share in 2024; online retail stores are expected to grow at a 5.90% CAGR.

France Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing male grooming segment boosts sales | +0.8% | France, with spillover to Europe | Medium term (2-4 years) |

| High consumer awareness of skincare and grooming | +1.2% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Innovative product launches cater to diverse needs | +0.9% | Global, with France as innovation hub | Short term (≤ 2 years) |

| Strong preference for natural and organic products | +1.1% | France leading Europe adoption | Medium term (2-4 years) |

| Cultural emphasis on personal aesthetics and elegance | +0.7% | National French cultural trait | Long term (≥ 4 years) |

| Influence of social media and beauty influencers | +0.6% | Global with local French adaptation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing male grooming segment boosts sales

The growth of men's grooming products is primarily driven by younger male consumers who view grooming as an essential part of their wellness routine. The shift in consumer behavior indicates a fundamental change in how men approach personal care, moving beyond traditional grooming products to advanced skincare solutions. This demographic represents significant lifetime value potential, comparable to or exceeding female consumer segments, as they tend to maintain consistent grooming habits throughout their lives. Companies offering effective skincare products at competitive prices can capitalize on this emerging market segment, where consumer preferences and category standards are still developing. The market presents opportunities for brands to establish themselves as category leaders by introducing innovative products and setting new benchmarks in male grooming. For instance, in June 2024, the French Essence brand launched a range of men's grooming products that include shaving foam, cream, and other products.

High consumer awareness of skincare and grooming

French consumers demonstrate a strong understanding of skincare ingredients and their effectiveness, driving demand for products with proven clinical results and clear formulation details. This knowledge influences premium product preferences as consumers focus on quality and measurable outcomes. The market leverages France's pharmaceutical background, with consumers preferring dermatologically-tested products and those endorsed by healthcare professionals. Brand and regulatory education programs improve consumer understanding, resulting in informed purchases and increased spending on scientifically validated products. Owing to the rising awareness, the market players are launching new products in the market. In May 2024, L'Oreal SA launched 6 new skincare innovations in Paris. The innovation includes Gen Ai beauty labs and others for a more personalized skincare experience.

Innovative product launches cater to diverse needs

Artificial intelligence and augmented reality technologies support both shade matching capabilities and supply chain optimization in the beauty industry. These digital tools analyze customer preferences, skin tones, and product compatibility to provide accurate recommendations. L'Oréal's Beauty Genius AI analyzes customer data to recommend products while identifying slow-moving inventory for price reduction or product reformulation. The system processes historical purchase patterns, seasonal trends, and regional preferences to optimize stock levels across distribution networks. This consumer-focused technology also improves back-office operations by streamlining inventory management, reducing waste, and enhancing demand forecasting accuracy. The integrated approach reduces the return period on digital investments and enables new initiatives in virtual fragrance testing and touch-based product sampling. These innovations allow beauty companies to test new digital concepts while maintaining operational efficiency.

Strong preference for natural and organic products

The increasing consumer preference for natural and organic formulations aligns with the growing trend of wellness and environmental awareness. Consumers are becoming increasingly aware of the potential health risks associated with synthetic ingredients and are actively seeking products with natural alternatives. Rising concerns about synthetic ingredients in the country have prompted market players to develop new products that meet this demand. The shift toward natural formulations is particularly evident in personal care products, where consumers scrutinize ingredient lists more carefully. For instance, in June 2025, French brand Mircea introduced three shower gels: cypress and eucalyptus, fig and peppermint, and cedarwood and rosemary, which are also suitable for use on hands and face. Advancements in biotechnology have enabled companies to develop natural alternatives to synthetic ingredients, improving the efficacy and stability of natural formulations while maintaining their eco-friendly properties.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Counterfeit products erode brand trust | -0.9% | National with cross-border implications | Medium term (2-4 years) |

| High competition and market penetration | -0.7% | National market saturation | Long term (≥ 4 years) |

| Stringent EU regulations on cosmetics | -0.5% | EU-wide with France compliance focus | Short term (≤ 2 years) |

| Economic uncertainty and inflation | -0.8% | National economic conditions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit products erode brand trust

Counterfeit cosmetics pose a significant challenge to market integrity. These products contain harmful ingredients that can cause adverse reactions in consumers, potentially damaging the brand's reputation and eroding consumer trust. The impact extends beyond immediate financial losses, with the European Union Intellectual Property Office reporting approximately 32,000 job losses in the EU cosmetics sector due to counterfeit competition[1]European Union Intellectual Property Office, “Counterfeit Cosmetics Study,” euipo.europa.eu. E-commerce platforms face challenges in identifying and removing counterfeit listings, while advanced packaging replication makes it increasingly difficult for consumers to distinguish genuine products. Companies must allocate substantial resources to authentication technologies, legal enforcement, and consumer awareness programs, reducing investments in product development and market expansion.

Economic uncertainty and inflation

The reduced purchasing power of French households, despite government economic support measures, has created downward pressure on consumer spending. This economic challenge stems from several factors, including rising inflation, increasing energy costs, and heightened market uncertainty. Cosmed's 2024 annual report reveals that 70% of women spend less than USD 58.95 per month on facial care products, reflecting budget constraints that affect premium product segments[2]Cosmed, “French Consumer Spending Survey 2024,” cosmed.fr. The "lipstick effect" partially offsets this trend, as consumers continue to purchase beauty products as affordable luxuries during economic challenges, although they often opt for lower-priced alternatives. This consumer behavior demonstrates the resilience of the beauty market, even as purchasing patterns shift toward more economical options. Manufacturers face pressure from rising raw material and packaging costs, requiring them to balance price adjustments with maintaining sales volume, which impacts profit margins and reduces funds available for innovation and marketing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominance Drives Market Expansion

Personal Care Products hold a 91.57% market share in 2024, as French consumers prioritize essential daily-use items over cosmetics. The segment is projected to grow at a 4.47% CAGR from 2025 to 2030, supported by expanding subcategories. The skin care subsegment advances through personalized formulations, with companies using AI and bioprinting technologies to develop targeted solutions for various skin conditions. The men's grooming products subsegment is experiencing strong growth as male consumers adopt comprehensive skincare routines that extend beyond shaving products.

Bath and shower products sustain growth through premium offerings, while oral care focuses on natural ingredients and sustainable packaging solutions. Deodorants and antiperspirants manufacturers adapt to ingredient regulations, creating market opportunities for compliant formulations. The smaller cosmetics/make-up products segment is expected to grow through social media influence and post-pandemic recovery, particularly in eye cosmetics and lip and nail makeup products, which appeal to younger consumers seeking self-expression.

By Category: Premium Segment Accelerates Despite Economic Pressures

Premium products demonstrate steady growth with a 5.52% CAGR (2025-2030), while Mass products maintain market leadership with a 53.70% share in 2024. French consumers are increasingly choosing premium products, especially in skincare, where product effectiveness justifies higher prices. During economic uncertainty, the "lipstick effect" supports this trend as consumers opt for fewer, high-quality items rather than multiple lower-priced products.

Mass products maintain their dominant position through widespread availability in hypermarkets and supermarkets. However, the segment faces competition from expanding private label offerings, as retailers like Carrefour develop their cosmetics lines for price-sensitive consumers. The market dynamic creates opportunities for brands offering premium-quality formulations at moderate prices through "mass prestige" positioning. Mass brands compete with premium alternatives by focusing on packaging innovation, ingredient transparency, and sustainability while maintaining competitive pricing for cost-conscious consumers.

By Ingredient Type: Natural Transformation Reshapes Formulation Strategies

Conventional/synthetic products retain a dominant 67.34% market share in 2024 despite growing regulatory and consumer pressures. The segment maintains its position through established supply chains, proven efficacy, and cost advantages that appeal to price-sensitive consumers. The market increasingly rewards companies that effectively combine natural and synthetic ingredients, utilizing biotechnology to develop hybrid formulations that balance the safety of natural ingredients with the performance benefits of synthetics.

Natural/organic products demonstrate the strongest growth trajectory, with a 6.93% CAGR (2025-2030), driven by regulatory changes and an increasing consumer preference for clean formulations. France's implementation of the PFAS ban in cosmetics, starting January 2026, prompts manufacturers to accelerate their reformulation efforts by removing synthetic chemicals under regulatory review. Companies that transition to natural alternatives before broader EU implementation gain competitive advantages in the market.

By Distribution Channel: Digital Integration Transforms Retail Landscape

Supermarkets/ Hypermarkets hold the largest market share at 35.21% in 2024, highlighting the availability of various brands' products in beauty purchases. Supermarkets/hypermarkets face competition from specialized channels; they maintain their position through convenience and impulse purchase opportunities. The retail landscape favors businesses that integrate multiple channels, offering click-and-collect services, personalized digital experiences, and expert consultation. France's retail sector, comprising over 450,000 firms with a turnover of USD 638 billion, enables beauty brands to reach consumers through various distribution channels.

Online retail stores are projected to grow at a 5.90% CAGR (2025-2030), driven by the increased digital adoption that began during the pandemic. French B2C e-commerce reached USD 155 billion, with an annual growth rate of 13%, according to data from the International Trade Administration for 2024. Beauty products accounted for 40% of online purchases. This growth stems from enhanced digital experiences, including virtual try-on technologies, personalized recommendations, and omnichannel integration between online and offline shopping.

Geography Analysis

France’s beauty culture permeates daily routines, with Paris setting global style cues that ripple to provincial cities. Premium uptake is concentrated in Île-de-France, where disposable incomes can afford high-end serums. Provence and Occitanie anchor natural-ingredient supply chains, with farms that cultivate lavender, rosemary, and clary sage, which supply local brands. Coastal regions favor sun-care SKUs with high SPF and marine-safe filters, influenced by eco-tourism regulations protecting the Mediterranean.

E-commerce penetration peaks in urban zones connected by high-speed fiber, yet rural consumers also engage through mobile marketplaces, valuing doorstep delivery where physical stores are sparse. The PFAS ban positions domestic formulators as first movers within the EU, and export-oriented SMEs already market “PFAS-free” badges in Asia and North America, thereby elevating the reputation of the French personal care and cosmetics market abroad.

Macroeconomic divergence across regions shapes channel strategy: Northern industrial areas, facing higher unemployment, gravitate toward mass value packs, while southern resort towns sustain luxury fragrance sales, boosted by tourist spending. Government data forecasts a 0.7% uplift in national purchasing power for 2025, mitigating inflation’s bite and supporting incremental premium trading in mature urban clusters, according to the INSEE data[3]INSEE, “Household Purchasing Power Forecast 2025,” insee.fr.

Competitive Landscape

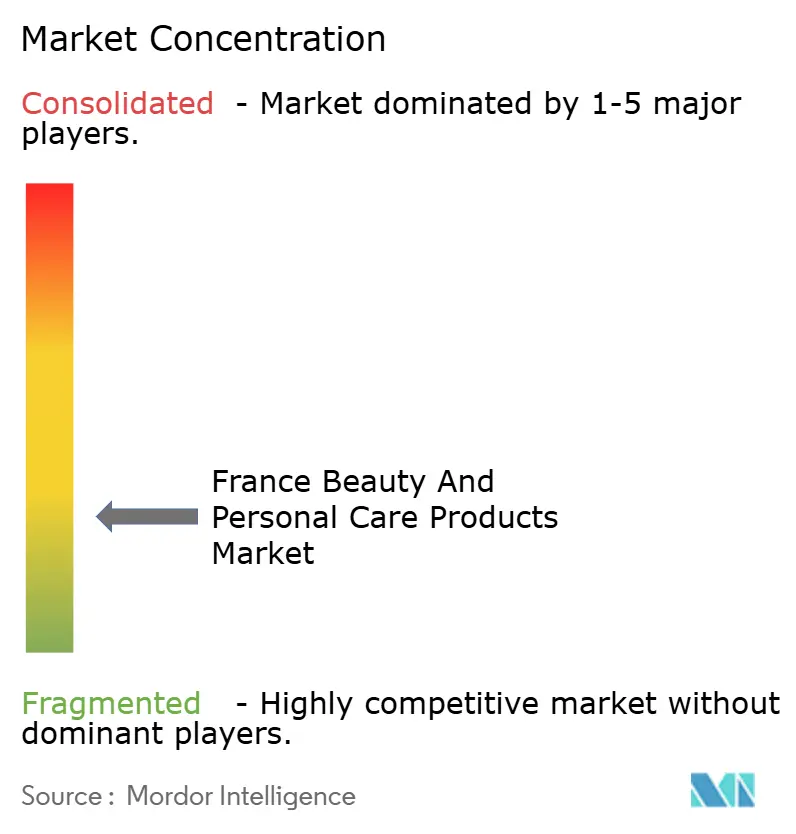

The French personal care and cosmetics market exhibits low concentration, indicating significant market fragmentation. This structure creates opportunities for both established players and emerging brands to gain market share. The competitive landscape encompasses a diverse range of product categories, price points, and distribution channels, with no single company dominating all segments. Major multinational corporations, such as L'Oréal S.A., Unilever PLC, Procter & Gamble Company, Beiersdorf AG, and The Estée Lauder Companies Inc., operate alongside specialized French brands and emerging indie companies in a dynamic environment where innovation and consumer engagement drive success.

Companies are increasingly focusing on technology integration and personalization as key competitive advantages in the French market. L'Oréal's partnerships with IBM for AI-powered formulation tools and Microsoft for generative AI applications demonstrate how established companies leverage technology to enhance innovation cycles. The integration of advanced technologies enables companies to develop more sophisticated products and deliver improved consumer experiences. These technological advancements have become crucial differentiators in the competitive landscape, particularly for established players seeking to maintain their market positions.

Significant market opportunities exist in male grooming, sustainable packaging solutions, and personalized skincare where demand exceeds current supply. New entrants target direct-to-consumer channels, clean ingredient formulations, and niche segments that larger companies find difficult to serve effectively. The launch of approximately two new beauty brands per week in France during 2023 has intensified competition for established companies. This continuous market entry creates pressure on existing players while demonstrating the market's attractiveness and growth potential.

France Beauty And Personal Care Products Industry Leaders

L'Oréal S.A.

Procter & Gamble Company

Beiersdorf AG

Unilever PLC

The Estée Lauder Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: At Viva Technology in Paris, L’Oréal unveiled its most extensive and cutting-edge portfolio of tech-driven beauty innovations, emphasizing its commitment to a more personalized, inclusive, and sustainable approach to beauty.

- March 2025: Innovative Beauty Group expanded its Curls Matter product line into 150 Monoprix stores across France, demonstrating the growing presence of premium textured haircare products in mass retail channels. This expansion reflects a broader market trend where premium beauty brands are increasingly entering mass retail spaces to reach a wider consumer base.

- March 2025: Clarins partnered with Albéa Cosmetics & Fragrance to launch its first refillable skincare jar. The product, manufactured at Albéa Simandre's facility in France, features a cap made from recycled PET with a pearlescent metallized finish. The inner cup is made of tinted virgin PP material. The Albéa Simandre facility serves as the company's center of excellence for skincare product packaging and metallization.

- November 2024: Chanel opened its first beauty house in Paris, France. The store has an area of 1,940 square feet. The store offers a wide range of brand products, including bath and body care products, perfumes, and more.

France Beauty And Personal Care Products Market Report Scope

The beauty and personal care market encompasses cosmetics, skincare, and hygiene products utilized for cleansing, beautifying, and enhancing personal appearance. Personal care products, cosmetics/makeup products, category, ingredient type, and distribution channel segment the France beauty and personal care products market. The personal care products is segmented into hair care products into shampoo, conditioners, hair oil, and other hair care products, by skincare products into facial care products, body care products, and lip care products, by bath and shower products into shower gels, soaps, bath salts, bathing accessories, and other bath and shower products, and by oral care products into toothbrushes and replacements, toothpaste, mouthwashes and rinses, additional oral care products, men's grooming products, deodorants and antiperspirants, and perfumes and fragrances. The cosmetics/makeup products segment is segmented into facial cosmetics, cosmetic eye products, and lip and nail makeup products. By category, the market is segmented into mass and premium products. By ingredient types, the market is segmented into natural and organic, and conventional/synthetic. Based on the distribution channel, the market studied is segmented into specialty stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Personal Care Products | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colourant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Others | ||

| Men’s Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Make-up Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Make-up Products | ||

| Premium Products |

| Mass Products |

| Natural/Organic |

| Conventional/Synthetic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioner | |||

| Hair Colourant | |||

| Hair Styling Products | |||

| Others | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Others | |||

| Oral Care | Toothbrush | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Others | |||

| Men’s Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Make-up Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Make-up Products | |||

| By Category | Premium Products | ||

| Mass Products | |||

| By Ingredient Type | Natural/Organic | ||

| Conventional/Synthetic | |||

| By Distribution Channel | Specialty Stores | ||

| Supermarkets/Hypermarkets | |||

| Online Retail Stores | |||

| Other Channels | |||

Key Questions Answered in the Report

What is the current value of the France personal care and cosmetics market?

The market stands at USD 17.56 billion in 2025 and is projected to hit USD 22.83 billion by 2030, growing 5.39% annually.

Which product category holds the largest share?

Personal care products dominate with 92.37% share in 2024 and will maintain leadership through 2030.

Why are natural and organic cosmetics gaining traction?

Consumer eco-awareness and France’s PFAS ban spur demand; natural/organic lines are forecast to expand 6.93% annually to 2030.

How important is e-commerce for beauty sales in France?

Online retail stores post the fastest CAGR at 7.24%, supported by live-stream shopping, AR try-ons, and rapid delivery services.

Page last updated on: