Connected Motorcycle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 2.28 Billion |

| Growth Rate (2026 - 2031) | 32.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Connected Motorcycle Market Analysis by Mordor Intelligence

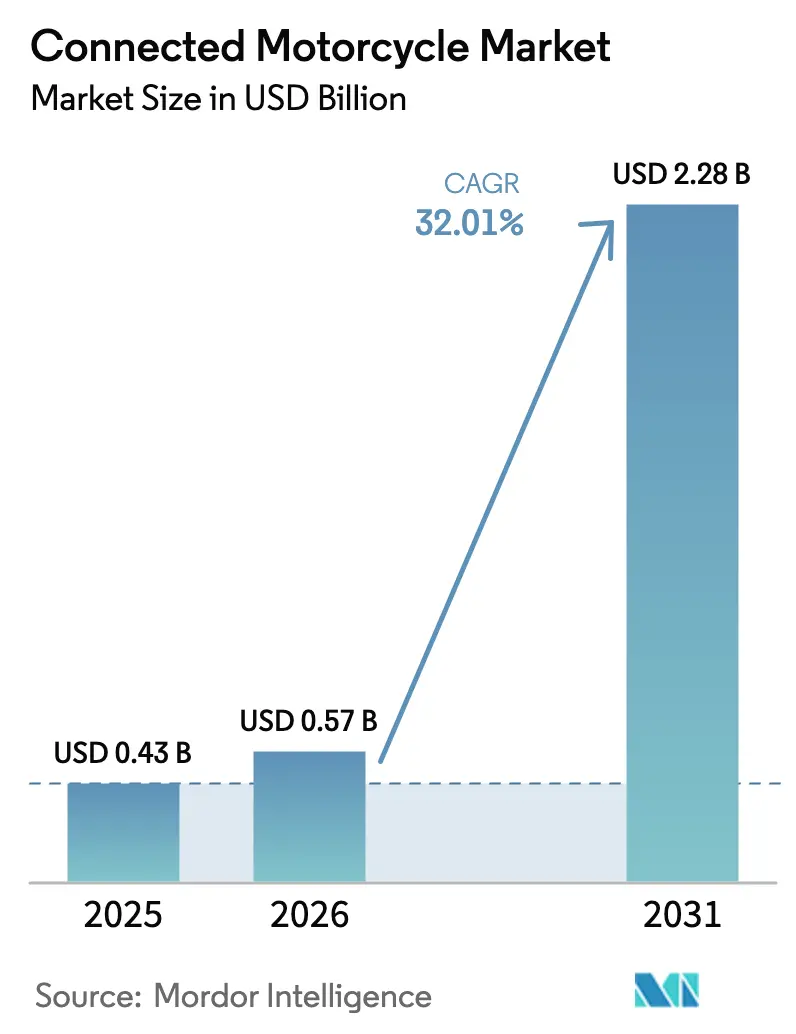

The connected motorcycle market size is expected to grow from USD 0.43 billion in 2025 to USD 0.57 billion in 2026 and is forecasted to reach USD 2.28 billion by 2031 at a 32.01% CAGR over 2026-2031. Regulatory cybersecurity deadlines, 5G network densification, and the increasing integration of telematics in premium two-wheelers underpin this rapid rise in value. Cellular 4G and 5G technologies already account for the majority of on-road links. At the same time, radar-enabled rider assistance is poised to surpass infotainment features as collision avoidance transitions from prototypes to series production. Hardware suppliers are reducing power draw with edge-AI chips, alleviating battery-life concerns and encouraging OEMs to integrate always-on connectivity across more price tiers. The Asia-Pacific region remains the epicenter of growth, driven by India’s burgeoning premium segment and China’s investments in smart roads, while Europe and North America sustain solid momentum as the UNECE R155 and R156 rules make secure telematics compulsory.

Key Report Takeaways

- By service, infotainment retained 34.31% revenue share in 2025, while the driver assistance sub-segment is projected to post a 44.21% CAGR through 2031.

- By hardware type, embedded control units held 54.82% of the connected motorcycle market share in 2025, while smartphone-based solutions are set to register a 37.51% CAGR through 2031.

- By end user, private consumers accounted for 68.31% of the connected motorcycle market in 2025, whereas commercial fleets are expected to grow at a 32.11% CAGR through 2031.

- By network type, cellular 4G/5G networks led with 59.31% of the connected motorcycle market share in 2025 and are expanding at a 41.11% CAGR through 2031.

- By geography, Asia-Pacific led the connected motorcycle market with 41.73% market share in 2025 and is projected to expand at a 35.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Connected Motorcycle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Roll-Outs | +7.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Cyber-Security Mandates (UNECE R155/156) | +6.0% | Europe, North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Integration of eSIM-Based Telematics | +5.5% | Global, strongest in Europe and Asia-Pacific | Medium term (2-4 years) |

| ADAS-Ready Two-Wheelers | +4.8% | Europe, North America, premium Asia-Pacific | Medium term (2-4 years) |

| Premium Bike Sales Boom | +3.7% | Asia-Pacific core, spill-over to Middle East | Long term (≥ 4 years) |

| Edge-AI Chips | +2.5% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Roll-Outs Enabling Ultra-Low-Latency V2X

With stand-alone 5G networks achieving radio latency in the millisecond range, features like collision warnings and cooperative adaptive cruise control are becoming a reality for riders. Autotalks and Rolling Wireless have unveiled a 5G-V2X chipset family set for series production, compatible with both cellular V2X and older DSRC modes. Japan has allocated a dedicated frequency band for V2X, laying the groundwork for nationwide V2X pilot corridors. Meanwhile, in the United States, efforts are underway to expand V2X coverage on highways. Such initiatives firmly establish 5G as the cornerstone of the connected motorcycle market, enabling advanced safety features and seamless communication for riders over the coming decade.

Government Cyber-Security Mandates (UNECE R155/156)

UNECE Regulation 155 obliges every new motorcycle type-approval from July 2029 to include a full Cyber Security Management System, while Regulation 156 codifies software-update logging and validation. These rules apply to category L vehicles and push security hardware costs into even entry-level models. Tier-one suppliers respond with bundled telematics and ABS units that amortize certification expense. Smaller manufacturers must weigh white-label platforms against in-house solutions, a strategic fork that can alter brand differentiation. Early adoption helps firms avoid future production bottlenecks as the deadline approaches.

Surging Integration of eSIM-Based Telematics

eSIM modules displace physical SIM cards, allowing motorcycles to roam seamlessly and switch carriers without hardware swaps. Qualcomm’s QWM2290 chipset combines LTE/5G connectivity and GNSS into a single package, reducing board space and certification cycles[1]"Qualcomm® QWS2290/QWM2290 Processors", Qualcomm, qualcomm.com. Fleet operators use the technology to optimize coverage and service fees, while Sentiance reports 30-40% reductions in claims for bikes fitted with behavior-tracking telematics. Partnerships like Sibros with PIERER Mobility illustrate how over-the-air platforms shorten feature rollouts and reduce dealership visits. Collectively, these developments strengthen the connected motorcycle market across premium and mainstream segments.

OEM Push Toward ADAS-Ready Two-Wheelers

Motorcycle makers emulate automotive safety roadmaps by embedding adaptive cruise control, blind-spot detection, and emergency call functions. Bosch's radar-based cruise control on the Ducati Multistrada V4 and BMW R 1250 RT, combining its inertial measurement unit with front-facing sensors to maintain safe distances[2]Edward C. Fatzinger, William Gonzaga, "An Evaluation of the Bosch Radar-Based Adaptive Cruise Control System on a 2022 Ducati Multistrada V4S", ResearchGate GmbH, www.researchgate.net. BMW’s ConnectedRide initiative integrates motorcycles into Car-to-X networks, allowing other vehicles to receive proximity alerts from two-wheelers. Higher safety ratings support insurance discounts, enlarging the total addressable connected motorcycle market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incremental BOM Cost | -3.2% | Global, acute in South Asia, Africa, South America | Short term (≤ 2 years) |

| Li-Ion Thermal-Runaway Recalls | -2.1% | Asia-Pacific, spill-over to Europe and North America | Medium term (2-4 years) |

| Rider Privacy Concerns | -1.8% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Limited DSRC/5.9 GHz Spectrum | -1.5% | Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Incremental BOM Cost for Mass-Market Bikes

Entry-level motorcycle manufacturers are experiencing a squeeze on margins as the addition of telematics, displays, and secure gateways significantly increases component costs. Renesas is addressing this challenge with its single-chip telematics controllers, which reduce both PCB area and firmware overhead. However, costs are further increased by UNECE R155 compliance, which requires comprehensive cybersecurity audits. To maintain their edge, manufacturers such as Hero MotoCorp are turning to smartphone-based dashboards. These dashboards shift much of the processing burden to the rider’s device. Yet, this integration complexity can detract from the overall user experience. Such challenges are curbing the rapid adoption of connected motorcycles, especially in price-sensitive segments.

Li-Ion Thermal-Runaway Recalls Dampen OEM Appetite

High-profile battery fires in 2024-2025 highlighted the risk of thermal runaway in compact electric motorcycles, triggering official safety investigations. Regulators responded by strengthening battery-test protocols, which now include thermal-propagation and vibration checks, thereby raising the compliance bar for every new model. OEMs consequently scrutinize add-on electronics near the battery enclosure, and telematics modules draw particular focus because they introduce continuous power consumption in a confined space. Engineers counter the risk with ultra-low-sleep-mode designs and layered battery-management controls that isolate failing cells before temperatures escalate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Driver Assistance Surges as Collision Avoidance Scales

Infotainment accounted for 34.31% of 2025 revenue, indicating the current center of gravity in the connected motorcycle market. Driver assistance services are projected to grow at 44.21% between 2026 and 2031, the fastest among all service categories. Mandatory eCall functions, as outlined by the European Commission, transform safety services into non-optional add-ons. Meanwhile, remote diagnostics and firmware updates satisfy UNECE security rules, and usage-based insurance gains favor with risk-averse insurers in high-traffic regions. The combined pull of regulation and insurer incentives positions driver assistance as the lead growth engine over the forecast horizon.

Regulation influences adoption priorities, encouraging OEMs to invest in over-the-air capabilities while leaving infotainment dependent on discretionary spending. Driver assistance sits between crowd-pleasing features and mandatory functions, giving it a balanced mix of regulatory and market support. Commercial fleets tend to prioritize vehicle management for cost control, whereas private riders prefer a balance of entertainment and safety. As a result, service portfolios diverge by customer group, and suppliers craft tiered offerings that align with each segment’s willingness to pay. This dynamic ensures the connected motorcycle market continues to diversify its revenue streams.

By Hardware Type: Tethered Smartphone Solutions Gain as Cost Pressures Mount

Embedded control units commanded 54.82% of 2025 deployments, reflecting their ability to provide always-on connectivity and seamless over-the-air updates. Premium brands embed these units under the seat or fairing to deliver integrated navigation, diagnostics, and rider-assistance alerts. Rising production volumes gradually trim bill-of-materials costs, but budget-conscious OEMs still seek lower-priced alternatives to address price-sensitive buyers. Tethered smartphone solutions, forecast to grow at a 37.51% CAGR through 2031, answer that need by using the rider’s handset for data processing and network access. Although tethering lacks automatic crash notification if the phone is absent, it offers a compelling entry point for first-time connected motorcycle customers.

Hybrid architectures sit between both extremes, combining a small embedded module for mandatory safety functions with a phone-based app for infotainment and ride analytics. This split hardware model helps OEMs comply with regulations while avoiding the full cost of a high-spec ECU. Integrated cockpit clusters, which incorporate a color display and telematics modem into the instrument panel, appeal to touring riders who spend long hours on the road and expect rich mapping capabilities on demand. Suppliers continue to shrink display bezels and improve sunlight readability, enhancing perceived value. As these advances roll into mid-range models, hardware diversity broadens the connected motorcycle market size and keeps competition active across price tiers.

By End User: Commercial Fleets Drive Telematics Adoption Through Operational ROI

Private consumers accounted for 68.31% of 2025 demand, underscoring the continued role of motorcycles in leisure touring, sport riding, and daily commuting. Riders appreciate theft-recovery tracking and navigation support that smartphone apps or embedded clusters readily provide. They also value safety enhancements that deliver forward-collision and blind-spot warnings without diminishing the sense of control. Subscription pricing remains a hurdle for some retail buyers, but bundled data plans and pay-once upgrades ease adoption friction. As premium motorcycles filter into emerging economies, private uptake remains the volume backbone of the connected motorcycle market.

Commercial fleets, however, are projected to expand at a 32.11% CAGR through 2031, reflecting a clear operational payback on telematics investment. Delivery platforms, ride-hailing operators, and rental agencies utilize live vehicle data to optimize routing, curb reckless driving, and demonstrate compliance with local transportation regulations. Predictive maintenance alerts help keep bikes on the road during peak demand periods, which is critical when profit margins depend on high utilization rates. Usage-based insurance discounts further strengthen the business case, since premiums align with actual mileage and driving style rather than fixed risk tables. This cost-benefit loop supports a rapid shift from pilot projects to fleet-wide deployments, expanding the connected motorcycle market size in the enterprise channel.

By Network Type: Cellular Dominates as Satellite-IoT Targets Coverage Gaps

Cellular technologies accounted for 59.31% of the market share in 2025 and are expected to grow at a 41.11% CAGR through 2031, driven by the widespread availability of 4G and 5G networks. These networks strike a balance between bandwidth, latency, and cost, enabling both infotainment streaming and real-time hazard alerts under a single subscription. OEMs benefit from mature supply chains that deliver pre-certified modules with embedded SIMs, shortening development cycles. Regulatory bodies are increasingly viewing cellular-based eCall services as a baseline safety requirement, thereby solidifying the technology’s role. Continuous infrastructure upgrades ensure that even suburban and secondary roads gain reliable coverage over the forecast period.

Dedicated short-range communications and satellite-IoT solutions fill performance or coverage gaps rather than compete head-on with cellular. DSRC and C-V2X links offer ultralow latency for vehicle-to-vehicle messaging along test corridors, paving the way for future integration into broader safety frameworks. Satellite-IoT modules offer a fallback option for riders exploring remote deserts, mountains, and forest trails where terrestrial towers are scarce. This non-terrestrial layer supports asynchronous services such as stolen-vehicle recovery and emergency location beacons. By combining cellular reach with spot-coverage enhancers, OEMs create resilient connectivity packages that broaden the connected motorcycle market share across diverse geographies and riding styles.

Geography Analysis

The Asia-Pacific region accounted for 41.73% of 2025 revenue and is projected to grow at 35.81% through 2031, giving the region the steepest slope on the connected motorcycle market growth curve. China’s mandate for V2X-ready smart roads accelerates adoption in every major city. Japan and South Korea favor tethered architectures because high smartphone penetration lowers incremental hardware cost. At the same time, Southeast Asian fleets deploy telematics across food-delivery and ride-hailing bikes to control operating expenses and raise safety. Together, these demand vectors strengthen supply-chain resilience and encourage component vendors to localize production lines, shortening lead times. Government initiatives that pair smart infrastructure funding with tax incentives further boost momentum.

North America follows with a forecasted CAGR of 24.92%, as state-level insurance discounts prompt riders to accept telemetry in exchange for lower premiums. Federal agencies have not yet mandated eCall; however, proposed safety rules continue to pressure OEMs to embed crash notification capability before regulations are finalized. Europe advances at 23.99% despite strict GDPR compliance burdens that elevate development costs. Germany, France, and the United Kingdom dominate regional spending due to their high per-capita incomes and established touring cultures. Eastern Europe lags as patchy cellular coverage limits the utility of telematics beyond urban zones.

South America, the Middle East and Africa grow from smaller bases yet show pockets of rapid uptake. Brazilian riders in congested cities value theft-recovery services, but exchange-rate fluctuations constrain upgrade cycles. Gulf states are investing in smart-city corridors that require V2X compliance for all new vehicles, thereby driving demand for premium connected models. Africa’s vast rural expanses favor hybrid cellular-satellite modules that ensure emergency connectivity where cellular towers are scarce. As terrestrial networks spread, suppliers position low-cost retrofit kits to tap the vast installed base of unconnected motorcycles.

Competitive Landscape

The connected motorcycle market remains moderately fragmented, with Robert Bosch GmbH, Continental AG, and BMW Motorrad accounting for most of the worldwide revenue. Bosch combines telematics, ABS, and radar into bundled offerings that increase per-bike content and lock in OEM relationships for multiple product cycles. Continental leverages passenger-car economies of scale to underwrite competitive pricing for motorcycle-grade telematics, while BMW integrates its proprietary Connected Ride software to deepen customer loyalty and drive data monetization.

A second tier of participants, including Panasonic, Autotalks, and several mid-size module makers, focuses on specialist capabilities such as ruggedized displays, dual-mode V2X chipsets, and low-power satellite transceivers. Their niche orientation allows premium pricing yet exposes them to volume swings as Tier 1 suppliers push integrated platforms. Connectivity service providers operate on a horizontal plane, offering cloud dashboards, eSIM provisioning, and roaming optimization that enable OEMs to outsource complex network operations. This model improves time-to-market while ensuring regulatory compliance across every jurisdiction.

Emerging disruptors use hybrid cellular-satellite architectures to address the last 10% of roads without reliable terrestrial signals. They partner with chipset vendors to embed non-terrestrial network logic directly into automotive SoCs, removing the need for separate satellite modems and antennas. Helmet communication specialists enter the fray with mesh-network products that extend short-range V2X coverage between riders on group tours, opening a fresh adjacency for data services. Patent filings centered on lean-angle-aware radar algorithms illustrate continued R&D focus on two-wheeler-specific safety, and the licensing value of these patents is likely to shape competitive advantage in coming years.

Connected Motorcycle Industry Leaders

-

Robert Bosch GmBH

-

Panasonic Corporation

-

Continental AG

-

BMW Motorad

-

Autotalks

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Honda joined the Zephyr Project, supporting the open-source RTOS initiative’s quest for IEC 61508 safety certification.

- January 2025: During CES 2025, Flying Flea unveiled its strategy to incorporate select Qualcomm Snapdragon products into its forthcoming motorcycle lineup. This integration will introduce features such as voice assistance, smartphone-enabled keys, and customizable ride modes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the connected motorcycle market as revenue generated from new two-wheelers, motorcycles, scooters, and mopeds fitted at the factory with embedded, integrated, or tethered control units that allow always-on data exchange for safety, infotainment, diagnostics, fleet, and over-air update services.

(Scope exclusion) We exclude retrofit telematics add-ons, standalone connected helmets, and aftermarket subscription revenues not sold with the vehicle at first registration.

Segmentation Overview

-

By Service

- Driver Assistance

- Infotainment

- Safety and Emergency Call

- Vehicle Management / OTA Updates

- Insurance and UBI

-

By Hardware Type

- Embedded Control Unit

- Tethered Smartphone-based

- Integrated Cockpit Cluster

-

By End User

- Private Consumers

- Commercial / Fleet

-

By Network Type

- Cellular (4G/5G)

- Dedicated Short-Range Comms (C-V2X/802.11p)

- Satellite-IoT and LPWAN

-

Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Egypt

- Turkey

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed connectivity architects at leading OEMs, tier-1 module suppliers, shared-mobility fleet managers, and regulators across Asia-Pacific, Europe, and the Americas. Their insights refined penetration assumptions, validated average selling prices, and clarified regulatory timing, ensuring the model mirrors on-ground adoption realities.

Desk Research

Mordor analysts began by mapping the global stock of mid- and premium two-wheelers using open sources such as IMMA production statistics, national transport ministries' registration ledgers, UN Comtrade HS-8711 trade flows, and telecom authority reports on 4G/5G roll-outs. We've layered these with peer-reviewed IEEE papers on V2X latency, insurer white papers on usage-based insurance, and D&B Hoovers filings to benchmark OEM output and pricing corridors. These examples illustrate the public datasets used; many other publications supported data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down construct converts country-level premium bike registrations into an addressable unit pool, applies expert-validated connectivity penetration curves, and then multiplies by blended hardware-plus-service price bands. Supplier roll-ups and channel checks act as a bottom-up sense check that adjusts totals when gaps emerge. Key drivers, smartphone adoption among riders, premium bike sales mix, 5G coverage expansion, eCall and UNECE R155 milestones, and service subscription take-rates feed a multivariate regression with scenario overlays for regulatory pace to project values through 2030. Anomalies are re-tested with experts before lock-in.

Data Validation & Update Cycle

Model outputs run through variance filters against independent metrics, including telecom SIM activations, customs declarations, and disclosed OEM connected-unit counts. Senior reviewers sign off after any discrepancies are resolved. Reports refresh each year, with mid-cycle updates released when material events alter market fundamentals.

Credibility Behind Mordor's Connected Motorcycle Baseline

Published estimates often diverge because every firm carves scope, price stacks, and forecast cut-off years differently.

Mordor's disciplined boundaries, annual refresh cadence, and dual-track validation give decision-makers a dependable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 96.31 million (2025) | Mordor Intelligence | N/A |

| USD 460 million (2025) | Global Consultancy A | Counts retrofit kits and bundled smartphone apps, applies uniform ASP across regions |

| USD 378 million (2024) | Industry Data Publisher B | Treats connected scooter batteries as separate revenue and uses static penetration assumptions |

In short, alternative totals swing widely when retrofit revenues, battery replacements, or flat penetration curves are folded in. Mordor's transparent variables, iterative expert reviews, and timely updates give clients a balanced, reproducible view they can trust.

Key Questions Answered in the Report

What is the current size of the connected motorcycle market?

The connected motorcycle market size stands at USD 0.57 billion in 2026 and is projected to reach USD 2.28 billion by 2031.

Which region leads connected motorcycle adoption?

Asia-Pacific commanded 41.73% revenue in 2025 and is forecast to grow at a 35.81% CAGR through 2031, the fastest worldwide.

Which service category is growing fastest?

Driver assistance services will expand at 44.21% CAGR between 2026 and 2031 as collision-avoidance functions move into mainstream models.

How are commercial fleets using motorcycle telematics?

Fleet operators deploy GPS tracking and behavior analytics to cut fuel use, lower insurance premiums, and reduce unplanned maintenance.

Page last updated on: