Hair Accessories Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.42 Billion |

| Market Size (2031) | USD 35.74 Billion |

| Growth Rate (2026 - 2031) | 7.92% CAGR |

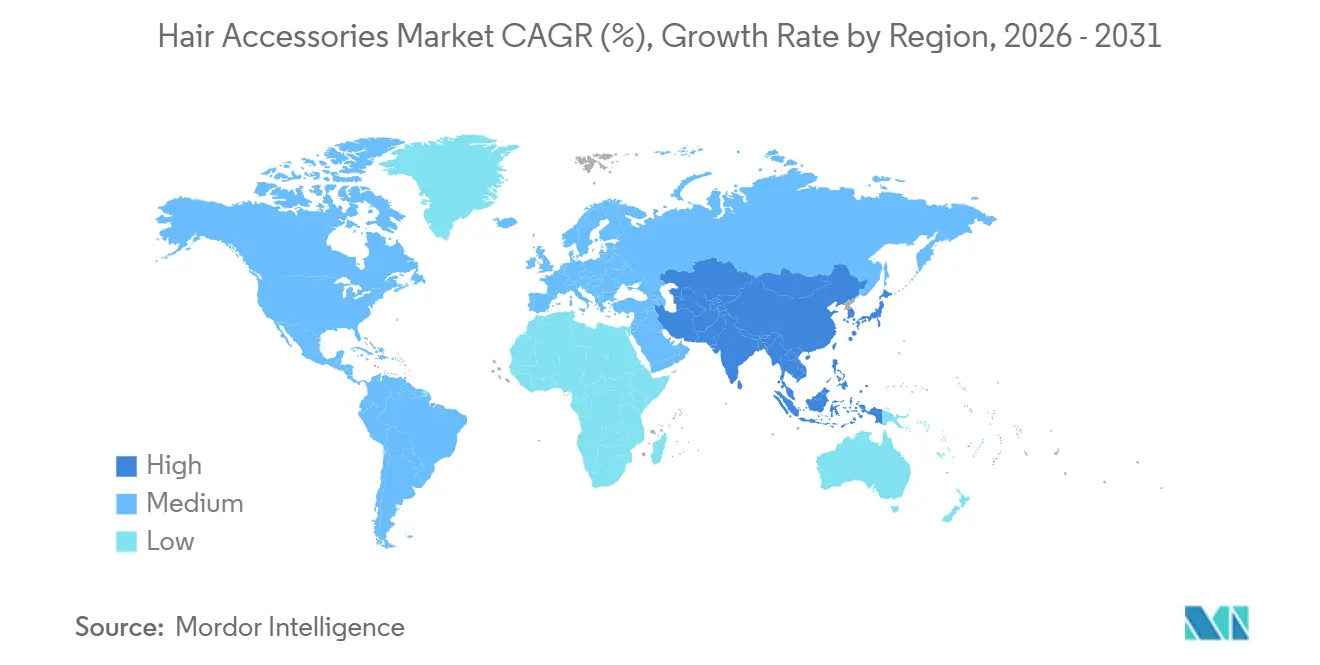

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

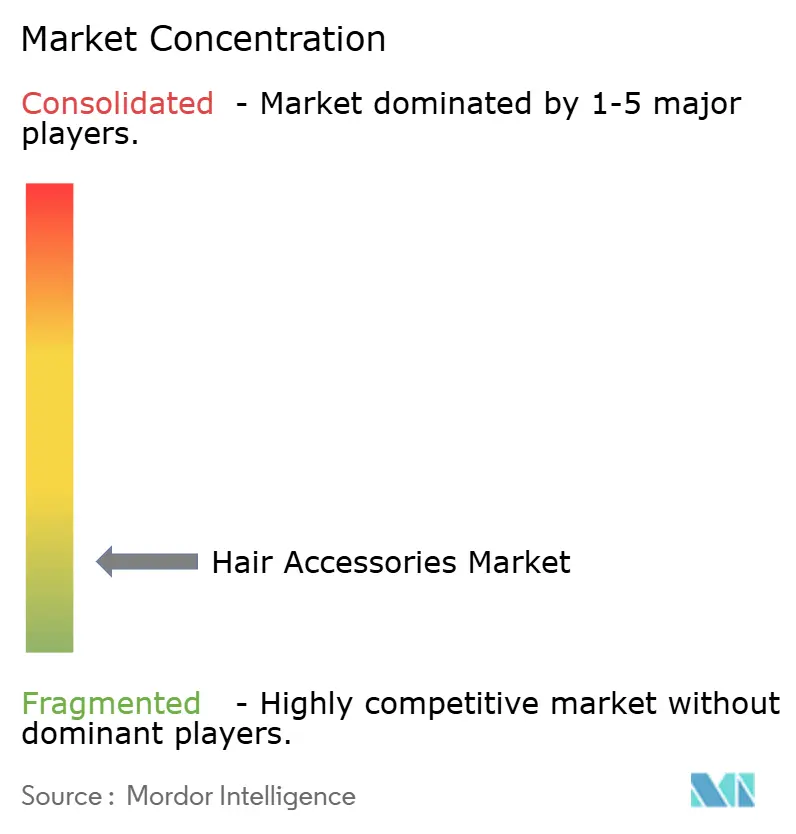

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Accessories Market Analysis by Mordor Intelligence

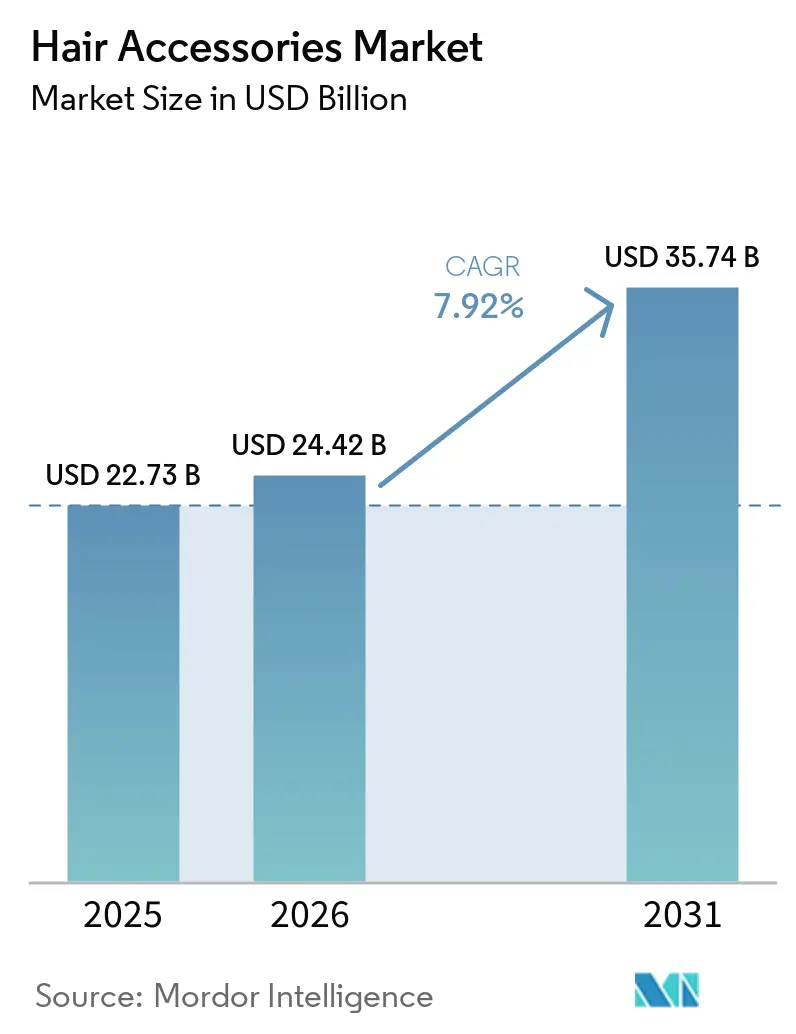

The hair accessories market size is expected to grow from USD 22.73 billion in 2025 to USD 24.42 billion in 2026 and is forecast to reach USD 35.74 billion by 2031 at 7.92% CAGR over 2026-2031. The global hair accessories market, once primarily functional, has evolved into a dynamic segment within the fashion and lifestyle industry. This transformation is driven by premiumization, the mainstream adoption of wigs and hair extensions, and the growing influence of Korean and Japanese beauty aesthetics. E-commerce and social media platforms are playing a pivotal role in this shift, enabling consumers to engage with brands more effectively while empowering agile direct-to-consumer (DTC) companies to gain a competitive advantage. According to the International Telecommunication Union, global internet users reached six billion by 2025, marking an increase from 5.5 billion in the previous year. This represents 74% of the global population[2]Source: International Telecommunication Union, "Facts and Figures 2025," itu.int. Additionally, the rise of cultural exports, increasing emphasis on sustainability, and a growing focus on scalp health are positioning hair accessories as tools for self-expression and wellness. However, the market's fragmented nature fosters innovation but also heightens competitive pressures. Brands face significant challenges, including counterfeiting and volatility in raw material prices. To succeed in this rapidly evolving landscape, businesses must prioritize authentic consumer engagement, invest in innovative product designs, and strategically integrate beauty and fashion to deliver meaningful value.

Key Report Takeaways

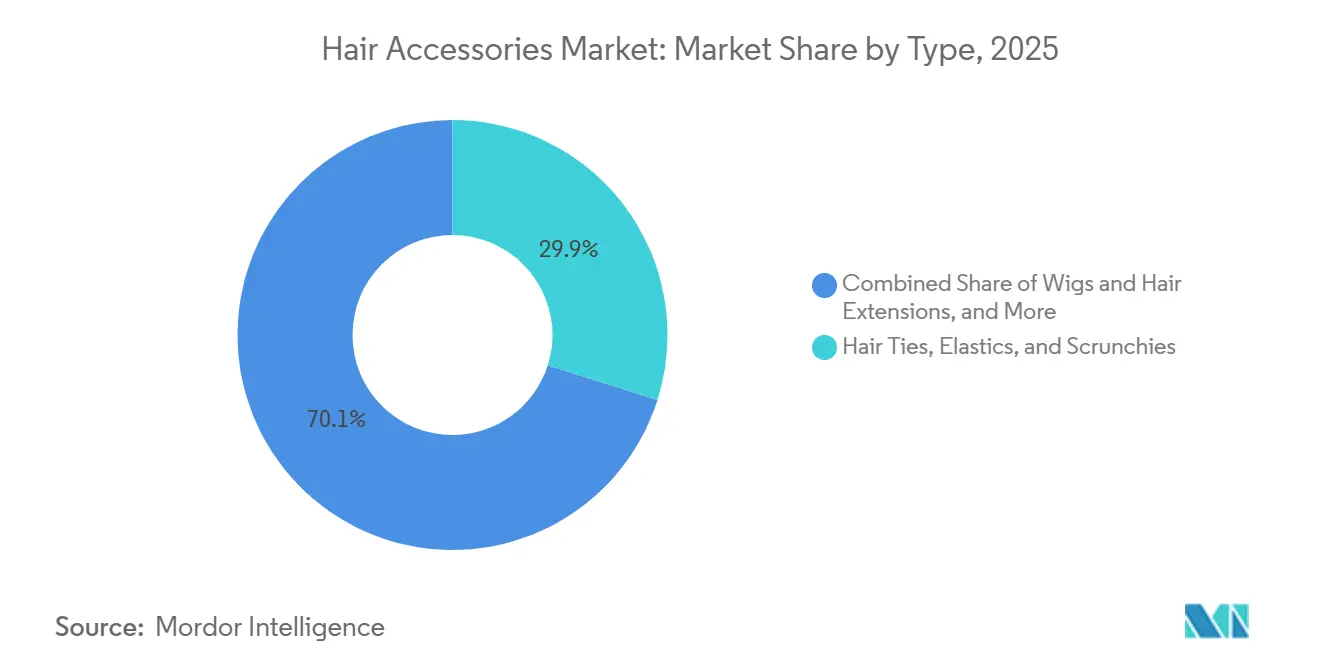

- By product type, hair ties, elastics, and scrunchies led the global hair accessories market with a share of 29.89% in 2025, while wigs and hair extensions are anticipated to register the fastest CAGR of 9.22% during 2026-2031.

- By material, plastic retained 39.96% share in 2025, whereas fabric/textile is forecast to expand at an 8.91% CAGR through 2031.

- By end user, women held 52.30% of 2025 revenue, but men are expected to grow fastest at 8.57% through 2031.

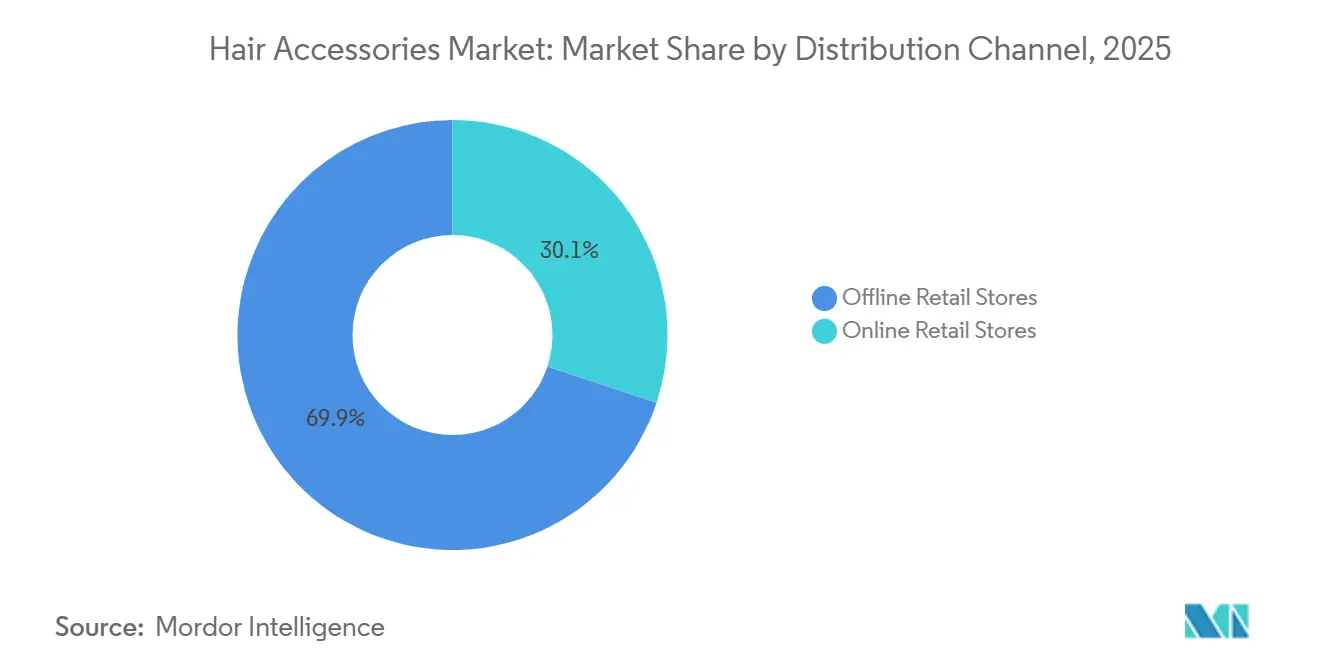

- By distribution channel, offline retail stores led the global hair accessories market with a share of 69.89% in 2025, while online retail stores are anticipated to register the fastest CAGR of 10.05% during 2026-2031.

- By geography, Asia-Pacific led the global hair accessories market with a share of 35.21% in 2025, and is anticipated to register the fastest CAGR of 9.78% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hair Accessories Market Trends and Insights

Drivers Impact Table*

| Driver | ~% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fashion consciousness and increasing use of hair accessories as style statement | +1.8% | Global | Short term (≤ 2 years) |

| Social media and celebrity-driven hair styling trends boosting product adoption | +1.5% | Global; concentrated in North America, Asia-Pacific, and Europe | Short term (≤ 2 years) |

| Growing demand for premium and fashion-oriented hair accessories | +1.1% | North America and Europe | Medium term (2-4 years) |

| Increasing popularity of wigs and hair extensions for fashion and aesthetic enhancement | +0.9% | Global; Asia-Pacific and North America as key markets | Medium term (2-4 years) |

| Expansion of fast fashion accessory collections | +0.8% | Global; Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Rising influence of K-beauty, J-beauty, and global fashion trends | +0.6% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising fashion consciousness and increasing use of hair accessories as style statement

Driven by increasing fashion awareness and the influence of digital trend culture, the hair accessories market has transitioned from offering purely functional products to delivering significant style statements. Gen Z, recognized for its fashion-forward spending behavior, is leading this shift by adopting aesthetics such as the "clean girl" and "soft girl" styles. In 2024, Gen Z constitutes approximately 20.81% of the United States population, according to the United States Census Bureau[3]Source: United States Census Bureau, "Birth Cohorts Geographic Mobility Report," census.gov. These trends have transformed basic items like hair elastics into premium offerings, including silk scrunchies and acetate barrettes. Social media platforms, including TikTok and Pinterest, are instrumental in amplifying these trends, driving demand for accessories that cater to specific subcultures rather than generalized categories. As a result, manufacturers that can adapt to rapidly evolving aesthetics and maintain close cultural alignment with trend-driven communities are achieving enhanced customer loyalty and higher-value transactions. This evolution highlights the increasing importance of design flexibility and authentic storytelling, which are now more critical to success than traditional mass-market approaches.

Social media and celebrity-driven hair styling trends boosting product adoption

Social media platforms, particularly TikTok and Instagram, are transforming the hair accessories market. Trends now evolve at unprecedented speeds, with viral content directly driving consumer purchasing behavior. These platforms function as both discovery and transaction channels, heavily influenced by electronic word-of-mouth (eWOM). A 2025 study published in PLOS ONE underscores the impact of eWOM, demonstrating its statistically significant positive effect on Generation Z's purchase intentions, with a path coefficient of β = 0.167 (p < 0.05)[1]Source: Public Library of Science (PLOS), "Uncovering the influence of social media marketing activities on Generation Z’s purchase intentions," journals.plos.org. The study further highlights that eWOM positively mediates the relationship between information adoption and perceived product quality. This accelerated feedback mechanism benefits agile direct-to-consumer (DTC) brands and challenger companies, enabling them to quickly adapt to evolving consumer preferences. Conversely, legacy brands with longer production cycles face the risk of inventory misalignment. In this rapidly changing market environment, success hinges on speed, cultural relevance, and the ability to effectively engage with digital communities.

Growing demand for premium and fashion-oriented hair accessories

The increasing demand for premium and fashion-oriented hair accessories is driving a significant segmentation within the market, distinguishing luxury styling products from mass-market offerings. Luxury brands, such as Balmain Hair Couture, are leading this trend. Their handcrafted cellulose acetate clips, featuring 18-karat gold-plated signature logos, are positioned as high-value investment pieces. Despite mounting counterfeit challenges in the mid-tier segment, Balmain continues to maintain disciplined pricing strategies. Simultaneously, sustainability regulations, including the European Union (EU) Green Deal, are facilitating premiumization. By adopting biodegradable and recycled materials, brands are not only ensuring regulatory compliance but also leveraging sustainability as a competitive advantage. Furthermore, premiumization extends beyond material luxury to include functional innovation. For example, Goody's ComfortFlex line, launched in February 2026 and designed for active consumers, exemplifies this shift. Collectively, these dynamics highlight that premium hair accessories now encompass luxury, sustainability, and functionality, each addressing distinct consumer motivations and reinforcing the market's transformation into a fashion-forward lifestyle category.

Increasing popularity of wigs and hair extensions for fashion and aesthetic enhancement

Wigs and hair extensions, previously considered niche products, have experienced significant growth in demand, establishing themselves as essential components within the fashion industry. Their adaptability enables immediate transformations, making them indispensable for both routine use and high-profile events. Modern consumers, influenced by celebrity endorsements and trends propagated through social media platforms, increasingly utilize these products to experiment with various hair lengths, textures, and colors without committing to permanent changes. Technological advancements in synthetic fiber production, which now deliver natural-looking and heat-resistant options, have enhanced accessibility. This development allows a wider consumer base to access premium-quality styling solutions at competitive price points. This trend reflects a broader cultural shift toward personalization and self-expression, positioning wigs and hair extensions as critical tools for defining individual identity and aesthetic preferences. As a result, these products have transitioned from niche offerings to integral elements of the evolving fashion landscape, seamlessly integrating innovation, creativity, and everyday practicality.

Restraints Impact Analysis*

| Restraint | ~% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit and low-quality products affecting brand value | -1.3% | Asia-Pacific (India, China); Middle East and Africa; South America | Short term (≤ 2 years) |

| Raw material price volatility impacting manufacturing costs | -0.9% | Global | Medium term (2-4 years) |

| High susceptibility to rapidly changing fashion trends | -0.7% | Global | Short term (≤ 2 years) |

| Limited product replacement cycle for basic hair accessories | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit and low-quality products affecting brand value

Counterfeit and low-quality products are negatively impacting brand value in the global hair accessories market. Ultra-realistic replicas now closely imitate both the design and packaging of genuine items, rendering them nearly indistinguishable. These "super-fakes" gain momentum through social media narratives, which portray them as legitimate alternatives. This practice not only diminishes consumer trust but also weakens the identity of premium brands. Simultaneously, mass-market platforms are inundated with ultra-cheap, unbranded products, exerting pressure on the profit margins of volume-tier players. The implications are significant: In April 2025, 'Headline Hairs' and 'Hair-fixing' at Chalakuzhy sold a counterfeit wig to a 52-year-old cancer patient, who was assured it was made from real human hair. This incident prompted a police investigation under the Bureau of National Standards (BNS) Section 318 (4) for cheating. Such cases highlight the direct harm counterfeits can cause to consumers and the resulting damage to brand credibility. To address these challenges, companies are increasingly implementing measures such as design patent enforcement, trade dress protection, and adherence to compliance frameworks regarding material labeling and product safety. These initiatives emphasize the critical role of authenticity and consumer trust as primary drivers of competitive differentiation.

Raw material price volatility impacting manufacturing costs

In the global hair accessories market, rising costs of specialty inputs, such as cellulose acetate for premium clips, elastane (a synthetic fiber known for its exceptional elasticity) for hair ties, and high-purity metals for bobby pins and barrettes, are increasingly attributed to fragmented supply chains, geopolitical disruptions, and a shift towards sustainability. As brands strive to meet both consumer and regulatory demands, the transition towards certified organic and biodegradable materials presents procurement challenges, inflating costs and complicating product formulations. This unpredictability compresses lead times for seasonal planning, making it challenging to keep pace with rapidly evolving social media trends without jeopardizing profit margins or inventory alignment. While companies with vertically integrated supply chains or long-term supplier contracts navigate these pressures more effectively, others struggle to balance cost management with design flexibility. This volatility not only impacts profitability but also compels brands to reevaluate their sourcing strategies and innovation pipelines, emphasizing the need for resilience in a market where speed and authenticity are critical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hair Ties & Scrunchies Lead Volume While Wigs Drive Value Expansion

In 2025, hair ties, elastics, and scrunchies dominate the market, accounting for 29.89% of the market share. Their strong market position is attributed to their universal functionality, high replenishment frequency, and resilience to evolving fashion trends. Previously considered basic elastic bands, scrunchies have transitioned into high-demand fashion accessories. Premium variants crafted from materials such as silk, satin, velvet, and organic cotton now command higher price points. Other segments within the market further highlight this trend: Headbands balance practicality and fashion appeal. For example, Lele Sadoughi collaborated with United States Figure Skating for the 2025 World Championships, while Jennifer Behr launched The Adorned Fall Bridal Collection in June 2025, featuring heirloom-quality headpieces that elevate accessories into investment-worthy items. These developments emphasize the transformation of functional product categories into aspirational lifestyle offerings.

Conversely, Wigs and Hair Extensions represent the fastest-growing category, projected to achieve a CAGR of 9.22% during the forecast period of 2026 to 2031. This growth is driven by the global influence of K-pop aesthetics, the increasing popularity of sleek "glass hair" trends, and technological advancements in synthetic fibers that provide natural-looking, heat-resistant options at competitive price points. This segment is emerging as a key driver of market value expansion, enabling consumers to experiment with personal identity and style beyond traditional accessory boundaries. As product quality improves and aesthetic options diversify, wigs and hair extensions are becoming mainstream, redefining the premium segment of the market and unlocking new growth opportunities.

By Material: Plastic Anchors Volume as Fabric/Textile Captures the Sustainability Premium

In 2025, the plastic segment maintains its dominance in the global hair accessories market, accounting for a 39.96% market share. This leadership is primarily driven by its versatility, cost-effectiveness, and widespread application in high-demand products such as clips, headbands, and combs. However, this dominance is increasingly being challenged. Environmentally conscious consumers are shifting towards biodegradable alternatives, while high-end buyers are transitioning to cellulose acetate, which is recognized as a premium and more environmentally friendly substitute for conventional thermoplastics. Metal is also gaining strategic importance in the premium segment, with luxury brands such as Balmain Hair Couture introducing handcrafted clips featuring 18-karat gold-plated logos on hypoallergenic cellulose acetate bases. These developments highlight the impact of regulatory frameworks and evolving consumer expectations, which are reshaping the material composition in a category historically dominated by plastic.

Fabric and textile materials are emerging as the fastest-growing segment in the hair accessories market, with a CAGR of 8.91% projected between 2026 and 2031. This growth is fueled by increasing consumer demand for accessories that are gentle on the skin and minimize hair damage, aligning with broader trends in clean beauty and wellness. Natural fibers such as organic cotton and silk are gaining popularity, not only for their comfort but also for their strong sustainability credentials, supported by the global expansion of the organic textiles sector. In Europe, regulatory pressures targeting single-use plastics and requirements for compliance with circular economy principles are accelerating this transition, compelling brands to adapt more rapidly. As a result, fabric-based accessories are capitalizing on the sustainability premium, positioning themselves as aspirational and responsible choices in a market where material innovation is becoming a critical differentiator.

By End User: Women Lead but Men Represent the Decisive Growth Variable

In 2025, the women's segment dominates the global hair accessories market, commanding a 52.30% share. This trend underscores the historical association of hair accessories with female grooming and the tendency for women to spend more per transaction. While women's accessories cater to both practical needs and fashion aspirations, children's accessories, driven by school needs and character licensing, contribute to volume but lack premiumization. The prominence of women in this market highlights their pivotal role in steering product innovation, brand strategies, and ensuring market stability.

Meanwhile, the male segment is on a rapid ascent, anticipated to grow at a CAGR of 8.57% from 2026 to 2031. This surge is largely attributed to a generational shift, especially among Generation Z (Gen Z), in how men perceive and engage with their appearance. Notably, South Korean men's fashion is embracing gender-neutral accessories, from scrunchies to silk bands, a trend that's gaining traction globally, thanks in part to Korean pop (K-pop) and drama enthusiasts. Furthermore, collaborations, such as TELETIES’ partnership with Women's National Basketball Association (WNBA) star Lexie Hull in April 2026, underscore the burgeoning crossover between athletics and hair accessories. As societal norms shift towards inclusivity in styling, the male segment emerges as a key growth driver, with the potential to exceed current forecasts, especially if the trend of gender-neutral beauty continues its spread in both Asia-Pacific and Western regions.

By Distribution Channel: Offline Retail Retains Scale as Social Commerce Redefines the Online Opportunity

In 2025, offline retail stores maintain a dominant position, accounting for 69.89% of the global hair accessories market. This dominance highlights the tactile and impulse-driven nature of accessory purchases. Key sales channels include mass merchants, drugstores, and specialty beauty retailers. Offline retail demonstrates strength in capturing both habitual replenishment and spontaneous purchases. Trend-responsive business models, such as Lovisa, which operated 1,095 stores globally as of the first quarter of 2026, illustrate the continued viability of physical retail when paired with fast-refresh product assortments and strategic expansion of store locations. This distribution channel not only provides scale and stability but also reinforces its critical role in the overall market structure.

Conversely, online retail represents the fastest-growing distribution channel, with a projected CAGR of 10.05% between 2026 and 2031. This growth is driven by the rise of social commerce, direct-to-consumer (DTC) platforms, and the expansion of online marketplaces in high-growth regions. The online channel is increasingly recognized as a platform for aspirational purchases, gifting, and the discovery of new brands. Investments in supply chain infrastructure, such as Goody's 2026 automation-driven fulfillment partnership, underscore the operational requirements for scaling digital sales. As social commerce continues to mature, the growth of online retail will redefine consumer engagement. At the same time, immersive offline experiences are anticipated to counterbalance the commoditization of digital channels, fostering a complementary dynamic between the two distribution channels.

Geography Analysis

Asia-Pacific, commanding a 35.21% share in 2025, emerges as both the largest and fastest-growing region in the global hair accessories market, with a projected expansion at a 9.78% CAGR from 2026 to 2031. This dual status underscores its significance as a manufacturing hub and a vibrant consumer market. While China and India spearhead mass-market demand, South Korea, Japan, and Australia champion premiumization, each with their unique aesthetic influences. The K-hair movement is spurring regional spending, and Japan’s revival of Showa-era hairstyles introduces a distinct cultural nuance. Additionally, emerging markets like Indonesia, Vietnam, and Thailand are witnessing rapid growth, buoyed by a rising middle class, increased smartphone penetration, and the influence of e-commerce.

North America and Europe, while each holding substantial market shares, are shaped by their unique consumer dynamics. North America reaps the benefits of a mature retail infrastructure, robust direct-to-consumer (DTC) activities, and a strong influencer presence on platforms like TikTok and Instagram. In Europe, markets like France, Italy, and the United Kingdom emphasize fashion premiumization, while Germany and the Nordics navigate a regulatory-driven shift towards sustainability. The European Union (EU) Green Deal is steering brands towards biodegradable and recycled materials, a move that, while elevating per-unit costs, bolsters their premium positioning. Concurrently, collaborations like Goody’s 2026 partnership with Lee® denim underscore North America’s penchant for brand storytelling and limited-edition launches, fueling incremental demand.

While South America and the Middle East & Africa hold smaller market shares, they present distinct strategic opportunities. Brazil stands as the anchor for South America, with a consistent demand for wigs, extensions, and protective-style accessories, underscoring the cultural importance of Afro-Brazilian beauty practices. In the Middle East, conservative fashion norms drive a specialized demand for decorative pins, fabric headbands, and hair ties, often worn with head coverings. This segment remains largely untapped by global brands. Meanwhile, Africa is on a rapid ascent, led by South Africa, Nigeria, and Egypt, where wigs and braiding extensions are culturally significant.

Competitive Landscape

The global hair accessories market is highly fragmented, with competition spread across mass-market, luxury, and emerging challenger brands. At the mass-market tier, established players like Conair and Goody dominate traditional retail channels, while newer entrants are leveraging direct-to-consumer and social commerce strategies to capture attention and build scale. Kitsch is a prime example of this disruption, achieving global distribution and rapid growth through social-first marketing and omnichannel expansion. The strategic divide is clear: legacy brands rely on collaborations and limited-edition launches to drive consumer engagement, while innovators differentiate through proprietary comfort technologies and patented designs such as Invisibobble’s spiral hair tie.

White space opportunities are opening in underserved niches, including men’s styling accessories, gender-neutral products, and functional-performance segments aimed at athletic consumers. Luxury brands such as Jennifer Behr, Balmain Hair Couture, France Luxe, and Lele Sadoughi are carving out distinct positions through craftsmanship, material provenance, and intellectual property protection.

Emerging disruptors represent the most sustained challenge to incumbents, combining agile supply chains with social commerce execution to capture consumer attention at speed. Legacy mass-market players are responding with investments in fulfillment automation and collaboration-driven product pipelines to close this gap. The competitive field is therefore defined by a dynamic interplay between heritage scale, luxury exclusivity, and disruptive agility, a balance that will continue to shape how brands position themselves in a market where authenticity, innovation, and speed are decisive.

Hair Accessories Industry Leaders

-

Goody

-

Conair

-

Invisibobble

-

Kitsch

-

France Luxe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Prior to the start of the new WNBA season, Indiana Fever guard Lexie Hull collaborated with TELETIES to introduce a limited-edition hair accessory collection. The collection featured TELETIES' signature spiral hair ties, offered in various colors and sizes. Designed to deliver a strong, no-slip grip while being gentle on hair, these ties also served as a stylish wrist accessory.

- March 2026: Beauty By Imagination (BBI), a prominent company in the hair care industry, expanded its collaboration with Barrett Distribution Centers by transitioning the fulfillment operations of its Goody brand. As a result, Barrett managed the fulfillment for BBI's entire United States brand portfolio. Headquartered in Commack, New York, BBI housed a diverse range of brands, including WetBrush, Ouidad, Curls, Bio Ionic, and Goody.

- February 2026: Goody and Wet Brush launched a limited-edition collection in partnership with Mackenzie-Childs, a prominent artisan-driven American heritage home décor brand. This exclusive collection, introduced in 2026, was made available at Target and featured a curated range of hair brushes and accessories that combined reliable performance with Mackenzie-Childs' distinctive aesthetic.

Global Hair Accessories Market Report Scope

Hair accessories are decorative, functional, or styling products designed to secure, manage, enhance, or adorn hair. These products are used for everyday grooming, hairstyling, fashion expression, and special occasions across various age groups and genders. Hair accessories include items such as hair clips, pins, headbands, hair ties, elastics, scrunchies, combs, wigs, hair extensions, and other products used to hold, style, or embellish hair.

The hair accessories market is segmented based on product type, material, end user, distribution channel, and geography. By product type, the market is segmented into Hair Clips and Pins, Headbands, Hair Ties, Elastics and Scrunchies, Wigs and Hair Extensions, Hair Combs, and Others. By material, the market is segmented into Plastic, Fabric/Textile, Metal, and Others. By end user, the market is segmented into Women, Men, and Children. By distribution channel, the market is segmented into Offline Retail Stores and Online Retail Stores. By geography, the market is segmented by North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Hair Clips and Pins |

| Headbands |

| Hair Ties, Elastics and Scrunchies |

| Wigs and Hair Extensions |

| Hair Combs |

| Others |

| Plastic |

| Fabric/Textile |

| Metal |

| Others |

| Women |

| Men |

| Children |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hair Clips and Pins | |

| Headbands | ||

| Hair Ties, Elastics and Scrunchies | ||

| Wigs and Hair Extensions | ||

| Hair Combs | ||

| Others | ||

| By Material | Plastic | |

| Fabric/Textile | ||

| Metal | ||

| Others | ||

| By End User | Women | |

| Men | ||

| Children | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the size of the global hair accessories market in 2025, and what is its projected value by 2031?

The global hair accessories market was valued at USD 22.73 billion in 2025 and is projected to reach USD 35.74 billion by 2031, expanding at a CAGR of 7.92% during 2026–2031.

Which product type held the largest share in the Global Hair Accessories Market in 2025?

Hair Ties, Elastics & Scrunchies accounted for the largest share of the market, representing 29.89% of global revenue in 2025.

Which distribution channel dominated the Global Hair Accessories Market in 2025?

Offline Retail Stores dominated the market with a 69.89% share in 2025, supported by strong sales through supermarkets, beauty stores, and specialty retailers.

Which product type is expected to be the fastest-growing segment during 2026–2031?

The Wigs & Hair Extensions segment is projected to be the fastest-growing product category, registering a CAGR of 9.22% during the forecast period.

Which region accounted for the largest share of the Global Hair Accessories Market?

Asia-Pacific was the leading regional market, accounting for 35.21% of global revenue in 2025, and is also expected to be the fastest-growing region through 2031.

Page last updated on: