Outboard Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

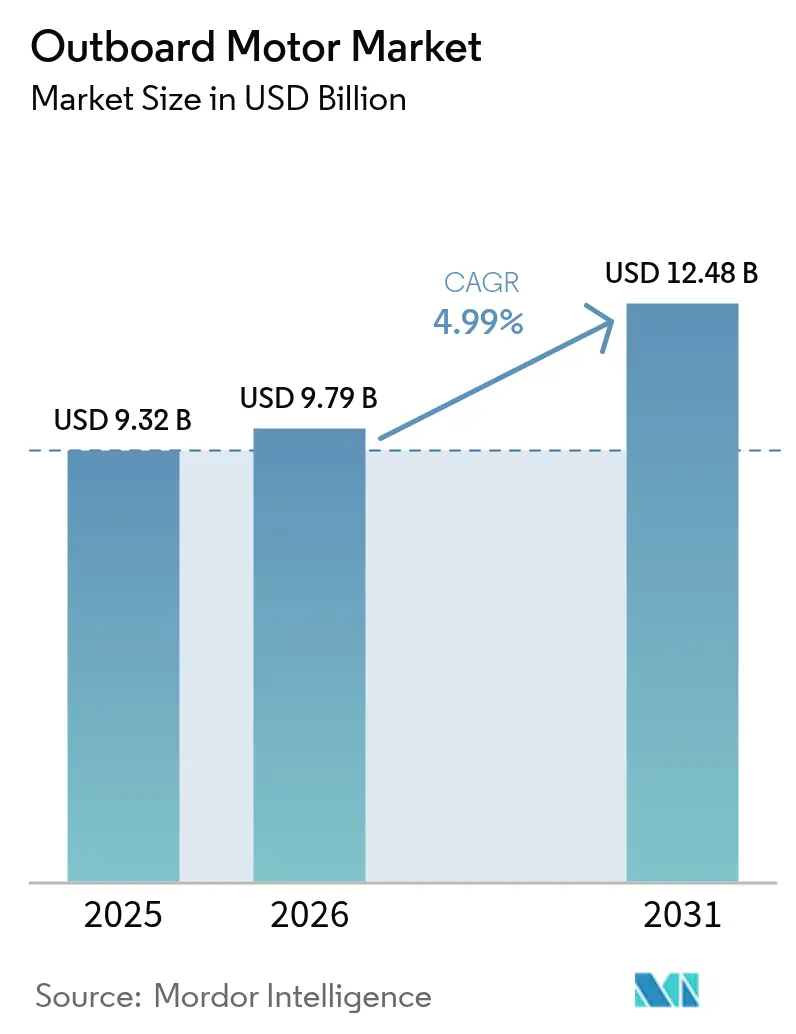

| Market Size (2026) | USD 9.79 Billion |

| Market Size (2031) | USD 12.48 Billion |

| Growth Rate (2026 - 2031) | 4.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outboard Motor Market Analysis by Mordor Intelligence

Outboard Motor Market size in 2026 is estimated at USD 9.79 billion, growing from 2025 value of USD 9.32 billion with 2031 projections showing USD 12.48 billion, growing at 4.99% CAGR over 2026-2031. Growth is sustained by an enlarged base of post-pandemic first-time boat owners who now drive recurring replacement and upgrade cycles, the enduring popularity of mid-range gasoline models for performance craft, and rapid innovation in clean-propulsion alternatives that attract regulatory incentives and eco-conscious consumers. Supply-chain measures undertaken since 2024—such as vertical integration into aluminum boat production and multisourcing of electronics—are gradually easing cost volatility, enabling manufacturers to protect margins even as input prices fluctuate. Meanwhile, tightening emissions standards in the United States and the European Union favor advanced four-stroke and electric powertrains, pushing research spending toward low-emission and alternative-fuel platforms. Competitive pressure intensifies as electric specialists expand into higher-horsepower brackets once dominated by internal-combustion incumbents, further segmenting the outboard motors market by performance, price, and environmental profile.

Key Report Takeaways

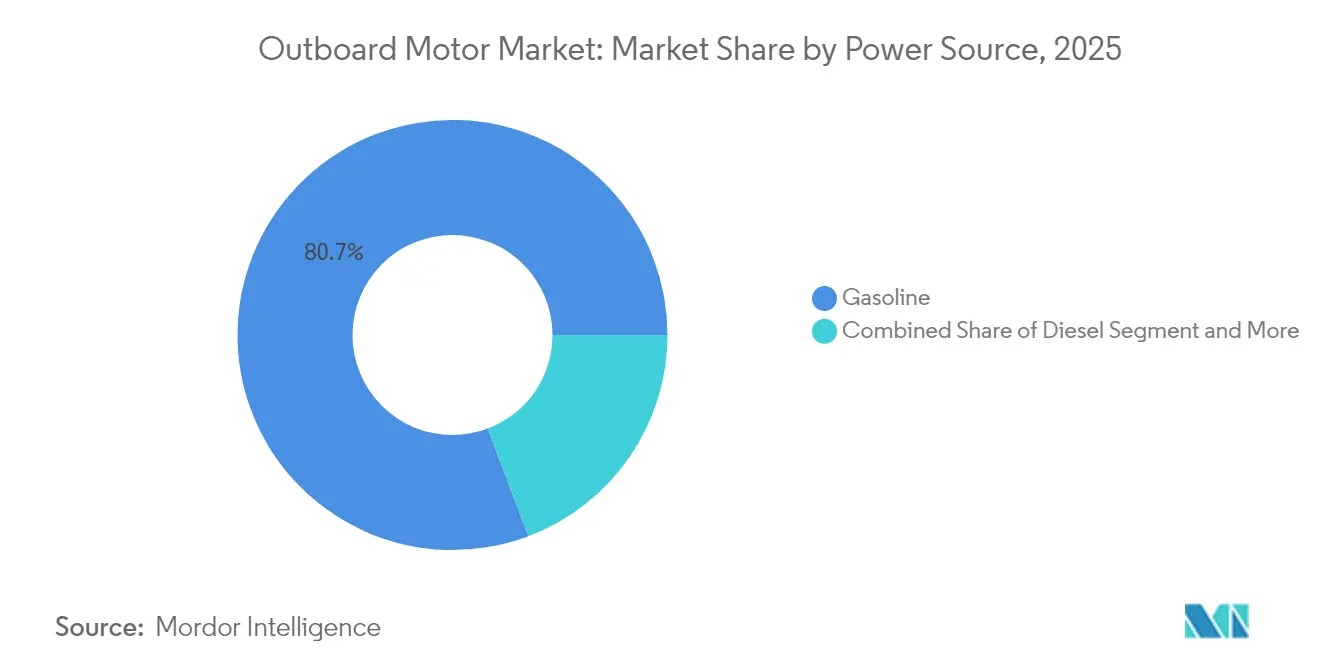

- By power source, gasoline engines held 80.74% of the outboard motors market share in 2025, while electric units are projected to advance at a 5.02% CAGR during the forecast period (2026-2031).

- By application type, recreational boating accounted for 75.68% of the outboard motors market size in 2025; commercial fleets segment is expected to grow at a 5.16% CAGR during the forecast period (2026-2031).

- By thrust class, the 26-150 hp mid-range segment commanded 52.96% of the outboard motors market share in 2025, whereas portable units below 25 hp segment is expected to grow at a 5.08% CAGR during the forecast period (2026-2031).

- By horsepower range, 100-199 hp models represented 35.55% of the outboard motors market size in 2025; sub-30 hp engines are forecast to expand at a 5.20% CAGR during the forecast period (2026-2031).

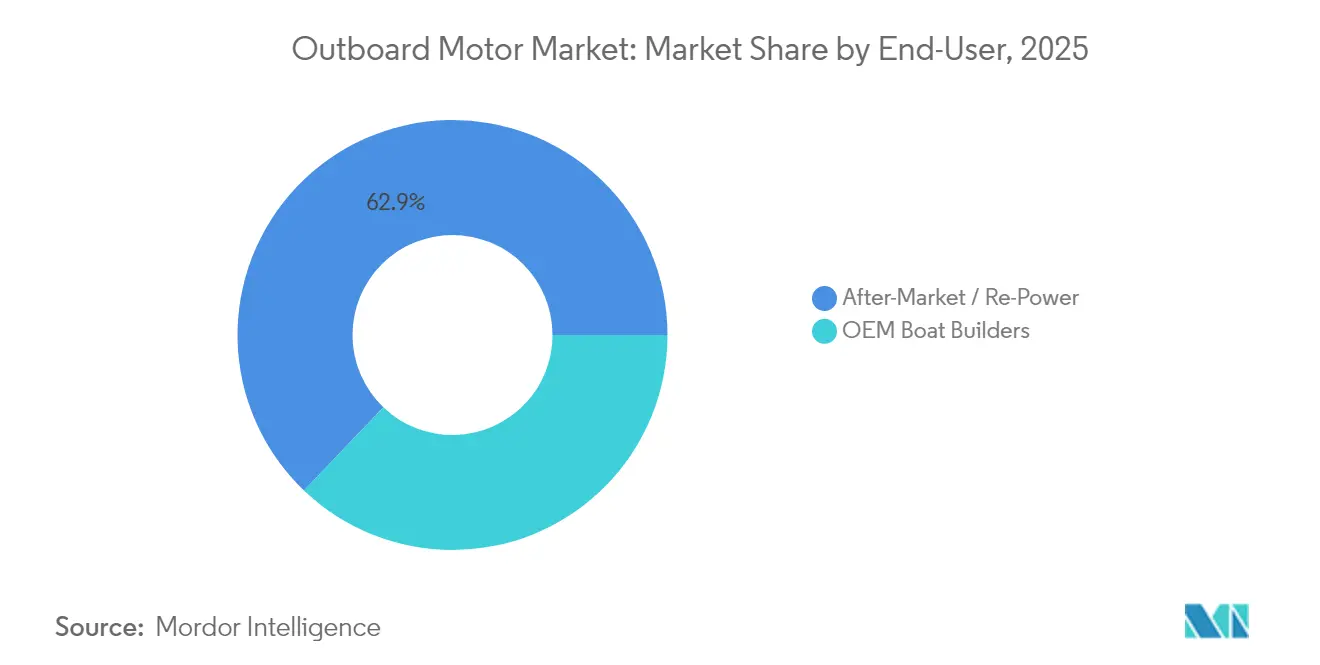

- By end-user, re-power and aftermarket channels captured 62.86% share of the outboard motors market size in 2025, while OEM boat builders segment is expected to grow at a 5.11% CAGR during the forecast period (2026-2031).

- By sales channel, direct marine dealers retained a 67.44% share in 2025; pure-play online platforms led channel segment is expected to grow at a 5.22% CAGR during the forecast period (2026-2031).

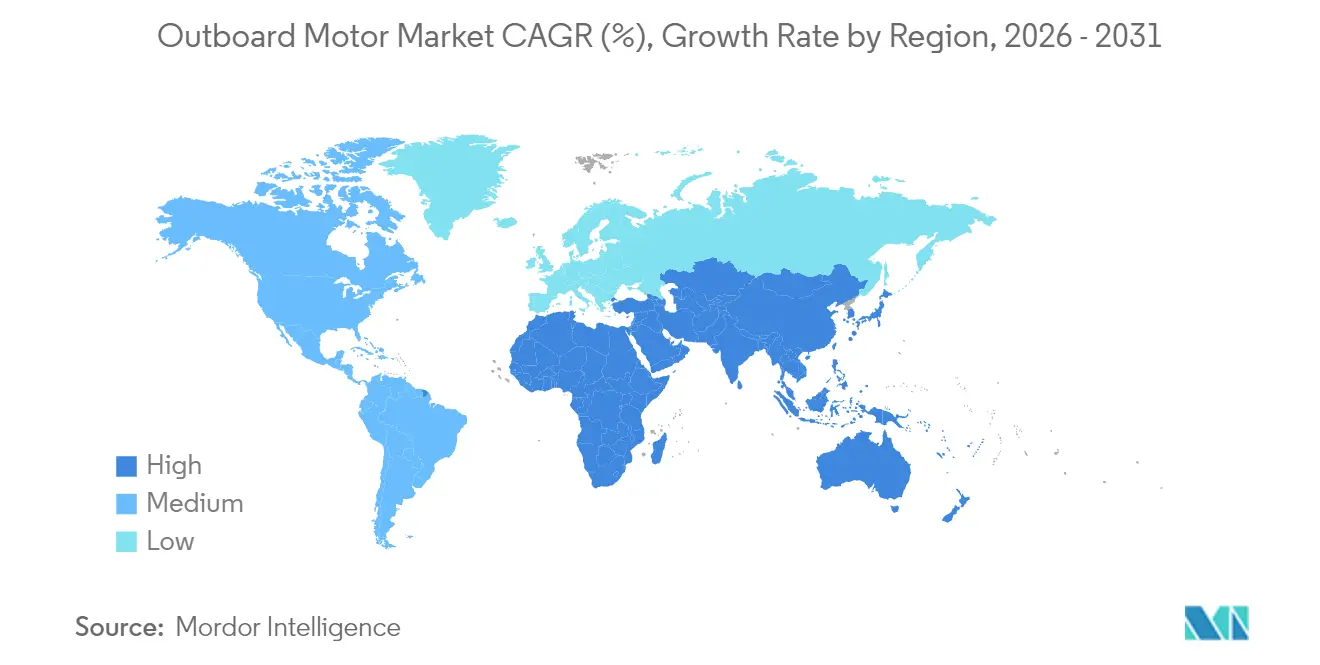

- By geography, North America led with 38.32% outboard motors market share in 2025, whereas Asia-Pacific is expected to grow at a CAGR of 5.13% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outboard Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged Boom In First-Time Boat Ownership | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Surge In High-Horse-Power | +0.8% | North America and Australia, spill-over to MEA | Long term (≥ 4 years) |

| Regulatory Pivot Toward Four-Stroke Efficiency | +0.7% | North America and EU, early adoption in Asia Pacific | Medium term (2-4 years) |

| Commercial Patrol Agencies | +0.4% | Global, with early gains in North America, EU, Australia | Long term (≥ 4 years) |

| Carbon-Credit-Funded Electrification | +0.3% | California, Singapore, EU ports | Short term (≤ 2 years) |

| Pilot Roll-Out Of Sustainable Drop-In Marine Fuels | +0.2% | UK, California, Texas with planned expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Boom in post-COVID first-time boat ownership

New entrants who bought their first boats in 2020–2021 continue to underpin replacement demand within the outboard motors market as they trade up from entry-level craft to higher-horsepower models. U.S. monthly new-boat sales jumped exponentially from April to May 2020, and retention surveys show that most of these owners remain active, with many planning propulsion upgrades within five years[1]“U.S. Recreational Boating Statistical Abstract 2025,” National Marine Manufacturers Association, nmma.org . Manufacturers target this cohort with bundled re-power packages and financing incentives, locking in lifetime customer value as owners repeatedly revisit dealerships for bigger engines, smart controls, and fuel-efficient technologies.

High-horsepower (>300 hp) re-powering of offshore craft

Offshore anglers and charter operators increasingly install triple or quad 300-plus-hp outboards—such as Mercury Marine’s 5.7 L V10 Verado—on existing hulls to achieve automobile-like acceleration without purchasing new boats. Retrofits often cost two-fifth less than a new hull yet deliver comparable top-speed gains, making re-powering a high-margin growth pocket for engine makers[2]“Verado® 5.7L V10 Outboard,” Mercury Marine, mercurymarine.com .

Regulatory shift toward four-stroke efficiency

The U.S. EPA Tier III Spark-Ignition rule and EU Stage V requirements are phasing out carbureted two-stroke models, steering the outboard motors market toward cleaner four-stroke platforms that cut fuel burn by one-fourth and slash particulate emissions[3]“Emission Standards for Spark-Ignition Marine Engines,” U.S. Environmental Protection Agency, epa.gov . Compliance timetables create predictable decommissioning cycles, encouraging owners to adopt digitally controlled four-strokes that boost resale values.

Commercial patrol agencies are adopting low-sulfur diesel outboards

Coast guards and law-enforcement fleets worldwide are specifying diesel outboards for range and torque advantages on long patrol routes. Low-sulfur diesel pricing and existing supply infrastructure shorten payback periods relative to gasoline engines, while recent 200-hp diesel launches deliver gasoline-like power-to-weight ratios that ease platform transition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Progressive Tightening Of Stage V / EPA SI Emission Limits | -0.6% | EU and North America, spreading to Asia Pacific | Medium term (2-4 years) |

| Supply-Chain Volatility In Aluminium & Electronics | -0.4% | Global, acute in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Rare-Earth Dependency | -0.3% | Global, concentrated in electric segment | Long term (≥ 4 years) |

| Dealer-Network Consolidation | -0.2% | North America and Europe, rural markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Stage V / EPA SI emissions limits

Stricter caps on NOx, CO, and fine particulates mean small manufacturers must invest in costly catalytic after-treatment or exit regulated markets. Mid-range engine brackets are most exposed because consumers resist significant price increases, eroding volume growth until compliance solutions become cost-neutral.

Volatility in aluminum & electronics supply

Aluminum prices spiked more than one-fifth in 2024, while global microcontroller shortages stretched outboard lead times to six months, squeezing mid-range profitability where substitution is limited. Yamaha’s purchase of Australian boatbuilder Telwater typifies the vertical-integration strategy to secure metal supply and hedge currency swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Gasoline Dominance Faces Electric Disruption

Gasoline outboards represented 80.74% of the outboard motors market share in 2025, translating into the largest single revenue pool within the outboard motors market size. Four-stroke designs now reach 300-plus hp brackets with slimmer gearcases and digital-shift systems that meet EPA Stage III limits, sustaining loyalty among offshore anglers and performance cruisers. Manufacturers cross-promote aftermarket propeller kits and joystick controls to lift lifecycle value and keep internal-combustion engines relevant during the energy transition.

Electric propulsion is pacing the power-source growth leaderboard at 5.02% CAGR, propelled by harbor-craft mandates and carbon-credit financing programs on both coasts of the United States. Torqeedo’s 50 kW Deep Blue and Yamaha’s 48 V HARMO platform illustrate how quiet, instant-torque solutions win over marinas with strict noise and emission bylaws. Battery swap stations and floating solar charging pontoons reduce range anxiety for rental fleets. This demonstrates that well-defined duty cycles like coach boats and short-haul water taxis can go fully electric without operational penalties.

By Application Type: Recreational Volume, Commercial Margin

Recreational boating consumed 75.68% of the outboard motors market size in 2025 after new-boat sales spiked during the 2020 lockdowns. OEMs bundle color-matched cowlings, touchscreen helm displays, and plug-and-play mobile apps to upsell lifestyle buyers who value seamless user experiences. Subscription-based maintenance plans and extended warranties convert recreational owners into predictable annuity streams for dealers.

Commercial fleets, including patrol, fishing, charter, and aquaculture, are expanding faster at a 5.16% CAGR. Their total-cost-of-ownership equations favor fuel-sipping four-strokes and diesel models that minimize downtime. Governments tap stimulus budgets to modernize enforcement craft, while large-scale fish farms electrify auxiliary tenders to meet sustainability targets. As a result, per-unit ASPs in commercial channels run one-fourth above the recreational average, powering top-line growth even at lower volumes.

By Thrust Class: Mid-Range Core, Portable Upside

The 26-150 hp mid-range bracket delivered 52.96% outboard motors market share in 2025 because it matches the power needs of pontoons, bowriders, and near-shore fishing boats that populate marinas worldwide. OEMs have refreshed this category with lean-burn mapping, variable intake geometry, and microelectronic oil sensors, squeezing one-tenth better fuel economy since 2023 while holding sticker prices flat in real terms.

Portable units at or below 25 hp will post a 5.08% CAGR thanks to electrification tailwinds, lighter composite lower units, and tourism adoption in protected lakes where combustion is banned. Suitcase-style battery packs enable renters to carry power sources home for overnight charging, sidestepping dockside infrastructure constraints. Manufacturers bundle accessories such as foldable transom brackets and Bluetooth engine telemetry to differentiate offerings in a crowded field.

By Horse-Power Range: 100-199 hp Sweet Spot

Engines rated 100-199 hp accounted for 35.55% of the outboard motors market size in 2025, powering popular 20-to 24-foot craft across both salt and freshwater segments. This sweet spot balances purchase cost, towing weight, and fuel economy, making it the preferred upgrade path for first-time owners moving off entry-level rigs.

Sub-30 hp units will accelerate at 5.20% CAGR as sailing schools, coach boats, and rental fleets electrify. Motor-battery packages now weigh 28% less than their 2022 predecessors yet deliver around one-fifth greater thrust, eroding gasoline’s weight advantage. Conversely, 300-plus-hp behemoths will remain niche but lucrative, buoyed by luxury center-console builders catering to triple-engine configurations that top 70 mph.

By End-User: After-Market Rules the Dock

Re-power and aftermarket sales controlled 62.86% of the outboard motors market share in 2025, reflecting the 25-year average hull life that encourages propulsion upgrades every 7-10 years. Dealers stage “re-power weekends” offering on-site financing and trade-in credits, enabling owners to switch from obsolete two-strokes to fuel-injected four-strokes without changing boats.

OEM installations sold with new hulls will grow quicker at 5.11% CAGR as builders pre-rig integrated digital helm suites and joystick docking. Partnerships between engine makers and boat brands (e.g., Brunswick’s Sea Ray lines with factory-installed Mercury joystick systems) increase switching costs, anchoring long-term platform loyalty.

By Sales Channel: Dealer Dominance Meets Digital Surge

Brick-and-mortar marine dealers accounted for 67.44% of 2025 engine revenue due to the complexity of rigging, warranty activation, and periodic maintenance. Outboard motors market participants incentivize certified service training and parts stocking to uphold brand reputation and preserve resale value.

Online pure-plays and marketplace platforms will expand at a 5.22% CAGR by catering to DIY owners buying sub-20 hp kickers, propellers, and ECU upgrade kits. Flexible fulfillment, ship-to-store, curbside pickup, or dockside drone delivery, attracts tech-savvy boaters, although high-horsepower installations remain dealership territory due to liability and calibration requirements.

Geography Analysis

North America held 38.32% of the outboard motors market share in 2025, anchored by the United States’ multiple registered boats and a mature marina network that promoted high utilization. EPA clean-air regulations prompt rapid turnover of carbureted two-strokes, and state noise rules in Florida, California, and Minnesota accelerate four-stroke adoption. Dealer consolidation yields regional super-stores capable of stocking every power class and offering mobile service units that keep downtime low during peak summer months.

Asia-Pacific is set to record the highest regional CAGR at 5.13% through 2031, propelled by rising middle-class disposable income in China, India, Thailand, and Indonesia. Governments in Vietnam and the Philippines are modernizing artisanal fishing fleets with durable mid-range four-strokes to comply with new coastal-emission codes, creating sizeable replacement cycles. Domestic manufacturers in China supply more minor portable electrics, yet imported Japanese and American brands dominate 100-plus-hp brackets due to performance reputation.

Europe remains a high-value, regulation-led arena where Stage V emissions have already eliminated legacy two-strokes on most inland waterways. Scandinavian lake districts are pilot zones for HVO fueling docks that let existing four-stroke fleets cut CO2 output by up to four-fifth. At the same time, Amsterdam and Venice canals enforce zero-emission mandates favoring rim-drive electric motors. Southern Europe’s charter sector rebounds strongly post-pandemic, renewing fleets with joystick-controlled twin outboards rated 150-200 hp, lifting unit ASPs across the region.

Competitive Landscape

Legacy leaders—Brunswick (Mercury Marine), Yamaha, Suzuki, and Honda—continue to frame the outboard motors industry narrative by combining scale manufacturing with proprietary ECU software and global dealer footprints. Mercury’s 2025 launch of the V10 Verado series added 350–400 hp coverage without increasing block width, underscoring incremental innovation strategies that protect share in the high-horsepower category. Yamaha broadened its electric reach by rolling out the 48 V HARMO system and acquiring equity stakes in battery integrators, signaling that incumbents will not cede clean-propulsion turf.

Disruptors such as Torqeedo, Vision Marine Technologies, and Pure Watercraft target niche beachheads where electric advantages outweigh range constraints, then scale upward in power. Vision Marine’s 180 hp E-Motion package shattered acceleration records at the 2024 Lake of the Ozarks shootout, proving battery-driven speed is feasible in mainstream runabouts. Early-stage players focusing on hydrogen or ammonia combustion provide optionality in zero-carbon road maps, though infrastructure remains nascent.

Strategic moves emphasize ecosystem control: Mercury’s SmartCraft Connect API now interfaces with 40 third-party apps, while Yamaha’s Helm Master EX joystick system integrates autopilot and GPS anchor functions. Suppliers pursue vertical integration, illustrated by Suzuki’s in-house fuel-injector plant and Honda’s in-house block casting, to secure component availability amid geopolitical trade risk. Partnerships with marina operators on fast-charge infrastructure or HVO supply broaden non-engine revenue pools.

Outboard Motor Industry Leaders

Yamaha Motor Co. Ltd

Honda Marine

Suzuki Motor Corporation

Tohatsu Corporation

Brunswick Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Yamaha introduced the HARMO electric rim-drive outboard equivalent to 9.9 hp gasoline, offered with 20-inch and 25-inch shafts and modular lithium packs.

- February 2025: Honda Marine refreshed its BF115/BF140/BF150 inline trio and BF200/BF225/BF250 V6 lineup, citing enhanced corrosion resistance and 2% fuel-burn improvement in cruising rpm.

- November 2024: Suzuki relaunched its V6 200 hp model with redesigned lower unit and electronic throttle-and-shift, promising 12% better hole-shot performance versus the 2022 version.

Global Outboard Motor Market Report Scope

An outboard motor is a type of boat propulsion system that is one of the most common motorized methods of propelling watercraft. Unlike inboard motors, this type of motor is intended to be installed on the outside of the transom or outside the boat, allowing for more space in the interior. Outboard motors have many advantages, including a high horsepower-to-weight ratio, ease of installation and maintenance, and extended maintenance intervals.

The outboard motor market is segmented by application type (commercial and recreational), thrust (portable, mid-range, and high power), and geography (North America, Europe, Asia-Pacific, and the Rest of the World). The report offers market size and forecasts for the market studied in value (USD ) for all the above segments.

| Gasoline |

| Diesel |

| Electric |

| Hybrid / Propane / LPG |

| Recreational |

| Commercial |

| Portable |

| Mid-range |

| High-power |

| Less than 30 hp |

| 30–99 hp |

| 100–199 hp |

| 200–299 hp |

| More than or equal to 300 hp |

| OEM Boat Builders |

| After-Market / Re-Power |

| Direct Marine Dealer |

| Online Pure-Play |

| Boat-OEM Integrated |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Mexico | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Power Source | Gasoline | |

| Diesel | ||

| Electric | ||

| Hybrid / Propane / LPG | ||

| By Application Type | Recreational | |

| Commercial | ||

| By Thrust Class | Portable | |

| Mid-range | ||

| High-power | ||

| By Horse-Power Range | Less than 30 hp | |

| 30–99 hp | ||

| 100–199 hp | ||

| 200–299 hp | ||

| More than or equal to 300 hp | ||

| By End-User | OEM Boat Builders | |

| After-Market / Re-Power | ||

| By Sales Channel | Direct Marine Dealer | |

| Online Pure-Play | ||

| Boat-OEM Integrated | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Mexico | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the outboard motors sector and its projected growth rate?

The sector is valued at USD 9.79 billion in 2026 and is forecast to rise to USD 12.48 billion by 2031, reflecting a 4.99% compound annual growth rate.

Which power source is expanding fastest in outboard propulsion?

Electric outboards are leading growth at a 5.02% CAGR through 2031, helped by zero-emission mandates and carbon-credit funding for coach and harbor craft.

Which region is expected to add the most incremental demand over the next five years?

Asia-Pacific is projected to post the strongest regional expansion at a 5.13% CAGR, driven by rising middle-class recreation spending and fishing-fleet upgrades.

What horsepower range currently generates the highest unit volume?

Engines rated 100-199 hp hold the largest share at 35.55%, fitting the power needs of popular 20- to 24-foot leisure craft.

How concentrated is supplier competition in this space?

The combined share of the top five brands, Brunswick’s Mercury, Yamaha, Suzuki, Honda, and Torqeedo, sits near three-fifth of the share, indicating moderate concentration with room for disruptors.

What are the main factors encouraging owners to replace existing engines?

Stricter Stage V/EPA emissions rules, the desire for better fuel economy, and cost-effective re-powering of offshore craft are prompting many boat owners to upgrade from older two-stroke models to modern four-stroke or electric alternatives.

Page last updated on: