Hair Removal Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

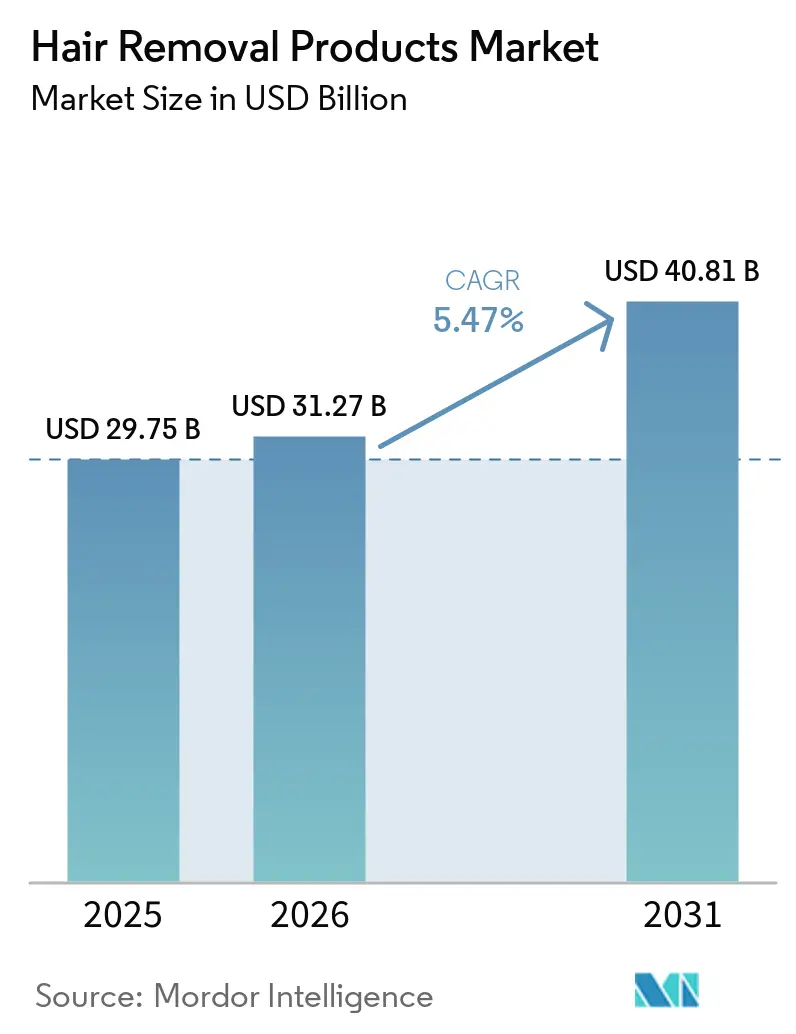

| Market Size (2026) | USD 31.27 Billion |

| Market Size (2031) | USD 40.81 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

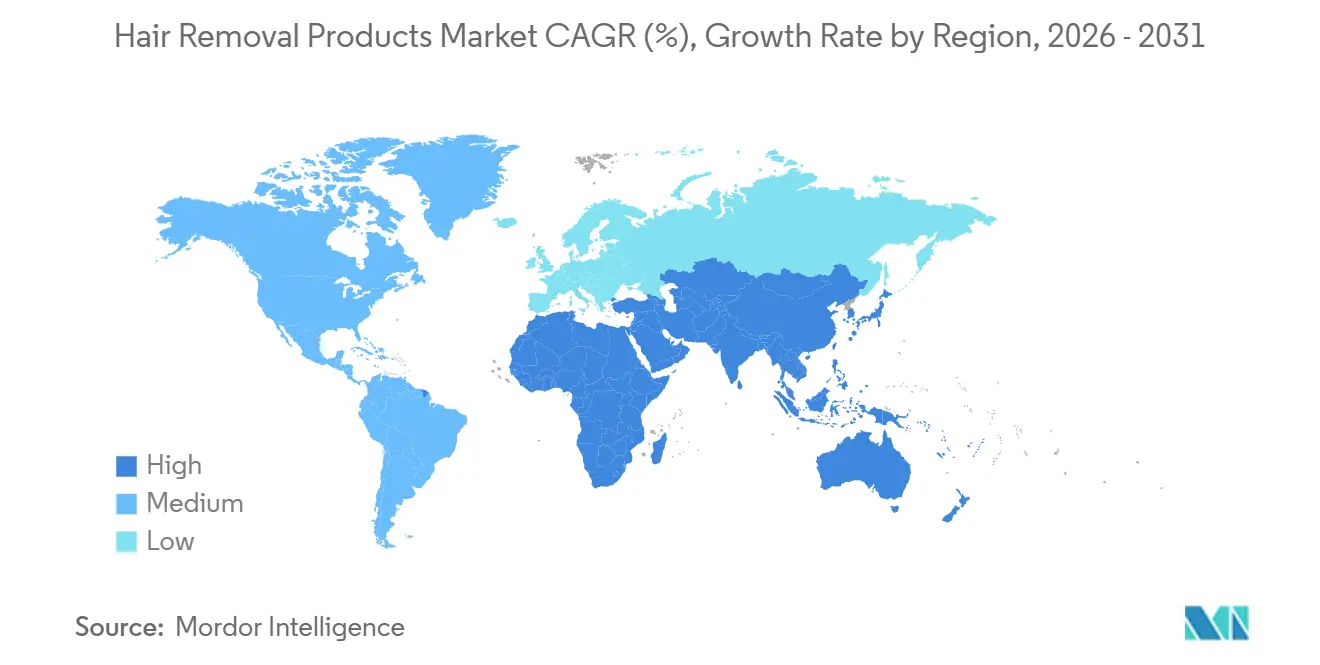

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Removal Products Market Analysis by Mordor Intelligence

The hair removal products market size is expected to increase from USD 29.75 billion in 2025 to USD 31.27 billion in 2026 and reach USD 40.81 billion by 2031, growing at a CAGR of 5.47% over 2026-2031. Durable demand combines with a consumer shift toward premium at-home devices, the harmonization of global laser‐safety rules, and steady brand investment in artificial-intelligence-enabled product upgrades. Regulatory milestones, most notably the United States FDA’s Laser Notice No. 56 and the European Union’s EN 50689:2021 standard, have lowered compliance friction for multinational manufacturers, accelerating product launches across regions. Meanwhile, North America remains the largest regional contributor, yet Asia-Pacific’s rapid urbanization and rising disposable incomes are lifting regional volumes at the fastest pace. Consolidation among professional-equipment suppliers and incremental innovations in razors, blades, and smart IPL devices keep competitive pressure moderate while still leaving room for new entrants.

Key Report Takeaways

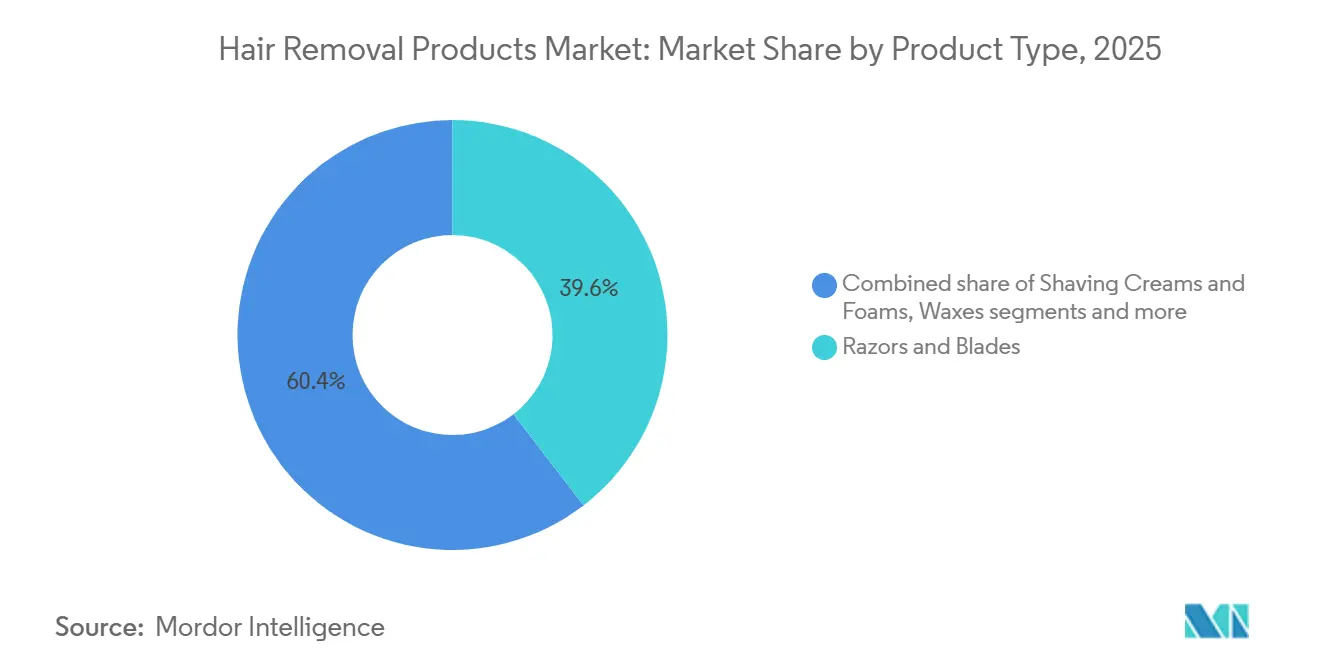

- By product type, razors and blades led with 39.56% revenue share in 2025; electronic devices are projected to expand at a 5.90% CAGR through 2031.

- By end user, the household/personal segment held 71.94% of the hair removal products market share in 2025, whereas professional establishments are forecast to post a 7.38% CAGR to 2031.

- By gender, male consumers accounted for a 58.49% share of the hair removal products market size in 2025, while the female segment is set to grow at a 7.01% CAGR.

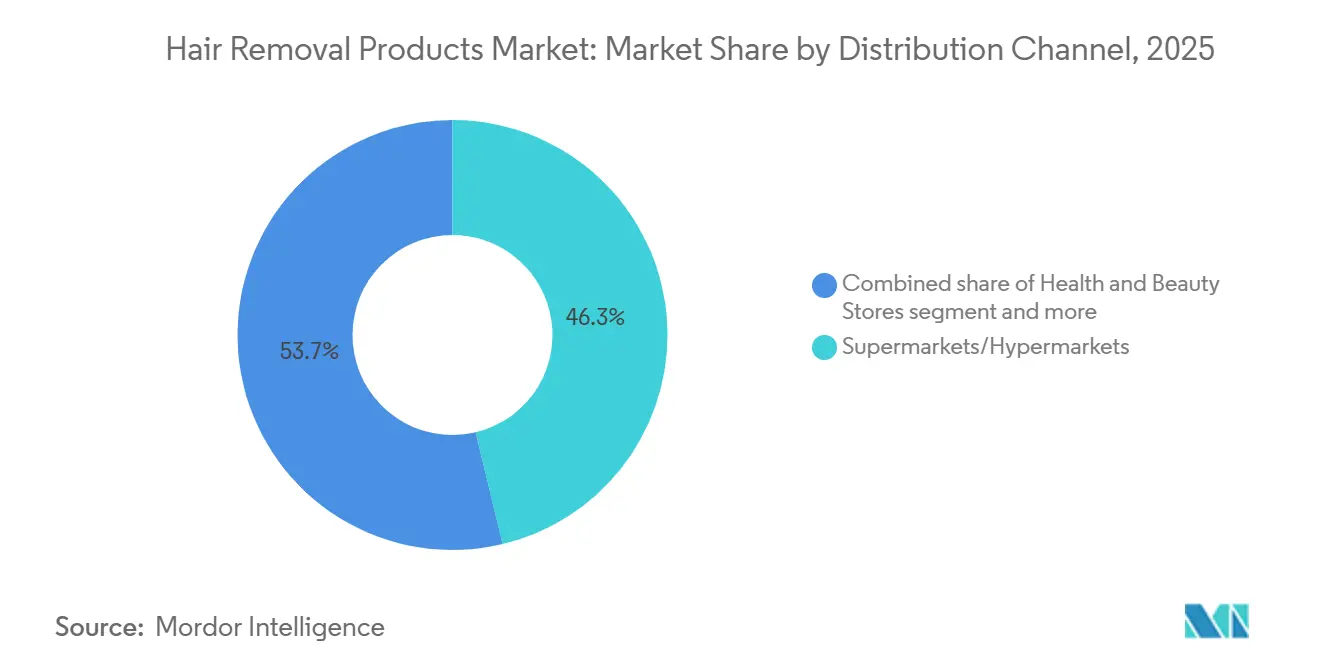

- By distribution channel, supermarkets/hypermarkets captured 46.27% share in 2025; online retail is advancing at a 6.72% CAGR.

- By geography, North America retained a 32.48% contribution in 2025; Asia-Pacific is expected to clock a 6.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hair Removal Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing emphasis on personal grooming and hygiene | +1.2% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Demand for convenient at-home solutions | +1.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Rising influence of social media and beauty influencers | +0.8% | Global, particularly strong in Asia-Pacific | Short term (≤ 2 years) |

| Increasing marketing and education by brands | +0.6% | Global, especially in Middle East, South America, and Asia-Pacific | Medium term (2-4 years) |

| Technological advances in laser and IPL devices | +1.1% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Expansion of product variety to suit different skin types and preferences | +0.7% | Global, particularly in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing emphasis on personal grooming and hygiene

Consumer spending on personal grooming and hygiene continues to increase as maintenance routines become integral to daily life. Data from Poland's Central Statistical Office shows monthly spending on personal hygiene increased from PLN 47.86 in 2022 to PLN 53.6 in 2023, indicating growing consumer investment in self-care [1]Source: Central Statistical Office of Poland, "Household budget survey in 2023", stat.gov.pl . Companies like Veet (Reckitt Benckiser), Nair (Church & Dwight), Philips, Sally Hansen, and The Man Company offer diverse hair removal solutions, including depilatory creams, waxes, IPL devices, and male grooming products. These companies continue developing products that are convenient, skin-safe, and technologically efficient for at-home use. Digital marketing, influencer partnerships, and e-commerce accessibility have normalized hair removal practices like shaving, waxing, and cream-based depilation as standard hygiene routines. Market players are expanding their consumer base through product innovations, awareness campaigns, and specialized offerings for demographics, including men and individuals with sensitive skin. This increased focus on personal grooming contributes to the growth of the global hair removal products market.

Demand for convenient at-home solutions

The demand for at-home hair removal solutions has increased due to privacy concerns, cost-efficiency, and technological improvements that provide results comparable to professional treatments. The FDA's implementation of Class II special controls for low-level laser systems validates the safety and effectiveness of these home-use devices, increasing consumer trust [2]Source: Food and Drug Administration (FDA), "Low Level Laser System for Aesthetic Use - Class II Special Controls Guidance for Industry and FDA Staff", fda.gov . At-home treatments offer time savings, flexible scheduling options, eliminate appointment requirements, and reduce potential exposure to communicable diseases. Current IPL devices achieve up to 90% hair reduction within a month and include app-based guidance for personalized treatment, making professional-level results possible at home. This technology particularly appeals to younger consumers who prefer self-administered treatments and integrated digital solutions. Companies like Philips, TRIA Beauty, and MiSMON dominate the market with devices featuring skin sensors and adjustable settings for various hair and skin types. The expansion of online retail channels increases product accessibility, addressing consumer needs for privacy, convenience, and effective hair removal solutions. These factors contribute to market growth, reflecting increased demand for self-care solutions and hygienic personal grooming options.

Rising influence of social media and beauty influencers

The hair removal products market has evolved through social media platforms, transforming personal grooming activities into widely discussed beauty practices that influence consumer behavior and market dynamics. Influencers on Instagram, TikTok, and YouTube demonstrate product performance through testimonials and tutorials, which influence purchasing decisions more effectively than traditional marketing. These content creators provide guidance on product application, safety protocols, and expected results, addressing information gaps that previously constrained market expansion. Specialized influencers have created dedicated communities centered on specific hair removal methods, skin concerns, and cultural preferences, building brand loyalty and organic marketing. The international reach of social media has increased acceptance of hair removal practices in regions where they were previously uncommon, expanding the market's geographic and demographic scope. Companies like Veet (Reckitt Benckiser), Philips, and Nair leverage these trends through influencer partnerships that connect with younger, digitally engaged consumers. This social media integration has positioned hair removal as an accessible beauty practice, driving market growth through increased consumer awareness, community participation, and product confidence developed through online platforms.

Increasing marketing and education by brands

Technological advancements in laser and IPL devices have significantly enhanced the hair removal industry in 2024, offering faster, safer, and more effective solutions for a diverse range of skin tones and hair types. For example, the AresSmart DL500, a state-of-the-art laser system, utilizes multi-wavelength technology, combining various laser frequencies to address a broader spectrum of hair colors and thicknesses. AI integration further optimizes treatments by enabling real-time analysis and automatic adjustments to ensure personalized safety and efficacy. These devices also incorporate advanced cooling technologies to minimize discomfort, while larger treatment windows reduce session times by up to 40% compared to earlier models. Similarly, IPL technology has progressed with smart skin recognition, allowing device settings to adapt to individual skin conditions and reducing the risk of irritation. At-home IPL and laser devices have become more sophisticated, featuring app-based guidance and adjustable energy levels to deliver professional-grade results to consumers. Leading brands such as Philips and TRIA Beauty are driving innovation by offering treatments that are faster, eco-friendly, and less painful, appealing to both male and female users. These technological developments are instrumental in expanding market accessibility, improving user experiences, and addressing previously unmet needs in permanent hair reduction solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns over skin irritation, allergies, and side effects from chemical or mechanical methods | -0.9% | Global, particularly in regions with sensitive skin populations | Short term (≤ 2 years) |

| Chemical-safety scrutiny on depilatories | -0.4% | Global, with stricter enforcement in North America and Europe | Medium term (2-4 years) |

| Lack of awareness or education regarding proper use for effective results | -0.5% | Emerging markets in Asia-Pacific, South America, Middle East and Africa | Short term (≤ 2 years) |

| Growing social acceptance of body hair | -0.6% | Primarily Western markets, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns over skin irritation, allergies, and side effects from chemical or mechanical methods

Safety concerns regarding skin irritation, allergies, and side effects impact hair removal product sales and market performance, particularly as consumer awareness increases and regulatory oversight intensifies. The Australian Radiation Protection and Nuclear Safety Agency has documented severe adverse effects from laser and IPL devices, including burns and eye injuries, emphasizing the importance of professional expertise and safety protocols [3]Source: Australian Radiation Protection and Nuclear Safety Agency (ARPANSA), "Lasers and Intense Pulsed Light (IPL) sources used for cosmetic purposes", arpansa.gov.au. Chemical depilatories face regulatory challenges due to ingredient safety reviews, particularly concerning potential allergens and carcinogens, necessitating product reformulations or restrictions. While the International Commission on Non-Ionizing Radiation Protection advocates for standardized global safety regulations, varying country-specific standards create compliance challenges for manufacturers and consumers. The UK's 2024 recall of non-compliant IPL products demonstrates how safety issues can damage consumer confidence and trigger regulatory actions. Market expansion faces limitations among sensitive demographics, including individuals with darker skin tones, pregnant women, and those with dermatological conditions. Companies are developing safer, clinically tested formulations and devices, while implementing consumer education programs to reduce risks. The hair removal market's continued growth depends on maintaining a balance between innovation and safety standards to ensure consumer protection.

Chemical-safety scrutiny on depilatories

Consumer attitudes toward body hair are shifting, influencing hair removal product manufacturers and their market strategies. This trend is particularly evident among younger consumers who challenge traditional beauty standards through social media movements and feminist discussions. Celebrities endorsing natural body hair have further influenced this shift, especially among women who view this choice as an expression of personal autonomy. While this movement originated in Western markets, social media has expanded its reach globally. In response, hair removal companies such as Wilkinson and Billie have adapted their marketing approaches to emphasize personal choice and body positivity rather than focusing solely on hair removal. However, traditional preferences for hair removal persist in many professional settings and cultural contexts, limiting the impact of this trend on market growth. Companies are responding by diversifying their product portfolios to include both hair removal and hair care options, aiming to serve consumers across different preference segments. This market evolution reflects the need for companies to balance emerging body positivity trends with continued demand for hair removal products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electronic Devices Drive Innovation Premium

Razors and blades hold the dominant market share at 39.56% in 2025, while electronic devices show the highest growth rate at 5.90% CAGR through 2031, as consumers increasingly adopt advanced grooming technology. The wet shaving segment continues to evolve through product development, exemplified by Procter & Gamble's Gillette Venus introducing enhanced formulations with skin care benefits in March 2025. Besides, shaving creams and foams remain complementary to razor sales but face competition from waterless options and multi-purpose products. Also, wax products sustain consistent demand across hot, cold, and strip variants, especially in professional salons where immediate results outweigh discomfort considerations.

Hair removal devices maintain premium price points through technological advancements, including AI integration and app connectivity that enhance effectiveness and user experience. While depilatory creams remain widely used due to convenience, regulatory oversight regarding chemical safety, specifically concerning allergens and carcinogens, limits their market growth. The development of AI-enabled devices has established electronic products as the main growth segment in the hair removal market, attracting consumers who seek professional-level results at home. Companies such as Philips, RaysDanc, and Braun demonstrate this trend by developing devices with customizable settings, skin sensors, and pain reduction features. These technological capabilities increase user confidence, support higher pricing, and drive market adoption, establishing electronic devices as key drivers of market expansion.

By End User: Professional Segment Accelerates Despite Household Dominance

The household/personal user segment accounts for 71.94% of hair removal product sales in 2025, as consumers increasingly choose accessible options like depilatory creams, wax strips, and home-use electronic devices. The professional segment, comprising salons and clinics, is expected to grow at a CAGR of 7.38% through 2031. This expansion stems from investments in advanced equipment that combines hair removal with additional treatments like skin rejuvenation, optimizing equipment usage, and per-client revenue. Consumer preference for professional services remains strong, particularly for treatments requiring specialized expertise in sensitive areas, with customers willing to pay higher prices for reliable results.

The professional segment's growth stems from institutional investments in advanced technologies, which often lead to innovations that later enter the consumer market. Companies like Philips have positioned IPL technology for home use by emphasizing its development by dermatologists, creating similarities between professional and personal-use devices. However, the professional segment maintains high barriers to entry through training requirements and regulatory compliance, which protect established providers and maintain safety standards. Professional providers distinguish themselves through specialized treatments and personalized consultations, preserving their premium service positioning despite home-use device advancements. This positioning helps maintain the professional segment's significant role in the global hair removal market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Supermarkets/hypermarkets maintain a 46.27% market share in 2025, driven by their convenience and impulse purchasing advantages. Online retail stores are experiencing robust growth, with a 6.72% CAGR projected through 2031, reflecting the increasing adoption of digital commerce and direct-to-consumer strategies. Traditional retail channels benefit from immediate product availability and the opportunity for consumers to examine products before purchase. This is particularly significant for personal care items, where texture, scent, and packaging heavily influence purchasing decisions. Health and beauty stores leverage specialized expertise and product demonstrations to support premium pricing and establish brand differentiation. Additionally, other distribution channels, such as pharmacies and department stores, target specific demographic segments with curated product assortments.

The growth of online retail is driven by convenience, competitive pricing, and access to a broader range of products, particularly niche or specialized items that are often unavailable in physical stores. This channel supports subscription-based models for consumable products such as razor blades and depilatory creams, ensuring recurring revenue streams and enhancing customer retention. Digital platforms address information gaps found in traditional retail by offering product education through reviews, tutorials, and comparison tools. The COVID-19 pandemic accelerated the adoption of online shopping, leading to lasting behavioral shifts that favor digital purchasing for personal care products. Additionally, mobile commerce and social media integration improve the accessibility of online channels, particularly among younger demographics who prioritize digital-first shopping experiences.

By Gender: Female Growth Accelerates Despite Male Market Leadership

Male consumers hold a 58.49% share of the market in 2025. The female segment is projected to grow at a 7.01% CAGR through 2031, reflecting evolving beauty standards and increased disposable income directed toward grooming. The dominance of the male segment is attributed to daily shaving requirements and higher product usage frequency, supported by continuous innovations in electric shavers and grooming tools. For instance, Procter & Gamble's grooming segment reported a 2% organic sales increase in Q2 2025, driven by product innovation and volume growth across male-focused brands. Traditional male grooming has expanded beyond facial hair to include body grooming, creating opportunities for specialized products and techniques.

Meanwhile, the female segment growth is driven by changing beauty standards that promote smooth skin across multiple body areas. Social media trends and workplace appearance norms further support this growth. Besides, technological improvements address key consumer concerns like skin sensitivity and treatment time. European Wax Center's EWC TREAT Brightening Ingrown Hair Wipes, recognized at the 2025 NewBeauty Awards, showcase advancements in post-treatment solutions. The market increasingly adopts gender-neutral marketing while maintaining products tailored to specific physiological needs. The alignment of male and female grooming preferences creates market opportunities for unisex products and shared household devices.

Geography Analysis

North America holds 32.48% market share in the hair removal products market in 2025, supported by high market penetration and consumer preference for premium grooming products. The region's strength stems from established grooming practices, structured regulatory environments, and consumer adoption of advanced electronic hair removal devices from manufacturers like Philips and Reckitt Benckiser. The extensive retail network, including supermarket chains and specialty stores, ensures broad product accessibility. The market benefits from integration between the United States, Canada, and Mexico through trade relationships and shared consumer preferences, solidifying North America's market leadership.

Asia-Pacific demonstrates the highest growth rate at 6.13% CAGR through 2031. This growth stems from increasing urbanization, higher female workforce participation, and the growing influence of Western beauty trends. Japan, the fourth-largest cosmetics market globally, and South Korea maintain product quality through regulatory bodies PMDA and KFDA. China's Cosmetics Supervision and Administration Regulation has improved product approval processes, as evidenced by Beiersdorf's Thiamidol approval in 2024. The region's large young population with increasing beauty awareness drives demand for modern hair removal solutions.

Europe maintains consistent market growth through unified regulations across countries, building consumer confidence in product safety. Germany, the United Kingdom, France, and Spain show strong demand for premium and environmentally conscious products. Besides, South America, and Middle East and Africa offer growth potential through increasing grooming awareness and social media influence, despite current market limitations. Companies like Sally Hansen and Emjoi are expanding their presence in these regions as market accessibility improves, indicating future growth opportunities in the global hair removal market.

Competitive Landscape

The hair removal products market has a moderately fragmented structure with multinational corporations, device manufacturers, and technology firms competing for market share. Companies like Procter & Gamble, Philips, and Reckitt Benckiser maintain their market positions through established brand recognition, distribution networks, and research and development investments. These companies focus on product innovation and premium positioning, supported by marketing campaigns and retail partnerships. While their market presence creates entry barriers, changing consumer preferences provide opportunities for new competitors.

Companies compete primarily through technological advancement, with investments in AI integration, skin sensing technologies, and personalized treatment protocols. These developments improve product efficacy and safety while enabling premium pricing through customized treatment options. Companies like TRIA Beauty and MiSMON have developed smart devices that combine hardware and software capabilities to deliver optimized hair removal results across various skin types and hair characteristics.

Furthermore, market opportunities exist in underserved segments, particularly for consumers with darker skin tones requiring specialized IPL settings, and in emerging markets where grooming product infrastructure continues to develop. Companies that successfully combine hardware innovation with software ecosystems gain market advantages through data-driven personalization and enhanced user experience. This integrated approach transforms single-purchase products into ongoing services, influencing the market's competitive landscape.

Hair Removal Products Industry Leaders

-

Procter & Gamble Company

-

Edgewell Personal Care Company

-

Koninklijke Philips N.V.

-

Reckitt Benckiser Group PLC

-

Société Bic S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tress Wellness launched its Premium Waxing Kit at BJ's Wholesale Club. The kit included an At-Home Wax Kit, On-the-Go Wax Kit, and Pre & Post-Wax Spray Kit. The dermatologically tested products contained natural ingredients and were suitable for all skin types, including body, facial, and bikini areas. This comprehensive bundle offered convenience, portability, and value.

- October 2024: Wakse, an at-home waxing brand, introduced Meltoway, its new hair removal product, to the United Kingdom market. The one-step cream removes unwanted hair using a gentle, botanical formula suitable for all skin types, including sensitive areas. The vegan and cruelty-free product was available in four fragrances: Guava Butter, Mango Magic, Milk & Honey, and Fairy Floss (cotton candy scent).

- May 2024: Svish introduced a hair removal spray for men, which was endorsed by cricketer Shikhar Dhawan in India. The product became the first hair removal spray to receive certification from Safe Cosmetics Australia, validating its safety and effectiveness.

Global Hair Removal Products Market Report Scope

The Hair Removal Products Market Report is Segmented by Product Type (Razors and Blades, Shaving Creams and Foams, Waxes, and More), End User (Household/Personal, Professional), Gender (Male, Female), Distribution Channel (Supermarkets/Hypermarkets, Health and Beauty Stores, Online Retail Stores, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Razors and Blades |

| Shaving Creams and Foams |

| Waxes (Hot, Cold, Strips) |

| Depilatory Creams and Lotions |

| Electronic Devices |

| Household/Personal |

| Professional |

| Male |

| Female |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Razors and Blades | |

| Shaving Creams and Foams | ||

| Waxes (Hot, Cold, Strips) | ||

| Depilatory Creams and Lotions | ||

| Electronic Devices | ||

| By End User | Household/Personal | |

| Professional | ||

| By Gender | Male | |

| Female | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue value for the hair removal products market by 2030?

Revenue is forecast to reach USD 40.81 billion by 2031, equating to a 5.47% CAGR over 2026-2031.

Which product category is expanding fastest within global hair removal products?

Electronic devices such as IPL handsets will post a 5.90% CAGR, outpacing other categories through AI-driven personalization and premium pricing.

Which region shows the quickest growth momentum for hair-removal product solutions?

Asia-Pacific leads with a projected 6.13% CAGR, propelled by rising incomes, urbanization, and evolving beauty norms.

How dominant are at-home users compared with professional service clients?

Household users contributed 71.94% of 2025 revenue, but professional clinics will expand faster at a 7.38% CAGR through 2031 thanks to technology upgrades.

Page last updated on: