New Zealand Two-Wheeler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

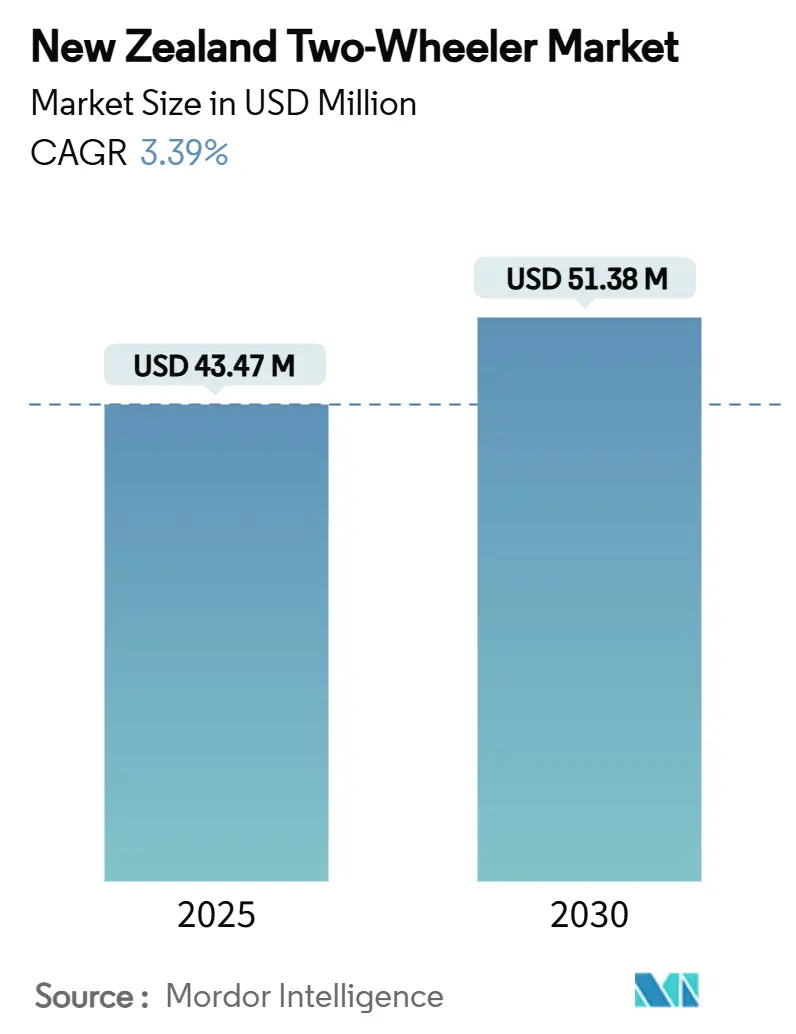

| Market Size (2025) | USD 43.47 Million |

| Market Size (2030) | USD 51.38 Million |

| Growth Rate (2025 - 2030) | 3.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

New Zealand Two-Wheeler Market Analysis by Mordor Intelligence

The New Zealand two-wheeler market size stands at USD 43.47 million in 2025 and is forecast to reach USD 51.38 million by 2030, reflecting a 3.39% CAGR across the period. The expansion is steady rather than rapid because the market is moving from an early-growth phase to measured maturity as regulations tighten, purchase incentives recede and buyers weigh total cost of ownership more carefully. Internal-combustion products still dominate today, but the electric transition is under way as fleet buyers chase sustainability goals and as the country’s largely renewable electricity mix supports low-carbon transport. Urban congestion in Auckland and Wellington, evolving consumer lifestyles that favour compact personal mobility, and improving digital sales channels all work in tandem to keep demand on an upward trajectory. At the same time, the termination of the Clean Car Discount at the end of 2023 and the introduction of road-user charges (RUC) for higher-powered electric vehicles in April 2024 add friction to short-term electrification, while stringent graduated licensing slows first-time adoption among younger riders.

Key Report Takeaways

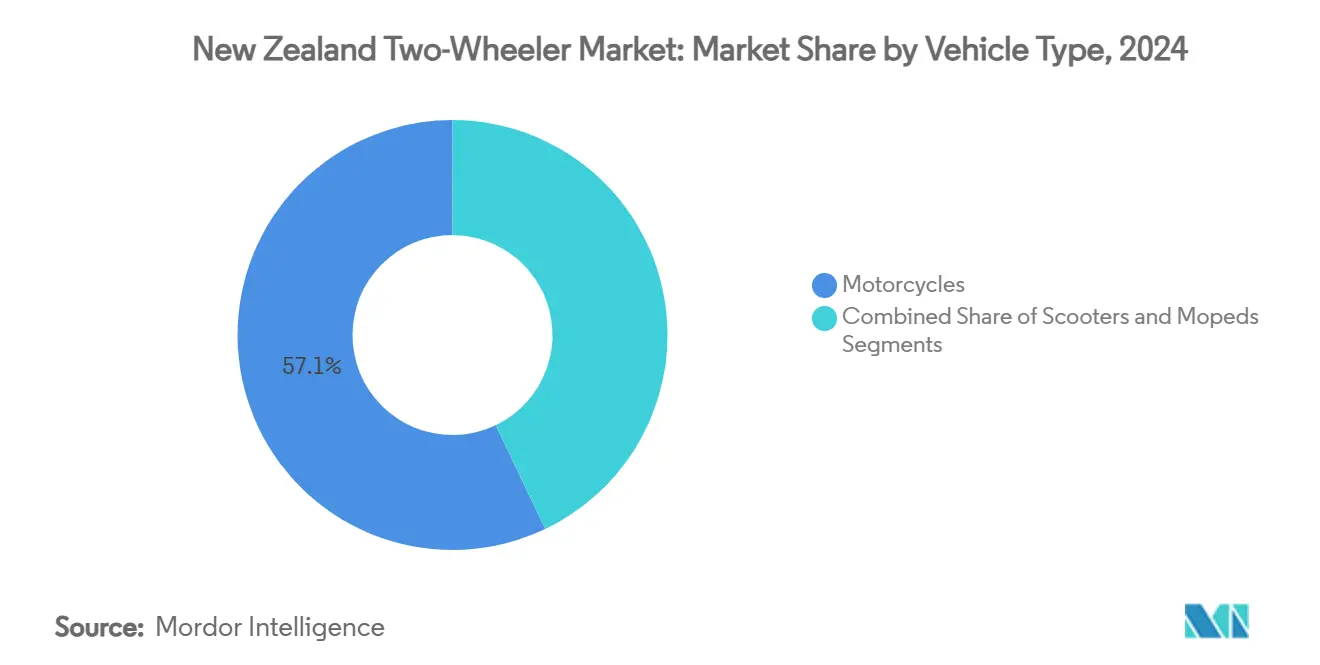

- By vehicle type, motorcycles held 57.13% of the New Zealand two-wheeler market share in 2024, while scooters are projected to record the fastest 28.26% CAGR through 2030.

- By technology, internal-combustion models accounted for 78.42% of the New Zealand two-wheeler market size in 2024, whereas electric two-wheelers are forecast to expand at a 34.72% CAGR.

- By transmission, manual machines led with 71.87% share in 2024, and automatic/CVT units are expected to advance at a 22.93% CAGR to 2030.

- By fuel type, petrol powertrains commanded 80.08% share in 2024, while electric alternatives are set to grow at a 34.69% CAGR over the forecast period.

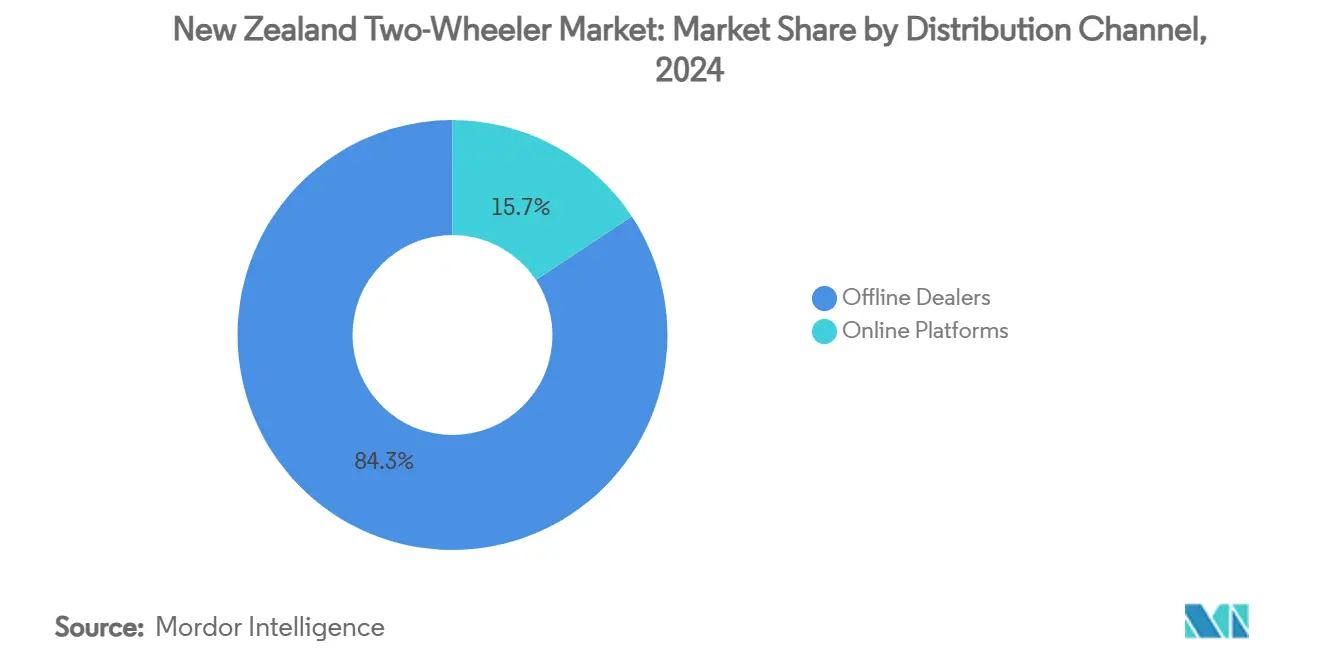

- By distribution channel, offline dealers captured 84.31% of 2024 revenue, whereas online platforms are projected to rise at a 25.38% CAGR.

- By end-user, personal ownership represented 69.76% share in 2024, while commercial and fleet demand is poised to increase at a 30.14% CAGR.

- By geography, North Island contributed 73.52% of 2024 sales, whereas South Island is expected to post the quickest 9.58% CAGR to 2030.

New Zealand Two-Wheeler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Congestion & Parking Shortage | +0.8% | North Island, concentrated in Auckland and Wellington | Medium term (2-4 years) |

| Rising Fuel Prices & Cost-Conscious Riders | +0.6% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| Fleet Electrification by Corporates | +0.5% | National, with early adoption in major cities | Medium term (2-4 years) |

| Rise in Off-Road Riding Culture | +0.4% | South Island, with spillover to North Island | Long term (≥ 4 years) |

| Adventure Tourism in Back-Country Trails | +0.3% | South Island, concentrated in Queenstown and Central Otago | Long term (≥ 4 years) |

| Govt Rebates for E-Two-Wheelers | +0.2% | National, with early adoption in urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Urban Congestion and Parking Scarcity

Auckland's traffic congestion will cost the city USD 2.6 billion annually by 2026, with residents wasting over 17 hours yearly in traffic delays[1]Maia Ingoe, "Traffic congestion could cost Auckland $2.6 billion a year," RNZ, rnz.co.nz.. This economic burden drives two-wheeler adoption as commuters seek alternatives to car dependency, particularly given that 90% of traffic consists of private vehicles. The mayor's advocacy for congestion charging mechanisms creates additional pressure for modal shift toward motorcycles and scooters. Wellington faces similar constraints due to geographic limitations and government workforce concentration. The government's USD 1.5 billion cut to public transport funding paradoxically amplifies two-wheeler appeal as alternative transport options diminish. Parking scarcity in central business districts further incentivizes compact vehicle adoption, with two-wheelers offering superior maneuverability and storage efficiency compared to traditional automobiles.

Escalating Petrol Prices and Cost-Sensitive Commuters

Rising fuel costs disproportionately impact New Zealand consumers given the country's geographic isolation and import dependence for petroleum products. Two-wheelers typically achieve 2-3 times better fuel efficiency than passenger cars, creating compelling economic value propositions for cost-conscious commuters. The government's road user charges introduction for electric vehicles at USD 76 per 1,000 kilometers from April 2024 paradoxically makes petrol-powered two-wheelers more competitive in certain use cases. This policy shift occurred as electric vehicle adoption reached 2% of the light vehicle fleet, suggesting timing sensitivity around incentive structures. Corporate fleet operators increasingly evaluate total cost of ownership models that favor two-wheelers for last-mile delivery applications. HELL Pizza's USD 160,000 investment in 45 electric bikes demonstrates how businesses leverage fuel efficiency advantages to reduce operational expenses while addressing environmental commitments.

Growing Recreational Off-Road Riding Culture

South Island's adventure tourism recovery drives recreational two-wheeler demand, with guided motorcycle tours priced from USD 11,200 to USD 23,738 targeting international and domestic riders. The region's diverse terrain spanning coastal routes, mountain passes, and back-country trails creates unique value propositions for adventure motorcycles and off-road capable scooters. Tourism operators emphasize safety training and local road rule familiarization, addressing concerns about narrow, twisty roads and left-hand traffic patterns. The recreational segment benefits from New Zealand's 80% renewable electricity generation, making electric off-road vehicles environmentally attractive[2]Ripu Bhatia, "Electric motorcycle, moped numbers double on NZ roads in five years," Stuff, stuff.co.nz. . UBCO's 2X2 Work Bike, despite the company's recent receivership, demonstrated market appetite for electric adventure vehicles with 75-mile range and all-wheel drive capability. This segment's growth trajectory remains resilient to short-term policy changes given its discretionary spending nature and tourism industry recovery momentum.

Government Rebates for E-Two-Wheelers

The Clean Car Discount scheme's termination in December 2023 eliminated direct purchase incentives for electric two-wheelers, contributing to the 55% decline in electric vehicle registrations. However, the government maintains its commitment to 10,000 public EV chargers by 2030, up from 1,378 currently, through USD 68.5 million in concessionary loans to private operators[3]"Accelerating the roll-out of public EV chargers," Beehive, beehive.govt.nz.. This infrastructure investment indirectly supports electric two-wheeler adoption by addressing range anxiety concerns. The road user charges exemption for very light electric vehicles, including electric motorcycles, preserves cost advantages for specific vehicle categories. Corporate fleet incentives through the Low Emissions Transport Fund continue supporting commercial electric vehicle adoption, benefiting delivery and service applications. The policy environment suggests selective support rather than broad-based subsidies, requiring manufacturers to demonstrate clear value propositions beyond purchase price incentives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Rider Licensing & Safety Rules | -0.5% | National, with higher impact on younger demographics | Medium term (2-4 years) |

| High Insurance for less than 25-Year Riders | -0.4% | National, with concentrated impact on entry-level segments | Medium term (2-4 years) |

| Low Battery Pack Assembly Capacity | -0.3% | National, affecting electric vehicle supply chains | Long term (≥ 4 years) |

| Competitive TCO of Micro-Cars | -0.2% | Urban areas, particularly North Island cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Graduated Rider-Licensing and Safety Rules

New Zealand's graduated driver licensing system creates multi-stage barriers for motorcycle adoption, requiring progression through learner, restricted, and full license categories with mandatory waiting periods and testing requirements. The Learner Approved Motorcycle Scheme restricts novice riders to specific vehicle models, limiting market access for higher-performance segments. Insurance companies apply additional excesses for riders under 25 and those with less than two years experience, creating cost barriers for younger demographics. The government's proposed licensing reforms for 2026 focus on car licenses rather than motorcycle-specific improvements, suggesting continued regulatory complexity. Safety concerns around e-scooters, with crash victims requiring more surgeries than motorbike riders according to New Zealand Medical Journal studies, create regulatory caution that may extend to broader two-wheeler categories. These regulatory frameworks prioritize safety over market accessibility, constraining entry-level adoption rates.

Limited Domestic Battery-Pack Assembly Capacity

UBCO's receivership in January 2025 eliminated New Zealand's primary electric two-wheeler manufacturer, constraining local production capabilities and reinforcing import dependence. The company's failure despite USD 70 million funding and Australia Post contracts highlights challenges in scaling electric vehicle manufacturing in small markets. Aspiring Materials' Christchurch facility produces nickel-manganese-cobalt materials for lithium-ion batteries but lacks integration with local vehicle assembly operations. This supply chain fragmentation increases costs and lead times for electric two-wheeler manufacturers. The government's Clean Car Import Standard creates emissions thresholds that favor electric vehicles but provides limited support for domestic manufacturing capabilities. Import duties and shipping costs from Asian manufacturing centers add 15-20% to vehicle costs, disadvantaging New Zealand consumers relative to larger markets. The absence of local assembly also limits customization for New Zealand's unique regulatory requirements and operating conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Motorcycles Lead Despite Scooter Surge

Motorcycles captured 57.13% market share in 2024, reflecting New Zealand's preference for versatile vehicles capable of both urban commuting and recreational touring across diverse terrain. The segment benefits from established dealer networks and comprehensive model ranges spanning entry-level LAMS-approved bikes to premium adventure motorcycles. Honda's XL750 Transalp at USD 19,495 exemplifies the adventure touring category's appeal, featuring 755cc parallel-twin engines and five riding modes for varied conditions. Scooters demonstrate the fastest growth at 28.26% CAGR through 2030, driven by urban congestion pressures and aging population demographics seeking accessible mobility solutions.

Mopeds occupy a specialized niche focused on cost-conscious consumers and delivery applications, benefiting from simplified licensing requirements and lower operating costs. The segment faces pressure from electric alternatives offering superior performance and environmental credentials. Corporate fleet adoption increasingly favors electric scooters over traditional mopeds for last-mile delivery, as demonstrated by NZ Post's deployment of Paxster vehicles capable of carrying 200 kilograms with 70-90 kilometer range. This shift toward electric powertrains across all vehicle types suggests traditional internal combustion segments will face sustained pressure despite current market dominance.

By Technology: Electric Acceleration Despite ICE Dominance

Internal combustion engines maintained 78.42% market share in 2024, supported by established infrastructure, competitive pricing, and performance characteristics suited to New Zealand's varied geography. The 126-180cc segment captures significant volume through LAMS-approved motorcycles targeting new riders, while larger displacement categories serve touring and recreational applications. Honda's NX500 with 471cc twin-cylinder engine demonstrates the sweet spot for urban and light off-road use at USD 13,595. Electric powertrains accelerate at 34.72% CAGR despite policy headwinds, with the 4-7kW category leading adoption through urban commuter applications.

Electric motorcycle and moped registrations doubled from 225 units in 2015 to 422 units in 2023, though high costs of USD 3,000-4,500 constrain broader adoption. The government's 80% renewable electricity generation creates compelling environmental value propositions for electric vehicles, particularly in corporate fleet applications where total cost of ownership models favor electric powertrains. UBCO's receivership eliminates local electric manufacturing capability, potentially slowing adoption rates through reduced model availability and higher import costs. The less than 4kW segment benefits from road user charges exemptions, maintaining cost advantages over higher-power electric alternatives subject to USD 76 per 1,000 kilometer charges.

By Transmission: Manual Preference Yields to Convenience

Manual transmissions held 71.87% market share in 2024, reflecting traditional rider preferences for control and performance characteristics. The segment benefits from lower purchase prices, reduced maintenance complexity, and superior fuel efficiency compared to automatic alternatives. Enthusiast segments particularly favor manual transmissions for recreational and touring applications where rider engagement remains paramount. Automatic and CVT systems grow at 22.93% CAGR through 2030, driven by urban commuter preferences for convenience and accessibility, particularly among aging demographics and new riders seeking simplified operation.

The shift toward automatic transmissions accelerates in scooter segments where convenience outweighs performance considerations. Corporate fleet applications increasingly specify automatic transmissions to reduce training requirements and improve operational efficiency for delivery personnel. Electric powertrains inherently offer automatic operation, contributing to transmission segment evolution as electrification progresses. The government's graduated licensing system creates entry barriers that favor automatic transmissions for novice riders, as simplified operation reduces learning curve complexity. This demographic shift suggests sustained growth for automatic systems despite traditional manual preferences among experienced riders.

By Fuel Type: Petrol Dominance Faces Electric Challenge

Petrol powertrains commanded 80.08% market share in 2024, supported by established refueling infrastructure and competitive operating costs relative to electric alternatives following the introduction of road user charges. The segment benefits from diverse model availability across all vehicle categories and price points. Rising fuel costs create pressure for more efficient powertrains, driving interest in smaller displacement engines and hybrid alternatives. Electric fuel systems achieve 34.69% CAGR growth through 2030, accelerated by corporate fleet adoption and environmental consciousness despite policy headwinds.

The government's road user charges implementation at USD 76 per 1,000 kilometers for electric vehicles above certain power thresholds reduces cost advantages previously enjoyed by electric powertrains. However, very light electric vehicles, including electric motorcycles, retain exemptions, preserving competitive positioning for specific categories. CNG and LPG alternatives remain niche due to limited refueling infrastructure and vehicle availability, though environmental benefits may drive future adoption in commercial applications. The fuel type evolution reflects broader transportation electrification trends, with New Zealand's renewable electricity generation providing compelling environmental value propositions for electric powertrains despite short-term policy challenges.

By Distribution Channel: Digital Disruption Challenges Traditional Dealers

Offline dealers maintained 84.31% market share in 2024, leveraging established relationships, service capabilities, and inventory management advantages. Traditional dealerships provide essential functions, including financing, warranty support, and technical expertise that online platforms struggle to replicate. Honda and Kawasaki's nationwide dealer networks exemplify the channel's importance for customer acquisition and retention. Online platforms demonstrate 25.38% CAGR growth through 2030, driven by price transparency, convenience, and expanded model availability from international suppliers.

Digital channels particularly benefit electric vehicle segments where traditional dealers lack expertise and inventory depth. Direct-to-consumer sales models adopted by electric vehicle manufacturers bypass traditional distribution constraints, though service network limitations remain challenging. The COVID-19 pandemic accelerated online research and purchase behaviors, creating permanent shifts in consumer expectations for digital engagement. Combining online research with offline fulfillment, hybrid distribution models emerge as optimal approaches, allowing consumers to leverage digital convenience while accessing traditional dealer services. This channel evolution requires traditional dealers to enhance digital capabilities while online platforms develop service network partnerships to address post-purchase support requirements.

By End-User: Commercial Fleet Growth Outpaces Personal Use

Personal use applications captured 69.76% market share in 2024, driven by commuting, recreational, and touring applications across New Zealand's diverse geography. The segment benefits from emotional purchase drivers and discretionary spending patterns that support premium pricing and feature content. Adventure tourism recovery in the South Island creates growth opportunities for recreational applications, with guided motorcycle tours demonstrating market appetite for experiential offerings. Commercial and fleet applications accelerate at a 30.14% CAGR through 2030, propelled by last-mile delivery optimization and corporate sustainability initiatives.

NZ Post's fleet electrification strategy demonstrates commercial adoption momentum, with over 400 electric delivery vehicles operational and full electrification targeted by 2030 through USD 20 million green financing. Food delivery services, including HELL Pizza, invest in electric two-wheelers to reduce operational costs and environmental impact, with USD 160,000 committed to 45 electric bikes. Commercial applications benefit from total cost of ownership advantages, predictable usage patterns, and corporate environmental commitments that justify premium pricing for electric alternatives. The segment's growth trajectory suggests sustained expansion as businesses optimize delivery networks and embrace sustainability mandates.

Geography Analysis

North Island dominates with 73.52% market share in 2024, driven by Auckland's 1.7 million population concentration and Wellington's government workforce density creating substantial urban commuting demand. The region benefits from established dealer networks, service infrastructure, and parts availability that support market development across all vehicle categories. Auckland's projected USD 2.6 billion annual congestion cost by 2026 creates compelling value propositions for two-wheeler adoption as commuters seek alternatives to car dependency. Wellington's compact geography and government employment concentration favor scooters and smaller motorcycles for urban mobility applications. The region's corporate fleet concentration drives electric vehicle adoption through sustainability initiatives and operational efficiency programs, with NZ Post's 400+ electric delivery vehicles demonstrating commercial market leadership.

South Island demonstrates faster growth at 9.58% CAGR through 2030, propelled by adventure tourism recovery and recreational riding culture expansion across diverse terrain spanning coastal routes, mountain passes, and back-country trails. The region's tourism operators offer guided motorcycle tours priced from USD 11,200 to USD 23,738, targeting both international visitors and domestic enthusiasts seeking experiential offerings. Queenstown and Central Otago regions particularly benefit from adventure tourism positioning, with operators emphasizing safety training and local road rule familiarization to address narrow, twisty road conditions. The region's lower population density creates opportunities for off-road and adventure motorcycle segments that leverage New Zealand's unique geography. UBCO's Christchurch-based operations, despite recent receivership, demonstrated South Island's potential for electric vehicle manufacturing and innovation, though supply chain constraints limit near-term development prospects.

Competitive Landscape

The New Zealand two-wheeler market exhibits moderate fragmentation across established Japanese manufacturers and emerging electric specialists, with no single player commanding a dominant market position. Traditional manufacturers, including Yamaha, Honda, Suzuki, and Kawasaki, leverage established dealer networks, comprehensive model ranges, and proven reliability to maintain market leadership across ICE segments. These incumbents face pressure from electric vehicle specialists and changing consumer preferences toward sustainable mobility solutions. Honda's NX500 and XL750 Transalp models demonstrate traditional manufacturers' adaptation strategies, combining proven powertrains with modern technology features, including traction control and smartphone connectivity.

White-space opportunities emerge in electric commercial vehicles and adventure tourism applications, where specialized requirements create differentiation possibilities beyond traditional volume segments. UBCO's receivership eliminates local electric manufacturing capability, creating market gaps for international electric vehicle manufacturers willing to address New Zealand's unique regulatory and geographic requirements. CFMOTO's 21% growth in 2024 with USD 1.6 billion first-half profits demonstrates emerging manufacturers' potential to disrupt established market dynamics through competitive pricing and modern technology integration. The competitive landscape suggests continued evolution toward electrification and technology integration, with success dependent on balancing innovation with proven reliability and service network capabilities.

New Zealand Two-Wheeler Industry Leaders

-

Yamaha Motor Co.

-

Honda Motor Co.

-

Suzuki Motor Corp.

-

Kawasaki Heavy Industries

-

KTM AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: In October 2024, Yamaha expanded its supersport lineup with the official launch of the new YZF-R9. As per Yamaha Motor New Zealand’s announcement, the R9 integrates the aggressive design language of the R-series with the reliable 890cc CP3 triple-cylinder engine, also utilized in the MT-09. Engineered for both road and track applications, the R9 features advanced rider assistance systems, an upgraded chassis, and improved aerodynamics, positioning it as a high-performance yet accessible middleweight option within the sportbike market.

- June 2024: In June 2024, BSA Motorcycles, the iconic British brand, announced its return to the New Zealand market after decades of absence. Revived under Classic Legends, a subsidiary of the Mahindra Group, BSA plans to reintroduce its retro-inspired lineup, starting with the Gold Star 650. This development aligns with the increasing demand for heritage-style motorcycles, which combine classic designs with modern engineering. BSA's re-entry highlights a growing interest in vintage motorcycling culture within New Zealand's two-wheeler market.

New Zealand Two-Wheeler Market Report Scope

| Scooters |

| Mopeds |

| Motorcycles |

| Internal-Combustion (ICE) | Less than100 cc |

| 100 to 125 cc | |

| 126 to 180 cc | |

| 181 to 250 cc | |

| 251 to 500 cc | |

| 501 to 800 cc | |

| 801 to 1600 cc | |

| More than 1600 cc | |

| Electric | Less than 4 kW |

| 4 to 7 kW | |

| 7 to 15 kW | |

| More than 15 kW |

| Manual |

| Automatic/CVT |

| Petrol |

| Electric |

| CNG/LPG |

| Offline Dealers |

| Online Platforms |

| Personal |

| Commercial/Fleet |

| North Island |

| South Island |

| By Vehicle Type | Scooters | |

| Mopeds | ||

| Motorcycles | ||

| By Technology | Internal-Combustion (ICE) | Less than100 cc |

| 100 to 125 cc | ||

| 126 to 180 cc | ||

| 181 to 250 cc | ||

| 251 to 500 cc | ||

| 501 to 800 cc | ||

| 801 to 1600 cc | ||

| More than 1600 cc | ||

| Electric | Less than 4 kW | |

| 4 to 7 kW | ||

| 7 to 15 kW | ||

| More than 15 kW | ||

| By Transmission | Manual | |

| Automatic/CVT | ||

| By Fuel Type | Petrol | |

| Electric | ||

| CNG/LPG | ||

| By Distribution Channel | Offline Dealers | |

| Online Platforms | ||

| By End-User | Personal | |

| Commercial/Fleet | ||

| By Geography | North Island | |

| South Island | ||

Key Questions Answered in the Report

What is the current value of the New Zealand two-wheeler market?

The New Zealand two-wheeler market size is USD 43.47 million in 2025.

How fast is the New Zealand two-wheeler market expected to grow?

The market is projected to expand at a 3.39% CAGR between 2025 and 2030.

Which vehicle type holds the largest share in New Zealand?

Motorcycles led with 57.13% New Zealand two-wheeler market share in 2024.

What segment is growing the quickest?

Scooters are forecast to post the fastest 28.26% CAGR through 2030.

Page last updated on: