Middle East and Africa HCM Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

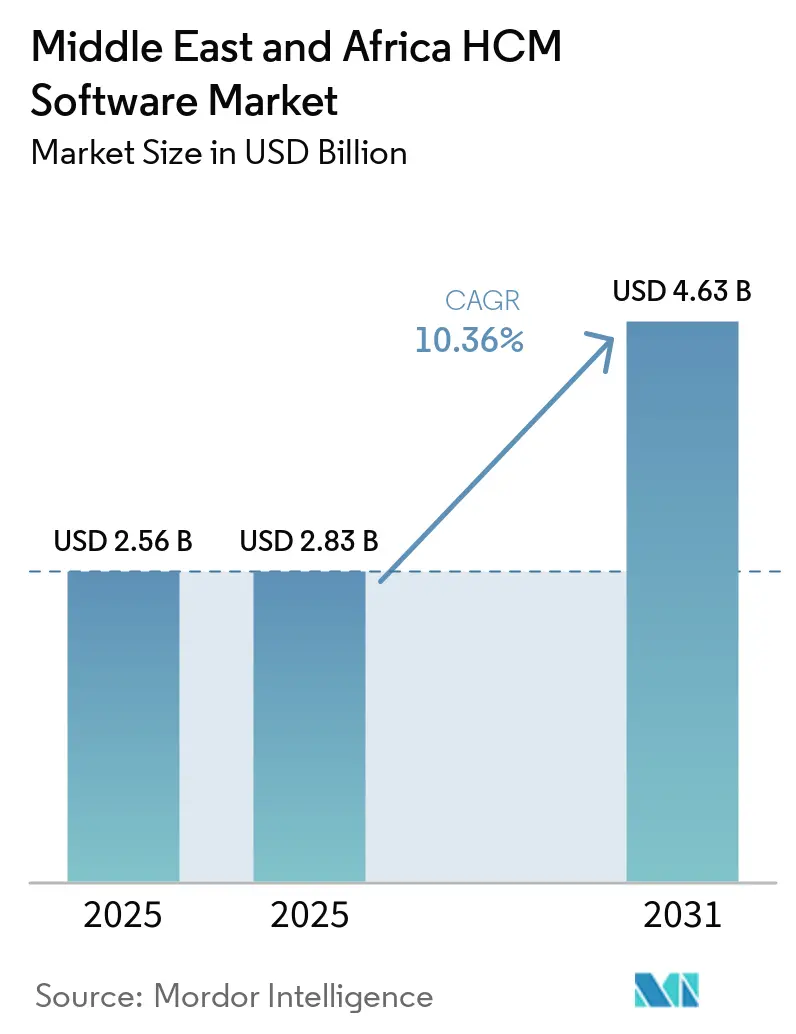

| Base Year Market Size (2025) | USD 2.56 Billion |

| Market Size (2025) | USD 2.83 Billion |

| Market Size (2031) | USD 4.63 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

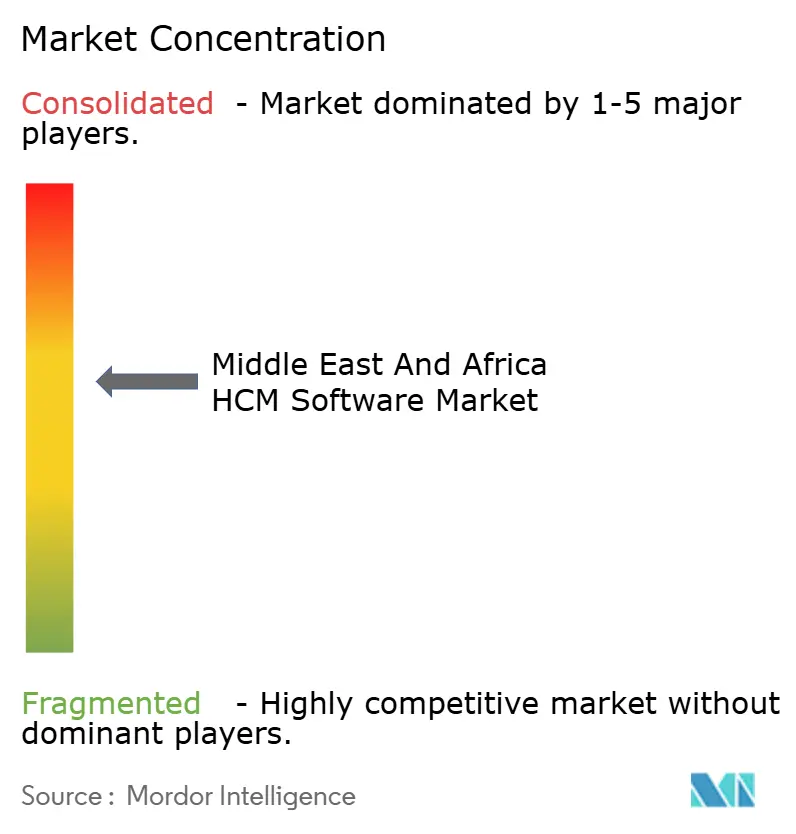

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa HCM Software Market Analysis by Mordor Intelligence

The Middle East and Africa HCM Software market size is projected to expand from USD 2.56 billion in 2025 to USD 2.83 billion in 2026 and USD 4.63 billion by 2031, registering a CAGR of 10.36% between 2026 and 2031. Strong sovereign digital-government programs, wage-protection mandates, and fintech-enabled payroll rails are accelerating the replacement of spreadsheets and on-premises HR databases with unified, cloud-native suites. Vendors that can embed local payroll rules, Arabic interfaces, and biometric attendance capture are growing fastest as employers seek a single system of record that can satisfy Gulf nationalization quotas and African social security enrollment requirements. Hyperscaler data center investments are lowering latency and allaying data residency concerns, yet intermittent grid power means many buyers still demand hybrid architectures. The competitive field remains moderately concentrated because global enterprise-resource-planning incumbents continue to cross-sell HCM, while regional specialists win mid-market accounts through deeper localization.

Key Report Takeaways

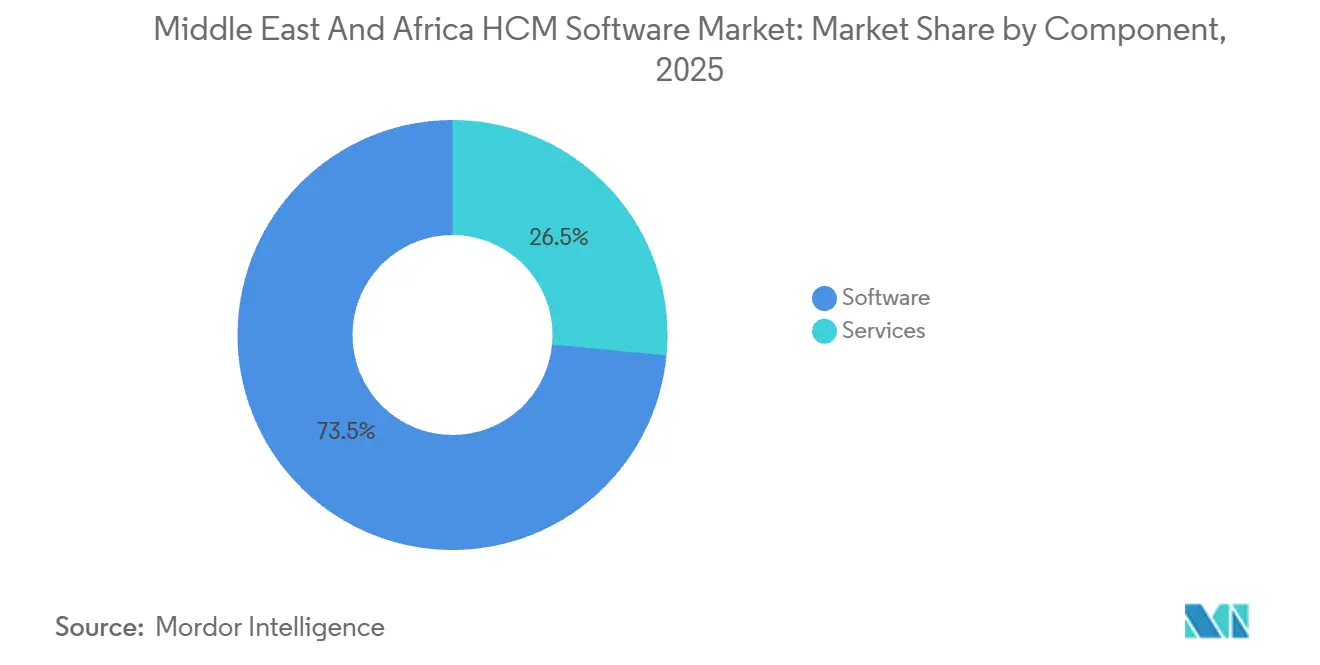

- By component, software accounted for 73.48% of 2025 spending in the Middle East and Africa HCM software market, while services are forecast to grow at a 11.24% CAGR through 2031.

- By deployment mode, cloud deployment accounted for 68.92% of 2025 revenue in the Middle East and Africa HCM software market and is projected to expand at a 11.56% CAGR through 2031.

- By organization size, large enterprises accounted for 64.81% of 2025 expenditure, but small and medium enterprises are forecast to expand at 11.72% through 2031.

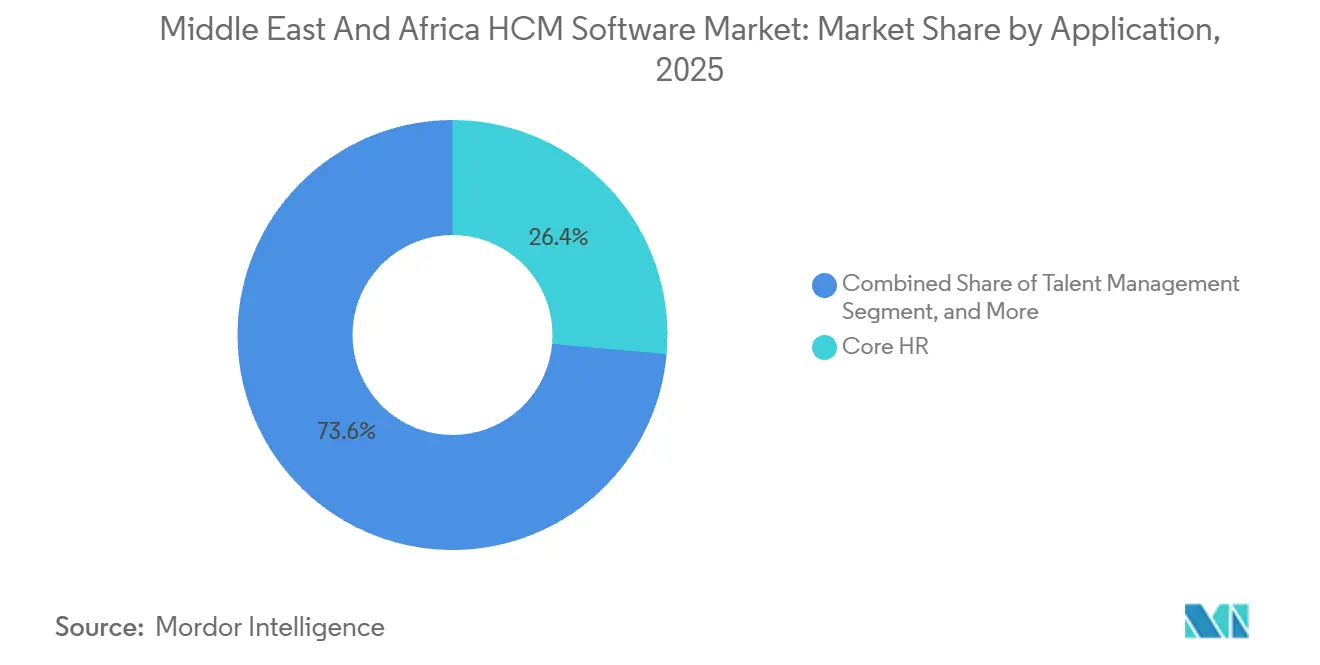

- By application, core HR led with a 2025 share of 26.42%, whereas talent management is forecast to advance at 12.08% over the forecast period.

- By end-user industry, BFSI accounted for 25.87% of 2025 revenue, yet healthcare and life sciences are projected to post the highest segment CAGR of 11.94% on the back of stringent license-tracking requirements.

- By geography, the Middle East captured 61.24% of 2025 value, while Africa is forecast to grow at 11.88% as donor-funded civil-service reforms and fintech payroll rails catalyze first-time adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa HCM Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Cloud Adoption Across GCC Enterprises | +2.8% | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman | Medium term (2-4 years) |

| Regulatory Push for Wage Protection and Compliance Automation | +2.4% | Gulf Cooperation Council core, spillover to Egypt and Jordan | Short term (≤ 2 years) |

| Growing Demand for Workforce Analytics and AI-Powered Insights | +1.9% | Saudi Arabia, United Arab Emirates, South Africa, Kenya | Medium term (2-4 years) |

| Rising Mobile and Remote Workforce Requiring Unified HCM Platforms | +1.6% | Nigeria, Kenya, Egypt | Short term (≤ 2 years) |

| Saudi NEOM Mega-Projects Driving Labor-Tracking Digitization Demand | +1.2% | Saudi Arabia, spillover to United Arab Emirates and Qatar | Long term (≥ 4 years) |

| Africa’s Fintech-Led Payroll Infrastructure Leapfrogging Legacy HR Systems | +1.5% | Nigeria, Kenya, South Africa, Ghana, Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Cloud Adoption Across GCC Enterprises

Gulf employers are rapidly modernizing legacy HR databases to meet real-time reporting standards embedded in national transformation plans. Saudi Arabia reached 95% digitization of government services in 2024, and private-sector boards now benchmark against those standards, creating a halo effect for cloud HCM rollouts. The United Arab Emirates integrated its labor-market compliance APIs with private HCM suites, cutting audit cycles from quarterly to monthly and rewarding firms that maintain seamless cloud connectivity.[1]UAE Ministry of Human Resources and Emiratisation, “Wage Protection System 2.0,” mohre.gov.ae Qatar’s Civil Service and Government Development Bureau partnered with SAP SuccessFactors in 2025 for more than 85,000 workers, publishing configuration blueprints that private companies now reuse. Vendors that operate sovereign-cloud nodes inside Saudi Arabia and the United Arab Emirates have shortened sales cycles by reducing data-residency objections. As hyperscaler regions come online, hybrid security policies are easing concerns among banks and utilities, unlocking postponed migrations.

Regulatory Push for Wage Protection and Compliance Automation

Wage-protection frameworks have turned payroll into a mission-critical compliance process. The United Arab Emirates’ Wage Protection System 2.0 obliges employers to transfer salaries within 10 working days through accredited institutions, with hefty fines and work-permit suspensions for repeat breaches. Saudi Arabia’s Mudad platform cross-references payroll with social-insurance and immigration records, delivering 85-90% contract compliance in 2025 and forcing companies to replace siloed HR modules with integrated suites that automatically feed Qiwa. Kuwait now mandates biometric attendance capture, while Oman requires digital contract filings within 30 days of hire, further expanding the compliance footprint that HCM must cover.

Growing Demand for Workforce Analytics and AI-Powered Insights

Nationalization targets, strict overtime rules, and productivity benchmarks are pushing HR from administrative record-keeping to predictive analytics. Saudi Arabia’s Nitaqat program audits expatriate-versus-citizen headcount every quarter, so employers deploy dashboards that forecast quota gaps and simulate hiring scenarios. A leading telecom group reduced voluntary attrition among high-performing Saudi nationals by 12% in the first year after enabling Oracle HCM Cloud predictive models to flag flight-risk employees.[2]Oracle Corporation, “e and Customer Success Story,” oracle.com South African banks apply scheduling algorithms to trim overtime, posting 15% labor-cost savings within 12 months. Kenya’s Teachers Service Commission, interfacing payroll to its iTax network, removed thousands of ghost workers, unlocking donor-funding tranches tied to fiscal transparency. As boardrooms request forward-looking metrics, AI modules in talent pipelines, engagement scores, and absence forecasting become core purchase criteria.

Rising Mobile and Remote Workforce Requiring Unified HCM Platforms

Gig-economy couriers, project-site laborers, and field sales staff rarely sit at desktop browsers, so offline-first mobile HCM has become table stakes. Nigerian logistics and e-commerce firms now issue GPS-enabled attendance apps that time-stamp deliveries and release instant payments through mobile money. Kenya-born platforms cache payroll data locally, then sync when bandwidth returns, addressing the reality that 40% of Sub-Saharan workers face intermittent connectivity. The United Arab Emirates’ construction regulators require biometric punches on remote sites, which wearable-ready HCM apps deliver in real time. Saudi Arabia’s NEOM mega-project relies on a single control tower that consolidates attendance and safety certificates for more than 140,000 workers across multiple contractors. Because mobile use cases stretch across payroll, timekeeping, and benefits enrollment, vendors that architect natively on smartphones are displacing desktop-centric incumbents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Residency Regulations Increasing Deployment Complexity | -1.4% | Saudi Arabia, United Arab Emirates, South Africa, Nigeria | Medium term (2-4 years) |

| Limited Cloud-Skilled Talent Pool in Several African Markets | -1.1% | Sub-Saharan Africa excluding South Africa, North Africa excluding Egypt | Long term (≥ 4 years) |

| Fragmented Arabic Dialects Hindering NLP Adoption in HCM Software | -0.8% | Gulf Cooperation Council, Egypt, North Africa | Long term (≥ 4 years) |

| High Cost of Regional Data-Center Power Impacting SaaS Pricing | -0.9% | Nigeria, Kenya, Egypt, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Residency Regulations Increasing Deployment Complexity

Sovereign data-protection acts oblige vendors to localize employee records, fragmenting what could be a single multi-tenant cloud into jurisdiction-specific instances. The United Arab Emirates maintains a whitelist of data-export mechanisms, extending procurement by up to 6 months as buyers await regulatory clearance.[3]Telecommunications and Digital Government Regulatory Authority, “UAE Data Protection FAQ,” tdra.gov.ae South Africa’s Information Regulator has begun issuing enforcement notices, raising liability concerns that are stalling migrations among conservative banks. Nigeria now requires data-protection impact assessments for high-risk HR processing, a burden that small employers pass through to vendors by demanding turnkey compliance services. The resulting patchwork forces suppliers to maintain multiple infrastructure footprints, inflating the cost of goods sold and slowing roadmap delivery.

Limited Cloud-Skilled Talent Pool in Several African Markets

Strong buyer interest often collides with a shortage of certified administrators who can configure, integrate, and govern cloud HCM platforms. Kenya’s ICT Authority estimated only 12,000 cloud-accredited professionals against a demand four times larger in 2024. Nigeria launched a 100,000-strong upskilling program, yet first-year certification pass rates sat below 20%, extending timelines for mid-market go-lives. Ethiopia’s USD 70 million civil-service reform earmarked one-third of its budget for external integrators after no local firm met the skill threshold, tripling projected labor costs. Because talent scarcities hit small and medium enterprises hardest, vendors increasingly bundle managed services, but that raises the total cost of ownership and dilutes the pure-software margin profile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum as Localization Deepens

Services are forecast to outpace software growth, expanding at an 11.24% CAGR through 2031. The Middle East and Africa HCM Software market is expanding, driven by implementation, integration, and managed services, as every Gulf country integrates payroll with unique pension rules, multi-lingual interfaces, and government gateway connections. Oracle’s 2025 deal with e and embedded a three-year managed-services layer that covers compliance updates for 38 countries, illustrating how vendors lock in annuity streams once core modules go live. Start-ups such as Jisr secure recurring consulting fees by mapping Saudization thresholds into automated dashboards that executives can self-serve. As public-sector grants fund civil-service reforms in Ethiopia and Sierra Leone, local partners gain opportunities to deliver training and change-management work that global vendors do not staff locally.

Software still accounted for 73.48% of 2025 spending, as perpetual-license upgrades and SaaS subscriptions anchor every project. Nevertheless, price pressure intensifies as mid-market buyers weigh open API ecosystems against monolithic suites. Regional challengers bundle attendance scanners, insurance aggregation, and earned-wage access inside a single per-employee fee, prompting large platforms to unbundle specific micro-services to retain agility. Over the forecast window, the share of total services in the Middle East and Africa HCM Software market is expected to reach the low-30% range, confirming that productization alone cannot absorb the region’s localization load.

By Deployment Mode: Hybrid Bridges Sovereignty and Scale

Cloud solutions delivered 68.92% of the 2025 value and are set to grow at an 11.56% CAGR, yet legal and power-grid realities mean purely public architectures are uncommon beyond software-as-a-service talent modules. Buyers in banking and government increasingly opt for split-stack topologies that house payroll on sovereign nodes while pushing analytics to multiregion clouds. The Middle East and Africa HCM Software market share attributed to hybrid deployments will likely climb because Microsoft, Oracle, and SAP now offer region-specific instances that replicate sensitive tables to in-country storage.

On-premises footprints persist, particularly inside ministries that forbid external internet routes, but even these sites adopt containerized orchestration to gain patch automation. Kenya’s suspended data-center project demonstrated that power scarcity can slow hyperscaler rollout, keeping standby diesel-based data rooms in play. Vendors that supply synchronization agents and zero-trust gateways capture wallet share because they let clients toggle between sovereign and public capacity without rewrites.

By Organization Size: SMEs Accelerate Under Regulatory Formalization

Large enterprises held 64.81% of 2025 spending due to multi-country complexity and premium support contracts, yet growth decelerates as refresh cycles lengthen. The Middle East and Africa HCM Software market shows sharper momentum in small and medium enterprises, forecast to rise at 11.72% through 2031 as wage-protection audits and tax digitization compel even 50-person workshops to adopt compliant payroll engines. Nigerian start-ups that integrate pension remittance APIs lower entry costs, while Gulf micro-retailers gravitate toward Arabic mobile interfaces that employees can navigate with minimal training.

Freemium tiers that gate advanced analytics behind paywalls help vendors seed thousands of micro-clients who will up-convert once regulators expand the scope. In East Africa, donor-funded voucher programs reimburse part of the first-year subscription fees to expedite adoption among informal merchants. As a result, SME revenue could exceed one-third of the total Middle East and Africa HCM Software market size by the end of the forecast period.

By Application: Talent Management Emerges as Strategic Battleground

Core HR maintained a 26.42% share in 2025 as the foundational system of record, but talent management is projected to clock the fastest 12.08% CAGR through 2031. Skills shortages and nationalization quotas mean employers can no longer rely solely on job boards; they need AI-driven matching, onboarding, and upskilling loops. Platforms that surface learning paths aligned to Gulf Labor Ministries’ competency frameworks are winning tenders. The Middle East and Africa HCM Software market size allocated to performance and succession suites is therefore expanding faster than to plain payroll engines.

Workforce management and payroll grow roughly in line with the overall market, but innovation centers on predictive scheduling, biometric attendance, and automated compliance reports that feed government dashboards. Learning systems lagged historically, yet Saudi Arabia’s Human Capability Development Program now subsidizes micro-credential content, injecting budget into corporate-learning modules that integrate directly with HCM skill graphs.

By End-User Industry: Healthcare Rises on Credential-Tracking Needs

Banking, financial services, and insurance owned 25.87% of 2025 spending thanks to early ERP adoption, but healthcare and life sciences are forecast to outstrip all sectors with an 11.94% CAGR. Gulf hospitals rely on expatriate clinicians, so they need digital verification of licenses, visas, and continuing-education hours to avoid regulatory fines. An integrated HRMS recently linked Saudi providers with the Saudi Commission for Health Specialties, slashing onboarding from 90 days to 30 days and spotlighting how sector-specific connectors elevate adoption.

As pandemic backlogs push governments to recruit globally, modules that synchronize license status with immigration data move from optional to essential, expanding the Middle East and Africa HCM Software market share attributable to healthcare. Retail, telecom, and manufacturing hover near the market average, propelled by mobile attendance and earned-wage access. Government remains high-value but slow, because multi-year tenders stipulate sovereign-cloud and local implementation depth that only a handful of bidders satisfy.

Geography Analysis

The Middle East accounted for 61.24% of the 2025 value of the Middle East and Africa HCM software market. The Middle East and Africa HCM Software market displays especially strong momentum in Saudi Arabia, where the Qiwa platform processed records for over 13 million workers in 2025, creating a de facto standard for private-sector audits. Saudi Arabia's Microsoft data-center region, launching in Q4 2026 with three availability zones, addresses Personal Data Protection Law requirements and positions the Kingdom as a sovereign-cloud hub for government and financial-services HCM workloads.[4]Microsoft Azure, “Saudi Arabia Cloud Region,” azure.microsoft.com United Arab Emirates construction and hospitality employers, facing biometric time-capture mandates, rushed cloud migrations to avoid wage-protection penalties, lifting software bookings throughout 2025. Qatar’s public-sector showcase of SAP SuccessFactors is influencing private adopters, reinforcing Doha’s position as a reference hub.

Africa, projected at an 11.88% CAGR, exhibits pronounced heterogeneity. South Africa shows high saturation in mines and banks but steady upgrades as firms adopt AI analytics. Nigeria advances on the back of fintech payroll rails that release same-day wages across 40+ countries, a functionality that multinationals now request even for expatriate staff. Egypt is emerging as a regional cloud hub given a pipeline of USD 694 million in data-center capital by 2030, bringing latency-sensitive HR workloads closer to North African and Levantine users. Kenya demonstrates donor-driven adoption as its Teachers Service Commission removed ghost workers via a unified payroll linked to taxation, a model neighboring states plan to replicate.

Infrastructure underpins adoption velocity. Microsoft’s 200-megawatt region scheduled for Q4 2026 in the United Arab Emirates will furnish low-latency endpoints that satisfy cross-border data-transfer rules, while Microsoft’s Riyadh zones let financial institutions meet Saudi residency mandates. Nigeria’s plan to double data-center megawatts by 2030 still battles grid instability, convincing enterprises to specify hybrid failover in tender documents. These supply-side variables dictate deployment mix and thereby shape regional market trajectory.

Competitive Landscape

The Middle East and Africa HCM Software market remains moderately concentrated, with global suites such as Oracle, SAP, Workday, and ADP holding entrenched large-enterprise positions, but localization-first challengers eroding mid-market turf. Oracle’s 2025 rollout for e and embedded AI attrition models and anchored a land-and-expand motion into 38 countries, illustrating how incumbents leverage integrated analytics to secure renewals. SAP’s RISE stack, procured by Qatar’s Civil Service bureau, bundles ERP, analytics, and HCM under one subscription, locking institutions into multi-decade relationships.

Regional specialists differentiate on Arabic user experience, flexible pricing, and embedded benefits brokerage. Bayzat unifies health and life insurance inside payroll, gathering more than 1,000 Gulf clients by 2025 and underscoring the demand for total-rewards orchestration.[5]Bayzat, “Customer Milestone Release,” bayzat.com ZenHR tailors pay-slip templates to Gulf legal codes, appealing to SMEs that consider tier-one interfaces cumbersome. On the African front, SeamlessHR’s offline-first architecture and Workpay’s earned-wage rails provide competitive moats difficult for global vendors to replicate without alliances. Government tenders, such as Ethiopia’s civil-service overhaul, remain contested because delivery risk weighs heavily; players with local integrator networks gain scoring advantages.

Technology continues to separate leaders from followers. Vendors that embed natural-language chatbots in both Modern Standard Arabic and Gulf dialects, even with human-in-the-loop fallback, increase user adoption. Predictive models that recommend rota adjustments or flag overtime breaches resonate with CFOs hunting for cost savings. Yet fragmented dialects and power-cost inflation still create friction, meaning no single vendor dominates enough to tip the market into high concentration.

Middle East and Africa HCM Software Industry Leaders

Automatic Data Processing, Inc.

Oracle Corporation

Workday, Inc.

UKG, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Delicate Software Solutions Launched Integrated Mobile Attendance and WPS Payroll System to Transform HR Operations for UAE SMEs.

- February 2026: Global technology group e& adopted Oracle Fusion Cloud Human Capital Management (HCM) to prepare its global workforce for the AI-driven economy, incorporating embedded artificial intelligence (AI), generative AI, and AI agents.

- October 2025: Sage introduced HR & Payroll Advanced, a cloud-based solution, in South Africa.

- September 2025: Workday expanded into the Middle East by opening a new office in Dubai and introducing its Enterprise AI Platform for People & Finance.

Middle East and Africa HCM Software Market Report Scope

The Middle East and Africa HCM software market comprises software platforms and associated services that manage, automate, and optimize workforce-related functions across enterprises and organizations operating in the Middle East and Africa. The market includes cloud-based and on-premises HCM applications that support the complete employee lifecycle, including workforce planning, recruitment, onboarding, payroll, compensation and benefits administration, time and attendance tracking, talent management, learning and development, employee engagement, performance management, succession planning, and workforce analytics.

The Middle East and Africa HCM Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and Learning and Development), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, Healthcare and Lifesciences, Retail and E-commerce, Government and Public Sector, and Other End-User Industries) and Geograpgy(Middle East (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain, and Rest of Middle East), and Africa (South Africa, Nigeria, Egypt, Kenya, and Rest of Africa)). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll Management |

| Learning and Development |

| IT and Telecommunications |

| BFSI |

| Industrial Manufacturing |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Kenya | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Core HR | |

| Talent Management | ||

| Workforce Management | ||

| Payroll Management | ||

| Learning and Development | ||

| By End-User Industry | IT and Telecommunications | |

| BFSI | ||

| Industrial Manufacturing | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Middle East and Africa HCM Software market be by 2031?

The market is projected to reach USD 4.63 billion by 2031, expanding at a 10.36% CAGR from 2026 to 2031 (Mordor Intelligence).

Which deployment mode is growing fastest across the region?

Cloud, including sovereign-cloud variants, is forecast to register an 11.56% CAGR through 2031 as data-center capacity rises (Mordor Intelligence).

Which application segment is expected to lead growth?

Talent management should post the highest 12.08% CAGR because Gulf nationalization quotas demand AI-driven recruitment and development analytics (Mordor Intelligence).

Why are services revenue growing faster than software licenses?

Employers need localized payroll rules, Arabic interfaces, and government-platform integrations, lifting implementation and managed-services demand above 11% annually (Mordor Intelligence).

Which industry vertical is likely to outpace others?

Healthcare and life sciences are projected to grow at 11.94% owing to stringent credential-tracking and high expatriate churn (Mordor Intelligence).

Page last updated on: