Natural Hair Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

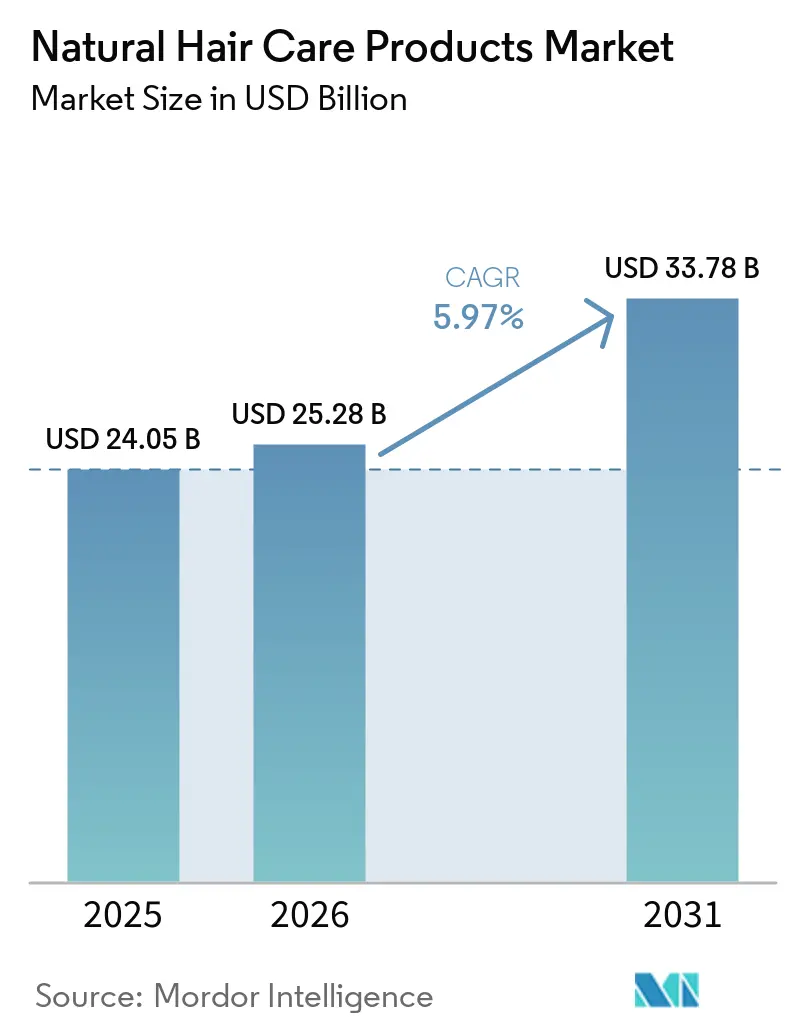

| Market Size (2026) | USD 25.28 Billion |

| Market Size (2031) | USD 33.78 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Natural Hair Care Products Market Analysis by Mordor Intelligence

The natural hair care products market size is projected to expand from USD 24.05 billion in 2025 to USD 25.28 billion in 2026, and to USD 33.78 billion by 2031, registering a CAGR of 5.9% between 2026 and 2031. This growth is driven by consumers focusing on ingredient safety, scalp tolerance, and daily use over short-term trends. In the U.S., MoCRA has increased attention on ingredient safety, while European brands are reformulating products with plant-based alternatives due to microplastics restrictions. North America leads in revenue, while Asia-Pacific shows the fastest growth, combining traditional botanical care with urban consumption. Global companies are expanding reformulated portfolios, and niche brands rely on certification, trust, and targeted positioning. Additionally, the market benefits from innovations in scalp care science, packaging compliance, and premium design, favoring brands that combine efficacy, cleaner formulations, and recyclable packaging.

Key Report Takeaways

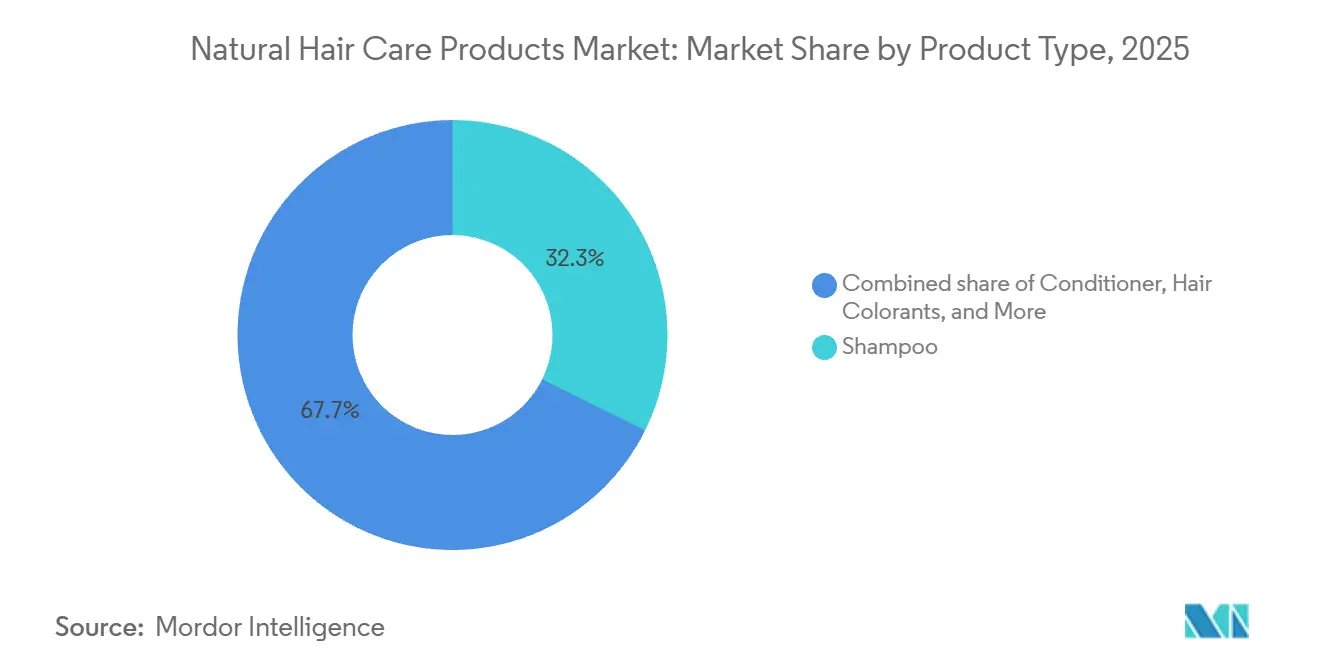

- By product type, shampoo held 32.32% of the natural hair care products market share in 2025, while hair styling products are forecast to grow at 6.23% CAGR through 2031.

- By category, premium products accounted for 55.51% share in 2025, while the mass segment is projected to expand at 6.98% CAGR through 2031.

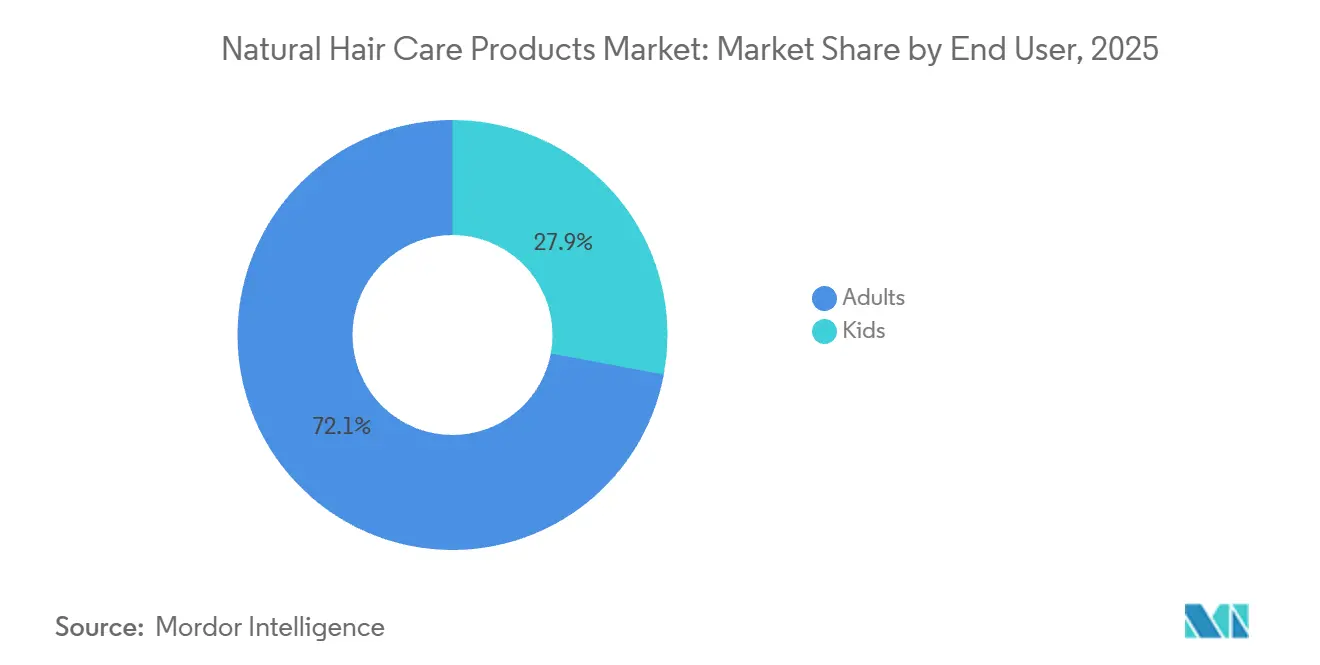

- By end user, adults represented 72.05% share in 2025, while kids are expected to grow at 7.09% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured a 36.72% share in 2025, while health and beauty stores are projected to grow at a 7.51% CAGR through 2031.

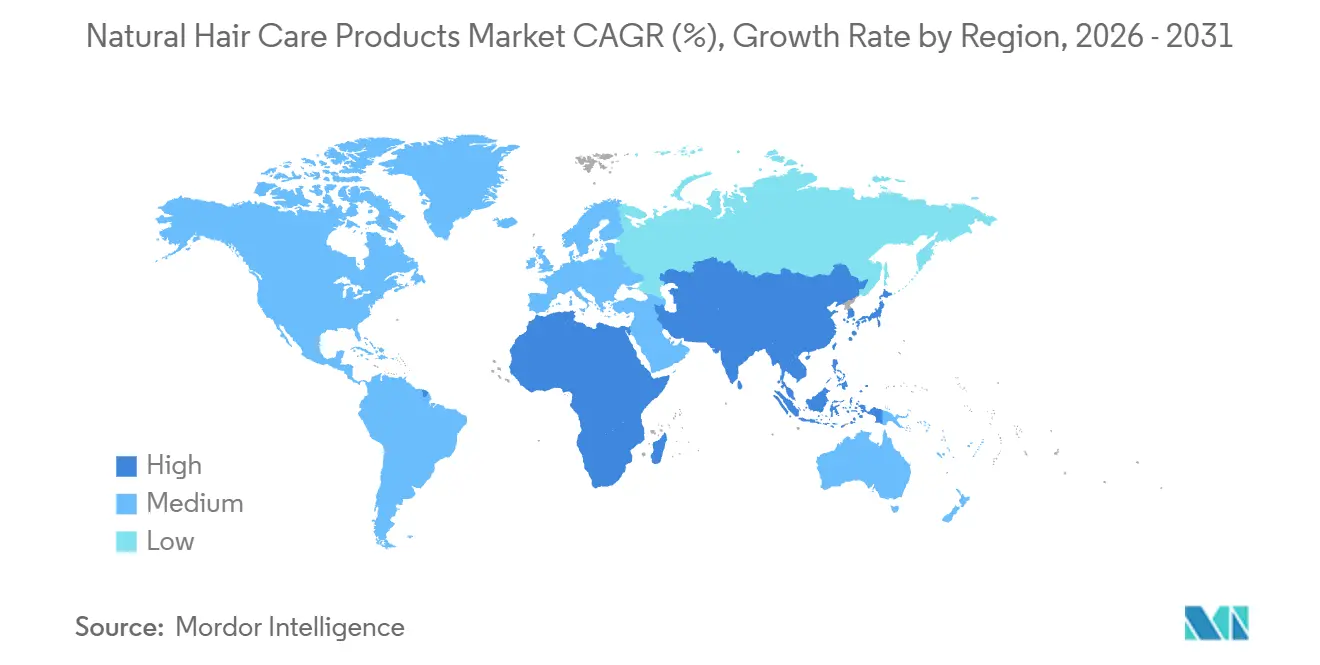

- By geography, North America accounted for 28.7% share of the natural hair care products market size in 2025, while Asia-Pacific is forecast to grow at 7.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Hair Care Products Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Consumer Awareness of Risks From Synthetic Chemicals | +1.2% | Global | Short term (≤ 2 years) |

| Rising Dermatological Concerns and Scalp Health Awareness | +1.0% | Global, strong in North America and Europe | Medium term (2-4 years) |

| Growing Emphasis on Sustainability and Eco-Friendly Practices | +0.8% | Europe and North America, spill-over to APAC | Medium term (2-4 years) |

| Expansion of E-Commerce and Online Shopping Channels | +0.7% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Innovation in New Product Launches and Formulations | +0.6% | Global, early leadership in North America and Europe | Medium term (2-4 years) |

| Adoption of COSMOS-Certified and Organic Ingredients | +0.5% | Europe-led, expanding to North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Awareness of Risks From Synthetic Chemicals

Consumer preference for avoiding synthetic ingredients has driven demand in the natural hair care products market. Buying decisions now focus on avoiding ingredients considered harsh or risky. Regulatory actions, such as MoCRA's increased federal oversight of cosmetics, have kept ingredient safety prominent in the U.S. Additionally, consumer concerns about ethylene oxide, parabens, and sulfates highlight that demand stems more from exclusionary choices than lifestyle aspirations. These exclusion-based habits are steady, as consumers link regular use to potential scalp irritation from cumulative exposure. In retail, clear communication about excluded ingredients improves shelf clarity and supports premium pricing. Over time, this trend strengthens the natural hair care market, giving compliant brands a competitive edge over conventional ones relying on older preservation or surfactant systems.

Rising Dermatological Concerns and Scalp Health Awareness

Scalp health has become a key focus in the natural hair care products market as consumers increasingly link hair quality to scalp conditions, inflammation control, and comfort. Research published in 2025 confirmed that scalp barrier conditions directly impact hair health, providing scientific support for bioactive and natural ingredient-based products. A 2026 study in Dermatology and Therapy showed significant improvements in inflammatory markers after a structured scalp care routine, strengthening the case for formulas addressing irritation and dandruff. The Cleveland Clinic demonstrated the effectiveness of clinical claims, reporting a 24-week therapeutic shampoo regimen that increased hair count by 5.68 hairs per cm² compared to a placebo. This shift is significant as buyers now seek evidence of scalp relief, resilience, and long-term hair support, beyond just natural softness. As a result, the natural hair care products market is evolving, integrating plant-based formulations, dermatological insights, and evidence-driven designs.

Growing Emphasis on Sustainability and Eco-Friendly Practices

Sustainability has become a key focus in the natural hair care products market as consumers increasingly examine how ingredients are sourced, processed, and disposed of. In 2024, Europe's Packaging and Packaging Waste Regulation heightened the importance of recyclability and packaging design, pushing beauty brands to prioritize these areas for shelf presence and regulatory compliance. The draft noted that in mature beauty markets, where certification awareness is higher, consumers remain willing to pay more for ethical and eco-friendly products. This shift impacts profit margins, brand positioning, and market access[1]Source: European Commission, “Packaging and Packaging Waste”,europa.eu. Larger, organized players gain an edge by spreading packaging and sourcing investments across multiple products. Additionally, the market's value communication now emphasizes both product composition and operational practices. Brands that align botanical sourcing, biodegradable ingredients, and compliant packaging are better positioned to maintain consumer trust amid rising scrutiny in the natural hair care market.

Adoption of COSMOS-Certified and Organic Ingredients

Certification is becoming increasingly important in the natural hair care products market, providing retailers and consumers with a reliable way to evaluate product claims. As of April 2025, the COSMOS standard certified 56,810 products and raw materials across 82 countries. Europe led with 46,212 certified items, followed by Asia with 6,514 and North America with 1,504. The framework requires minimum organic thresholds in rinse-off products and prohibits petrochemical-derived ingredients, making compliance easier for natural brands than legacy manufacturers using older formulations[2]Source: COSMOS-standard, “Leading The Way, COSMOS-Standard's Global Reach In Organic And Natural Cosmetics”, cosmos-standard.org. Certification is shifting from a marketing label to a trusted shelf entry, especially in Europe and premium retail settings. This change benefits brands investing early in ingredient traceability, documentation, and reformulation. As a result, the market may see a clear divide: certified products supporting premium claims versus alternatives struggling to prove their natural credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Shelf Life of Natural Formulations | -0.5% | Global, higher in emerging markets | Medium term (2-4 years) |

| High Competition From Established International Brands | -0.6% | Global | Short term (≤ 2 years) |

| Lack of Standardized Regulations for Natural Hair Care Products | -0.7% | Global, with partial exceptions in EU | Medium term (2-4 years) |

| Complexity in Sourcing and Maintaining Ingredient Quality | -0.5% | Highest in APAC and MEA supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Regulations for Natural Hair Care Products

In the natural hair care products market, the term "natural" varies widely across countries, retailers, and brand communications. The user-supplied draft noted that the European Union has a stronger certification culture than many regions, providing European buyers a clearer framework for evaluating claims. In less structured markets, established brands often rebrand or slightly modify products, using vague "natural" messaging to attract attention. This practice weakens price discipline, making it harder for certified products to justify premium pricing. The issue is more evident in mass retail, where shoppers make quick decisions and may not understand technical standards. Although MoCRA has improved U.S. cosmetic oversight, the market still faces inconsistent claim verification across regions and channels. As a result, trust in the natural hair care market grows more slowly in areas with limited certification awareness, rule consistency, and retailer education.

Complexity in Sourcing and Maintaining Ingredient Quality

The natural hair care products market faces supply-side challenges due to agricultural systems' vulnerability to climate variability, harvest fluctuations, and inconsistent quality control. Ingredients like amla, bhringraj, rosemary, Kalahari melon extract, and African plant oils vary by season, origin, and processing method. COSMOS control rules further complicate sourcing by requiring traceable and segregated practices, increasing costs and documentation for manufacturers. Smaller brands, with limited suppliers, struggle to manage raw material fluctuations or diversify sourcing. These issues affect product consistency, performance, shelf stability, and consumer experience if formulations are not tightly controlled. As a result, supply resilience and ingredient governance are now as critical as branding in the natural hair care products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Anchors the Category, Styling Products Grow Faster

In 2025, shampoo held a 32.32% revenue share, maintaining its lead in the natural hair care market. Its dominance is due to cleansing being the most routine and essential hair care step. High adoption rates are driven by consistent usage, widespread household penetration, and a shift from traditional sulfates to gentler, plant-based surfactants that appeal to both mainstream and premium consumers. Additionally, the growing focus on scalp health is significant, as consumers often judge products by their cleansing ability and scalp comfort before trusting them for specialized treatments. Clinical support, such as the Cleveland Clinic's findings of increased hair count after a 24-week therapeutic shampoo regimen, strengthens the case for shampoos combining natural ingredients with scalp benefits. Commercially, shampoos are the easiest product for both global brands and new entrants to scale due to repeat purchases, diverse pricing, and strong retail visibility.

Hair styling products are projected to grow at a 6.23% CAGR through 2031, making them the fastest-growing segment in the natural hair care market. This growth is driven by a shift from synthetic polymers and heavy fixatives to plant-based waxes and biodegradable materials. The transition is especially urgent in Europe, where microplastic regulations are pushing brands to innovate in achieving desired textures and finishes. Styling products balance regulatory compliance, performance, and consumer expectations. Brands that can reformulate while maintaining product feel and finish gain a competitive edge. While conditioners, hair colorants, and other products grow as the market expands into restoration and specialized treatments, ingredient substitution is most visible and impactful in the styling segment.

By Category: Premium Leads Revenue, Mass Broadens Access

In 2025, premium products accounted for 55.51% of the revenue, underscoring that the natural hair care market derives significant value from consumers prioritizing stronger claims, cleaner labels, and trusted sourcing. This premium segment has gained traction, particularly in Europe, thanks to certification systems like COSMOS, which help retailers distinguish verified natural products from their less credible counterparts. Premium positioning resonates with scalp care and treatment-led routines, as these areas benefit from detailed ingredient narratives and enhanced margin protection. Thus, in the natural hair care market, premium demand transcends mere pricing; it's deeply rooted in trust, formulation discipline, thorough documentation, and brand credibility. This trust-centric approach elucidates why premium products have thrived, even amidst selective broader consumer spending.

Projected to grow at a 6.98% CAGR through 2031, the mass segment indicates that the natural hair care market is broadening its appeal beyond niche adopters. While cost pressures persist, innovations in ingredients and broader retail acceptance are enabling natural claims to penetrate more accessible price points, all while retaining performance credibility. A case in point: Honasa Consumer, in Q4 FY26, reported a revenue of INR 682 crore (USD 81.2 million), marking a 28% year-on-year growth, with notable momentum in shampoos targeting natural hair fall care. This mass opportunity holds particular significance in South and Southeast Asia, where herbal traditions are ingrained, and volume growth can surge once price barriers diminish. Thus, the natural hair care market is evolving; it's not solely about premium conversions anymore, but also about brands adeptly scaling simplified natural offerings to vast populations.

By End User: Adults Hold the Largest Base, Kids Show the Faster Growth Rate

In 2025, adults contributed 72.05% of revenue, maintaining their position as the largest end user group in the natural hair care products market. This dominance is due to the wide range of adult needs addressed, including routine cleansing, scalp comfort, color maintenance, frizz control, curl definition, thinning concerns, and age-related hair quality issues. Adult demand varies by age: younger buyers focus on ingredient transparency and value alignment, while older consumers prioritize efficacy, scalp support, and visible hair condition. This diversity offers brands multiple entry points, driving repeat purchases across premium, mid-tier, and mass formats. Additionally, adult-focused products often act as a foundation for brand building, enabling companies to expand into treatments, scalp care systems, and family-oriented formats.

Kids are expected to grow at a 7.09% CAGR through 2031, making them the fastest-growing end user segment in the natural hair care products market. The key driver is parents’ increased scrutiny of ingredients, especially in products used frequently on sensitive scalps. Messaging around being sulfate-free, paraben-free, and tear-free holds significant appeal. For instance, in February 2026, Mielle Organics launched its Lavender & Lychee Scalp Care Collection, a dermatologist-reviewed, sulfate-free range designed for natural hair and protective styles, catering to sensitive scalp needs. The draft also noted that household buying in this segment tends to be "sticky," as parents who choose natural routines for children often remain loyal to those brands as their kids grow. This loyalty extends the customer value cycle in the natural hair care products market, with family trust serving as a retention tool rather than just an acquisition strategy.

By Distribution Channel: Supermarkets and Hypermarkets Lead, Specialty Stores Improve Mix Quality

In 2025, supermarkets and hypermarkets led the natural hair care products market, accounting for 36.72% of revenue. Their dominance is driven by routine replenishment habits, wide geographic reach, price comparison visibility, and the placement of natural products alongside conventional ones, enabling direct switching. These retailers help major manufacturers scale quickly through established logistics, promotional calendars, and disciplined shelving for personal care items. This is vital for the natural hair care market, where household penetration depends on easy access, familiar shopping missions, and confidence in finding preferred items without visiting specialist outlets. However, large-format retailers can pressure pricing and promotions, making it challenging for some natural brands to maintain margins or positioning.

Health and beauty stores, projected to grow at a 7.51% CAGR through 2031, are the fastest-growing channel in the natural hair care products market. These stores align well with the category by offering curated selections, better product education, and a shopping environment suited for discussing ingredient quality and hair type compatibility. This setting benefits premium and treatment-focused products, as buyers often seek assurances on formulations, certifications, scalp compatibility, and routine pairings before paying higher prices. Online retail and direct-to-consumer platforms further drive growth by supporting product storytelling, education-led conversions, and repeat orders. Other channels, such as pharmacies, social commerce, and subscription-based replenishments, add flexibility. Still, specialty-led selling remains crucial for protecting brand value while expanding market reach.

Geography Analysis

In 2025, North America commanded a dominant 28.7% share of the revenue, solidifying its position as the leading region in the natural hair care products market. The U.S. natural hair movement's cultural prominence, coupled with a broader acceptance of textured hair care and a robust presence in both mass and specialty retail outlets, bolstered the region's standing. Furthermore, with MoCRA intensifying scrutiny on ingredient safety and compliance in U.S. cosmetics, regulatory oversight has gained heightened visibility. Meanwhile, Europe plays a pivotal role in the natural hair care landscape, as its adoption of certifications, standards in pharmacies and specialty retail, and packaging compliance norms are redefining and rewarding the definition of natural claims.

Asia-Pacific is set to be the fastest-growing region in the natural hair care products market, with projections of a 7.9% CAGR through 2031. This growth is fueled by a blend of age-old botanical care traditions and the rapid rise of modern retail, digital accessibility, and a burgeoning middle-income urban demographic. Key players like India, China, and Southeast Asia are at the forefront, where consumers, already attuned to herbal ingredients, are now exploring a broader spectrum of branded and reformulated offerings. The market's momentum is further amplified by the cultural endorsement of brands leveraging Ayurvedic and Traditional Chinese Medicine-linked formulations for their botanical efficacy. Japan, on the other hand, emphasizes premium quality, anti-aging priorities, and meticulous formulation discipline in its hair care routines.

While South America and the Middle East and Africa hold smaller stakes in the natural hair care products market, both regions present niche opportunities. Brazil emerges as a focal point in South America, with a strong cultural affinity for curl care, textured hair routines, and plant-based moisture systems. Meanwhile, Argentina, Colombia, and Chile are catching up, bolstered by improved retail access. In the Middle East and Africa, premium spending, halal preferences, and a focus on afro-textured or dry hair types drive demand for oil-rich, moisture-intensive natural formulations. Morocco and Turkey play a strategic role, bridging European formulation standards with regional distribution and natural ingredient sourcing, catering to both compliance-driven and tradition-oriented consumers.

Competitive Landscape

The natural hair care products market is fragmented, with large multinationals dominating while smaller brands gain visibility through targeted products for specific hair types. Major players leverage their scale in R&D, manufacturing, and retail access, spreading certification and compliance costs across broader portfolios. This scale is crucial as regions tighten standards on ingredient safety, packaging, and traceability. However, smaller brands still find opportunities by building trust through precise formulations, community engagement, and transparent ingredient benefits.

Key players include Procter & Gamble, Unilever Plc, L’Oréal S.A., The Estée Lauder Companies Inc., and Honasa Consumer Limited. employ diverse strategies. At CES 2026, L'Oréal introduced the Light Straight + Multi-styler, using infrared light for premium hair protection, showcasing how large players use beauty tech for differentiation. In April 2026, Unilever's Dove launched the UV Repair & Glow Collection, demonstrating how clinically-driven designs can achieve mass distribution while maintaining a clean care message. In February 2026, Mielle Organics expanded into scalp care with its Lavender & Lychee line, showing how scaled brands retain specialization within larger systems. These developments blur the lines between premium niches and mainstream offerings, as both adopt scalp science, safety, and tailored routines.

Challenger brands thrive when they turn authenticity into repeat sales and broader reach. Honasa Consumer's FY26 report highlights strong revenue growth, rapid outlet expansion, and success with naturally positioned shampoos. Compliance readiness now acts as a competitive advantage, with documentation, sourcing control, and packaging alignment critical for regional scalability. The market favors companies combining broad distribution with disciplined formulations, while weaker claims and unstable sourcing may limit smaller players' ability to sustain market share.

Natural Hair Care Products Industry Leaders

The Procter & Gamble Company

Unilever Plc

L’Oréal S.A.

The Estée Lauder Companies Inc.

Honasa Consumer Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Arctic Fox expanded its hair color portfolio with the launch of Naturals AF, its first range of semi-permanent natural hair color shades. The collection is designed to provide salon-inspired, natural-looking hair colors for at-home users while avoiding the permanent commitment associated with traditional hair dyes. The range includes five shades: Golden Hour, Enchanted Espresso, Diet Cola, Ruby Red, and Apricot Anarchy.

- February 2026: Mielle Organics launched the Lavender & Lychee Scalp Care Collection, its first dedicated scalp care system since the Procter & Gamble acquisition, featuring dermatologist-reviewed, sulfate-free formulations with pyrithione zinc and niacinamide. The collection is available at Target, Walmart, CVS, Walgreens, Amazon, and independent beauty supply stores.

- January 2025: Mielle Organics launched the Kalahari Melon & Aloe Vera collection, a 5-product moisture retention system for textured hair, including a Deep Hydration Shampoo, 2-Minute Deep Conditioner, Leave-In Conditioner, Curl Forming Glaze, and Weightless Oil, available at major U.S. retailers at USD 15.99 per product.

Global Natural Hair Care Products Market Report Scope

| Shampoo |

| Conditioner |

| Hair Colorants |

| Hair Styling Products |

| Other Product Types |

| Premium Products |

| Mass Products |

| Adults |

| Kids |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Others Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Shampoo | |

| Conditioner | ||

| Hair Colorants | ||

| Hair Styling Products | ||

| Other Product Types | ||

| By Category | Premium Products | |

| Mass Products | ||

| By End User | Adults | |

| Kids | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Others Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the natural hair care products space be by 2031?

It is forecast to reach USD 33.78 billion by 2031, rising from USD 25.28 billion in 2026 at a 5.97% CAGR.

Which product type leads revenue today?

Shampoo leads with 32.32% share in 2025 because it remains the most routine and repeat purchase category in everyday hair care.

Which region is growing the fastest?

Asia-Pacific is the fastest growing region, with projected growth of 7.89% through 2031 as botanical heritage and urban consumption expand together.

Which distribution channel is expanding the quickest?

Health and beauty stores are growing the fastest at 7.51% CAGR because shoppers in this category often want better curation, education, and product guidance before buying.

Page last updated on: