Antisense Oligonucleotides Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

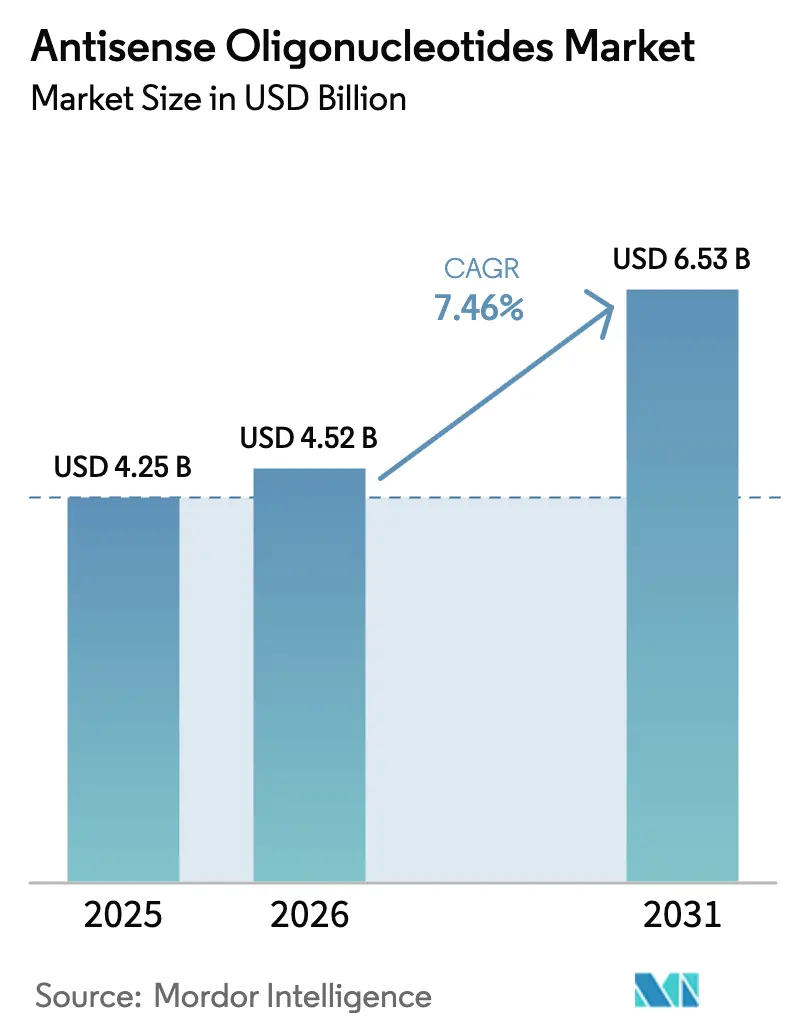

| Market Size (2026) | USD 4.52 Billion |

| Market Size (2031) | USD 6.53 Billion |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

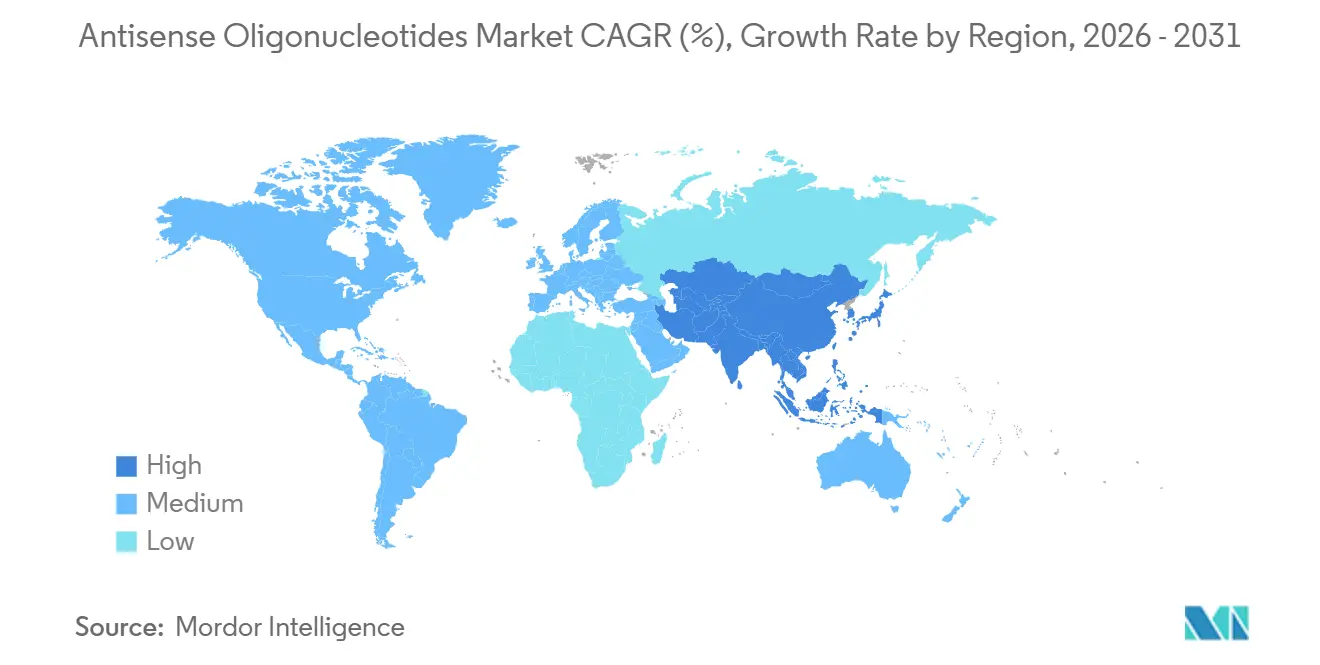

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

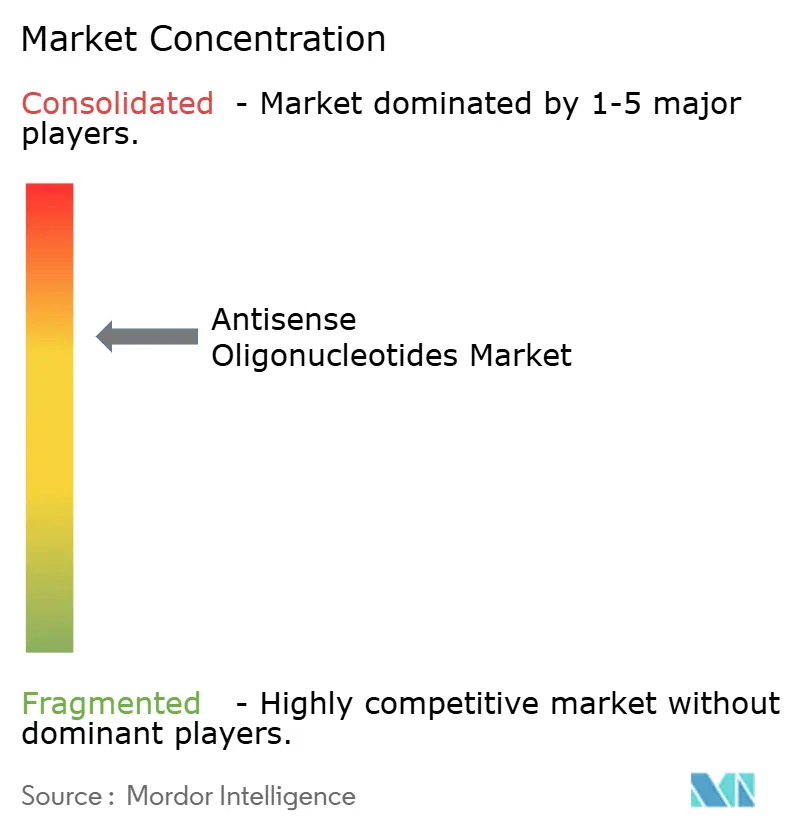

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antisense Oligonucleotides Market Analysis by Mordor Intelligence

The Antisense Oligonucleotides Market size was valued at USD 4.25 billion in 2025 and is estimated to grow from USD 4.52 billion in 2026 to reach USD 6.53 billion by 2031, at a CAGR of 7.46% during the forecast period (2026-2031).

Phosphorothioate-modified molecules currently dominate revenues, yet next-generation constrained ethyl (cEt) chemistries are expanding faster, reflecting the market’s shift toward higher potency at lower doses. Therapeutic demand remains anchored in neurological and neuromuscular disorders, though oncology pipelines are accelerating as KRAS and TP53 splice modulators progress through mid-stage trials. Clinical preference for intrathecal dosing underscores the concentration of central-nervous-system indications, while early oral candidates highlight a long-term opportunity to move chronic therapies away from injections. Outsourcing to contract research and manufacturing organizations (CROs/CMOs) is rising as sponsors seek the specialized equipment and talent needed for complex phosphoramidite synthesis.

Key Report Takeaways

- By drug chemistry, phosphorothioate-modified antisense oligonucleotides held 41.43% of antisense oligonucleotides market share in 2025. Constrained ethyl ASOs are projected to post the segment’s fastest expansion at an 11.44% CAGR through 2031.

- By therapeutic area, neurological and neuromuscular disorders generated 37.55% of 2025 revenue. Oncology applications are expected to advance at a 10.32% CAGR, the quickest among therapeutic areas.

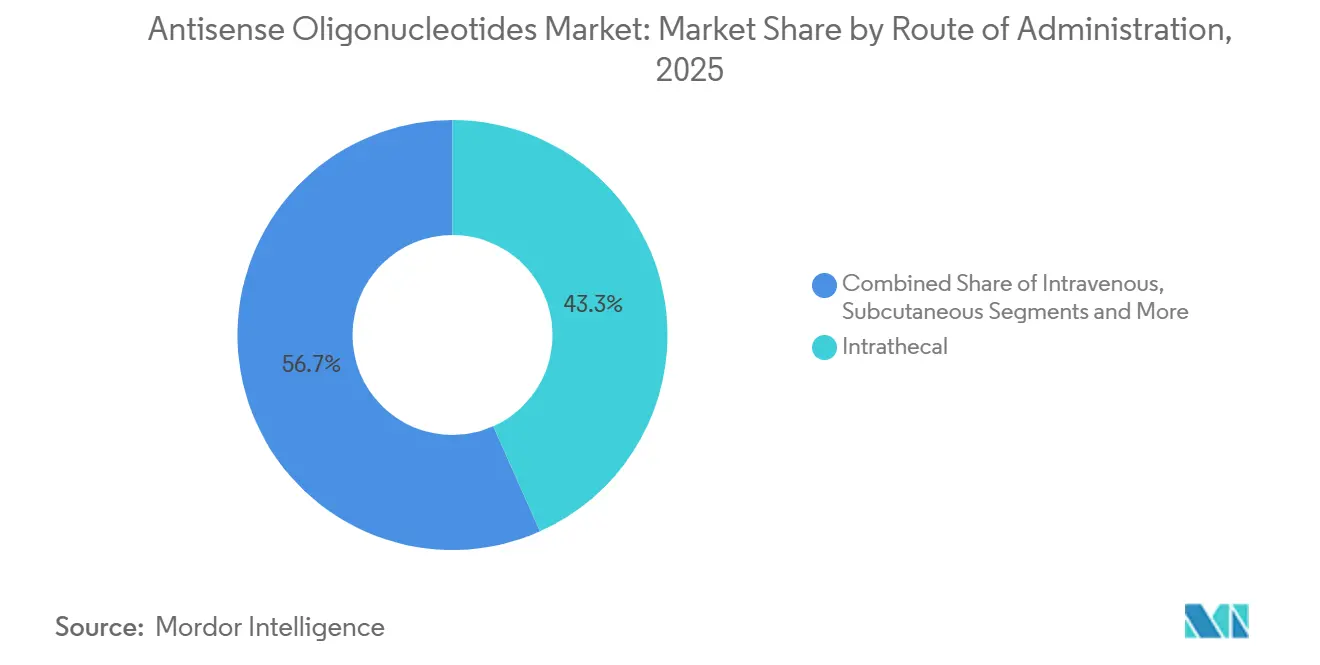

- By route of administration, intrathecal delivery captured 44.77% of 2025 sales. Oral formulations are anticipated to grow at a 9.29% CAGR, outpacing all other routes.

- By end user, academic and research institutes accounted for 39.64% of 2025 demand. CROs and CMOs are forecast to record the fastest rise, expanding at a 10.26% CAGR through 2031.

- By geography, North America contributed 56.52% of revenue in 2025. Asia-Pacific is set to achieve the highest regional growth, with a 9.13% CAGR projected over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antisense Oligonucleotides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of genetic and rare disorders | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Increasing FDA/EMA approvals of ASO drugs | +1.5% | North America, Europe, spill-over APAC | Medium term (2–4 years) |

| Advances in oligonucleotide chemistry and delivery | +1.3% | Global | Medium term (2–4 years) |

| Growing R&D investment and big-pharma partnerships | +1.2% | North America, Europe, emerging APAC | Short term (≤ 2 years) |

| Decentralized GMP facilities lowering supply risk | +0.9% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| AI-enabled antisense design platforms | +0.8% | North America, Europe, early APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Genetic & Rare Disorders

Newborn screening programs now detect spinal muscular atrophy in 48 U.S. states and across the European Union, expanding the eligible patient pool for splice-modulating treatments by 22% since 2023. European disease registries report double-digit growth in confirmed Duchenne muscular dystrophy diagnoses, chiefly due to wider access to genetic sequencing. Huntington disease prevalence has risen to 1 in 7 500 in Western populations, but fewer than 8% of gene-positive individuals receive disease-modifying therapy. Improved imaging has uncovered a larger transthyretin amyloidosis population, with an estimated 50 000 U.S. patients now considered treatment-eligible.[1]Jeffrey W. Clark, “Transthyretin Amyloidosis Diagnosis and Imaging,” Journal of the American College of Cardiology, jacc.org Collectively, earlier genetic diagnosis is increasing the addressable base for antisense interventions across neuromuscular and cardiometabolic conditions.

Increasing FDA/EMA Approvals of ASO Drugs

The U.S. FDA granted accelerated approval to three antisense drugs in 2024, the highest annual count since nusinersen in 2016. The European Medicines Agency followed with two conditional authorizations in early 2025, both leveraging natural-history controls to shorten development cycles.[2]European Medicines Agency, “Conditional Marketing Authorizations for ASOs 2025,” ema.europa.eu Japan’s Pharmaceuticals and Medical Devices Agency added a sakigake designation specific to oligonucleotides, trimming review time to six months.[3]Pharmaceuticals and Medical Devices Agency, “Sakigake Designation for Oligonucleotide Therapeutics,” pmda.go.jp China’s first domestically developed antisense therapy secured approval in December 2025, affirming the global convergence of regulatory pathways. Faster approvals accelerate commercial uptake and reinforce sponsor confidence in the modality.

Advances in Oligonucleotide Chemistry & Delivery

Constrained ethyl backbones deliver 40% greater mRNA knockdown versus legacy 2'-O-methoxyethyl designs in primate studies. Locked-nucleic-acid gapmers conjugated to transferrin-receptor antibodies achieve three-fold higher brain penetration, bolstering programs for Huntington disease. Peptide-nucleic-acid scaffolds show negligible off-target hybridization in vitro, mitigating a long-standing safety concern. Early oral formulations reach 12% bioavailability in Phase I, a milestone that could unlock self-administered chronic dosing. Together, chemistry innovation is reducing dose frequency, enhancing tissue selectivity, and improving patient adherence.

Growing R&D Investment & Big-Pharma Partnerships

Novartis committed USD 2.9 billion in upfront and milestone payments to Ionis across four antisense deals, emphasizing cardiovascular and renal targets. Sanofi invested USD 450 million to build a dedicated oligonucleotide plant in Massachusetts, while GlaxoSmithKline entered a USD 1.2 billion co-development pact with Arrowhead. Venture funding in oligonucleotide-focused start-ups reached USD 3.4 billion in 2024, up 28% year-on-year. This capital influx de-risks clinical assets and supports pipeline breadth beyond rare neurological indications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and manufacturing costs | -0.7% | Global | Medium term (2–4 years) |

| Delivery challenges and off-target toxicities | -0.6% | Global | Long term (≥ 4 years) |

| Trade tariffs on nucleotide raw materials | -0.4% | North America, Europe, APAC | Short term (≤ 2 years) |

| Talent gap in oligo bioinformatics and production | -0.3% | Global, acute in APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Development and Manufacturing Costs

Clinical-grade phosphorothioate building blocks cost USD 80 000–USD 120 000 per kilogram, reflecting limited supplier competition. Phase III trials for rare-disease antisense drugs averaged USD 180 million in 2024, driven by lengthy natural-history comparators. Downstream purification represents up to 40% of total COGS despite efforts to adopt continuous processing. The capital intensity of GMP facilities exceeds USD 200 million, limiting participation to well-funded sponsors.

Delivery Challenges and Off-Target Toxicities

Hepatotoxicity occurred in 18% of participants receiving high-dose phosphorothioate ASOs in pooled analyses. Platelet reductions linked to off-target binding forced biweekly monitoring in cardiovascular trials. Intrathecal dosing carries a 0.5% risk of aseptic meningitis. Injection-site reactions and renal-tubular toxicity further constrain dose ceilings, narrowing eligible populations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Chemistry: Constrained Ethyl Formulations Redefine Potency Benchmarks

Phosphorothioate constructs maintained 41.43% revenue in 2025, supported by blockbuster brands such as nusinersen. Constrained ethyl designs are projected to grow at 11.44% CAGR, drawing sponsors with higher affinity and reduced off-target risk. Locked-nucleic-acid gapmers held roughly 18% share and are gaining favor for brain-penetrant applications. Phosphorodiamidate morpholinos account for about 12%, chiefly in Duchenne muscular dystrophy, whereas peptide-nucleic-acid candidates hold under 5% but attract investment for their nuclease resistance. The antisense oligonucleotides market size for constrained ethyl chemistry is forecast to widen significantly as composition-of-matter patents extend exclusivity.

Pipeline breadth indicates sustained momentum. cEt backbones deliver equivalent efficacy at one-third the dose, cutting manufacturing cost per patient. Regulatory bodies recognize cEt and LNA as distinct entities, enabling new patent estates and de-risking life-cycle management. By 2031, cEt and LNA together could surpass 60% of segment revenue, realigning the antisense oligonucleotides market toward chemistries with superior pharmacokinetics.

By Therapeutic Area: Oncology Splice Modulators Challenge Neurological Dominance

Neurological and neuromuscular disorders generated 37.55% of 2025 sales, led by spinal muscular atrophy, Duchenne muscular dystrophy, and transthyretin amyloidosis. Oncology pipelines, however, are projected to deliver a 10.32% CAGR, the fastest within the antisense oligonucleotides market. Cardiometabolic indications represent about 22% share, buoyed by APOC3 inhibitors that reduce triglycerides by up to 70%. Ophthalmology sits near 8% thanks to intravitreal programs for inherited retinal dystrophies.

Clinical proof around KRAS G12D splice modulation and TP53 exon skipping is attracting cross-disciplinary capital. The antisense oligonucleotides market size for oncology is expected to expand sharply once first-in-class approvals arrive, supported by existing chemotherapy reimbursement pathways. Meanwhile, infectious-disease and autoimmune applications remain nascent but benefit from modular design and rapid manufacturing cycles.

By Route of Administration: Oral Formulations Inch Toward Clinical Viability

Intrathecal dosing captured 44.77% share in 2025, reflecting the central-nervous-system focus of approved products. Subcutaneous injection followed at roughly 28%, favored for lipid and renal targets. Intravenous delivery contributed around 18% in acute oncology settings. Oral formulations, though still pre-commercial, are forecast for a 9.29% CAGR as bioavailability rises above the 10% threshold required for chronic diseases. The antisense oligonucleotides market share of oral products could reach high single digits by 2031 if ongoing Phase II studies confirm once-daily tablet feasibility.

Regulators require dose-proportional pharmacokinetics and stable plasma levels for oral filings, prompting sponsors to invest in enteric coatings and controlled-release matrices. Success would reposition antisense therapies as mainstream options alongside small molecules, broadening patient access.

By End User: CRO and CMO Specialization Accelerates Outsourcing Shift

Academic and research institutes accounted for 39.64% of demand in 2025, driven by public grants exceeding USD 600 million. Pharmaceutical and biotech companies held about 32% as top players funneled capital into late-stage trials. CROs and CMOs are growing at 10.26% CAGR, reflecting the antisense oligonucleotides market’s preference for specialized synthesis capacity over costly in-house builds. Hospitals and specialty clinics provided roughly 12%, primarily through intrathecal administration services.

Expanded CMO lines in Brussels, Singapore, and South Korea are expected to shorten lead times for Phase III material from 18 to under 12 months, easing a chronic bottleneck. Outsourcing rates among biotech sponsors rose from 55% in 2023 to 68% in 2025, a trajectory that mirrors the biologics sector’s maturation curve.

Geography Analysis

North America generated 56.52% of 2025 revenue as the FDA granted six priority reviews across two years and Medicare Part B reimbursed 80% of intrathecal procedure costs. Europe supplied 24%, concentrated in Germany, France, and the United Kingdom, where orphan-drug frameworks mandate reimbursement within 90 days of approval. Asia-Pacific is projected for a 9.13% CAGR as China’s National Medical Products Administration and Japan’s sakigake pathway accelerate local launches.

Middle East and Africa contributed about 3% after Saudi Arabia introduced a USD 150 million rare-disease fund. South America remained below 2% because of limited reimbursement, though Brazil approved its first antisense therapy under an expedited route. Regulatory harmonization via the International Council for Harmonisation is reducing global launch gaps from 36 to 18 months, a benefit for ultra-rare indications with geographically dispersed patients.

Regional manufacturing investments are accompanying approvals. Lonza’s Singapore plant will serve the Asia-Pacific antisense oligonucleotides market, while Catalent’s Brussels suite supports EU demand. Such capacity localization mitigates tariff exposure and positions each region for faster post-approval scale-up.

Competitive Landscape

Ionis, Biogen, Sarepta Therapeutics, together controlled major share of 2025 commercial revenue, indicating a moderately concentrated field. Ionis licensed 11 programs to large-cap partners, retaining double-digit royalties while defraying late-stage risk. Sanofi’s USD 450 million facility and Novartis’s Lonza capacity agreement signal increased vertical integration. Wave Life Sciences and Avidity Biosciences differentiate via stereopure and antibody-oligonucleotide conjugate platforms, respectively, drawing USD 600 million in combined capital.

Niche players pursue white-space indications. Antisense Therapeutics focuses on Duchenne exon 44 skipping, while Regulus Therapeutics advances microRNA inhibition. Patent cliffs loom for first-generation phosphorothioate drugs, inviting biosimilar interest, particularly from Indian and Chinese firms preparing analytical comparability packages.

Competitive intensity is highest in neurological and cardiometabolic segments, each hosting four to six overlapping programs. Oncology and autoimmune arenas remain less crowded, offering potential first-mover advantage. Overall, the antisense oligonucleotides market remains dynamic as chemistry shifts and delivery breakthroughs redraw barriers to entry.

Antisense Oligonucleotides Industry Leaders

Ionis Pharmaceuticals

Sarepta Therapeutics

Biogen

Wave Life Sciences

Alnylam Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Protalix BioTherapeutics and Secarna Pharmaceuticals formed a discovery collaboration targeting rare renal diseases.

- December 2025: Stoke Therapeutics and Biogen presented zorevunersen data supporting disease modification in Dravet syndrome.

- September 2025: Ionis reported positive pivotal data for zilganersen in Alexander disease, positioning the therapy for FDA filing.

Global Antisense Oligonucleotides Market Report Scope

Antisense oligonucleotides (ASOs) are short, synthetic nucleic acid strands (DNA or RNA, 13-30 nucleotides) designed to bind to specific RNA sequences and modulate gene expression, offering targeted therapy for genetic disorders, cancers, and viral infections.

The Antisense Oligonucleotides Market Report is segmented by Drug Chemistry, Therapeutic Area, Route of Administration, End User, and Geography. By Drug Chemistry, the market is segmented into Phosphorothioate-modified ASOs, 2'-O-methoxyethyl ASOs, Locked-Nucleic-Acid Gapmers, Constrained Ethyl ASOs, PMO Morpholino ASOs, and Peptide Nucleic Acid ASOs. By Therapeutic Area, the market is segmented into Neurological & Neuromuscular Disorders, Oncology, Cardiometabolic & Renal Disorders, Ophthalmology, Infectious Diseases, Metabolic & Endocrine Disorders, and Auto-immune Disorders. By Route of Administration, the market is segmented into Intrathecal, Intravenous, Subcutaneous, Oral, and Topical/Localised Delivery. By End User, the market is segmented into Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Specialised Clinics, and CROs & CMOs. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Phosphorothioate-modified ASOs |

| 2'-O-methoxyethyl (2'-MOE) ASOs |

| Locked-Nucleic-Acid (LNA) gapmers |

| Constrained Ethyl (cEt) ASOs |

| PMO Morpholino ASOs |

| Peptide Nucleic Acid (PNA) ASOs |

| Neurological & Neuromuscular Disorders |

| Oncology |

| Cardiometabolic & Renal Disorders |

| Ophthalmology |

| Infectious Diseases |

| Metabolic & Endocrine Disorders |

| Auto-immune Disorders |

| Intrathecal |

| Intravenous |

| Subcutaneous |

| Oral (in development) |

| Topical / Localised Delivery |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Hospitals & Specialised Clinics |

| CROs & CMOs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Chemistry | Phosphorothioate-modified ASOs | |

| 2'-O-methoxyethyl (2'-MOE) ASOs | ||

| Locked-Nucleic-Acid (LNA) gapmers | ||

| Constrained Ethyl (cEt) ASOs | ||

| PMO Morpholino ASOs | ||

| Peptide Nucleic Acid (PNA) ASOs | ||

| By Therapeutic Area | Neurological & Neuromuscular Disorders | |

| Oncology | ||

| Cardiometabolic & Renal Disorders | ||

| Ophthalmology | ||

| Infectious Diseases | ||

| Metabolic & Endocrine Disorders | ||

| Auto-immune Disorders | ||

| By Route of Administration | Intrathecal | |

| Intravenous | ||

| Subcutaneous | ||

| Oral (in development) | ||

| Topical / Localised Delivery | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Hospitals & Specialised Clinics | ||

| CROs & CMOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the antisense oligonucleotides market in 2026?

The market was valued at USD 4.52 billion in 2026 and is projected to grow to USD 6.53 billion by 2031.

Which drug chemistry is growing fastest?

Constrained ethyl formulations lead growth, with an 11.44% CAGR projected through 2031.

What therapeutic area offers the highest future upside?

Oncology shows the strongest outlook, with a 10.32% CAGR as KRAS and TP53 programs advance.

Why are CROs and CMOs gaining share?

Specialized synthesis equipment, talent shortages, and high capital costs are driving sponsors to outsource GMP production, resulting in a 10.26% CAGR for service providers.

Which region will expand most rapidly?

Asia-Pacific is forecast for a 9.13% CAGR through 2031, supported by accelerated approval pathways in China and Japan.

Are oral antisense drugs realistic?

Phase I data showing 12% bioavailability suggest oral products could achieve commercial viability for chronic indications later in the forecast period.

Page last updated on: