SUV Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 0.95 Trillion |

| Market Size (2031) | USD 1.29 Trillion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SUV Market Analysis by Mordor Intelligence

The SUV market size was valued at USD 0.89 trillion in 2025 and is estimated at USD 0.95 trillion in 2026, forecast to reach USD 1.29 trillion by 2031, at a CAGR of 6.65% over 2026-2031. As consumers increasingly favor higher-riding models for their perceived safety and flexible cargo space, the demand for sedans continues to wane. To finance their electrification initiatives, automakers are prioritizing premium, high-margin full-size nameplates, even as compact models anchor the global SUV market. While falling battery prices and stringent emissions regulations in Europe, China, and India are hastening the shift to electric SUVs, internal combustion engine (ICE) vehicles still reign in areas with low fuel taxes and inconsistent charging networks. The competitive landscape is becoming more challenging, with Chinese new energy vehicle (NEV) specialists rapidly scaling up, compelling established OEMs to modernize their manufacturing and software systems to maintain their pricing power.

Key Report Takeaways

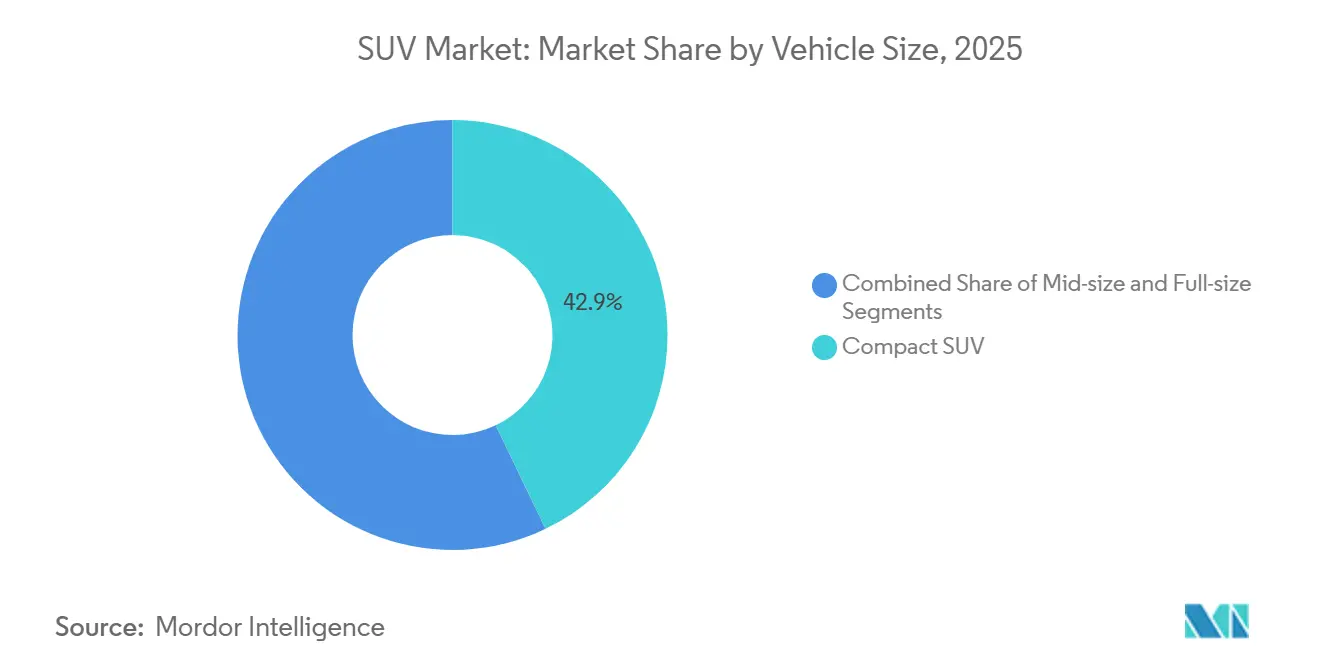

- By vehicle size, compact SUVs accounted for 42.88% of the 2025 SUV market revenue, while full-size platforms are projected to expand at an 11.39% CAGR through 2031.

- By fuel type, petrol models retained 59.36% of 2025 revenue share, yet electric SUVs are forecast to surge at a 20.56% CAGR over 2026-2031.

- By drivetrain, two-wheel-drive configurations captured 47.08% of 2025 sales, whereas AWD variants are advancing at a 9.79% CAGR to 2031.

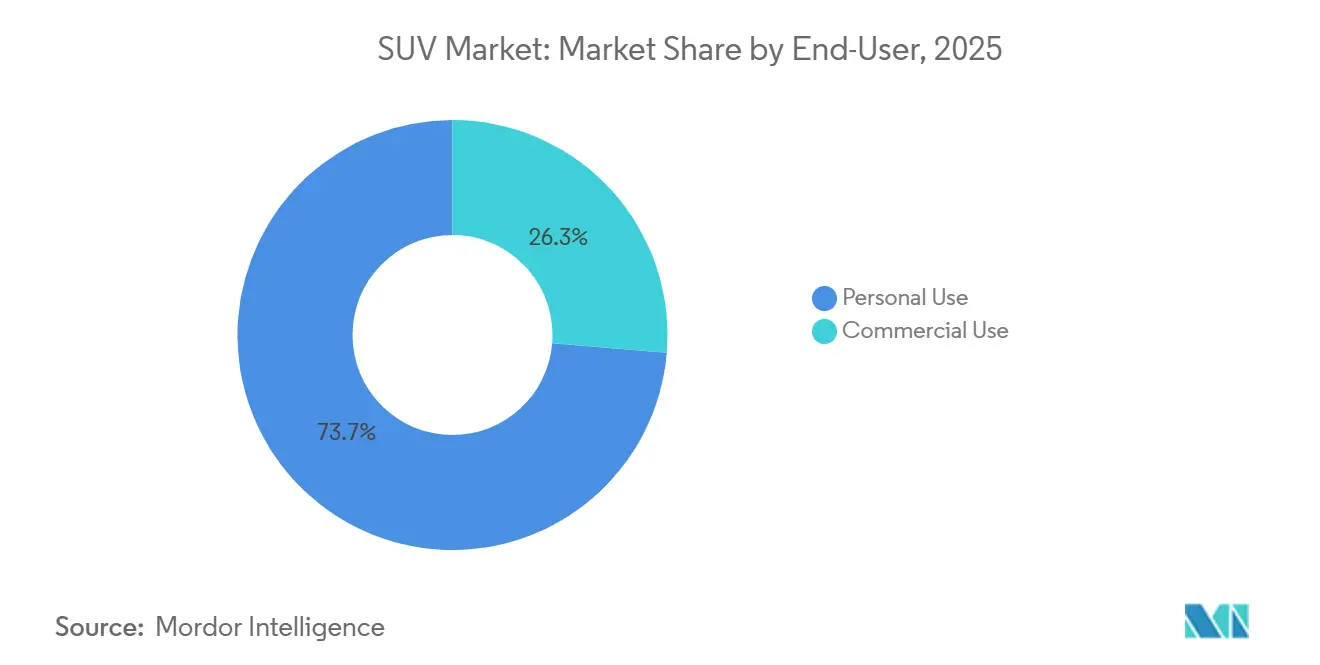

- By end-user, personal buyers accounted for 73.69% of 2025 demand, while commercial fleets are growing fastest at a 7.89% CAGR through 2031.

- By seating capacity, five-seater layouts held 62.43% of 2025 volume, yet seven-seater models are set to expand at a 6.79% CAGR during the forecast period.

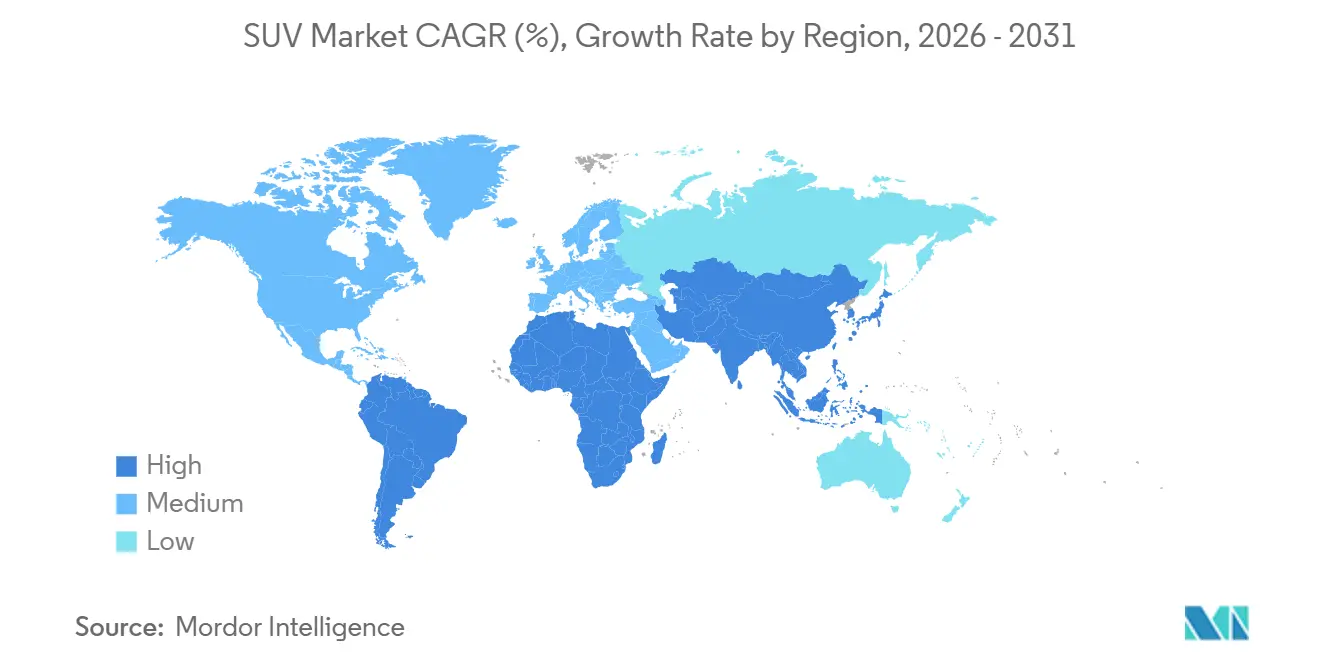

- By geography, Asia-Pacific led with 38.89% of global SUV revenue in 2025 and is forecast to rise at an 8.19% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SUV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Margin SUV Platforms | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Shift Toward Larger Vehicles | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Compact and Sub-Compact SUVs | +1.4% | Global urban centers, led by Asia-Pacific | Short term (≤ 2 years) |

| AWD/Off-Road Demand | +0.9% | North America and the EU, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Premium SUV Uptake | +0.3% | Europe and North America urban markets | Short term (≤ 2 years) |

| Fuel-Cell SUV Pipeline | +0.1% | Japan, Germany, select markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Focus on High-Margin SUV Platforms to Fund Electrification

Ford, GM, and Stellantis are reaping the rewards of SUV platforms, enjoying EBIT margins that outpace those of similar sedan programs. This financial edge allows them to invest heavily in battery plants, software innovations, and versatile vehicle designs [1]“Ford Accelerates EV Transition With Universal Electric Vehicle Platform,”, Ford Motor Company, ford.com. By directing funds toward large SUVs, these automakers not only champion the transition to zero-emission powertrains but also shield their cash flow from the volatility of EV demand. Furthermore, the lucrative margins from SUVs serve as a vital cushion, helping these companies navigate the hefty initial costs of electrification. This includes investments in cutting-edge battery research and the development of comprehensive EV supply chains. Their SUV-centric strategy strikes a harmonious balance between addressing today's market needs and pursuing future sustainability objectives.

Proliferation of Compact and Sub-Compact SUVs in Urban Areas

Across Asia-Pacific, Europe, and Latin America, the compact-SUV sub-segment is emerging as the entry point to SUV ownership. In urban areas with limited parking and congestion charges, there's a preference for shorter wheelbases. However, consumers still desire the elevated seating and adaptable cargo space that SUVs offer. This trend solidifies the compact SUV's role as the primary catalyst for the SUV market's overall growth. Additionally, the compact-SUV sub-segment appeals to a wide range of demographics, including young professionals, small families, and retirees, due to its balance of affordability, practicality, and style. Automakers are increasingly focusing on this sub-segment by introducing new models with advanced features, fuel efficiency, and competitive pricing, further driving its popularity and market expansion.

Demand for AWD/Off-Road Capability in Lifestyle Vehicles

Premium trims, featuring electronic AWD, skid plates, and rugged styling, are capitalizing on the allure of adventure branding. These trims not only cater to off-road enthusiasts but also appeal to urban buyers who view AWD as a safety boost in wet or snowy conditions. This dual appeal is driving sustained price premiums and elevating average revenue per unit in the SUV market. Additionally, the integration of advanced features in premium trims enhances the overall value proposition, making them a preferred choice for consumers seeking both functionality and style. The growing demand for such trims reflects a broader trend in the SUV market, where manufacturers are leveraging innovation and design to meet diverse consumer needs.

Hydrogen Fuel-Cell SUV Pipeline for Long-Range Use Cases

Japanese and Korean OEMs are turning to fuel-cell SUVs as a strategic buffer against the volatility of battery-material prices. These vehicles offer significant advantages, including rapid refueling and a longer driving range, making them an attractive alternative to battery-electric vehicles. Early deployments in Germany, California, and Seoul underscore their potential in addressing the limitations of current electric vehicle technology. However, high costs associated with tanks and stacks limit these vehicles to pilot programs for now, as manufacturers continue to explore cost-reduction strategies and scalability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CAFE / CO₂ Rules | -1.8% | North America & EU regulatory zones | Medium term (2-4 years) |

| Chip Supply Constraints | -1.2% | Global, acute in EU & North America | Short term (≤ 2 years) |

| Access Fees and Congestion Bans | -0.7% | EU urban centers, expanding globally | Short term (≤ 2 years) |

| Higher Insurance/TCO | -0.4% | Developed markets primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening CAFE / CO₂ Rules Targeting SUVs

Regulators across three continents have tightened loopholes, previously exploited by heavier SUVs to meet lenient fuel-economy standards. These regulatory changes aim to address environmental concerns and promote sustainable practices in the automotive industry. With the introduction of new emission curves, compliance costs have surged, pushing automakers to hasten the rollout of hybrids and BEVs. Simultaneously, they're reducing weight by incorporating aluminum closures and unicast chassis components, which not only improve fuel efficiency but also align with evolving regulatory requirements [2]“Final CAFE Standards 2027-2031,”, National Highway Traffic Safety Administration, nhtsa.dot.gov.

Battery-Material and Chip Supply Constraints for e-SUVs

Despite robust order books, electric-SUV penetration faces potential caps due to upstream fragility, underscored by production halts at several OEMs in 2025. This fragility stems from the ongoing structural shortages of critical materials such as lithium, nickel, and premium microcontrollers, which are essential for electric vehicle production. While strategies like dual-chemistry batteries and domestic chip plants offer medium-term solutions to address these challenges, they won't provide immediate respite. The industry continues to navigate these supply chain constraints, which could influence production timelines and market dynamics in the near term [3]“Global EV Regulatory Landscape 2026,”, International Council on Clean Transportation, theicct.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Size: Compact Strength, Premium Surge

Compact SUVs accounted for 42.88% of 2025 revenue share, while full-size platforms are projected to expand at an 11.39% CAGR through 2031. Driven by urbanization and favorable tax brackets, while mid-size offerings bridge versatility and operating cost. Continuous wheelbase stretching on modular platforms blurs traditional size demarcations, allowing OEMs to pivot output without new tooling.

Compact leaders like Toyota’s Corolla Cross continue to dominate Southeast Asian streets, whereas North America anchors profitability with Chevrolet Tahoe, GMC Yukon, and Ford Expedition. The SUV industry monetizes full-size demand through premium interiors and advanced driver-assistance technology, using these surpluses to bankroll electrification of entry-level lines.

By Fuel Type: Combustion Relevance, Electric Lift-Off

Electric SUVs are forecast to clock a 20.56% CAGR, yet started from a modest base in 2025, when petrol retained 59.36% of global registrations. In Europe, diesel traction is on the decline. However, in markets with limited charging infrastructure, hybrid systems are providing a buffer against this transition. Original Equipment Manufacturers (OEMs) are now standardizing skateboard platforms to accommodate both Internal Combustion Engine (ICE) and Battery Electric Vehicle (BEV) drivetrains. This strategy not only safeguards their previous investments but also ensures compliance with tightening CO₂ regulations.

As battery prices are expected to decrease, electric SUVs could soon match the prices of their gasoline counterparts in both China and the EU. While plug-in hybrids will continue to serve as a transitional technology due to regulatory mandates, Europe's tightening utility-factor regulations are set to reduce their compliance credits in the future.

By Drivetrain: Efficiency Versus Capability

Two-wheel-drive configurations captured 47.08% of 2025 sales, whereas AWD variants are advancing at a 9.79% CAGR to 2031. Dual-motor BEV layouts simplify power delivery to both axles, often at lower mechanical complexity than transfer-case-based 4WD. This trend lifts the SUV market because AWD variants deliver USD 2,000-4,000 extra gross profit per unit for the same body shell.

Two-wheel-drive still dominates emerging markets that prioritize price and fuel economy. Nevertheless, manufacturers bundle electronic stability aids and traction-mode selectors to close the perceived capability gap and defend pricing tiers.

By End-User: Personal Dominance, Fleet Upswing

Personal-use buyers accounted for 73.69% of the SUV market share in 2025. Fleet operators—from ride-hailing groups to corporate shuttle services—value the high utilization and residuals of SUVs, propelling the end-user sub-segment at a 7.89% CAGR. Lower 5-year total cost of ownership for BEV SUVs versus comparable sedans, especially in regions with generous electricity subsidies, is catalyzing bulk orders among logistics and mobility-as-a-service firms.

Personal buyers, who still represent roughly three-quarters of demand, continue to choose SUVs for elevated seating and cargo flexibility. Insurance data indicate parity in accident outcomes with modern sedans, yet perceptions of safety persist, reinforcing the SUV market narrative.

By Seating Capacity: Five-Seat Pragmatism, Seven-Seat Growth

Five-seat layouts held 62.43% of the SUV market share in 2025. This configuration strikes an ideal balance, balancing passenger capacity and cargo flexibility to meet the transportation needs of families and individuals alike. By maximizing cargo space behind the second row and keeping exterior dimensions and fuel economy in check, these layouts prove especially advantageous in urban settings, where parking and maneuverability are paramount. The dominance of the five-seater configuration underscores a clear consumer preference: vehicles that can occasionally accommodate passengers without sacrificing daily functionality or driving dynamics.

Seven-seaters, on a 6.79% CAGR trajectory, address multigenerational travel and shared-mobility shuttles. Sliding second rows and panoramic roofs improve third-row livability, while power-assisted entry reduces loading strain for older passengers. OEMs market these variants as do-everything solutions, capturing upgrade spending and widening SUV market size contributions in suburban corridors. Apparently, 7-seater models command premium pricing through enhanced utility and family-focused positioning.

Geography Analysis

Asia-Pacific captured 38.89% of the SUV market revenue in 2025 and is projected to expand at an 8.19% CAGR as Chinese NEVs reach ~50% penetration of new passenger vehicle sales by 2025 and Indian SUVs account for a major portion of passenger-vehicle sales. In China's lower-tier cities, first-time buyers are gravitating towards compact electric SUVs priced under USD 25,000. Meanwhile, Australia and Thailand show a strong appetite for ladder-frame off-roaders, which are often used as work vehicles.

North America is the profit powerhouse of the global SUV market. In a significant move, General Motors is increasing transmission production at its Toledo, Ohio, facility, transitioning from EV drive unit manufacturing to components for gasoline vehicles. While the uptake of electric vehicles (EVs) has been slower than anticipated, prompting original equipment manufacturers (OEMs) to extend the life of internal combustion engine (ICE) full-size programs, federal revisions to the Corporate Average Fuel Economy (CAFE) standards are pushing these manufacturers to invest concurrently in battery plants.

Europe is expected to record the highest SUV share of total new-vehicle registrations globally, with SUVs accounting for roughly ~60% of new-car sales. However, the continent grapples with challenges: stringent CO₂ regulations and urban congestion fees are tightening margins on heavier SUV models. While the European Commission's recent allowance of limited e-fuel credits offers a temporary shield for high-performance SUVs, it simultaneously accelerates the industry's shift towards compact electric crossovers produced within the EU. Meanwhile, emerging markets in South America and the Middle East bolster global demand, with consistent growth in mid-size SUVs driven by rising infrastructure investments and rising incomes.

Mordor Intelligence provides coverage of the suv market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

In the global SUV arena, a handful of players dominate. The top automakers, led by Toyota and closely followed by Volkswagen Group and Hyundai Motor, are poised to command a significant share of the market. Meanwhile, Chinese automaker BYD is making waves by leveraging vertical integration to slash battery costs and challenge established pricing norms.

As technology and scale increasingly intertwine, Ford is making bold moves. Its Universal Electric Vehicle architecture, harnessing giga-castings and a zonal electrical backbone, aims for ambitious margin targets. Stellantis, not to be outdone, is pouring significant investments into reviving U.S. plants, focusing on large SUVs that will share components with its innovative STLA-Frame EV truck platform. Tesla, while setting the standard for OTA software updates, finds legacy OEMs rapidly catching up through dedicated software hubs and key partnerships.

Emerging niches are evident: fuel-cell SUVs for long-range commercial fleets and rugged compact models for budget-conscious adventurers in developing markets. With numerous new electric SUVs set to debut, many under an enticing price point, the competitive landscape is primed for heightened intensity.

SUV Industry Leaders

Toyota Motor Corporation

Volkswagen AG

Hyundai Motor Group

Renault–Nissan–Mitsubishi Alliance

General Motors Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Maruti Suzuki has unveiled the Victoris compact SUV, marking it as the flagship of its Arena network. The Victoris is expected to strengthen Maruti Suzuki's position in the compact SUV market, catering to the growing demand for SUVs in India. This launch highlights the company's focus on expanding its product portfolio and enhancing its presence in the competitive automotive market.

- July 2025: Li Auto unveiled a fully electric six-seat SUV, specifically designed to cater to the needs of affluent families in mainland China. The vehicle aims to combine luxury, space, and sustainability, aligning with the growing demand for premium electric vehicles in the region.

Global SUV Market Report Scope

The SUV market report is segmented by vehicle size (compact, mid-size, and full-size), fuel type (petrol, diesel, hybrid, and electric), drivetrain (2WD, 4WD, and AWD), end-user (personal use and commercial use), seating capacity (5-seater and 7-seater), and geography (North America, South America, Europe, Asia-Pacific and Middle East and Africa). The market forecasts are provided in terms of value (USD) and Volume (Units).

| Compact |

| Mid-size |

| Full-size |

| Petrol |

| Diesel |

| Hybrid |

| Electric |

| 2WD |

| 4WD |

| AWD |

| Personal Use |

| Commercial Use |

| 5-Seater |

| 7-Seater |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Size | Compact | |

| Mid-size | ||

| Full-size | ||

| By Fuel Type | Petrol | |

| Diesel | ||

| Hybrid | ||

| Electric | ||

| By Drivetrain | 2WD | |

| 4WD | ||

| AWD | ||

| By End-User | Personal Use | |

| Commercial Use | ||

| By Seating Capacity | 5-Seater | |

| 7-Seater | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global SUV market in 2026?

The SUV market size stands at USD 0.95 trillion in 2026 and is projected to reach USD 1.29 trillion by 2031.

Which SUV segment is growing fastest?

Full-size SUVs are expanding at an 11.39% CAGR during 2026-2031 as automakers monetize higher margins to fund electrification.

What are key regulatory challenges facing SUVs?

Stricter CAFE standards in the U.S. and tighter CO₂ limits in the EU and India increase compliance costs and accelerate electrification.

How quickly are electric SUVs capturing share from combustion versions?

Battery-electric SUVs are expanding at a 20.56% CAGR through 2031, the fastest of all fuel types as infrastructure scales up.

Which seating configuration dominates global SUV demand?

Five-seat layouts command 62.43% of shipments, balancing everyday practicality with manageable exterior dimensions.

Page last updated on: