Plasmid DNA Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

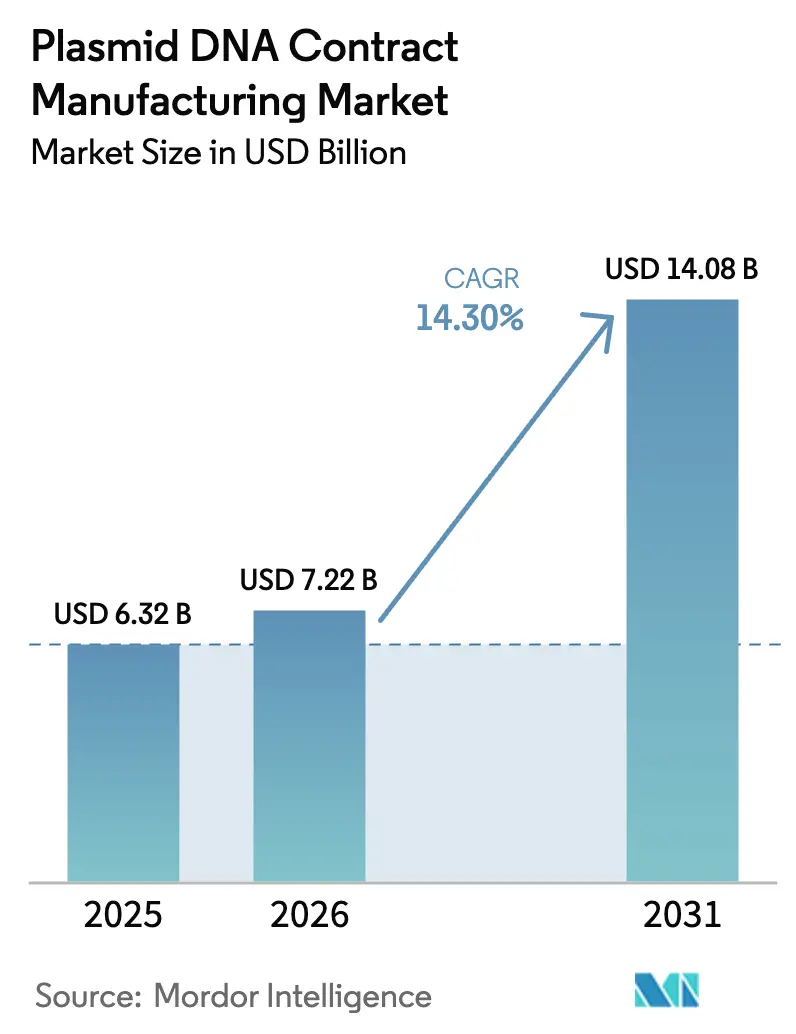

| Market Size (2026) | USD 7.22 Billion |

| Market Size (2031) | USD 14.08 Billion |

| Growth Rate (2026 - 2031) | 14.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

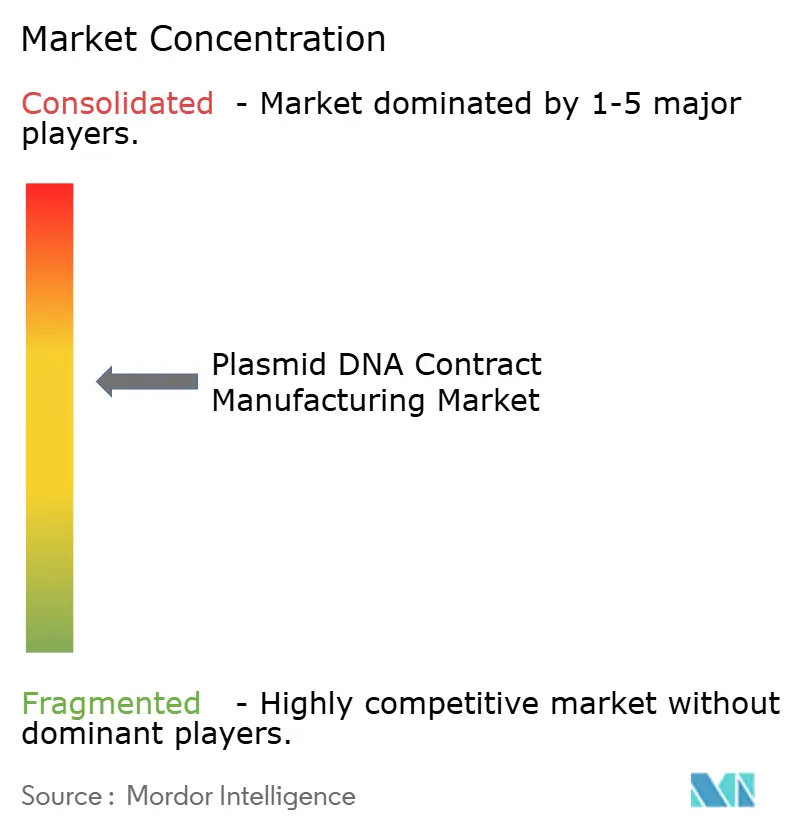

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plasmid DNA Contract Manufacturing Market Analysis by Mordor Intelligence

The Plasmid DNA Contract Manufacturing market size is expected to grow from USD 6.32 billion in 2025 to USD 7.22 billion in 2026 and is forecast to reach USD 14.08 billion by 2031 at 14.30% CAGR over 2026-2031. This sustained expansion is tied to faster regulatory approvals for advanced therapies, the rapid adoption of single-use bioreactors, rising venture funding in specialist CDMOs, and the post-COVID mRNA vaccine backlog that still demands high-quality plasmid templates. Capacity additions, particularly in North America and Asia Pacific, are scaling to meet a wave of commercial launches, while synthetic minicircle platforms attract premium pricing due to safety and yield advantages. Pricing remains firm because the supply of GMP-grade enzymes, resins, and skilled staff has not kept pace with demand, shifting negotiation power toward CDMOs that can guarantee on-time delivery. Collectively, these factors position the Plasmid DNA Contract Manufacturing market as a critical gatekeeper of advanced-therapy commercialization.[1]PMC Staff, “Advanced therapy development accelerates,” ncbi.nlm.nih.gov

Key Report Takeaways

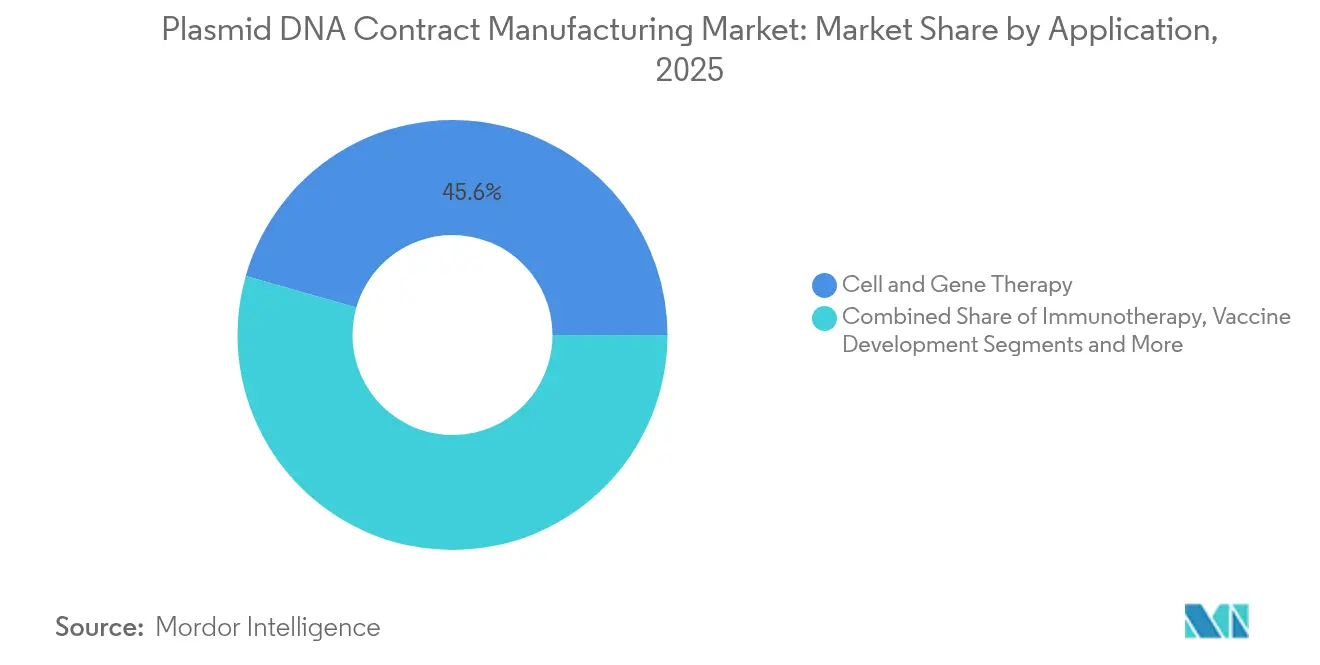

- By application, cell and gene therapy led with 45.58% revenue share in 2025; vaccine development is projected to expand at a 24.64% CAGR to 2031.

- By therapeutic area, oncology accounted for 37.55% of the Plasmid DNA Contract Manufacturing market share in 2025, while rare and orphan diseases recorded the highest projected CAGR at 21.55% through 2031.

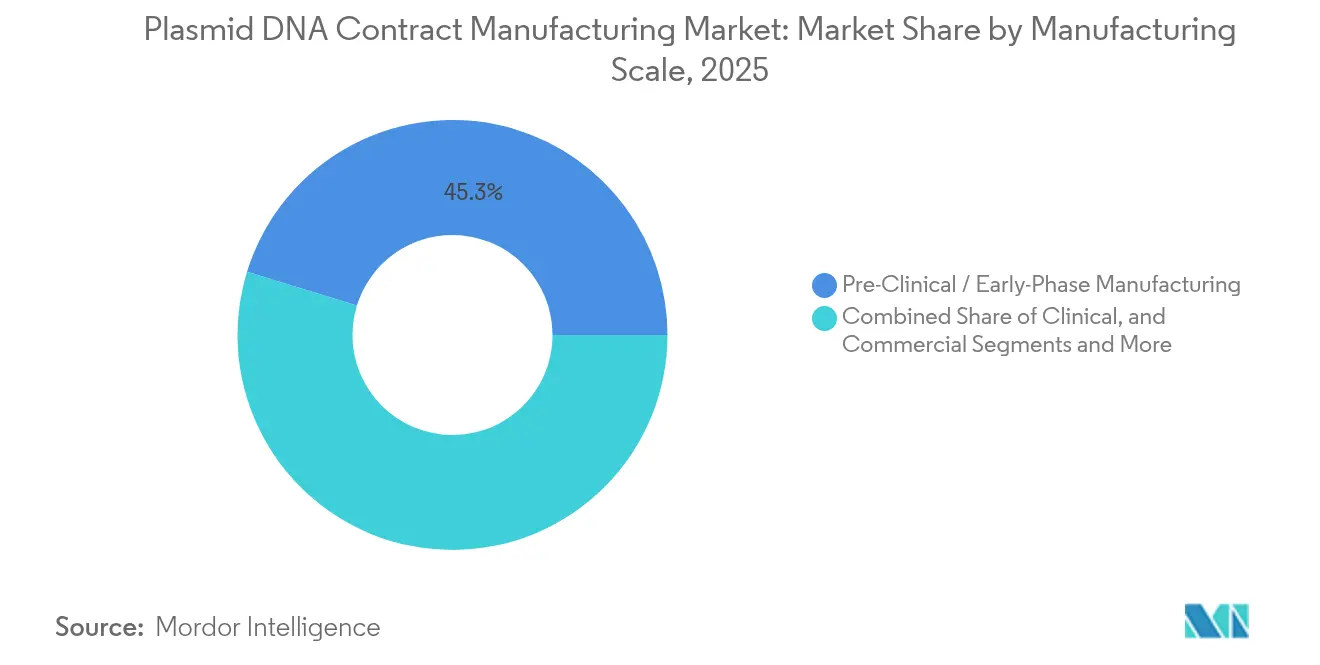

- By manufacturing scale, pre-clinical and early-phase campaigns held 45.25% share of the Plasmid DNA Contract Manufacturing market size in 2025, whereas commercial-scale volumes are set to rise at a 27.54% CAGR between 2026 and 2031.

- By plasmid configuration, conventional circular plasmids commanded 91.65% share in 2025; minicircle DNA platforms are forecast to accelerate at 26.87% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies represented 60.85% demand in 2025; cell and gene therapy developers advance fastest at 26.06% CAGR through 2031.

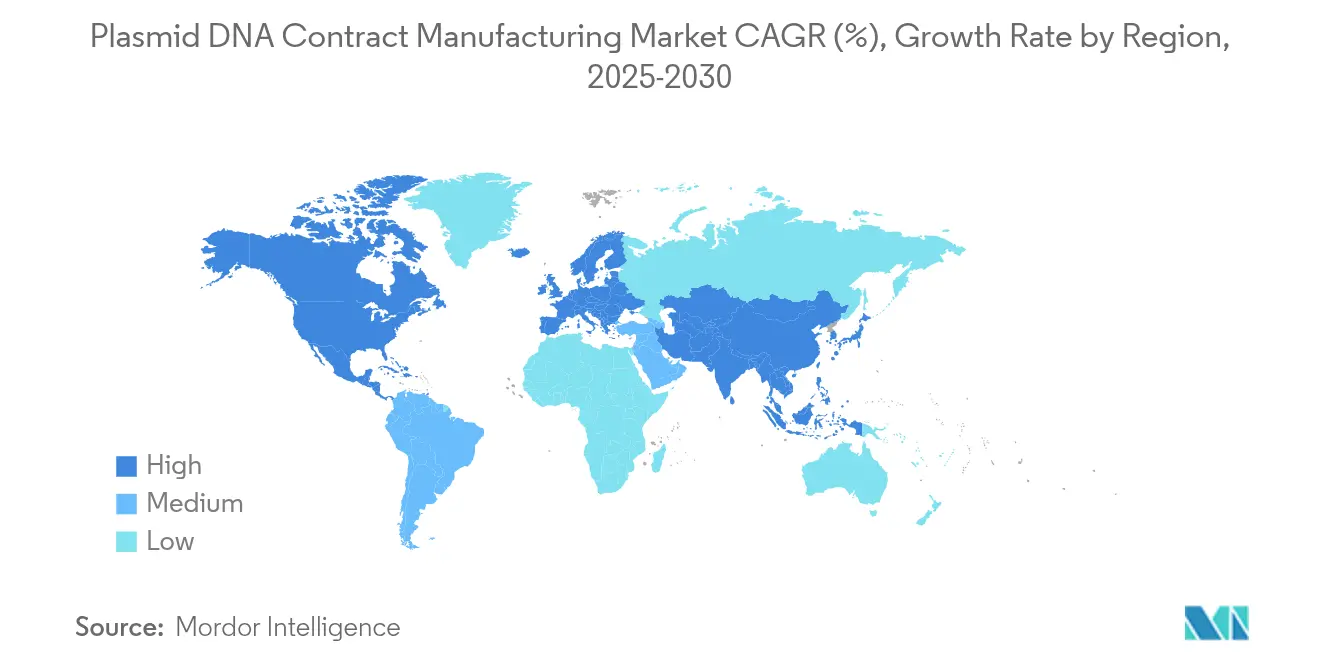

- By geography, North America led with 35.75% share in 2025, while Asia Pacific is anticipated to grow at a 19.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plasmid DNA Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Cell & Gene Therapy Regulatory Approvals | +3.20% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Expansion Of CDMO Capacity Via Single-Use Bioreactors | +2.80% | Global, concentrated in North America & APAC | Short term (≤ 2 years) |

| Rising Venture Funding For Advanced-Therapy CDMOs | +2.10% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| COVID-Era mRNA Vaccine Pipeline Backlog | +1.90% | Global, with manufacturing hubs in North America & EU | Short term (≤ 2 years) |

| Synthetic "Doggybone/Minicircle" DNA Platforms Shorten Lead-Times | +1.70% | Global, early adoption in North America | Long term (≥ 4 years) |

| AI-Optimised High-Density Fermentation Boosts Yields | +1.40% | Global, technology leaders in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Cell & Gene Therapy Regulatory Approvals

Approvals such as EMA’s clearance of the CRISPR-based Casgevy have validated the clinical and regulatory pathway for gene-edited products, triggering predictable demand spikes for clinical-grade plasmids. Coordinated guidance between FDA and EMA has trimmed duplicative batch release testing, enabling CDMOs to service multi-region trials from single facilities. Breakthrough therapy designations compress development timelines, prompting sponsors to lock in extra plasmid supply to avoid schedule slippage. These procedural efficiencies give CDMOs the confidence to deploy capital for dedicated suites that meet viral-vector and non-viral modality specifications.[2]European Medicines Agency, “EMA authorises first CRISPR/Cas9 therapy Casgevy,” ema.europa.eu

Expansion of CDMO Capacity via Single-Use Bioreactors

Thermo Fisher’s 5,000 L single-use reactors, already adopted by Takara Bio, have cut cleaning validation downtime by up to 60%. Rapid installation of modular units allows greenfield plants to reach GMP readiness within 18 months, compared with the 36-month cycle for stainless-steel builds. The economics favor early-phase volumes, where underutilization of fixed assets is a key risk. Single-use systems also mitigate cross-contamination for antibiotic-free minicircle workflows, aligning with stricter regulatory expectations for residual antibiotic markers.[3]Thermo Fisher Scientific, “DynaDrive Single-Use Bioreactors Scale-up Study,” biopharma-apac.com

Rising Venture Funding for Advanced-Therapy CDMOs

Private equity transactions, typified by ARCHIMED’s stake in PlasmidFactory, illustrate investor confidence in differentiated plasmid platforms that can command double-digit EBITDA margins. Capital infusions fund regional expansion, proprietary purification technology, and AI-driven process analytics that boost yield consistency. Well-funded challengers acquire smaller local players, tightening a market that once consisted of fragmented Mom-and-Pop labs and reinforcing the strategic value of intellectual property around high-density fermentation.

COVID-Era mRNA Vaccine Pipeline Backlog

Moderna’s new UK, Australian, and Canadian plants, operational in 2025, together require hundreds of GMP plasmid batches annually for template synthesis. Platform readiness for future pathogens means capacity will remain booked even as COVID volumes normalize. CEPI’s USD 4.7 million award to DNA Script illustrates policy support for automated template production, shrinking lead times from weeks to days, and protecting CDMOs from obsolescence when a 100-day vaccine sprint is the new benchmark.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Constraints For GMP-Grade Enzymes & Resins | -1.80% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Scarcity Of Skilled Bioprocess Talent In Emerging Regions | -1.40% | APAC & Latin America, spillover to MEA | Medium term (2-4 years) |

| Rising QC Failure Rates (Endotoxin / Supercoiling) | -1.10% | Global, concentrated in high-volume facilities | Short term (≤ 2 years) |

| Regulatory Uncertainty Around Synthetic DNA Constructs | -0.90% | Global, early impact in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Constraints for GMP-Grade Enzymes & Resins

Agarose resin capacity remains tight even after Purolite’s USD 150 million plant comes online, leaving downstream purification as the primary bottleneck. Export controls and pandemic-related logistics disruptions highlighted over-reliance on single suppliers of DNase and RNase. CDMOs now dual-source and carry buffer inventory, tying up working capital but insulating client programs from delays.

Scarcity of Skilled Bioprocess Talent in Emerging Regions

Roles in manufacturing, QC, and logistics are climbing faster than academic programs can produce qualified graduates. India’s BioE3 policy and new apprenticeship schemes are promising yet still in ramp-up. Without enough supervisors certified in GMP documentation and plasmid analytics, new facilities risk under-utilization even when equipment is installed. Fujifilm Diosynth’s North Carolina expansion underscores that, in high-complexity biomanufacturing, people remain the limiting factor as much as fermenter volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cell & Gene Therapy Dominance Drives Platform Consolidation

Cell and gene therapy programs held 45.58% of the Plasmid DNA Contract Manufacturing market in 2025. Robust clinical pipelines in CAR-T, in vivo gene editing, and ex vivo autologous therapies feed sustained demand for GMP plasmids. Lonza’s multi-year supply deal for CASGEVY illustrates how sponsors now secure multi-metric-ton capacity early to mitigate launch risk. Vaccine development is the fastest-growing niche at 24.64% CAGR, thanks to government-funded pandemic preparedness facilities that require template DNA for both mRNA and self-amplifying RNA modalities. The mRNA vaccine boom has normalized premium pricing for high-purity, antibiotic-free plasmids that improve downstream transcription efficiencies.

Template supply for research, diagnostics, and small-batch therapeutics offers a baseline of recurring orders that evens out CDMO capacity utilization. Compared with bespoke cell therapy vectors, standardized vaccine plasmids lend themselves to platform manufacturing, permitting economies of scale. As a result, sponsors prefer CDMOs that can pivot from 1 L R&D runs to 1,000 L clinical lots without tech-transfer delays. Cross-training staff on both modalities reduces idle time and maximizes revenue per square meter, reinforcing the Plasmid DNA Contract Manufacturing market’s integrated-service trend.

By Therapeutic Area: Oncology Leadership Faces Rare Disease Disruption

Oncology represented 37.55% of the Plasmid DNA Contract Manufacturing market size in 2025. CAR-T, TCR-T, and neoantigen vaccine programs dominate order books due to their larger trial populations and funding depth. Yet rare and orphan disorders are projected at 21.55% CAGR to 2031, a pace twice that of oncology. Regulatory incentives such as priority review vouchers and market exclusivity encourage sponsors to pursue gene replacement strategies in ultra-small populations, each demanding bespoke plasmids for lentiviral or AAV vectors.

Infectious diseases remain material after the COVID experience, with seasonal boosters and pan-influenza candidates keeping fermenters busy even in non-pandemic years. Autoimmune and cardiovascular targets follow behind but offer compelling scale-up potential as proof-of-concept data matures. Sponsors in these segments value CDMOs that can combine plasmid supply with analytical release testing tailored to complex regulatory packages, further consolidating demand toward end-to-end providers in the Plasmid DNA Contract Manufacturing market.

By Manufacturing Scale: Commercial Transition Accelerates Platform Economics

Early-phase campaigns retained a 45.25% share in 2025, reflecting the sector’s pipeline-heavy orientation. Nonetheless, therapies entering Phase III and commercial launch will lift large-batch volumes at 27.54% CAGR. CDMOs that invested in 2,000 L microbial fermenters and high-capacity chromatography skids now capture long-term contracts that smooth revenue visibility. Platform processes, such as Charles River’s off-the-shelf plasmids, compress tech-transfer durations, reduce deviation rates, and sustain 90% capacity utilization.

Scale-up challenges include maintaining supercoiled purity and endotoxin thresholds at higher biomass densities. Advanced process analytical technology with real-time in-line UV monitoring is increasingly mandatory. Kaneka Eurogentec’s record 1 kg batch proved technical feasibility but also highlighted the need for redundant QC instrumentation. Sponsors, therefore, gravitate toward CDMOs with in-house equipment redundancy and digital batch-record infrastructure that can withstand health authority pre-approval inspections.

By Plasmid Configuration: Innovation Challenges Conventional Dominance

Conventional circular plasmids still represent 91.65% of total orders in 2025, anchored by regulatory familiarity and streamlined SOPs. However, minicircle DNA is expanding at 26.87% CAGR and is forecast to erode the incumbent share as sponsors pursue higher expression yields and reduced immunogenicity. Minicircles eliminate unnecessary bacterial backbone sequences, simplifying regulatory filings and improving patient safety profiles.

Linearized constructs and covalently closed linear DNA such as Touchlight’s doggybone technology have gained traction in in vitro transcribed RNA workflows, reducing transcriptional read-through artifacts. Production challenges, notably in separating parental plasmid from minicircles, necessitate tailor-made ion-exchange steps that drive up COGS. Still, premium contract pricing offsets higher consumable costs, and early adopters can lock in limited specialist capacity, giving configurational innovators an edge in the Plasmid DNA Contract Manufacturing market.

By End User: Pharma Incumbents Face Specialized Challenger Growth

Pharmaceutical and biotechnology companies commanded 60.85% of 2025 demand, leveraging established quality assurance procedures and global regulatory teams to oversee supplier compliance. Their bulk orders fill baseline fermenter capacity, making them favored anchor clients for large CDMOs. In contrast, cell and gene therapy developers are growing at 26.06% CAGR, driven by venture-backed startups focused exclusively on autologous and in vivo gene editing platforms.

Academic institutions and smaller biotechs still procure research-grade plasmids yet lack the volumes and regulatory rigor to incentivize large-scale CDMO investment. Mergers like BioCina and NovaCina illustrate an industry shift toward integrated modalities where plasmid DNA, mRNA transcription, LNP formulation, and fill-finish occur under one roof, satisfying new entrants that want faster development and single-contract accountability. These dynamics underline a procurement bifurcation, compelling CDMOs to offer both standardized high-volume packages and flexible rapid-turn services in the Plasmid DNA Contract Manufacturing industry.

Geography Analysis

North America retained 35.75% of global revenue in 2025 due to FDA regulatory clarity, dense biotech clusters, and ample CDMO capacity. Lonza’s USD 1.2 billion Vacaville purchase added 330,000 L of fermenter volume, while Thermo Fisher’s Lengnau acquisition contributed another 12,000 L of specialized line, ensuring regional clients avoid overseas tech transfers. Two-way dialogue with regulators supports accelerated clearance of new facilities, reinforcing first-mover advantages for domestic providers.

Asia Pacific is the fastest-growing territory, with a 19.40% CAGR through 2031. India’s BioE3 framework promotes domestic biomanufacturing, and the US Biosecure Act redirects federal outsourcing away from China, improving order flow to Indian and Southeast Asian CDMOs. Australia’s Aurora Biosynthetics launched end-to-end RNA therapeutics production, including plasmid supply, taking advantage of R&D tax incentives and English-language GMP documentation that eases USFDA site inspections. China continues to align with ICH guidelines, offering multinationals a clearer path to utilize local capacity through partnerships and joint ventures.

Europe maintains a balanced outlook supported by EMA leadership in advanced therapy regulation. The Commission’s biotech strategy stresses strategic autonomy in critical medicines, sparking investments in plasmid suites co-located with viral-vector plants. Smaller states demonstrate therapeutic niche specialization: Slovenia focuses on rare-disease gene therapy trials, drawing CDMOs that can structure small-lot, high-value campaigns. Harmonized quality expectations across the region lighten the compliance burden for CDMOs that serve pan-European trials, maintaining a steady flow of clinical and commercial orders in the Plasmid DNA Contract Manufacturing market.

Competitive Landscape

The Plasmid DNA Contract Manufacturing market is moderately concentrated and trending toward deeper vertical integration. Global leaders such as Lonza, Thermo Fisher, and Catalent capitalize on multi-modal platforms that bundle plasmid production with viral-vector assembly, analytical services, and fill-finish. Lonza’s USD 1.2 billion Vacaville expansion signals a scale-up race to secure commercial-stage contracts. Catalent’s acquisition of Delphi Genetics upgraded in-house antibiotic-free plasmid generation, appealing to mRNA clients that require high-titre, endotoxin-safe templates.

Innovation-led specialists provide competition by offering proprietary technologies that large incumbents cannot quickly replicate. Touchlight markets covalently closed linear DNA for doggybone constructs, reducing regulatory vector payload risk. Kaneka Eurogentec’s kilogram-scale batch has set a new productivity benchmark and illustrates how niche players can differentiate on technical milestones alone.

Private equity financing is accelerating consolidation. ARCHIMED’s PlasmidFactory deal funded capacity doubling and the rollout of AI-driven process controls, giving the mid-tier player a stepping-stone toward global reach. Pharmaceutical sponsors are responding with technology partnerships rather than pure fee-for-service contracts, illustrated by GSK’s USD 35 million licensing pact with Elegen for fast-cycle linear DNA. This environment heightens competition on innovation, delivery time, and combined modality capability rather than on unit price alone.

Plasmid DNA Contract Manufacturing Industry Leaders

Lonza

PlasmidFactory GmbH & Co. KG.

BioCina

Charles River Laboratories

Catalent Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Aurora Biosynthetics opened a Sydney facility providing end-to-end GMP plasmid, mRNA, and LNP services in partnership with the NSW Government and RNA Australia.

- February 2025: BioCina and NovaCina completed their merger, creating an integrated CDMO platform spanning plasmid DNA through sterile fill-finish with sites in Adelaide and Perth.

- January 2025: Moderna confirmed that new UK, Australian, and Canadian mRNA plants will reach operational status, each requiring dedicated plasmid DNA supply chains for up to 300 million annual vaccine doses.

- October 2024: Lonza finalized the USD 1.2 billion acquisition of Genentech’s Vacaville site, adding 330,000 L bioreactor capacity to its North American network.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the plasmid DNA contract manufacturing market as all fee-based production of research, clinical, and commercial-grade plasmid DNA performed by third-party CDMOs for biopharma sponsors that lack, or choose not to use, internal plasmid capacity. Processes span microbial fermentation, harvest, downstream purification, quality release, and associated tech-transfer activities across every therapeutic area and geography.

Scope Exclusions: In-house plasmid runs, viral-vector fill-finish services, and sales of purification kits or instrumentation are excluded.

Segmentation Overview

- By Application

- Cell & Gene Therapy

- Immunotherapy

- Vaccine Development

- DNA / RNA Template Supply for mRNA

- Others

- By Therapeutic Area

- Oncology

- Infectious Diseases

- Autoimmune Disorders

- Cardiovascular Diseases

- Rare / Orphan Diseases

- By Manufacturing Scale

- Pre-clinical / Early Phase

- Clinical (Phase I–III)

- Commercial

- By Plasmid Configuration

- Circular

- Linearised

- Minicircle

- By End User

- Pharmaceutical & Biotechnology Companies

- Cell & Gene Therapy Developers

- CDMO / CMO Partners

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Several semi-structured interviews with CDMO executives, regulatory consultants, and therapy developers across North America, Europe, and Asia clarified average selling prices, batch failure rates, and clinical ramp-up schedules; findings filled data gaps and refined model assumptions.

Desk Research

We reviewed open datasets from the US FDA Drug Master Files, EMA GMP certificates, ClinicalTrials.gov, and the Alliance for Regenerative Medicine to map current and pending plasmid demand. Trade and customs series from UN Comtrade and OECD STAN helped size inter-regional plasmid shipments, while earnings calls, 10-Ks, and press releases revealed CDMO capacity additions. Subscription resources, D&B Hoovers for company revenue splits and Dow Jones Factiva for deal flow, added financial granularity. These sources illustrate rather than exhaust our desktop evidence pool, which is far broader.

Market-Sizing & Forecasting

A top-down construct begins with modeled global plasmid demand inferred from active gene, cell, and mRNA therapy trial counts, typical dose requirements, and stage-specific attrition; demand is then linked to outsource penetration and validated through selective bottom-up checks (sampled CDMO capacity × weighted utilization). Key variables include GMP fermenter installed base, median microbial yield per liter, trial initiation cadence, regulatory approval velocity, currency movements, and observed ASP drift. Multivariate regression and scenario analysis project these drivers to 2030, while stochastic sensitivity tests flag inputs that most influence value.

Data Validation & Update Cycle

Mordor analysts cross-compare outputs with shipment trends, CDMO order backlogs, and secondary market indicators; variances beyond preset bands trigger model re-runs and peer review. The dataset refreshes annually, with ad-hoc updates after material events such as facility expansions or step-change approvals.

Why Mordor's Plasmid DNA Contract Manufacturing Baseline Earns Trust

Published estimates can diverge because firms choose different inclusion rules, cost bases, and refresh cadences. Our disciplined scope, demand-led modeling, and yearly recalibration keep figures decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.32 B (2025) | Mordor Intelligence | - |

| USD 2.02 B (2024) | Global Consultancy A | Limits geography to US and EU and omits pre-clinical batches, leading to understated volume |

| USD 0.32 B (2023) | Industry Journal B | Treats plasmids as a sub-line within broader viral-vector study and uses static 2022 ASPs |

The comparison shows that when scope narrows or older cost inputs persist, valuations swing widely; by grounding our model in current, global demand signals and live ASP checks, Mordor Intelligence provides a balanced, transparent baseline clients can rely on.

Key Questions Answered in the Report

What is the current value of the Plasmid DNA Contract Manufacturing market?

The market is valued at USD 7.22 billion in 2026 and is projected to grow to USD 14.08 billion by 2031.

Which application segment generates the largest demand?

Cell and gene therapy programs hold 45.58% of 2025 revenue, making them the largest application for GMP plasmid supply.

Which region is growing fastest for contract plasmid services?

Lonza, PlasmidFactory GmbH & Co. KG., BioCina, Charles River Laboratories and Catalent Inc. are the major companies operating in the Plasmid DNA Contract Manufacturing Market.

Which is the fastest growing region in Plasmid DNA Contract Manufacturing Market?

Asia Pacific is expected to expand at a 19.40% CAGR through 2031, driven by new capacity in India, China, and Australia.

Why are minicircle plasmids gaining momentum?

Minicircles remove bacterial sequences, improving transfection efficiency and safety, which supports a 26.87% CAGR forecast for this configuration.

What is the main bottleneck limiting further industry growth?

Shortages of GMP-grade enzymes and chromatography resins remain the primary near-term constraint, curbing an estimated 1.8% of potential CAGR.

How are CDMOs differentiating in a competitive market?

Providers invest in single-use bioreactors, AI-driven fermentation control, and proprietary DNA formats to secure long-term, higher-margin contracts.

Page last updated on: