Sterile Injectables CDMO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.13 Billion |

| Market Size (2031) | USD 26.92 Billion |

| Growth Rate (2026 - 2031) | 9.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

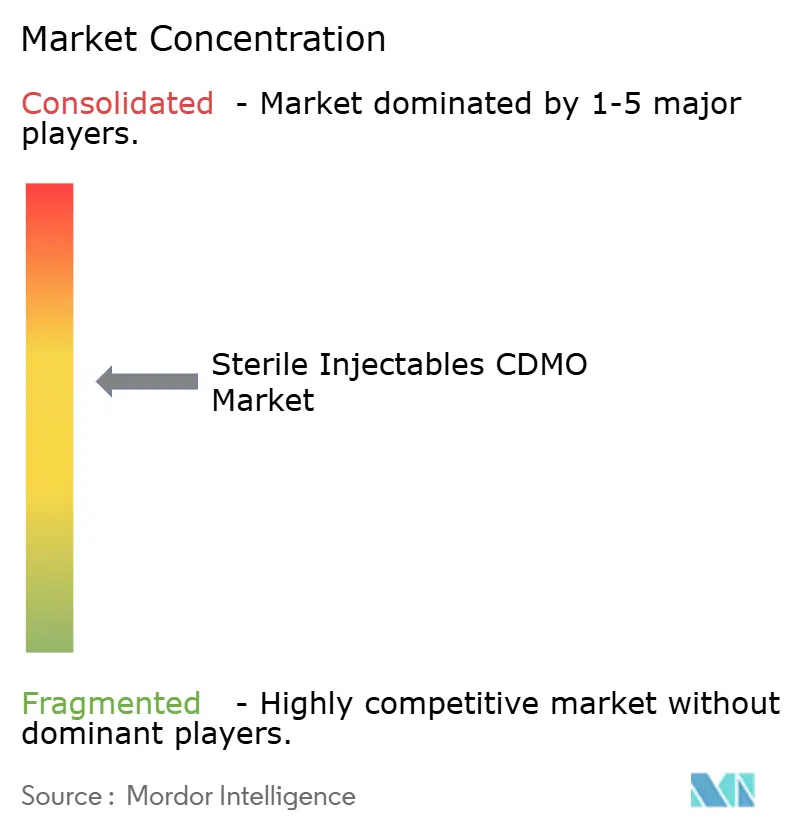

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterile Injectables CDMO Market Analysis by Mordor Intelligence

The Sterile Injectables CDMO Market size is projected to expand from USD 15.64 billion in 2025 and USD 17.13 billion in 2026 to USD 26.92 billion by 2031, registering a CAGR of 9.47% between 2026 to 2031.

Sponsors are expanding outsourcing budgets as regulatory complexity, biologics innovation, and capital scarcity make specialized partners indispensable. Mid-size pharmaceutical companies are redirecting funds from in-house suites toward flexible CDMOs that shorten launch timelines, while virtual biotech models embed external manufacturing from preclinical stages onward. CDMOs that combine end-to-end development, analytical, and high-speed fill-finish capabilities are winning long-term contracts as innovators seek supply-chain simplicity. Technology investments in isolator-based aseptic processing, continuous manufacturing, and automated inspection are emerging as the primary levers for faster batch release and regulatory confidence.

Key Report Takeaways

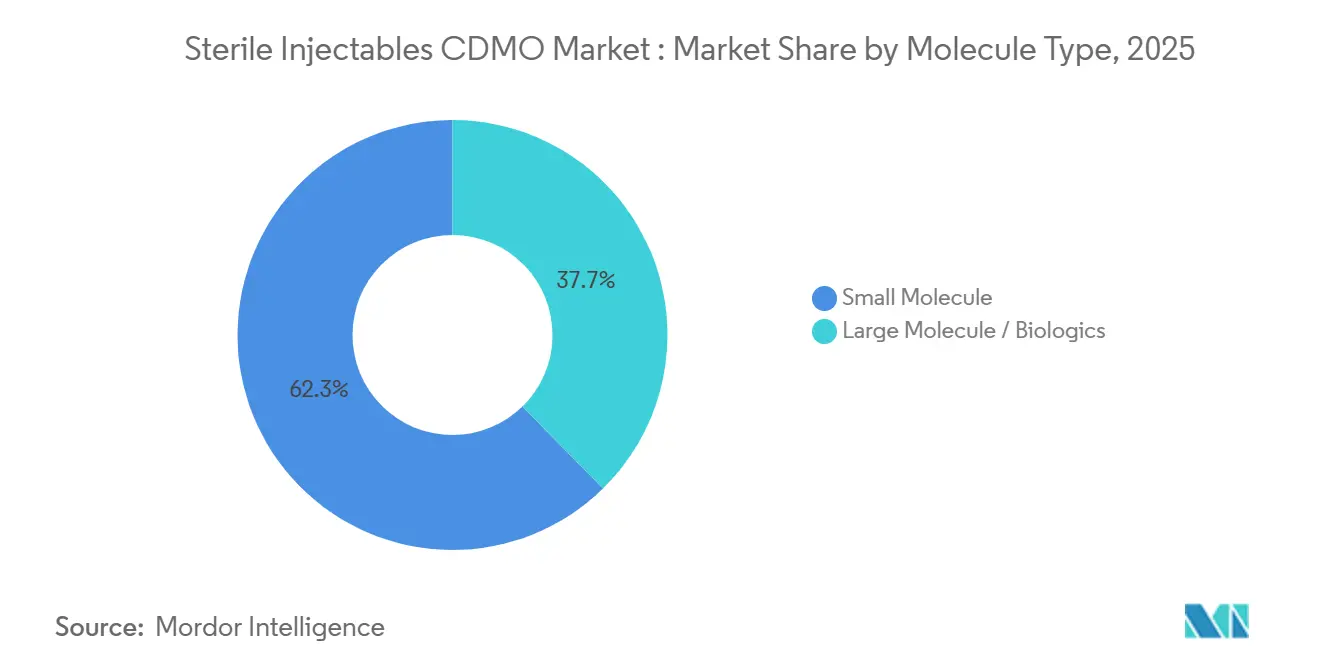

- By molecule type, small molecules captured 62.34% of the Sterile injectables CDMO market share in 2025, whereas biologics are advancing at a 10.34% CAGR through 2031.

- By service, analytical and testing led with 39.95% revenue share in 2025, while manufacturing services are forecast to expand at a 9.67% CAGR to 2031.

- By dosage form, vials and ampoules accounted for 45.01% of the Sterile injectables CDMO market size in 2025 and are growing at an 8.65% CAGR through 2031.

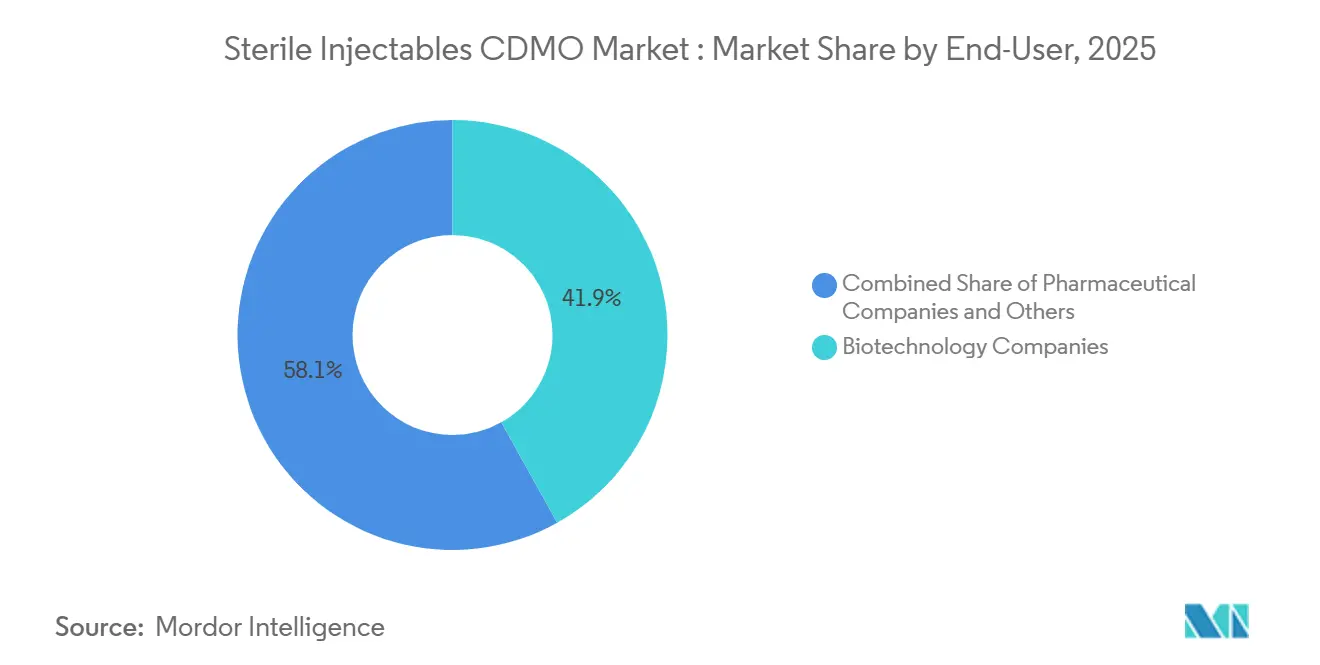

- By end-user, biotechnology companies held 41.91% of revenue in 2025 and are projected to rise at a 10.65% CAGR to 2031.

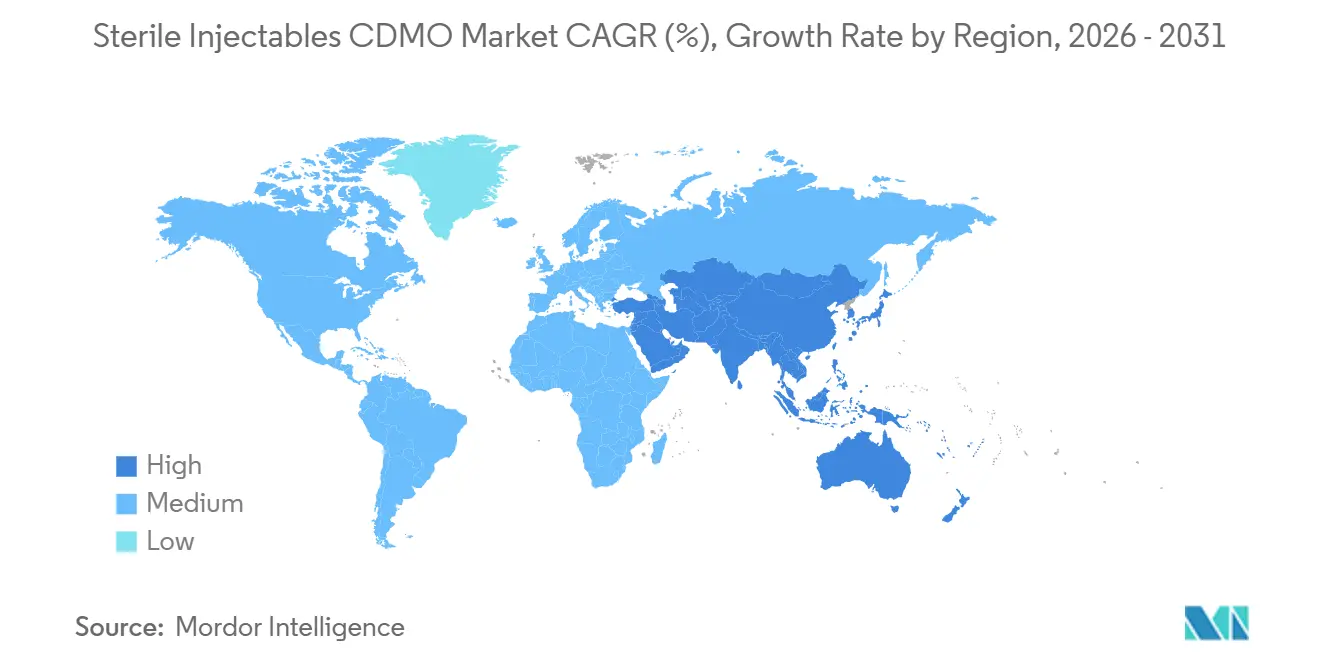

- By geography, North America commanded 45.25% revenue share in 2025, whereas the Asia-Pacific is recording the fastest regional CAGR at 10.48% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sterile Injectables CDMO Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid biologics pipeline expansion | +2.1% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Shortage of in-house aseptic capacity | +1.8% | North America and Europe with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Growing demand for ready-to-use formats | +1.5% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Heightened regulatory scrutiny | +1.4% | Global, especially EU and FDA territories | Long term (≥ 4 years) |

| Increased prevalence of chronic diseases | +1.3% | Global, aging in developed markets | Long term (≥ 4 years) |

| Automation-enabled micro-batch processing | +1.0% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Biologics Pipeline Expansion

Biologics represented about 40% of the 55 novel drugs cleared by the FDA in 2024, up from 25% five years earlier.[1]Food and Drug Administration, “New Drug Therapy Approvals 2024,” fda.gov Continuous antibody engineering, gene therapy breakthroughs, and a wave of biosimilars are pushing innovators toward partners that can manage sterile fill-finish at clinical and commercial scale. Patent expirations for agents such as adalimumab and bevacizumab have expanded biosimilar pipelines, yet very few mid-tier firms possess validated biologics suites. CDMOs with proven track records in cytotoxic handling and isolator technology are capturing disproportionate demand as antibody-drug conjugates and bispecifics require specialized containment.

Shortage of In-house Aseptic Capacity among Mid-size Pharma

Building a dedicated aseptic line can exceed USD 300 million and take up to five years. With clinical success rates near 10% for early-stage assets, many mid-size companies see limited return on such capital and therefore outsource. Industry surveys show global fill-finish utilization surpassed 85% in 2024, with lyophilization lines even higher, creating 18- to 24-month scheduling backlogs. Virtual biotech models, now more than 60% of early biologics developers, depend on CDMOs for everything from toxicology runs to commercial release.

Growing Demand for Ready-to-use (RTU) Fill-finish Formats

Ready-to-use syringes and nested vials eliminate washing and sterilization steps, lowering microbial risk and shortening cycle times. FDA guidance in 2023 explicitly endorsed RTU containers as a contamination-mitigation tool. High-value biologics, where a single lost batch can exceed USD 10 million, justify the 30%–50% premium pricing of RTU components. CDMOs that retrofit isolator lines for RTU compatibility are expanding margins and attracting innovators prioritizing sterility assurance over unit cost.

Heightened Regulatory Scrutiny Driving Outsourcing to Experts

The European Union implemented a revised Annex 1 in 2023, demanding more stringent contamination control and continuous process verification.[2]European Medicines Agency, “Annex 1 Manufacture of Sterile Medicinal Products,” ema.europa.eu Compliance upgrades cost smaller manufacturers USD 5–20 million per facility and often require new environmental monitoring infrastructure. Sponsors lacking in-house regulatory teams move production to CDMOs with multi-site GMP approvals, transferring audit risk to experienced partners. Similar dynamics follow the FDA’s 2024 aseptic guidance, making inspection readiness a core differentiator.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited global lyophilization capacity | -1.2% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Fragmented regulatory requirements in EMs | -0.9% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2–4 years) |

| Glass-vial shortages & CCI failures | -0.7% | Global, particularly North America, Europe, Asia-Pacific | Short to medium term (1–3 years) |

| Talent scarcity in high-potent aseptic suites | -1.0% | Global, most severe in North America, Europe, Asia-Pacific | Medium to long term (3–5 years) |

| Source: Mordor Intelligence | |||

Limited Global Lyophilization Capacity Causing Schedule Bottlenecks

Lyophilization remains the preferred stabilization method for heat-sensitive biologics, yet global freeze-drying capacity lags demand by an estimated 15-20%, with lead times for commercial-scale campaigns extending to 18-24 months. The capital intensity of lyophilization lines, USD 15-25 million per unit, plus 12-18 months for installation and validation, deters rapid capacity expansion, while energy costs for multi-day freeze-drying cycles have surged 30-40 % since 2022. Sponsors face a strategic choice: accept extended timelines that delay market entry or reformulate products for liquid-stable presentations, a path that requires additional regulatory filings and clinical bridging studies. CDMOs with existing lyophilization capacity leverage this scarcity to command premium pricing, yet the bottleneck constrains overall market growth. The constraint is most acute for biosimilars, where price competition limits sponsors' willingness to absorb premium CDMO fees, creating a bifurcated market where innovator biologics secure capacity while biosimilar developers queue.

Highly Fragmented Regulatory Requirements Across Emerging Markets

China’s NMPA still requires local trials for biologics, adding up to two years and USD 40 million in spend. [3]National Medical Products Administration, “Technical Guidelines for Acceptance of Overseas Clinical Trial Data,” nmpa.gov.cn Brazil’s ANVISA enforces unique stability protocols, while Gulf Cooperation Council states each demands separate GMP site inspections. CDMOs operating globally must keep parallel quality systems, inflating overhead by 20%. Smaller providers steer clear, consolidating share within multinational CDMOs yet raising costs for innovators targeting fast-growing regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule Type: Biologics Outpace Small Molecules Despite a Smaller Base

Small molecules generated 62.34% of the sterile injectables CDMO market revenue in 2025, anchored by entrenched hospital injections in anesthesia and oncology. Biologics, although starting from a lower base, are growing at a 10.34% CAGR to 2031. This momentum reflects premium pricing of USD 50,000–150,000 per patient and technical barriers that limit competition. Antibody-drug conjugates and GLP-1 analogs depend on CDMOs with cytotoxic suites, an asset held by fewer than 20 global providers. Dual-capability CDMOs that run adjacent small-molecule and biologic lines can flex capacity based on pipeline swings, but margins clearly favor biologics due to batch values and extended exclusivity.

Robust biosimilar development is another catalyst. Developers racing to seize share after patent expiry for monoclonal antibodies rely on third-party plants to meet tight launch windows. Continuous manufacturing remains nascent yet offers promise for future small-molecule cost reduction. Meanwhile, biologics outsourcing decisions hinge on cold-chain logistics and lyophilization slots, issues that magnify the importance of an integrated partner. As a result, the Sterile injectables CDMO market is seeing capital flow toward biologic capacity, though generic oncology injections still sustain base volumes in small-molecule lines.

By Services: Manufacturing Gains While Analytical Testing Plateaus

Analytical and testing services contributed 39.95% of segment revenue in 2025 as regulators tightened assay expectations for potency, endotoxin, and extractables. Yet manufacturing services are accelerating at a 9.67% CAGR because constructing new clean rooms is uneconomic for many sponsors. Modern fill-finish suites now integrate robotics for vial handling and camera-based inspection that cut operator contact and elevate output. Formulation development, though smaller, is mission-critical for viscosity reduction in concentrated biologics.

Demand for bundled contracts is rising. Sponsors prefer a single master service agreement covering formulation, analytics, and commercial batches to reduce hand-offs. Consequently, stand-alone analytical labs face slower growth unless they offer niche assays such as cell-based potency tests for gene therapies. CDMOs adopting process analytical technology for in-line release can shorten batch disposition from weeks to hours, a future competitive edge. Over the forecast, the sterile injectables CDMO market is expected to see manufacturing’s revenue share inch upward as capital investment migrates toward high-speed lines equipped for ready-to-use containers.

By Dosage Form: Vials Dominate but Prefilled Syringes Gain Share

Vials and ampoules accounted for 45.01% of the Sterile injectables CDMO market revenue in 2025, favored for versatility and hospital familiarity. Growth at an 8.65% CAGR is sustained by oncology infusions and anti-infective therapies that still rely on vial reconstitution. Prefilled syringes are accelerating fastest in relative terms as self-administration for chronic conditions expands. Biologics targeting rheumatoid arthritis or multiple sclerosis often launch directly in a prefilled device to boost adherence.

Autoinjectors and pens are proliferating and commanding special assembly lines with tighter particulate specifications. Quality hurdles remain, notably container-closure integrity failures that jeopardize sterility. CDMOs are combating the risk with laser-based leak detection and machine-vision systems, both of which increase capex but unlock higher price points for high-value biologics. As device complexity rises, partners that can integrate drug, device, and packaging validation in one facility will capture larger slices of the Sterile injectables CDMO market.

By End-User: Biotechnology Companies Lead Growth as Virtual Models Proliferate

Biotechnology companies held 41.91% of revenue in 2025 and are predicted to rise at a 10.65% CAGR to 2031. Asset-light strategies have created virtual firms that outsource everything from toxicology batches to commercial supply, embedding CDMO relationships early. Pharmaceutical companies remain significant clients but grow more slowly as they still retain some internal capacity. Academia and government agencies, notable during COVID-19, now represent a smaller yet strategic share for pandemic countermeasures.

CDMOs servicing biotech firms emphasize flexibility, routinely running 10-liter micro-batches in the same suite that shifts to 2,000-liter campaigns. Speed matters more than price, especially when venture funding is tied to clinical milestones. Conversely, large pharma seeks global networks and cost efficiency, pressing CDMOs to harmonize GMP documentation across continents. This dual mandate of flexibility and scale underscores why the sterile injectables CDMO market values partners owning multiple sites that share a common quality framework.

Geography Analysis

North America generated 45.25% of the sterile injectables CDMO market revenue in 2025, buoyed by dense biotech clusters in Boston, North Carolina, and California. Catalent’s acquisition by Novo Holdings for USD 16.5 billion, followed by Novo Nordisk purchasing three Catalent plants for USD 11.7 billion, signals vertical integration aimed at securing GLP-1 fill-finish slots. Thermo Fisher added capacity by taking over Sanofi’s Ridgefield, New Jersey site in 2025, and Vetter broke ground on a clinical plant in Illinois slated for 2029. High labor costs are a headwind, yet FDA credibility keeps North American capacity in high demand for global launches.

Europe hosts extensive aseptic facilities across Germany, France, Italy, and Spain, collectively representing regional capacity. Annex 1 revisions catalyzed facility upgrades that strengthen Europe’s reputation for quality, while France’s tax incentives are bringing fresh biologics investment. Private equity remains active, demonstrated by EQT and ADIA closing Recipharm’s purchase in 2025. Spain’s lower labor rates lure cost-sensitive projects, although regulated quality standards remain uniform across EMA states. The United Kingdom’s post-Brexit divergence introduces added documentation, but alignment on GMP keeps trade friction low.[4]Medicines and Healthcare products Regulatory Agency, “Great Britain Approved GMP Facilities,” mhra.gov.uk

Asia-Pacific is the fastest-growing region with a 10.48% CAGR through 2031. Samsung Biologics switched on its 180,000-liter Plant 5 in 2025 after investing KRW 1.9 trillion, making South Korea a leading biologics hub. WuXi Biologics is scaling multiple Chinese sites to serve domestic demand and exports. India’s large talent pool and competitive costs attract small-molecule projects, while Australia’s Pfizer plant is undergoing an AU 150 million antimicrobial upgrade, finishing in 2026. Regulatory harmonization remains a work in progress, yet steady improvements have drawn big-pharma audit approvals, reinforcing Asia-Pacific’s role in the Sterile injectables CDMO market.

Competitive Landscape

The sterile injectables CDMO market is moderately concentrated. Lonza, Novo Holdings’ Catalent, Thermo Fisher Scientific, Samsung Biologics, and WuXi Biologics collectively hold a dominant share, leaving headroom for mid-tier specialists such as Vetter, Recipharm, Siegfried, and Jubilant. Recent strategic moves underscore a shift from price competition to speed, capacity security, and technology leadership. Novo Nordisk’s site purchases protect GLP-1 supply, Samsung Biologics’ massive plant addition targets monoclonal antibodies, and Lonza is investing CHF 500 million in Vacaville to house late-stage biologics.

Technology adoption is racing ahead. Isolator-based filling lines paired with automated visual inspection cut contamination risk and operator time. Continuous manufacturing, now part of ICH Q13, offers real-time release and smaller footprints, though uptake remains limited to capital-rich CDMOs. High-potency handling for antibody-drug conjugates remains a scarce capability, granting pricing power to suppliers owning dedicated suites. Lyophilization remains another scarcity with queues stretching two years, letting incumbents command premiums during slot negotiations.

Regulatory track records have become a hard barrier to entry. Sponsors scrutinize FDA Form 483 trends and EMA certification histories before awarding multi-year contracts often exceeding USD 500 million. Smaller firms unable to upgrade quickly are partnering through alliances; for instance, fill-finish-only shops are teaming with formulation labs to bid jointly for full-service mandates. Private equity infusions, such as Signet Healthcare’s USD 25 million growth investment in RK Pharma in October 2025, are funding targeted upgrades but the window to catch up is narrowing.

Sterile Injectables CDMO Industry Leaders

Lonza Group AG

Samsung Biologics

Siegfried Holding AG

Thermo Fisher Scientific Inc. (Patheon)

WuXi Biologics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Adragos Pharma finalized the acquisition of a commercial-scale sterile fill-finish facility located in Maisons-Alfort, France, previously owned by Sanofi. The Maisons-Alfort site is recognized as one of Europe’s largest manufacturing facilities for sterile injectables, offering industrial-scale capabilities for pre-filled syringes (PFS) as well as liquid and lyophilized vials.

- December 2025: Incog BioPharma earmarked roughly USD 200 million to expand injectable capacity at its Fishers, Indiana site.

- October 2025: RK Pharma received a USD 25 million injection from Signet Healthcare Partners to scale sterile manufacturing in the United States.

Global Sterile Injectables CDMO Market Report Scope

As per scope of the report a sterile injectable CDMO is a specialized outsourcing partner that provides development, formulation, aseptic manufacturing, and fill-finish services for injectable drugs under strict sterile conditions. These organizations ensure compliance with global regulatory standards (FDA, EMA, WHO) and play a critical role in helping pharmaceutical and biotech companies bring injectable therapies to market.

The sterile injectables CDMO market segments by molecule type, services, dosage form, end-user, and geography. Molecule types include small molecule, and large molecule or biologics. By services market is segmented into formulation development, analytical and testing services, manufacturing, fill-finish & packaging, and others. By dosage forms the market is segmented into vials and ampoules, prefilled syringes, specialty injectables, to other forms. By end-users' market is segmented into of pharmaceutical companies, biotechnology companies, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Small Molecule |

| Large Molecule / Biologics |

| Formulation Development |

| Analytical and Testing Services |

| Manufacturing |

| Fill-Finish & Packaging |

| Others |

| Vials and Ampoules |

| Prefilled Syringes |

| Speciality Injectables |

| Others |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Molecule Type | Small Molecule | |

| Large Molecule / Biologics | ||

| By Services | Formulation Development | |

| Analytical and Testing Services | ||

| Manufacturing | ||

| Fill-Finish & Packaging | ||

| Others | ||

| By Dosage Form | Vials and Ampoules | |

| Prefilled Syringes | ||

| Speciality Injectables | ||

| Others | ||

| By End-User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Sterile injectables CDMO market by 2031?

The sector is forecast to reach USD 26.92 billion by 2031, growing at a 9.47% CAGR from 2026.

Which molecule class is expanding fastest in outsourced sterile injectables?

Biologics are rising at a 10.34% CAGR through 2031 thanks to biosimilars and novel modalities that require specialized fill-finish.

Why are virtual biotech firms vital to CDMO demand?

With no internal plants, virtual biotechs outsource every stage from toxicology to commercial supply, fueling double-digit CDMO revenue growth.

Which dosage forms are gaining share over vials?

Prefilled syringes and autoinjectors are advancing quickly because they enable self-administration and lower hospital costs.

What capacity constraint most limits market expansion?

Global lyophilization slots trail demand by roughly 15%, extending campaign lead times to up to two years.

Which region will grow fastest through 2031?

Asia-Pacific is on track for a 10.48% CAGR, backed by capacity additions in China, India, and South Korea.

Page last updated on: