India HCM Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.87 Billion |

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 3.68 Billion |

| Growth Rate (2026 - 2031) | 11.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India HCM Software Market Analysis by Mordor Intelligence

The India HCM software market size is expected to increase from USD 1.87 billion in 2025 to USD 2.09 billion in 2026 and reach USD 3.68 billion by 2031, growing at a CAGR of 11.84% over 2026-2031. Continuing modernization of payroll engines after the unified labor codes, data-localization mandates under the Digital Personal Data Protection Act, and the rising appeal of vernacular mobile apps in tier-2 and tier-3 cities keep the India HCM software market on an upward trajectory. Cloud deployment already dominates, yet the services category is expanding faster because buyers need consultants to rewire statutory rules for 28 states and eight union territories. Small and medium enterprises are the volume engine, while large enterprises still anchor high-value contracts that bundle consulting, managed support, and multi-country payroll. Competitive intensity is sharpening as domestic vendors scale internationally and global suppliers open local data centers to win regulated customers.

Key Report Takeaways

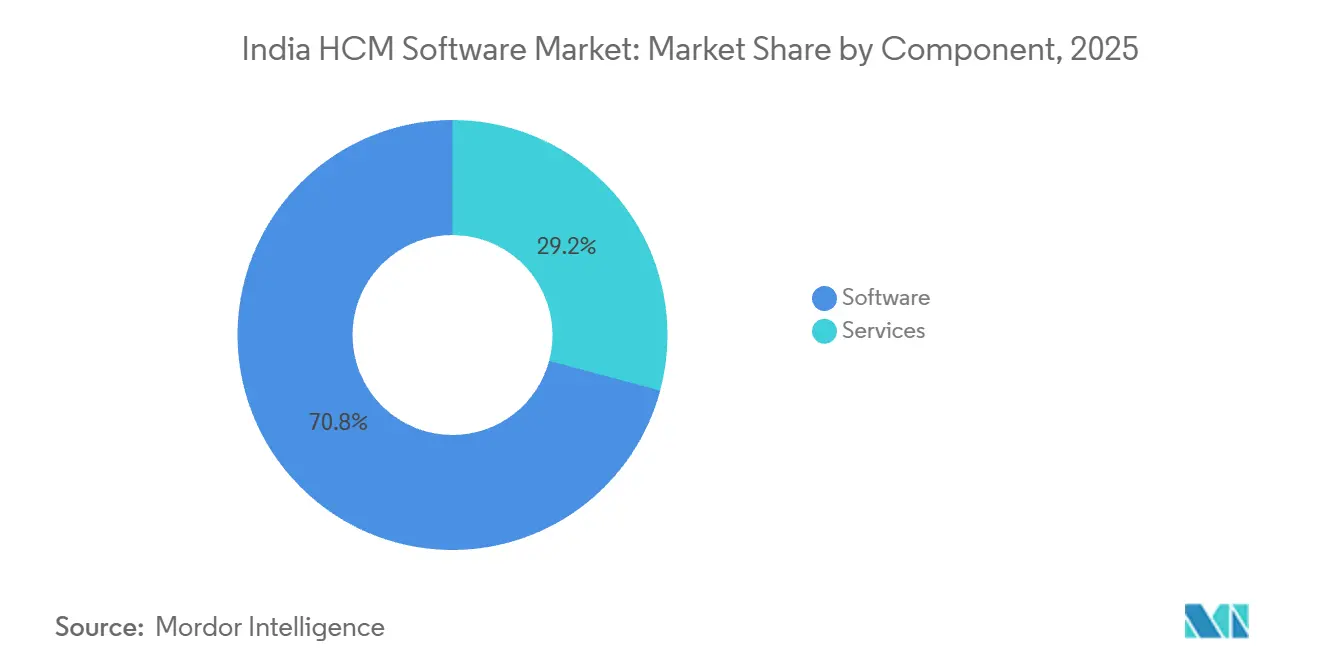

- By component, cloud deployment captured 70.84% of the India HCM software market share in 2025, while services is advancing at a 13.12% CAGR through 2031.

- By deployment mode, cloud accounted for 62.91% share of the India HCM software market size in 2025 and is expanding at 13.54% CAGR between 2026-2031.

- By organization size, large enterprises led with 66.62% revenue share in 2025, while the SMEs segment is forecast to expand at a 13.28% CAGR to 2031.

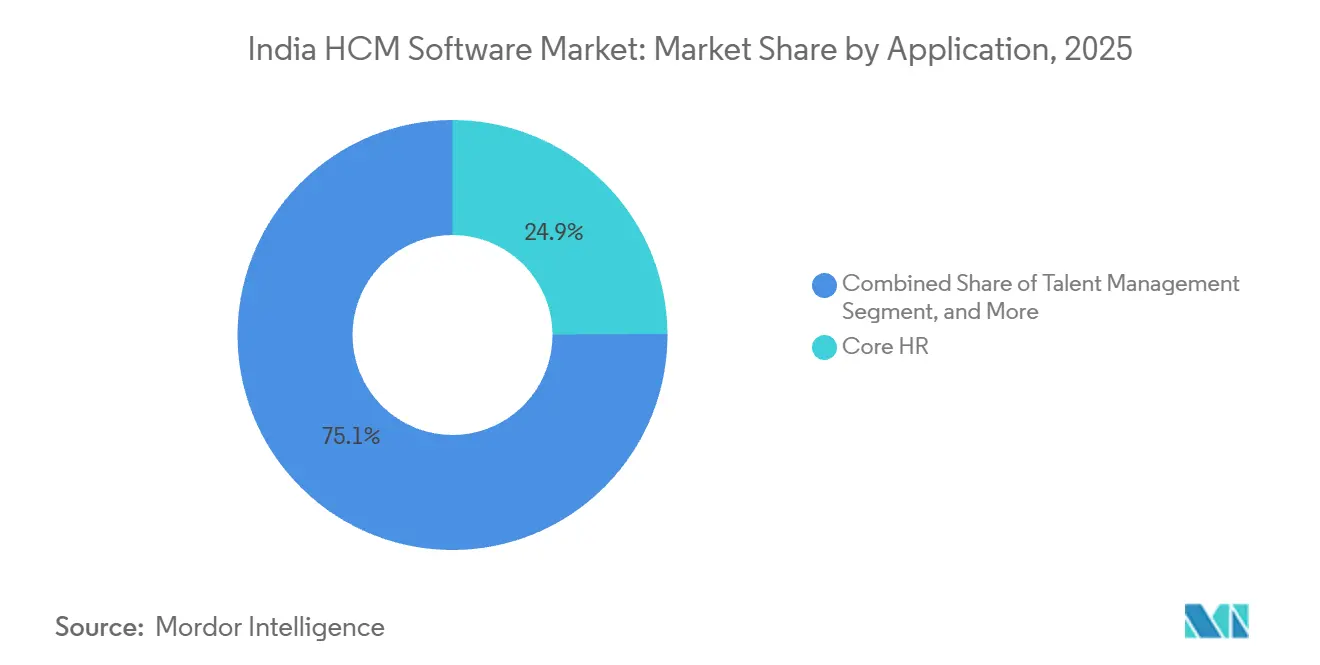

- By application, core HR retained a 24.92% share of the India HCM software market size in 2025, whereas talent management is projected to grow at 13.86% CAGR through 2031.

- By end-user industry, IT and telecommunications commanded 28.64% of the India HCM software market share in 2025, while retail and e-commerce is growing at a 13.41% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India HCM Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Based HCM Platforms | +3.2% | National, metro hubs | Medium term (2-4 years) |

| Growing Demand for Automation and AI-Driven HR Processes | +2.8% | National, BFSI, IT, retail | Medium term (2-4 years) |

| Increasing Regulatory Compliance Complexity | +2.4% | National, multi-state firms | Short term (≤ 2 years) |

| Expanding SME Digitization and SaaS Affordability | +2.1% | National, tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Integration of HCM with Government Digital Portals | +1.6% | National, all employers | Short term (≤ 2 years) |

| Rise of Vernacular Mobile HR Apps for Gig Workforce | +1.2% | National, urban gig sectors | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Based HCM Platforms

Cloud deployment already holds a 62.91% foothold in the India HCM software market and is on a 13.54% CAGR path because pay-per-employee pricing eliminates hardware outlays. Workday’s AWS-hosted data center in Chennai gives multinational clients sovereign data storage while keeping a single global instance. Oracle HCM Now bundles core HR, payroll, and time tracking on one cloud stack, and Wipro cut payroll-cycle time by 60% after migration.[1]Oracle Newsroom, “Oracle HCM Now Debuts for Indian Mid-Market,” Oracle, oracle.com Domestic challenger Keka processes 1.5 million payrolls each month with geo-fencing and regional-language screens that resonate with field workers. Falling budgets for on-premises customization push spending toward API ties with portals such as EPFO and ESIC, reinforcing cloud momentum.

Growing Demand for Automation and AI-Driven HR Processes

Talent management suites are embedding résumé parsing, interview scheduling, and attrition prediction that shorten time-to-hire by 30%. SAP SuccessFactors stitched in G-P’s Gia agent in December 2025 so clients can reconcile payroll across 50 countries in one view. ADP’s healthcare trends report shows 84% of providers expect AI to relieve paperwork, even as 65% struggle with upskilling. Hunar.AI engaged 10 million candidates through WhatsApp and voice bots to tackle 103% attrition in frontline banking roles. The market now splits between enterprises adopting predictive analytics and SMEs opting for chatbots that automate leave requests and roster swaps.

Increasing Regulatory Compliance Complexity

India’s four unified labor codes took effect in November 2025 but leave room for states to set their own professional-tax slabs and overtime rules, creating a dense compliance grid. EPFO rolled out facial authentication and ECR 2.0 uploads, forcing HCM vendors to rebuild APIs for real-time filing. The Digital Personal Data Protection Act begins enforcement in May 2027, with hefty fines and a 72-hour breach notification rule. Large employers now prefer single-vendor suites to cut the number of statutory touchpoints.

Expanding SME Digitization and SaaS Affordability

SMEs are posting a market-leading 13.28% CAGR because per-head pricing has fallen below INR 80. Zoho Payroll is free for the first 10 workers and charges a minimal amount thereafter, removing budget friction. greytHR serves 23,000 customers across 25 countries and channels, and Series F funds are being invested in AI modules that it plans to upsell to existing SME clients. The India SME Forum reports that 70% of manufacturing leaders see workforce-visibility gaps, leaving a wide runway for first-time digital adoption. Tier-2 buyers want vernacular UIs over deep analytics, nudging vendors to fork their product roadmaps into lightweight and enterprise editions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cybersecurity Concerns | -1.8% | National, BFSI and healthcare | Short term (≤ 2 years) |

| High Total Cost of Ownership for Full-Suite HCM | -1.4% | National, 100–500 employee firms | Medium term (2-4 years) |

| Fragmented State-Level Labor Regulations | -1.1% | National, multi-state operations | Long term (≥ 4 years) |

| Shortage of HR Analytics Talent | -0.9% | National, tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Concerns

The Personal Data Protection Act sets 72-hour breach disclosure, one-year audit logs, and hefty penalties, stretching legal reviews and lengthening procurement cycles. Workday opened an India data center in December 2025 to satisfy localization demands, but vendors lacking ISO 27001 or SOC 2 attestations are now routinely cut from enterprise shortlists. BFSI and healthcare buyers conduct more in-depth penetration tests because employee files contain financial and medical data. As a result, discount platforms that skip two-factor logins may win price-sensitive SMEs but rarely break into regulated verticals.

High Total Cost of Ownership for Full-Suite HCM

Mid-market firms discover that the first-year bill includes not just licenses but 40-50% more for implementation, API tuning, and biometric hardware.[2]HR One Editorial, “True Cost of HRMS in India’s Mid-Market,” HR One, hrone.com Hidden charges such as CSV export fees, API rate limits, and year-two price hikes erode SaaS affordability. Modular licensing that staggers modules over three budget cycles is emerging as a hedge, and vendors with transparent renewal caps are winning deals for 100-500 employees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge as Implementation Complexity Rises

Services revenue is growing at a 13.12% CAGR and will account for a growing share of the India HCM software market as enterprises outsource statutory mapping and API integration. Software retained a 70.84% share in 2025, anchored by license and subscription revenue, yet the rising share of services revenue signals that vendors are monetizing post-sale value delivery rather than relying solely on per-seat pricing. Oracle's Wipro case study, where payroll cycle time fell by 60% after cloud migration, required a 6-month implementation phase with dedicated consultants to map state-specific professional tax rules and integrate EPFO facial-authentication APIs.

Domestic vendors copy this playbook. greytHR’s post-sale team retrofits labor-code updates, and Keka bundles onboarding support into subscription tiers. The strategic implication is that vendors with robust partner ecosystems and certified consultants are capturing a disproportionate share of mid-market and enterprise deals, while those offering software-only licenses are confined to self-service SME segments.

By Deployment Mode: Cloud Dominance Masks Hybrid Complexity

Cloud deployments commanded a 62.91% share in 2025 and are forecast to grow at a 13.54% CAGR through 2031, while hybrid rollouts are gaining ground when sensitive payroll data must reside on-prem, while talent modules run in the cloud. Workday’s local data center lets global instances coexist with sovereign storage, while Oracle HCM Now removes many on-prem customizations through an integrated stack. On-premises deployments, though declining in share, persist in government and public-sector organizations where procurement rules favor capital expenditure over operating expenditure and where legacy ERP systems lack cloud-migration pathways.

Hybrid architectures, which combine on-premises core HR with cloud-based talent acquisition and workforce analytics, are emerging as a compromise for mid-market manufacturers that operate in multiple states and need centralized compliance engines but decentralized shift-scheduling tools. Manufacturers with patchy connectivity use edge devices that sync attendance data later, proving that hybrid is less about architecture dogma and more about matching site realities with compliance rules.

By Organization Size: SMEs to Witness Substantial Growth

Large enterprises accounted for 66.62% of 2025 revenue, and SMEs are projected to grow at a 13.28% CAGR, propelled by affordable SaaS pricing models that eliminate capital expenditures for servers and database licenses. Zoho Payroll’s free starter tier exemplifies the low-friction entry strategy.[3]Zoho Payroll Pricing Sheet, “Cost Structure for Small Firms,” Zoho, zoho.com Keka's 10,000-business customer base, spanning 150 countries, demonstrates that Indian SME-focused platforms are achieving scale by bundling payroll, attendance, and leave management into a single subscription.

Enterprises still anchor high-ticket contracts. Darwinbox’s USD 140 million raise supports predictive AI and global payroll that attract Fortune 500 customers, with 60% of revenue now generated offshore. Vendors, therefore, split road-maps into a fixed-price SME edition with vernacular screens and an enterprise tier with modular pricing, dedicated account management, and white-glove implementation support.

By Application: Talent Management Outpaces Core HR

Core HR held a 24.92% share in 2025, as compliance engines remain indispensable, but talent management is sprinting ahead at a 13.86% CAGR. Talent management applications, growing at 13.86% CAGR through 2031, are absorbing AI-driven attrition prediction, skills-based hiring, and continuous feedback modules that reduce time-to-hire by 30%, according to NASSCOM's 2025 survey of 500 Indian enterprises.

Learning and development platforms are gaining traction as enterprises confront skills gaps in data analytics, cybersecurity, and AI governance. Workforce management tools using geo-fencing are critical for retail and logistics, and continuous-calculation payroll engines, such as Dayforce, shift tax withholding to real-time. Vendors that couple learning with skills-gap dashboards win enterprise renewals, while point payroll products increasingly serve only micro-businesses.

By End-User Industry: Retail and E-Commerce Accelerate Gig Workforce Digitization

The IT and telecommunications sector led demand, accounting for 28.64% of the India HCM software market in 2025, reflecting early cloud adoption. Retail and e-commerce segment, however, is charting a 13.41% CAGR through 2031. Betterplace's gigBetter platform, which covers 19,000 pin codes and serves 500 customers with 12 million verified employees, exemplifies the shift toward Aadhaar-based onboarding and real-time compliance tracking for contract labor

Healthcare and life sciences organizations are deploying HCM to manage credentialing, compliance penalties, and state-specific rules, while BFSI faces substantially high attrition, fueling WhatsApp-based hiring via Hunar.AI. Manufacturing seeks shift scheduling and contractor oversight, but digital maturity in SMEs is still only 40%, leaving long-term upside. Other end-user industries, including hospitality, logistics, and professional services, are adopting mobile-first HCM to manage distributed workforces and project-based staffing models.

Geography Analysis

Metro hubs, including Bengaluru, Hyderabad, Pune, and Chennai, generate the deepest spend because they host IT, telecom, and GCC workforces that rely on AI-ready HCM solutions. Workday’s INR 220 crore (USD 23.1 million) capability center in Chennai employs 3,000 staff and anchors sovereign-cloud services for 1,800 local customers. Oracle timed its HCM Now launch to hit manufacturing corridors in Gujarat, Maharashtra, and Tamil Nadu, where shift automation is a priority.

Tier-2 and tier-3 cities such as Jaipur, Coimbatore, Indore, and Visakhapatnam are the growth frontier because SaaS prices dipped under INR 80 per seat. The India SME Forum confirms that 70% of factory owners there see HCM as vital for head-count visibility, even though digital maturity lags at 40%.[4]India SME Forum Insights, “Digital Maturity of Tier-2 Manufacturing SMEs,” India SME Forum, indiasme.com Vernacular interfaces in Hindi, Tamil, Telugu, and Marathi help Keka win frontline users who lack English proficiency.

State variation complicates payroll in the market. For instance, Maharashtra applies unique overtime calculations, Karnataka enforces biometric attendance, and Tamil Nadu has separate leave encashment rules. Vendors that maintain fortnightly update cycles across all 28 states and eight union territories outsell rivals that rely on annual patches. India is also a springboard for export; Darwinbox has leveraged its complex-regulation expertise to land customers in Southeast Asia and the Middle East.

Competitive Landscape

Global suppliers such as Oracle Corporation, SAP SE, Workday, and ADP dominate enterprise accounts by coupling India-ready payroll with global workforce analytics. Workday’s enterprise momentum score hit 41.9% in 2025, edging SAP and Oracle as buyers favored continuous-calculation payroll and open APIs.[5]Workday Investor Factsheet, “Momentum Score Points to Share Gains,” Workday, workday.com Domestic challengers Darwinbox, Keka, greytHR, and ZingHR jointly serve 40,000 businesses by localizing statutory engines and pricing for SMEs.

Capital is flowing into homegrown platforms. Darwinbox’s March 2025 raise valued it at near USD 1 billion, funding AI assistants and U.S. expansion. greytHR’s August 2024 Series F bankrolls talent modules for its 23,000-client base. Vendors are pairing vertical templates such as healthcare credentialing, manufacturing shift rotas, and retail gig scheduling, with horizontal AI agents to automate routine HR tickets.

Price transparency and data-ownership clauses are new battlegrounds. Buyers increasingly reject CSV export fees and renewal escalators. Vendors offering flat renewal caps and unlimited API calls close mid-market deals faster than rivals that rely on opaque discounting. As AI becomes table stakes, trust signals such as ISO audits, local data centers, and verifiable uptime differentiate platforms in the India HCM software market.

India HCM Software Industry Leaders

Oracle Corporation

SAP SE

Workday Inc.

ADP, Inc.

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Workday announced further investments in AI-driven HCM capabilities and restructuring initiatives to strengthen AI-led workforce management offerings globally, including India-focused enterprise deployments.

- January 2026: Pocket HRMS, India’s leading provider of cloud-based Human Resource Management Systems (HRMS) and payroll automation solutions, announced the launch of HRMS Copilot, an advanced AI-powered enhancement to its intelligent HR Copilot.

- December 2025: SAP SuccessFactors embedded G-P’s Gia AI agent to automate global payroll reconciliation and compliance checks for Indian multinationals.

- May 2025: Darwinbox became the first HR technology platform to launch its own MCP (Model Context Protocol) server for AI integration, strengthening generative AI capabilities in HR workflows.

India HCM Software Market Report Scope

The India Human Capital Management (HCM) Software Market refers to the market for software platforms and related services used by organizations in India to manage, automate, and optimize the entire employee lifecycle, including workforce planning, recruitment, onboarding, payroll, core HR administration, attendance and workforce management, performance management, learning and development, and compensation management.

The India HCM Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and Learning and Development), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, Healthcare and Lifesciences, Retail and E-commerce, Government and Public Sector, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll Management |

| Learning and Development |

| IT and Telecommunications |

| BFSI |

| Industrial Manufacturing |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Core HR |

| Talent Management | |

| Workforce Management | |

| Payroll Management | |

| Learning and Development | |

| By End-User Industry | IT and Telecommunications |

| BFSI | |

| Industrial Manufacturing | |

| Healthcare and Lifesciences | |

| Retail and E-commerce | |

| Government and Public Sector | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected value of the India HCM software market by 2031?

The India HCM software market is forecast to reach USD 3.68 billion by 2031, rising at an 11.84% CAGR.

Which deployment mode holds the largest India HCM software market share today?

Cloud deployment led with a 62.91% India HCM software market share in 2025, a position it is expected to retain through 2031.

Which segment is growing fastest within the India HCM software industry?

Talent management applications are expanding at a 13.86% CAGR, the quickest among all function modules .

How are data-localization laws impacting vendor strategy?

The Digital Personal Data Protection Act compels global vendors to open India data centers, as seen in Workday’s Chennai facility, to satisfy sovereign storage requirements.

What is the main cost challenge for mid-market HCM buyers?

Total cost of ownership can be 40-50% higher than license fees once implementation, API customization, and hardware are included, though modular pricing is easing cash-flow constraints.

Page last updated on: