Electric Motorcycle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

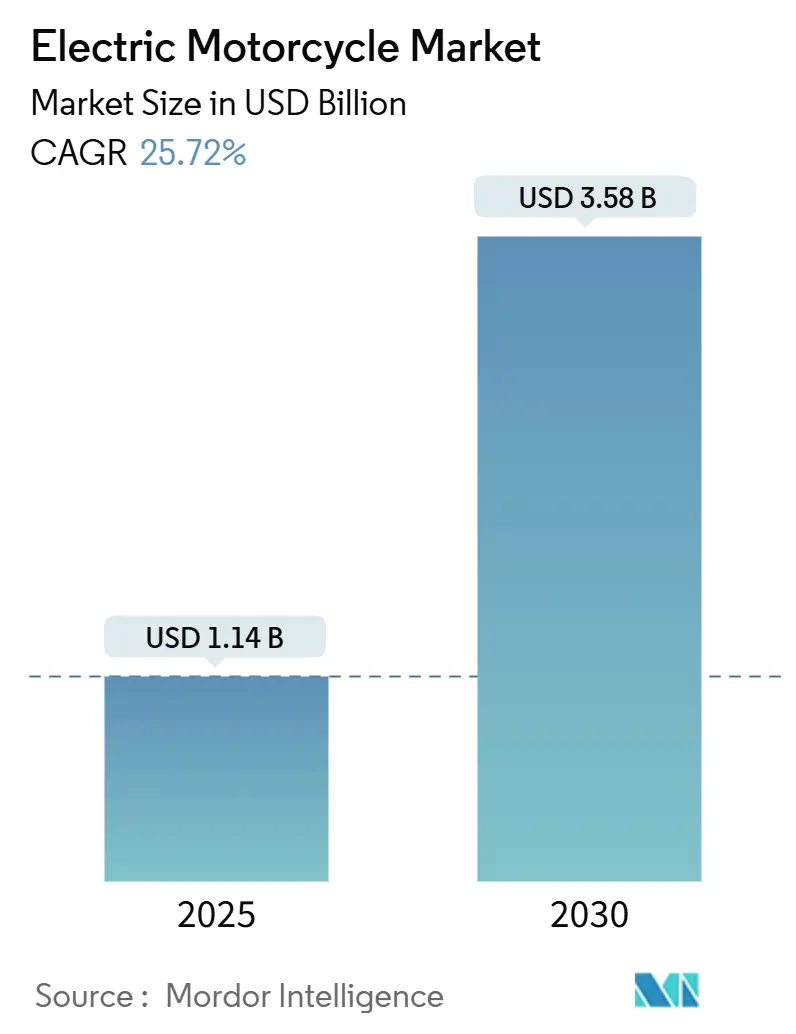

| Market Size (2025) | USD 1.14 Billion |

| Market Size (2030) | USD 3.58 Billion |

| Growth Rate (2025 - 2030) | 25.72% CAGR |

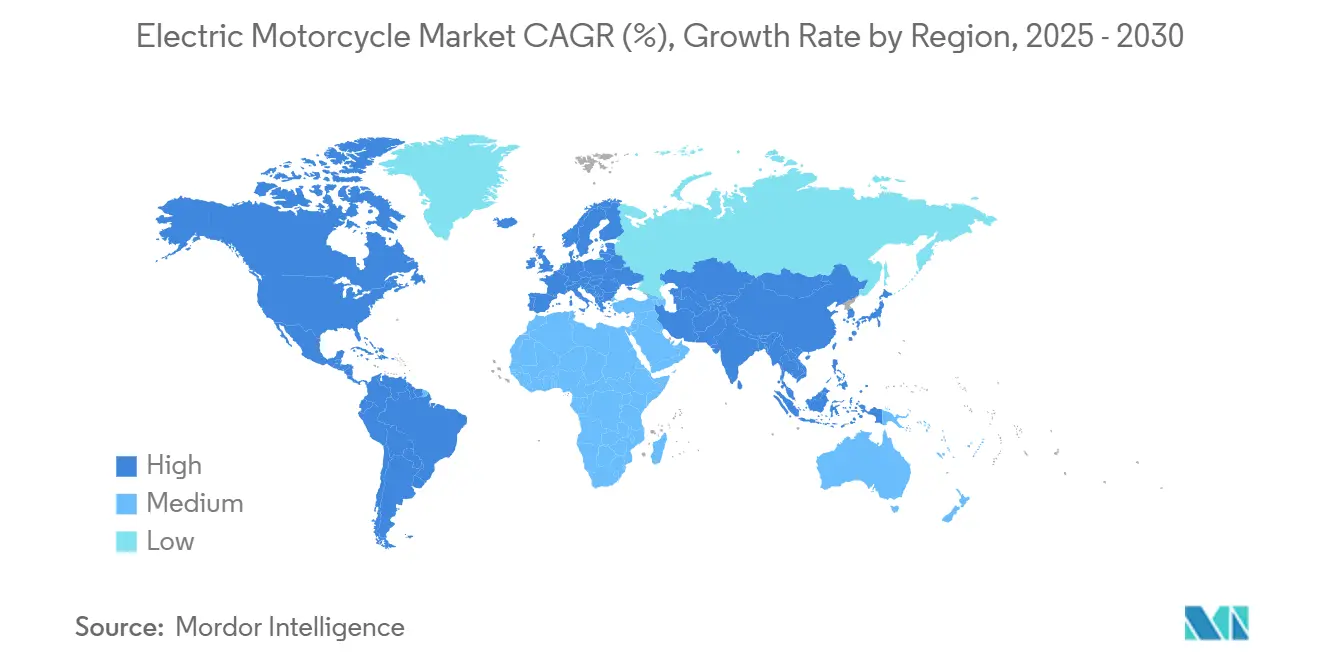

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

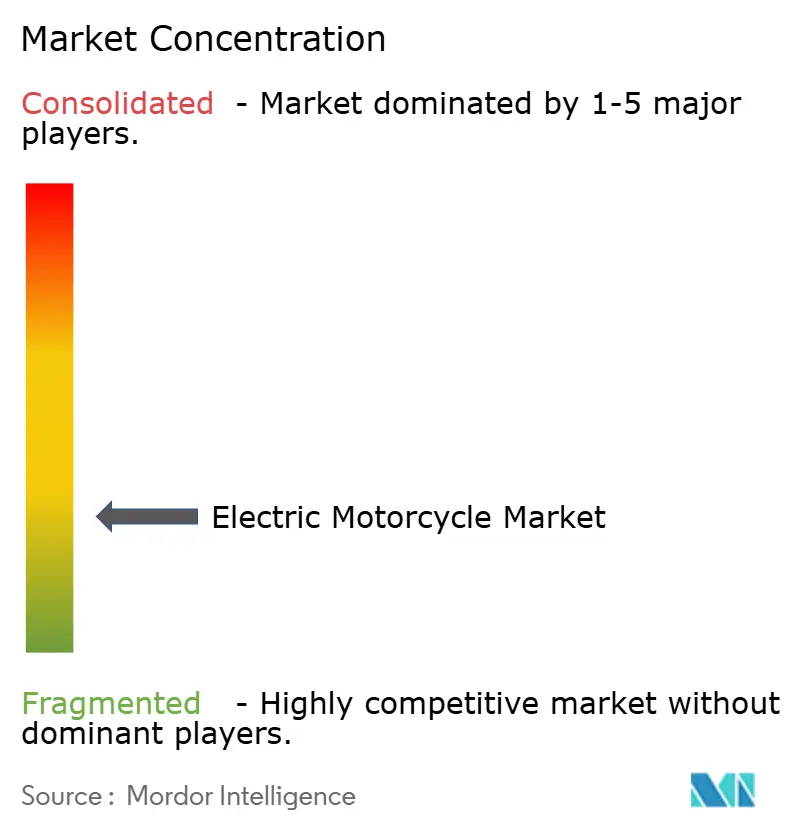

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Motorcycle Market Analysis by Mordor Intelligence

The electric motorcycle market size is USD 1.14 billion in 2025 and is forecast to reach USD 3.58 billion in 2030, expanding at a 25.72% CAGR during the forecast period. Falling lithium-ion battery prices in 2024 have pushed the total cost of ownership below that of comparable ICE models in many use cases. Scaling battery production, growing charging networks, and zero-emission mandates reinforce demand and shorten payback periods. Asia-Pacific’s entrenched manufacturing base secures cost advantages that encourage exports to price-sensitive regions, while policy incentives in South America, North America, and Europe broaden demand beyond early adopters. Technology migration toward sodium-ion and solid-state chemistries promises lower material costs, higher energy density, and improved safety, positioning the market for mainstream, long-range applications. Competitive intensity remains moderate as scale leaders defend share and new entrants address delivery fleets and premium performance niches.

Key Report Takeaways

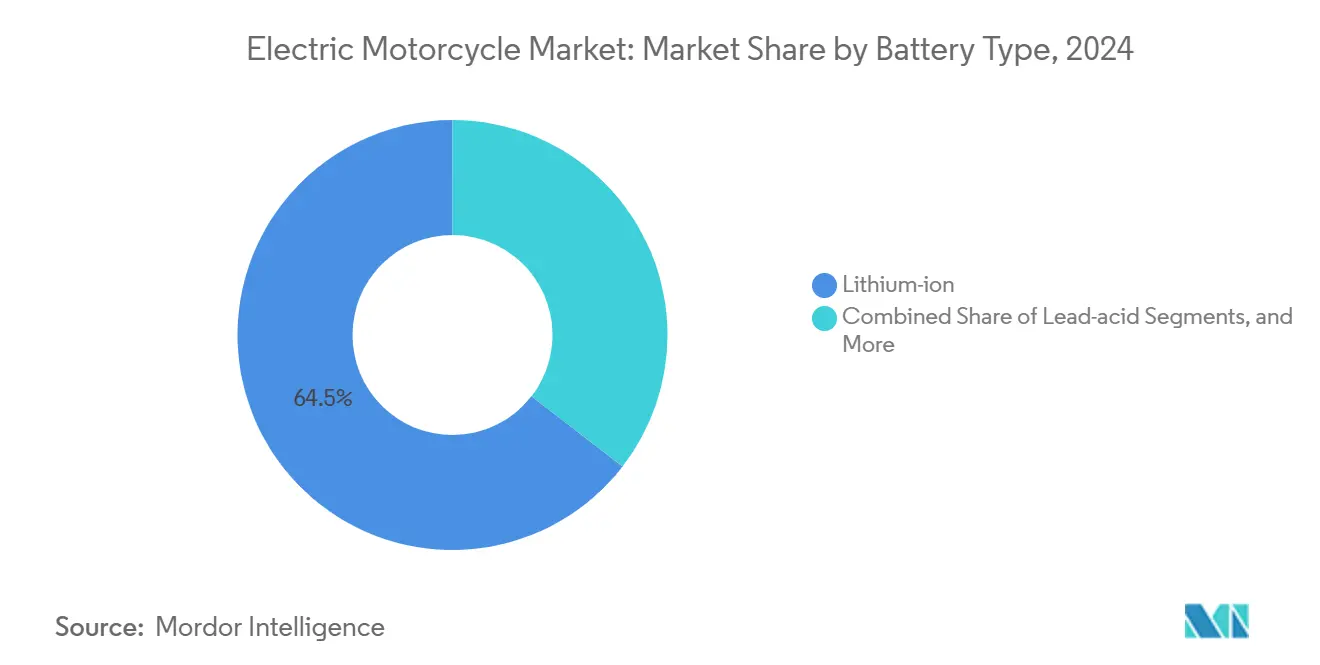

- By battery type, lithium-ion captured 64.52% of the electric motorcycle market share in 2024; sodium-ion systems are projected to compound at a 26.28% CAGR to 2030.

- By power output, the sub-3.6 kW class accounted for 44.21% of the electric motorcycle market share in 2024, while models above 10 kW are advancing at a 27.71% CAGR through 2030.

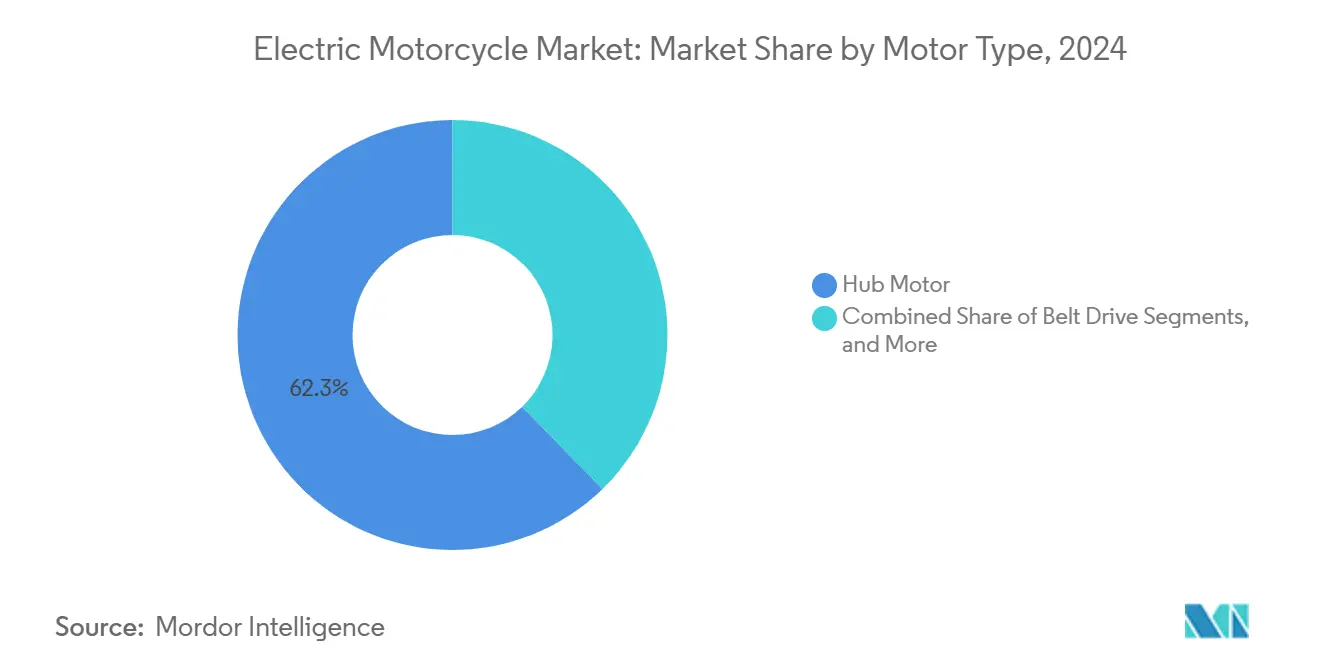

- By motor type, hub motors held 62.29% of the electric motorcycle market share in 2024; mid-drive units record the highest forecast CAGR at 27.81% to 2030.

- By end-use, personal ownership represented 78.31% of the electric motorcycle market share in 2024, whereas delivery and logistics applications are growing at a 28.64% CAGR through 2030.

- By region, Asia-Pacific commanded 73.28% of the electric motorcycle market share in 2024, and South America is expanding fastest at a 26.43% CAGR to 2030.

Global Electric Motorcycle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Li-Ion Cost Drop and Energy Density Gains | +4.2% | Global, with strongest impact in Asia-Pacific and Europe | Medium term (2-4 years) |

| Govt Incentives and Zero-Emission Mandates | +3.8% | North America and EU core, expanding to Asia-Pacific markets | Short term (≤ 2 years) |

| 2W Charging and Swap Network Expansion | +3.1% | Asia-Pacific core, spill-over to South America and MEA | Medium term (2-4 years) |

| Breakthrough Sodium-Ion and Solid-State Chemistries | +2.9% | Global, with early commercialization in China and India | Long term (≥ 4 years) |

| Micromobility Fleets Lower TCO, Drive Adoption | +2.7% | Urban centers globally, concentrated in North America and Europe | Short term (≤ 2 years) |

| OTA Connectivity and In-Vehicle Data Monetization | +1.8% | Developed markets first, expanding to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling Lithium-Ion Battery Costs and Rising Energy Density

As lithium-ion battery costs plummet, electric motorcycles are becoming increasingly affordable, challenging traditional fuel-powered models worldwide. This trend narrows the economic divide between electric vehicles and their internal combustion engine (ICE) counterparts.

Advancements in battery technology have produced lighter vehicles with extended ranges. Manufacturers now provide warranties on par with those of traditional motorcycles. Such innovations have emboldened companies, especially from China, to penetrate global markets like Southeast Asia and Latin America, introducing electric models at prices within reach of a broader audience.

Government Purchase Incentives and Zero-Emission Mandates

Purchase subsidies in Indonesia of up to IDR 7 million (USD 467) and Germany’s EUR 2,500 bonus push electric two-wheelers into mainstream price bands[1]“Program Kendaraan Bermotor Listrik,” Indonesian Ministry of Industry, kemenperin.go.id. California’s Advanced Clean Cars II rule compels dealers to meet zero-emission sales quotas that include motorcycles, guaranteeing baseline demand for several years. Similar frameworks are under review in India and Brazil for roll-out by 2027, accelerating local assembly programs and building-volume economies.

Expansion of Two-Wheeler Charging and Swap Networks

Gogoro’s 12,000-station battery-swap grid across Taiwan, India, and China shows that standardized packs can scale profitably in dense corridors[2]Gogoro, “Gogoro Network Expansion Update,” Gogoro, gogoro.com. Partnership models with OEMs bring interoperability, which eases fleet procurement decisions and reduces stranded-asset risk for infrastructure investors. Government backing in Taiwan and India further compresses deployment timelines and drives urban adoption curves upward.

Breakthrough Sodium-Ion / Solid-State Chemistries

Yadea’s 2024 commercial sodium-ion launch cut battery material outlays by 20–30%, allowing MSRP reductions without sacrificing urban range[3]Yadea, “Yadea Launches Sodium-Ion Motorcycle,” Yadea, yadea.com. Solid-state prototypes from QuantumScape and Toyota target 400 Wh/kg energy density by 2028, enabling highway speeds and longer tours with shorter charge stops. Thermally stable chemistries also reduce cooling system complexity, lowering maintenance for fleet operators in tropical climates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost vs. ICE Motorcycles | -2.8% | Global, with strongest impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Limited Range and Slow Charging Above 7kW | -2.1% | Global, particularly affecting highway and long-distance applications | Medium term (2-4 years) |

| Thermal Safety Challenges in Tropical Fleets | -1.6% | Tropical regions including Southeast Asia, India, and parts of South America | Medium term (2-4 years) |

| Weak Battery End-of-Life Collection in Emerging Markets | -1.3% | Emerging markets in Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Thermal-Safety Concerns in Tropical Fleet Duty Cycles

High ambient temperatures accelerate cell degradation and heighten the risk of thermal runaway during rapid charging. This challenge is especially pronounced in regions with persistently elevated temperatures, affecting battery performance and longevity. In Jakarta and Manila, fleet managers impose daytime charging breaks to cool battery packs, resulting in diminished productivity and operational inefficiencies. These interruptions throw off fleet schedules and inflate overall operational costs. Yet, a wider embrace of advanced battery technologies, like sodium-ion and solid-state chemistries, is projected to mitigate these issues post-2027. These novel chemistries promise better thermal stability and heightened safety, ideal for hotter climates.

Weak End-of-Life Battery Collection in Emerging Markets

In Southeast Asia and certain regions of Africa, the scarcity of formal collection channels has resulted in a reliance on informal recycling methods. These methods not only fail to capture the material's value but also present significant environmental risks. Meanwhile, ongoing discussions surrounding EPR (Extended Producer Responsibility) rules are causing delays in investments. Such investments are crucial for establishing reverse logistics networks, which play a pivotal role in realizing the cost-saving benefits of a circular economy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Sodium-Ion Disrupts Lithium Dominance

Lithium-ion held a 64.52% share of the electric motorcycle market in 2024, leveraging mature supply chains and proven performance. Sodium-ion platforms, led by Yadea’s 2024 release, are growing at 26.28% CAGR as OEMs seek cost relief from lithium volatility and cobalt exposure. This pivot is evident in China and India, where domestic salt reserves provide raw material security. Lithium-ion polymer variants stay relevant in premium sport and touring machines that prioritize weight reduction and compact packaging. Regulators increasingly reward chemistries with lower environmental footprints, accelerating sodium adoption in cost-sensitive commuter models.

Although limited to shorter urban ranges due to lower energy density, sodium-ion batteries offer cost advantages and safer thermal characteristics, making them appealing to fleet operators. While still serving the ultra-budget segment, lead-acid batteries are losing relevance as charging infrastructure becomes more accessible. Solid-state battery technology is progressing toward pilot-scale production. Once commercialized, these batteries are expected to power premium electric vehicles with higher energy capacity, potentially shifting lithium-ion batteries to mainstream applications.

By Power Output: High-Performance Applications Drive Growth

Sub-3.6 kW motorcycles led with a 44.21% share of the electric motorcycle market in 2024, favored for dense-city commutes and regulatory exemptions. The over-10 kW class is forecast to rise 27.71% CAGR through 2030, propelled by highway-capable launches from Zero Motorcycles and LiveWire. Customers seeking weekend touring and daily inter-city rides gravitate toward these models as charging corridors mature. Mid-power bands (3.6–10 kW) serve mixed-use riders yet face segmentation pressure as low-power urban specialists and high-power tourers diverge.

Growth at the top end demands liquid cooling, advanced BMS, and higher voltage architecture, lifting ASPs and margins. Financing products now bundle battery warranties to calm buyer concerns over residual values. Successful scale hinges on public fast chargers and renewable portfolio standards guaranteeing green electricity for long-range travelers.

By Motor Type: Mid-Drive Gains Performance Edge

Hub motors captured a 62.29% share of the electric motorcycle market in 2024, owing to cost-effective integration and reduced mechanical parts. Mid-drive systems expand 27.81% CAGR because they centralize mass and permit gear reductions that improve hill-climb torque. Honda’s EV-Fun concept showcases low-cost hub solutions for emerging markets, whereas Zero’s FXE mid-drive underscores performance credentials. Belt and chain drives survive in specialty off-road models requiring precise torque delivery or ease of sprocket changes.

Hub motors dominate entry scooters and swap-battery fleets because sealed designs limit water ingress and lower maintenance. Yet as riders graduate to heavier loads and faster routes, OEMs adopt mid-drive to meet handling expectations.

By End-Use: Commercial Applications Accelerate Adoption

Personal use accounted for 78.31% of the electric motorcycle market in 2024, reflecting entrenched two-wheeler cultures in the Asia-Pacific. Delivery and logistics are the fastest risers at 28.64% CAGR through 2030, strengthened by e-commerce surges and environmental regulations on last-mile fleets. Australia Post’s plan illustrates how institutional buyers aggregate demand that de-risks factory capacity investments. Micromobility platforms secure bulk discounts and influence battery-swap network roll-outs by clustering usage.

Lower operating costs, route predictability, and depot charging balance the higher purchase price for fleet managers. As on-board telematics mature, fleet owners are expected to monetize data services such as predictive parts ordering, further justifying electric conversion. The demonstration effect on couriers and ride-hail riders feeds into personal uptake, reinforcing market flywheels.

Geography Analysis

Asia-Pacific controlled 73.28% share of the electric motorcycle market in 2024. China supplies most global lithium-ion packs and commands scale benefits that ripple across export markets. India’s production-linked incentive program has drawn brands such as Ather and TVS into capacity expansions. At the same time, Indonesia’s IDR 7 million subsidy pushes local assemblers to switch from semi-knockdown to full localization. Dense urban corridors and long traditions of two-wheeler commuting make the region a natural locus for electric adoption.

South America grows fastest at 26.43% CAGR during the forecast period, led by Brazil’s surging e-commerce sector and municipal zero-emission delivery zones in São Paulo and Bogotá. Argentina’s volatile fuel prices boost the arithmetic for lower operating cost electrical fleets, and regional battery-swap pilots in Santiago garner positive regulator feedback. Supply constraints still exist, yet partnerships with Chinese OEMs promise local CKD assembly that slashes import tariffs.

North America and Europe prioritize performance and lifestyle positioning over raw affordability. LiveWire, Zero Motorcycles, and CAKE compete on range, acceleration, and connected features, while EU safety standards such as UN ECE R136 create compliance thresholds that favor established engineering houses. Middle East and Africa remain nascent, but renewable energy build-outs and high solar insolation hint at future on-site charging opportunities once ASPs fall. Across all regions, early-stage policy alignment on battery recycling will shape long-term competitiveness and cluster manufacturing footprints.

Competitive Landscape

Market concentration is moderate. Yadea, NIU, and Zero combine vertical battery supply, multi-brand portfolios, and global dealer networks to protect share. Honda, Yamaha, and TVS integrate electric lines into legacy distribution, leveraging after-sales infrastructure. Hero MotoCorp’s tie-up with Gogoro grants immediate access to swap-battery tech, avoiding heavy R&D outlays. BMW and TVS co-engineer premium variants that enter showrooms faster than ground-up development would allow.

New entrants exploit white spaces. Ultraviolette emphasizes AI-powered telemetry to cut fleet downtime. LAND Moto targets North American buyers seeking artisanal design married to urban range convenience.

Strategic moves concentrate on platform sharing and software-defined differentiation. OTA updates extend vehicle life cycles, and data-as-a-service models promise annuity revenue that lifts lifetime margin per unit. Compliance with UN ECE standards has become a gating factor, slowing smaller startups and conferring a regulatory moat to incumbents. Over the next three years, cross-industry alliances with battery and semiconductor firms are expected to decide the pace of cost reductions and performance leaps.

Electric Motorcycle Industry Leaders

NIU Technologies

Yadea Group Holdings Ltd.

LiveWire EV, LLC

Vmoto Limited

Zero Motorcycles Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Oben Electric, an Indian manufacturer of electric motorcycles, introduced the Rorr EZ Sigma in the Indian market. The Rorr EZ Sigma comes with battery choices of 3.4 kWh and 4.4 kWh, providing a maximum range of 175 kilometers on a single charge.

- September 2025: Honda introduced its first electric motorcycle, the "Honda WN7," in Europe. Featuring a lithium-ion battery, the Honda WN7 offers an estimated range of over 130 km.

Global Electric Motorcycle Market Report Scope

| Lead-acid |

| Lithium-ion |

| Lithium-ion Polymer |

| Sodium-ion & Emerging Chemistries |

| Below 3.6 kW |

| 3.6 - 7.2 kW |

| 7.2 - 10 kW |

| Above 10 kW |

| Hub Motor |

| Belt Drive |

| Chain Drive |

| Mid-drive Motor |

| Personal / Individual |

| Commercial & Corporate Fleets |

| Micromobility Service Providers |

| Delivery & Logistics |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East & Africa |

| By Battery Type | Lead-acid | |

| Lithium-ion | ||

| Lithium-ion Polymer | ||

| Sodium-ion & Emerging Chemistries | ||

| By Power Output | Below 3.6 kW | |

| 3.6 - 7.2 kW | ||

| 7.2 - 10 kW | ||

| Above 10 kW | ||

| By Motor / Drive Type | Hub Motor | |

| Belt Drive | ||

| Chain Drive | ||

| Mid-drive Motor | ||

| By End-use | Personal / Individual | |

| Commercial & Corporate Fleets | ||

| Micromobility Service Providers | ||

| Delivery & Logistics | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How large is the electric motorcycle market in 2025?

It is USD 1.14 billion and is projected to reach USD 3.58 billion by 2030 at a 25.72% CAGR.

Which region holds the largest share of electric motorcycle sales?

Asia-Pacific accounts for 73.28% of 2024 revenue thanks to integrated battery supply chains and supportive incentives.

Why are delivery fleets shifting to electric motorcycles?

Operating costs drop 40–60% versus ICE models, and predictable routes align well with depot charging solutions.

What are the main barriers to broader adoption?

Higher upfront prices, limited fast-charge infrastructure, and thermal-safety challenges in hot climates moderate near-term growth.

What battery technology is growing fastest in electric motorcycles?

Sodium-ion & Emerging Chemistries are expanding at a 26.28% CAGR as manufacturers seek lower material costs and supply security.

Page last updated on: