Oligonucleotide Synthesis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

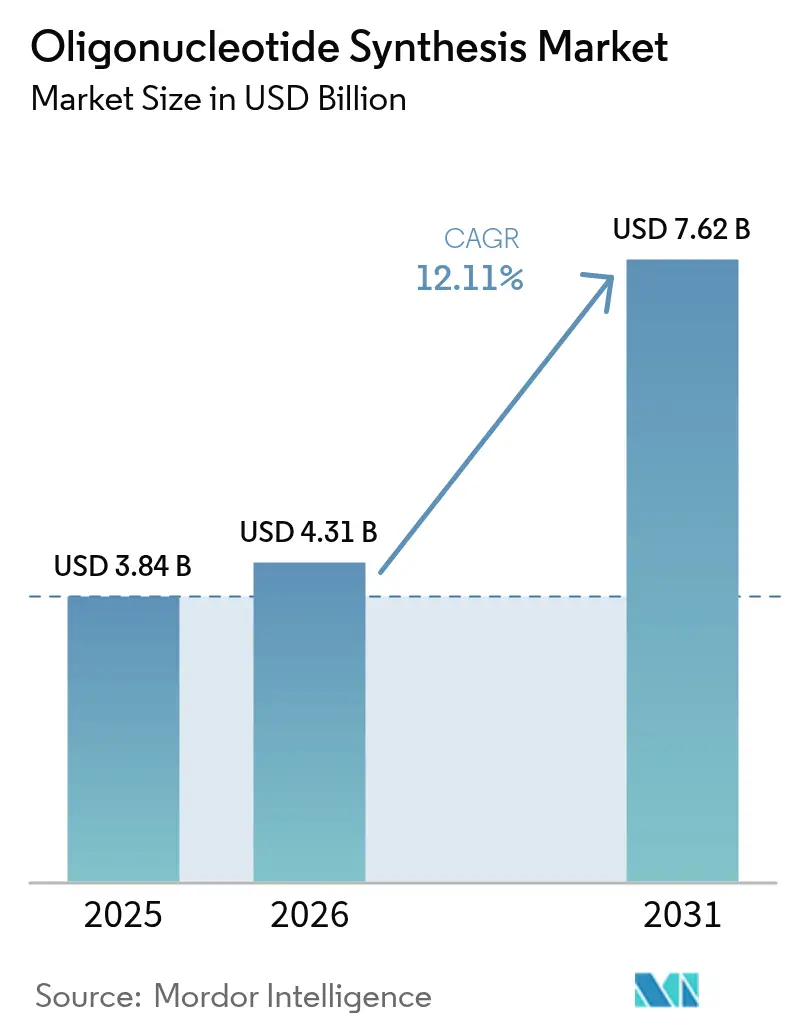

| Market Size (2026) | USD 4.31 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 12.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oligonucleotide Synthesis Market Analysis by Mordor Intelligence

Oligonucleotide synthesis market size in 2026 is estimated at USD 4.31 billion, growing from 2025 value of USD 3.84 billion with 2031 projections showing USD 7.62 billion, growing at 12.11% CAGR over 2026-2031. Enzymatic platforms that create longer, cleaner strands without hazardous reagents are reshaping the oligonucleotide synthesis market by challenging four decades of phosphoramidite dominance. Government grants, notably the NIH’s RNA-focused USD 15.4 million program, catalyze new production methods while contract manufacturers scale capacity to meet rising pharmaceutical outsourcing needs. Clinical approvals underscore momentum: 22 nucleic-acid drugs cleared regulators by late 2023, and four more won clearance in 2024, pulling the oligonucleotide synthesis market beyond its research-reagent roots into industrial-scale biologics. Environmental scrutiny of PFAS-linked reagents pressures legacy processes, amplifying interest in enzymatic alternatives that reduce waste while complying with evolving regulations.

Key Report Takeaways

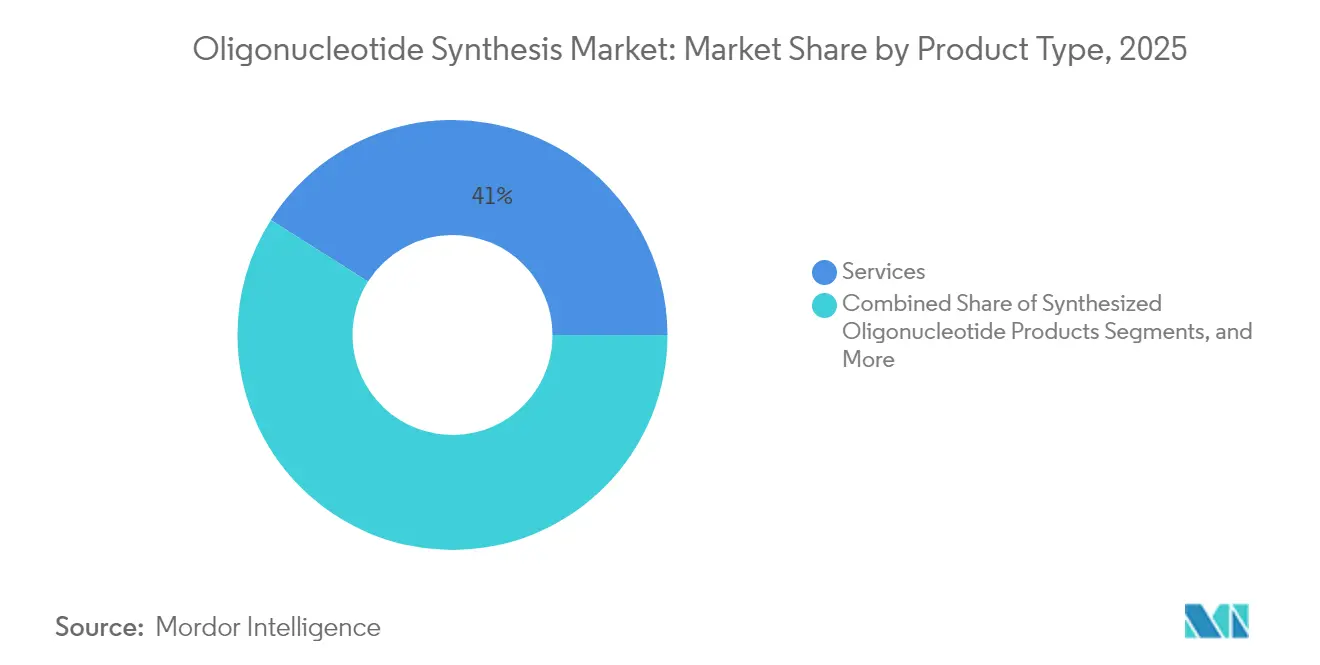

- By product type, services accounted for 41.02% revenue share of the oligonucleotide synthesis market in 2025, while synthesized oligonucleotide products are positioned to post the fastest growth through 2031.

- By chemistry, DNA dominated with 43.12% of oligonucleotide synthesis market share in 2025; RNA is on course to narrow the gap as mRNA and CRISPR pipelines mature.

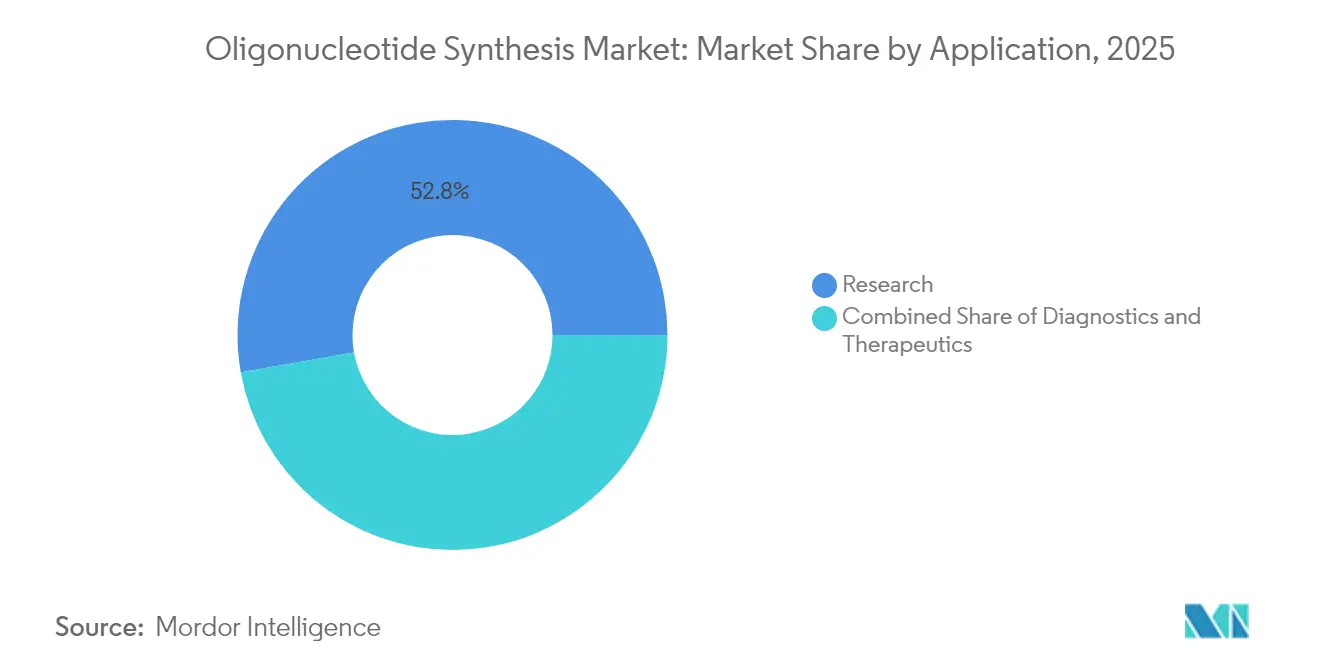

- By application, research held 52.78% share of the oligonucleotide synthesis market size in 2025, yet therapeutics already command premium pricing and are expanding the fastest.

- By end-user, academic institutes generated 72.32% volume in 2025, while pharmaceutical and biotechnology companies delivered the highest value through clinical-grade contracts.

- By geography, North America led with 42.55% share in 2025, whereas Asia-Pacific shows the steepest upward curve on the back of USD 4 billion in Chinese funding rounds and multi-hundred-million-dollar capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Oligonucleotide Synthesis Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government funding surge post-pandemic | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Clinical adoption of synthesized oligos in advanced diagnostics | +1.8% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Expansion of contract development & manufacturing (CDMO) capacity | +1.5% | Global, with major investments in Asia-Pacific | Medium term (2-4 years) |

| Patent cliffs driving next-gen antisense/RNA therapies | +1.2% | North America and Europe primarily | Long term (≥ 4 years) |

| Micro-array based ultrahigh-throughput synthesis platforms | +0.9% | Global, technology centers in North America | Short term (≤ 2 years) |

| Enzymatic, benchtop "DNA printer" launch pipelines | +0.7% | North America and Europe initially | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Funding Surge Post-Pandemic

Federal investment elevated oligonucleotides to critical-infrastructure status for pandemic preparedness and precision medicine. The NIH earmarked USD 15.4 million for RNA research that improves microfluidic long-strand synthesis and nanopore sequencing, while its Technology Development Coordinating Center secures USD 1.5 million annually through 2029 to refine nucleic-acid production systems [1]National Human Genome Research Institute, “RNA Technology Development Funding,” genome.gov. Parallel European grants create a trans-Atlantic push to localize supply chains, reinforce biosecurity, and accelerate oligonucleotide standards that underpin therapeutic approvals.

Clinical Adoption of Synthesized Oligos in Advanced Diagnostics

Fresh FDA guidance issued in 2024 clarifies quality requirements, accelerating diagnostic assay rollouts and boosting the oligonucleotide synthesis market [2]FDA, “Drug Development Guidance for Nucleic Acid–Based Therapeutics,” fda.gov. GalNAc-conjugated antisense oligos received their first approval, confirming precise delivery chemistries that rely on high-fidelity synthesis. Personalized “N-of-1” treatments now demand rapid micro-batch production, prompting service providers to integrate design-to-clinic workflows that transform how rare-disease patients are treated.

Expansion of Contract Development & Manufacturing (CDMO) Capacity

Agilent’s USD 725 million build-out, WuXi STA’s 27 production lines, and MilliporeSigma’s EUR 300 million Korean facility collectively double global therapeutic output, signalling how CDMOs anchor the oligonucleotide synthesis market. Outsourced operations supply GMP-grade strands faster than in-house teams can qualify equipment, positioning CDMOs as strategic allies for drug sponsors racing toward commercialization.

Patent Cliffs Driving Next-Gen Antisense/RNA Therapies

The expiry of foundational antisense patents invites new entrants, while high-profile CRISPR disputes exemplified by Broad Institute vs. CVC reshape licensing flows without dimming investor enthusiasm. Recent rulings that invalidated select guide-RNA claims open freedom-to-operate for smaller firms, lifting barriers that once limited oligonucleotide portfolios.

Enzymatic, Benchtop “DNA Printer” Launch Pipelines

DNA Script’s SYNTAX, Ansa’s 1,005-base record, and Telesis Bio’s Gibson SOLA highlight how template-free polymerases deliver longer strands with fewer toxic reagents, aligning production with rising sustainability mandates. Wider availability sparks biosecurity reviews, leading to new sequence-screening frameworks that balance open innovation against dual-use risks.

Restraints Impact Analysis of Oligonucleotide Synthesis Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent high purification & QC costs | -1.4% | Global, particularly affecting smaller players | Long term (≥ 4 years) |

| IP disputes around CRISPR / gene-editing sequences | -0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Supply bottlenecks for specialty phosphoramidites | -0.6% | Global, with Asia-Pacific supply chain concentration | Short term (≤ 2 years) |

| PFAS-linked environmental regulations on fluorinated nucleic acids | -0.4% | Europe and North America regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent High Purification & QC Costs

Therapeutic-grade purification can consume 60-70% of manufacturing budgets as high-performance liquid chromatography remains the standard for removing truncated strands and reactive impurities. Yield erosion, demonstrated by 30-mer sequences falling to 55% at 98% coupling efficiency, forces over-production that inflates reagent use and waste disposal, stressing smaller players that lack economies of scale.

IP Disputes Around CRISPR / Gene-Editing Sequences

Overlapping patent claims create legal landmines where a single guide RNA may trigger multiple licenses, driving up costs and delaying launches. Although some patents were invalidated in 2024, ongoing appeals sustain uncertainty, prompting conservative sequence designs that narrow the addressable therapeutic space.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Oligonucleotide Synthesis Market Segment Analysis

By Product Type:

Services Anchor Outsourcing MomentumServices generated 41.02% of overall 2025 revenue as pharmaceutical sponsors prioritized turnkey solutions that compress development timelines. This dominance confirms the oligonucleotide synthesis market preference for external capacity that bundles synthesis, purification, and regulatory support into single-vendor contracts. The model suits high-value clinical batches where each lot must pass stringent GMP audits. Reagent consumption scales in parallel, offering steady annuity streams for consumables providers even as benchtop enzymatic platforms appear.

Looking ahead, service revenue is expected to outpace product sales because compliance complexity continues to rise. CDMOs spread analytical costs across dozens of clients, whereas individual biotechs seldom justify multi-million-dollar cleanroom investments. Equipment suppliers respond with higher-throughput instruments such as 384-well synthesizers that cut per-oligo costs, yet most machines will still land inside service facilities rather than drug-maker labs. The oligonucleotide synthesis market size expansion therefore tracks CDMO build-outs, while specialized benchtop systems address niche rapid-turnaround needs within research cores.

By Chemistry:

DNA Holds Sway as RNA AcceleratesDNA retained 43.12% command of the oligonucleotide synthesis market in 2025 thanks to mature phosphoramidite protocols that deliver >99% coupling efficiency for strands up to 120 bases. RNA’s 13.95% share is set to climb as mRNA vaccines, CRISPR guides, and siRNA drugs gain clinical traction. Enzymatic synthesis favors RNA because aqueous enzymology avoids the acidic deprotection steps that degrade 2'-hydroxyl groups, extending feasible lengths beyond 200 bases without capping agents.

Modified backbones such as phosphorothioates and 2'-O-methyl riboses already dominate antisense and RNAi therapeutics, commanding multiples of DNA’s price per base. Niche chemistries (LNA, PNA, Morpholino) occupy small slices yet supply indispensable tools for stability-critical indications. As therapeutic demand intensifies, production shifts toward GMP-compliant enzymes and greener solvents, lifting the oligonucleotide synthesis market share of RNA while DNA remains foundational for gene-assembly and PCR primer volumes.

By Application:

Research Volume Meets Therapeutic ValueResearch retained 52.78% of 2025 activity, but therapeutics, with 14.69%, drive the lion’s share of profit as each clinical oligo can bill at 10- to 20-fold the price of a laboratory primer. Twenty-two approved nucleic-acid medicines by 2023 validated the modality, while four 2024 approvals confirm a steady pipeline. Companion diagnostics marry drug and test, doubling sequence orders per indication and tightening links between therapeutic and diagnostic markets.

From 2025 onward, therapeutic CAGR is positioned to outrun research volumes. Patent expiries on first-generation antisense constructs open room for rare-disease developers, and venture funding flows into start-ups crafting personalized oligos. Consequently, the oligonucleotide synthesis market size attached to therapeutics will expand faster than any other segment, even if absolute unit counts stay below research quantities.

By End-User:

Academic Institutes Lead Volume, Pharma Captures MarginAcademic institutions drove 72.32% of sequences in 2025, underlining how discovery science still underpins oligonucleotide demand. University labs churn through primers and probes for CRISPR screens, transcriptomics, and synthetic biology. Yet revenue skews toward pharmaceutical and biotechnology companies, which represented only 14.35% of volume but booked the majority of dollar value through GMP projects.

Hospitals and diagnostic labs are the fastest-growing cohort as genetic tests migrate from central reference labs to point-of-care settings. This wave feeds the oligonucleotide synthesis market with medium-scale orders demanding medical-grade quality but not full GMP rigor, carving out a mid-tier service niche. As precision-medicine trials proliferate, academic–industry collaborations will deepen, funneling grant-backed discoveries into clinical pipelines that rely on CDMO strength.

Geography Analysis

North America Oligonucleotide Synthesis Market

North America captured 42.55% share in 2025, propelled by FDA guidance that de-risks development and by NIH funding that subsidizes platform innovation. United States-based firms leverage integrated ecosystems spanning venture capital, academic excellence, and manufacturing know-how. Canada benefits from proximity, with emerging GMP suites attracting cross-border projects. Mexico’s low-cost sites are beginning to draw reagent packaging and QC functions, though synthesis remains concentrated further north.

APAC Oligonucleotide Synthesis Market

Asia-Pacific held 14.78% yet registers the highest growth trajectory. Chinese sponsors poured more than USD 4 billion into small-nucleic-acid ventures during 2024, while provincial governments fast-tracked plant permits to localize supply. South Korea secured EUR 300 million from MilliporeSigma for a duplex biologics campus, and Singapore’s regulatory certainty lured multi-line expansions from WuXi STA and GenScript. India’s “Make in India” drive birthed CoDx-CoSara’s new Gujarat facility, signaling regional intent to rise up the value chain.

Europe, LATAM and GCC Oligonucleotide Synthesis Market

Europe remains an innovation powerhouse but encounters PFAS-related chemical restrictions that complicate legacy phosphoramidite workstreams. Germany’s BioSpring tripled capacity and added 1,500 jobs, offsetting supply headaches by pioneering fluorine-free reagents. The United Kingdom’s Catapult centers pair public grants with biotech spin-outs, while France cultivates enzymatic start-ups. Elsewhere, Brazil and Argentina lead Latin American uptake of genetic therapies, and Gulf states build precision-medicine hubs anchored by imported oligonucleotides, foreshadowing localized production over the next decade.

Regulatory Landscape

In the United States, federal policy is tightening biosecurity controls around synthetic nucleic acids via the White House Office of Science and Technology Policy (OSTP) Nucleic Acid Synthesis Screening Framework. For federally funded life-sciences procurement, requirements tied to the framework apply from April 26, 2025. This shifts sourcing decisions for buyers of synthetic nucleic acids and benchtop nucleic acid synthesis equipment toward providers and manufacturers that implement sequence screening practices aligned with the framework.

The framework also sets stepped technical thresholds that affect how suppliers design screening and compliance workflows. A key milestone is October 13, 2026, when the screening window standard decreases to 50 nucleotides and benchtop nucleic acid synthesis equipment manufacturers must integrate capability to screen sequences for sequences of concern. In Europe, the European Medicines Agency (EMA) moved to formalize expectations through its draft Guideline on the Development and Manufacture of Oligonucleotides (EMA/CHMP/CVMP/QWP/262313/2024), with the consultation phase concluding in early 2025. This adds momentum around clearer CMC and analytical-control expectations for therapeutic-grade oligonucleotides.

Value Chain Analysis

The oligonucleotide synthesis value chain starts with upstream suppliers of nucleoside building blocks and specialty inputs (phosphoramidites for solid-phase synthesis and enzymes/nucleoside precursors for enzymatic routes), along with solvents and process reagents. It then moves through synthesis platform providers (instruments, software, and workflow consumables), CDMOs that perform GMP synthesis, purification, and analytical characterization, and finally to end users across academic research, diagnostics, and biopharma sponsors. The services layer is central because it bundles synthesis, purification, and QC into audit-ready packages, aligning with the market shift toward outsourced clinical-grade production.

Operational bottlenecks concentrate in manufacturing scale-up and downstream processing. High process mass intensity, reported at roughly 1,500 kg of solvent per 1 kg of product, makes solvent availability (notably acetonitrile) a supply-chain risk. Energy-intensive steps such as lyophilization and specialized chromatography capacity also introduce constraints. To reduce cost, waste, and cycle time, the chain is incorporating partnerships that connect novel chemistries and enzymatic platforms into established CDMO workflows, including Codexis and Axolabs (LGC Group) evaluating the ECO Synthesis platform for scalable RNA therapeutics (January 2026), and Luxna Biotech extending its partnership with BioSpring to manufacture oligonucleotides incorporating GuNA amidites (June 2026).

Competitive Landscape

The oligonucleotide synthesis market shows moderate fragmentation. Thermo Fisher, Agilent, and Danaher’s Integrated DNA Technologies wield global plants, broad reagent portfolios, and automated analytics. Agilent’s USD 725 million capacity upgrade and BIOVECTRA acquisition illustrate how scale secures high-value therapeutic contracts. Twist Bioscience, DNA Script, and Ansa Biotechnologies disrupt with enzymatic innovations that extend sequence length and cut solvent use, reshaping buyer preference toward greener chemistry.

Strategic M&A quickens: Merck’s USD 600 million Mirus Bio purchase adds lipid nanoparticle know-how, while Thermo Fisher’s USD 3.1 billion deal for Olink expands proteomic adjacency. Smaller firms carve niches in personalized medicine; Aldevron and IDT completed a bespoke CRISPR therapeutic from design to clinic in six months, demonstrating agile pathways big incumbents now chase. Patent maneuvers remain potent weapons, evidenced by Editas-Vertex licensing pacts that lock down CRISPR components even amid legal flux. Environmental regulation and supply-chain localization further complicate competition, rewarding players that pre-emptively adapt chemistry and geographic footprint.

Oligonucleotide Synthesis Industry Leaders

Thermo Fisher Scientific

Agilent Technologies

Merck KGaA

Bio-Synthesis Inc

Eurofins Scientific

- *Disclaimer: Major Players sorted in no particular order

Oligonucleotide Synthesis Market Companies Covered in this Report

- Agilent Technologies

- Thermo Fisher Scientific

- Merck

- Danaher (IDT)

- Eurofins

- Kaneka (Eurogentec)

- Genscript

- LGC Biosearch Technologies

- Maravai Life Sciences (TriLink)

- Biogen

- Sarepta Therapeutics

- Twist Bioscience

- Integrated DNA Technologies

- Bioneer

- Bio-Synthesis

- Biolegio

- GE Healthcare (Cytiva)

- Synbio Technologies

- Creative Biogene

- Vivantis Technologies

- Macrogen

Market Opportunities and Future Outlook

Commercial whitespace is expanding around integrated, therapeutic-grade supply models that shorten handoffs between development, GMP API production, and specialized analytics for next-generation oligonucleotide modalities. CDMOs are putting visible capacity and service-matrix structures in place, including Asymchem unveiling an integrated TIDES commercial supply matrix at its TJ4 site in Tianjin (April 2026), with stated oligonucleotide capacity of 180 mol/year. Sponsor-side demand signals also support large-batch readiness, with ST Pharm signing a KRW 89.7 billion oligonucleotide API supply contract in March 2026, which points to API-scale supply agreements becoming more repeatable.

Opportunities also sit in higher-complexity formats and workflow specialization, including oncology-adjacent applications that require higher-throughput, high-quality oligonucleotides (for example, MRD workflows). Integrated DNA Technologies completed an expansion of its Coralville, Iowa manufacturing facility in April 2026, reporting more than a threefold increase in synthesis capacity aimed at MRD and oncology-focused oligonucleotides. This supports demand for adjacent capabilities in purification, analytics, and modified-oligo inputs. On the technology front, enzymatic and one-pot methods are moving into evaluations for commercial manufacturing, such as Axolabs evaluating Codexis ECO Synthesis (January 2026). At the same time, biosecurity compliance requirements under the U.S. OSTP screening framework create an additional opportunity layer for screening-enabled software, instrumentation, and compliant-provider networks for both service providers and benchtop equipment manufacturers.

Recent Industry Developments in Oligonucleotide Synthesis Market

- May 2026: Agilent Technologies entered a two-year research collaboration with Singapore's Nucleic Acid Therapeutics Initiative (NATi) to advance analytical and preparative workflows for lipid-conjugated oligonucleotides. The collaboration targets complex conjugate formats where method development and robust characterization can be gating steps, strengthening Agilent's position across tools and services supporting therapeutic oligo programs.

- May 2025: Thermo Fisher Scientific partnered with Mirai Bio to combine Thermo Fisher's cGMP manufacturing services and global capacity with Mirai's nucleic acid therapeutic design optimization platform. The pairing links design-for-manufacture considerations with scalable production, reinforcing an end-to-end outsourcing model for sponsors progressing nucleic acid therapeutics.

- May 2024: Merck KGaA signed a definitive agreement to acquire Mirus Bio for USD 600 million, expanding its life science portfolio in transfection reagents used in viral vector production for cell and gene therapies. While centered on upstream delivery technologies, the deal broadens Merck's adjacent toolkit around nucleic acid modalities and can deepen bundled offerings that sit alongside oligonucleotide manufacturing and development support.

Oligonucleotide Synthesis Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the oligonucleotide synthesis market is defined as revenue generated from producing and supplying synthetic oligonucleotides and closely related offerings used in research, diagnostics, and therapeutic development, across commercial and institutional buyers.

Scope exclusions: Finished drug products that contain an oligonucleotide as an active ingredient are excluded from the market totals.

Segments Covered in This Report

- By Product Type

- Synthesized Oligonucleotide Products

- Reagents

- Equipment

- Services

- By Chemistry

- DNA (Phosphoramidite)

- RNA

- LNA / PNA / Morpholino

- By Application

- Research

- Diagnostics

- Therapeutics

- By End-user

- Academic Research Institutes

- Pharmaceutical & Biotechnology Companies

- Hospital & Diagnostic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of APAC

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial market boundary and to anchor key demand signals that can be checked year after year. We referred to public sources such as the National Institutes of Health (NIH) funding data and RePORTER, the US FDA drug and biologics databases for approvals and filings, the USPTO and other patent repositories for technology direction, and the OECD and World Bank indicators for R&D intensity and macro context.

To avoid sizing the market on a single proxy, additional reading was done through company annual reports, investor presentations, association webpages related to nucleic acids and biotechnology manufacturing, and reputable science journals that describe synthesis chemistries and scale limits. In parallel, selected paid subscriptions were used for structured company financials and news tracking, as well as for patent landscaping, so our assumptions could be cross-checked with comparable disclosures. The sources listed here are illustrative only, and many other public references were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary conversations helped us convert desk signals into workable sizing inputs, particularly where public data is not reported in a consistent format across regions. We spoke with a mix of manufacturers, contract synthesis providers, distributors, and end users across pharma and biotech, hospitals and diagnostic labs, and academic research settings, and then reconciled their inputs with the modeled volume and pricing logic across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 19% | APAC: 46% |

| Mid tier: 43% | Functional/Unit leaders: 28% | EMEA: 31% |

| Smaller Players: 19% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

The market was first built using a top-down approach where research and clinical activity indicators were translated into an addressable demand pool for oligos, and then mapped to spend across products, equipment, and services. Results were corroborated with selective bottom-up checks, such as rolling up a sample of supplier revenues, validating channel markup ranges, and testing implied average selling prices (ASP) against common order sizes and purity requirements.

Key inputs used in the model included the pace of oligonucleotide-based therapeutic pipeline progression, the share of demand coming from research versus clinical and commercial use, typical synthesis scale ranges (from small research quantities to larger batches), purification and modification intensity by application, and regional lab and biomanufacturing capacity signals. Where direct volume cues were not available, gaps were handled through conservative penetration rates tied to interview feedback, followed by sensitivity tests on ASP bands.

For forecasting, scenario analysis was used around a core set of drivers that were repeatedly validated through expert feedback, and then translated into year-by-year growth paths. The final outlook reflects how ordering patterns, required chemistries (DNA, RNA, and modified forms), and capacity expansion plans are expected to evolve, without assuming a perfect linear ramp in either volumes or prices.

Data Validation & Update Cycle

Validation was carried out through multiple checks so the final numbers stay consistent with real-world operating signals. We compared the modeled totals against independent indicators such as funding trends, clinical activity, capacity additions, and supplier commentary, and then reviewed any unusual year-to-year jumps before sign-off.

When a variance was large, follow-up outreach was triggered to recheck pricing, mix shifts, and whether a data point was being counted in products versus services. The report is refreshed annually, and interim updates are made when material events occur that can change volumes, ASPs, or supply availability. Before delivery, a final analyst pass is completed so clients receive the most recent view based on the latest available inputs.

Mordor Intelligence's Oligonucleotide Synthesis Market Estimate Compared With Other Published Estimates

Published market sizes for oligonucleotide synthesis often vary because firms do not always align on what is counted as market revenue, which year is treated as the base, and how pricing is carried forward in the forecast. Differences also show up when one estimate leans more on pipeline optimism, while another stays conservative around manufacturing constraints.

In our refresh-led process, the size is kept stable through currency timing consistency, periodic ASP rechecks (by chemistry, purity, and order scale), and repeat validation against demand signals like research funding and clinical activity, which in turn explains why Mordor Intelligence lands away from figures that rely on older price points or broader revenue buckets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.31 B (2026) | |

| Trade Journal B | USD 3.64 B (2025) | Uses a different base year and a product and service scope that may treat services like purification or custom synthesis differently, which can shift the starting value before forecasting even begins. |

| Industry Research Group A | USD 3.44 B (2024) | Earlier-year sizing can understate later-period pricing and mix changes, and the estimate appears to rely on a broader CAGR carry-forward without the same level of year-by-year ASP and currency timing normalization. |

The table shows that most of the spread comes from timing and what is bundled into revenue totals, rather than a disagreement that demand exists. By locking the scope to synthesis-related revenues and then repeatedly rechecking ASP bands and external activity signals, the resulting number stays easier to trace, reproduce, and update when market conditions shift.

Key Questions Answered in the Report

How big is the Oligonucleotide Synthesis Market?

The Oligonucleotide Synthesis Market size is expected to reach USD 4.31 billion in 2026 and grow at a CAGR of 12.11% to reach USD 7.62 billion by 2031.

What is driving the rapid growth of the oligonucleotide synthesis market?

Strong therapeutic pipelines, enzymatic production advances, and expanding CDMO capacity collectively fuel a 12.11% CAGR through 2031.

Who are the key players in Oligonucleotide Synthesis Market?

Thermo Fisher Scientific, Agilent Technologies, Merck KGaA, Bio-Synthesis Inc and Eurofins Scientific are the major companies operating in the Oligonucleotide Synthesis Market.

Which is the fastest growing region in Oligonucleotide Synthesis Market?

Asia-Pacific, led by China and South Korea, records the steepest growth thanks to multi-billion-dollar funding rounds and new manufacturing plants.

Page last updated on: