India Hair Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.92 Billion |

| Market Size (2026) | USD 4.1 Billion |

| Market Size (2031) | USD 5.19 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Hair Care Products Market Analysis by Mordor Intelligence

India hair care products market size in 2026 is estimated at USD 4.1 billion, growing from 2025 value of USD 3.92 billion with 2031 projections showing USD 5.19 billion, growing at 4.73% CAGR over 2026-2031. This growth trajectory reflects the market's evolution from traditional home remedies toward scientifically formulated solutions, driven by urbanization and rising disposable incomes across tier-2 and tier-3 cities. The market's resilience stems from its ability to adapt to diverse consumer needs while navigating regulatory complexities under the Drugs and Cosmetics Act, 1940.

Key Report Takeaways

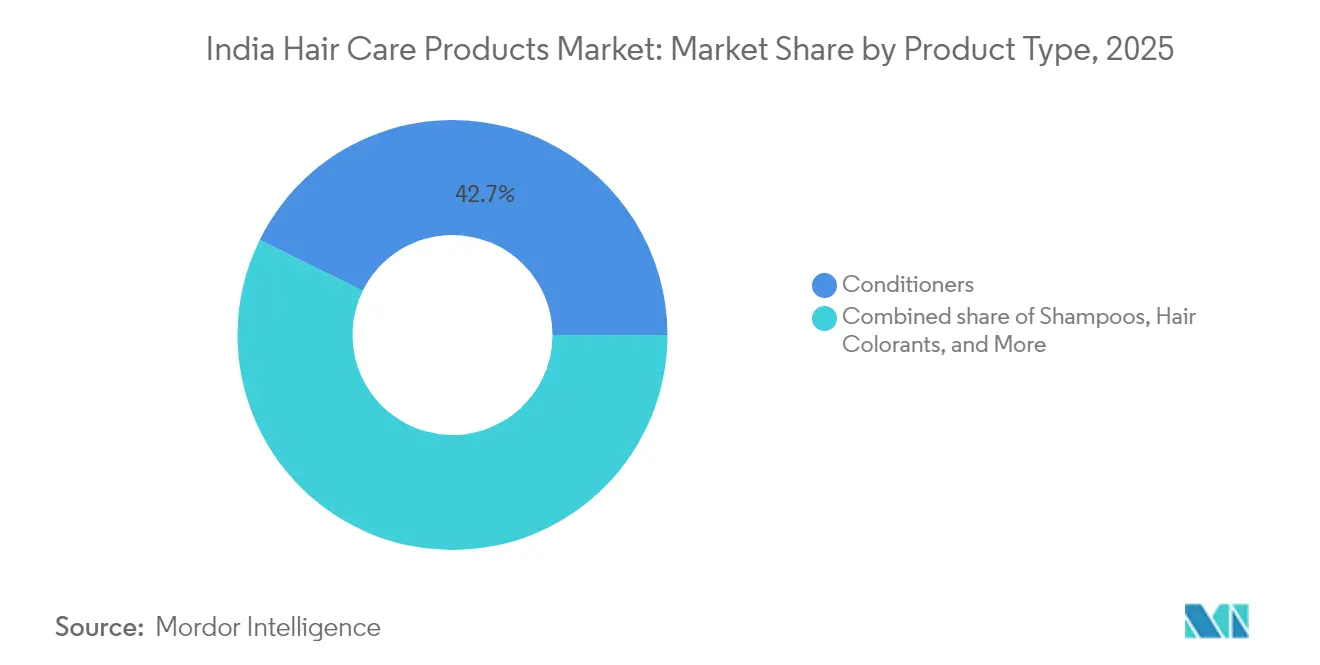

- By product type, conditioners led with 42.71% of the India hair care products market share in 2025; hair styling products are forecast to expand at 5.20% CAGR between 2026-2031 across metro and mini-metro cities.

- By category, mass offerings commanded 84.97% of the 2025 India hair care products market size, while premium/luxury lines are projected to grow at 5.60% CAGR through 2031, especially in tier-1 geographies.

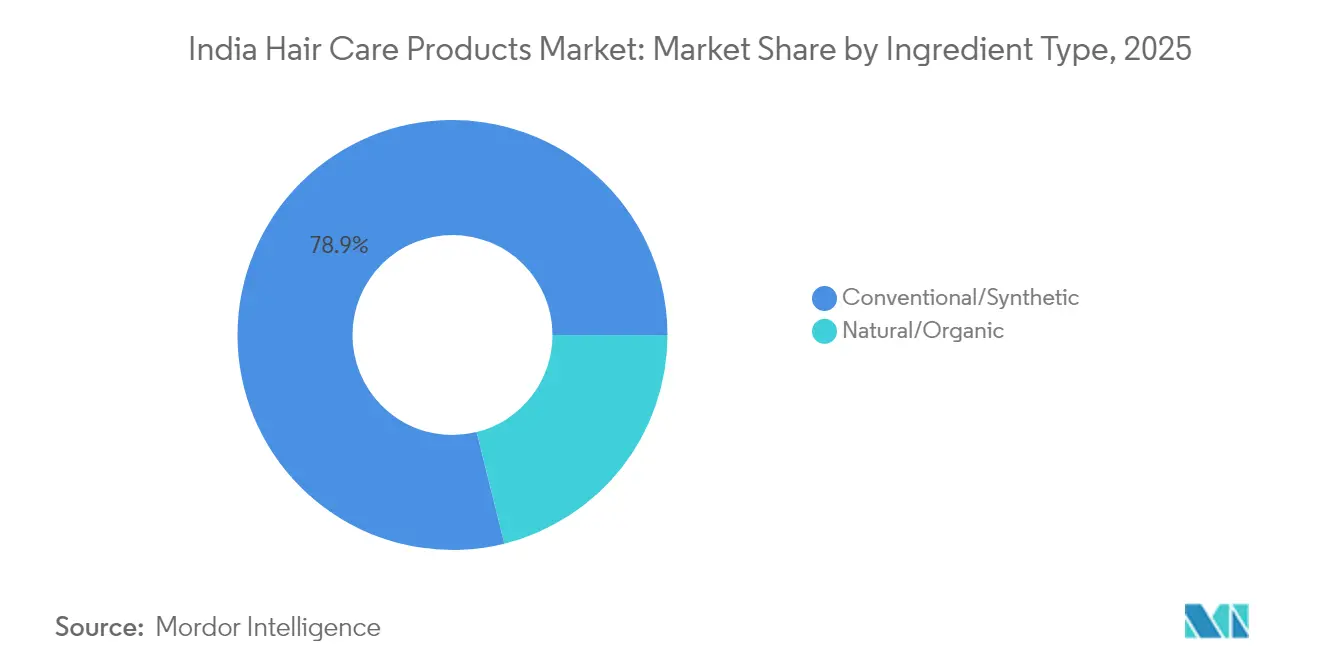

- By ingredient type, conventional formulations accounted for 78.88% share of the India hair care products market in 2025, whereas natural/organic variants are set to advance at a 5.95% CAGR.

- By distribution channel, convenience/traditional grocery stores delivered 38.92% share of 2025 sales, yet online retail is positioned for a 6.32% CAGR to 2031 as digital penetration rises nationwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Hair Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising grooming consciousness among men | +1.2% | Urban centers, tier-1 and tier-2 cities with spillover to tier-3 markets | Medium term (2-4 years) |

| Shift to natural/ayurvedic formulations | +0.8% | Pan-India with concentration in North and West regions | Long term (≥ 4 years) |

| Growing demand for hair fall and targeted solutions | +0.6% | Metro cities and urban areas with high stress levels | Short term (≤ 2 years) |

| Increasing focus on scalp health | +0.5% | Urban markets with awareness of dermatological care | Medium term (2-4 years) |

| Ingredient-transparency regulation momentum | +0.4% | National with early adoption in regulatory-compliant states | Long term (≥ 4 years) |

| Rising social media and influencer impact | +0.3% | Digital-native demographics in urban and semi-urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising grooming consciousness among men

Male grooming consciousness drives market expansion as traditional gender barriers dissolve across urban India. Traya's comprehensive study revealed 50.31% of Indian men under 25 experience hair loss, with primary triggers including dandruff (65%), stress (60%), gut health issues (37%), and irregular sleep patterns (30%) [1]Source: Tatvartha Health Pvt. Ltd., “Hair Loss Statistics India: Insights from 5 Lakh Indian Men,” traya.health. This demographic shift creates substantial opportunities for targeted formulations addressing male-specific concerns like premature balding and scalp sensitivity. D2C brands like Dapr capitalize on this trend, offering specialized styling products including pomades, setting clays, and heat-protection sprays tailored for Indian male consumers. The convergence of workplace professionalism demands and social media influence accelerates adoption of premium grooming regimens, particularly in tier-1 and tier-2 cities where disposable incomes support category premiumization.

Shift to natural/ayurvedic formulations

Ayurvedic formulation adoption accelerates through AYUSH certification protocols and consumer preference for traditional ingredients with modern efficacy claims. Vedix exemplifies this trend with customized Ayurvedic regimens based on Dosha analysis, offering sulfate-free, paraben-free formulations verified by certified Ayurvedic doctors. The regulatory framework supports this shift through Bureau of Indian Standards specifications for herbal cosmetics and increased scrutiny of synthetic ingredient safety profiles. Companies leverage traditional ingredients like fenugreek, hibiscus, and onion oil while ensuring compliance with modern safety and efficacy standards. This dual approach satisfies consumer demand for natural solutions while meeting regulatory requirements for product registration and market access across Indian states.

Growing demand for hair fall and targeted solutions

Hairfall concerns are becoming increasingly widespread across different groups, with a significant number of individuals in Delhi NCR experiencing hair loss. Many attribute the issue to the poor quality of water, particularly the hardness of the water used in daily routines. According to data published by the National Council on Aging, Inc. in April 2025, approximately 63% of men aged 21 to 61 experience hair loss [3]Source: National Council on Aging, Inc., “Hair Loss Statistics,” ncoa.org. This widespread concern drives demand for specialized treatments addressing root causes rather than cosmetic masking. Companies respond with targeted serums, growth activators, and scalp treatments incorporating clinically proven ingredients like Redensyl, Kopexil, and Procapil. The market witnesses a proliferation of dermatologist-approved formulations and trichologist-developed solutions, reflecting consumer willingness to invest in scientifically validated treatments. Urban pollution exacerbates hairfall issues, creating sustained demand for protective and restorative formulations across metropolitan markets.

Ingredient-transparency regulation momentum

Regulatory momentum builds toward enhanced ingredient disclosure and safety standards, with NEERI studies revealing 40% of tested cosmetics exceeded EU siloxane limits [2]Source: National Environmental Engineering Research Institute, “Siloxane Levels in Indian Cosmetics 2024,” neeri.res.in. This regulatory scrutiny drives companies toward cleaner formulations and transparent labeling practices. BIS standards evolution and potential separate legislation for beauty products create compliance pressures that favor established players with robust regulatory capabilities. The regulatory landscape increasingly aligns with international standards, particularly EU guidelines on restricted substances, creating opportunities for export-oriented manufacturers while challenging smaller players lacking compliance infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity and counterfeit proliferation | -0.7% | Rural markets and price-conscious urban segments | Short term (≤ 2 years) |

| Cultural practices and natural home remedies | -0.5% | Traditional households across India with rural concentration | Long term (≥ 4 years) |

| Hard-water and urban pollution challenges | -0.4% | Metro cities and industrial areas with water quality issues | Medium term (2-4 years) |

| Fragmented rural distribution logistics | -0.3% | Rural and semi-urban markets with infrastructure gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price sensitivity and counterfeit proliferation

Price sensitivity constrains market expansion as counterfeit products undermine branded offerings through aggressive pricing strategies. Enforcement actions across Kerala, Maharashtra, and Telangana throughout 2024 revealed extensive networks of spurious cosmetics, unlicensed imports, and trademark violations affecting legitimate market growth. The proliferation of unregulated products creates consumer confusion and safety concerns while eroding brand equity investments. Rural and semi-urban markets remain particularly vulnerable to counterfeit penetration due to limited regulatory oversight and price-conscious purchasing behavior. This dynamic forces legitimate manufacturers to balance quality investments with competitive pricing pressures, potentially constraining innovation and premium positioning strategies.

Fragmented rural distribution logistics

Rural distribution fragmentation limits market penetration despite representing significant untapped demand across India's vast rural population. Infrastructure constraints including poor road connectivity, inadequate cold storage facilities, and fragmented retail networks increase distribution costs and reduce product availability. The complexity of serving diverse regional preferences through fragmented supply chains creates operational inefficiencies that constrain market expansion. Traditional distribution models struggle with last-mile connectivity, while modern retail formats remain concentrated in urban areas. This structural challenge requires innovative distribution strategies and partnerships with local retailers to achieve sustainable rural market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conditioners Lead While Styling Surges

Hair conditioners hold the largest market share at 42.71% in 2025, while hair styling products are expected to grow at the highest CAGR of 5.20% through 2031. This growth disparity reflects evolving consumer behavior toward specialized styling solutions, driven by social media influence and professional appearance requirements. Conditioners benefit from universal usage patterns and established consumer habits, while styling products capitalize on emerging trends like heat protection, curl definition, and texture enhancement.

Companies increasingly invest in styling product innovation, with brands like Arata launching alcohol-free gels and texture sprays targeting Indian climate conditions. The styling segment benefits from premiumization trends as consumers seek professional-quality results for home use. Regulatory compliance factors influence product development, with BIS standards governing formulation safety and labeling requirements across all product categories. Shampoos constitute the second-largest segment in the market, with consistent demand due to essential hair cleansing requirements. The segment shows moderate growth due to market maturity. Hair colorants demonstrate growth in urban markets, particularly with increasing consumer preference for natural and organic products.

By Category: Mass Dominance Amid Premium Acceleration

The premium/luxury segment is growing at a CAGR of 5.60%, while mass market categories maintain 84.97% market share in 2025, demonstrating a dual-track market development. This divergence reflects income polarization and evolving consumer sophistication across urban and rural markets. Mass segments benefit from price accessibility and wide distribution reach, particularly in rural areas where value-for-money considerations drive purchasing decisions. Premium segments capitalize on urbanization trends, rising disposable incomes, and consumer willingness to invest in specialized formulations with proven efficacy claims. The premiumization trend accelerates in metropolitan markets where consumers increasingly prioritize ingredient quality, brand reputation, and personalized solutions over price considerations.

D2C brands like SkinKraft and Vedix demonstrate premium positioning through customization technology and dermatologist-approved formulations, commanding price premiums while building direct consumer relationships. Traditional mass-market players respond by launching premium sub-brands and upgrading existing formulations to capture evolving consumer preferences. The category dynamics suggest sustained growth opportunities in both segments, with mass markets providing volume growth and premium segments driving value expansion.

By Ingredient Type: Natural Formulations Gain Momentum

Natural/organic formulations surge at 5.95% CAGR despite conventional/synthetic variants holding 78.88% market share in 2025, indicating accelerating consumer preference for clean beauty solutions. This growth reflects regulatory momentum around ingredient transparency and consumer awareness of potential health impacts from synthetic chemicals. Conventional formulations maintain dominance through established efficacy profiles, cost advantages, and extensive distribution networks built over decades.

Natural variants face challenges, including higher raw material costs, shorter shelf life, and limited availability of proven active ingredients at scale. However, regulatory support through AYUSH certification and BIS standards for herbal cosmetics creates favorable conditions for natural product expansion. Companies invest heavily in natural ingredient sourcing and formulation technology, with brands like Ashba Botanics positioning around 100% natural, sulfate-free formulations targeting specific hair types. The ingredient evolution reflects broader consumer trends toward sustainability and health consciousness, supported by social media education and influencer advocacy for clean beauty practices.

By Distribution Channel: Digital Disruption Accelerates

Online retail channels are growing at a CAGR of 6.32%, while convenience/traditional grocery stores hold a 38.92% market share in 2025, driven by increased digital adoption following the COVID-19 pandemic. This channel disruption transforms consumer shopping behavior and brand engagement strategies across the hair care ecosystem. Traditional channels benefit from established consumer habits, immediate product availability, and personal interaction with retailers who provide usage guidance.

Online channels capitalize on convenience, wider product selection, competitive pricing, and personalized recommendations through AI-driven platforms. The digital shift enables direct-to-consumer brands to bypass traditional distribution networks while providing established players with new customer acquisition channels. Hypermarkets/supermarkets and pharmacy/drug stores represent stable distribution channels with moderate growth, serving consumers who prefer physical product inspection and professional consultation. The channel evolution accelerates through technology adoption, with salon management platforms like Invoay enabling digital inventory management, customer relationship management, and integrated e-commerce capabilities for professional channels.

Geography Analysis

Urban markets, particularly in tier-1 cities such as Mumbai, Delhi, Bangalore, and Chennai, drive growth in the premium segment and new product adoption. These metropolitan areas demonstrate higher acceptance of international brands, D2C offerings, and specialized treatments due to elevated disposable incomes and exposure to global beauty trends.

Tier-2 and tier-3 cities represent emerging growth opportunities as infrastructure development and rising middle-class incomes expand market accessibility. Rural markets remain largely untapped despite representing significant population potential, constrained by distribution challenges, price sensitivity, and preference for traditional home remedies.

State-level regulatory variations impact market dynamics, with states like Kerala, Maharashtra, and Telangana demonstrating more aggressive enforcement against counterfeit products and unlicensed imports. Northern and western regions show stronger adoption of Ayurvedic formulations, aligning with cultural preferences and traditional medicine acceptance. The geographic diversity within India creates opportunities for localized product development and targeted marketing strategies that address regional preferences, climate conditions, and cultural practices while maintaining national brand consistency

Regulatory Landscape

Hair care products in India are governed under the Drugs and Cosmetics Act, 1940 and the Cosmetics Rules, 2020. Oversight is shared between the Central Drugs Standard Control Organisation (CDSCO) and State Licensing Authorities for manufacturing permissions, with compliance expectations varying by route to market. Importers register products through the SUGAM portal (Form COS-1) to obtain an import registration certificate (Form COS-2), while domestic manufacturers obtain a manufacturing license (Form COS-8) linked to GMP expectations under Schedule M-II.

Regulatory scrutiny has been especially visible in hair color cosmetics, where CDSCO communications in June 2026 asked for submission of compliance documentation aligned to applicable Bureau of Indian Standards (BIS) specifications. Standards such as IS 4707 (Part 1 and Part 2) and IS 8481 cover permitted and restricted ingredients, labeling and warning statements, and patch-test related requirements. BIS also published IS 15205:2026 for auto-oxidation hair dyes and colors, increasing the importance of updated technical dossiers and label-change controls for brands and contract manufacturers.

Competitive Landscape

The India hair care products market exhibits moderate concentration with a market concentration index of 6 out of 10, indicating balanced competition between established multinational corporations and emerging domestic players. Established giants like Hindustan Unilever, Procter & Gamble, and L'Oréal leverage extensive distribution networks, brand equity, and R&D capabilities to maintain market leadership, while domestic players like Marico, Dabur, and Patanjali capitalize on local consumer insights and Ayurvedic positioning.

The competitive landscape is becoming more fragmented as direct-to-consumer (D2C) brands such as Mamaearth, WOW Skin Science, Vedix, and SkinKraft challenge traditional distribution models through direct consumer engagement and targeted positioning. Technology adoption emerges as a critical competitive differentiator, with companies investing in AI-driven personalization, virtual try-on capabilities, and data analytics for consumer insights. L'Oréal's partnership with ModiFace for hairstyling applications and Reliance's Tira platform demonstrate how technology integration creates competitive advantages in consumer engagement and retail innovation.

White-space opportunities exist in customized formulations, men's grooming, and sustainable packaging solutions, areas where agile startups can challenge established players through innovation and direct consumer relationships. Regulatory compliance factors increasingly influence competitive positioning, with companies investing in ingredient transparency, safety testing, and certification processes to meet evolving regulatory standards and consumer expectations.

India Hair Care Products Industry Leaders

L'Oréal S.A.

Marico Limited

Dabur India Ltd

Procter & Gamble

Unilever Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization and science-led innovation are creating whitespace for performance-focused hair care centered on concerns such as hairfall, scalp health, and damage repair. Recent launches point to faster product-cycle activity beyond traditional shampoo and oil routines. In May 2026, Marico entered the shampoo segment with Parachute Advansed Protein Shampoo, and in April 2026, CavinKare introduced Nyle++ variants positioned as hybrid haircare (serum shampoo and chia seed gel shampoo), reinforcing demand for specialized cleansing and multi-benefit formats that combine treatment and styling needs.

M&A and investment activity are also widening the competitive set between incumbents and digital-first challengers, including adjacencies that can reshape how consumers build hair care regimens, such as hair therapy and nutraceutical positioning. In June 2026, Honasa Consumer initiated an acquisition of a majority stake in Fluence Pharma, and in January 2026, L'Oreal announced an approximately EUR 326 million investment to build a Global Capability Centre in Hyderabad focused on AI-driven beauty innovation and R&D. This supports opportunities in personalization, faster innovation pipelines, and more granular demand and inventory planning. At the same time, tighter enforcement under the Cosmetics Rules, 2020 and expanding BIS coverage for sensitive categories such as hair dyes increases the advantage for players that can sustain compliant ingredient documentation, labeling controls, and quality systems at scale.

Recent Industry Developments

- May 2026: Marico launched Parachute Advansed Protein Shampoo, marking the Parachute Advansed brand's entry into the hair cleansing segment. The launch expands Marico's participation across core hair care routines by adding a higher-frequency usage category to an established brand used in online and general trade replenishment.

- October 2025: Dabur launched Dabur Ventures, an investment platform with a capital allocation of up to INR 500 crore to invest in new-age, digital-first businesses spanning personal care and Ayurveda. This formalizes an external innovation and portfolio-expansion pathway that can accelerate Dabur's access to premium and targeted hair care propositions through minority and strategic stakes.

- October 2024: Dabur entered into an agreement to merge Sesa Care Private Limited with Dabur India to strengthen its Ayurvedic hair care portfolio. The proposed consolidation supports deeper control over a heritage hair care franchise and can streamline brand, distribution, and manufacturing decisions under a single corporate structure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the retail and consumer sales value of hair care and styling products sold in India, counted at the product level across common consumer channels. It includes products used to cleanse, condition, treat, style, and color hair, based on what is actually sold into the country market.

Scope exclusions: Services (salon labor), devices (dryers, straighteners), and raw bulk ingredients sold for manufacturing are excluded from the market value.

Segmentation Overview

- By Product Type

- Shampoos

- Conditioners

- Hair Colorants

- Hair Styling Products

- Others

- By Category

- Mass

- Premium/Luxury

- By Ingredient Type

- Conventional/Synthetic

- Natural/Organic

- By Distribution Channel

- Hypermarkets/Supermarkets

- Pharmacy and Drug Stores

- Convenience/Traditional Grocery Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base and keep the model consistent year to year, before any interviews were run. We reviewed public sources such as the Ministry of Commerce and Industry trade statistics, customs import and export series, the Reserve Bank of India for macro indicators, and official inflation and consumer spending data from national statistics releases.

To convert these signals into usable market inputs, we also read company annual reports and investor presentations, distributor and retailer updates in reputed business press, and category notes from industry associations. Where available, an import and export shipment level database and company financials and intelligence databases were used to sanity check large brand scale and pricing movements across time. This desk list is illustrative, and other public and official sources were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives value growth in India hair care and styling, especially the way pricing ladders move, pack sizes change, and channel mix shifts. We spoke with a mix of brand and sales leaders, distribution and retail managers, and category specialists across major consuming clusters, so the assumptions could be checked against on-ground behavior in key cities and retail formats.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | |

| Mid tier: 46% | Functional/Unit leaders: 42% | |

| Smaller Players: 22% | Managers: 44% |

Market-Sizing & Forecasting

The market was built using a top-down approach where the India demand pool is reconstructed through category level consumption signals, trade flows, and retail channel expansion, then mapped to product groups that consumers actually buy. Once this structure is in place, selective bottom-up checks are run, such as sampled price points by pack sizes, channel checks on category mix, and supplier level roll-ups for a few high visibility product lines.

Key inputs that shaped the model included shampoo and hair oil penetration trends, pricing and pack size migration between mass and premium lines, online retail share movement versus traditional grocery, changes in personal care inflation, and shifts in colorants and styling adoption in urban centers. When gaps appeared in any product group, we filled them using conservative interpolation tied to adjacent categories and then rechecked totals against the full market value.

For forecasting, scenario analysis was used since near term growth depends on a few variables moving together, which were reviewed with interview respondents. Base, upside, and downside cases were created around inflation and pricing pass-through, e-commerce growth rates, and category premiumization, and then consolidated into the final outlook.

Data Validation & Update Cycle

Outputs were validated through multiple checks so that any single data point did not drive the final number. We compared modeled totals against independent signals such as trade trends, reported category growth commentary, and channel expansion, then investigated variances that looked out of line with the broader consumer goods environment in India.

A second analyst review is completed before sign off, and re-contact is triggered when pricing, channel shares, or category splits show unexplained breaks across years. The report is refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery pass so the latest information is reflected in the numbers.

Mordor Intelligence's India Hair Care and Styling Products Market Market Size Compared Against Other Published Estimates

Published market sizes for India hair care and styling products can look far apart, even when the category names sound similar. The gaps usually come from different timing choices for currency conversion, how average selling prices are trended across pack sizes, and whether the publisher refreshes assumptions when channel mix shifts quickly.

In this study, the refresh cycle is designed to recheck price ladders and channel shares with recent validation calls, and then apply consistent currency timing for the base year, which helps explain why the 2025 value lands where it does for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.92 B (2025) | |

| Global Research Reseller A | USD 5.85 B (2024) | Uses an earlier base year and a higher growth path that may reflect a different price escalation curve across categories, with limited visibility on pack size mix and currency conversion timing. |

| Industry Publisher B | USD 4.10 B (2024) | Sits closer in value but appears to follow a broader hair care framing that can treat styling lines and adjacent treatments differently, and it is not always clear how online channel share shifts are refreshed year to year. |

The table shows that most variance is explained by base year choice and how pricing is carried forward as consumers trade up across packs and channels. By keeping the scope tied to sell-in and sell-through signals inside India and by revalidating key price and mix assumptions during updates, the final number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the India hair care products market?

The India hair care products market size is valued at USD 4.1 billion in 2026 and is expected to climb to USD 5.19 billion by 2031.

Which product segment dominates sales?

Conditioners hold the largest share at 42.71% of 2025 revenue, benefiting from broad household usage and routine replenishment.

Which channel is growing the fastest?

Online retail leads growth with a projected 6.32% CAGR, owing to wider assortment, faster delivery, and AI-based personalization.

How fast are premium/luxury lines expanding?

Premium/luxury formats are set to rise at a 5.60% CAGR between 2026-2031, far outpacing mass growth in metro and mini-metro cities.

Page last updated on: