Polynucleotides Injectable Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 146.99 Million |

| Market Size (2030) | USD 299.02 Million |

| Growth Rate (2025 - 2030) | 15.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polynucleotides Injectable Market Analysis by Mordor Intelligence

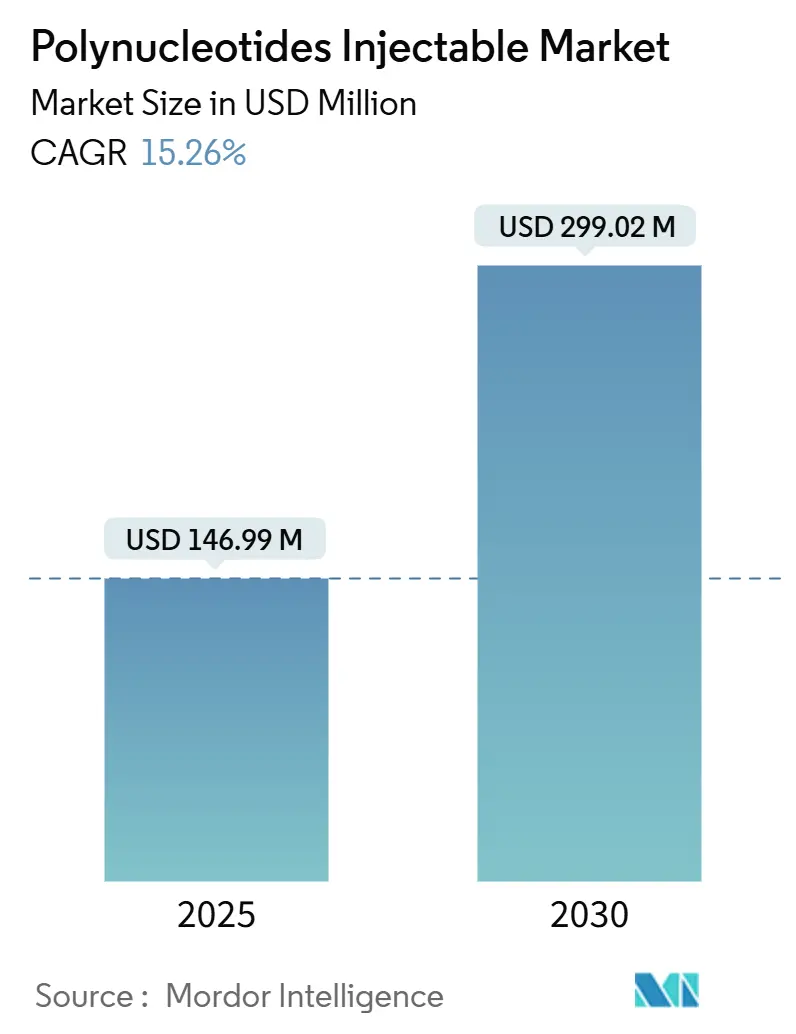

The current polynucleotides injectable market size stands at USD 146.99 million in 2025 and is expected to climb to USD 299.02 million by 2030, translating into a solid 15.26% CAGR over the forecast window. This trajectory is underpinned by mounting clinical validation that polynucleotides stimulate collagen synthesis, accelerate tissue repair, and temper inflammatory responses through adenosine A2A receptor activation.[1]Luiza Pitassi, “Polynucleotides in Skin Regeneration: Targeting the Adenosine A2A Receptor and Salvage Pathway,” Dermatologic Surgery, nature.comStrong consumer acceptance of minimally invasive procedures, rising veterinary use, and production advances that boost purity and cut costs all sustain the rapid expansion of the polynucleotides injectable market. Competitive intensity is growing as established aesthetic specialists contend with biotech entrants pursuing synthetic or recombinant DNA platforms that address sustainability and allergenicity concerns.[2]Doobyeong Chae, “Microbial-Derived Polydeoxyribonucleotide: A Sustainable Alternative,” Current Issues in Molecular Biology, mdpi.com Headwinds include premium pricing, inconsistent reimbursement, and entrenched hyaluronic-acid fillers, yet productivity gains in good-manufacturing-practice (GMP) facilities are lowering unit costs and easing regulatory scrutiny. Geography further shapes demand: North America provides established aesthetic infrastructure, Asia-Pacific posts the highest procedure volumes, and Europe couples clinical sophistication with sustainability expectations, each bolstering regional slices of the polynucleotides injectable market.

Key Report Takeaways

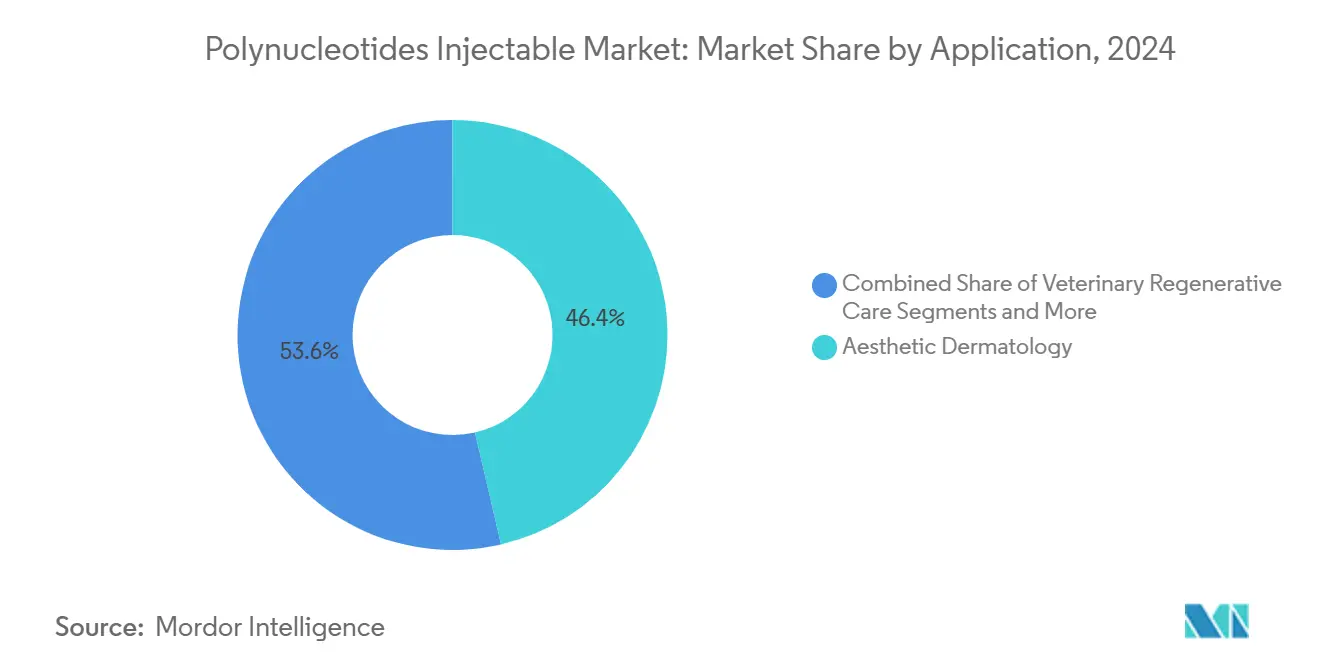

- By application, aesthetic dermatology held 46.37% of polynucleotides injectable market share in 2024, while veterinary regenerative care is projected to post the fastest 18.37% CAGR through 2030.

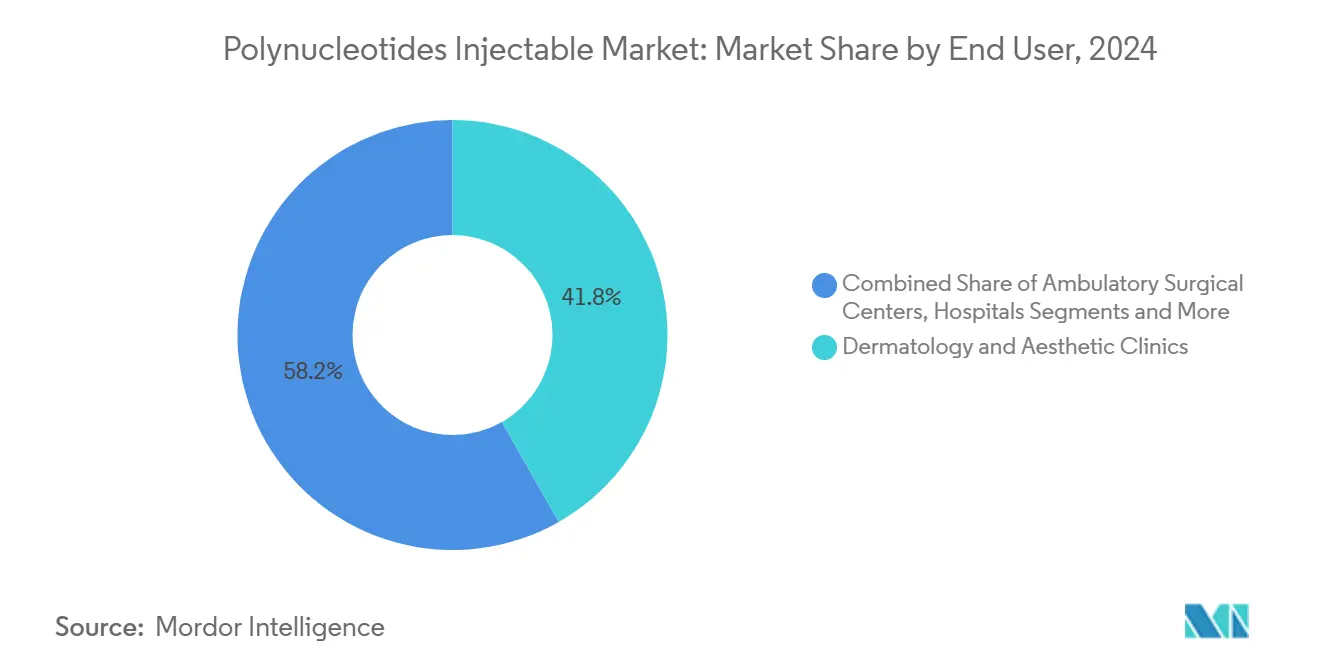

- By end user, dermatology and aesthetic clinics accounted for 41.77% of the polynucleotides injectable market size in 2024; veterinary clinics are forecast to expand at 17.38% CAGR through 2030.

- By origin, salmon-derived formulations commanded 59.27% share of the polynucleotides injectable market in 2024, but recombinant and synthetic lines are forecast to rise at 19.38% CAGR to 2030.

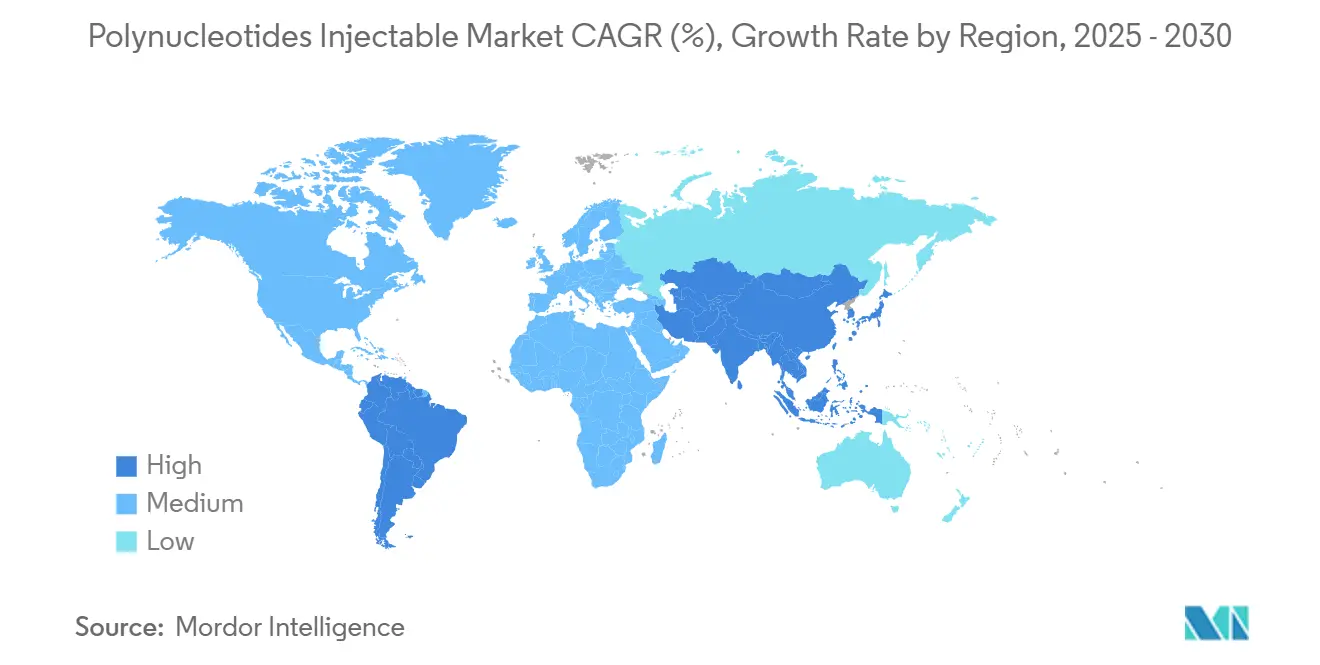

- By geography, North America led with 31.24% share in 2024; Asia-Pacific is slated to grow at a robust 17.66% CAGR during the same period.

Global Polynucleotides Injectable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally invasive regenerative aesthetic procedures | +2.8% | Global; strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Growing research evidence & regulatory approvals in dermal fillers | +2.1% | North America & Europe; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing aging population seeking anti-aging solutions | +1.9% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Advancements in GMP production improving purity & safety | +1.6% | Global; led by Europe & North America | Medium term (2-4 years) |

| Veterinary regenerative-medicine adoption | +1.4% | North America & Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Synergistic use with PRP & exosome therapies | +1.2% | Global; early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Regenerative Aesthetic Procedures

Patients increasingly favor tweaks that deliver natural-looking enhancement with limited downtime, positioning polynucleotides as an appealing option for skin rejuvenation and repair. Peer-reviewed studies confirm endogenous collagen upregulation without the volumizing effect seen in traditional fillers.[3]Matin Ahmadi, “The Efficacy of Polynucleotide Injections in Aesthetic Medicine: A Review,” PMFA Journal, thepmfajournal.com Younger consumers adopt preventive regimens that keep skin healthy rather than reverse deep wrinkles, broadening the addressable base of the injectable polynucleotides market. Post-pandemic preferences for short recovery times, social-media visibility of micro-procedures, and clinician advocacy together accelerate uptake. The driver adds momentum, especially in high-volume Asian and North American clinics, sustaining mid-term growth.

Growing Research Evidence & Regulatory Approvals in Dermal Fillers

Meta-analyses show consistent gains in skin texture, scar quality, and wound closure when polynucleotides are injected, shifting perception from experimental therapy to evidence-backed tool. U.S. and European regulators now outline clearer standards for oligonucleotide products, easing path-to-market while underlining pharmacologic rather than purely mechanical action. Pipeline trials span aesthetics, orthopedics, and wound care, enlarging the eventual label scope. Harmonized manufacturing protocols offset earlier consistency concerns, and international alignment gradually lifts cross-border barriers.

Increasing Aging Population Seeking Anti-Aging Solutions

Adults over 65 accumulate rapidly worldwide, and many wish to preserve skin integrity alongside health. Polynucleotides activate adenosine A2A receptors, promoting regenerative rather than masking effects. Higher disposable income among baby boomers, coupled with rising male participation, widens demand for premium injectables. Longevity clinics integrate polynucleotides into holistic programs that blend wellness and aesthetics, a trend expected to amplify over the long term.

Advancements in GMP Production Improving Purity & Safety

Modern chromatographic purification and microbial fermentation yield highly pure DNA fragments that meet stringent pharmacopoeia standards. Leading contract manufacturers invest in automated lines and real-time analytics, reducing batch variability and per-dose costs. Smaller fragment lengths improve bioavailability and curb immunogenicity, tackling residual safety reservations. These advances reinforce physician confidence and underpin medium-term gains for the polynucleotides injectable market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & limited reimbursement coverage | -2.4% | Global; most significant in price-sensitive markets | Medium term (2-4 years) |

| Regulatory ambiguity between drug & device classifications | -1.8% | North America & Europe; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Competition from established hyaluronic-acid fillers | -1.6% | Global; strongest in mature markets | Medium term (2-4 years) |

| Allergenic concerns over fish-derived DNA | -1.2% | Global; heightened in allergy-sensitive populations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Reimbursement Coverage

A single polynucleotide injection often costs USD 500–1,500, and regimens require multiple sessions, deterring price-sensitive consumers. Insurers rarely cover aesthetic indications, and even wound-care uses face evidence hurdles. The burden is larger in emerging economies where elective spending competes with essential care. While outcome-based pricing models could align payment with benefit, robust longitudinal data remain scarce, prolonging the restraint’s medium-term influence.

Regulatory Ambiguity Between Drug & Device Classifications

Polynucleotides straddle pharmaceutical and device definitions: some agencies judge them biological due to receptor activity, others view them as filler devices because they are injected locally. Divergent dossiers inflate development budgets and delay launches, especially for small firms. Manufacturing standards differ by pathway, adding compliance complexity. Until supranational guidelines converge, the polynucleotides injectable market must navigate uneven rules that temper expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Aesthetic Dermatology Leads, Veterinary Care Accelerates

Aesthetic dermatology controlled 46.37% of the polynucleotides injectable market in 2024. Clinical trials show measurable gains in skin elasticity and fine-line reduction within three months of treatment, prompting wide adoption among millennials seeking preventive care. Social-media visibility and celebrity endorsements sustain procedure growth, while combined protocols that layer polynucleotides over light-based therapies raise ticket sizes. Scar management and wound-healing programs in hospitals illustrate therapeutic breadth, and orthopedic investigators report tendon-repair benefits that may open a future musculoskeletal niche.

Veterinary regenerative care registered the fastest 18.37% CAGR outlook to 2030. Companion-animal spending climbs as owners treat pets as family, and equine practitioners adopt injectables for performance injuries. In livestock, polynucleotides shorten healing and avoid antibiotic residues, aligning with residue-free mandates. Conferences spotlight positive case reports, and regulators clarify veterinary biologic pathways, inviting new entrants and lifting segment visibility within the polynucleotides injectable market.

By End User: Clinics Dominate, Veterinary Facilities Expand Rapidly

Dermatology and aesthetic clinics captured 41.77% of global revenue in 2024, reflecting practitioner expertise, specialized devices, and strong patient pipelines. Clinics bundle polynucleotide sessions with chemical peels or micro-needling, elevating revenue per visit. Hospitals deploy injectables for complex wounds, but budget constraints limit volumes. Ambulatory surgical centers incorporate polynucleotides into minimally invasive facelifts, yet overall share remains secondary.

Veterinary clinics are set to clock a brisk 17.38% CAGR through 2030. Many invest in regenerative-medicine wings, offering polynucleotides plus stem-cell concentrates. Equine centers treat tendon and ligament trauma, while small-animal hospitals address osteoarthritis. Training programs proliferate, and supplier outreach furnishes dosing guides, together scaling clinical competence in this channel of the polynucleotides injectable market.

By Origin: Salmon-Derived Products Lead, Synthetic Alternatives Gain Ground

Salmon-derived formulations retained 59.27% share in 2024, backed by decades of safety data and optimized extraction. Suppliers refine enzymatic deproteinization and high-resolution filtration, achieving pharmaceutical-grade purity that reassures clinicians. Still, fish-based supply hinges on aquatic harvests, and environmental scrutiny grows.

Recombinant and synthetic sources are projected to grow at 19.38% CAGR, the quickest among origin types. Microbial fermentation yields DNA fragments with tighter molecular-weight profiles and lower immunogenicity, while controlled-synthesis platforms enable consistent batches suited to scale-up. Sustainability and allergen avoidance amplify appeal, helping this category seize incremental polynucleotides injectable market size by 2030.

Geography Analysis

North America led the polynucleotides injectable market with 31.24% share in 2024. The United States hosts deep practitioner networks, reimbursable wound-care trials, and large-scale GMP plants; recent investments include a USD 3 billion injectable expansion by Eli Lilly and a USD 2 billion build-out by Biogen. Canada’s public health system evaluates polynucleotides for burns, whereas Mexico leverages medical-tourism hubs to attract cost-conscious consumers from abroad. Regulatory pathways are clearer than a decade ago, but drug-device ambiguity still slows niche applications.

Europe combines aesthetic heritage with stringent quality oversight. Germany and Italy pioneer professional training, the United Kingdom pushes combination-therapy research, and France emphasizes scar-reduction grants. Sustainability priorities shape sourcing decisions, with Croma-Pharma advancing climate-neutral goals by 2035. Cross-border recognition of CE-marked devices simplifies market access, supporting a healthy growth clip.

Asia-Pacific is the fastest-growing region with a 17.66% CAGR outlook. South Korea’s competitive beauty culture accelerates technique innovation, and surveys reveal that over two-thirds of Korean dermatologists already inject polynucleotides. China’s urban clinics scale rapidly to meet middle-class demand, while local manufacturers expand oligonucleotide capacity at sites such as WuXi STA. Japan’s aging demographic sets the stage for therapeutic indications, and Australia blends research capability with high per-capita procedure counts. Collectively the bloc is set to outpace global averages and capture rising fractions of the polynucleotides injectable market.

Competitive Landscape

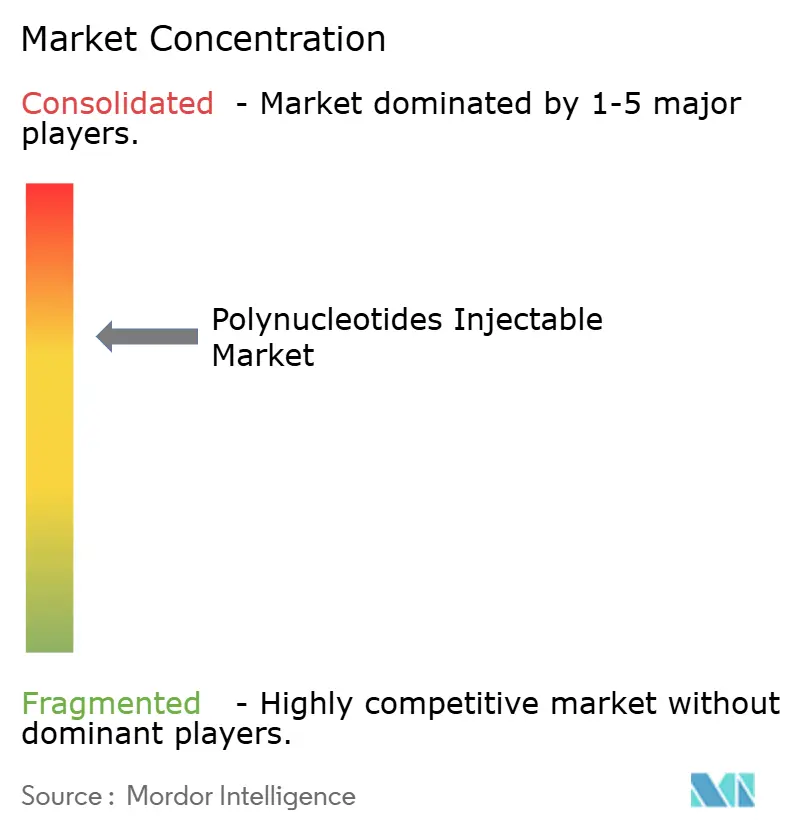

The polynucleotides injectable market is moderately concentrated. Croma-Pharma, IBSA Derma, and Mastelli together held slightly over 25% of sales in 2024. Croma-Pharma recently rebranded its PhilArt line to PolyPhil to sharpen brand recall and support global rollout. Established groups emphasize post-marketing evidence, distributor reach, and bundled supply of ancillary needles and after-care creams.

Emerging biotech firms target synthetic or microbial DNA routes, claiming enhanced antioxidant and wound-healing profiles. Several license next-generation purification modules that cut residual proteins below one part per million, a specification that appeals to regulatory auditors. Start-ups often ally with contract-development-and-manufacturing organizations to scale output while preserving capital.

Product innovation centers on multi-component injectables blending hyaluronic acid, growth factors, or exosomes with polynucleotides to capture additive benefits. Companies file patents on viscosity modifiers that improve injection ease and reduce post-procedure edema. As hybrid offerings proliferate, competition pivots on clinical differentiation rather than price alone, creating room for premium positioning across the polynucleotides injectable market.

Polynucleotides Injectable Industry Leaders

Mastelli S.r.l.

PharmaResearch Products

Croma-Pharma GmbH

Huons BioPharma

IBSA Derma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Croma-Pharma rebranded PhilArt to PolyPhil to bolster global recognition of its polynucleotide portfolio.

- January 2025: EPFL and flowbone reported a hyaluronic-acid/hydroxyapatite hydrogel that increased rat bone density four-fold and plan human trials.

- December 2024: Eli Lilly committed USD 3 billion to expand injectable-drug capacity, adding 750 jobs in 2025.

- November 2024: A case-series using Rejuran showed marked scar-texture improvement across eight patients, reinforcing dermatologic potential for polynucleotides.

Global Polynucleotides Injectable Market Report Scope

| Aesthetic Dermatology |

| Wound Healing & Scar Management |

| Orthopedics & Sports Medicine |

| Veterinary Regenerative Care |

| Hospitals |

| Dermatology & Aesthetic Clinics |

| Ambulatory Surgical Centers |

| Veterinary Clinics |

| Salmon-derived Polynucleotides |

| Mammalian-derived Polynucleotides |

| Recombinant / Synthetic Polynucleotides |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Aesthetic Dermatology | |

| Wound Healing & Scar Management | ||

| Orthopedics & Sports Medicine | ||

| Veterinary Regenerative Care | ||

| By End User | Hospitals | |

| Dermatology & Aesthetic Clinics | ||

| Ambulatory Surgical Centers | ||

| Veterinary Clinics | ||

| By Origin | Salmon-derived Polynucleotides | |

| Mammalian-derived Polynucleotides | ||

| Recombinant / Synthetic Polynucleotides | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast revenue for the polynucleotides injectable market by 2030?

The polynucleotides injectable market is projected to reach USD 299.02 million by 2030.

How fast is demand expected to grow over the next five years?

The market is set to expand at a 15.26% CAGR from 2025 to 2030.

Which application will post the strongest growth?

Veterinary regenerative care is projected to grow at an 18.37% CAGR through 2030, the fastest among all uses.

Why are synthetic polynucleotides gaining traction?

Recombinant and synthetic products avert fish-allergy concerns and support sustainability goals, driving a 19.38% CAGR outlook.

Which region shows the highest growth rate?

Asia-Pacific leads with a 17.66% CAGR, fueled by surging procedure volumes in South Korea and China.

Page last updated on: