Advanced Driver Assistance Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

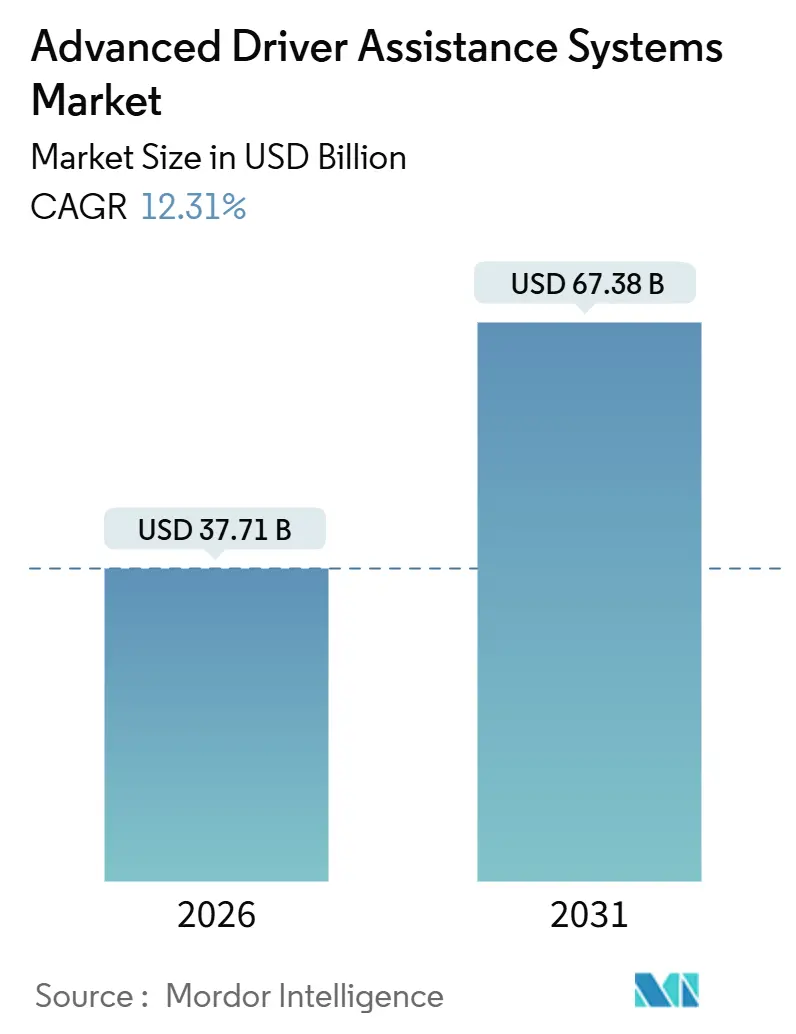

| Market Size (2026) | USD 37.71 Billion |

| Market Size (2031) | USD 67.38 Billion |

| Growth Rate (2026 - 2031) | 12.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Driver Assistance Systems Market Analysis by Mordor Intelligence

The Advanced Driver Assistance Systems Market size is estimated at USD 37.71 billion in 2026, and is expected to reach USD 67.38 billion by 2031, at a CAGR of 12.31% during the forecast period (2026-2031). Buoyant growth reflects converging safety regulations, rapid sensor-cost deflation, and software-defined vehicle architectures that let automakers unlock subscription revenue long after delivery. Level 2+ feature bundling is moving down-segment as AI-based sensor fusion curbs hardware redundancy, while rising SUV and premium-car demand in emerging economies widens the total addressable pool for the advanced driver assistance system market. North American insurance-telematics discounts, Euro NCAP’s Safe Driving domain, and China’s C-NCAP alignment accelerate mandatory fitment, forcing OEMs to standardize automatic emergency braking, lane-keeping assist, and pedestrian detection. Competitive intensity remains high as Tier-1 suppliers vie for domain-controller contracts and semiconductor partners battle for design wins in the compute stack.

Key Report Takeaways

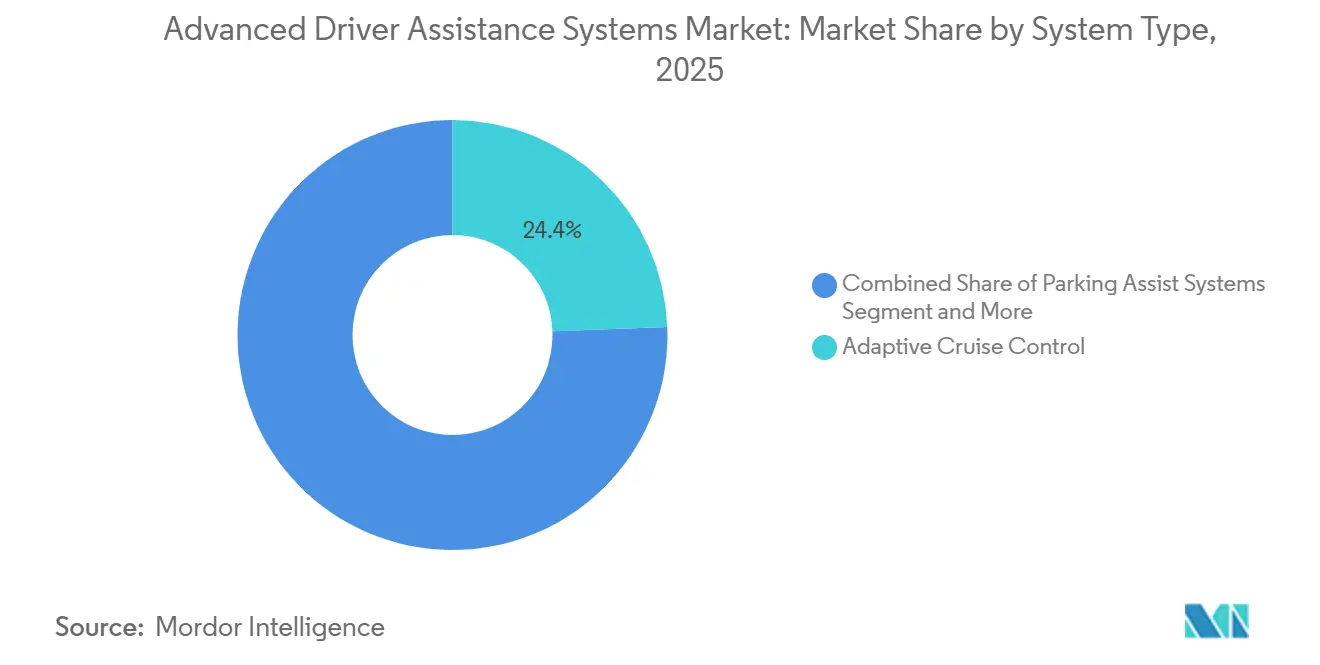

- By system type, adaptive cruise control led with 24.41% revenue share in 2025, while automatic emergency braking is advancing at a 12.3% CAGR through 2031.

- By sensor type, radar captured 45.54% share of the advanced driver assistance system market size in 2025 and LiDAR is projected to expand at a 12.41% CAGR to 2031.

- By vehicle type, passenger cars accounted for 73.37% of deployments in 2025 and two-wheelers are growing at 12.45% annually to 2031.

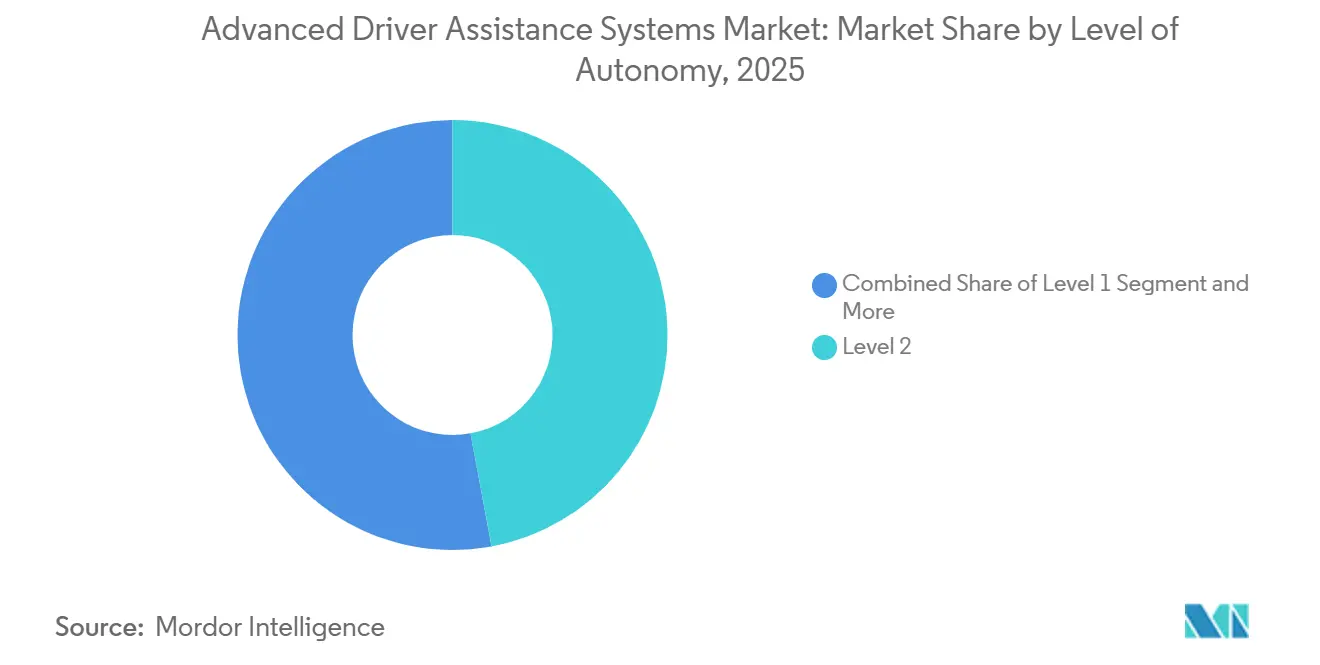

- By level of autonomy, Level 2 commanded 47.13% share in 2025, whereas Level 3 is the fastest-growing layer with a 12.37% CAGR to 2031.

- By sales channel, OEM-fitted systems held 87.73% share in 2025 and the aftermarket retrofit segment is set to post a 12.47% CAGR through 2031.

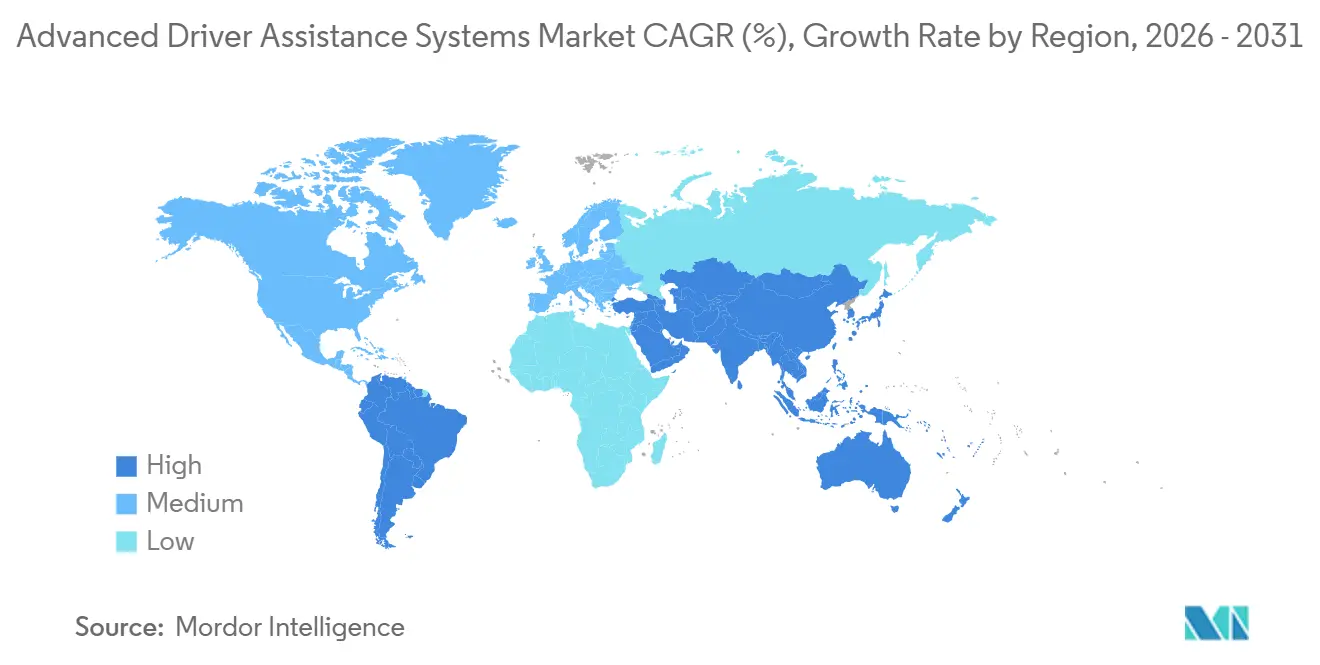

- By geography, North America led with 38.71% share in 2025, while Asia Pacific is the fastest climber at a 12.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Driver Assistance Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Safety Mandates | +3.2% | Global, with North America and EU leading enforcement | Short term (≤ 2 years) |

| AI-Based Sensor Fusion Enabling L2+ Feature Bundling | +2.8% | Global, Asia Pacific core with rapid adoption in China, Japan, South Korea | Medium term (2-4 years) |

| Rapid Sensor-Cost Deflation | +2.5% | Global, particularly Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| SDV/OTA Architectures Unlocking Post-Sale Revenue | +2.1% | North America and EU premium segments, expanding to Asia Pacific | Medium term (2-4 years) |

| Growing SUV & Premium-Car Penetration | +1.4% | Asia Pacific (China, India), Middle East, South America | Long term (≥ 4 years) |

| Usage-Based Insurance Discounts | +0.8% | North America, Western Europe, with pilot programs in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Safety Mandates Compress Adoption Timelines

Regulators now hard-code ADAS functions into star-rating and type-approval rules, eliminating voluntary loopholes that once slowed uptake. NHTSA’s 2024 update requires automatic emergency braking with pedestrian detection on every new passenger vehicle sold in the United States, while Euro NCAP’s “Safe Driving” domain forces infrared driver-monitoring cameras into even entry-level trims [1]“NHSTA Roadmap (NCAP),” NHSTA, www.nhtsa.gov . China’s C-NCAP aligns with these benchmarks, mandating lane-keeping assist and traffic-sign recognition for five-star status. The result is an elevated baseline that removes basic safety as a differentiation lever, steering competition toward richer Level 2+ packages that boost the advanced driver assistance system market.

AI-Based Sensor Fusion Unlocks Level 2+ Bundles

Machine-learning models trained on millions of driving hours fuse radar, LiDAR, and camera data into a 360-degree scene more robust than any single sensor can deliver. NVIDIA’s DRIVE Orin and Mobileye’s SuperVision illustrate how compute density supports highway hands-off capability, automated lane changes, and self-parking. These bundles migrate into mid-range vehicles as hardware costs fall, generating recurring subscription fees that enlarge revenue per unit within the advanced driver assistance system market [2]“The world leader in accelerated computing,” NVIDIA Investor Presentation, investor.nvidia.com.

Rapid Sensor-Cost Deflation Broadens Access

LiDAR units dropped below USD 500 in 2025 as Chinese suppliers scaled solid-state production, while 4D imaging radar fell to USD 150 per module. Eight-megapixel cameras with LED-flicker suppression enhance perception without adding redundant hardware. Lower bills of material let mass-market sedans and fleet retrofits justify payback in three years, expanding the total pool for the advanced driver assistance system market.

SDV and OTA Architectures Create Post-Sale Upside

Software-defined vehicles decouple hardware cycles from feature launches, allowing OEMs to activate dormant sensors via secure over-the-air updates. Volkswagen, Hyundai, and Volvo now monetize adaptive front-lighting or traffic-jam assist months after delivery, smoothing cash flow while keeping owners engaged. Compliance with UNECE R155 cybersecurity norms ensures secure boot and encrypted payloads, further de-risking the advanced driver assistance system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Lidar/Radar System Cost | -1.8% | Global, with acute impact in price-sensitive Asia Pacific and South America markets | Short term (≤ 2 years) |

| Functional Limitations in Poor Weather & Lighting | -1.3% | Northern Europe, North America (snow/fog regions), monsoon-affected Asia Pacific | Medium term (2-4 years) |

| mmWave Chipset & Substrate Supply Bottlenecks | -1.1% | Global, concentrated in semiconductor fab regions (Taiwan, South Korea, Japan) | Short term (≤ 2 years) |

| Cybersecurity Liability & Data Privacy Risk | -0.9% | EU (GDPR enforcement), North America (state-level privacy laws) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Sensor Cost Restricts Entry-Level Adoption

Despite recent price drops, a high-end LiDAR system significantly increases the cost of a sedan, making it challenging to adopt in countries like India, Brazil, and Indonesia, where car prices are considerably lower. Similarly, imaging radar adds a notable expense, restricting its application to premium car trims. The issue is even more pronounced for two-wheelers, where the cost of radar technology represents a substantial portion of the vehicle's price, further slowing its adoption in the advanced driver assistance system market.

Poor-Weather Performance Constrains Operational Domains

LiDAR range collapses from 200 meters to under 50 meters in heavy rain, while cameras suffer at dawn, dusk, or in snow glare. Radar maintains range but cannot resolve fine details, making multimodal fusion essential yet imperfect. Level 3 features such as Mercedes-Benz Drive Pilot disengage in precipitation, curbing real-world utility and dampening user confidence in the advanced driver assistance system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Regulatory Momentum Lifts AEB Leadership

Automatic emergency braking recorded the fastest 12.33% CAGR outlook to 2031 as global rules convert it into mandatory equipment, underscoring its centrality to the advanced driver assistance system market. Adaptive cruise control retained a 24.41% share in 2025 because advanced control and handling improvements uplift the driving experience.

Parking-assist suites that blend ultrasonic sensors with surround-view cameras gain traction amid urban congestion, while blind-spot detection and lane-departure warning commoditize into entry trims. Night vision, traffic-sign recognition, and driver drowsiness alert linger at niche volumes as higher sensor costs and limited consumer awareness cap early uptake. Forward-collision warning subsumes into AEB packages, reducing standalone demand but strengthening system bundling across the advanced driver assistance system market.

By Sensor Type: Radar Dominates, LiDAR Scales Up

Radar sensors averaged 45.54% of the advanced driver assistance system market share in 2025 owing to their all-weather reliability and mid-range affordability. LiDAR boasts a 12.41% CAGR to 2031 after Chinese suppliers pushed unit prices below USD 500, fueling Level 2+ deployment in mid-segment sedans.

Cameras occupy mid-30s revenue share as 8-megapixel imagers replace legacy units, raising low-light detection quality without prohibitive cost. Ultrasonic sensors remain relegated to parking assist and face substitution by compact radars. Infrared remains niche, reserved for night-vision and driver-monitoring applications in luxury vehicles. Multisensor fusion therefore defines the procurement roadmap as OEMs demand integrated suites that simplify calibration and shorten validation cycles in the advanced driver assistance system market.

By Level of Autonomy: Level 3 Secures Regulatory Traction

Level 2 systems delivered 47.13% of volume in 2025, anchoring the mainstream user experience for the advanced driver assistance system market. Level 3 autonomy grows at 12.37% CAGR through 2031 on the back of approvals in Germany, Japan, and select U.S. states that now endorse conditional automation on limited road segments.

Real-world usage remains bounded by daylight and weather restrictions, yet OEM road-maps reveal expansion to 130 kilometers per hour speed caps and broader route coverage. Level 1 retains relevance for price-sensitive trims, while Level 4 and Level 5 stay in pilot fleets such as Waymo and Cruise. Harmonized rules under UNECE R157 provide a regulatory floor that should widen Level 3 operating envelopes and extend penetration across the advanced driver assistance system market.

By Vehicle Type: Two-Wheelers Spark New Growth Pools

Passenger cars claimed 73.37% of global deployments in 2025, reflecting mature supply chains and mandatory fitment in core markets. Two-wheelers, however, are projected to post a 12.45% CAGR as radar-based blind-spot detection tailored for motorcycles proliferates in dense Asian cities.

India’s and Indonesia’s volume motorcycle segments adopt collision warning due to USD 200 radar modules that deliver insurance savings inside three years. Heavy trucks and buses adopt ADAS for fleet-insurance rebates, yet fragmented ownership slows total uptake. As regulations converge on motorcycle ADAS, suppliers anticipate a vast tailwind that diversifies revenue across the advanced driver assistance system market.

By Sales Channel: Retrofit Solutions Court Fleets

OEM factory installs captured 87.73% share in 2025 because integrated harnesses ease calibration and deliver optimal sensor placement. The aftermarket retrofit channel will nonetheless log a 12.47% CAGR through 2031 as commercial operators retrofit aging fleets to unlock usage-based insurance metrics.

Mobileye’s 8 Connect kit illustrates retrofit traction, but calibration complexity and patchy regulatory acceptance limit scale in passenger vehicles. Standardization work by industry associations aims to codify installation protocols, which would expand channel potential and enlarge the advanced driver assistance system market.

Geography Analysis

North America led with 38.71% of 2025 revenue after NHTSA mandated automatic emergency braking with pedestrian detection on every new passenger car, leading to a swift boost in the advanced driver assistance system market. Furthermore, insurance giants Progressive and State Farm rolled out usage-based insurance schemes, offering enticing premium discounts for vehicles equipped with ADAS. In early 2025, Canada harmonized its regulations with those of the U.S., eliminating homologation hurdles. Coupled with a mature telematics infrastructure, insurers in Canada swiftly capitalized on monetizing safety data.

Asia Pacific will post the fastest 12.39% CAGR through 2031. This surge is primarily attributed to China, India, and Japan, as they progressively integrate Level 2+ functions into mainstream vehicle segments. China's ambitious directive mandates that by 2027, all new cars must feature adaptive cruise control and traffic-sign recognition. This move potentially impacts a significant portion of the market. Simultaneously, India's Bharat NCAP is urging local manufacturers to adopt electronic stability control and lane-keeping assist as standard features. Japan's endorsement of Level 3 expressway driving further solidifies this regulatory momentum, expanding the market horizons for advanced driver assistance systems.

In 2025, Europe, the Middle East, and Africa collectively accounted for a notable share of the market. This was largely driven by Euro NCAP's 2024 initiative, which emphasized scoring driver-monitoring systems under its Safe Driving domain. In a significant move, Germany greenlit Mercedes-Benz's Drive Pilot, marking the dawn of Level 3 liability frameworks and paving the way for broader OEM introductions. Meanwhile, governments within the Gulf Cooperation Council began enforcing mandates for Automatic Emergency Braking (AEB) and lane-departure warnings on their state fleets starting in 2025. In a forward-looking gesture, Brazil is formulating ADAS requirements set for 2028, hinting at a potential surge from late adopters. Not to be overlooked, Turkey's production hubs are rolling out ADAS at rates comparable to Western Europe, simultaneously exporting components to the expansive advanced driver assistance system market.

Competitive Landscape

Continental, Bosch, DENSO, Aptiv, and ZF, the top five suppliers, collectively dominate a significant portion of the global revenue, indicating a moderate concentration in the advanced driver assistance system market. The competitive edge hinges on sensor-to-software integration, as OEMs lean towards validated stacks that expedite development. Being geographically close to Asia Pacific production hubs is advantageous, especially since this region is a major producer of light vehicles and requires swift engineering responses.

Deal flows are influenced by compute-platform alliances. Collaborations between tier-one suppliers and chip giants like NVIDIA, Mobileye, and Qualcomm bolster domain-controller initiatives, merging numerous legacy ECUs into streamlined zonal architectures. Disruptors such as Hesai and RoboSense have significantly reduced LiDAR prices, securing partnerships with key automotive players. Patent filings indicate a shift towards fail-operational architectures and redundant perception loops, aligning with UNECE R157 and ISO 21434 standards. Suppliers that can't certify cyber-secure OTA pipelines may find themselves sidelined from new vehicle platforms, raising the qualification standards in the advanced driver assistance system market.

Retrofit specialists target commercial fleets, capitalizing on long asset-replacement cycles and insurance incentives that boost ROI. Mobileye leverages crowdsourced REM mapping from a vast number of vehicles to enhance lane precision, establishing a software advantage that counters hardware commoditization. With an increase in Level 3 approvals, established players boasting validated safety stacks and robust cybersecurity will gain market share, while niche players will focus on cost-effective sensor suites tailored for emerging markets in the advanced driver assistance system arena.

Advanced Driver Assistance Systems Industry Leaders

Continental AG

DENSO Corporation

Robert Bosch GmbH

ZF Friedrichshafen AG

Aptiv PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Volkswagen Group, Valeo and Mobileye announced a strategic partnership to deploy Level 2+ ADAS across future MQB vehicles.

- January 2025: Aurora, Continental and NVIDIA formed a long-term alliance to mass-produce driverless truck hardware based on NVIDIA DRIVE Thor.

- December 2024: Neural Propulsion Systems released an AI-powered hyper-definition radar with enhanced object classification.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Advanced Driver Assistance Systems (ADAS) market as the total manufacturer-level revenue generated by electronic systems that use on-board sensors, processors, and software to warn, assist, or temporarily automate driving tasks across passenger cars and commercial vehicles. Systems covered include adaptive cruise control, automatic emergency braking, lane keeping, blind-spot detection, parking aids, driver monitoring, and other SAE Level 1-3 functions delivered as factory fit or certified retrofits.

Scope exclusion: fully autonomous Level 4-5 robo-taxis and pure software simulation tools sold without on-road deployment are outside this market.

Segmentation Overview

- By System Type

- Parking Assist Systems

- Adaptive Front-Lighting

- Night Vision Systems

- Blind-Spot Detection

- Automatic Emergency Braking

- Forward Collision Warning

- Driver Drowsiness Alert

- Traffic Sign Recognition

- Lane Departure Warning

- Adaptive Cruise Control

- By Sensor Type

- Radar

- LiDAR

- Camera

- Ultrasonic

- Infra-red

- By Vehicle Type

- Two-Wheelers

- Passenger Cars

- Medium and Heavy Commercial Vehicles

- By Level of Autonomy

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

- By Sales Channel

- OEM-Fitted

- Aftermarket Retrofit

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Tier-1 module engineers, ADAS product managers at five global OEMs, regional dealer groups, and vehicle inspection centers across North America, Europe, China, India, and Brazil. These discussions clarified typical take-rate ladders, average selling prices, sensor supply tightness, and regulatory certification timelines, validating and adjusting insights from secondary work.

Desk Research

We began with public data from transport safety regulators such as NHTSA, Euro NCAP, and China's MIIT, traffic crash databases, tariff-coded sensor trade flows from UN Comtrade, and production volumes from OICA. Analyst access to D&B Hoovers, Dow Jones Factiva, and WSTS provided company revenue splits, design wins, and semiconductor shipment clues, which were then matched with quarterly filings and investor decks. Academic papers and patents retrieved through Questel helped us benchmark radar range gains and LiDAR cost curves that shape future penetration rates. The sources named are illustrative only; many additional documents fed our desk analysis.

Market-Sizing & Forecasting

A top-down build starts with light-vehicle production, commercial-vehicle registrations, and parc renewal, which are multiplied by verified ADAS fitment ratios and calibrated ASP bands. Supplier roll-ups and sampled dealer channel checks provide a bottom-up sense check before totals are locked. Key variables include: 1) Euro GSR-II safety mandate phase-in calendar, 2) LiDAR unit price compression, 3) sensor fusion content per vehicle, 4) regional SUV share shifts, and 5) semiconductor lead-time trends. Multivariate regression with scenario analysis projects each driver to 2030; expert consensus then benchmarks the base, high, and low cases. Gaps in bottom-up data are bridged through weighted regional proxies and homologation-linked adoption lags.

Data Validation & Update Cycle

Outputs pass anomaly, variance, and currency checks, followed by peer review and senior analyst sign-off. Reports refresh annually, with mid-cycle updates if new safety laws, major recalls, or technology cost shocks alter the baseline. A final pre-delivery sweep ensures clients receive the latest view.

Why Mordor's Advanced Driver Assistance Systems (ADAS) Baseline Earns Decision-Makers' Confidence

Published ADAS values often differ because firms pick unequal system bundles, apply distinct ASP trajectories, or freeze exchange rates at different points.

Key gap drivers we observe include omission of aftermarket retrofits, over-optimistic LiDAR price drops, or single-region refresh cycles, whereas Mordor captures global OEM and certified retrofit flows, uses live currency feeds, and revisits variables every twelve months.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 38.54 B (2025) | Mordor Intelligence | - |

| USD 37.46 B (2025) | Global Consultancy A | Limited retrofit coverage and static ASP ladder |

| USD 42.90 B (2024) | Industry Journal B | Uses production forecast only; no in-service fleet adjustment |

| USD 47.76 B (2025) | Regional Consultancy C | Assumes accelerated LiDAR penetration without cost validation |

The comparison shows that while other publishers swing high or low depending on narrower scopes or aggressive component assumptions, Mordor delivers a balanced, transparent baseline grounded in verifiable production, fitment, and pricing evidence clients can trace and reproduce.

Key Questions Answered in the Report

What was the worldwide advanced driver assistance system market size in 2025?

It reached USD 35.24 billion in 2025 and is forecast to grow to USD 67.38 billion by 2031.

Which region led ADAS revenue in 2025?

North America accounted for 38.71% of total revenue, driven by mandatory automatic emergency braking and insurance-telematics discounts.

Which ADAS system type shows the fastest growth to 2031?

Automatic emergency braking is projected to rise at a 12.33% CAGR through 2031.

How fast will Level 3 autonomy expand?

Level 3 functions are set to advance at a 12.37% CAGR as Germany, Japan, and select U.S. states approve conditional automation.

Why is LiDAR adoption accelerating?

Chinese suppliers cut unit prices below USD 500, enabling solid-state LiDAR deployment in mid-segment sedans and boosting a 12.41% CAGR for the sensor segment.

What drives aftermarket retrofit demand?

Commercial fleets retrofit older vehicles to qualify for usage-based insurance savings, pushing the retrofit channel toward a 12.47% CAGR through 2031.

Page last updated on: