Motorcycle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 142.83 Billion |

| Market Size (2030) | USD 166.55 Billion |

| Growth Rate (2025 - 2030) | 3.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Motorcycle Market Analysis by Mordor Intelligence

The global motorcycle market size stands at USD 142.83 billion in 2025 and is forecast to touch USD 166.55 billion by 2030, reflecting a 3.12% CAGR over the period. Steady demand in Asia-Pacific, premium-segment upgrades in Europe and North America, and electrification momentum in all major regions collectively anchor this trajectory. Rapid urbanization across emerging economies continues to favor two-wheeler ownership as a congestion-beating mobility choice, while premium adventure and touring models attract affluent riders seeking lifestyle versatility. Government purchase incentives for battery-powered two-wheelers, expanding battery-swap infrastructure in Southeast Asia, and telematics-enabled value-added services from OEMs further reinforce demand. Meanwhile, raw-material price swings and Euro 5+ compliance costs intensify margin management pressures but also accelerate strategic pivots toward electric propulsion and digital revenue streams.

Key Report Takeaways

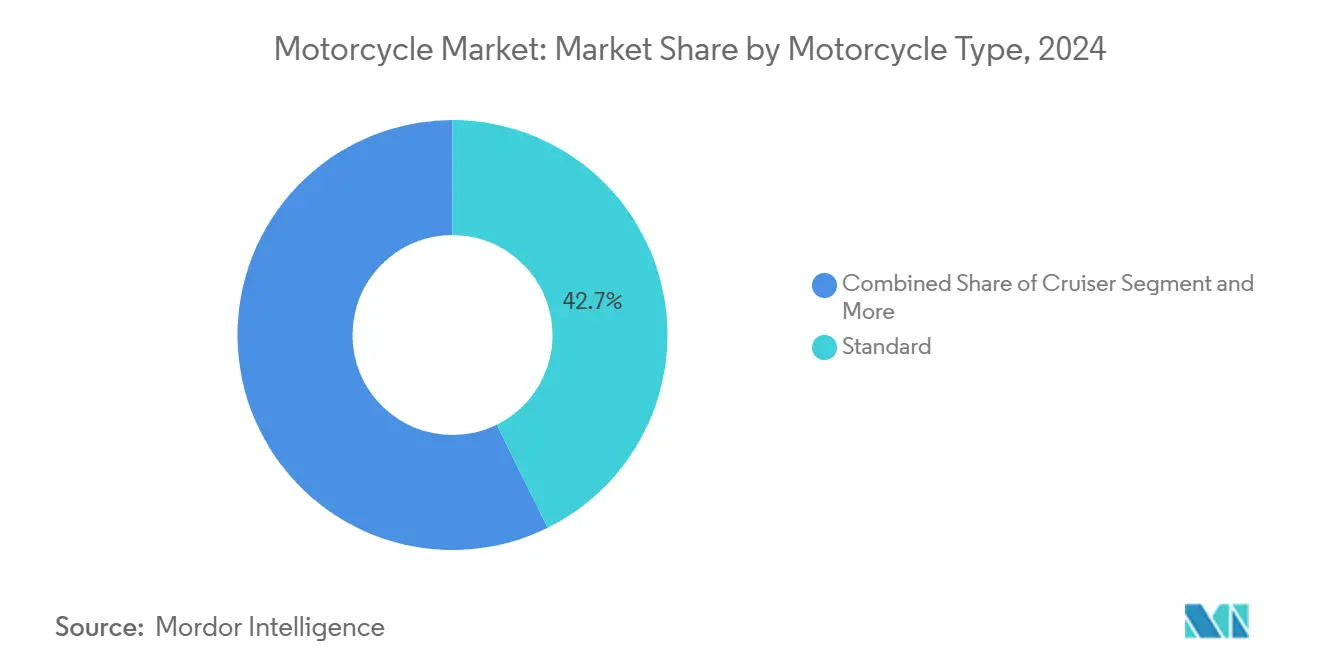

- By motorcycle type, standard models led with a 42.73% revenue share of the motorcycle market in 2024, whereas adventure motorcycles are advancing at a 10.12% CAGR through 2030.

- By engine capacity, motorcycles up to 200 cc accounted for the largest share at 50.86% in 2024, while the electric-dominant 200–400 cc segment is projected to expand at 12.38% CAGR through 2030.

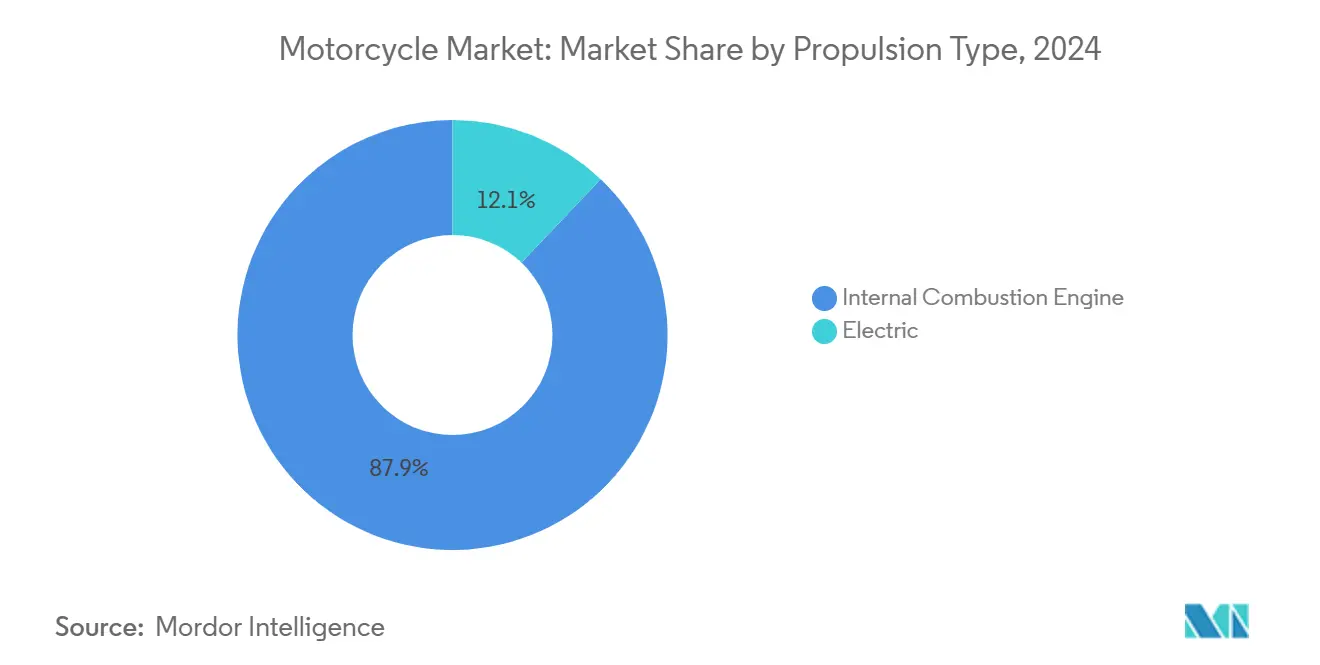

- By propulsion type, ICE variants retained 87.92% of motorcycle market share in 2024, yet electric models are expanding at a robust 23.77% CAGR to 2030.

- By application, personal use controlled 93.14% of the motorcycle market size in 2024, while commercial fleets are projected to compound at an 11.26% CAGR over the forecast window.

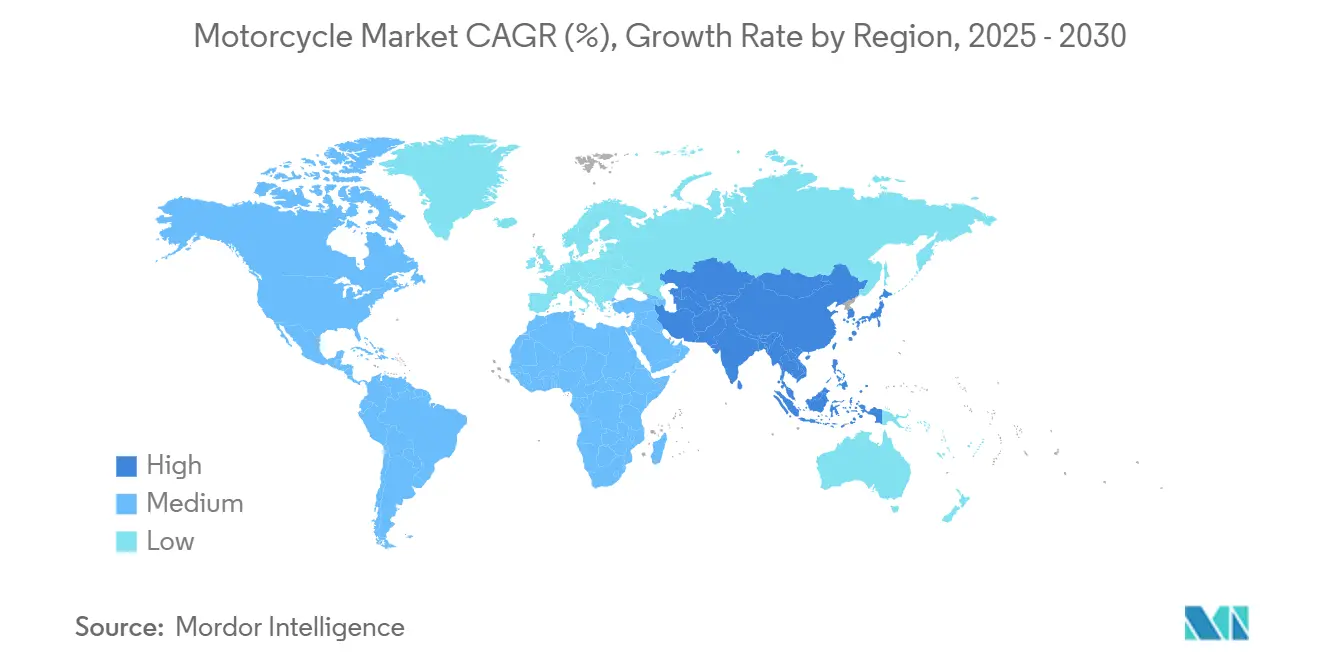

- By geography, Asia-Pacific captured 71.68% of 2024 revenue and is set to register an 8.09% CAGR between 2025 and 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Motorcycle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urban Middle-Class Expansion in South and Southeast Asia | +0.8% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Government EV Incentives Accelerating E-Motorcycle Uptake | +0.6% | Global, strongest in EU, North America, and Asia-Pacific | Short term (≤ 2 years) |

| Integration of ADAS and Connected Tech (IoT/Telematics) | +0.4% | North America and EU, expanding to Asia-Pacific premium segments | Long term (≥ 4 years) |

| After-Sales Subscription Revenue Models by OEMs | +0.3% | Global, led by premium markets | Medium term (2-4 years) |

| Growth of Last-Mile Gig-Economy Delivery Fleets | +0.7% | Global urban centers, strongest in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Low-Cost Battery-Swap Networks in Emerging Markets | +0.5% | Asia-Pacific core, pilot programs in Latin America and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Middle-Class Expansion in South and Southeast Asia

Southeast Asia's motorcycle adoption accelerates as urban middle-class populations expand, with Thailand targeting a 20-25% greenhouse gas reduction by 2030 while mandating that zero-emission vehicles comprise 30% of automotive production. This demographic shift creates a unique market dynamic where traditional mobility patterns intersect with environmental consciousness, driving demand for conventional and electric two-wheelers. Indonesia is the th ird-largest motorcycle market globally, following China and India. In 2024, motorcycle sales in Indonesia were recorded at 6.4 million units[1]"Behind the Slowdown in New Motorcycle Sales," kompas.id.. The region's infrastructure development lags behind vehicle adoption, creating opportunities for manufacturers who can deliver affordable, reliable transportation solutions that navigate congested urban environments while meeting emerging environmental standards.

Government EV Incentives Accelerating E-Motorcycle Uptake

Policy frameworks increasingly favor electric motorcycle adoption through direct purchase subsidies and infrastructure investments, with Indonesia implementing a Rp 7 million subsidy program that expanded eligibility criteria in August 2024 to accelerate motorcycle market penetration[2]"Data Collection and Confirmation Survey on Electrical Motorcycle Industry Development and Strengthening of Supply Chain in Indonesia," Japan International Cooperation Agency (JICA), openjicareport.jica.go.jp.. European markets face mandatory Euro 5+ emissions compliance, creating cost pressures that inadvertently accelerate electric adoption as manufacturers balance compliance investments against electric development programs. The strategic implication extends beyond immediate sales impact—governments are essentially subsidizing the transition infrastructure that will determine long-term market leadership. Thailand's battery-swapping pilot programs through Oyika demonstrate how policy support enables ecosystem development that traditional charging infrastructure cannot match in dense urban environments.

Integration of ADAS and Connected Tech (IoT/Telematics)

Advanced driver assistance systems and connectivity features transform motorcycles from purely mechanical devices into data-generating platforms that enable new revenue streams and safety improvements in the motorcycle market. Harley-Davidson's H-D Connect system exemplifies this evolution, providing theft protection, vehicle diagnostics, and ride tracking capabilities that create ongoing customer relationships beyond the initial purchase transaction. The technology integration extends to fleet management applications where commercial operators leverage telematics for route optimization, maintenance scheduling, and driver behavior monitoring. Ultraviolette's AI co-pilot system demonstrates how electric motorcycle manufacturers embed intelligence that traditional ICE competitors cannot easily replicate, creating differentiation opportunities in premium segments of the motorcycle market.

After-Sales Subscription Revenue Models by OEMs

Manufacturers increasingly monetize the ownership experience through subscription-based services that generate recurring revenue streams while strengthening customer relationships in the motorcycle market. Zero Motorcycles' integration with Salesforce demonstrates how electric motorcycle companies leverage customer data platforms to deliver personalized services, predictive maintenance alerts, and software updates that enhance vehicle performance over time. This business model transformation reflects broader automotive industry trends where hardware sales represent the initial transaction while software and services drive long-term profitability. The approach particularly benefits electric motorcycle manufacturers who can offer battery health monitoring, charging optimization, and performance tuning services that ICE competitors cannot match with equivalent value propositions in the motorcycle market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE Phase-Out Regulations in Europe Raising Compliance Costs | -0.4% | Europe core, regulatory influence spreading globally | Short Term (≤ 2 years) |

| Raw-Material Price Volatility for Li-Ion Batteries | -0.6% | Global, most acute in cost-sensitive emerging markets | Medium Term (2-4 years) |

| Micro-Mobility Alternatives Cannibalising 0 to 200cc Demand | -0.3% | North America and EU urban centers, expanding to Asia-Pacific | Long Term (≥ 4 years) |

| Limited Resale Value of First-Gen E-Motorcycles | -0.2% | Global, most pronounced in developed markets | Medium Term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Last-Mile Gig-Economy Delivery Fleets

Commercial motorcycle adoption surges as e-commerce platforms and food delivery services scale operations, with business users in Indonesia typically covering 150-200 kilometers daily compared to private users' 15-70 kilometer range. This usage intensity creates distinct market dynamics where total cost of ownership calculations favor electric alternatives despite higher upfront costs, particularly when battery-swapping infrastructure enables rapid turnaround times that maximize earning potential. Pos Malaysia's fleet expansion demonstrates how institutional buyers drive volume adoption that accelerates infrastructure development and reduces per-unit costs through economies of scale. The commercial segment's growth at 11.26% CAGR reflects this fundamental shift where motorcycles transition from personal transportation to essential business tools that require different performance, reliability, and service characteristics in the motorcycle market.

ICE Phase-Out Regulations in Europe Raising Compliance Costs

Euro 5+ emissions standards impose particulate matter limits of 0.045 grams per kilometer alongside tightened carbon monoxide, hydrocarbon, and nitrogen oxide restrictions that fundamentally challenge two-stroke engine viability[3]"Euro 5 motorcycles," Infineum International Limited, insightinfineuminsight.com.. Manufacturers face substantial compliance investments for catalytic converters, advanced onboard diagnostics, and durability testing that must demonstrate emissions compliance after 20,000 kilometers of service life. The regulatory framework creates a strategic inflection point where traditional engine development costs increasingly compete with electric powertrain investments, potentially accelerating the industry's electrification timeline beyond market-driven adoption rates. Smaller manufacturers particularly struggle with compliance costs that favor larger players with greater R&D resources and global scale to amortize regulatory investments across multiple motorcycle markets.

Raw-Material Price Volatility for Li-ion Batteries

Lithium-ion battery costs, representing approximately 40% of electric motorcycle manufacturing expenses, create margin pressure that constrains electric adoption in price-sensitive motorcycle markets. Supply chain disruptions and raw material scarcity drive cost volatility that makes electric motorcycle pricing unpredictable, complicating manufacturer planning and consumer purchase decisions in the motorcycle market. The challenge extends beyond immediate cost impacts to encompass strategic supply chain dependencies where battery cell production concentration in specific geographic regions creates geopolitical risks that traditional ICE supply chains do not face. Manufacturers increasingly pursue vertical integration or long-term supply agreements to mitigate volatility, yet these strategies require substantial capital commitments that smaller players cannot easily accommodate in the motorcycle market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motorcycle Type: Adventure Segment Drives Premium Shift

Standard motorcycles command a 42.73% share, while the Adventure segment has the fastest growth at 10.12% CAGR in 2024, reflecting consumer preferences for versatile platforms that accommodate urban commuting and recreational touring applications. This segment expansion aligns with demographic trends where affluent millennials and Gen X riders seek multipurpose vehicles that justify higher price points through enhanced capability and premium positioning. Cruiser motorcycles benefit from Harley-Davidson's strategic repositioning, with the company launching updated 2025 models, including the Street Glide Ultra and Pan America ST, that target both traditional enthusiasts and younger demographics.

Sports motorcycles face headwinds from insurance costs and regulatory restrictions in key markets, while touring variants capture growth from aging demographics who prioritize comfort over performance. Off-road motorcycles experience steady demand driven by recreational usage and utility applications in rural markets. However, electric variants remain nascent due to range limitations and charging infrastructure constraints in remote areas. The segmentation shift toward adventure and touring categories signals broader market maturation where differentiation increasingly depends on lifestyle positioning rather than pure transportation utility.

By Engine Capacity: Electric Penetration Reshapes Traditional Categories

The up to 200cc segment maintains 50.86% market share in 2024, yet the electric-dominant 200-400cc category accelerates at 12.38% CAGR as manufacturers position electric powertrains in displacement categories traditionally serving urban commuting applications. This strategic positioning reflects electric motorcycles' torque characteristics that deliver performance comparable to larger displacement ICE engines while meeting regulatory requirements and consumer expectations for urban mobility. The 400-800cc segment experiences moderate growth as manufacturers balance performance demands with fuel efficiency requirements, while the above 800cc categories serve niche enthusiast markets with limited volume impact.

Electric motorcycle manufacturers increasingly target the 200-400cc equivalent performance range where battery technology delivers acceptable range and charging characteristics for typical usage patterns. Hero MotoCorp's VIDA Z electric scooter launch and TVS Motor's connected features demonstrate how traditional manufacturers integrate electric alternatives within existing product portfolios rather than creating separate electric brands. The capacity segmentation evolution suggests future market structure will increasingly reflect performance characteristics rather than traditional displacement categories as electric adoption accelerates.

By Propulsion Type: Electric Growth Accelerates Despite ICE Dominance

In 2024, ICE variants retained a dominant 87.92% market share, sustaining volumes for traditional manufacturers, while electric motorcycles are advancing rapidly with a projected 23.77% CAGR, positioning them as the primary driver of future market growth. This growth differential reflects infrastructure development, battery cost reductions, and regulatory support that collectively improve electric motorcycle value propositions relative to ICE alternatives. Indonesia's electric motorcycle sales growth from 10,000 units in 2021 to 62,000 units in 2023 demonstrates the acceleration potential when government subsidies align with improving technology and expanding infrastructure.

The propulsion type segmentation reveals strategic challenges for traditional manufacturers who must balance ICE product development investments with electric transition requirements. Yamaha's premium strategy in India, targeting 25-30% premium segment share by decade-end while expanding into 700-900cc categories, illustrates how established players leverage ICE expertise to fund electric development programs. Battery-swapping infrastructure development in markets like Thailand and Indonesia creates ecosystem advantages for electric alternatives that traditional fueling infrastructure cannot replicate, potentially accelerating the transition timeline beyond current forecasts.

By Application: Commercial Segment Expansion Drives Market Evolution

Personal applications dominate with 93.14% market share in 2024, yet commercial usage accelerates at 11.26% CAGR as delivery platforms, ride-hailing services, and logistics companies increasingly adopt motorcycles for last-mile operations. This application shift creates distinct market dynamics where total cost of ownership calculations, reliability requirements, and service network access become primary purchase criteria rather than traditional consumer preferences for styling, performance, or brand prestige. Commercial operators' daily usage intensity of 150-200 kilometers in markets like Indonesia creates favorable economics for electric alternatives despite higher upfront costs, particularly when battery-swapping infrastructure enables rapid turnaround times.

The application segmentation evolution reflects broader economic trends where gig economy expansion and e-commerce growth create new demand categories that traditional motorcycle manufacturers did not historically serve. Fleet operators increasingly require integrated telematics, predictive maintenance capabilities, and financing solutions that extend beyond individual vehicle sales to comprehensive mobility services. This transition suggests future market leadership may depend on manufacturers' ability to serve commercial customers' operational requirements rather than traditional consumer marketing approaches focused on individual buyers' emotional connections to motorcycle brands.

Geography Analysis

Asia-Pacific maintains 71.68% market share in 2024 while sustaining 8.09% CAGR through 2025-2030, driven by India's motorcycle production surge and the Philippines' 7% sales growth in 2024 to 1.68 million units—the highest growth rate in ASEAN. The region's dominance reflects urbanization trends, expanding middle-class populations, and infrastructure development favoring two-wheeler adoption over four alternatives in congested urban environments. Battery-swapping infrastructure development through partnerships like PowerPod-Mamotor in Southeast Asia creates competitive advantages that traditional markets cannot easily replicate, potentially extending Asia-Pacific's leadership position as electrification accelerates.

North America and Europe exhibit mature market characteristics with moderate growth rates yet drive premium segment expansion and technological innovation that influences global product development trends. European markets face regulatory pressures from Euro 5+ emissions standards that accelerate electric adoption while creating compliance costs for traditional manufacturers. Harley-Davidson's strategic repositioning in these markets, with 2025 model launches and expanded dealer networks, illustrates how premium manufacturers adapt to changing demographics and regulatory requirements while maintaining brand positioning. The regional contrast between Asia-Pacific's volume growth and Western markets' value growth creates different strategic imperatives for manufacturers seeking global scale versus premium positioning.

Latin America emerges as a growth opportunity with Mexico's motorcycle market projected to reach 6 million annual sales by 2029, tripling from current levels as delivery services and urban mobility needs drive adoption. The region's growth potential reflects economic development, urbanization trends, and infrastructure constraints that favor two-wheeler solutions over traditional automotive alternatives. Peru's 12.4% Q1 2025 growth demonstrates the region's momentum while Brazil's scooter segment expansion at 30.02% in H1 2024 illustrates category-specific opportunities. Middle East and Africa represent emerging opportunities where economic development and infrastructure needs create demand for affordable, reliable transportation solutions, though market development remains constrained by economic volatility and infrastructure limitations.

Competitive Landscape

The motorcycle industry exhibits moderate consolidation, with Japanese manufacturers Honda and Yamaha controlling a significant share of the combined global market, yet it faces intensifying competitive pressure from Chinese electric specialists and emerging market players who leverage cost advantages and government support to challenge established positions. Traditional competitive dynamics centered on brand loyalty, dealer networks, and engineering heritage increasingly give way to technology integration, total cost of ownership calculations, and ecosystem partnerships that encompass charging infrastructure, financing solutions, and digital services. KTM's financial restructuring and BMW's strategic acquisition discussions illustrate how even established premium manufacturers face pressure to consolidate or partner to maintain competitiveness in an evolving market landscape.

Electric motorcycle entrants like Zero Motorcycles, Energica, and regional players such as Ultraviolette create white-space opportunities by targeting performance segments that traditional manufacturers have not prioritized for electric conversion. The competitive landscape transformation accelerates as battery-swapping networks, subscription revenue models, and connected vehicle platforms create new competitive moats that favor companies with technology capabilities over traditional manufacturing scale advantages. Regulatory compliance requirements, particularly Euro 5+ emissions standards, create barriers that favor larger manufacturers with greater R&D resources while potentially opening opportunities for electric specialists who avoid ICE compliance costs entirely.

Motorcycle Industry Leaders

-

Honda Motor Co., Ltd.

-

Yamaha Motor Co., Ltd.

-

Hero MotoCorp Ltd.

-

Bajaj Auto Ltd.

-

TVS Motor Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Yamaha Motor India announced strategic expansion targeting 25-30% premium segment market share by decade-end, with plans to enter 700-900cc categories and scale Blue Square dealer network to 600 outlets while leveraging India as global export hub . This positioning reflects premium market opportunities in emerging economies where affluent consumers seek advanced motorcycle technologies.

- March 2025: Ultraviolette Automotive announced USD 70-100 million investment over 2-3 years to expand product portfolio across 5 platforms with 14 planned models, targeting 100,000 annual units within 3-4 years while exploring joint manufacturing synergies with TVS Motor. The investment demonstrates electric motorcycle manufacturers' scaling ambitions and partnership strategies.

- April 2024: Bajaj Auto announced INR 800 crore capex for FY25 including three-wheeler plant completion and Chetak electric scooter capacity expansion, alongside CNG motorcycle launch targeting mileage-conscious buyers in Northern and Western India markets. The investment reflects diversification strategies across propulsion technologies and market segments.

- April 2024: Hero MotoCorp opened 75,000-unit annual capacity assembly facility in Nepal through partnership with CG Motors, expanding international manufacturing footprint while serving growing South Asian demand through local production. The facility demonstrates regional expansion strategies that leverage cost advantages and market access.

Global Motorcycle Market Report Scope

| Standard |

| Cruiser |

| Sports |

| Adventure |

| Touring |

| Off-road |

| Up to 200 cc |

| 200 to 400 cc |

| 400 to 800 cc |

| Above 800 cc |

| Internal Combustion Engine (ICE) |

| Electric |

| Personal |

| Commercial |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Motorcycle Type | Standard | |

| Cruiser | ||

| Sports | ||

| Adventure | ||

| Touring | ||

| Off-road | ||

| By Engine Capacity | Up to 200 cc | |

| 200 to 400 cc | ||

| 400 to 800 cc | ||

| Above 800 cc | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Electric | ||

| By Application | Personal | |

| Commercial | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global motorcycle market in 2025?

It is valued at USD 142.83 billion with a forecast to reach USD 166.55 billion by 2030 at a 3.12% CAGR.

Which region leads in motorcycle sales?

Asia-Pacific holds 71.68% of 2024 revenue and will continue expanding at 8.09% CAGR through 2030.

What is driving the surge in electric motorcycles?

Purchase subsidies, battery-swap infrastructure, and tightening emissions rules are propelling a 23.77% CAGR for electric models.

Which motorcycle segment is growing the fastest?

Adventure motorcycles are rising at 10.12% CAGR as riders seek versatile, premium experiences.

How are OEMs generating recurring revenue?

They are rolling out connected-bike subscriptions, telematics data services, and battery-leasing plans that add income beyond initial sales.

What risks threaten expansion?

Euro 5+ compliance costs, lithium-ion price swings, and micro-mobility alternatives can shave up to 1.5 percentage points off projected CAGR.

Page last updated on: