Off-road Vehicle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

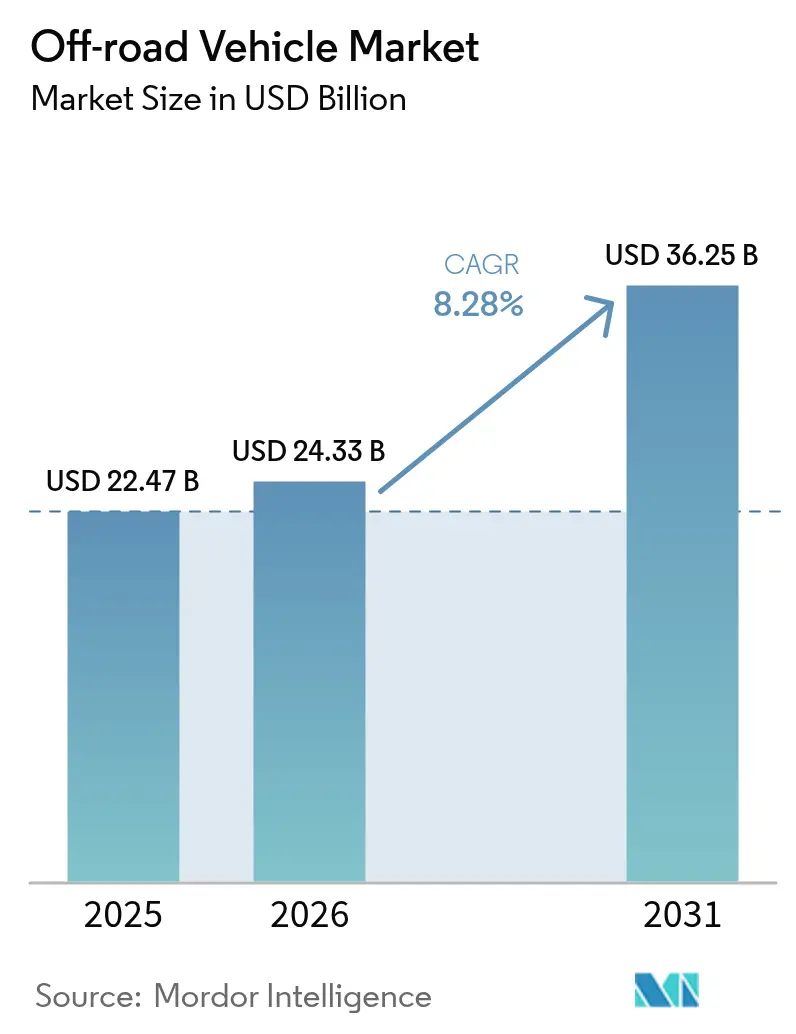

| Market Size (2026) | USD 24.33 Billion |

| Market Size (2031) | USD 36.25 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

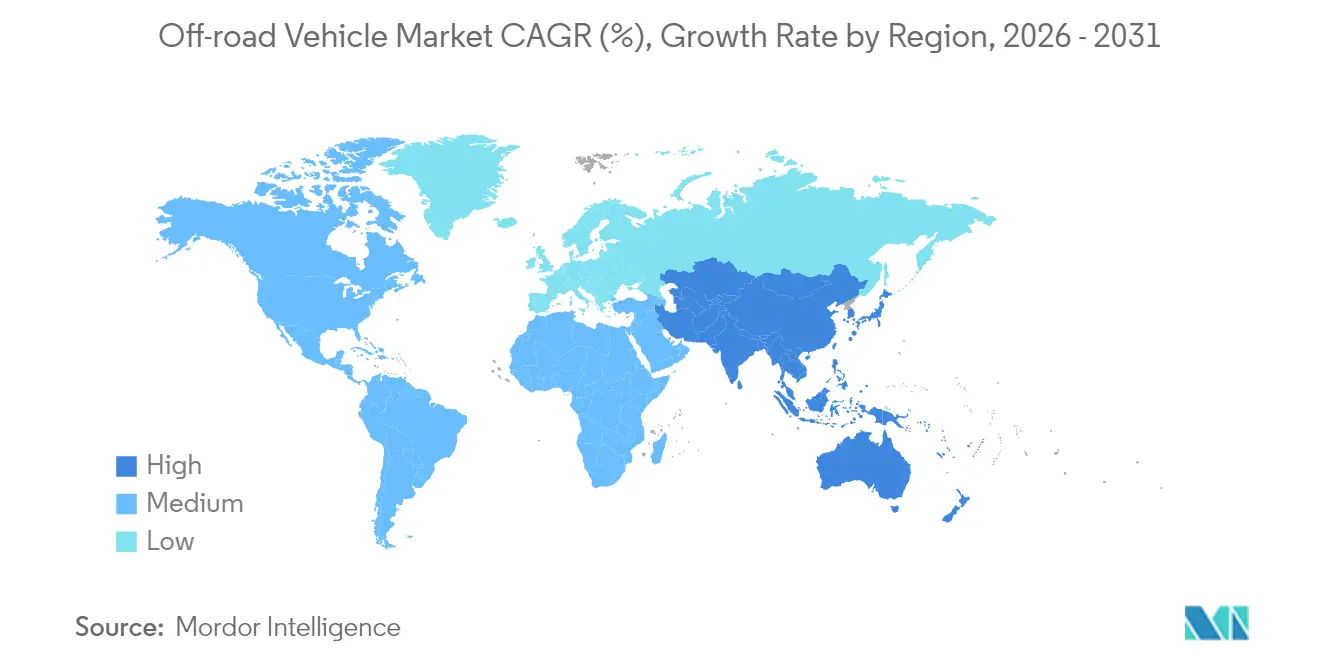

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

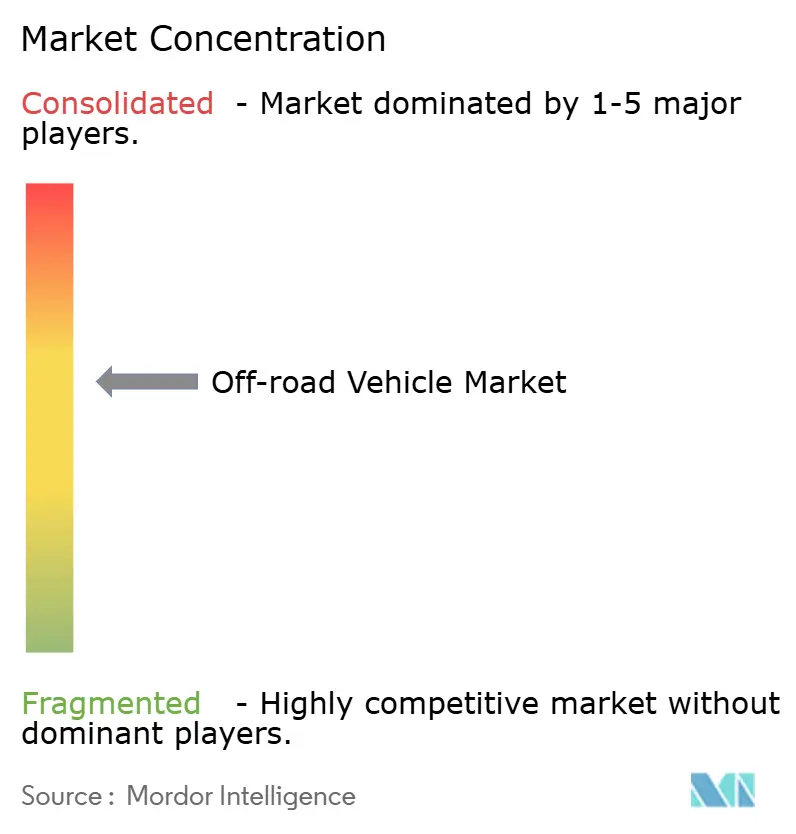

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Off-road Vehicle Market Analysis by Mordor Intelligence

Off-road Vehicle Market size in 2026 is estimated at USD 24.33 billion, growing from 2025 value of USD 22.47 billion with 2031 projections showing USD 36.25 billion, growing at 8.28% CAGR over 2026-2031. This growth arises from a confluence of rising outdoor recreation participation, accelerating electrification, and expanding utility applications that continue to offset cyclical revenue fluctuations among leading manufacturers. Growing trail infrastructure funding, precision-farming uptake, and military mobility modernization programs further widen demand pools, while technology convergence around electronic power steering (EPS), telematics, and advanced suspension systems enhances value propositions for both consumer and commercial buyers. Even with revenue contractions at major suppliers during 2024, the off-road vehicle market shows resilience through diversification into electric variants, specialty defense contracts, and subscription-based connectivity services that solidify long-term revenue streams.

Key Report Takeaways

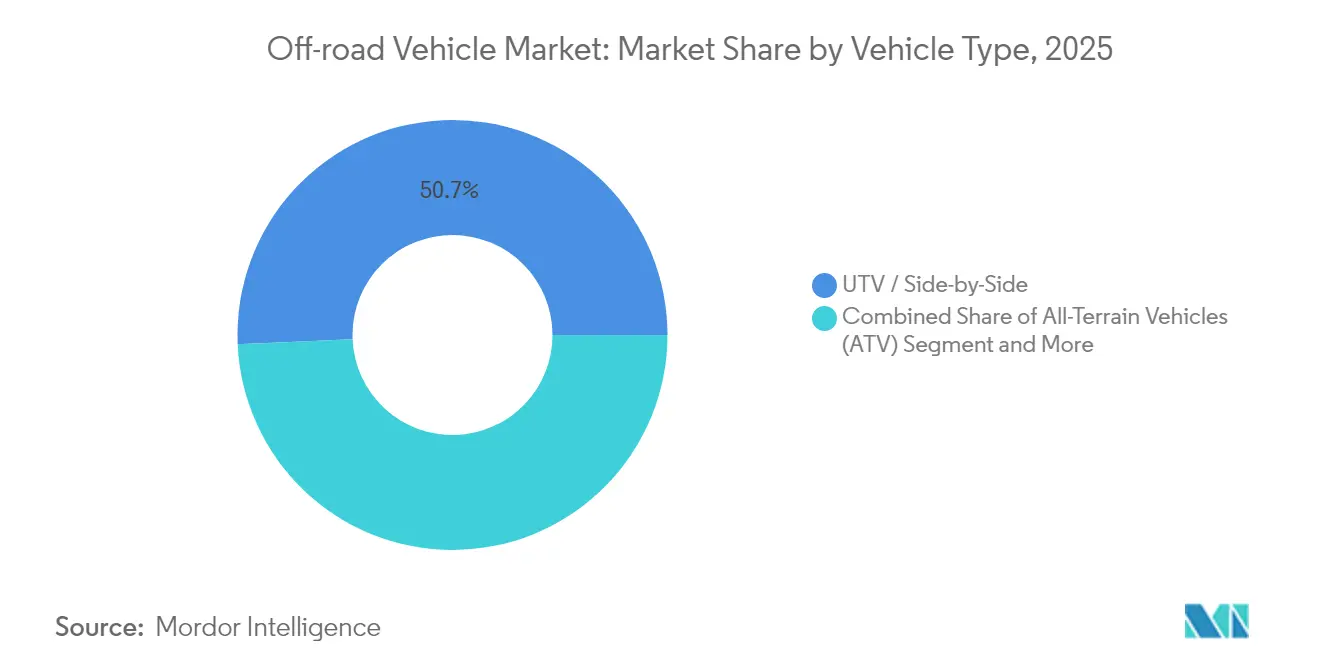

- By vehicle type, UTV/Side-by-Sides led with 50.68% of off-road vehicle market share in 2025; electric UTVs are forecast to grow at an 8.32% CAGR to 2031.

- By application, sports and recreation accounted for 41.05% of the off-road vehicle market size in 2025, while military and law-enforcement demand is expanding at an 8.35% CAGR through 2031.

- By propulsion type, conventional internal combustion engines retained 83.05% share of the off-road vehicle market size in 2025, yet battery-electric models will post the highest 8.30% CAGR to 2031.

- By engine displacement, the 400-800 cc bracket held 44.78% of off-road vehicle market share in 2025; engines above 800 cc are poised for an 8.37% CAGR through 2031.

- By power output, the 50-100 kW band captured 38.29% of the off-road vehicle market size in 2025, whereas units exceeding 100 kW are projected to register an 8.44% CAGR by 2031.

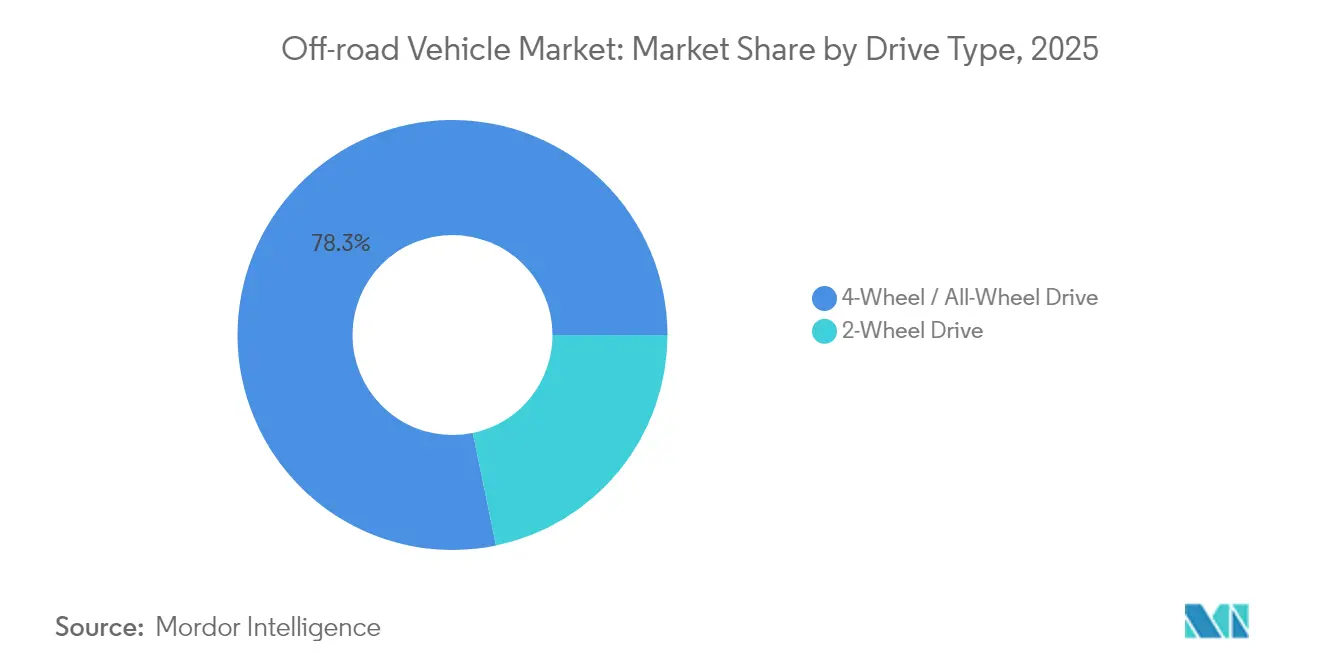

- By drive system, AWD solutions controlled 78.25% of off-road vehicle market share in 2025 and are expected to progress at an 8.40% CAGR through 2031.

- By seating capacity, two-rider layouts represented 51.72% of the off-road vehicle market size in 2025; three-plus-passenger platforms will expand at an 8.47% CAGR to 2031.

- By geography, North America represented 37.84% of the off-road vehicle market size in 2025; Asia Pacific will expand at an 8.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Off-road Vehicle Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Outdoor Recreational Tourism | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Tactical ATV/UTV Procurement | +1.1% | Global, emphasis on NATO and Asia Pacific regions | Medium term (2-4 years) |

| Rapid Mechanization Of Midsize Farms | +0.9% | Global, concentrated in Asia Pacific and Latin America | Long term (≥ 4 years) |

| Adoption Of Advanced EPS and Telematics | +0.7% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Demand For Low-Noise E-ATVs | +0.4% | Global, concentrated in media production hubs | Short term (≤ 2 years) |

| Nordic Trail-Maintenance Subsidies | +0.3% | Nordic countries, spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In Outdoor Recreational Tourism

Outdoor recreation contributed USD 1.2 trillion to U.S. GDP in 2024, equal to 2.3% of national output and supporting multiple jobs. Participation increased, spurring ATV and UTV purchases for trail riding and overlanding. In 2024, motorcycling and ATVing generated a large share of value-added economic output, underscoring strong demand in the off-road vehicle market. State grant programs amplify the effect: Colorado’s Outdoor Recreation Fund distributed a massive amount to access projects, while Oregon’s matching grants nurtured rural manufacturing clusters. Trail systems create powerful spillovers; Minnesota's snowmobile network generates significant annual tourism revenue, reinforcing the sector's multiplier effect on local economies and stabilizing seasonal vehicle sales.

Tactical ATV/UTV Procurement By Defense Forces

Defense agencies seek light mobility assets for border patrol, special operations, and logistics in difficult terrain. India’s upcoming northern-border tender specifies helicopter-sling capability, four-seat layouts, and autonomous navigation options to maximize tactical flexibility. Europe’s FAMOUS program, coordinated by Finland, focuses on Arctic operability with vehicles tolerating –46 °C start-up and amphibious functionality for thaw periods. The United States allocates some amount annually to acquire Ultra-Light Combat Vehicles with 4,500-pound curb-weight caps and 250-mile range requirements. Such multi-program momentum encourages vendors to develop modular chassis that accept armor kits, counter-drone sensors, and hybrid powertrains, strengthening order backlogs despite civilian cyclical swings.

Rapid Mechanization Of Midsize Farms

Midsize farms increasingly adopt utility ATVs and UTVs to bridge labor gaps and improve field efficiency. Real-Time Kinematic GPS steering modules now retrofit 250-500 cc platforms, enabling centimeter-level accuracy for seeding and spraying that was once limited to large tractors. Attachment ecosystems have multiplied, with mini-harrows, aerators, and sprayers expanding the functional envelope of mid-displacement engines. As precision-agriculture platforms integrate telematics, farm managers gain remote diagnostics and usage analytics, extending asset life cycles and lowering total cost of ownership. The trend is particularly pronounced in India, Brazil, and Thailand, where fragmented landholdings make compact vehicles more economic than full-sized machinery.

Adoption Of Advanced EPS & Telematics

New-generation digital power steering systems integrate electronic torque sensors and brushless motors that reduce driver fatigue while allowing programmable steering feel across terrain modes. Electro-hydraulic designs replace bulky hydraulic links with lightweight wiring, cutting steering effort by up to two-fifth and trimming cabin noise to enhance comfort on long rides. Parallel advances in telematics mirror long-haul trucking: CAN-bus connectivity delivers real-time performance dashboards, predictive maintenance alerts, and geofencing for fleet operators. OEMs already embed radar-based collision avoidance and automatic emergency braking, aligning off-road safety standards with on-road commercial requirements and widening acceptance among institutional buyers such as energy utilities and emergency services.

Restraints Impact Analysis of Off-road Vehicle Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront and Lifecycle Costs | -1.1% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Lithium Supply-Chain Crunch | -0.9% | Global, acute in battery-dependent regions | Medium term (2-4 years) |

| Rising Injury-Related Regulations | -0.8% | Global, strictest in EU and developed markets | Short term (≤ 2 years) |

| Conservation-Area Usage Bans | -0.6% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lithium Supply-Chain Crunch For E-Powertrains

China currently refines more than three-fifths of global lithium and fabricates four-fifths of batteries, creating exposure for global OEMs as demand surges. The United States allocated funding under the Inflation Reduction Act for domestic processing, but permitting hurdles and community concerns are delaying mine openings. Electro-chemical extraction startups promise lower-impact solutions yet remain pre-commercial. Until diversified supply materializes, battery prices may remain volatile, constraining the total-cost parity that accelerates electric ATV adoption, particularly in price-sensitive developing markets.

Rising Injury-Related Regulations & Speed Caps

After a series of high-profile accidents, regulators worldwide imposed tighter speed governors, revised helmet standards, and mandatory rider safety training. The European Union simultaneously layered Stage V emission ceilings on non-road engines, requiring expensive after-treatment systems in segments above 19 kW. California’s Advanced Clean Fleets rules introduce transitional compliance phases obligating zero-emission options in dealer fleets, complicating inventory management for OEMs. Complying with diverse regional rulebooks elevates homologation costs and lengthens development cycles, temporarily damping new-model launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Off-road Vehicle Market Segment Analysis

By Vehicle Type:

UTV Leadership with Electric MomentumUTVs and side-by-sides captured 50.68% of the off-road vehicle market share in 2025 by blending passenger capacity, cargo utility, and suspension sophistication. The segment reached a robust level of off-road vehicle market size, buoyed by recreation, agriculture, and defense orders. Electric UTV derivatives now post the fastest 8.32% CAGR as OEMs introduce 15 kWh battery packs delivering 80 km/h top speed and sub-3-hour recharge cycles.

Demand for all-terrain vehicles (ATVs) remains robust in regions with strict width restrictions that favor narrower chassis. In contrast, niche demand for amphibious and snowmobile platforms persists where climatic extremes prevail. Competitive differentiation hinges on adjustable suspension, Polaris’s DYNAMIX live valve architecture, and cabin digitization through touchscreen ride-command systems. The vehicle-type portfolio, therefore, balances legacy ICE volumes against emerging electric growth vectors, enabling OEMs to hedge against propulsion uncertainty.

By Application:

Recreation Dominance Amid Military UpswingSports and recreation account for 41.05% of the off-road vehicle market in 2025, benefiting from record trail participation as millions of Americans venture outdoors. Military and law enforcement demand will escalate at an 8.35% CAGR as procurement agencies seek light tactical mobility with helicopter-sling compatibility and hybrid silent-watch modes.

Agriculture and forestry absorb mid-displacement UTVs outfitted with PTO-driven implements, while construction firms requisition high-payload units for remote-site logistics. Emerging tourism concepts such as guided overlanding expeditions further widen commercial use cases. Multi-role adaptability, therefore, sustains baseline volumes even when consumer discretionary spending dips.

By Propulsion Type:

ICE Holds Ground, Electric Gains PaceInternal-combustion engines commanded 83.05% of the off-road vehicle market share in 2025, backed by ubiquitous fueling infrastructure and mature supply chains. Battery-electric models, however, record the steepest 8.30% CAGR, reflecting policy push and falling cell costs.

Hybrid range-extender concepts bridge customer anxiety by pairing 10 kWh packs with compact generators, extending runtime without compromising low-speed torque. Hydrogen fuel-cell prototypes remain R&D efforts but signal pathways for heavy-duty rescue fleets requiring rapid cold-weather refueling. Propulsion diversification mitigates regulatory risks while inviting new supplier ecosystems around battery leasing and recycling.

By Engine Displacement:

Mid-Range Sweet Spot, High-End GrowthEngines from 400 cc to 800 cc represented 44.78% of off-road vehicle market share in 2025, favored for balanced torque and weight that suits mixed recreational and utility roles. Units above 800 cc post the highest 8.37% CAGR through 2031, powered by performance enthusiasts and commercial operators hauling heavier payloads or towing trail groomers.

Sub-400 cc machines preserve entry-level affordability, sustaining channel throughput for dealerships and cultivating new rider cohorts. The displacement hierarchy is gradually disrupted by electric powertrains measured in kilowatts rather than cubic centimeters, compelling OEMs to reframe marketing narratives around torque curves and modular battery capacities.

By Power Output:

Premiumization Drives High-kW DemandPlatforms in the 50-100 kW bracket comprised 38.29% of the off-road vehicle market size in 2025 as they adequately address most consumer adventure and light-commercial requirements. Vehicles delivering more than 100 kW exhibit an 8.44% CAGR, supported by affluent buyers prioritizing acceleration, hill-climb capability, and accessory power for winches or HVAC cabins.

Sub-50 kW offerings remain vital for youth training, rental fleets, and cost-sensitive rural users. Electric drivetrains allow selectable power modes that let owners downrate output for novice riders, expanding household addressability and improving resale value by accommodating diverse skill levels.

By Drive Type:

AWD Dominance Reinforced by Electronic Torque VectoringAWD and 4WD systems held 78.25% of the off-road vehicle market share in 2025, reflecting user expectations for all-terrain confidence across mud, snow, and rock scenarios. Next-generation drivetrains incorporate electronic limited-slip differentials and predictive traction algorithms that adjust torque split within milliseconds, enhancing fuel economy and battery range while minimizing wheelspin damage to sensitive trails.

Two-wheel drive persists in flat agricultural fields and budget-constrained segments but loses share as OEMs standardize selectable 4WD across mid-tier trims. Due to simplified components and shared parts bins, the long-term cost of ownership narrows between 2WD and 4WD units, ensuring AWD remains the default choice for multipurpose buyers.

By Seating Capacity:

Group Experiences Propel Multi-Passenger UptakeTwo-rider units retained 51.72% of the off-road vehicle market share in 2025, capitalizing on couples and guide-client pairings. Vehicles configured for three or more occupants, however, grow at an 8.47% CAGR by appealing to families and tour operators emphasizing shared experiences.

OEMs differentiate with modular bench seats, fold-flat cargo beds, and integrated child-seat anchors that broaden demographic reach. Multi-passenger cabins open ancillary sales of roof racks, infotainment, and climate-control options, lifting average transaction prices while distributing vehicle costs across group adventures.

Geography Analysis

North America Off-road Vehicle Market

North America secured 37.84% of off-road vehicle market share in 2025, underpinned by the outdoor recreation GDP contribution and extensive trail networks subsidized by state grants. Snowbelt states invested huge amount annually in grooming programs that stimulated in tourism receipts, while Wisconsin and Alaska reimbursed 100% of eligible trail maintenance costs, anchoring steady demand even during economic slowdowns. Dealer financing partnerships, such as Sheffield Financial’s renewal with Polaris, ease credit access for buyers and sustain showroom turnover. Nevertheless, conservation-area restrictions across Canadian provinces introduce operational complexity, nudging OEMs to supply quieter powertrains and emission-compliant engines to satisfy permitting criteria.

APAC Off-road Vehicle Market

Asia-Pacific delivers the fastest 8.42% CAGR through 2031 as urbanizing middle-class consumers embrace outdoor lifestyle brands and governments fund rural connectivity. India’s ATV sales grew drastically which was supported by adventure-tourism marketing and agricultural mechanization drives. Regional OEMs such as CFMOTO leverage vertically integrated supply chains to offer competitive pricing, enabling them to capture export contracts and reach two-fifth global market share.

Europe Off-road Vehicle Market

Europe’s growth lags but regulatory thrust aligns with electrification imperatives. Stage V emission norms for non-road machinery elevate R&D spending on after-treatment and alternative powertrains, indirectly spurring innovation in hybrid and fuel-cell concepts. New NRMM rules effective 2028 set small-series thresholds of 70 units, granting boutique electric startups manageable certification pathways. Nordic countries deploy long-run trail-maintenance subsidies to catalyze tourism, a template that Germany and Austria now evaluate for alpine regions. Consequently, although compliance burdens restrain short-term volumes, long-term demand will pivot toward low-emission models, allowing European suppliers to recoup investments through premium pricing.

Competitive Landscape

The sector displays moderate fragmentation, with the top five players, including Polaris, BRP, Yamaha, Honda, and Arctic Cat, commanding notable combined off-road vehicle market share. Revenue volatility hit incumbents in 2024: Polaris slipped slightly in the past years, while BRP reported a one-fifth sales decline and a four-fifth net-income drop, reflecting inventory normalization after pandemic pull-forward demand. Cost-competitive challengers from China and Taiwan gain ground by bundling accessories and extending warranties, forcing legacy brands to accelerate electrification and connected-services rollouts[1]“Q3 2024 Investor Presentation,” BRP Inc., brp.com.

Technology investment differentiates leaders; Polaris scales its DYNAMIX active-suspension, whereas BRP integrates Smart-Shox adaptive damping to widen ride-comfort gaps. Yamaha leverages its motorsports pedigree to introduce clutch-less transmissions and drive-by-wire throttle maps, improving novice accessibility. Patents underscore innovation focus: Cummins’ energy-management system balances hybrid power delivery to run winches and HVAC without straining battery reserves, appealing to fleet operators in utilities and mining[2]“Energy Management and Vehicle Accessory Control System Patent US 12043241 B2,” United States Patent and Trademark Office, uspto.gov .

Strategic alliances proliferate: Synchrony Financial renewed a multi-year agreement with BRP to furnish retail loans, while Hitachi supplies electronic control units enabling over-the-air software upgrades that unlock paid performance modes. These partnerships shift revenue models toward service subscriptions that smooth unit-sales cyclicality. Electric specialists such as Volcon and Segway address white-space niches like drone cinematography with near-silent powertrains, nibbling at premium margins and pressing incumbents to launch EV sub-brands or joint ventures with battery makers.

Off-road Vehicle Industry Leaders

Arctic Cat Inc.

Bombardier Recreational Products Inc.

Honda Motor Co. Ltd

Polaris Inc.

Yamaha Motor Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Off-road Vehicle Market Companies Covered in this Report

- Polaris Inc.

- Bombardier Recreational Products Inc. (Can-Am)

- Yamaha Motor Corp.

- Textron Inc. (Arctic Cat)

- Kawasaki Heavy Industries Ltd.

- Suzuki Motor Corp.

- Honda Motor Co. Ltd.

- CFMOTO Powersports Inc.

- Kwang Yang Motor Co. Ltd. (Kymco)

- American LandMaster

- Tracker Off-Road (Bass Pro Shops)

- Kubota Corp. (RTV)

- John Deere (Gator)

- Mahindra & Mahindra Ltd.

- Segway Powersports

- Hisun Motors Corp.

- Linhai Group

- TGB (Taiwan Golden Bee)

- DRR USA

Recent Industry Developments in Off-road Vehicle Market

- April 2025: Sheffield Financial and Polaris Inc. extended their retail financing partnership, upgrading dealer pre-qualification tools to accelerate approvals on new and pre-owned Polaris products.

- March 2025: Polaris Inc. unveiled its 2026 snowmobile lineup, adding Voyageur work-and-play models, limited-edition PRO RMK trims, and an expanded TITAN series, with SnowCheck customization running through March 2025.

Global Off-road Vehicle Market Report Scope

Off-road vehicles are specially designed vehicles used for driving on rugged roads and off-highway applications. The vehicles provide improved traction, durability, and power output compared to regular vehicles. Off-road vehicles have a wide range of users across agriculture, mining, construction, and other sectors.

The off-road vehicle market is segmented by vehicle type, application, and geography. Based on the vehicle type, the market is segmented into utility task vehicles (UTV) and all-terrain vehicles (ATV). Based on the application type, the market is segmented into sports, agricultural, and other applications. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. The market size and forecast for each segment have been calculated based on value (USD billion).

Segmentation Overview

| All-Terrain Vehicles (ATV) |

| Utility Task Vehicles (UTV) / Side-by-Sides |

| Dirt / Off-road Motorcycles |

| Snowmobiles |

| Amphibious & Specialty ORVs |

| Sports & Recreation |

| Agriculture & Forestry |

| Industrial & Construction |

| Military & Law-Enforcement |

| Other Commercial (tourism, search-and-rescue) |

| Internal-Combustion (Gasoline / Diesel) |

| Hybrid |

| Battery-Electric |

| Hydrogen Fuel-Cell |

| Less than 400 cc |

| 400 – 800 cc |

| More than 800 cc |

| Less than 50 kW |

| 50 – 100 kW |

| More than 100 kW |

| 2-Wheel Drive |

| 4-Wheel / All-Wheel Drive |

| 1 Rider |

| 2 Riders |

| More than or equal to 3 Passengers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | All-Terrain Vehicles (ATV) | |

| Utility Task Vehicles (UTV) / Side-by-Sides | ||

| Dirt / Off-road Motorcycles | ||

| Snowmobiles | ||

| Amphibious & Specialty ORVs | ||

| By Application | Sports & Recreation | |

| Agriculture & Forestry | ||

| Industrial & Construction | ||

| Military & Law-Enforcement | ||

| Other Commercial (tourism, search-and-rescue) | ||

| By Propulsion Type | Internal-Combustion (Gasoline / Diesel) | |

| Hybrid | ||

| Battery-Electric | ||

| Hydrogen Fuel-Cell | ||

| By Engine Displacement (cc) | Less than 400 cc | |

| 400 – 800 cc | ||

| More than 800 cc | ||

| By Power Output (kW) | Less than 50 kW | |

| 50 – 100 kW | ||

| More than 100 kW | ||

| By Drive Type | 2-Wheel Drive | |

| 4-Wheel / All-Wheel Drive | ||

| By Seating Capacity | 1 Rider | |

| 2 Riders | ||

| More than or equal to 3 Passengers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What growth rate is expected for off-road vehicle demand through 2031?

Unit revenue is projected to climb at an 8.28% CAGR, taking global value from USD 24.33 billion in 2026 to USD 36.25 billion by 2031.

Which vehicle class currently leads global sales?

UTV/Side-by-Sides hold 50.68% of 2025 volume due to their blend of passenger capacity and cargo utility.

How quickly are electric off-road models growing?

Battery-electric variants will outpace the broader field with an 8.30% CAGR to 2031, supported by regulation and falling battery costs.

Why is Asia-Pacific the fastest-expanding region?

Rising disposable income, adventure-tourism promotion, and farm mechanization spur Asia-Pacific sales, producing an 8.42% CAGR through 2031.

What factors add pressure to traditional engine suppliers?

Stage V emission rules, lithium supply constraints, and widening safety regulations all heighten compliance costs and hasten propulsion diversification.

Page last updated on: