Automotive Telematics System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

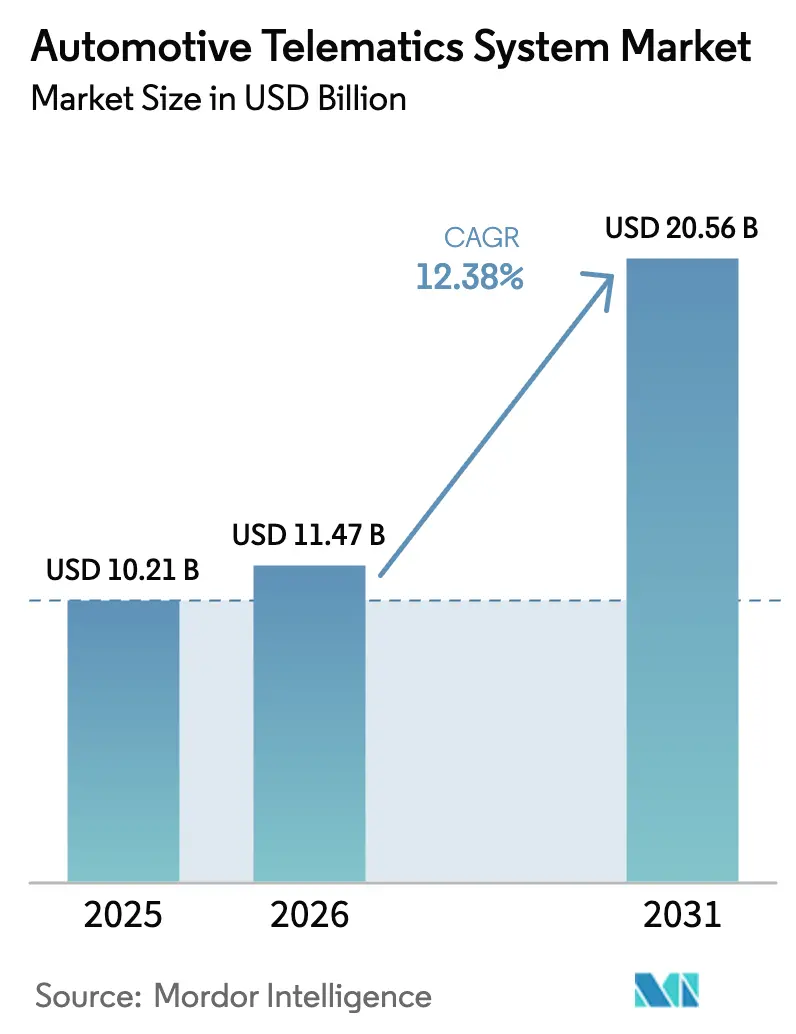

| Market Size (2026) | USD 11.47 Billion |

| Market Size (2031) | USD 20.56 Billion |

| Growth Rate (2026 - 2031) | 12.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Telematics System Market Analysis by Mordor Intelligence

Automotive telematics system market size in 2026 is estimated at USD 11.47 billion, growing from 2025 value of USD 10.21 billion with 2031 projections showing USD 20.56 billion, growing at 12.38% CAGR over 2026-2031. Rising regulatory requirements for in-vehicle emergency calls, falling connectivity costs, and the shift toward software-defined vehicles are expanding baseline connectivity across model ranges. Commercial operators are turning to telematics to offset fuel volatility and driver shortages, which lifts demand for fleet-management platforms capable of double-digit fuel savings and crash reduction. Growth opportunities also stem from electric-vehicle charging optimization, vehicle-to-grid services, and emerging API marketplaces that let third parties purchase anonymised data streams.

Key Report Takeaways

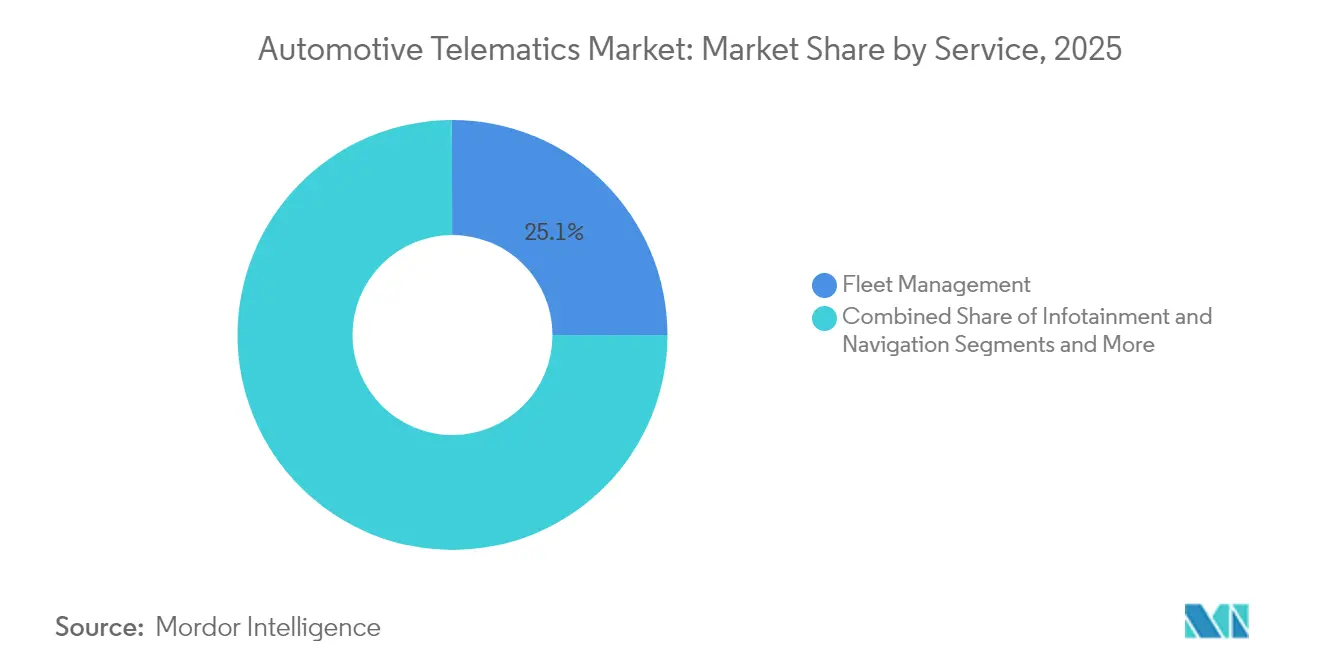

- By service, fleet management led with 25.05% revenue share in 2025, whereas V2X & OTA updates are projected to expand at a 31.02% CAGR to 2031.

- By sales channel type, OEM-fitted systems accounted for 66.45% of the automotive telematics market share in 2025, while the aftermarket is set to grow at 19.2% CAGR through 2031.

- By connectivity solution, embedded architectures held 69.40% of the automotive telematics market size in 2025 and are advancing at a 27.1% CAGR.

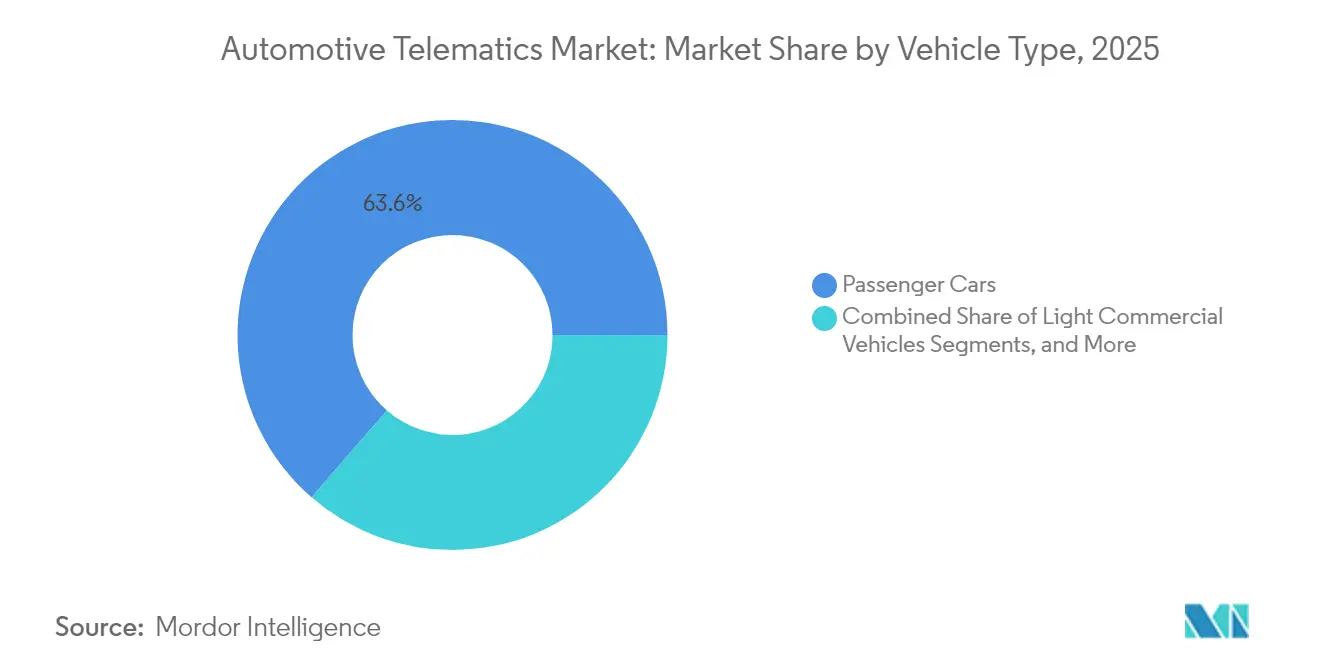

- By vehicle type, passenger cars contributed 63.62% of 2025 revenue; light commercial vehicles are forecast to grow at 17.9% CAGR between 2026-2031.

- By end-user, fleet operators captured 32.70% of 2025 revenue, whereas car-sharing and mobility providers will record the fastest growth at 24.85% CAGR.

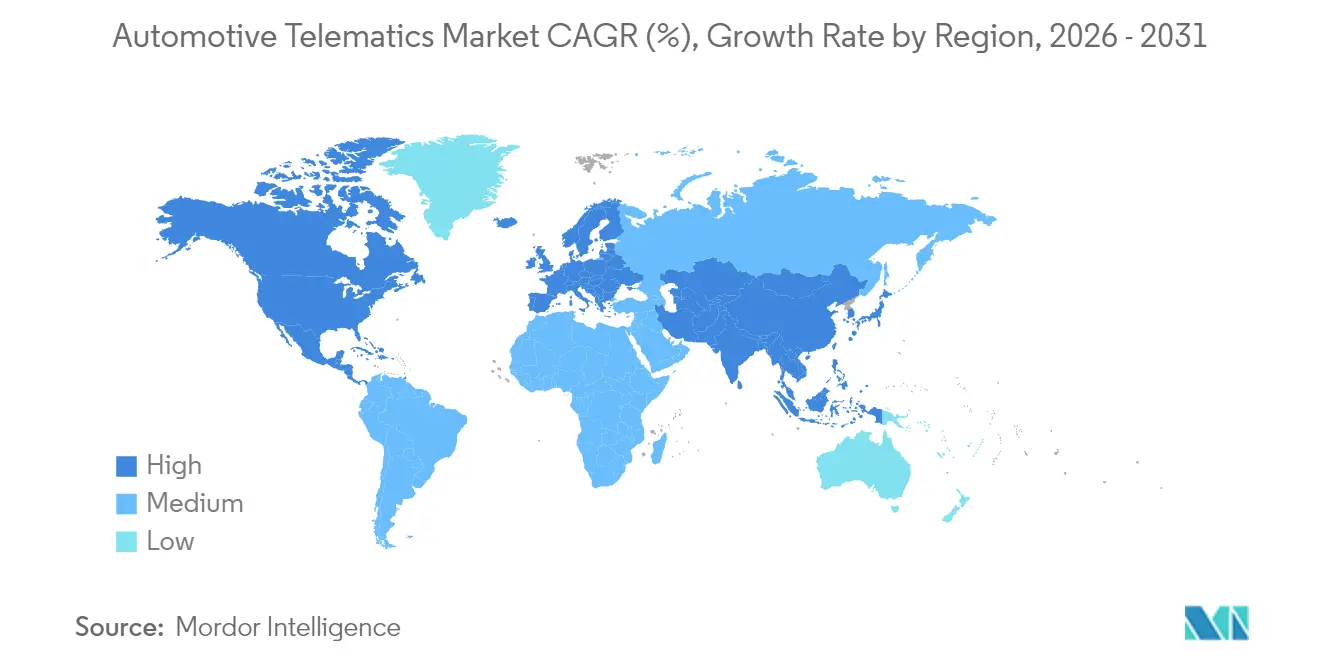

- By geography, North America maintained a 26.90% revenue share in 2025; Asia-Pacific is rising at a 20.9% CAGR on the back of Chinese and Indian digitisation mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Telematics System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government eCall Mandates | +2.1% | Europe, Russia, Brazil, spillover to APAC | Medium term (2–4 years) |

| Fleet-Optimization Amid Fuel Volatility | +1.8% | Global; focus on North America & Europe | Short term (≤ 2 years) |

| Usage-Based-Insurance Adoption | +1.5% | North America, Europe, core APAC markets | Medium term (2–4 years) |

| EV Charging-Network Integration | +1.2% | China, EU, California | Long term (≥ 4 years) |

| Monetization of In-Vehicle Data | +0.9% | Developed markets | Long term (≥ 4 years) |

| UNECE OTA-Cyber-Security Regulations | +0.7% | Europe; global harmonization | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government eCall & Similar Mandates Drive Baseline Connectivity

Mandatory emergency-call systems under the EU eCall regulation and comparable rules in Russia and Brazil have made cellular modules standard equipment in new passenger cars, laying a foundation for added paid services[1]“eCall: Life-Saving Automatic Emergency Call System,” European Commission, europa.eu. Countries in Asia–Pacific are drafting alike frameworks, ensuring the automotive telematics market keeps a minimum penetration rate even in budget segments. Automakers leverage this compulsory hardware for value-added remote diagnostics and stolen-vehicle recovery, which lifts average revenue per unit. Tier-1 suppliers respond with integrated 5G TCUs that meet both accident notification and over-the-air-update needs. The resulting installed base expedites scale economies, pushing unit costs down and facilitating wider mass-market deployment.

Fleet-Optimization Demand Intensifies Amid Fuel-Price Volatility

Diesel and gasoline price swings continue to pressure logistics margins, prompting fleets to adopt real-time telematics that cut idle time and penalize aggressive driving. Studies show 10–15% fuel-cost reduction when advanced routing and driver coaching modules are enabled. Insurer analyses covering US and UK fleets find crash and claim frequencies fall more than 70% once telematics data is fused with driver-training programs. Utilities, construction firms, and municipal services now embed telematics in procurement policies, broadening the end-user base beyond long-haul trucking. Artificial-intelligence add-ons that predict maintenance further improve uptime, increasing the platform’s payback and accelerating adoption in mixed-asset fleets.

Usage-Based-Insurance Adoption Accelerates Insurer Digital Transformation

North American and European carriers have moved personalized premium models from pilot to mainstream, with 65% of policy-holders opting into app- or dongle-based monitoring programs. Real-time feedback nudges safer behaviour, and actuarial data confirms a double-digit drop in loss ratios, delivering rapid ROI to underwriters. Asia–Pacific regulators, notably in South Korea and Australia, support pay-as-you-drive tariffs, which stimulate cross-regional knowledge transfer and product standardization. Partnerships between insurers and automakers to access embedded data via secure APIs remove the cost of aftermarket hardware. As telematics-driven pricing gains consumer acceptance, the automotive telematics market experiences a virtuous circle of higher data volumes and improved risk models.

EV Charging-Network Integration Creates New Service Paradigms

Vehicle-to-grid trials in California and Denmark prove that bidirectional charging can triple the value of managed charging compared with unidirectional methods. Automakers embed telematics to orchestrate charge scheduling, state-of-charge alerts, and grid-service participation, which ensures battery-health safeguards comply with warranty terms. Utilities in the western United States aim for 5–15% onboarding of EV owners into demand-response schemes by 2027 [2]“2025 Vehicle-to-Grid Integration Assessment,” U.S. Department of Energy, energy.gov. These programs rely on secure, low-latency data exchanges governed by ISO 15118 and Open Charge Point Protocol, driving demand for cyber-hardened telematics modules. Charging service providers increasingly bundle connectivity in subscription plans, opening a fresh recurring-revenue pool for OEMs and platform vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device and Data-Plan Cost | -1.9% | Emerging markets: entry-level vehicles worldwide | Short term (≤ 2 years) |

| Persistent Semiconductor Shortages | -1.4% | Global, acute in Asian manufacturing hubs | Medium term (2–4 years) |

| Data-Privacy and Sovereignty Laws | -1.1% | Europe, North America, and expanding across APAC | Long term (≥ 4 years) |

| Country-Specific Telematics Taxation | -0.8% | Global; jurisdiction-dependent | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Device & Data-Plan Costs Limit Entry-Level Market Penetration

Low-margin vehicle segments in India, Brazil and Southeast Asia face consumer price sensitivity that squeezes optional connectivity features. Data-plan fees constitute a larger share of household spending in these markets, making subscription renewals particularly challenging. Local mobile operators rarely provide pan-regional M2M tariffs, adding complexity to exports. Hardware makers are miniaturizing chipsets and system-on-modules to cut bill-of-materials costs, yet inflationary headwinds in 2025 offset part of the gain. Flexible pay-per-use plans and government incentives for road-safety solutions could mitigate the barrier but are unevenly implemented.

Semiconductor Shortages Disrupt Telematics Hardware Supply Chains

While automotive chip availability improved compared with the 2021-2022 crisis, tight 28 nm and 16 nm capacity persists, affecting telematics control units and 5G modems. Automotive silicon represents 17% of global semiconductor sales, with Taiwan’s TSMC holding up to 80% share in mature nodes [3]“Semiconductor Supply Chain Risk,” U.S. Chamber of Commerce, uschamber.com. Shipping delays ripple through telematics retrofit programs, forcing fleets to prolong vehicle lifecycles or defer digital upgrades. Automakers are redesigning boards for multi-sourcing and adopting chiplet architectures, yet qualification cycles extend lead times. Investment in local fab capacity will ease constraints only toward the end of the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Fleet Management Anchors Market While V2X Accelerates

Fleet-management services generated the largest revenue slice in 2025, capturing 25.05% of the automotive telematics market. Logistics, utilities, and field-service fleets rely on routing optimization, fuel monitoring, and driver coaching to maintain margins amid volatile diesel prices. Safety and security modules remain a staple, and predictive-maintenance dashboards help defer costly roadside breakdowns. Diagnostics APIs that integrate with enterprise resource-planning systems are now standard in Western fleets and are gaining traction in Southeast Asia. The automotive telematics market size for V2X & OTA services is projected to expand at 31.02% CAGR, propelled by software-defined vehicle architectures that demand continuous feature deployment. Automakers use dual-radio modules to support both cellular-V2X and 5.9 GHz ITS-G5, unlocking cooperative perception, traffic-signal priority, and over-the-air firmware upgrades that keep vehicles compliant with evolving safety standards.

Second-order demand sources include insurer partnerships that add crash-AI reconstruction to V2X data feeds, improving liability assessments. Infotainment vendors also see an upgraded pathway from one-way streaming to bi-directional cloud gaming, creating incremental data-plan usage. Policy initiatives such as the U.S. DOT’s 5G Roadmap encourage transportation-infrastructure owners to enable lane-level warnings, fostering an ecosystem where public and private datasets converge. Consequently, telematics platforms bundle edge-computing resources and virtualized network functions to meet varying latency and bandwidth requirements across service tiers.

By Sales Channel Type: OEM Integration Dominance Faces Aftermarket Pressure

Factory-installed telematics controlled 66.45% of 2025 revenue as automakers seized data ownership and ensured seamless human-machine interface integration. European eCall mandates and proliferating EV remote-management features further support embedded adoption at the assembly line. The automotive telematics market share of aftermarket boxes, however, is set to escalate as legacy fleets and private owners retrofit non-connected vehicles, a segment growing at 19.2% CAGR. Aftermarket suppliers differentiate through rapid installation, device-agnostic cloud dashboards, and pay-as-you-go contracts.

Ride-hailing operators rely on aftermarket solutions to standardize data across mixed vehicle makes, enabling unified fleet analytics. Yet OEMs are countered by exposing freemium APIs to entice developers, which may cannibalize aftermarket add-ons over the medium term. Regulatory scrutiny over data portability under the EU Data Act could tip bargaining power toward third-party service providers, potentially reshaping channel economics.

By Connectivity Solution: Embedded Systems Lead Despite Integration Challenges

Embedded modules delivered 69.40% of 2025 revenue and are growing at 27.1% CAGR, primarily because they guarantee antenna placement, power management, and cybersecurity compliance that tethered smartphones struggle to match. A GSMA outlook anticipates more than 600 million embedded-connected cars on the road by 2025. The automotive telematics market size tied to embedded architectures scales further as shared data plans let drivers bundle vehicles with existing mobile subscriptions, enhancing stickiness.

Nevertheless, integrated-smartphone solutions remain pivotal in cost-sensitive segments where consumers value flexibility over deep vehicle integration. They serve as a steppingstone, generating behavioral datasets that encourage users to upgrade to embedded packages at vehicle replacement. Tethered dongles comprise a niche yet persistent category, especially in asset tracking and cold chain monitoring where temporary deployments are necessary.

By Vehicle Type: Commercial Segments Drive Electrification Adoption

Passenger cars retained the largest slice of revenue, accounting for 63.62% of the 2025 automotive telematics market share, thanks to universal eCall mandates and mature infotainment ecosystems that encourage consumer adoption. SUVs and MPVs show the highest feature penetration because higher sticker prices support bundled connectivity packages, whereas sedans and hatchbacks still register steady uptake as embedded hardware costs fall. Usage-based insurance programs now attract large chunk of global drivers, reinforcing data-rich telematics services that enhance underwriting accuracy. Heavy commercial vehicles keep robust adoption in long-haul logistics, where real-time route optimization and driver-behaviour monitoring deliver measurable fuel and safety gains. Two-wheeler connectivity remains nascent but is gaining ground in dense urban centers and last-mile delivery fleets that require theft tracking and ride-sharing integration.

Light commercial vehicles represent the fastest-growing category, advancing at an 17.9% CAGR through 2031 as fleet operators digitize vans and pickups to navigate fuel-price swings and tight delivery windows. Operators that pair telematics with driver-training tools report up to 72% crash-and-claim reduction, underlining the segment’s return on investment. Government incentives for zero-emission delivery zones push OEMs to embed 4G/5G modules at the factory, while aftermarket suppliers rush to provide retrofit kits for legacy diesel fleets. Together, these dynamics elevate commercial segments from a cost-control tool to a strategic pillar in electrified, data-centric logistics operations

By End-User: Fleet Operators Lead While Mobility Providers Accelerate

Fleet-operator demand formed 32.70% of 2025 revenue, driven by compelling ROI calculations on fuel, maintenance, and insurance-cost reduction. The automotive telematics industry sees 51% of surveyed fleets planning feature enhancements within the next 12 months. Car-sharing and subscription businesses are expanding at 24.85% CAGR because telematics underpin keyless access, billing accuracy, and real-time utilization monitoring.

Consumer adoption remains steady, aided by bundled infotainment and safety-alert subscriptions that extend beyond the initial free trial. Leasing companies integrate telematics to monitor asset usage and residual-value risk, often mandating device installation as part of contract terms. The confluence of these end-user groups broadens the data lake, enabling more granular segmentation and personalized service offers.

Geography Analysis

North America retained leadership with 26.90% of 2025 revenue, supported by dense 4G/5G coverage, mature fleet-management adoption, and early migration to usage-based insurance. Federal crash-data standards encourage open APIs that simplify insurer and law-enforcement access, while carrier sunsets of 3G networks drove a wave of hardware upgrades across long-haul carriers and delivery fleets. Strong aftermarket penetration complements factory-fit growth because mixed-brand enterprise fleets require uniform dashboards for compliance reporting.

Asia-Pacific is the fastest-growing territory at a 20.9% CAGR, propelled by China’s connected-vehicle mandates and India’s commercial-vehicle digitization rules that make AIS-140 telematics units compulsory. Local automakers pre-install 4G modules in new-energy vehicles to comply with MIIT data-sharing requirements, generating a large, embedded base for value-added apps. Japan and South Korea run V2X corridor pilots that showcase low-latency safety messages, while Southeast Asian ride-hailing fleets rely on smartphone-centric solutions that are beginning to migrate toward embedded hardware as electric-vehicle warranties demand deeper battery analytics. Regional telecom operators are forming cross-border roaming alliances to cut data costs, a move likely to lift small-fleet adoption in 2026-2027.

Europe delivers steady growth underpinned by universal eCall compliance and emerging CO₂-emission monitoring schemes that use telematics payloads for real-world verification. GDPR and the forthcoming EU Data Act raise operating complexity but also create new market space for privacy-preserving analytics vendors. The Middle East and Africa, though still nascent, gain momentum from Gulf smart-city corridors and South African insurers piloting mileage-based premiums, with satellite-IoT and low-power networks extending reach beyond urban centers. Harmonized UNECE cybersecurity rules apply across these regions, guiding procurement toward compliant hardware and making secure over-the-air update capability a non-negotiable feature for both premium and entry-level vehicles.

Competitive Landscape

Competition sits at a moderate level of concentration as factory-fit solutions from global automakers—including General Motors, Stellantis, Ford, and Toyota—overlap with specialist aftermarket providers such as Verizon Connect, Geotab, Trimble, and TomTom. Pure-play players emphasise data analytics and open-API ecosystems that appeal to enterprise fleets, while Tier-1 suppliers like Continental, Bosch, ZF, and Harman embed 5G and cybersecurity capabilities directly into telematics control units. Technology conglomerates—including LG Electronics and Qualcomm—supply cloud, edge-compute, and AI toolchains that allow smaller brands to white-label end-to-end platforms.

Strategic partnerships define market evolution. LG Electronics invested USD 60.5 million in a Mexican telematics factory, adding 400 jobs to shorten North American supply chains. HERE Technologies expanded its HD mapping collaboration with fleet-management vendors to deliver centimeter-level lane guidance. Cybersecurity vendors capitalize on UNECE R155 compliance audits, offering managed threat-detection services embedded at the TCU and gateway levels. White-space niches such as agricultural equipment, micro-mobility, and off-highway machinery attract start-ups that bundle ruggedized sensors with cloud dashboards.

Technological differentiation hinges on multi-radio (satellite, cellular, Wi-Fi) connectivity, edge-compute offload, and AI-driven predictive models. 5G Release 17 features like reduced-capability NR devices allow cost-effective rural coverage, while vehicle-edge containerization supports low-latency sensor fusion essential for assisted-driving functions. The race to secure developer mindshare intensifies, with OEMs and Tier-1s launching app stores offering SDKs, documentation and revenue-sharing terms. Success factors now encompass data-governance maturity and the ability to provide cross-domain digital twins linking vehicles, infrastructure and energy grids.

Automotive Telematics System Industry Leaders

Robert Bosch GmbH

Continental AG

Denso Corporation

Harman International (Samsung)

Verizon Connect

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Roadzen Inc. partnered with a global telematics provider to launch a UK-integrated vehicle protection product that combines asset tracking and GAP insurance, paving the way for European expansion.

- March 2025: Geotab and General Motors Mexico unveiled the country’s first OEM telematics integration, enabling fleets to access real-time data from OnStar-equipped vehicles without the need for aftermarket hardware.

- February 2025: Platform Science completed the acquisition of Trimble’s transportation-telematics arm; Trimble became a strategic investor to co-develop the Virtual Vehicle platform.

- January 2025: Samsara expanded its Stellantis collaboration through Mobilisights, providing European businesses with hardware-free access to data from post-2024 vehicles and select 2018–2024 models.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive telematics system market as revenue from factory-installed or retrofit electronic control units and the associated connectivity services that send, receive, and analyze vehicle data over cellular or satellite networks for safety, navigation, remote diagnostics, fleet optimization, and usage-based insurance in passenger and light commercial vehicles.

Scope exclusion: stand-alone infotainment head units that lack bi-directional data transfer are not covered.

Segmentation Overview

- By Service

- Infotainment and Navigation

- Fleet Management

- Safety & Security

- Diagnostics and Prognostics

- Insurance Telematics

- V2X and OTA Updates

- By Sales Channel Type

- OEM-fitted

- Aftermarket

- By Connectivity Solution

- Embedded

- Integrated-smartphone

- Tethered / Portable

- By Vehicle Type

- Two-Wheelers

- Passenger Cars

- Hatchbacks

- Sedans

- SUVs and MPVs

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- By End-User

- Private Consumers

- Fleet Operators

- Insurance and Leasing Firms

- Car-Sharing and Mobility Providers

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Egypt

- Turkey

- Saudi Arabia

- United Arab of Emirates

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with tier-one telematics hardware makers, multi-country fleet managers, mobility insurers, and regional telecom operators let us sharpen attach-rate curves, service price points, and 4G-to-5G migration timelines across North America, Europe, China, India, and the Gulf.

Desk Research

We began by lining up baseline indicators from open sources such as OICA vehicle production volumes, ITU mobile coverage statistics, NHTSA crash files, European Commission eCall notes, and FMCSA fleet registries. Company 10-Ks, investor decks, and respected automotive trade journals helped us benchmark technology cost curves and attach-rate shifts.

Mordor analysts then tapped Marklines build logs, D&B Hoovers financial snapshots, and Dow Jones Factiva news runs to cross-check shipment trends and average selling prices.

The sources quoted are illustrative, not exhaustive, and many other credible references informed the data gathering.

Market-Sizing & Forecasting

We start with a top-down attach-rate build that multiplies regional vehicle production and in-service parc by telematics penetration levels shaped by regulatory triggers. We corroborate results with selective bottom-up checks, such as sampled control unit ASPs times shipment volume and surveyed fleet subscription cohorts. Key variables include new vehicle output, aftermarket installation rates, average revenue per active unit, eCall and AIS-140 mandates, 5G coverage expansion, and electrified fleet share. Forecasts use multivariate regression informed by primary research consensus, followed by scenario analysis to test upside and downside paths. Any gaps in bottom-up data are bridged with proxy ratios validated in follow-up calls.

Data Validation & Update Cycle

Outputs move through time-series variance scans, peer ratio comparisons, and senior analyst reviews. Anomalies prompt re-contact with sources. We refresh the model every year, and we issue interim updates when events like sudden retrofit mandates alter the baseline.

Why Mordor's Automotive Telematics System Baseline Stands Reliable

Published estimates often diverge because firms mix hardware sales with service revenue, apply different attach-rate ramps, or update at uneven intervals.

Typical gap drivers include whether motorcycles and off-highway equipment are counted, the treatment of aftermarket retrofits, currency conversion dates, and the pace at which analysts roll forward 5G-driven pricing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.21 B (2025) | Mordor Intelligence | |

| USD 10.02 B (2025) | Global Consultancy A | Counts only OEM embedded units, omits aftermarket subscriptions |

| USD 12.42 B (2024) | Industry Research B | Adds infotainment hardware and broader connected services revenue |

| USD 91.81 B (2024) | Trade Journal C | Aggregates the entire connected vehicle ecosystem, including SIM fees |

The comparison shows that our disciplined scope choices, transparent variable list, and annual refresh cadence deliver a balanced, reproducible baseline that decision makers can trust.

Key Questions Answered in the Report

What is the current size of the automotive telematics market?

The market generated USD 11.47 billion in 2026 and is forecast to reach USD 20.56 billion by 2031, growing at a 12.38% CAGR.

Which service category holds the largest share of the automotive telematics market?

Fleet-management platforms lead with a 25.05% revenue share in 2025, thanks to proven fuel savings and safety benefits.

Why is Asia–Pacific the fastest-growing region for automotive telematics?

Chinese connected-car mandates and Indian commercial-vehicle digitization policies are driving a 20.9% CAGR in Asia–Pacific adoption.

How do OEM-fitted and aftermarket channels compare?

OEM-fitted systems captured 66.45% of 2025 revenue, but aftermarket solutions are expanding at 19.2% CAGR as older fleets retrofit connectivity.

Page last updated on: