Oligonucleotide CDMO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

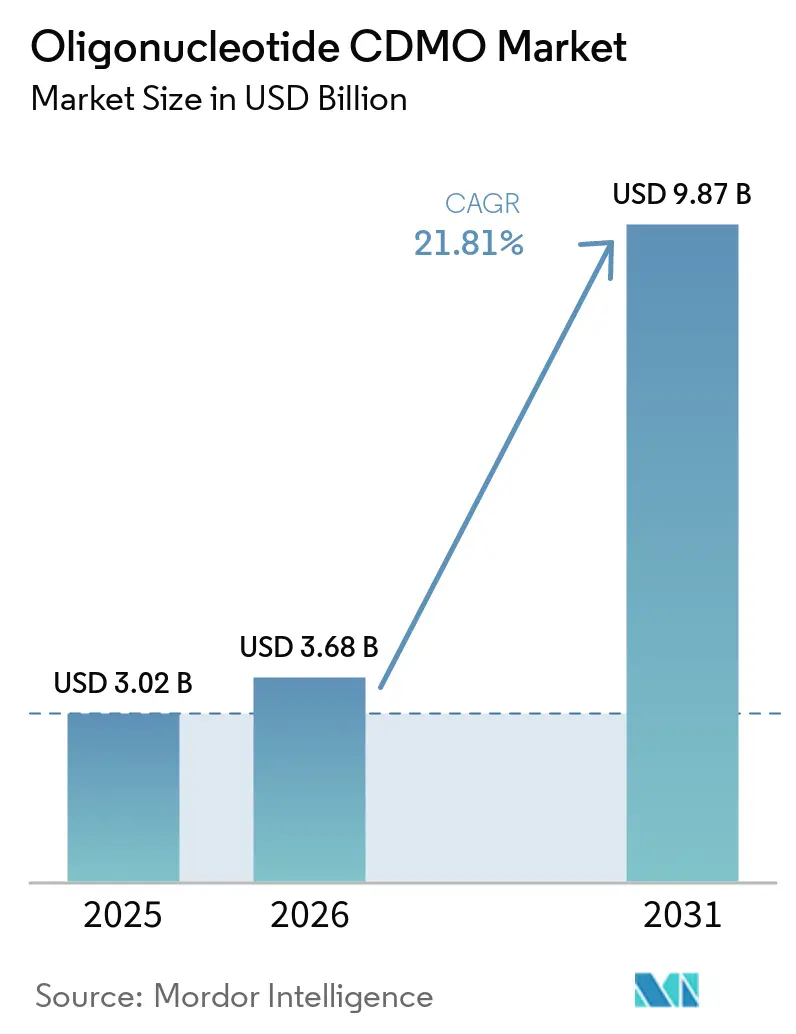

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 9.87 Billion |

| Growth Rate (2026 - 2031) | 21.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oligonucleotide CDMO Market Analysis by Mordor Intelligence

The Oligonucleotide CDMO Market size was valued at USD 3.02 billion in 2025 and is estimated to grow from USD 3.68 billion in 2026 to reach USD 9.87 billion by 2031, at a CAGR of 21.81% during the forecast period (2026-2031).

The oligonucleotide CDMO market is undergoing significant growth, driven by the expanding RNA therapeutics pipeline, advancements in solid-phase synthesis, and increased reliance on outsourced manufacturing over internal capacity. By 2026, 24 FDA and EMA-approved nucleic acid drugs were available in the market, with additional programs contributing to rising commercial demand. Many sponsors lack the required synthesis, purification, and sterile fill capacities for GMP-grade oligonucleotide APIs and drug products, keeping external partners integral to scale-up strategies.

Key Report Takeaways

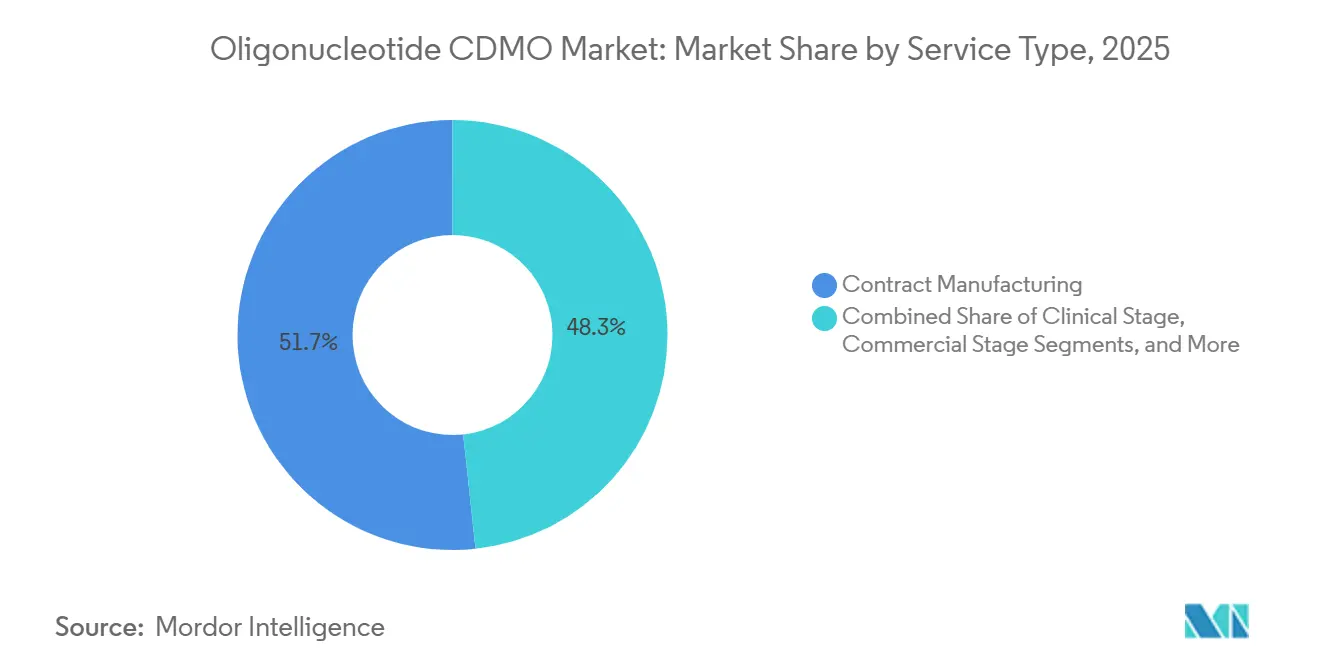

- By service type, contract manufacturing led with 51.68% revenue share in 2025, while contract development is projected to grow at 22.90% CAGR through 2031.

- By oligonucleotide type, antisense oligonucleotides held 58.23% share in 2025, while small interfering RNA is forecast to expand at 23.25% CAGR through 2031.

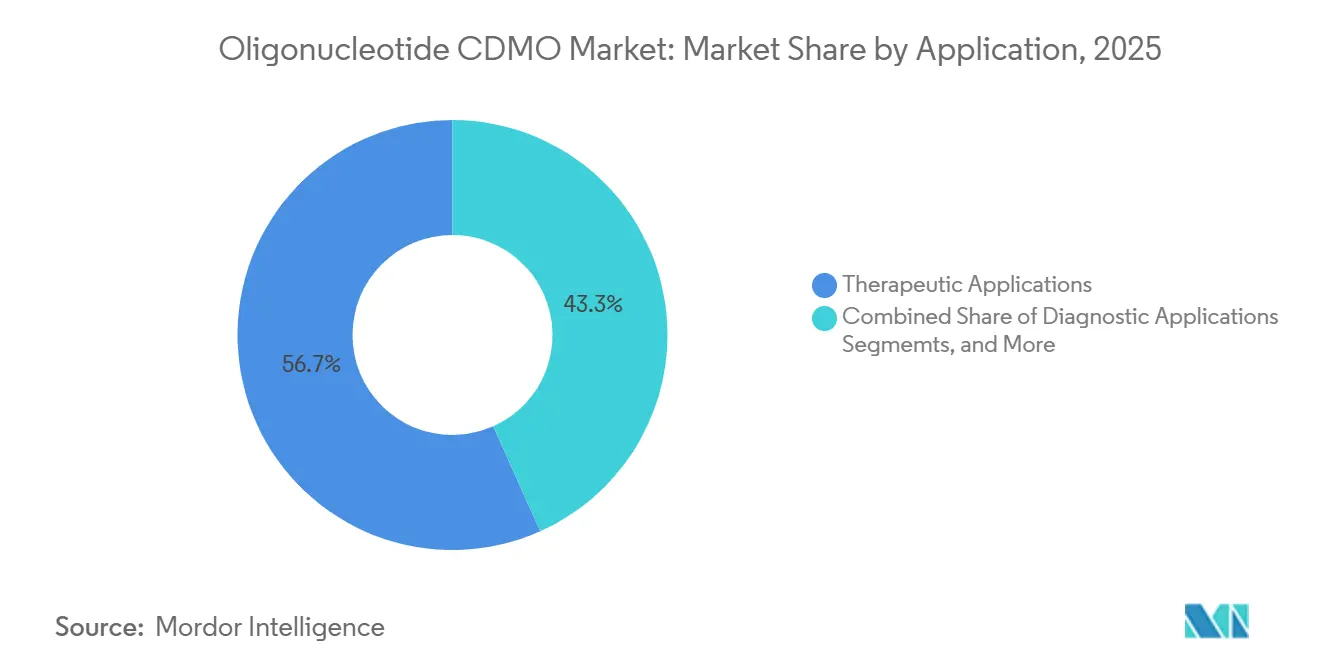

- By application, therapeutic applications accounted for 56.74% of revenue in 2025, while diagnostic applications are expected to grow at 23.55% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 52.71% of demand in 2025, while diagnostic companies are projected to record the highest CAGR at 24.33% through 2031.

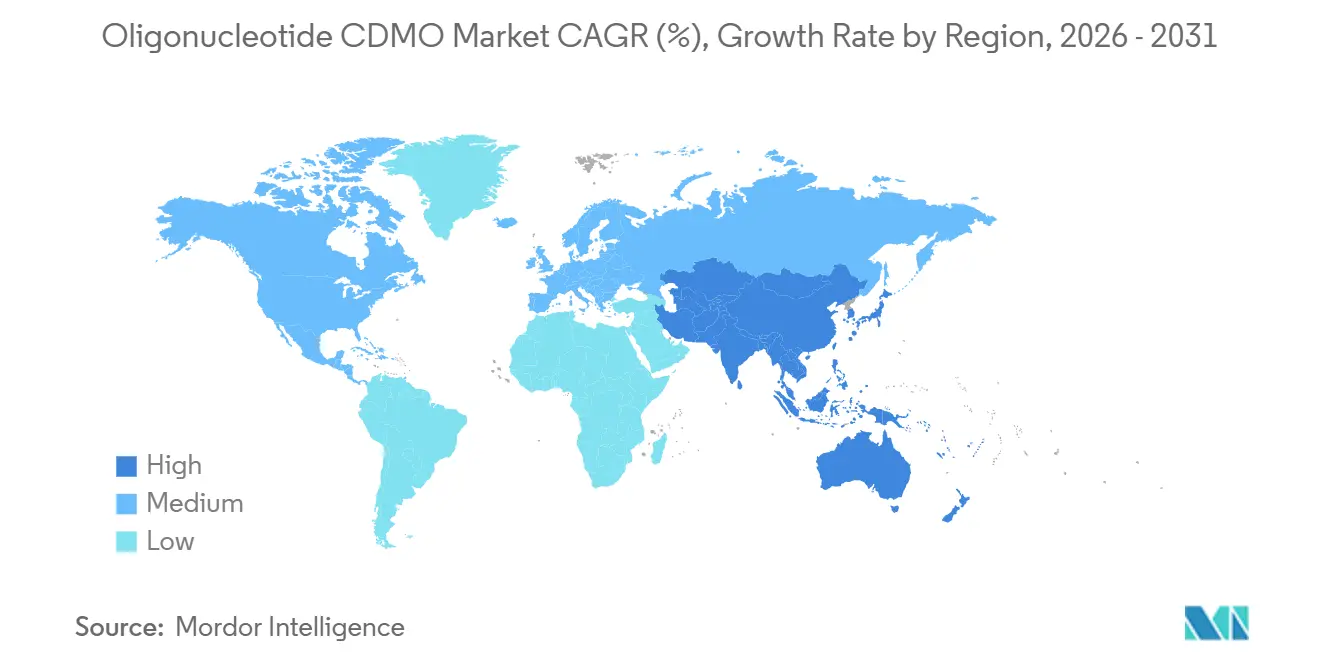

- By geography, North America held 39.55% of the market in 2025, while Asia-Pacific is projected to expand at 24.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oligonucleotide CDMO Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding clinical pipelines for RNA-targeted medicines | +6.2% | Global | Short term (≤ 2 years) |

| Outsourcing shift for complex oligonucleotide synthesis and fill-finish | +5.0% | Global, particularly North America & Europe | Medium term (2-4 years) |

| Rising demand for precision medicine and rare-disease programs | +4.5% | North America & Europe | Medium term (2-4 years) |

| Scale-up pressure from dual-route manufacturing, clinical and GMP | +3.0% | Global | Medium term (2-4 years) |

| Analytical release burden for modified and conjugated oligomers | +1.8% | North America & Europe | Long term (≥ 4 years) |

| Supply localization for nucleoside, phosphoramidite, and specialty raw materials | +1.3% | APAC, with spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Clinical Pipelines For RNA-Targeted Medicines

By mid-2026, over 200 organizations were contributing to the global oligonucleotide clinical pipeline, offering a broad customer base for the oligonucleotide CDMO market. Every IND-stage and late-stage program requires GMP material before approval and commercialization. The pipeline is shifting toward larger cardiometabolic opportunities, increasing batch sizes and adding pressure on commercial supply planning. Traditional synthesis setups are not designed for kilogram-to-tonne level demands for chronic conditions, leading sponsors to reserve capacity well in advance, tightening global GMP slot availability. Pipeline quality, timing, and volume are now critical factors shaping commercial contracts alongside scientific readiness.

Outsourcing Shift For Complex Oligonucleotide Synthesis And Fill-Finish

Challenges in managing complex oligonucleotide synthesis internally are driving an outsourcing trend. Manufacturing GalNAc-conjugated siRNA requires precise control across multiple stages, each adding technical complexity. By the first half of 2025, WuXi AppTec’s TIDES platform supported 69 molecules for API and drug product services, more than doubling its count from two years earlier. The fill-finish step is becoming crucial as products transition to subcutaneous and prefilled formats, requiring sterile capacities beyond API synthesis. Asymchem’s TJ4 facility, with an annual output of 45 million pre-filled syringe units in 2026, highlights the market's shift toward integrated API-to-drug-product solutions, raising entry barriers for smaller providers.

Rising Demand For Precision Medicine And Rare-Disease Programs

The oligonucleotide CDMO market is gaining momentum from personalized medicine and rare-disease programs, where rapid GMP execution is essential despite low batch volumes. By 2026, over 20 individualized ASOs had been developed and administered to more than 30 patients globally, showcasing the model's practical application. The FDA’s independent trial pathway for n-of-1 ASOs has reduced access barriers, improving feasibility for development and manufacturing. CDMOs capable of delivering validated small batches quickly while maintaining GMP quality are securing better pricing and stronger sponsor relationships. Ajinomoto Bio-Pharma Services’ 2025 collaboration with Gene Tools reflects this trend, linking early-stage PMO synthesis with GLP and GMP continuity for Duchenne muscular dystrophy programs.[1]BiochemPEG, “Nucleic Acid Drugs Market Overview and Approved Product Count,” BiochemPEG, biochempeg.com

Scale-Up Pressure From Dual-Route Manufacturing, Clinical And GMP

The oligonucleotide CDMO market faces scale-up challenges as small-column clinical systems struggle to meet larger commercial demands. While solid-phase synthesis remains dominant, enzymatic ligation is emerging as a viable alternative for large-scale production. Alnylam’s USD 250 million expansion at its Norton, Massachusetts RNAi site in 2025, deploying the siRELIS enzymatic ligation platform, highlights this shift. Agilent has invested over USD 740 million since 2023 in oligonucleotide manufacturing, with Train C starting production in 2026 and Train D set for enzymatic ligation in 2027. Sponsors now expect readiness across both manufacturing methods, making vendor qualification more complex. Future leaders in the oligonucleotide CDMO market will be defined by their flexibility across platforms rather than capacity alone.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High process complexity and yield sensitivity in long-chain oligonucleotides | -1.5% | Global | Short term (≤ 2 years) |

| Stringent purity, impurity, and potency control requirements | -1.2% | North America & Europe | Medium term (2-4 years) |

| Limited availability of specialized talent and qualified GMP capacity | -0.9% | Global, acute in APAC | Medium term (2-4 years) |

| Raw-material dependency and batch-level supply volatility | -0.8% | Global, acute in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Process Complexity And Yield Sensitivity In Long-Chain Oligonucleotides

The oligonucleotide CDMO market faces significant technical challenges due to the stepwise synthesis process, where one nucleotide is added at a time. For example, a 20-mer ASO undergoes at least 20 coupling cycles, and even minor efficiency losses at each step can lead to a noticeable drop in full-length yield. The complexity increases with modifications like phosphorothioate backbones, 2'-fluoro substitutions, or GalNAc ligands, which introduce side reactions and analytical difficulties. Providers transitioning from peptides or small molecules often underestimate transfer timelines, impurity management, and batch failure risks, resulting in slower capacity ramp-up despite strong demand. This explains why commercial supply remains concentrated among experienced companies with established operational histories.

Stringent Purity, Impurity, And Potency Control Requirements

The oligonucleotide CDMO market is constrained by strict analytical requirements. Oligonucleotide drug products must meet tight specifications for full-length sequences, deletion variants, diastereomer patterns, and residue-related impurities. Each product may require 15 to 20 analytical methods across platforms like HPLC, mass spectrometry, and electrophoresis, increasing staffing needs and validation efforts. Analytical headcount often grows faster than synthesis throughput, pressuring margins and timelines. Ionis’ investments in commercial-scale analytical and CMC capabilities highlight the depth needed to support multiple approved products and late-stage filings. Many providers lack such capabilities, leading to inspection risks or filing delays, especially for newer conjugate formats with evolving regulatory expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Commercial-Scale Manufacturing Anchors Revenue While Development Services Accelerate

In 2025, Contract Manufacturing held 51.68% of the oligonucleotide CDMO market share, reflecting the industry's reliance on GMP production for approved products and late-stage clinical programs. As sponsors advance into Phase 2, Phase 3, and launch preparation, the market prioritizes assured scale over exploratory support. Bachem’s Building K in Bubendorf began GMP commercial production ramp-up in 2026, adding kilogram-scale supply to the European network. ST Pharm’s USD 126 million capacity expansion, targeting 14 moles annually, highlights the growing importance of commercial manufacturing as a core differentiator. Revenue remains anchored by companies capable of consistent GMP-quality production at scales sufficient for launch planning.

Contract Development is the fastest-growing segment in the oligonucleotide CDMO market, with a 22.90% CAGR projected through 2031. Sponsors increasingly seek seamless process design transitions from early development to commercial readiness, especially for programs with modified backbones or emerging chemistries. Impurity control, process transfer, and analytical expectations now require attention well before pivotal studies. Analytical and Quality Control Services, though smaller in revenue, are becoming integral to development as release strategies impact manufacturability and regulatory timelines. Regulatory and CMC Support Services are also gaining traction as sponsors prefer single partners to streamline process work and quality packages.

By Oligonucleotide Type: ASO Dominance Challenged by siRNA's Commercial Momentum

In 2025, Antisense Oligonucleotides (ASOs) accounted for 58.23% of the oligonucleotide CDMO market, driven by demand in central nervous system, hepatic, and cardiometabolic indications. Ionis maintained a 12-candidate neurology pipeline in 2026, underscoring the strong outsourcing demand tied to ASOs. Established chemistry simplifies processes but still requires experienced CDMOs for transfer, scale-up, and validation, keeping ASOs as the largest revenue contributor despite growing interest in newer modalities.

Small Interfering RNA (siRNA) is the fastest-growing oligonucleotide type, with a 23.25% CAGR projected through 2031. This growth is fueled by expanding commercial portfolios and advancing late-stage pipelines. Alnylam’s commercial footprint and Arrowhead’s Phase 3 progress in cardiometabolic diseases are driving siRNA-oriented manufacturing needs. Guide RNA and aptamers, though smaller categories, are gaining relevance as gene editing programs advance. Other oligonucleotide types, such as PMOs and splice-switching formats, remain niche but commercially viable for specialized providers. The market is diversifying, even as ASOs continue to dominate revenue.

By Application: Therapeutic Segment Diversifies Across Indications While Diagnostics Scales Independently

In 2025, Therapeutic Applications held 56.74% of the oligonucleotide CDMO market, driven by drug development and supply. The market is shifting from a rare-disease focus to a broader mix, including cardiometabolic and oncology programs with larger supply implications. Cardiometabolic assets like PCSK9 and Lp(a) offer higher revenue potential per approval. Collaborations like GSK and CAMP4, valued at USD 458 million, highlight the entry of major pharmaceutical players into areas previously dominated by RNA biotechs. Therapeutic demand is expected to remain central to capacity planning.

Diagnostic Applications are the fastest-growing segment, with a 23.55% CAGR projected through 2031. Growth is supported by oncology liquid biopsies, infectious disease surveillance, and pharmacogenomic testing, which require large volumes of probes and primers. Research Applications, though smaller, feed into the development chain that transitions to GLP and GMP demand. The line between research-grade and development-grade materials is blurring, creating opportunities for CDMOs that ensure continuity without batch handoffs.

By End User: Pharma and Biotech Anchor Demand as Diagnostics Firms Build Direct CDMO Relationships

In 2025, Pharmaceutical and Biotechnology Companies accounted for 52.71% of end-user demand in the oligonucleotide CDMO market. Their dominance reflects commercial volumes and the material needs of Phase 2 and Phase 3 programs. Large pharmaceutical companies secure multi-year strategic supplies, while emerging biotechs rely on external partners for process development and scale-up. Bachem’s collaboration with Lilly, with potential annual order volumes of CHF 100 million, exemplifies the preferred-supplier model that prioritizes capacity for key programs.

Diagnostic Companies are the fastest-growing end-user segment, with a 24.33% CAGR projected through 2031. Their growth is tied to the adoption of qPCR and sequencing platforms requiring scalable oligonucleotide input. Academic and Research Institutes remain vital as originators of early programs transitioning into formal development. Gene and Cell Therapy Developers are also gaining importance, requiring specialized components like guide RNA and splice-correcting oligonucleotides. This diverse buyer base is expected to reduce reliance on any single sponsor profile, even as pharmaceutical and biotechnology companies remain the largest customers.

Geography Analysis

In 2025, North America held a 39.55% share of the oligonucleotide CDMO market, driven by a concentration of RNA-targeted drug developers and established GMP sites in the U.S. and Canada. Companies like Alnylam, Ionis, Arrowhead, and Wave Life Sciences, along with manufacturing leaders such as Agilent and Thermo Fisher Scientific, anchor the region's market. Agilent's 2026 launch of Agilent Advanced Therapeutics, integrating BIOVECTRA in Canada and Nucleic Acid Solutions in Colorado, strengthened North America's CDMO offerings. Familiarity with FDA regulations and long GMP track records make the region a preferred partner for NDA-enabling and launch-related supplies. However, its lead may narrow as global capacities expand and delivery time advantages diminish.

Europe remains a key technical hub in the oligonucleotide CDMO market, led by Germany and Switzerland with high-purity API manufacturing and sustained capital investments. BioSpring's EUR 100 million investment in a new nucleic acid API facility in Offenbach, spanning 15,200 m², is set for completion by late 2027. Bachem invested CHF 332.6 million in 2025, advancing Building K to commercial production in 2026, with over CHF 400 million in additional 2026 CapEx planned. Lonza, projecting 11-12% sales growth for 2026, continues to enhance advanced synthesis and antibody-oligonucleotide conjugate capabilities at its Oss site in the Netherlands. Europe's strength lies in its technical expertise, regulatory rigor, and ability to meet stringent quality demands.

Asia-Pacific is the fastest-growing region in the oligonucleotide CDMO market, with a 24.56% CAGR projected through 2031, driven by capacity expansions in China, South Korea, and Japan. Asymchem's TJ4 facility in Tianjin, launched in 2026, offers 180 mol per year of oligonucleotide capacity with advanced processing tools and an integrated drug product facility. WuXi AppTec's API sites in Changzhou and Taixing passed FDA inspections in 2025, ensuring continued U.S. supply. Japan's Nippon Shokubai is expanding GMP-compliant nucleic acid API capacity tenfold. South America and the Middle East & Africa remain emerging markets, primarily relying on imports from North America, Europe, and Asia-Pacific hubs.

Competitive Landscape

The oligonucleotide CDMO market exhibits moderate concentration at the top, as a small group of scaled, multi-site companies controls much of the commercial GMP synthesis capacity. Bachem, Lonza, Agilent through Agilent Advanced Therapeutics, WuXi AppTec through WuXi TIDES, and ST Pharm lead the market, while mid-sized specialists actively compete for clinical-stage projects. The division between commercial and clinical work creates distinct competitive dynamics. Large-scale players focus on reliability, integrated services, and capacity reservation, while specialists emphasize chemistry-specific strengths such as PMOs, GalNAc conjugates, or emerging enzymatic methods. This dynamic keeps the market active despite the concentration at the top.

Vertical integration has become a key strategy in the oligonucleotide CDMO market. Bachem’s seven-year collaboration with Lilly, with an annual order potential of up to CHF 100 million, highlights how pharmaceutical companies secure preferred suppliers before product launches. Agilent’s launch of Agilent Advanced Therapeutics in March 2026 consolidated Canadian and U.S. CDMO assets into a single end-to-end platform. Similarly, Asymchem’s TJ4 expansion integrates oligonucleotide API production, drug product capabilities, process technology, and AI-assisted PAT into one supply matrix. These developments reflect a growing preference for broad execution capabilities alongside synthesis capacity.

Technology is becoming a critical differentiator in the oligonucleotide CDMO market as enzymatic ligation gains credibility alongside traditional solid-phase synthesis. Agilent’s Train D, Alnylam’s siRELIS-linked expansion, and Asymchem’s chemoenzymatic approach indicate a shift toward longer, cleaner, and more scalable production methods. Geopolitical factors are also influencing supplier choices, with sponsors seeking to reduce exposure to policy risks associated with Chinese capacity.

Oligonucleotide CDMO Industry Leaders

Agilent Technologies, Inc.

Thermo Fisher Scientific Inc.

Lonza Group Ltd

Bachem Holding AG

WuXi AppTec Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Asymchem introduced its integrated TIDES commercial supply matrix in Tianjin, featuring an oligonucleotide production capacity of 180 mol/yr, a 6,000 m² drug product facility, and an annual output of 45 million pre-filled syringe units.

- March 2026: Agilent Technologies launched Agilent Advanced Therapeutics, consolidating BIOVECTRA in Canada and Nucleic Acid Solutions in Colorado under a single CDMO platform.

- February 2026: Lonza expanded its Advanced Synthesis capabilities in the Netherlands by adding bioconjugate solutions, including antibody-oligonucleotide conjugates, lipid nanoparticles, and protein-protein conjugates.

- October 2025: Ajinomoto Bio-Pharma Services collaborated with Gene Tools, LLC to enhance PMO therapeutic access using early-stage synthesis and liquid-phase technology.

Global Oligonucleotide CDMO Market Report Scope

As per the scope of the report, an oligonucleotide CDMO (Contract Development and Manufacturing Organization) is a specialized outsourcing partner. They develop, synthesize, and manufacture oligonucleotides, which are short, synthetic strands of DNA or RNA used as active ingredients in targeted genetic and RNA therapies.

The oligonucleotide CDMO market is segmented by service type, oligonucleotide type, application, end-user, and geography. By service type, the market includes contract manufacturing (clinical stage and commercial stage), contract development, analytical and quality control services, and regulatory and CMC support services. By oligonucleotide type, the market is segmented into antisense oligonucleotides, small interfering RNA, guide RNA, aptamers, and other oligonucleotide types. By application, the market is categorized into therapeutic applications (rare diseases, oncology, neurology, cardiometabolic diseases, and infectious diseases), research applications, diagnostic applications, and others. By end-user, the market is segmented into pharmaceutical and biotechnology companies, diagnostic companies, academic and research institutes, gene therapy and cell therapy developers, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Contract Manufacturing |

| Clinical Stage |

| Commercial Stage |

| Contract Development |

| Analytical and Quality Control Services |

| Regulatory and CMC Support Services |

| Antisense Oligonucleotides |

| Small Interfering RNA |

| Guide RNA |

| Aptamers |

| Other Oligonucleotide Types |

| Therapeutic Applications |

| Rare Diseases |

| Oncology |

| Neurology |

| Cardiometabolic Diseases |

| Infectious Diseases |

| Research Applications |

| Diagnostic Applications |

| Others |

| Pharmaceutical and Biotechnology Companies |

| Diagnostic Companies |

| Academic and Research Institutes |

| Gene Therapy and Cell Therapy Developers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Contract Manufacturing | |

| Clinical Stage | ||

| Commercial Stage | ||

| Contract Development | ||

| Analytical and Quality Control Services | ||

| Regulatory and CMC Support Services | ||

| By Oligonucleotide Type | Antisense Oligonucleotides | |

| Small Interfering RNA | ||

| Guide RNA | ||

| Aptamers | ||

| Other Oligonucleotide Types | ||

| By Application | Therapeutic Applications | |

| Rare Diseases | ||

| Oncology | ||

| Neurology | ||

| Cardiometabolic Diseases | ||

| Infectious Diseases | ||

| Research Applications | ||

| Diagnostic Applications | ||

| Others | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Diagnostic Companies | ||

| Academic and Research Institutes | ||

| Gene Therapy and Cell Therapy Developers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the oligonucleotide CDMO space by 2031?

The oligonucleotide CDMO market is projected to reach USD 9.87 billion by 2031 from USD 3.68 billion in 2026, at a CAGR of 21.81%.

What is driving outsourcing demand in oligonucleotide manufacturing?

Outsourcing is rising because complex synthesis, purification, analytics, and sterile fill-finish remain difficult for most sponsors to handle internally at GMP standards.

Which service segment currently brings in the most revenue?

Contract Manufacturing led with 51.68% revenue share in 2025, supported by approved products and late-stage clinical supply needs.

Which oligonucleotide type is growing the fastest through 2031?

Small Interfering RNA is projected to grow the fastest at 23.25% CAGR, supported by expanding commercial products and late-stage pipeline activity.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific is projected to expand at 24.56% CAGR because China, South Korea, and Japan are adding major production capacity and improving technical sophistication.

What is the main operational challenge for suppliers in this field?

Yield sensitivity in long-chain synthesis and the heavy analytical burden remain the main challenges, especially when modified backbones and conjugates are involved.

Page last updated on: