Japan HCM Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

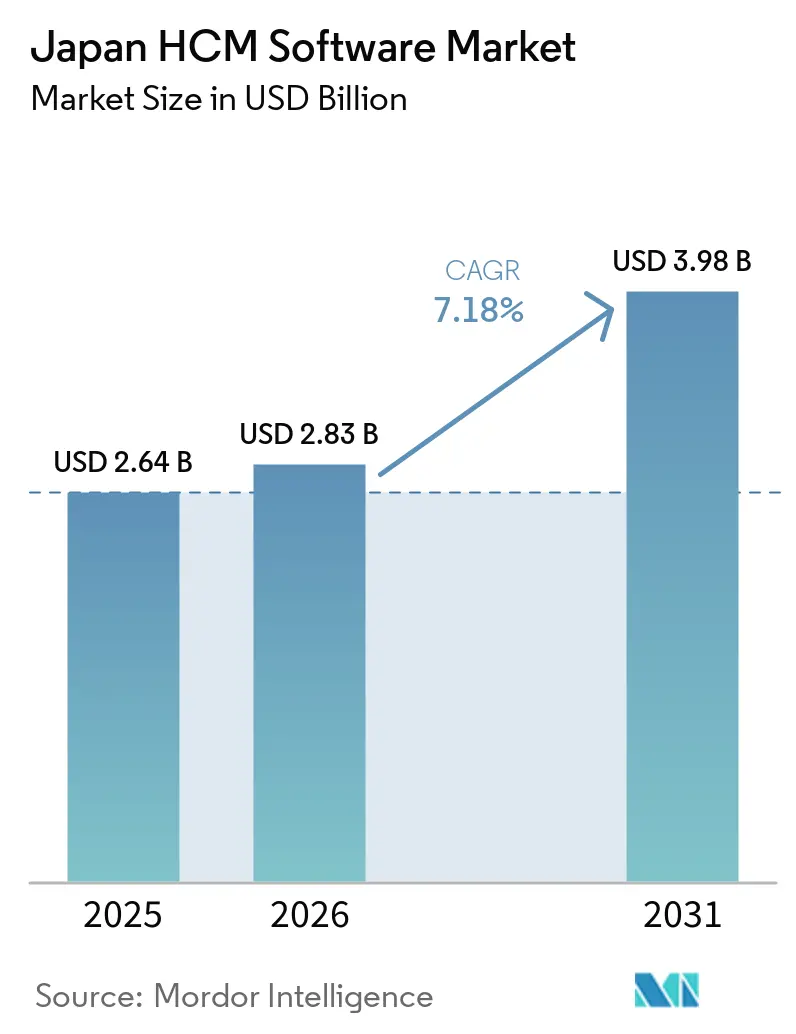

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 3.98 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

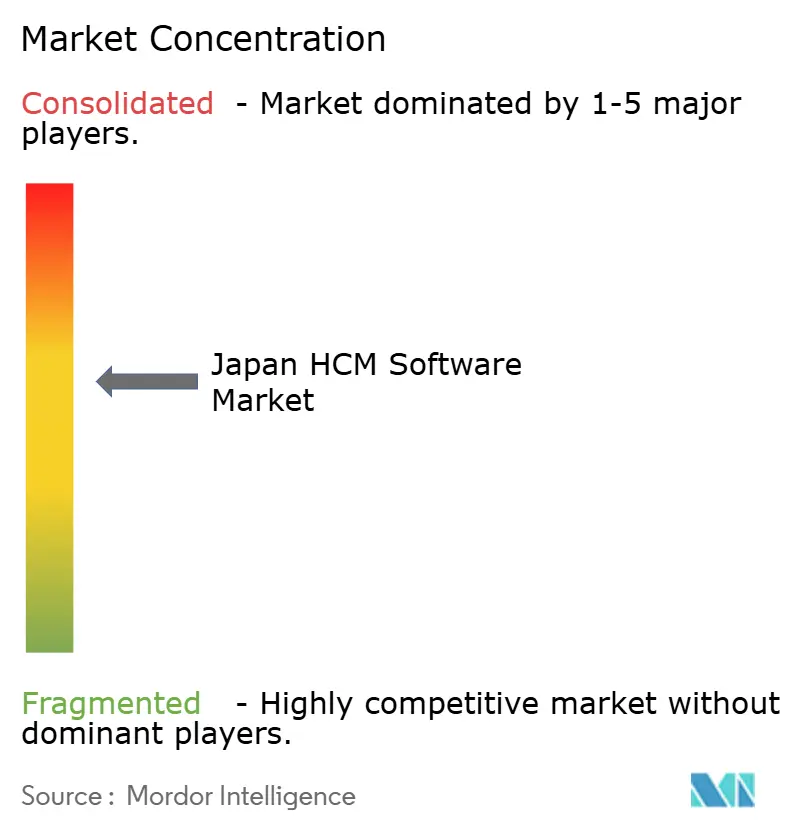

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan HCM Software Market Analysis by Mordor Intelligence

The Japan HCM Software market size is expected to increase from USD 2.64 billion in 2025 to USD 2.83 billion in 2026 and reach USD 3.98 billion by 2031, growing at a CAGR of 7.18% over 2026-2031. Rising digital-transformation budgets, compliance-driven system upgrades, and demographic pressures are combining to lift platform renewals across every major industry. Software retained dominance in 2025, yet service-led engagements are expanding faster as enterprises seek integration, change management, and localization expertise. Cloud deployment remains the default for new rollouts, although hybrid architectures are gaining traction as firms weigh data-sovereignty rules against the need for elastic capacity. Accelerated adoption among small and medium enterprises, fueled by government subsidies, is reshaping the competitive landscape and compelling vendors to unbundle freemium modules that convert free users into paying subscribers. Large enterprises continue to account for most revenue, yet the fastest incremental growth now comes from first-time buyers in the SME segment, underscoring a structural pivot toward volume-driven expansion.

Key Report Takeaways

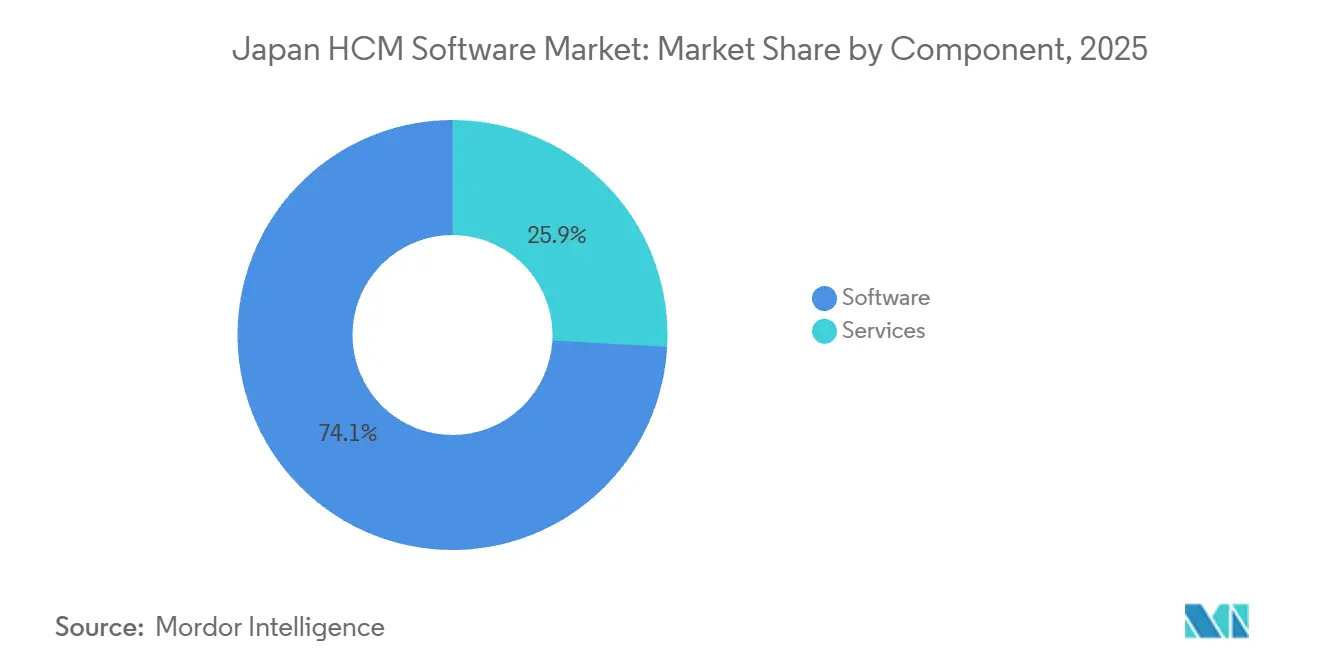

- By component, software led with 74.12% revenue share in 2025, while services are forecast to expand at an 8.26% CAGR through 2031.

- By deployment mode, cloud accounted for 65.38% of the Japan HCM Software market share in 2025, while hybrid architectures are expected to record the highest projected CAGR at 8.74% through 2031.

- By organization size, large enterprises accounted for 74.27% of revenue in 2025, yet SMEs are projected to grow at a 8.41% CAGR through 2031.

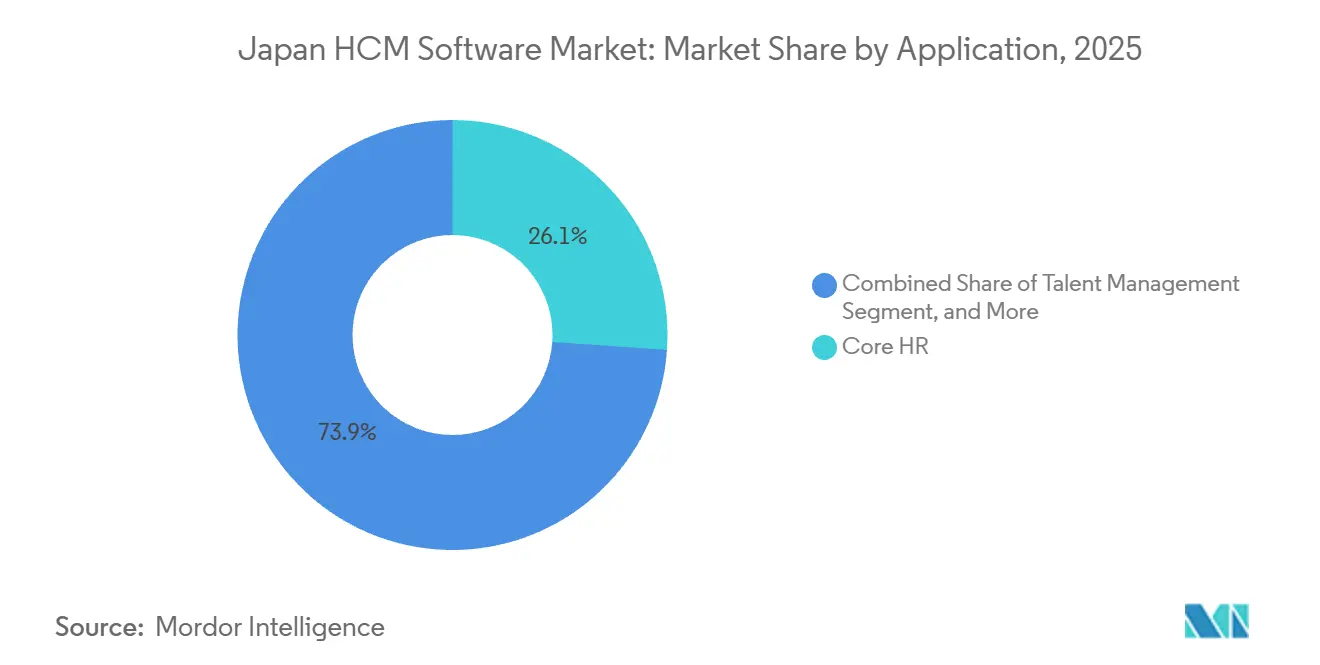

- By application, core HR represented 26.11% of the Japan HCM Software market size in 2025, and talent management is advancing at an 8.92% CAGR through 2031.

- By end-user industry, industrial manufacturing captured 27.42% revenue share in 2025, while healthcare and lifesciences is forecast to expand at an 8.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan HCM Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation Initiatives Across Japanese Enterprises | +1.8% | National, early gains in Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Rising Adoption of Cloud-Based HR Solutions by SMEs | +1.5% | National, concentrated in prefectures with high SME density | Short term (≤ 2 years) |

| Government Mandate on Work Style Reform and Labor Law Compliance | +1.3% | National | Short term (≤ 2 years) |

| Aging Workforce Driving Demand for Strategic Workforce Planning Tools | +1.2% | National, acute in rural prefectures | Long term (≥ 4 years) |

| Integration of AI and Analytics in HR Processes Enhancing Value Proposition | +0.9% | National, early adoption in IT, BFSI, and large manufacturing | Medium term (2-4 years) |

| Growing Gig Economy Necessitating Flexible Talent Management Platforms | +0.5% | Urban centers, spillover to regional hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Initiatives Across Japanese Enterprises

Tax incentives unveiled in 2025 are nudging enterprises to treat HR systems as revenue-enabling assets rather than back-office utilities. Large conglomerates that once ran dozens of standalone HR databases are consolidating onto unified suites to unlock real-time analytics and reduce onboarding cycle time. Mitsui and Co. deployed Oracle Fusion Cloud HCM across 40,000 employees in 2025, integrating payroll, time, and talent modules to eliminate fragmented regional systems and enable real-time workforce analytics.[1]Oracle Corporation, “Mitsui Customer Story,” oracle.com Multi-year cloud rollouts by conglomerates in manufacturing, advertising, and chemicals demonstrate a shift from bespoke on-premise builds toward standardized, upgradeable platforms. The return on these projects is increasingly quantified in terms of workforce agility, with firms citing faster redeployment of skilled labor as a direct contributor to new-business wins.

Rising Adoption of Cloud-Based HR Solutions by SMEs

Subsidies covering up to three-quarters of first-year subscription fees have lowered entry barriers for firms that historically relied on spreadsheets. Freemium pricing, two-week implementation templates, and app-store connectors are shortening sales cycles and allowing vendors to convert large pools of micro-enterprises into recurring-revenue accounts. Interoperability pacts between payroll and attendance specialists eliminate duplicate data entry, positioning cloud HCM as a low-risk upgrade for owners with limited IT staff. The addressable SME base remains vast, and vendors that master automated onboarding are poised to collect outsized share of future growth.

Government Mandate on Work Style Reform and Labor Law Compliance

Overtime caps, mandatory leave, harassment prevention, and gender-pay reporting have moved compliance from optional to mission-critical. Each new rule generates configuration tasks that spreadsheets cannot handle at scale, creating durable demand for automated policy engines embedded inside HCM suites. Time-tracking and scheduling modules that trigger alerts before legal thresholds are breached are now standard RFQ items. Because penalties for non-compliance are immediate, spending on these features is largely insulated from macroeconomic swings, forming a reliable revenue floor for vendors.

Aging Workforce Driving Demand for Strategic Workforce Planning Tools

Japan’s demographic tilt toward an older labor force is forcing companies to model succession scenarios well beyond conventional five-year horizons. AI-enabled talent-matching engines, mentorship dashboards, and phased-retirement workflows are no longer experimental add-ons but core evaluation criteria in RFPs. Financial services and industrial firms are embedding age-profile data within carbon-tracking initiatives to balance ESG disclosure with continuity planning. Vendors offering native analytics around knowledge transfer and reskilling enjoy early-mover pricing power in bids dominated by population-aging pain points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency and Security Concerns Among Traditional Industries | -0.8% | National, acute in BFSI, healthcare, and government sectors | Short term (≤ 2 years) |

| Shortage of HR Tech Skilled Professionals for Implementation and Maintenance | -0.6% | National, concentrated in non-metropolitan prefectures | Medium term (2-4 years) |

| High Upfront Costs for On-Premise Custom Solutions for Large Enterprises | -0.4% | Large enterprises in manufacturing and heavy industry | Long term (≥ 4 years) |

| Resistance to Organizational Change in Conservative Corporate Culture | -0.3% | Traditional sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Residency and Security Concerns Among Traditional Industries

More stringent cross-border data rules are compelling banks, hospitals, and ministries to retain personnel records within national borders. Although sovereign clouds and dedicated regions now exist, limited vendor certification under government security programs constrains product choice and lengthens procurement cycles. Hybrid models that split payroll from ancillary functions offer a workaround, yet many legacy buyers still default to on-premise installations, slowing full cloud penetration.

Shortage of HR Tech Skilled Professionals for Implementation and Maintenance

Successful HCM transformation requires specialists fluent in both labor law and API orchestration, a profile in short supply outside major metros. A 2025 survey by the Japan HR Technology Association found that 58% of enterprises delayed HCM cloud migrations due to a lack of internal staff capable of configuring workflows, integrating payroll engines, and managing change, with rural prefectures reporting vacancy rates above 70% for HR systems administrators.[2]Japan HR Technology Association, “Skills Gap Research 2025,” jhrta.or.jp Delays stemming from unfilled systems-administrator roles frequently extend project timelines, tempering deal velocity despite available budgets. Vendors are countering with managed-services bundles and university partnerships, but labor scarcity remains a tangible drag on installation speed, particularly for AI-enabled modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Software as Complexity Rises

Software commanded 74.12% of Japan's HCM market revenue in 2025, reflecting the dominance of license and subscription fees for core HR, payroll, and time-and-attendance modules. However, Services are forecast to grow at 8.26% CAGR during 2026-2031. Works Human Intelligence highlights the shift by packaging quarterly rule updates and managed payroll with its core suite, capturing margin in the operational layer.[3]Works Human Intelligence, “COMPANY HCM Product Page,” works-hi.co.jp

Demand for business-process outsourcing further elevates service intake. A joint payroll-and-attendance offering from JOE and SmartHR bundles cloud software with certified BPO labor, attracting clients who prefer to transfer compliance risk. The Japan HCM Software market size captured by services is therefore expected to climb steadily as vendors monetize ongoing administration rather than one-time licenses.

By Deployment Mode: Hybrid Gains as Sovereignty Trumps Pure Cloud

Cloud deployment held 65.38% market share in 2025, driven by SME adoption and the cost advantages of multi-tenant SaaS. Yet Hybrid models are expanding at 8.74% CAGR through 2031, the fastest rate among deployment modes, as large enterprises and regulated industries demand data residency without sacrificing scalability. Oracle’s dedicated-region expansion lets clients run full-stack OCI services behind their own firewalls while synchronizing with public-cloud modules, a design tailored to stringent data-sovereignty rules.

On-Premises deployments, though declining in share, persist among heavy manufacturers and public-sector entities that prioritize air-gapped security and customization depth, but new adoption tilts toward hybrid deployments that keep sensitive payroll data locally and push learning or engagement tools offsite. Cloud will remain the largest slice by absolute revenue, yet its share inches down as large enterprises retrofit hybrid blueprints for mission-critical workloads.

By Organization Size: SMEs Accelerate as Barriers Fall

Large Enterprises accounted for 74.27% of Japan's HCM market revenue in 2025, reflecting their complex multi-entity structures, global payroll requirements, and willingness to invest in customized implementations. However, Small and Medium Enterprises are projected to grow at 8.41% CAGR during 2026-2031, driven by government subsidies, vendor freemium strategies, and pre-built integrations that lower switching costs.

Freemium suites from leading vendors convert micro-firms into subscribers who subsequently layer paid modules, lifting average revenue per account. Large enterprises still anchor deal value in multi-module contracts that require custom integrations. However, as SME rollouts proliferate, the Japan HCM Software market share balance will gradually tilt toward volume-driven growth, rewarding vendors that automate onboarding and embed policy templates for firms lacking HR staff.

By Application: Talent Management Surges as Demographics Bite

Core HR applications held 26.11% of the Japan HCM market share in 2025, encompassing employee master data, organizational hierarchies, and basic personnel administration. Yet Talent Management is forecast to grow at 8.92% CAGR through 2031, the fastest rate among application types, as enterprises shift from reactive record-keeping to proactive workforce planning in response to Japan's shrinking labor pool and rising wage inflation. AI-based succession dashboards, turnover-risk predictors, and psychometric profiling are now mainstream bid requirements.

Kaonavi’s acquisition of a personality-assessment specialist exemplifies product roadmaps that fuse behavioral science with core HR data.[4]PR Times, “Kaonavi Acquires Mitsukari,” prtimes.jp Core HR remains foundational for record keeping, but its relative weight declines as analytics-heavy layers capture incremental budget. The Japan HCM Software market size tied to predictive talent tools, therefore, grows faster than transactional modules, signaling a pivot from compliance to foresight.

By End-User Industry: Healthcare Overtakes as Complexity Compounds

Manufacturing accounted for the largest share at 27.42% in 2025. However, Healthcare and Lifesciences are growing fastest at 8.58% CAGR through 2031, as hospital consolidation, nurse-scheduling complexity, and regulatory mandates for patient-safety staffing ratios force providers to replace paper-based rosters with algorithmic workforce-management tools. A flagship deployment at Tokyo Saiseikai Central Hospital cut admin overhead by 25%, demonstrating quantifiable ROI for providers grappling with nurse shortages.

IT and Telecommunications, BFSI, and Retail and E-commerce sectors exhibit robust adoption as well, each facing distinct workforce challenges. Mizuho Financial Group deployed Fujitsu's Eco Track in January 2026 to integrate carbon footprint tracking with workforce analytics, enabling the bank to link employee travel and facility usage to sustainability targets and to optimize staffing patterns to reduce emissions. Gig-economy hubs integrate freelance-management layers to accommodate non-traditional labor pools, widening the use cases addressed by enterprise suites.

Geography Analysis

Metropolitan Tokyo, Osaka, and Nagoya collectively accounted for the majority of 2025 revenue in the Japan HCM software market, reflecting headquarters concentration and proximity to certified data centers. Tokyo alone hosts over 50% of Japan's publicly listed companies and serves as the primary deployment hub for global HCM vendors such as Oracle, SAP, and Workday, which maintain local data centers, customer-success teams, and partner networks in the capital region. Oracle’s multi-billion-dollar regional build-out and Microsoft’s USD 10 billion investment in engineering skills are both anchored in these hubs, reinforcing their critical mass.

Regional prefectures, though smaller in absolute terms, are experiencing faster growth as SME adoption accelerates and government subsidies democratize access to cloud HCM. Growth rates are steeper in second-tier prefectures where SMEs leverage subsidies to leapfrog on-premise eras. Adoption outside the megacities jumped 9 percentage points in 2025 as field teams from leading vendors and BPO partners blended implementation with managed services, sidestepping local talent shortages.

The regional adoption pattern of HCM solutions in Japan closely aligns with industrial concentration trends. Aichi Prefecture, anchored by Toyota and a strong automotive manufacturing ecosystem, demonstrates significant adoption of workforce management and employee shift scheduling solutions across manufacturing enterprises. Meanwhile, Osaka, which hosts a large base of pharmaceutical and medical device companies, is witnessing growing adoption of HCM platforms integrated with compliance monitoring and quality management capabilities. Startup-friendly Fukuoka incubates AI-centric HR apps that plug into established suites, further diversifying the Japan HCM Software market.

Competitive Landscape

The Japanese HCM software market shows moderate concentration. Domestic champions differentiate through payroll-rule depth and Japanese-language workflows, whereas global suites win on multi-module breadth. Global incumbents such as Oracle, SAP, and Workday compete on breadth, offering integrated ERP-HCM suites that appeal to multinational corporations that require unified finance, supply chain, and HR data.

Oracle's April 2026 announcement that DENSO expanded its Oracle Fusion Cloud deployment to include SCM modules alongside existing HCM and ERP illustrates how platform vendors leverage cross-module synergies to deepen customer lock-in. Domestic pure-plays such as Works Human Intelligence, SmartHR, and freee differentiate through their depth of localization, offering out-of-the-box support for Japan's complex payroll rules, social-insurance filing, and year-end tax adjustments, which global vendors often require extensive customization to replicate.

White-space opportunities in Japan’s HCM software market are increasingly emerging at the convergence of HCM and adjacent workforce technologies, particularly in talent analytics, gig workforce administration, and AI-driven employee retention forecasting. In March 2026, PatosLogos secured JPY 3.1 billion (USD 20.6 million) in funding and expanded its collaboration with Workday to introduce localized talent analytics dashboards capable of identifying employee flight-risk indicators and visualizing organizational skills gaps. This reflects growing enterprise demand for advanced workforce intelligence capabilities beyond traditional core HCM deployments.

Japan HCM Software Industry Leaders

Workday Inc.

Oracle Corporation

SAP SE

ADP, Inc.

Dayforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Oracle announced that DENSO expanded its Oracle Fusion Cloud footprint to include supply chain and manufacturing modules, and the partners opened a joint AI center of excellence.

- April 2026: Kaonavi acquired Mitsukari, adding psychometric profiling to its performance-management suite.

- April 2026: Microsoft committed USD 10 billion to Japan for 2026-2029, partnering with national integrators to train 1 million engineers by 2030.

- January 2026: Workday launched Built on Workday Japan, enabling local extensions for social-insurance filing and year-end tax adjustment.

Japan HCM Software Market Report Scope

The Japan Human Capital Management (HCM) software market comprises revenue generated from the sale of software licenses, SaaS subscriptions, implementation, integration, support, maintenance, and managed services associated with HCM platforms used by organizations operating in Japan. The market includes revenues derived from core HR management, payroll and tax compliance, workforce management, talent acquisition, recruitment, performance management, learning and development, employee engagement, compensation management, succession planning, HR analytics, and AI-enabled workforce optimization solutions.

The Japan HCM Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and Learning and Development), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, Healthcare and Lifesciences, Retail and E-commerce, Government and Public Sector, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll Management |

| Learning and Development |

| IT and Telecommunications |

| BFSI |

| Industrial Manufacturing |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Core HR |

| Talent Management | |

| Workforce Management | |

| Payroll Management | |

| Learning and Development | |

| By End-User Industry | IT and Telecommunications |

| BFSI | |

| Industrial Manufacturing | |

| Healthcare and Lifesciences | |

| Retail and E-commerce | |

| Government and Public Sector | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected value for Japan’s HCM software space by 2031?

It is forecast to reach USD 3.98 billion by 2031, growing from USD 2.83 billion in 2026.

Why are hybrid deployments gaining ground?

Hybrid models balance Japan’s strict data-sovereignty rules with cloud scalability, giving them the fastest forecast CAGR at 8.74%

What demographic trend is influencing product roadmaps?

An aging workforce is pushing demand for succession planning and reskilling tools.

Which solution type is expanding most quickly?

Service-led engagements are projected to grow at an 8.26% CAGR through 2031.

How fast is spending on HCM platforms expected to expand?

Aggregate spending is set to rise at a 7.18% CAGR between 2026 and 2031.

Page last updated on: