Healthcare CDMO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

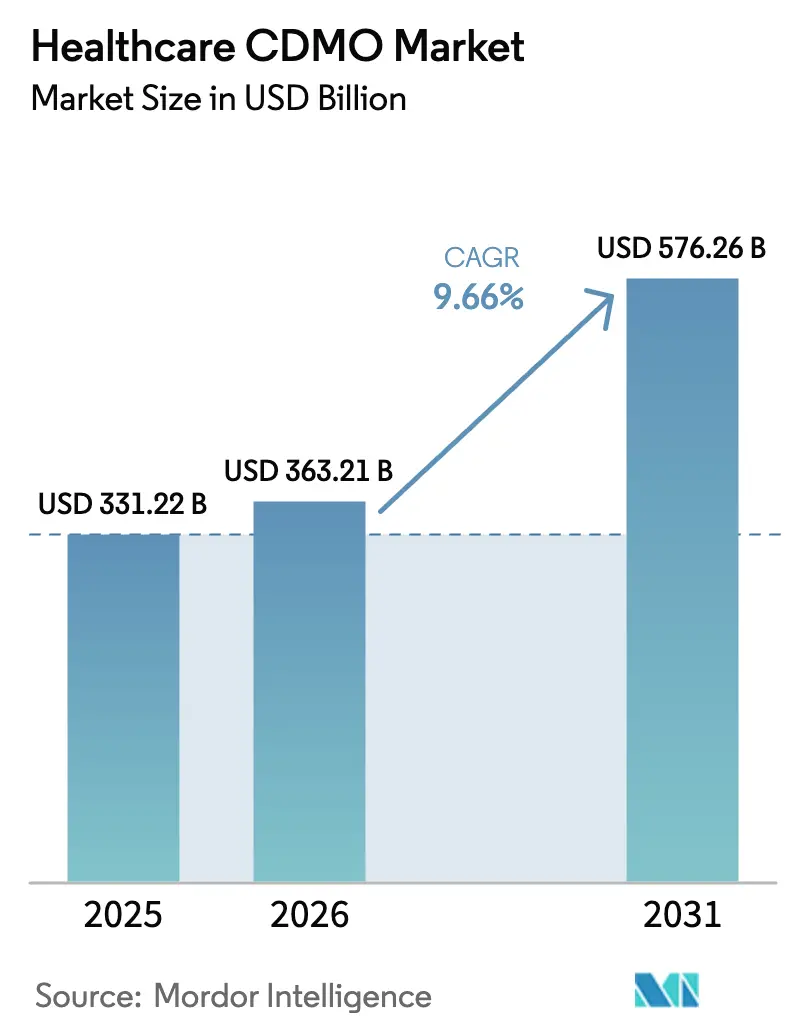

| Market Size (2026) | USD 363.21 Billion |

| Market Size (2031) | USD 576.26 Billion |

| Growth Rate (2026 - 2031) | 9.66% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare CDMO Market Analysis by Mordor Intelligence

Healthcare CDMO Market size in 2026 is estimated at USD 363.21 billion, growing from 2025 value of USD 331.22 billion with 2031 projections showing USD 576.26 billion, growing at 9.66% CAGR over 2026-2031.

This expansion underscores how biopharmaceutical companies are reallocating capital toward discovery while leaning on external partners for highly specialized production. Sustained demand for large-molecule treatments, steady regulatory endorsement of advanced manufacturing, and the widening gap between in-house capabilities and next-generation process requirements together fuel outsourcing momentum. Leading CDMOs have responded by scaling single-use and continuous platforms, embedding artificial intelligence in tech-transfer workflows, and widening late-stage support services that dovetail with accelerated approval pathways. Rapid geographic diversification of good manufacturing practice (GMP) capacity—most visibly across emerging Asia—adds a cost-efficient supply option yet reshapes the risk calculus for capacity planning. Competitive dynamics are moving from price-driven bidding toward platform differentiation, with integrated biologics and cell-therapy solutions commanding premium valuations.

Key Report Takeaways

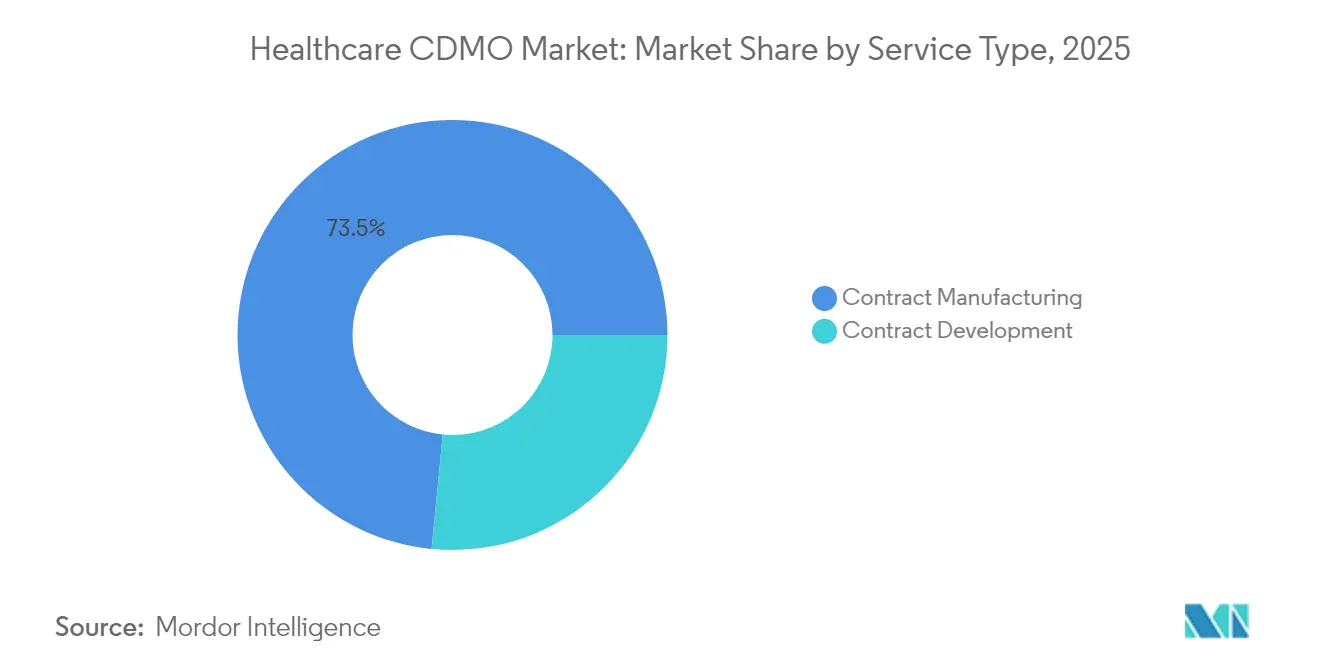

- By service type, Contract Manufacturing led with 73.45% healthcare contract development and manufacturing organization market share in 2025; Contract Development is projected to expand at a 10.44% CAGR through 2031.

- By development phase, Commercial and Post-Approval accounted for 39.35% of the healthcare contract development and manufacturing organization market size in 2025 and Phase I is advancing at a 10.78% CAGR through 2031.

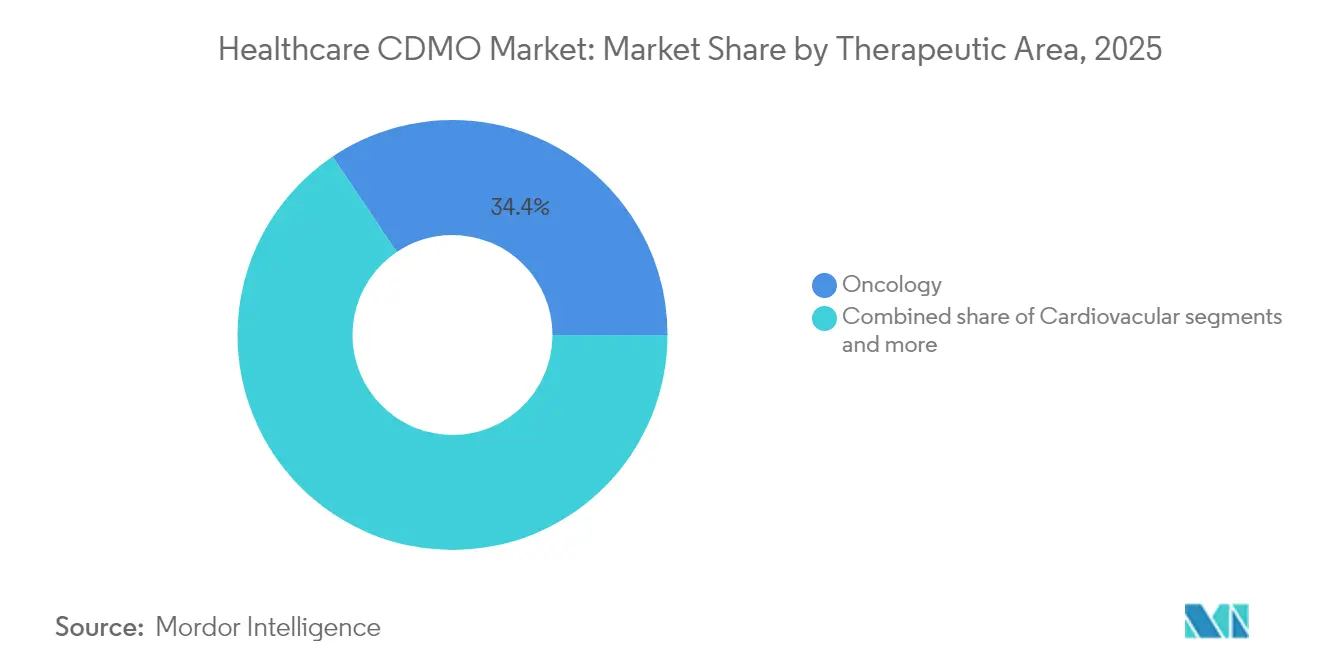

- By therapeutic area, oncology captured 34.41% share of the healthcare contract development and manufacturing organization market size in 2025 while neurology and CNS is forecast to record an 11.04% CAGR to 2031.

- By end user, Big Pharmaceutical companies held 53.10% of healthcare contract development and manufacturing organization market share in 2025; Emerging and Virtual Biotech firms are projected to grow at 11.33% CAGR between 2026 and 2031.

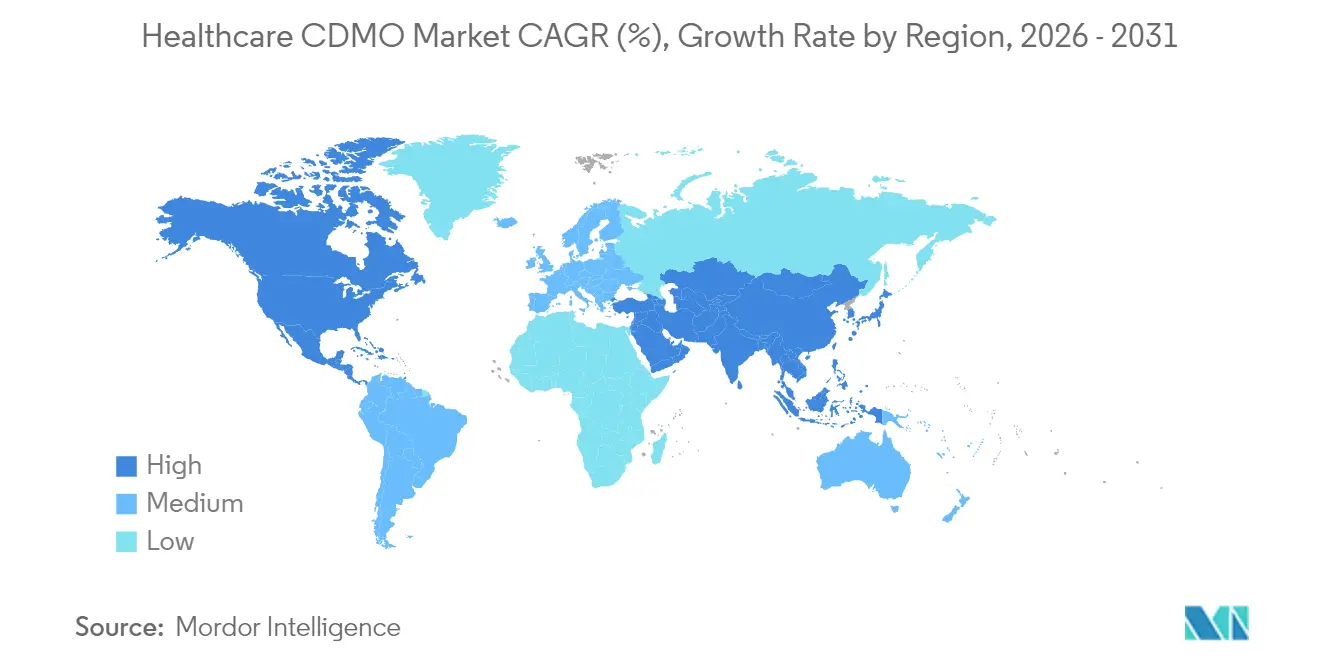

- By geography, North America commanded 41.75% share of the healthcare contract development and manufacturing organization market size in 2025 whereas Asia-Pacific is positioned to register an 11.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare CDMO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream outsourcing to focus on core competencies | +1.8% | Global, with strongest adoption in North America & Europe | Medium term (2-4 years) |

| Growth in biologics & advanced therapies | +1.2% | Global, concentrated in US, EU, and emerging Asia-Pacific | Long term (≥ 4 years) |

| Increasing molecule complexity demanding end-to-end CDMOs | +0.9% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| AI-driven process optimization slashing tech-transfer timelines | +0.7% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Single-use & continuous manufacturing boosting agile mid-tier CDMOs | +0.6% | Global, particularly benefiting Asia-Pacific facilities | Medium term (2-4 years) |

| Government incentives for GMP capacity across emerging Asia | +0.4% | Asia-Pacific core, with spillover to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream Outsourcing to Focus on Core Competencies

Rising research intensity and finite internal resources have pushed 86.9% of originators to outsource at least one manufacturing activity. Portfolio simplification enables sponsors to redeploy capital toward discovery while transferring fixed-asset risk to capable partners. Lonza’s USD 1.2 billion Vacaville acquisition, paired with the sale of its capsules unit, exemplifies the pivot toward high-value biologics focus. Large pharma is simultaneously divesting small-molecule plants, redirecting attention to first-in-class biologics and mRNA platforms. CDMOs benefit through multiyear master service agreements that underpin utilization planning and unlock cross-selling for analytical, regulatory, and fill-finish add-ons.

Growth in Biologics & Advanced Therapies

Monoclonal antibodies, antibody-drug conjugates (ADCs), cell, and gene therapies require cleanroom designs, containment protocols, and supply-chain orchestration few originators deem economical in-house. The FDA’s Advanced Manufacturing Technologies Designation Program finalized in 2025 further encourages novel production models, reducing approval risk for CDMOs that deploy innovative equipment. Capital intensity for viral vector suites and segregated high-potency lines drives sponsors to partner earlier, often during pre-clinical formulation. As commercial approvals of CAR-T and gene-edited products climb, so does demand for small-lot, just-in-time manufacturing and end-to-end logistics solutions that preserve cell viability.

Increasing Molecule Complexity Demanding End-to-End CDMOs

Combination products such as ADCs integrate biologic and chemical supply chains within one release specification, heightening the value of vertically integrated partners. AGC Biologics’ Proveo platform unites antibody expression, payload synthesis, conjugation, and aseptic fill-finish under a single quality system, shrinking timeline from DNA to commercial lot to 15 months. Sponsors avoid duplicated validation and mitigate regulatory questions on split-site control. Similar integrated offerings are proliferating across oligonucleotides, lipid nanoparticles, and viral vectors, strengthening switching costs and reinforcing the premium for full-scope CDMOs.

AI-Driven Process Optimization Slashing Tech-Transfer Timelines

Artificial intelligence models now interrogate multivariate datasets from upstream and downstream runs to predict optimal parameter sets in silico. The FDA announced forthcoming guidance to clarify expectations for AI-enabled process control, giving early adopters a compliance roadmap. Lonza’s collaboration with IBM leverages digital twins that iterate design-of-experiments virtually, cutting scale-up cycles by 30% and reducing material consumption. Predictive maintenance also drops unplanned downtime, lifting available capacity without new brick-and-mortar spend. Data governance and validation of self-learning algorithms remain challenges yet do not outweigh the competitive edge from reduced transfer times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capacity constraints & long CDMO lead-times | -0.6% | Global, most acute in specialized biologics manufacturing | Short term (≤ 2 years) |

| Stringent compliance / audit failures | -0.4% | Global, with heightened scrutiny in US and EU markets | Medium term (2-4 years) |

| Sustainability mandates raising green-capex | -0.3% | Europe & North America core, expanding globally | Long term (≥ 4 years) |

| Talent gaps in high-potency API engineering | -0.2% | Global, particularly acute in emerging APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capacity Constraints & Long CDMO Lead-Times

Even aggressive expansion has not fully met the surge in biologics outsourcing. Allocation windows for specialized ADC suites run 24–36 months, forcing sponsors to secure slots before Phase I readouts. Daiichi Sankyo’s USD 1 billion German ADC plant and AstraZeneca’s USD 1.5 billion project in Singapore will relieve pressure only from 2028 onward. The mismatch elevates negotiation leverage of integrated CDMOs and increases reservation fees, yet also spurs clients to pursue dual-sourcing or retain pilot capacity to protect timelines.

Stringent Compliance / Audit Failures

Regulators issued a flurry of warning letters in 2024–2025 touching sterile controls, data integrity, and quality management. Carve-outs show that remediation averages USD 14.8 million, not counting revenue loss. Heightened inspection frequency, including remote audits, adds to overhead for multi-site CDMOs juggling divergent client dossiers. Failures lead to supply interruptions that tarnish both sponsor timelines and CDMO credibility. Providers therefore invest heavily in quality-by-design, electronic batch records, and continuous monitoring systems to stay inspection-ready.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Manufacturing Dominance Faces Development Disruption

Contract Manufacturing held 73.45% of healthcare contract development and manufacturing organization market share in 2025 because large pharma historically retained formulation expertise while outsourcing volume production. The sub-segment spans small-molecule APIs, monoclonal antibody titers exceeding 15,000 L, and sterile injectables, each carrying distinct margin profiles. Demand for high-potency and cytotoxic suites pushes average selling price upward and commands multi-year take-or-pay agreements. In contrast, commoditized oral solids see price compression but still underpin line utilization.

Contract Development is forecast to post a 10.44% CAGR, reflecting earlier third-party involvement in pre-formulation, process characterization, and regulatory dossier assembly. Sponsors favor a single knowledge continuum from laboratory to commercial scale, which reduces validation repetition and eases change-control filings. The healthcare contract development and manufacturing organization market therefore sees hybrid contracts where a development retainer rolls into commercial supply options, aligning incentives for rapid technology transfer. As ADCs, vector-based vaccines, and personalized therapies proliferate, process knowledge becomes inseparable from late-stage manufacturing, blurring traditional boundaries between development and production services.

By Development Phase: Commercial Stability Meets Early-Stage Acceleration

Commercial and Post-Approval programs represented 39.35% of healthcare contract development and manufacturing organization market size in 2025, anchoring predictable revenue streams tied to approved molecules. Lifecyle-management activities such as formulation optimization or new dosage strengths sustain volumes beyond patent expiry. Price ceilings exist, yet high-margin biologics continue to offset commoditized mature brands.

Phase I work is expected to climb at 10.78% CAGR to 2031 as emerging modalities require specialized toxicology batches and flexible cleanrooms. Sponsors engage CDMOs before first-in-human dosing to hedge internal skill gaps around viral vector cGMP or mRNA encapsulation. Earlier engagement yields longer total contract duration and often positions the same partner for later commercial supply, enlarging the addressable healthcare contract development and manufacturing organization market size over the product life cycle. Phase II and III volumes grow steadily but face scheduling volatility tied to clinical success, prompting CDMOs to diversify client rosters to balance attrition risk.

By Therapeutic Area: Oncology Leadership Challenged by CNS Innovation

Oncology treatments captured 34.41% of healthcare contract development and manufacturing organization market share in 2025 because ADCs, cytotoxic payloads, and autologous cell therapies require sophisticated containment, segregated HVAC, and operator protection. Complex conjugation workflows drive premium pricing and high capital barriers, locking in clients for multiyear supply deals.

Neurology and CNS pipelines are projected to expand at 11.04% CAGR, outpacing oncology as disease-modifying therapies for Alzheimer’s and Parkinson’s advance. Blood-brain barrier penetration technologies demand nano-emulsion and lipid nanoparticle expertise that few originators possess internally. Cardiovascular, metabolic, and infectious disease programs remain steady contributors, while rare disease portfolios need agile micro-batch capability. The resulting therapeutic diversity encourages CDMOs to adopt modular suites able to switch between modalities without lengthy requalification, strengthening competitiveness in the healthcare contract development and manufacturing organization market.

By End User: Big Pharma Stability Meets Biotech Dynamism

Large Pharmaceutical companies supplied 53.10% of 2025 revenue, offering sizeable volume commitments that justify multi-reactor expansions and specialized biologics lines. These sponsors emphasize quality track record and global supply continuity, favoring CDMOs with harmonized multi-site capabilities.

Emerging and Virtual Biotech firms, though smaller in spending power, generate the fastest revenue lift at an 11.33% CAGR. Their asset-light model outsources nearly every manufacturing step, demanding integrated regulatory, CMC, and logistics support. CDMOs respond with accelerator programs, dedicated project management, and shared risk-reward fee structures. Generics manufacturers remain volume drivers but operate on thinner margins, encouraging process efficiency investments. Academic and non-profit entities sustain pre-clinical demand, especially in orphan disease and pandemic-preparedness grants, broadening the client mix within the healthcare contract development and manufacturing organization market.

Geography Analysis

North America held 41.75% of 2025 revenue, anchored by FDA familiarity, established cold-chain logistics, and concentrated sponsor headquarters. Recent capacity announcements in Syracuse and Kentucky target high-potency and sterile injectables, reflecting the region’s pivot to complex biologics rather than cost-sensitive APIs. Despite rising labor and utility costs, proximity to innovation hubs and seasoned regulatory talent keeps first-in-human and launch production onshore.

Asia-Pacific is set to post an 11.57% CAGR to 2031, driven by scale-up grants in China, Singapore, and South Korea. Government incentives lower capital hurdles for GMP suites, while competitive wages widen the cost differential with trans-Atlantic peers. Samsung Biologics added 360,000 L of capacity across Plants 4 and 5 and secured a USD 1.4 billion multi-product deal in early 2025. The region’s challenge remains regulatory harmonization, yet recent alignment with ICH guidelines has improved sponsor confidence.

Europe occupies a middle ground, pairing stringent quality culture with attractive R&D tax frameworks. Switzerland, Ireland, and Germany dominate high-value biologics, exemplified by Lonza’s ADC expansion in Visp. Eastern European sites cater to oral dose and sterile packaging at competitive rates. South America and Middle East & Africa still represent single-digit shares but win investment as part of geopolitical diversification and pandemic supply-chain resilience strategies.

Competitive Landscape

The healthcare contract development and manufacturing organization market remains moderately fragmented, yet megadeals are accelerating consolidation. Novo Holdings closed a USD 16.5 billion Catalent purchase in December 2024[1]Source: Novo Holdings, “Completion of Catalent Acquisition,” novoholdings.dk , vaulting the investor into pole position for integrated biologics. Agilent’s USD 925 million BIOVECTRA buyout adds North American viral-vector capacity[2]Source: Agilent Technologies, “Acquisition of BIOVECTRA,” agilent.com .

Scale, technology breadth, and regulatory reputation now underpin competitive leverage. Lonza, Thermo Fisher, and Samsung Biologics exceed USD 2.5 billion each in CDMO revenues, enabling continuous investment in high-throughput development labs and digital infrastructure. Mid-tier specialists differentiate through deep modality focus such as HPAPI synthesis or plasmid DNA, often partnering with logistics providers for full-chain solutions. AI adoption marks an emerging divide: early movers integrate predictive analytics into MES platforms to improve release times, while laggards risk being relegated to price-taker roles.

Future white-space opportunities include personalized vaccine manufacturing, CRISPR-based gene editing, and combination device-drug production where current capacity lags sponsor pipelines. Regulatory programs that expedite review of advanced platforms could allow nimble entrants to leapfrog scale incumbents if they prove compliance readiness. Overall, competitive intensity is shifting from capacity availability to capability differentiation within the healthcare contract development and manufacturing organization market.

Healthcare CDMO Industry Leaders

Catalent Inc.

Lonza

Recipharm AB

Thermo Fisher Scientific, Inc

Labcorp Drug Development

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Samsung Biologics reported KRW 1.3 trillion (USD 975 million) Q1 2025 revenue after Plant 5 start-up and signed a USD 1.4 billion multi-year molecule contract

- January 2025: WuXi Biologics secured a USD 925 million agreement with Candid Therapeutics for antibody production

Global Healthcare CDMO Market Report Scope

Healthcare contract development and manufacturing organization (CDMO) provides services to pharmaceutical, biotechnology, and medical device companies. These services often include developing, manufacturing, and testing medical products. CDMOs play a crucial role in the healthcare industry by offering specialized expertise and infrastructure to help bring new drugs and medical devices to market efficiently and safely.

The Healthcare Contract Development and Manufacturing Organization Market is Segmented By Services (Contract Development (Small Molecule (Preclinical (Bioanalysis and DMPK Studies, Toxicology Testing, and Other Preclinical Services) Clinical (Phase I, Phase II, Phase III, and Phase IV), Large Molecule (Cell Line development, Process Development (Upstream (Microbial, Mammalian, and Others), and Downstream (MABs, Recombinant Proteins, and Others) and Others) and (Contract Manufacturing (Small Molecule, Large Molecule (MABs, Recombinant Protein, and Others), High Potency API, Finished Dose Formulations (Solid Dose Formulation, Liquid Dose Formulation, and Injectable Dose Formulation), and Medical Devices (Class I, Class II, and Class III)), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD) for the above segments. The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

| Contract Development | Pre-formulation & Formulation Development | ||

| Process Development & Optimisation | |||

| Analytical, Stability & Release Testing | |||

| Contract Manufacturing | API Manufacturing | Small-molecule APIs | Monoclonal Antibodies |

| Large-molecule / Biologic APIs | Recombinant Proteins | ||

| Finished Dosage Formulation | Vaccines | ||

| Oral Solids (Tablets, Capsules) | Cell & Gene Therapies | ||

| Sterile Injectables / Fill-Finish | |||

| Topicals & Semi-solids | |||

| Other Dosage Forms | |||

| Packaging & Serialization Services | |||

| Medical Devices | Class I | ||

| Class II | |||

| Class III | |||

| Oncology |

| Cardiovascular |

| Infectious Diseases |

| Neurology / CNS |

| Auto-immune & Inflammatory |

| Metabolic Disorders (Diabetes, Obesity) |

| Rare & Orphan Diseases |

| Other Therapeutic Areas |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Commercial / Post-Approval |

| Big / Large Pharmaceutical Companies |

| Emerging & Virtual Biotech Firms |

| Generic Drug Manufacturers |

| Medical-Device & Combination-Product Firms |

| Academic, Government & Non-Profit Sponsors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Contract Development | Pre-formulation & Formulation Development | ||

| Process Development & Optimisation | ||||

| Analytical, Stability & Release Testing | ||||

| Contract Manufacturing | API Manufacturing | Small-molecule APIs | Monoclonal Antibodies | |

| Large-molecule / Biologic APIs | Recombinant Proteins | |||

| Finished Dosage Formulation | Vaccines | |||

| Oral Solids (Tablets, Capsules) | Cell & Gene Therapies | |||

| Sterile Injectables / Fill-Finish | ||||

| Topicals & Semi-solids | ||||

| Other Dosage Forms | ||||

| Packaging & Serialization Services | ||||

| Medical Devices | Class I | |||

| Class II | ||||

| Class III | ||||

| By Therapeutic Area | Oncology | |||

| Cardiovascular | ||||

| Infectious Diseases | ||||

| Neurology / CNS | ||||

| Auto-immune & Inflammatory | ||||

| Metabolic Disorders (Diabetes, Obesity) | ||||

| Rare & Orphan Diseases | ||||

| Other Therapeutic Areas | ||||

| By Development Phase | Pre-clinical | |||

| Phase I | ||||

| Phase II | ||||

| Phase III | ||||

| Commercial / Post-Approval | ||||

| By End User | Big / Large Pharmaceutical Companies | |||

| Emerging & Virtual Biotech Firms | ||||

| Generic Drug Manufacturers | ||||

| Medical-Device & Combination-Product Firms | ||||

| Academic, Government & Non-Profit Sponsors | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Middle East and Africa | GCC | |||

| South Africa | ||||

| Rest of Middle East and Africa | ||||

Key Questions Answered in the Report

How large is global CDMO revenue today?

The healthcare contract development and manufacturing organization market reached USD 363.21 billion in 2026 and is forecast to surpass USD 576.26 billion by 2031.

Which service category is expanding fastest?

Contract Development is the fastest-growing service line, set to rise at a 10.44% CAGR as sponsors engage CDMOs earlier for process development and regulatory support.

Why are ADCs important for outsourcing partners?

ADC production combines biologic expression, potent payload synthesis, conjugation, and aseptic fill-finish, creating manufacturing complexity that favors integrated CDMOs with end-to-end capabilities.

Which geographic region offers the quickest growth outlook?

Asia-Pacific is projected to grow at 11.57% CAGR through 2031 due to government incentives, cost advantages, and rising local biologics demand.

What role does artificial intelligence play in modern CDMOs?

AI augments process design, real-time control, and predictive maintenance, enabling transfers that finish months sooner while improving batch consistency and regulatory compliance.

Are capacity constraints easing soon?

Additional biologics plants are underway, yet many will not be fully online until 2028-2029, so tight capacity for high-potency and vector products is expected to persist in the near term.

Page last updated on: